Management Accounting Report

VerifiedAdded on 2020/02/05

|13

|3741

|409

Report

AI Summary

This report delves into management accounting, defining it and outlining essential system requirements. It explores various managerial accounting reporting methods, including budget reports, inventory and manufacturing reports, and job cost reports. The report then calculates unit cost and profit margin using both absorption and marginal costing, highlighting their differences and suitability. Different planning tools for budgetary control are examined, comparing the advantages and disadvantages of traditional (incremental) and modern (zero-base, activity-based) budgeting techniques. A case study involving the computation of PVC sheet standard cost and identification of material price and quantity variance is included. Finally, the report compares the management accounting systems used by Dell and HP to respond to financial problems, concluding that Dell's approach, utilizing zero-base and activity-based budgeting, is more effective in the modern business environment.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................2

P1 Defining management accounting and presenting the essential requirements of such

system.....................................................................................................................................2

P2 Explaining different methods used for managerial accounting reporting.........................3

P3 Calculating unit cost and profit margin by using absorption as well as marginal costing4

P4 Explaining the advantages and disadvantages of different types of planning tools that

are used for budgetary control................................................................................................6

A. Computation of PVC’s sheet standard cost.......................................................................8

B. Identifying material price and quantity price....................................................................8

P5 Comparing the management accounting system used by Dell with HP that is used to

respond financial problems....................................................................................................9

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................11

INTRODUCTION......................................................................................................................2

P1 Defining management accounting and presenting the essential requirements of such

system.....................................................................................................................................2

P2 Explaining different methods used for managerial accounting reporting.........................3

P3 Calculating unit cost and profit margin by using absorption as well as marginal costing4

P4 Explaining the advantages and disadvantages of different types of planning tools that

are used for budgetary control................................................................................................6

A. Computation of PVC’s sheet standard cost.......................................................................8

B. Identifying material price and quantity price....................................................................8

P5 Comparing the management accounting system used by Dell with HP that is used to

respond financial problems....................................................................................................9

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................11

INTRODUCTION

In the resent times, importance of management accounting increased significantly.

Moreover, it provides deeper insight to management about the financial performance and

position of each department. Field of management accounting lays high level of emphasis on

preparing and producing suitable reports about monetary as well as internal process and

performance. In this, by making continuous evaluation of performance level firm can take

strategic action that aid in both productivity and profitability aspect of firm. The present

report is based on Dell which offers high quality computer, laptops and electronic gazettes to

the customers. In this, report will provide deeper insight about the manner in which tools of

management accounting facilitates effective decision making. Besides this, report will also

shed light on the different type budgeting and budgetary control techniques. Along with this,

it will develop understanding about the way in which financial problems can be addressed.

P1 Defining management accounting and presenting the essential requirements of such

system

Management accounting is the field of finance which provides high level of assistance

to the team of higher management in decision making. Moreover, such accounting field lays

high level of emphasis on preparing and providing financial as well as statistical information

to the managers. Thus, daily reports which are made by management accounting team

facilitate day to day and effectual short term managerial decision making. By using such

reports manager of Dell can take suitable decision and thereby would become able to gain

competitive edge over others. Management accounting techniques highly differ from

financial accounting to a great extent (Management accounting: scope and importance,

2017). Moreover, reports which are produced on the basis of financial accounting technique

used by both internal and external stakeholders.

Further, financial accounting reports are prepared by the firm on quarterly, semi-annual

and annual basis. On the other side, management accounting reports are framed on daily,

weekly and monthly basis (Rubin, 2016). Thus, managerial accounting reports give input to

the higher management team of Dell for decision making. There are several management

accounting systems that can be undertaken by Dell are as follows:

Job costing: This method of costing lays high level of emphasis on accumulation of

several costs such as material, labor and overhead. By undertaking job costing method

In the resent times, importance of management accounting increased significantly.

Moreover, it provides deeper insight to management about the financial performance and

position of each department. Field of management accounting lays high level of emphasis on

preparing and producing suitable reports about monetary as well as internal process and

performance. In this, by making continuous evaluation of performance level firm can take

strategic action that aid in both productivity and profitability aspect of firm. The present

report is based on Dell which offers high quality computer, laptops and electronic gazettes to

the customers. In this, report will provide deeper insight about the manner in which tools of

management accounting facilitates effective decision making. Besides this, report will also

shed light on the different type budgeting and budgetary control techniques. Along with this,

it will develop understanding about the way in which financial problems can be addressed.

P1 Defining management accounting and presenting the essential requirements of such

system

Management accounting is the field of finance which provides high level of assistance

to the team of higher management in decision making. Moreover, such accounting field lays

high level of emphasis on preparing and providing financial as well as statistical information

to the managers. Thus, daily reports which are made by management accounting team

facilitate day to day and effectual short term managerial decision making. By using such

reports manager of Dell can take suitable decision and thereby would become able to gain

competitive edge over others. Management accounting techniques highly differ from

financial accounting to a great extent (Management accounting: scope and importance,

2017). Moreover, reports which are produced on the basis of financial accounting technique

used by both internal and external stakeholders.

Further, financial accounting reports are prepared by the firm on quarterly, semi-annual

and annual basis. On the other side, management accounting reports are framed on daily,

weekly and monthly basis (Rubin, 2016). Thus, managerial accounting reports give input to

the higher management team of Dell for decision making. There are several management

accounting systems that can be undertaken by Dell are as follows:

Job costing: This method of costing lays high level of emphasis on accumulation of

several costs such as material, labor and overhead. By undertaking job costing method

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

firm can assess the cost which is associated with the specific business activity (Job

costing, 2017). Hence, by using such method manager of the business unit can trace

the job and thereby would become able to identify whether cost can be reduced in the

later jobs or not. It is highly appropriate for the firms which are involved in designing

software, construction of machine and manufacturing of small batch products.

Batch costing: Such costing method is highly effectual which in turn helps in

assessing cost in the engineering component such as footwear, clothing and

manufacturing sector. In this, by assigning the batch number cost of similar units can

be assessed in an effectual way (Job and batch costing, 2017). Thus, by adding profit

margin in the unit cost business unit can determine suitable price of the products

offered. Such costing method is highly effective that can be used by Dell to ascertain

the cost and price of similarly manufactured units.

