HNC/D Business: Management Accounting for Decision Making

VerifiedAdded on 2023/06/17

|18

|4563

|112

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application in business decision-making. It covers the concept of management accounting, its advantages and disadvantages, and various methods used for developing management accounting reports. The report also delves into the integration of management accounting in business complexities. Practical aspects are explored through cost cards using absorption and marginal costing, profit statements, and flexed budget preparation. Furthermore, the report discusses planning tools for budgetary control and how management accounting can lead to sustainable business success. The document concludes by highlighting the importance of management accounting in solving financial problems and driving organizational growth.

Management Accounting

for Decision Making

Table of Contents

for Decision Making

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction......................................................................................................................................4

Part – A............................................................................................................................................4

Concept of Management Accounting..........................................................................................4

Advantages and disadvantages of the management accounting system.....................................5

Disadvantages of Management Accounting................................................................................7

Various methods used for developing management accounting report......................................8

The integration of the management accounting in the businesses complexities.........................9

Part – B..........................................................................................................................................10

Cost Card Using Absorption Costing........................................................................................10

Cost Card Using Marginal Costing...........................................................................................10

Profit statements using Absorption costing (10000 units)........................................................10

Profit statements using Marginal costing (10000 units)...........................................................11

Difference between the marginal and absorption costing is explained below: ........................11

Prepare a flexed budget for the actual activity for the year......................................................12

Various types of planning tools used for budgetary control.....................................................12

Part - C...........................................................................................................................................15

A) Planning tools for accounting respond by solving financial problems................................15

Management accounting can lead to sustainable success ........................................................16

Conclusion.....................................................................................................................................17

References......................................................................................................................................18

Books & Journals......................................................................................................................18

Part – A............................................................................................................................................4

Concept of Management Accounting..........................................................................................4

Advantages and disadvantages of the management accounting system.....................................5

Disadvantages of Management Accounting................................................................................7

Various methods used for developing management accounting report......................................8

The integration of the management accounting in the businesses complexities.........................9

Part – B..........................................................................................................................................10

Cost Card Using Absorption Costing........................................................................................10

Cost Card Using Marginal Costing...........................................................................................10

Profit statements using Absorption costing (10000 units)........................................................10

Profit statements using Marginal costing (10000 units)...........................................................11

Difference between the marginal and absorption costing is explained below: ........................11

Prepare a flexed budget for the actual activity for the year......................................................12

Various types of planning tools used for budgetary control.....................................................12

Part - C...........................................................................................................................................15

A) Planning tools for accounting respond by solving financial problems................................15

Management accounting can lead to sustainable success ........................................................16

Conclusion.....................................................................................................................................17

References......................................................................................................................................18

Books & Journals......................................................................................................................18

Introduction

Management accounting can be defined as an important component for every organization

that helps in developing the business objectives which is focussed towards the procedure of

identifying, classifying, measuring and communicating the relevant information with the

different interested parties of the business entity. The major objective is to analyse the financial

position of the company in marketplace. This concept of management accounting helps in

running the business operations in an efficient and consistent which will ultimately helps in

achieving the overall objective of the company. In context to this report, various topics related

to the management accounting are elaborated in context to the respective company

mentioned. Also, budget preparation is also done with the utilization of absorption costing and

marginal costing in relation to disclosing the results of the business organization in the financial

capacity.

Management accounting can be defined as an important component for every organization

that helps in developing the business objectives which is focussed towards the procedure of

identifying, classifying, measuring and communicating the relevant information with the

different interested parties of the business entity. The major objective is to analyse the financial

position of the company in marketplace. This concept of management accounting helps in

running the business operations in an efficient and consistent which will ultimately helps in

achieving the overall objective of the company. In context to this report, various topics related

to the management accounting are elaborated in context to the respective company

mentioned. Also, budget preparation is also done with the utilization of absorption costing and

marginal costing in relation to disclosing the results of the business organization in the financial

capacity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part – A

Concept of Management Accounting

Management accounting can be referred as the process of establishing the objectives of the

organization through identification, measurement, analysis, interpretation and the evaluation

of the financial information that is given to the managers for the purpose of taking important

business decisions (Banker, and et. al., 2018). The major objective of this concept is keep a

check on the costs of the business organization in relation to the manufacturing of the goods

and services. In context to Amoruso, there are different management accounting system that

helps an business organization to operate in the most efficient manner. The different systems

of the management accounting can be used by the respective business organization are

mentioned below:

Job Order Cost Accounting System: it can be defined as the management accounting

system that is specifically required for the purpose of the execution of the large

projects. This type of management accounting system is majorly used by the group of

producers pr manufacturers for the purpose of producing different range of products

which are different from each other. Since all the components are differentiated from

each other, a separate job cost record is highly required for the production. Therefore, it

is highly important to distinguish each job so that it becomes important to perform the

analysis of each job.

Cost Accounting System: It is considered as an important type of management

accounting system which is having the objective of the registering the activities related

to the production with the help of an effective inventory system. In other words, it can

also be specifically defines that the this system have an aim of tracking the inventory

flow in context to various stages of production. Therefore, in order to prepare an

efficient budget it is necessary to follow the cost accounting system.

