Management Accounting Report: Dell Company Financial Analysis

VerifiedAdded on 2020/02/05

|15

|3868

|390

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to Dell. It begins with an introduction to management accounting and its significance, followed by an examination of different management accounting systems, including traditional cost accounting, lean accounting, throughput accounting, and transfer pricing. The report then delves into various management accounting reporting methods such as job cost reporting, sales reports, cost accounting, and budgetary reports. Furthermore, it includes a detailed calculation and comparison of costs using absorption and marginal costing techniques, highlighting the differences and implications of each method. The report also explores the advantages and drawbacks of budgetary planning techniques. Finally, it assesses the effectiveness of the management accounting system in resolving financial problems, providing a well-rounded overview of the subject matter.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

management Accounting.................................................................................................................1

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

P1 Management accounting and requirement of different management accounting system......3

P2 Different methods used for management accounting reporting.............................................5

Task 2...............................................................................................................................................6

P3 Calculating the costs under absorption & marginal costs and examining the difference.......6

Task 3...............................................................................................................................................8

P4 Explaining advantages & drawbacks of the budgetary planning techniques.........................8

A. Computation of standards cost of PVC sheets........................................................................9

B. Calculation of material price and quantity variance.............................................................10

Task 4.............................................................................................................................................11

P5 Effectiveness of management accounting system in resolving financial problems.............11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

2

management Accounting.................................................................................................................1

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

P1 Management accounting and requirement of different management accounting system......3

P2 Different methods used for management accounting reporting.............................................5

Task 2...............................................................................................................................................6

P3 Calculating the costs under absorption & marginal costs and examining the difference.......6

Task 3...............................................................................................................................................8

P4 Explaining advantages & drawbacks of the budgetary planning techniques.........................8

A. Computation of standards cost of PVC sheets........................................................................9

B. Calculation of material price and quantity variance.............................................................10

Task 4.............................................................................................................................................11

P5 Effectiveness of management accounting system in resolving financial problems.............11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

2

INTRODUCTION

Management accounting is the technique that is used by the companies in order to record

their financial data so that management can develop strategies for the growth of the entities.

Therefore it plays significant role in the companies and helps the firms in making sound business

decisions (Scapens and Bromwich 2010). For the present report Dell Company is being taken

into account. Assignment will discuss the requirement of different types of management

accounting system in an organization. Several methods which are required by the entity to

accounting reporting will be explained in this study. Absorption cost and marginal cost will be

calculated in this report in order to prepare income statement (Yalcin, 2012). Advantage and

disadvantage of different types of planning tools will be described in this study and material

price and quantity variance will be computed.

TASK 1

P1 Management accounting and requirement of different management accounting system

Management accounting can be considered as process that helps in preparing the

accounting reports and used economic information’s in such manner so that entity can

make sound decisions which can help in the growth of the organization to great extent

(Tucker and Parker, 2014). This is tool through which managers of the company can carry

out business operations well and can contribute in accomplishing the short term goal of the

organization. The main objective of Dell of using management accounting is to identify the

risk and allocate resources well so that issues related to shortage of funds and others can be

minimized soon. Management accountant of Dell company gather information time to time

so that they can monitor current operations and can measure the effectiveness of the

existing process (Ambe,2016).

Type of management accounting system and its essential for the Dell Company

There are several types of management accounting system used by the entity (Clark,

Menifield and Stewart, 2017). These are described as below:

Traditional cost accounting: It is traditionally used method in which managers allocate cost to

the production so that goods can be manufactured. It includes costing of process, job order

and batch costing. Direct and indirect cost expenditures are included in the production

3

Management accounting is the technique that is used by the companies in order to record

their financial data so that management can develop strategies for the growth of the entities.

Therefore it plays significant role in the companies and helps the firms in making sound business

decisions (Scapens and Bromwich 2010). For the present report Dell Company is being taken

into account. Assignment will discuss the requirement of different types of management

accounting system in an organization. Several methods which are required by the entity to

accounting reporting will be explained in this study. Absorption cost and marginal cost will be

calculated in this report in order to prepare income statement (Yalcin, 2012). Advantage and

disadvantage of different types of planning tools will be described in this study and material

price and quantity variance will be computed.