Process costing: Such costing method that assists in tracing and accumulating direct

cost in an effectual way. By using this, company would become able to allocate

indirect cost in the best possible way (Process costing, 2017). Process costing method

is useful where mass production of similar products is undertaken. Further, it is highly

appropriate for the firms in which output of individual units cannot be differentiated

from each other. In this, manager of the firm assumes that cost of every product is

same.

P2 Explaining different methods used for managerial accounting reporting

Managerial accounting reports are the one which furnishes information about the

internal business process and performance. By making assessments of reports manager of the

firm can monitor performance level in an effectual way. On the basis of time sensitivity and

requirement manager prepares report on daily, weekly and monthly basis.

Budget report: Dell is the large sized business organization who deals in computer,

laptops and other electronic gazettes. Thus, in the large sized business organization,

manager of Dell can get information about the performance of each department

through the means of budget report. Moreover, such report contains information

regarding the extent to which specific department has attained budgeted figures. In

this, by using such report higher management team of Dell can assess the training

requirements of personnel (Bogsnes, 2016). In this way, by evaluating the causes of

deviations firm can take suitable action for improvement. Thus, budget report is

highly significant which in turn helps in measuring the efficiency level of personnel.

costing, 2017). Hence, by using such method manager of the business unit can trace

the job and thereby would become able to identify whether cost can be reduced in the

later jobs or not. It is highly appropriate for the firms which are involved in designing

software, construction of machine and manufacturing of small batch products.

Batch costing: Such costing method is highly effectual which in turn helps in

assessing cost in the engineering component such as footwear, clothing and

manufacturing sector. In this, by assigning the batch number cost of similar units can

be assessed in an effectual way (Job and batch costing, 2017). Thus, by adding profit

margin in the unit cost business unit can determine suitable price of the products

offered. Such costing method is highly effective that can be used by Dell to ascertain

the cost and price of similarly manufactured units.

Process costing: Such costing method that assists in tracing and accumulating direct

cost in an effectual way. By using this, company would become able to allocate

indirect cost in the best possible way (Process costing, 2017). Process costing method

is useful where mass production of similar products is undertaken. Further, it is highly

appropriate for the firms in which output of individual units cannot be differentiated

from each other. In this, manager of the firm assumes that cost of every product is

same.

P2 Explaining different methods used for managerial accounting reporting

Managerial accounting reports are the one which furnishes information about the

internal business process and performance. By making assessments of reports manager of the

firm can monitor performance level in an effectual way. On the basis of time sensitivity and

requirement manager prepares report on daily, weekly and monthly basis.

Budget report: Dell is the large sized business organization who deals in computer,

laptops and other electronic gazettes. Thus, in the large sized business organization,

manager of Dell can get information about the performance of each department

through the means of budget report. Moreover, such report contains information

regarding the extent to which specific department has attained budgeted figures. In

this, by using such report higher management team of Dell can assess the training

requirements of personnel (Bogsnes, 2016). In this way, by evaluating the causes of

deviations firm can take suitable action for improvement. Thus, budget report is

highly significant which in turn helps in measuring the efficiency level of personnel.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hence, by getting information regarding such aspect manager of Dell can develop

suitable incentive plan and bonus policies for personnel.

Inventory and manufacturing: Process of manufacturing can be made by the

company more efficient through the means of such reporting system. Inventory and

manufacturing report provides deeper insight about the wastage level, labor cost,

hours and per unit overhead cost (Francis and et.al., 2015). In this, by making

evaluation of the cost and wastage level manager of Dell can identify the area of

business operations which account for greater control. In this way, Dell can attain can

attain success by taking actions for improvement within the suitable time period.

Besides this, manager can also motivate the personnel of specific department who is

performing well.

Job cost report: This report shows the profitability which is associated with the

specific project. In this, by making estimation of expenses with the estimated amount

firm can evaluate the profitability which is associated with the specific job. By

undertaking such report business unit can identify the business areas which accounts

for higher profit (Goddard and Simm, 2017). In addition to this, such report also helps

in evaluating the job that has lower margin. By keeping all such aspects in mind firm

can take highly effectual and suitable action within the fewer time frames.

By considering all the above aspects, it can be stated that managerial reporting system

aids in suitable decision making.

P3 Calculating unit cost and profit margin by using absorption as well as marginal costing

Absorption costing: It is also known as full costing method which in turn helps in

presenting the suitable view of cost as well as profit. Absorption costing method assists in

dividing the total according to the cost center. Under this method, manager considers both

fixed and variable cost as product cost (Hernandez, Jonker and Kosse, 2017). In absorption

costing method, overhead cost can be presented in the form of production, administration,

selling & distribution. Hence, due to the inclusion of fixed cost profitability aspect of firm is

highly affected to a great extent. Thus, difference which takes place between the opening and

closing inventory has great impact on cost per unit. By using such method firm can evaluate

net profit margin and presents data in a conventional way.

Marginal costing: Decision making technique which is used to ascertain the total cost

of production is known as marginal costing method. In this, variable cost is considered as

suitable incentive plan and bonus policies for personnel.

Inventory and manufacturing: Process of manufacturing can be made by the

company more efficient through the means of such reporting system. Inventory and

manufacturing report provides deeper insight about the wastage level, labor cost,

hours and per unit overhead cost (Francis and et.al., 2015). In this, by making

evaluation of the cost and wastage level manager of Dell can identify the area of

business operations which account for greater control. In this way, Dell can attain can

attain success by taking actions for improvement within the suitable time period.

Besides this, manager can also motivate the personnel of specific department who is

performing well.

Job cost report: This report shows the profitability which is associated with the

specific project. In this, by making estimation of expenses with the estimated amount

firm can evaluate the profitability which is associated with the specific job. By

undertaking such report business unit can identify the business areas which accounts

for higher profit (Goddard and Simm, 2017). In addition to this, such report also helps

in evaluating the job that has lower margin. By keeping all such aspects in mind firm

can take highly effectual and suitable action within the fewer time frames.

