Management Accounting Report: Profitability and Strategic Decisions

VerifiedAdded on 2019/09/16

|14

|2594

|364

Report

AI Summary

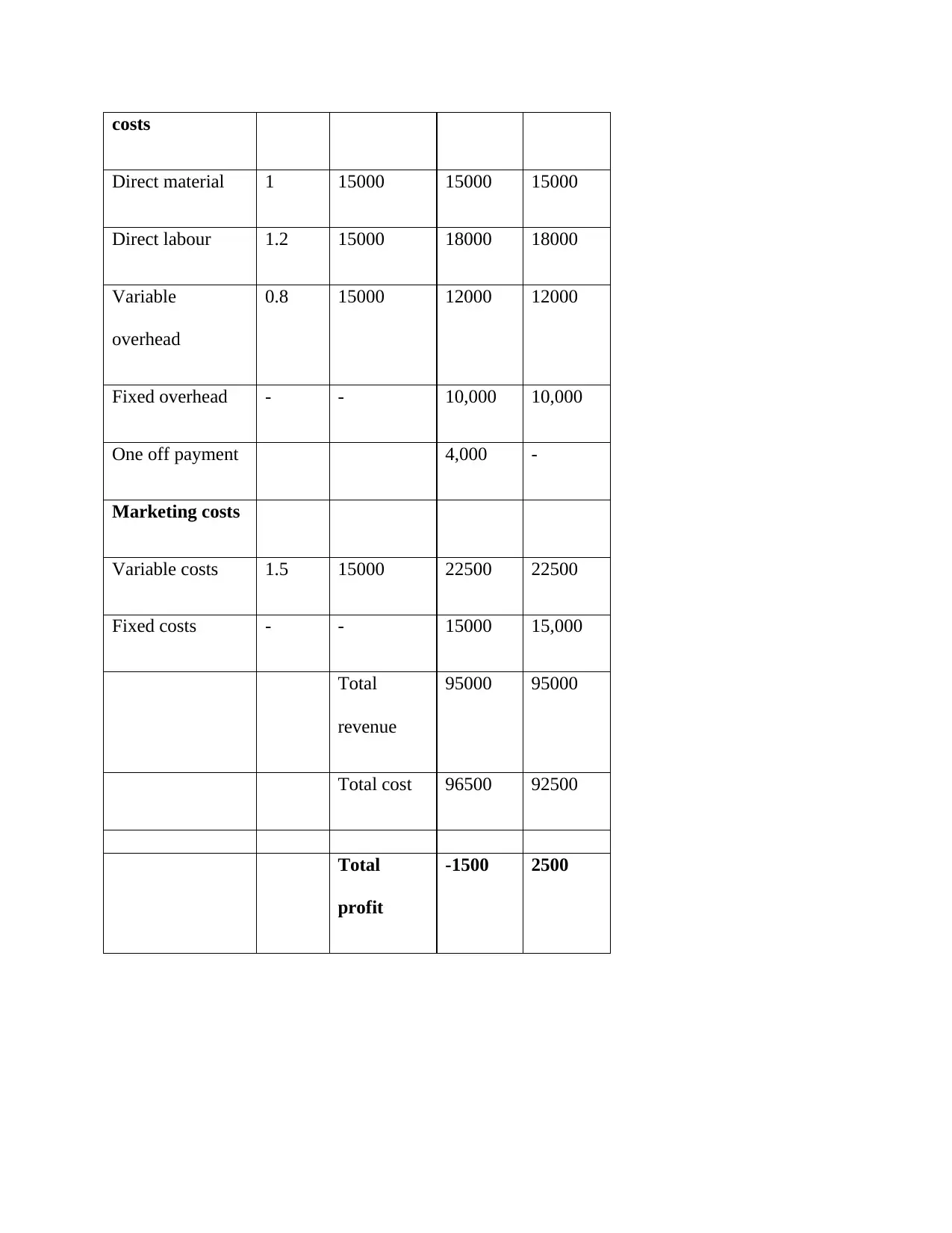

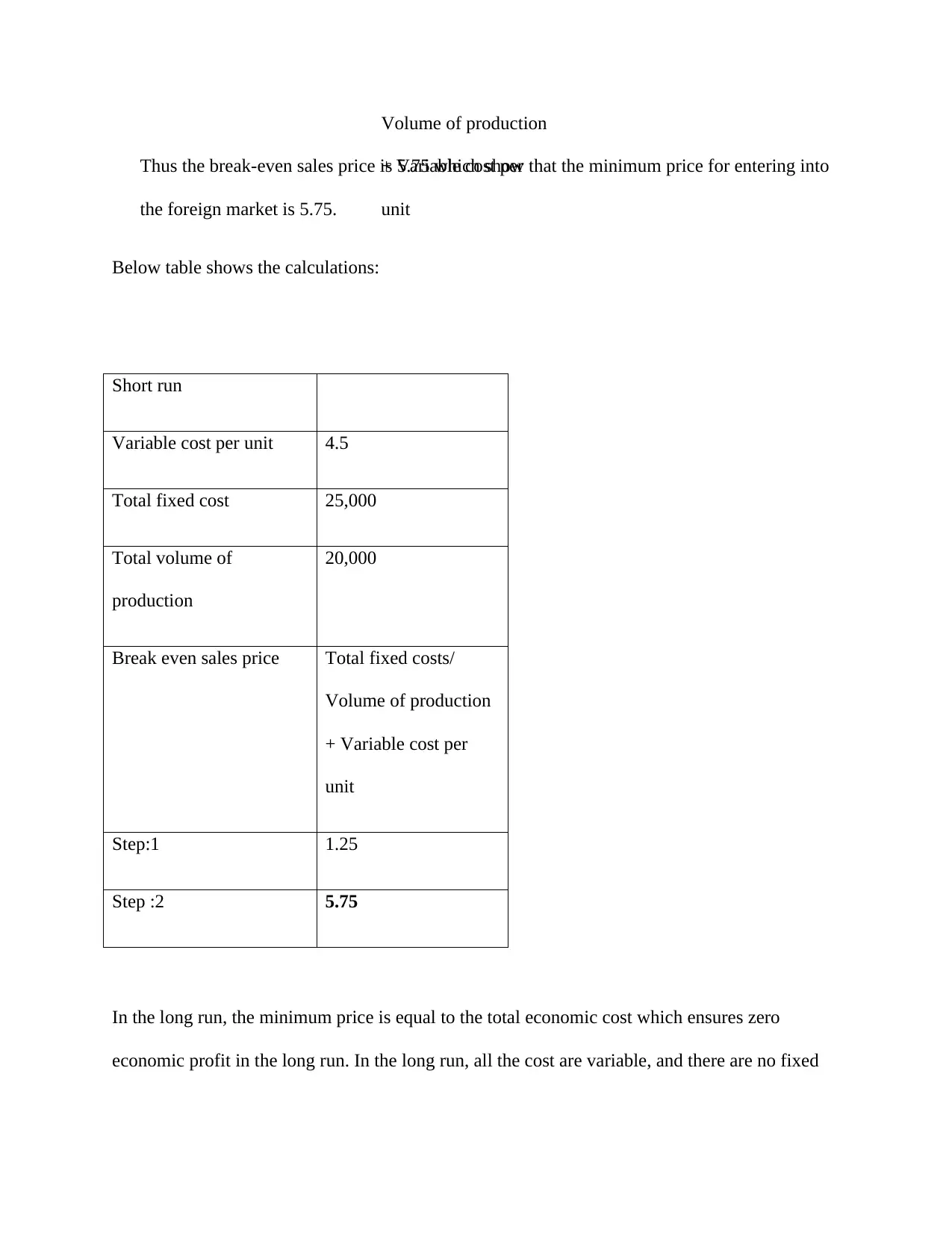

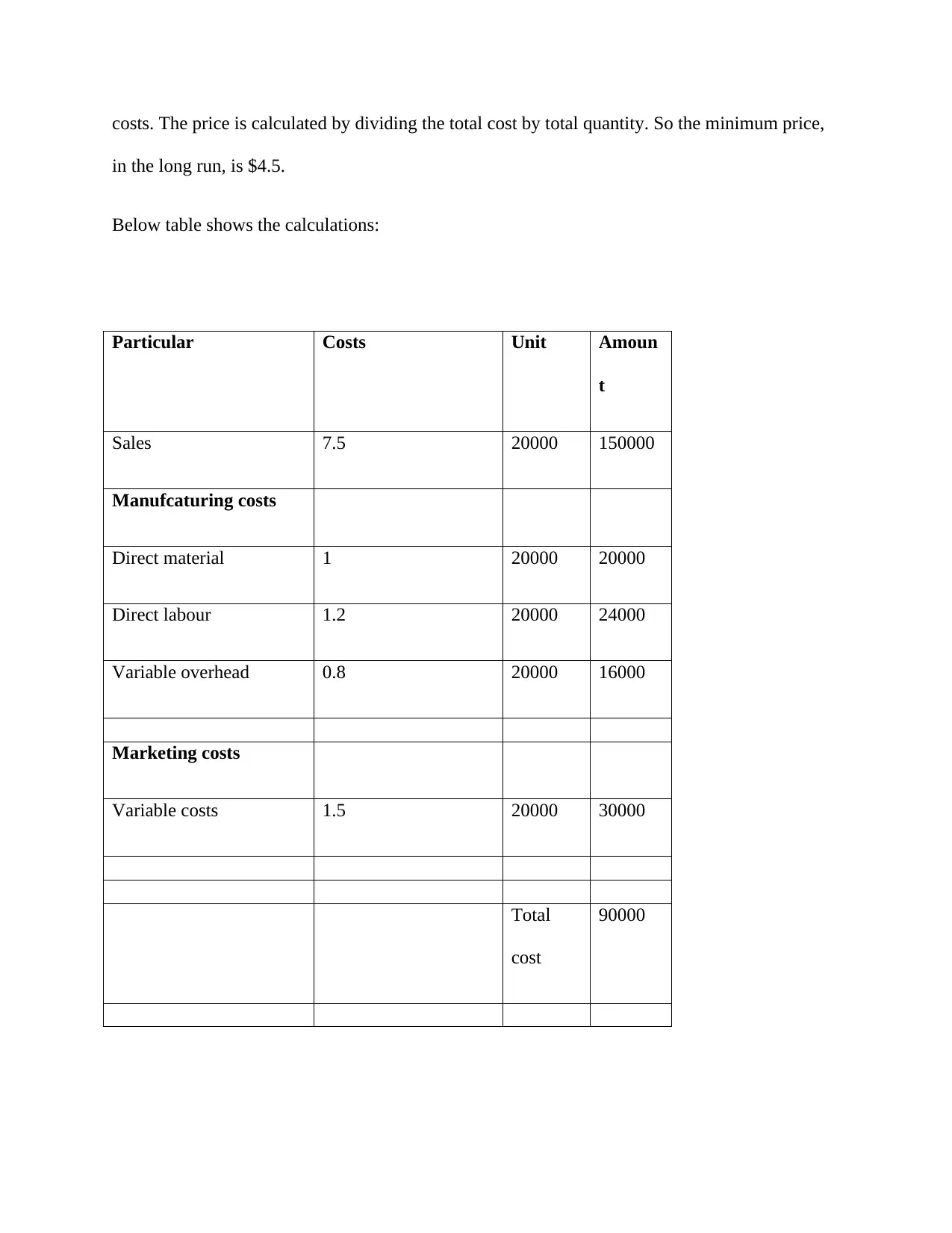

This management accounting report examines various aspects of a company's financial performance and strategic decision-making. It begins by calculating monthly profit, considering sales revenue, manufacturing costs (direct materials, labor, overhead), and marketing expenses. The report then analyzes factors crucial for accepting orders, including profit margins, offer value, brand benefits, and long-term implications. It evaluates a long-term government contract, assessing its impact on brand image, organizational value, and sustainable profit. Furthermore, the report explores the foreign market, determining the minimum selling price and break-even analysis. Finally, it assesses offers from outside suppliers, comparing in-house production costs with outsourcing options and analyzing the financial impact of different supplier offers, ultimately aiming to maximize profitability and achieve long-term goals. The report uses financial calculations to support its conclusions.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.