Inventory management System: It is an accounting system which helps in dealing out

with the management of the inventory of the business organization (Türegün, 2020).

The system is majorly focussed on extracting the information related to the exact

number of products that are available for the purpose of selling them in the market

Concept of Management Accounting

Management accounting can be referred as the process of establishing the objectives of the

organization through identification, measurement, analysis, interpretation and the evaluation

of the financial information that is given to the managers for the purpose of taking important

business decisions (Banker, and et. al., 2018). The major objective of this concept is keep a

check on the costs of the business organization in relation to the manufacturing of the goods

and services. In context to Amoruso, there are different management accounting system that

helps an business organization to operate in the most efficient manner. The different systems

of the management accounting can be used by the respective business organization are

mentioned below:

Job Order Cost Accounting System: it can be defined as the management accounting

system that is specifically required for the purpose of the execution of the large

projects. This type of management accounting system is majorly used by the group of

producers pr manufacturers for the purpose of producing different range of products

which are different from each other. Since all the components are differentiated from

each other, a separate job cost record is highly required for the production. Therefore, it

is highly important to distinguish each job so that it becomes important to perform the

analysis of each job.

Cost Accounting System: It is considered as an important type of management

accounting system which is having the objective of the registering the activities related

to the production with the help of an effective inventory system. In other words, it can

also be specifically defines that the this system have an aim of tracking the inventory

flow in context to various stages of production. Therefore, in order to prepare an

efficient budget it is necessary to follow the cost accounting system.

Inventory management System: It is an accounting system which helps in dealing out

with the management of the inventory of the business organization (Türegün, 2020).

The system is majorly focussed on extracting the information related to the exact

number of products that are available for the purpose of selling them in the market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

place which will ultimately assist the company in having right number of units at right

time and at right place. It is also necessary that they are available at the right price in

the market. In case of the absence of an ineffective inventory management system, it

will become a hindrance for the business organization in order to deal with the demands

of the consumers in the competitive markets.

Advantages and disadvantages of the management accounting system

Advantages of Management Accounting

Effective Decision Making:

Management accounting is considered as an effective tool that helps in taking some important

and relevant decisions for the business organization with the help of the financial information

provided. The financial information can be in the form of charts, tables and the forecasts which

helps the team of the management to take certain effective decisions for the constant

development of the firm.

Increases the efficiency in the business operations:

Management accounting is an important tool which plays an active role in increasing the overall

efficiency of the business entity. It plays an important role in evaluating the performance of the

firm in a highly consistent manner. Management accounting focusses on the removal of all the

hindrances which keeps on creating a barrier for growth and development of the company.

Therefore, if any deviation comes up, a corrective measure can also be implemented with the

application of the tool of management accounting tool effectively.

Enhance profitability:

management accounting application is a huge advantage for the business firm because when all

the financial activities are managed properly and consistently, there is an automatic

enhancement in the profitability levels of the company considerably (Gunarathne and

Rajasooriya, 2019). The various tools and techniques which are an effective part of the entity

namely, capital budgeting and budgetary tools ultimately helps in the attainment of the

objective of the organizational goal with enhanced level of profitability.

Motivating Employees:

time and at right place. It is also necessary that they are available at the right price in

the market. In case of the absence of an ineffective inventory management system, it

will become a hindrance for the business organization in order to deal with the demands

of the consumers in the competitive markets.

Advantages and disadvantages of the management accounting system

Advantages of Management Accounting

Effective Decision Making:

Management accounting is considered as an effective tool that helps in taking some important

and relevant decisions for the business organization with the help of the financial information

provided. The financial information can be in the form of charts, tables and the forecasts which

helps the team of the management to take certain effective decisions for the constant

development of the firm.

Increases the efficiency in the business operations:

Management accounting is an important tool which plays an active role in increasing the overall

efficiency of the business entity. It plays an important role in evaluating the performance of the

firm in a highly consistent manner. Management accounting focusses on the removal of all the

hindrances which keeps on creating a barrier for growth and development of the company.

Therefore, if any deviation comes up, a corrective measure can also be implemented with the

application of the tool of management accounting tool effectively.

Enhance profitability:

management accounting application is a huge advantage for the business firm because when all

the financial activities are managed properly and consistently, there is an automatic

enhancement in the profitability levels of the company considerably (Gunarathne and

Rajasooriya, 2019). The various tools and techniques which are an effective part of the entity

namely, capital budgeting and budgetary tools ultimately helps in the attainment of the

objective of the organizational goal with enhanced level of profitability.

Motivating Employees:

It is highly important to build an organizational culture which is oriented towards building a

culture in the organization which must motivate the employees to attain the objectives of the

organizations. Various periodic reports are presented in relation to the business operations.

Therefore, these reports can help the management of the company to motivate the employees

so that the performance of the business entity. This also helps in improvising the financial

efficiency.

Reliability

Management accounting is a tool which aims at inculcating the element of reliability which can

be used for the purpose of execution of the financial scientific tools. These help in ascertaining

the objectives of the company with effective management and communicating the relevant and

genuine information on which the management and the external users can rely to take the

important business decisions.