By considering all the above aspects, it can be stated that managerial reporting system

aids in suitable decision making.

P3 Calculating unit cost and profit margin by using absorption as well as marginal costing

Absorption costing: It is also known as full costing method which in turn helps in

presenting the suitable view of cost as well as profit. Absorption costing method assists in

dividing the total according to the cost center. Under this method, manager considers both

fixed and variable cost as product cost (Hernandez, Jonker and Kosse, 2017). In absorption

costing method, overhead cost can be presented in the form of production, administration,

selling & distribution. Hence, due to the inclusion of fixed cost profitability aspect of firm is

highly affected to a great extent. Thus, difference which takes place between the opening and

closing inventory has great impact on cost per unit. By using such method firm can evaluate

net profit margin and presents data in a conventional way.

Marginal costing: Decision making technique which is used to ascertain the total cost

of production is known as marginal costing method. In this, variable cost is considered as

product, whereas fixed is recognized as a period expenses (Simons, 2013). This costing

method classifies overhead cost in terms of fixed and variable. It assumes that variance which

takes place in the opening and closing stock does not have high level of impact on the value

of cost per unit. Along with this, it highlights contribution related to per unit and thereby

helps in assessing the subtraction of variable costs from sales related to each product.

Difference and suitability: Cost consideration is one of the main factors that differentiate

marginal costing from absorption. Moreover, in absorption costing method analysts consider

both fixed and variable cost while making assessment of profitability. On the other side,

marginal costing method only lays emphasis on undertaking variable cost. Hence, such aspect

creates difference between both costing methods significantly (Fullerton, Kennedy and

Widener, 2014). Besides this, inventory valuation methods or techniques also differ in

absorption and marginal costing method. Further, it can be presented that absorption costing

technique is highly effective as compared to marginal method. Moreover, absorption costing

method presents suitable view of financial aspects and thereby helps in making appropriate

decisions.

