Management Accounting Report: Decision Making in X Limited

VerifiedAdded on 2022/11/17

|14

|1594

|92

Report

AI Summary

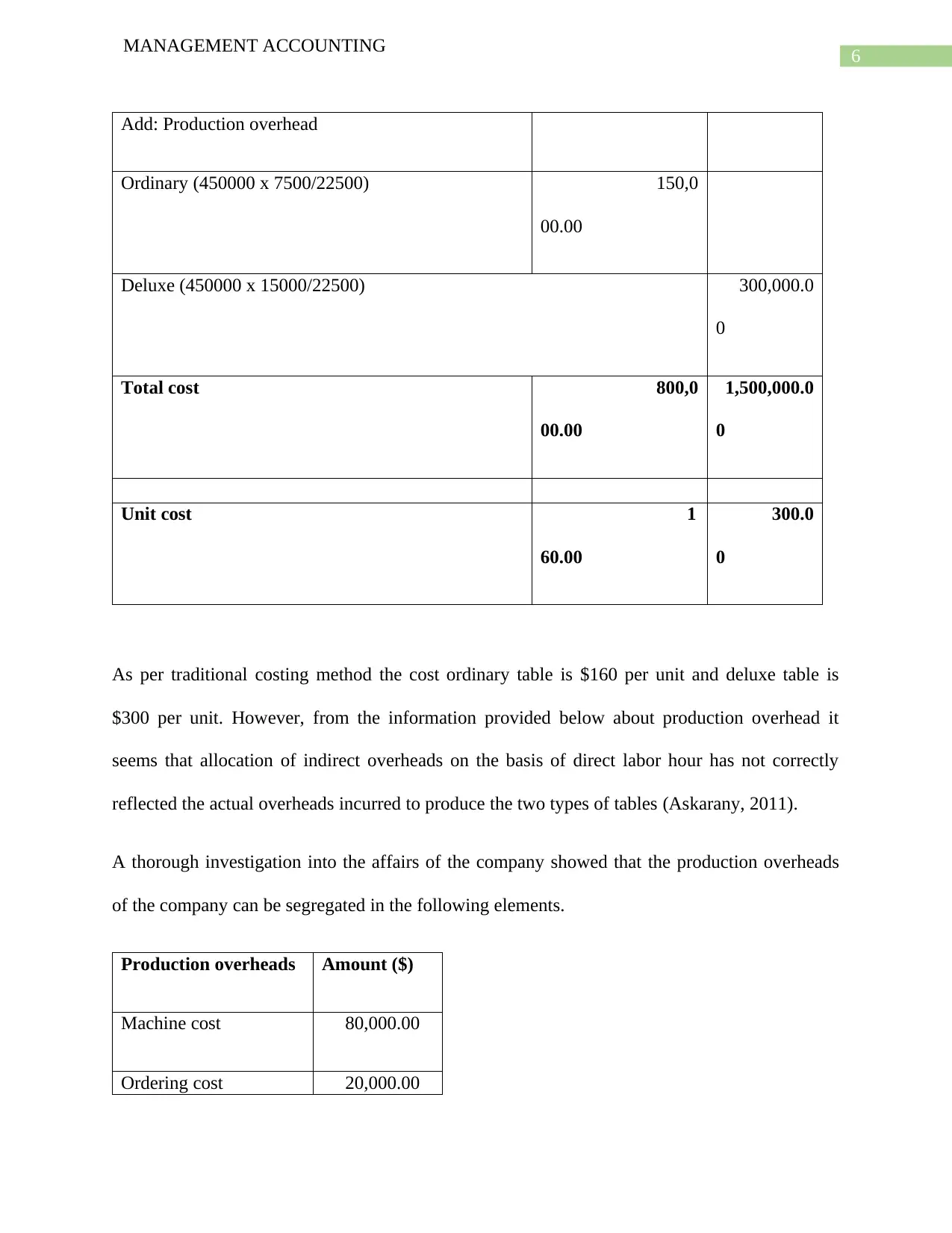

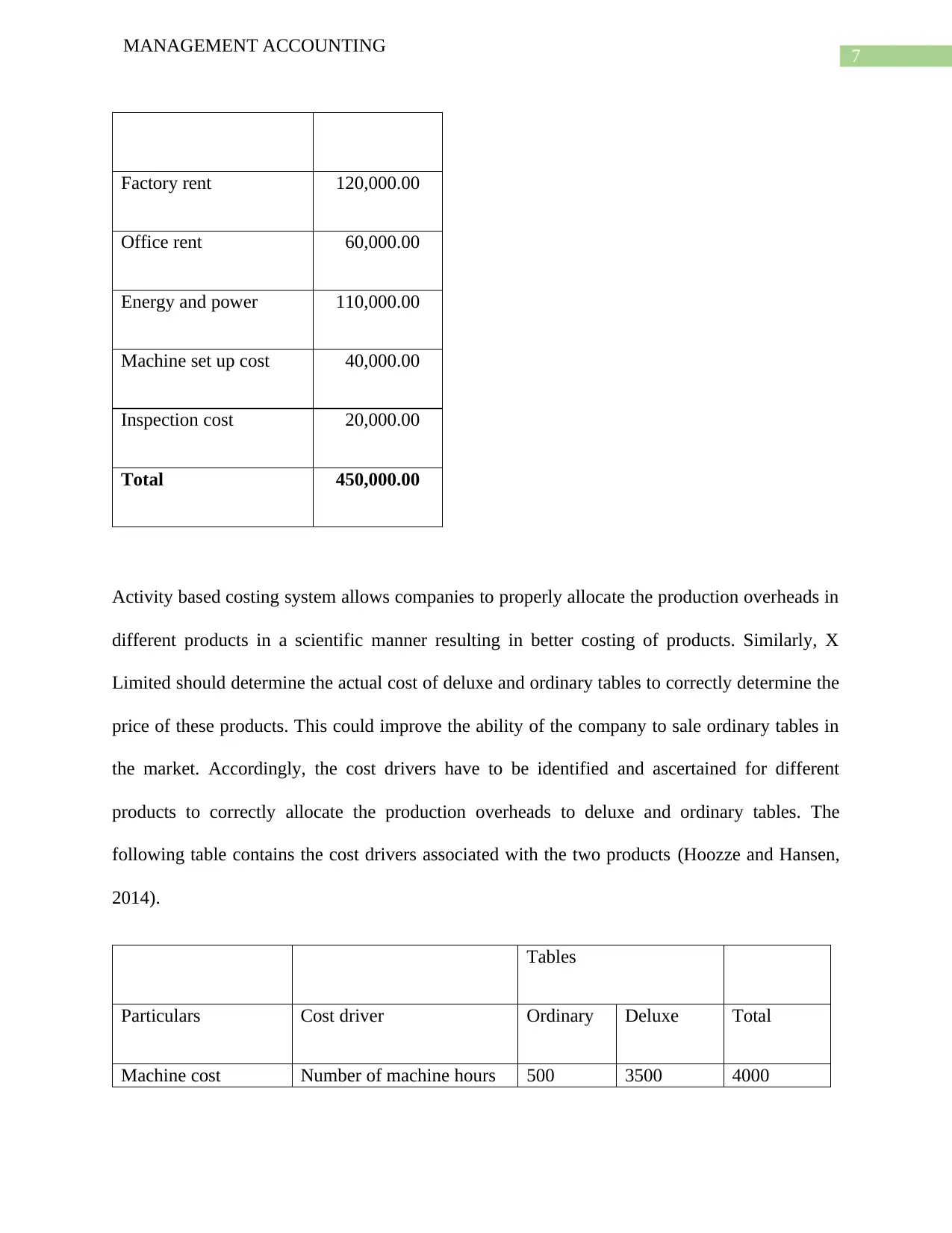

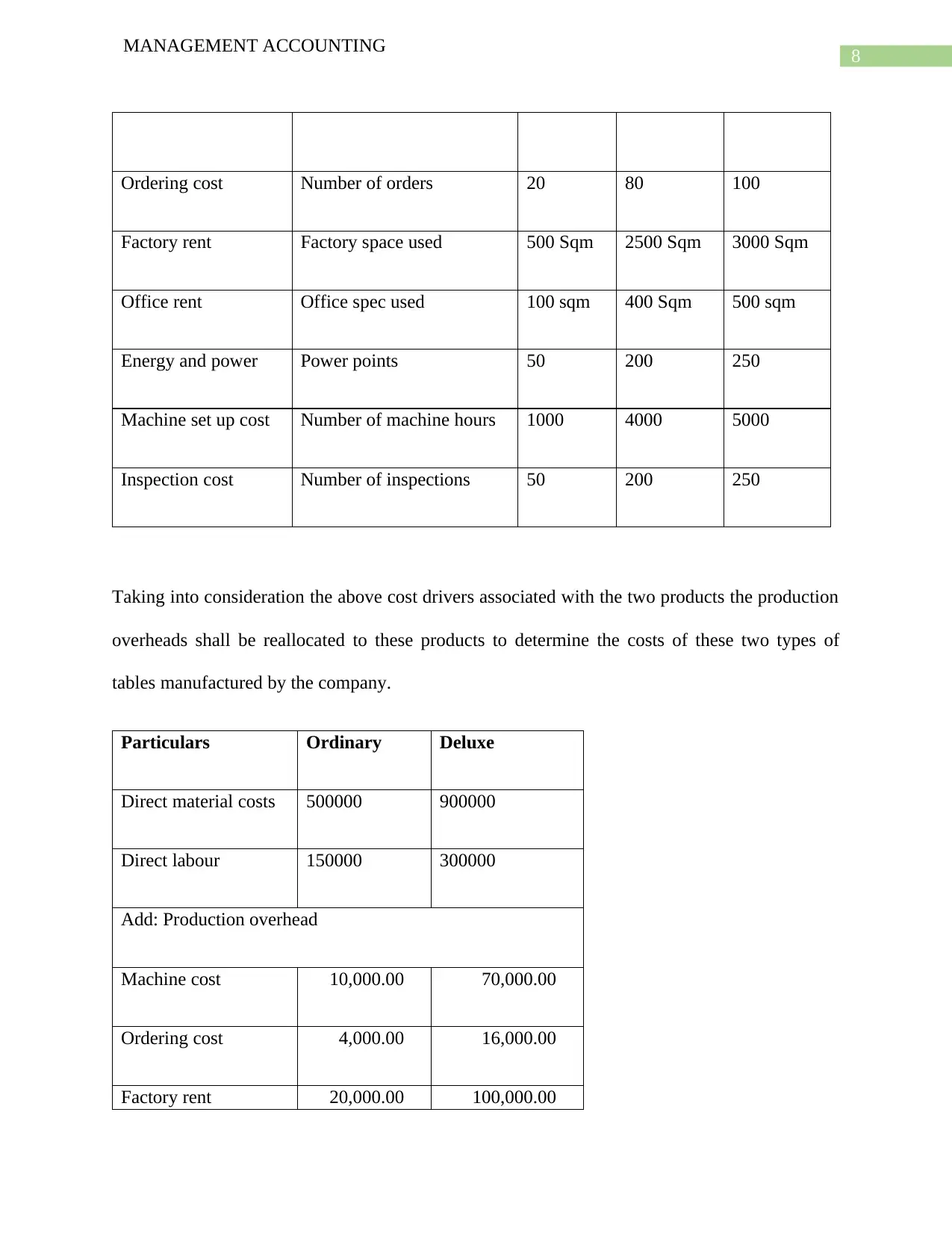

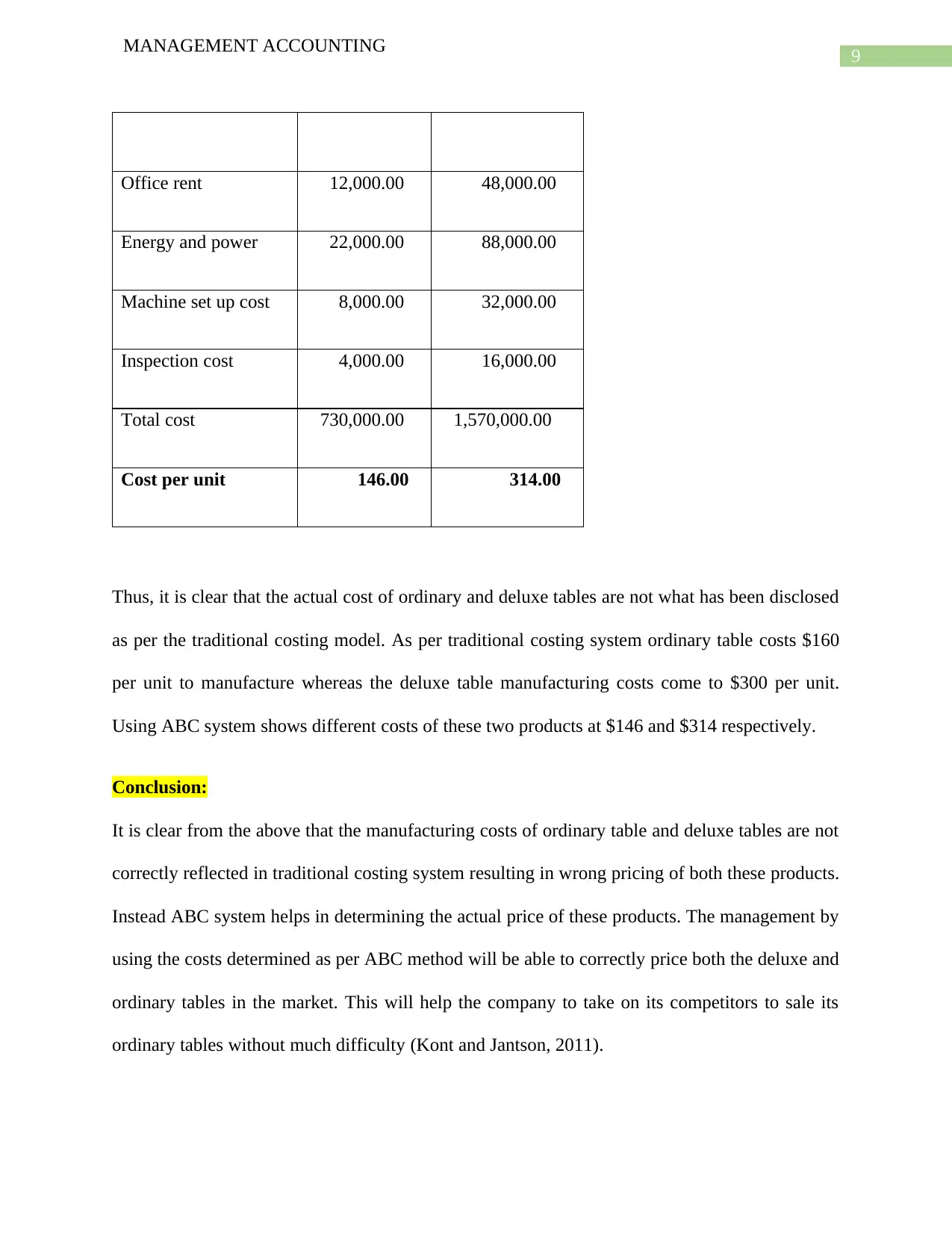

This report analyzes the significance of management accounting in business decision-making, using the case of X Limited, a computer table manufacturer. The company faces challenges selling its ordinary tables due to competitor pricing. The report examines the allocation of production overheads using traditional costing methods and identifies the limitations. It then demonstrates the application of Activity-Based Costing (ABC) to accurately allocate overheads, revealing the true costs of both ordinary and deluxe tables. The analysis includes quantitative data, cost driver identification, and a comparison of costing methods. The conclusion emphasizes the importance of ABC for correct product pricing and recommends adjusting selling prices based on ABC results to improve sales. The report highlights the benefits of management accounting in strategic pricing and competitive advantage.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.