Disadvantages of Management Accounting

Provides only data

Management accounting majorly aims at providing data but not the action plan which can help

in dealing the certain financial issues in an effective manner. Therefore, this becomes a

significant disadvantage for the business organization.

Personal Bias: This branch of accounting is a method which is mostly affected by the

element of personal bias which brings considerable amount of inefficiency in the

working of the company. The capacity of the company to interpret and analyse can also

get affected negatively.

Lack of specific Procedure:

The concept of accounting does not involve the presence of rules and regulations that

must be followed (Berle and Bhabha, 2018). Therefore, it can be reasoned that

establishment of accounting does not rely on the component of code of conduct or rules

and regulations in order to create the commercial enterprise statements.

Uncertain

culture in the organization which must motivate the employees to attain the objectives of the

organizations. Various periodic reports are presented in relation to the business operations.

Therefore, these reports can help the management of the company to motivate the employees

so that the performance of the business entity. This also helps in improvising the financial

efficiency.

Reliability

Management accounting is a tool which aims at inculcating the element of reliability which can

be used for the purpose of execution of the financial scientific tools. These help in ascertaining

the objectives of the company with effective management and communicating the relevant and

genuine information on which the management and the external users can rely to take the

important business decisions.

Disadvantages of Management Accounting

Provides only data

Management accounting majorly aims at providing data but not the action plan which can help

in dealing the certain financial issues in an effective manner. Therefore, this becomes a

significant disadvantage for the business organization.

Personal Bias: This branch of accounting is a method which is mostly affected by the

element of personal bias which brings considerable amount of inefficiency in the

working of the company. The capacity of the company to interpret and analyse can also

get affected negatively.

Lack of specific Procedure:

The concept of accounting does not involve the presence of rules and regulations that

must be followed (Berle and Bhabha, 2018). Therefore, it can be reasoned that

establishment of accounting does not rely on the component of code of conduct or rules

and regulations in order to create the commercial enterprise statements.

Uncertain

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting is a tool that is highly affected by the dynamic environment.

The main reason for the uncertainty is that the competitive environment is highly

dynamic in nature in order to deal with it in an effective manner.

Costly

The establishment of the management accounting in the business organization is an

economically costlier process which involves large amount of costs along with huge

expenditures. It grabs assistance from the professional so that the concept of management

accounting can be effectively applied in the business operations. Therefore, such type of costs

for hiring these professionals puts heavy burden on the financial capacities of the business

entity.

Various methods used for developing management accounting report

There are various management accounting methods which are used by the business

organization in order to implement and achieve the goals and objectives of the company

effectively. These methods helps in providing a platform which will helps the company to

maintain the financial position of the company to a greater extent. In order to maintain the

highest level of efficiency management accounting reporting makes it sure that the financial

information of the business entity is in accordance to the accounting records and the principles

on the basis of which the financial statements are prepared (Gisch, Hirsch and Lindermüller,

2021). In context to business organization Amoruso, there are some of the methods which are

majorly used in order to implement the management accounting reporting. They are

mentioned with the elaboration beneath:

Trend Analysis & Forecasting: It is one of the management accounting reporting

method which majorly helps in coping up with the latest trends by taking into

consideration the data of the previous year effectively. This analysis majorly focuses on

the historical financial data so that the latest trends can be implemented and adapted

effectively. In addition to this, it can be considered that the techniques of forecasting

and projecting helps in building the efficient reports of analysis. In order to build the

comparative financial analysis report, trend analysis is the most important component.

The main reason for the uncertainty is that the competitive environment is highly

dynamic in nature in order to deal with it in an effective manner.

Costly

The establishment of the management accounting in the business organization is an

economically costlier process which involves large amount of costs along with huge

expenditures. It grabs assistance from the professional so that the concept of management

accounting can be effectively applied in the business operations. Therefore, such type of costs

for hiring these professionals puts heavy burden on the financial capacities of the business

entity.

Various methods used for developing management accounting report

There are various management accounting methods which are used by the business

organization in order to implement and achieve the goals and objectives of the company

effectively. These methods helps in providing a platform which will helps the company to

maintain the financial position of the company to a greater extent. In order to maintain the

highest level of efficiency management accounting reporting makes it sure that the financial

information of the business entity is in accordance to the accounting records and the principles

on the basis of which the financial statements are prepared (Gisch, Hirsch and Lindermüller,

2021). In context to business organization Amoruso, there are some of the methods which are

majorly used in order to implement the management accounting reporting. They are

mentioned with the elaboration beneath:

Trend Analysis & Forecasting: It is one of the management accounting reporting

method which majorly helps in coping up with the latest trends by taking into

consideration the data of the previous year effectively. This analysis majorly focuses on

the historical financial data so that the latest trends can be implemented and adapted

effectively. In addition to this, it can be considered that the techniques of forecasting

and projecting helps in building the efficient reports of analysis. In order to build the

comparative financial analysis report, trend analysis is the most important component.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Therefore, this will help the company in focussing on the pro active approach to achieve

success in the longer run.