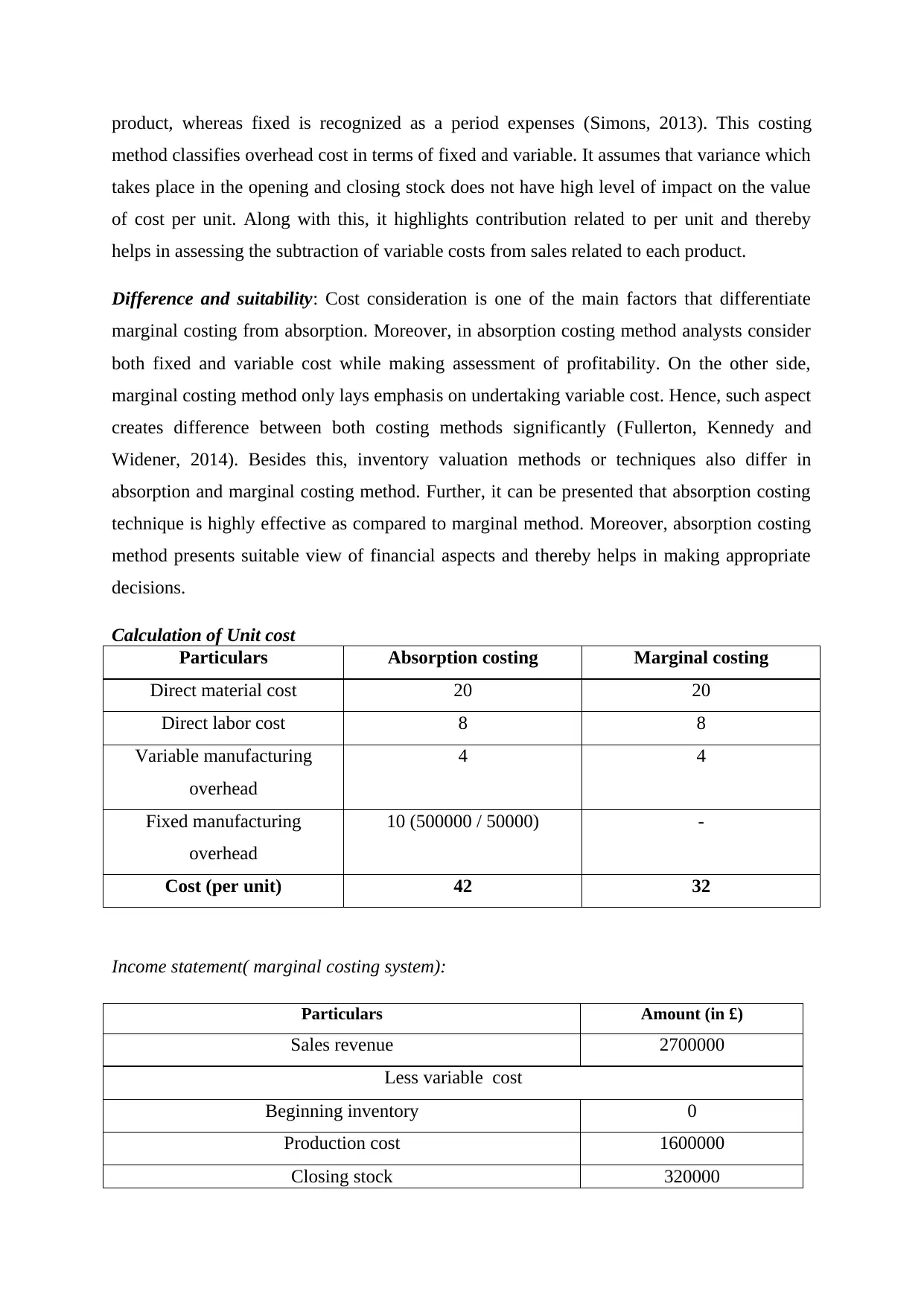

Calculation of Unit cost

Particulars Absorption costing Marginal costing

Direct material cost 20 20

Direct labor cost 8 8

Variable manufacturing

overhead

4 4

Fixed manufacturing

overhead

10 (500000 / 50000) -

Cost (per unit) 42 32

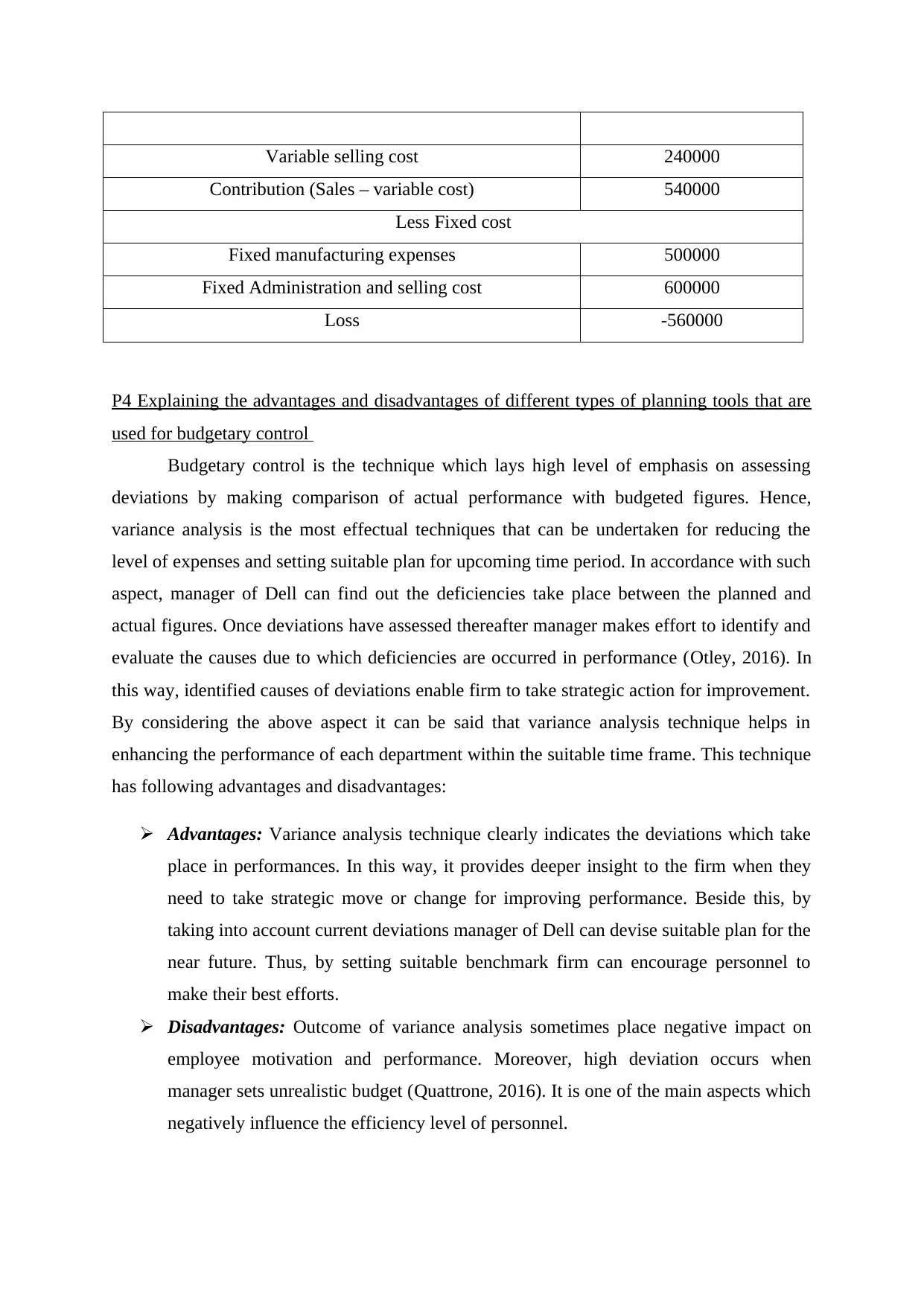

Income statement( marginal costing system):

Particulars Amount (in £)

Sales revenue 2700000

Less variable cost

Beginning inventory 0

Production cost 1600000

Closing stock 320000

method classifies overhead cost in terms of fixed and variable. It assumes that variance which

takes place in the opening and closing stock does not have high level of impact on the value

of cost per unit. Along with this, it highlights contribution related to per unit and thereby

helps in assessing the subtraction of variable costs from sales related to each product.

Difference and suitability: Cost consideration is one of the main factors that differentiate

marginal costing from absorption. Moreover, in absorption costing method analysts consider

both fixed and variable cost while making assessment of profitability. On the other side,

marginal costing method only lays emphasis on undertaking variable cost. Hence, such aspect

creates difference between both costing methods significantly (Fullerton, Kennedy and

Widener, 2014). Besides this, inventory valuation methods or techniques also differ in

absorption and marginal costing method. Further, it can be presented that absorption costing

technique is highly effective as compared to marginal method. Moreover, absorption costing

method presents suitable view of financial aspects and thereby helps in making appropriate

decisions.

Calculation of Unit cost

Particulars Absorption costing Marginal costing

Direct material cost 20 20

Direct labor cost 8 8

Variable manufacturing

overhead

4 4

Fixed manufacturing

overhead

10 (500000 / 50000) -

Cost (per unit) 42 32

Income statement( marginal costing system):

Particulars Amount (in £)

Sales revenue 2700000

Less variable cost

Beginning inventory 0

Production cost 1600000

Closing stock 320000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable selling cost 240000

Contribution (Sales – variable cost) 540000

Less Fixed cost

Fixed manufacturing expenses 500000

Fixed Administration and selling cost 600000

Loss -560000

P4 Explaining the advantages and disadvantages of different types of planning tools that are

used for budgetary control

Budgetary control is the technique which lays high level of emphasis on assessing

deviations by making comparison of actual performance with budgeted figures. Hence,

variance analysis is the most effectual techniques that can be undertaken for reducing the

level of expenses and setting suitable plan for upcoming time period. In accordance with such

aspect, manager of Dell can find out the deficiencies take place between the planned and

actual figures. Once deviations have assessed thereafter manager makes effort to identify and

evaluate the causes due to which deficiencies are occurred in performance (Otley, 2016). In

this way, identified causes of deviations enable firm to take strategic action for improvement.

By considering the above aspect it can be said that variance analysis technique helps in

enhancing the performance of each department within the suitable time frame. This technique

has following advantages and disadvantages:

Advantages: Variance analysis technique clearly indicates the deviations which take

place in performances. In this way, it provides deeper insight to the firm when they

need to take strategic move or change for improving performance. Beside this, by

taking into account current deviations manager of Dell can devise suitable plan for the

near future. Thus, by setting suitable benchmark firm can encourage personnel to

make their best efforts.

Disadvantages: Outcome of variance analysis sometimes place negative impact on

employee motivation and performance. Moreover, high deviation occurs when

manager sets unrealistic budget (Quattrone, 2016). It is one of the main aspects which

negatively influence the efficiency level of personnel.

Contribution (Sales – variable cost) 540000

Less Fixed cost

Fixed manufacturing expenses 500000

Fixed Administration and selling cost 600000

Loss -560000

P4 Explaining the advantages and disadvantages of different types of planning tools that are

used for budgetary control

Budgetary control is the technique which lays high level of emphasis on assessing

deviations by making comparison of actual performance with budgeted figures. Hence,

variance analysis is the most effectual techniques that can be undertaken for reducing the

level of expenses and setting suitable plan for upcoming time period. In accordance with such

aspect, manager of Dell can find out the deficiencies take place between the planned and

actual figures. Once deviations have assessed thereafter manager makes effort to identify and

evaluate the causes due to which deficiencies are occurred in performance (Otley, 2016). In

this way, identified causes of deviations enable firm to take strategic action for improvement.

By considering the above aspect it can be said that variance analysis technique helps in

enhancing the performance of each department within the suitable time frame. This technique

has following advantages and disadvantages:

Advantages: Variance analysis technique clearly indicates the deviations which take

place in performances. In this way, it provides deeper insight to the firm when they

need to take strategic move or change for improving performance. Beside this, by

taking into account current deviations manager of Dell can devise suitable plan for the

near future. Thus, by setting suitable benchmark firm can encourage personnel to

make their best efforts.

Disadvantages: Outcome of variance analysis sometimes place negative impact on

employee motivation and performance. Moreover, high deviation occurs when

manager sets unrealistic budget (Quattrone, 2016). It is one of the main aspects which

negatively influence the efficiency level of personnel.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

However, variance analysis technique offers suitable outcome only when evaluation

of current performance is made in against to highly realistic budget. Thus, preparation of

highly competent budgeting plan or framework is the prior requirement of variance analysis.

In this, by using below mentioned traditional and modern budgeting tools manager of Del can

prepare competent financial plan. Different types of budgeting technique which helps in

making proper forecast of income and expenses are enumerated below:

Traditional tools

Incremental budgeting technique: In this technique, manager of the business

organization makes some addition in the past framework. Thus, manager does not undertake

conceptual aspects to prepare suitable plan.

Advantages: Incremental budget can easily be prepared by the manager. Moreover,

past framework is considered by the manager to develop the new plan. In addition to

this, incremental budgeting technique saves times of the manager to a great extent

(Rubin, 2016). In this, by devoting time in framing competent policies manage can

contribute in the organizational growth and success.

Disadvantages: The main drawbacks of such budgeting technique that it avoids

current trend and changes. In this, finance personnel add some percentage in the

previous budgeting or financial plan.

Modern tools

Zero base budgeting: This budgeting technique is the reform over traditional tools. Under

zero base budgeting technique is the one which starts with 0 base and does not undertake past

year framework. In this, manager records each revenue and expense with proper justification

(Callaghan, Hawke and Mignerey, 2014). Hence, highly structured technique is employed by

the manager to prepare financial plan under zero base technique.

Advantages: Zero base technique is highly effectual which in turn helps in avoiding

redundant activities. Moreover, it places emphasis on emphasis on developing

relationship between cost and activities to the significant level (Lauth, 2014). Hence,

activity based budgeting technique assists is framing highly clear and precise plan

which in turn facilitates optimum use of financial resources.

Disadvantages: To prepare budget in accordance with zero base technique manager

requires highly competent personnel. Moreover, it is highly difficult for the manager

of current performance is made in against to highly realistic budget. Thus, preparation of

highly competent budgeting plan or framework is the prior requirement of variance analysis.

In this, by using below mentioned traditional and modern budgeting tools manager of Del can

prepare competent financial plan. Different types of budgeting technique which helps in

making proper forecast of income and expenses are enumerated below:

Traditional tools

Incremental budgeting technique: In this technique, manager of the business

organization makes some addition in the past framework. Thus, manager does not undertake

conceptual aspects to prepare suitable plan.

Advantages: Incremental budget can easily be prepared by the manager. Moreover,

past framework is considered by the manager to develop the new plan. In addition to

this, incremental budgeting technique saves times of the manager to a great extent

(Rubin, 2016). In this, by devoting time in framing competent policies manage can

contribute in the organizational growth and success.

Disadvantages: The main drawbacks of such budgeting technique that it avoids

current trend and changes. In this, finance personnel add some percentage in the

previous budgeting or financial plan.

Modern tools

Zero base budgeting: This budgeting technique is the reform over traditional tools. Under

zero base budgeting technique is the one which starts with 0 base and does not undertake past

year framework. In this, manager records each revenue and expense with proper justification

(Callaghan, Hawke and Mignerey, 2014). Hence, highly structured technique is employed by

the manager to prepare financial plan under zero base technique.

Advantages: Zero base technique is highly effectual which in turn helps in avoiding

redundant activities. Moreover, it places emphasis on emphasis on developing

relationship between cost and activities to the significant level (Lauth, 2014). Hence,

activity based budgeting technique assists is framing highly clear and precise plan

which in turn facilitates optimum use of financial resources.