Margin Analysis: It is another method of management accounting that helps in

identifying and ascertaining the equilibrium point which helps in effectively analysing

the process of production in an optimum manner. The major objectives which keeps on

focusing the business operations is specifically to generate sales amount at an optimum

level effectively. Therefore, it can be considered that margin analysis is a key tool to

effectively maintain the margins of profit to a greater level ultimate;y resulting into

higher level of efficiency.

Capital budgeting : This is one of the common method of management accounting

which contributes majorly in decision making process in regards to the capital structure

of the company. Capital budgeting also helps in keeping the track of different types of

the capital expenditures in an effective way for a business organization. The calculation

of the elements of Net present value and the pay back period along with internal rate if

return which majorly assists the finance managers to make various financial decisions

for the purpose of building effective capital budgeting.

The integration of the management accounting in the businesses complexities

Management accounting is considered as a vital tool that plays an important part in the

handling all the business operations of a business organization’s financial capacity. The major

factor which is accountable for the purpose of maintaining the performance of the company on

the basis of financial grounds are mainly the two components namely qualitative and the

quantitative data. That's how the management accounting concept has been integrated wit the

complications of the business operations effectively. The complications that often arises due to

many reasons but they play an important role in enhancing the efficiency and the performance

of the company to a greater level (Zhang, Zhao and Gupta, 2018). Therefore, in context to the

business organization Amoruso, it has been considered that it is very important to manage the

books of accounts with the application of the management accounting tools that will ultimately

help in achieving the goals and the objectives effectively. The major reason behind that is a

management accounting system is getting broader as well as wider which is becoming

success in the longer run.

Margin Analysis: It is another method of management accounting that helps in

identifying and ascertaining the equilibrium point which helps in effectively analysing

the process of production in an optimum manner. The major objectives which keeps on

focusing the business operations is specifically to generate sales amount at an optimum

level effectively. Therefore, it can be considered that margin analysis is a key tool to

effectively maintain the margins of profit to a greater level ultimate;y resulting into

higher level of efficiency.

Capital budgeting : This is one of the common method of management accounting

which contributes majorly in decision making process in regards to the capital structure

of the company. Capital budgeting also helps in keeping the track of different types of

the capital expenditures in an effective way for a business organization. The calculation

of the elements of Net present value and the pay back period along with internal rate if

return which majorly assists the finance managers to make various financial decisions

for the purpose of building effective capital budgeting.

The integration of the management accounting in the businesses complexities

Management accounting is considered as a vital tool that plays an important part in the

handling all the business operations of a business organization’s financial capacity. The major

factor which is accountable for the purpose of maintaining the performance of the company on

the basis of financial grounds are mainly the two components namely qualitative and the

quantitative data. That's how the management accounting concept has been integrated wit the

complications of the business operations effectively. The complications that often arises due to

many reasons but they play an important role in enhancing the efficiency and the performance

of the company to a greater level (Zhang, Zhao and Gupta, 2018). Therefore, in context to the

business organization Amoruso, it has been considered that it is very important to manage the

books of accounts with the application of the management accounting tools that will ultimately

help in achieving the goals and the objectives effectively. The major reason behind that is a

management accounting system is getting broader as well as wider which is becoming

significantly important for the business firms majorly in the process of controlling and planning

the business activities in making various efficient decisions during the execution phase.