Disadvantages: To prepare budget in accordance with zero base technique manager

requires highly competent personnel. Moreover, it is highly difficult for the manager

to justify each and every expense. Along with this, zero base budgeting technique is

highly time consuming process. The reason behind this, manager prepares new plan

by making in-depth assessment.

Activity based budgeting: In activity based budgeting technique, manager allocates fund

to each activity by identifying the relevant cost driver. In this way, activity based technique

facilitates optimum allocation of funds (Francis and et.al., 2015). By undertaking such

budgeting tool or technique manager can assess the consumption by each products or

services.

Advantages: ABB is the modern budgeting technique which helps in making suitable

allocation of overhead. Moreover, by using such technique manager of Dell can trace

overhead cost according to the cost object or process. Hence, in this cost is assigned

according to the level of resources used. The major benefits of using such method that

manager can easily assess whether specific product or service is making contribution

in the profitability aspect or not (Goddard and Simm, 2017). Thus, by making

evaluation of all such aspect manager can frame highly competent and strategic

framework.

Disadvantages: It is highly difficult for the manager to identify relevant cost driver.

ABB costing technique is highly difficult to understand so business unit is required to

conduct effectual training session (Simons, 2013). Moreover, without having proper

knowledge about such technique manager is not in position to make suitable

budgeting plan.

Hence, it is suggested to Dell to employ zero and activity based budgeting technique. By

following such planning tool business unit can prepare highly realistic and competent plan.

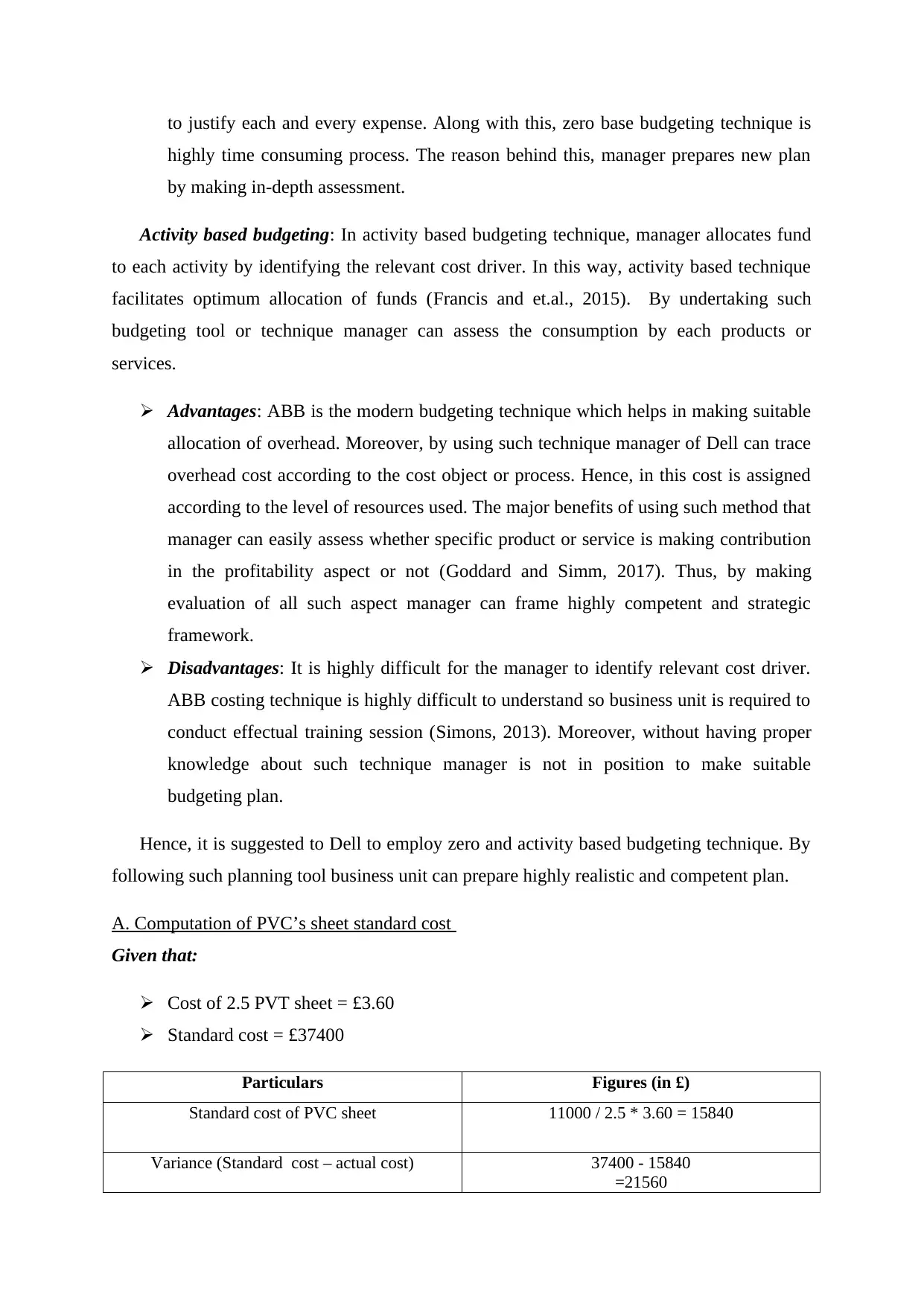

A. Computation of PVC’s sheet standard cost

Given that:

Cost of 2.5 PVT sheet = £3.60

Standard cost = £37400

Particulars Figures (in £)

Standard cost of PVC sheet 11000 / 2.5 * 3.60 = 15840

Variance (Standard cost – actual cost) 37400 - 15840

=21560

highly time consuming process. The reason behind this, manager prepares new plan

by making in-depth assessment.

Activity based budgeting: In activity based budgeting technique, manager allocates fund

to each activity by identifying the relevant cost driver. In this way, activity based technique

facilitates optimum allocation of funds (Francis and et.al., 2015). By undertaking such

budgeting tool or technique manager can assess the consumption by each products or

services.

Advantages: ABB is the modern budgeting technique which helps in making suitable

allocation of overhead. Moreover, by using such technique manager of Dell can trace

overhead cost according to the cost object or process. Hence, in this cost is assigned

according to the level of resources used. The major benefits of using such method that

manager can easily assess whether specific product or service is making contribution

in the profitability aspect or not (Goddard and Simm, 2017). Thus, by making

evaluation of all such aspect manager can frame highly competent and strategic

framework.

Disadvantages: It is highly difficult for the manager to identify relevant cost driver.

ABB costing technique is highly difficult to understand so business unit is required to

conduct effectual training session (Simons, 2013). Moreover, without having proper

knowledge about such technique manager is not in position to make suitable

budgeting plan.

Hence, it is suggested to Dell to employ zero and activity based budgeting technique. By

following such planning tool business unit can prepare highly realistic and competent plan.

A. Computation of PVC’s sheet standard cost

Given that:

Cost of 2.5 PVT sheet = £3.60

Standard cost = £37400

Particulars Figures (in £)

Standard cost of PVC sheet 11000 / 2.5 * 3.60 = 15840

Variance (Standard cost – actual cost) 37400 - 15840

=21560

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

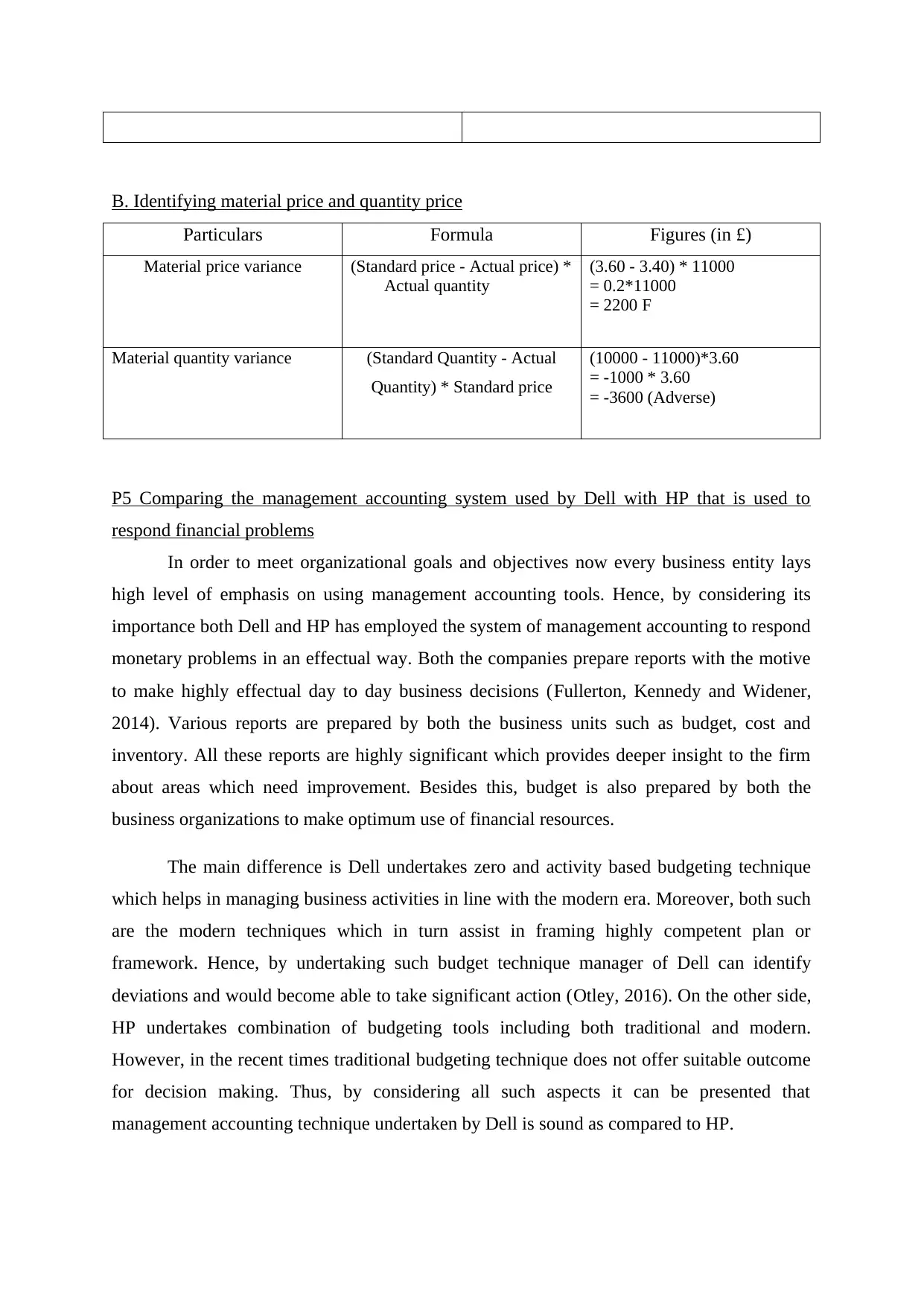

B. Identifying material price and quantity price

Particulars Formula Figures (in £)

Material price variance (Standard price - Actual price) *

Actual quantity

(3.60 - 3.40) * 11000

= 0.2*11000

= 2200 F

Material quantity variance (Standard Quantity - Actual

Quantity) * Standard price

(10000 - 11000)*3.60

= -1000 * 3.60

= -3600 (Adverse)

P5 Comparing the management accounting system used by Dell with HP that is used to

respond financial problems

In order to meet organizational goals and objectives now every business entity lays

high level of emphasis on using management accounting tools. Hence, by considering its

importance both Dell and HP has employed the system of management accounting to respond

monetary problems in an effectual way. Both the companies prepare reports with the motive

to make highly effectual day to day business decisions (Fullerton, Kennedy and Widener,

2014). Various reports are prepared by both the business units such as budget, cost and

inventory. All these reports are highly significant which provides deeper insight to the firm

about areas which need improvement. Besides this, budget is also prepared by both the

business organizations to make optimum use of financial resources.