Part – B

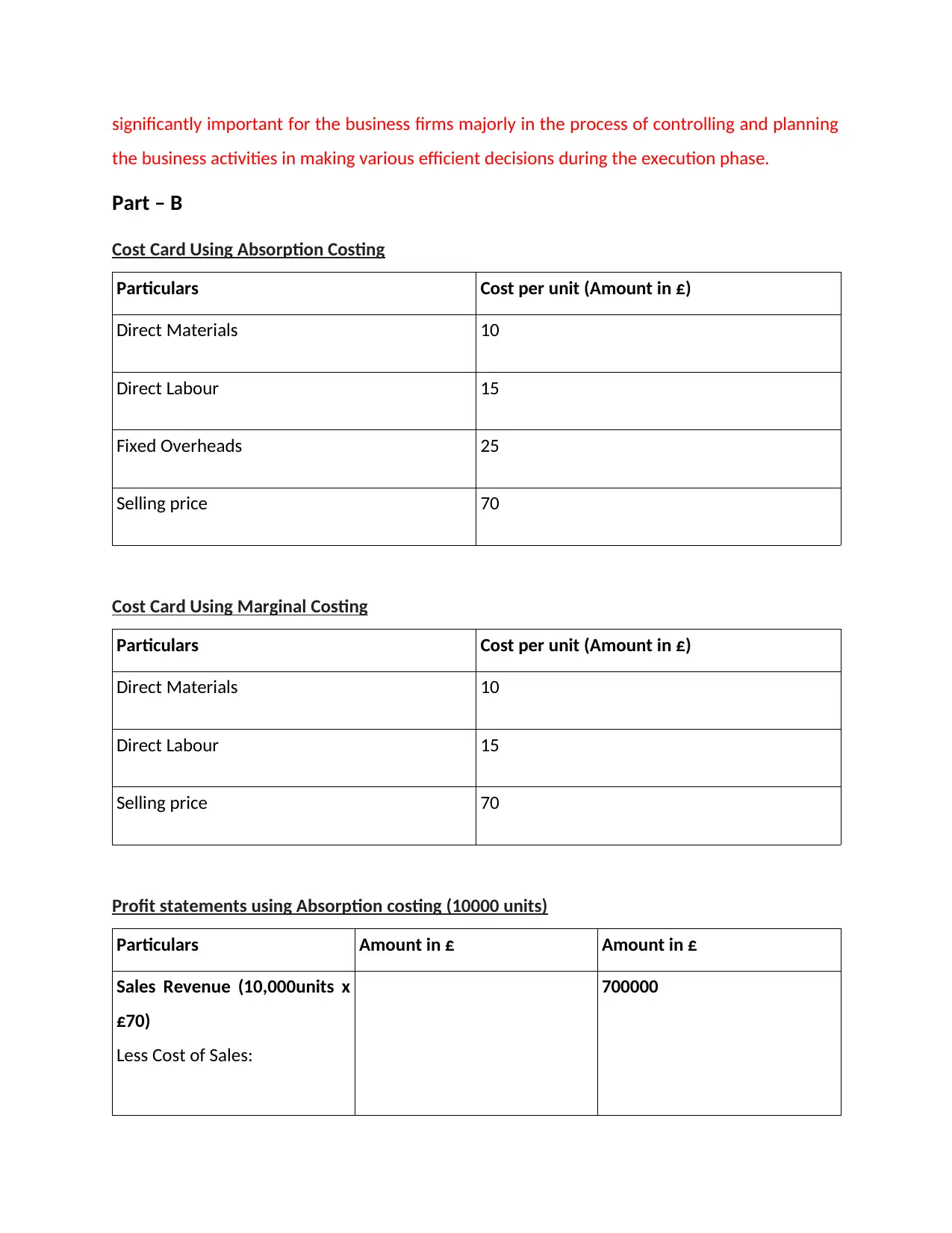

Cost Card Using Absorption Costing

Particulars Cost per unit (Amount in £)

Direct Materials 10

Direct Labour 15

Fixed Overheads 25

Selling price 70

Cost Card Using Marginal Costing

Particulars Cost per unit (Amount in £)

Direct Materials 10

Direct Labour 15

Selling price 70

Profit statements using Absorption costing (10000 units)

Particulars Amount in £ Amount in £

Sales Revenue (10,000units x

£70)

Less Cost of Sales:

700000

the business activities in making various efficient decisions during the execution phase.

Part – B

Cost Card Using Absorption Costing

Particulars Cost per unit (Amount in £)

Direct Materials 10

Direct Labour 15

Fixed Overheads 25

Selling price 70

Cost Card Using Marginal Costing

Particulars Cost per unit (Amount in £)

Direct Materials 10

Direct Labour 15

Selling price 70

Profit statements using Absorption costing (10000 units)

Particulars Amount in £ Amount in £

Sales Revenue (10,000units x

£70)

Less Cost of Sales:

700000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

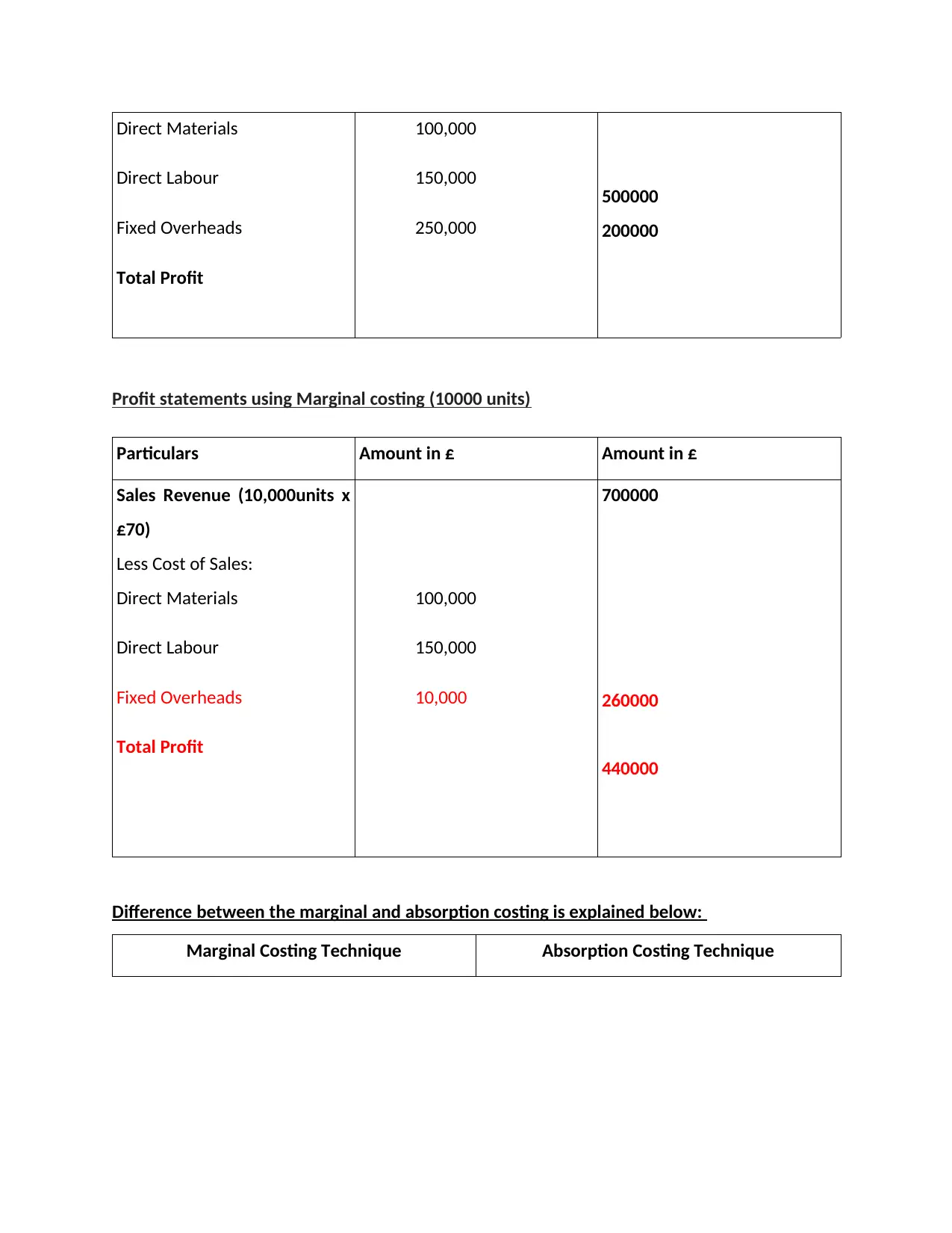

Direct Materials

Direct Labour

Fixed Overheads

Total Profit

100,000

150,000

250,000

500000

200000

Profit statements using Marginal costing (10000 units)

Particulars Amount in £ Amount in £

Sales Revenue (10,000units x

£70)

Less Cost of Sales:

Direct Materials

Direct Labour

Fixed Overheads

Total Profit

100,000

150,000

10,000

700000

260000

440000

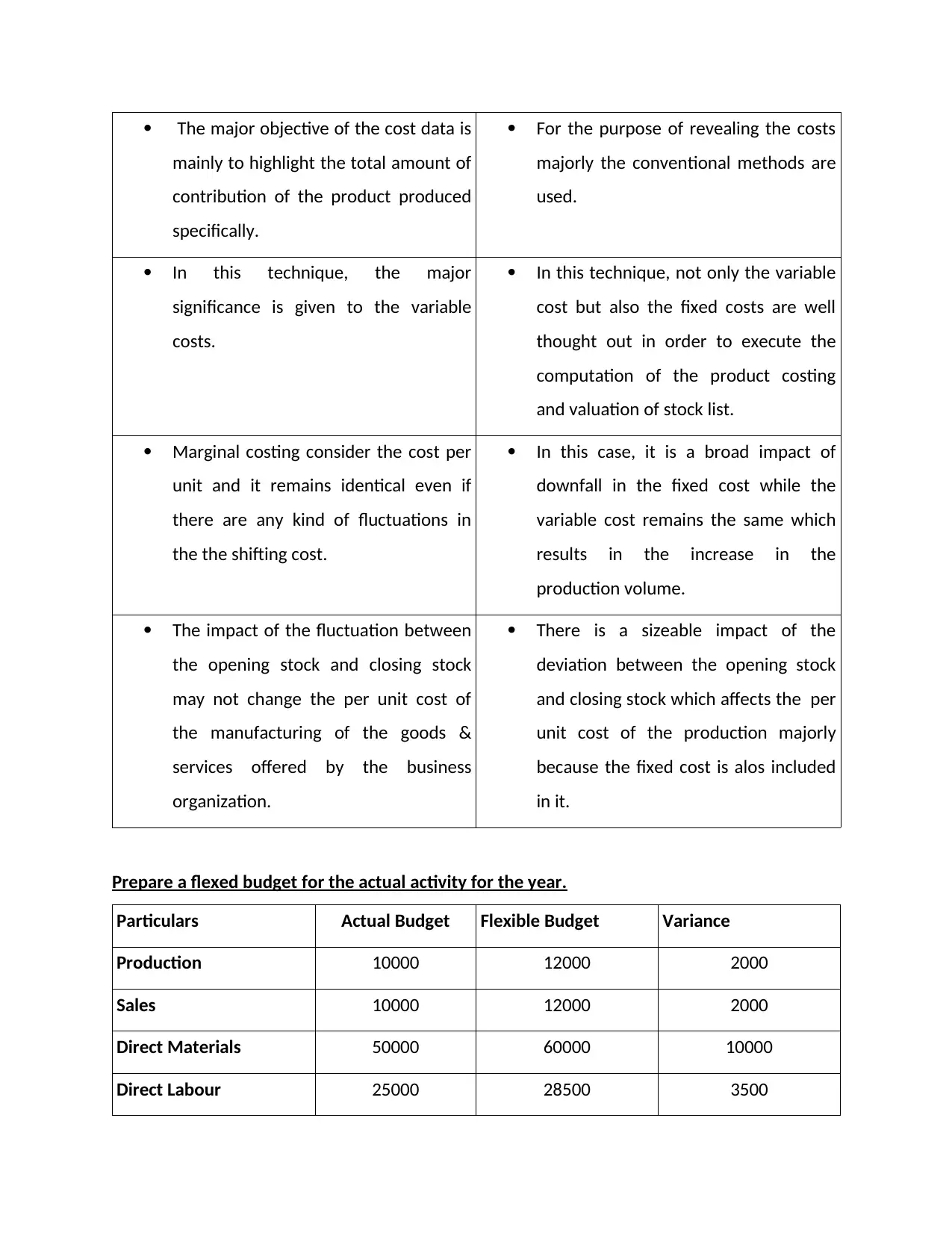

Difference between the marginal and absorption costing is explained below:

Marginal Costing Technique Absorption Costing Technique

Direct Labour

Fixed Overheads

Total Profit

100,000

150,000

250,000

500000

200000

Profit statements using Marginal costing (10000 units)

Particulars Amount in £ Amount in £

Sales Revenue (10,000units x

£70)

Less Cost of Sales:

Direct Materials

Direct Labour

Fixed Overheads

Total Profit

100,000

150,000

10,000

700000

260000

440000

Difference between the marginal and absorption costing is explained below:

Marginal Costing Technique Absorption Costing Technique

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The major objective of the cost data is

mainly to highlight the total amount of

contribution of the product produced

specifically.

For the purpose of revealing the costs

majorly the conventional methods are

used.

In this technique, the major

significance is given to the variable

costs.

In this technique, not only the variable

cost but also the fixed costs are well

thought out in order to execute the

computation of the product costing

and valuation of stock list.

Marginal costing consider the cost per

unit and it remains identical even if

there are any kind of fluctuations in

the the shifting cost.

In this case, it is a broad impact of

downfall in the fixed cost while the

variable cost remains the same which

results in the increase in the

production volume.

The impact of the fluctuation between

the opening stock and closing stock

may not change the per unit cost of

the manufacturing of the goods &

services offered by the business

organization.

There is a sizeable impact of the

deviation between the opening stock

and closing stock which affects the per

unit cost of the production majorly

because the fixed cost is alos included

in it.

Prepare a flexed budget for the actual activity for the year.

Particulars Actual Budget Flexible Budget Variance

Production 10000 12000 2000

Sales 10000 12000 2000

Direct Materials 50000 60000 10000

Direct Labour 25000 28500 3500

mainly to highlight the total amount of

contribution of the product produced

specifically.

For the purpose of revealing the costs

majorly the conventional methods are

used.

In this technique, the major

significance is given to the variable

costs.

In this technique, not only the variable

cost but also the fixed costs are well

thought out in order to execute the

computation of the product costing

and valuation of stock list.

Marginal costing consider the cost per

unit and it remains identical even if

there are any kind of fluctuations in

the the shifting cost.

In this case, it is a broad impact of

downfall in the fixed cost while the

variable cost remains the same which

results in the increase in the

production volume.

The impact of the fluctuation between

the opening stock and closing stock

may not change the per unit cost of

the manufacturing of the goods &

services offered by the business

organization.

There is a sizeable impact of the

deviation between the opening stock

and closing stock which affects the per

unit cost of the production majorly

because the fixed cost is alos included

in it.

Prepare a flexed budget for the actual activity for the year.