The main difference is Dell undertakes zero and activity based budgeting technique

which helps in managing business activities in line with the modern era. Moreover, both such

are the modern techniques which in turn assist in framing highly competent plan or

framework. Hence, by undertaking such budget technique manager of Dell can identify

deviations and would become able to take significant action (Otley, 2016). On the other side,

HP undertakes combination of budgeting tools including both traditional and modern.

However, in the recent times traditional budgeting technique does not offer suitable outcome

for decision making. Thus, by considering all such aspects it can be presented that

management accounting technique undertaken by Dell is sound as compared to HP.

Particulars Formula Figures (in £)

Material price variance (Standard price - Actual price) *

Actual quantity

(3.60 - 3.40) * 11000

= 0.2*11000

= 2200 F

Material quantity variance (Standard Quantity - Actual

Quantity) * Standard price

(10000 - 11000)*3.60

= -1000 * 3.60

= -3600 (Adverse)

P5 Comparing the management accounting system used by Dell with HP that is used to

respond financial problems

In order to meet organizational goals and objectives now every business entity lays

high level of emphasis on using management accounting tools. Hence, by considering its

importance both Dell and HP has employed the system of management accounting to respond

monetary problems in an effectual way. Both the companies prepare reports with the motive

to make highly effectual day to day business decisions (Fullerton, Kennedy and Widener,

2014). Various reports are prepared by both the business units such as budget, cost and

inventory. All these reports are highly significant which provides deeper insight to the firm

about areas which need improvement. Besides this, budget is also prepared by both the

business organizations to make optimum use of financial resources.

The main difference is Dell undertakes zero and activity based budgeting technique

which helps in managing business activities in line with the modern era. Moreover, both such

are the modern techniques which in turn assist in framing highly competent plan or

framework. Hence, by undertaking such budget technique manager of Dell can identify

deviations and would become able to take significant action (Otley, 2016). On the other side,

HP undertakes combination of budgeting tools including both traditional and modern.

However, in the recent times traditional budgeting technique does not offer suitable outcome

for decision making. Thus, by considering all such aspects it can be presented that

management accounting technique undertaken by Dell is sound as compared to HP.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report, it has been concluded that by using management accounting

systems Dell can ensure effective management of resources. Besides this, it can be inferred

that by managerial reporting system provides valuable framework to the business unit for

decision making. It can be revealed from the report that reports which are prepared by the

department of management accountant provide assistance to the firm in taking strategic

action for improvement. Further, it has been articulated that zero base budgeting technique is

highly effective which in turn helps company in making forecast and preparation of suitable

budgeting framework. It can be stated that Dell should employ the technique of absorption

costing. By doing this, firm can get suitable view of cost per unit and profit margin. It can be

seen in the report that financial tools and techniques undertaken by Dell is highly effective as

compared to the rival firm.

From the above report, it has been concluded that by using management accounting

systems Dell can ensure effective management of resources. Besides this, it can be inferred

that by managerial reporting system provides valuable framework to the business unit for

decision making. It can be revealed from the report that reports which are prepared by the

department of management accountant provide assistance to the firm in taking strategic

action for improvement. Further, it has been articulated that zero base budgeting technique is

highly effective which in turn helps company in making forecast and preparation of suitable

budgeting framework. It can be stated that Dell should employ the technique of absorption

costing. By doing this, firm can get suitable view of cost per unit and profit margin. It can be

seen in the report that financial tools and techniques undertaken by Dell is highly effective as

compared to the rival firm.

REFERENCES

Books and Journals

Bogsnes, B., 2016. Implementing beyond budgeting: unlocking the performance potential.

John Wiley & Sons.

Callaghan, S., Hawke, K. and Mignerey, C., 2014. Five myths (and realities) about zero-

based budgeting. McKinsey & Company. p.2.

Francis, B. and et.al., 2015. Gender differences in financial reporting decision making:

Evidence from accounting conservatism. Contemporary Accounting Research. 32(3).

pp.1285-1318.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting practices.

Journal of Operations Management. 32(7). pp.414-428.

Goddard, A. and Simm, A., 2017. Management accounting, performance measurement and

strategy in English local authorities. Public Money & Management. 37(4). pp.261-268.

Hernandez, L., Jonker, N. and Kosse, A., 2017. Cash versus debit card: the role of budget

control. Journal of Consumer Affairs. 51(1). pp. 91-112.

Lauth, T. P., 2014. Zero‐Base Budgeting Redux in Georgia: Efficiency or Ideology?. Public

Budgeting & Finance. 34(1). pp.1-17.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research. 31. pp.45-62.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31(9). pp.118-122.

Rubin, I. S., 2016. The politics of public budgeting: Getting and spending, borrowing and

balancing. CQ Press.

Simons, R., 2013. Performance Measurement and Control Systems for Implementing

Strategy Text and Cases: Pearson New International Edition. Pearson Higher Ed.

Books and Journals

Bogsnes, B., 2016. Implementing beyond budgeting: unlocking the performance potential.

John Wiley & Sons.

Callaghan, S., Hawke, K. and Mignerey, C., 2014. Five myths (and realities) about zero-

based budgeting. McKinsey & Company. p.2.

Francis, B. and et.al., 2015. Gender differences in financial reporting decision making:

Evidence from accounting conservatism. Contemporary Accounting Research. 32(3).

pp.1285-1318.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting practices.

Journal of Operations Management. 32(7). pp.414-428.

Goddard, A. and Simm, A., 2017. Management accounting, performance measurement and

strategy in English local authorities. Public Money & Management. 37(4). pp.261-268.

Hernandez, L., Jonker, N. and Kosse, A., 2017. Cash versus debit card: the role of budget

control. Journal of Consumer Affairs. 51(1). pp. 91-112.

Lauth, T. P., 2014. Zero‐Base Budgeting Redux in Georgia: Efficiency or Ideology?. Public

Budgeting & Finance. 34(1). pp.1-17.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research. 31. pp.45-62.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31(9). pp.118-122.

Rubin, I. S., 2016. The politics of public budgeting: Getting and spending, borrowing and

balancing. CQ Press.

Simons, R., 2013. Performance Measurement and Control Systems for Implementing

Strategy Text and Cases: Pearson New International Edition. Pearson Higher Ed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.