Particulars Actual Budget Flexible Budget Variance

Production 10000 12000 2000

Sales 10000 12000 2000

Direct Materials 50000 60000 10000

Direct Labour 25000 28500 3500

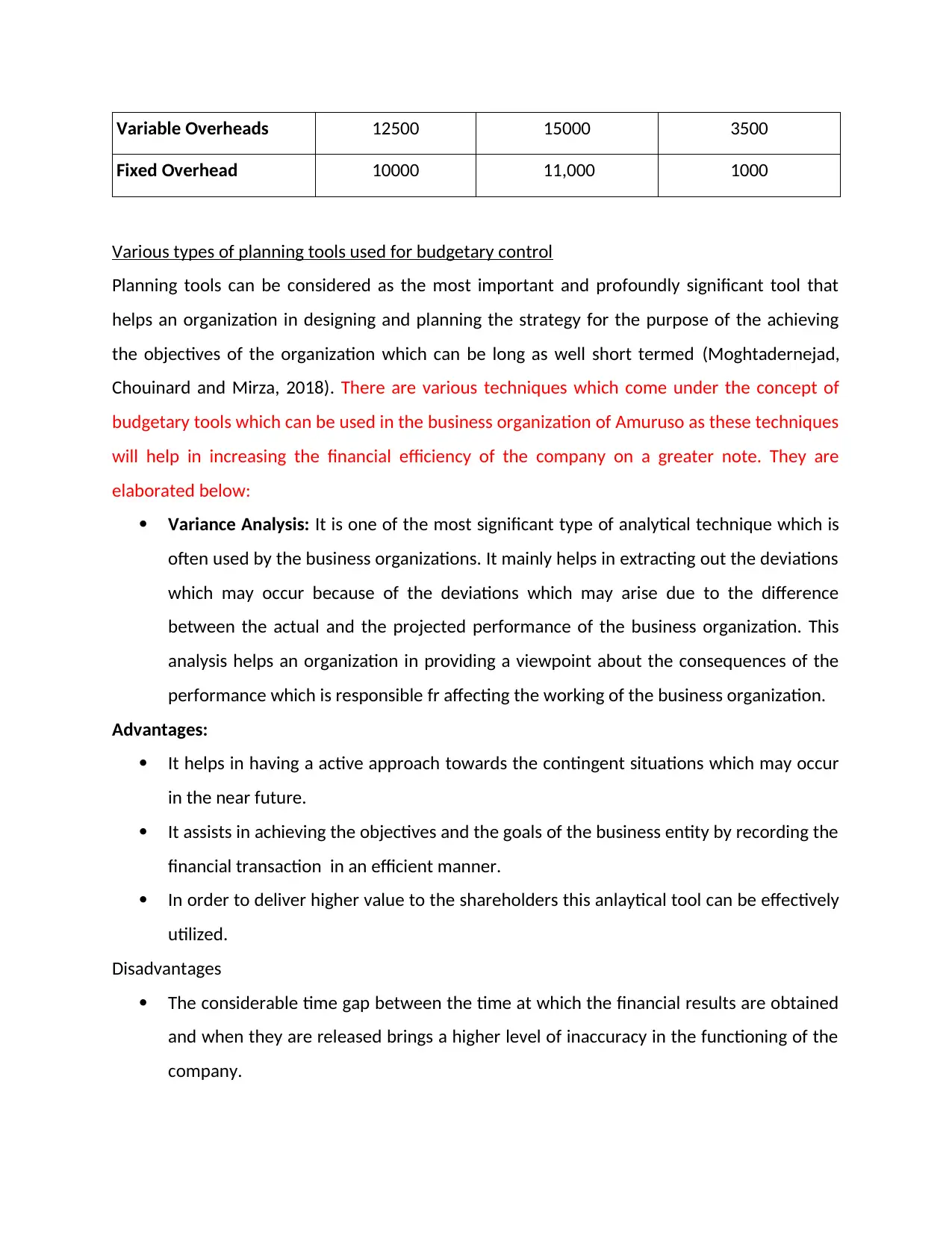

Variable Overheads 12500 15000 3500

Fixed Overhead 10000 11,000 1000

Various types of planning tools used for budgetary control

Planning tools can be considered as the most important and profoundly significant tool that

helps an organization in designing and planning the strategy for the purpose of the achieving

the objectives of the organization which can be long as well short termed (Moghtadernejad,

Chouinard and Mirza, 2018). There are various techniques which come under the concept of

budgetary tools which can be used in the business organization of Amuruso as these techniques

will help in increasing the financial efficiency of the company on a greater note. They are

elaborated below:

Variance Analysis: It is one of the most significant type of analytical technique which is

often used by the business organizations. It mainly helps in extracting out the deviations

which may occur because of the deviations which may arise due to the difference

between the actual and the projected performance of the business organization. This

analysis helps an organization in providing a viewpoint about the consequences of the

performance which is responsible fr affecting the working of the business organization.

Advantages:

It helps in having a active approach towards the contingent situations which may occur

in the near future.

It assists in achieving the objectives and the goals of the business entity by recording the

financial transaction in an efficient manner.

In order to deliver higher value to the shareholders this anlaytical tool can be effectively

utilized.

Disadvantages

The considerable time gap between the time at which the financial results are obtained

and when they are released brings a higher level of inaccuracy in the functioning of the

company.

Fixed Overhead 10000 11,000 1000

Various types of planning tools used for budgetary control

Planning tools can be considered as the most important and profoundly significant tool that

helps an organization in designing and planning the strategy for the purpose of the achieving

the objectives of the organization which can be long as well short termed (Moghtadernejad,

Chouinard and Mirza, 2018). There are various techniques which come under the concept of

budgetary tools which can be used in the business organization of Amuruso as these techniques

will help in increasing the financial efficiency of the company on a greater note. They are

elaborated below:

Variance Analysis: It is one of the most significant type of analytical technique which is

often used by the business organizations. It mainly helps in extracting out the deviations

which may occur because of the deviations which may arise due to the difference

between the actual and the projected performance of the business organization. This

analysis helps an organization in providing a viewpoint about the consequences of the

performance which is responsible fr affecting the working of the business organization.

Advantages:

It helps in having a active approach towards the contingent situations which may occur

in the near future.

It assists in achieving the objectives and the goals of the business entity by recording the

financial transaction in an efficient manner.

In order to deliver higher value to the shareholders this anlaytical tool can be effectively

utilized.

Disadvantages

The considerable time gap between the time at which the financial results are obtained

and when they are released brings a higher level of inaccuracy in the functioning of the

company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.