TASK 1

P1 Management accounting and requirement of different management accounting system

Management accounting can be considered as process that helps in preparing the

accounting reports and used economic information’s in such manner so that entity can

make sound decisions which can help in the growth of the organization to great extent

(Tucker and Parker, 2014). This is tool through which managers of the company can carry

out business operations well and can contribute in accomplishing the short term goal of the

organization. The main objective of Dell of using management accounting is to identify the

risk and allocate resources well so that issues related to shortage of funds and others can be

minimized soon. Management accountant of Dell company gather information time to time

so that they can monitor current operations and can measure the effectiveness of the

existing process (Ambe,2016).

Type of management accounting system and its essential for the Dell Company

There are several types of management accounting system used by the entity (Clark,

Menifield and Stewart, 2017). These are described as below:

Traditional cost accounting: It is traditionally used method in which managers allocate cost to

the production so that goods can be manufactured. It includes costing of process, job order

and batch costing. Direct and indirect cost expenditures are included in the production

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

process so both these expenditures are considered in this cost accounting process (Hülle,

Kaspar and Möller, 2011).

Lean accounting: It is another type of management accounting tool which can be beneficial for

the Dell Company. It is the method through which cited firm make effective control over

its cost and can remove wastage from the system significantly. It is used by most of the

entities in order to gather relevant information so that they can make sound decisions for

the growth of the firms (Ball, Grubnic and Birchall, 2014 ). Lean accounting is the type

of method which is used by manufacturing firms mostly because by this way they try to

eliminate the wastage and increase efficiency level of the production. By this way

companies like Dell can understand its overall financial worthiness. If cited firm uses this

tool then it can be safe from future uncertainties and can enhance its profitability to great

exten (Clark, Menifield and Stewart, 2017)t.

Throughput accounting system: It is completely differed from the traditional management

accounting system. It concentrates more on the constrains which are exist under the

production system due to this its performance is not good. With the help of this system

Dell can minimize the issues related to material or labor and can improve production

capacity (Banerjee and Das, 2017). Throughput accounting system is the method which

focuses more on minimizing the per unit cost of produced goods so that overall profit of

the organization can get improved. Its main focus in on sales so management of Dell uses

this system and concentrates more on producing quality products so that sales volume of

the cited firm can get improved (Clark, Menifield and Stewart, 2017).

Transfer pricing accounting system: If entities are engaged in the import and export business

then it is necessary for them to follow legal guidance and they have to pay tax

accordingly (Bhimani and et.al, 2013). For example if Dell is US bases firm and it

imports some equipments from France then it will have to follow this management

accounting system and have to pay tax as per the norms of particular nation. It is applied

when business is run between two different countries (Clark, Menifield and Stewart,

2017).

4

Kaspar and Möller, 2011).

Lean accounting: It is another type of management accounting tool which can be beneficial for

the Dell Company. It is the method through which cited firm make effective control over

its cost and can remove wastage from the system significantly. It is used by most of the

entities in order to gather relevant information so that they can make sound decisions for

the growth of the firms (Ball, Grubnic and Birchall, 2014 ). Lean accounting is the type

of method which is used by manufacturing firms mostly because by this way they try to

eliminate the wastage and increase efficiency level of the production. By this way

companies like Dell can understand its overall financial worthiness. If cited firm uses this

tool then it can be safe from future uncertainties and can enhance its profitability to great

exten (Clark, Menifield and Stewart, 2017)t.

Throughput accounting system: It is completely differed from the traditional management

accounting system. It concentrates more on the constrains which are exist under the

production system due to this its performance is not good. With the help of this system

Dell can minimize the issues related to material or labor and can improve production

capacity (Banerjee and Das, 2017). Throughput accounting system is the method which

focuses more on minimizing the per unit cost of produced goods so that overall profit of

the organization can get improved. Its main focus in on sales so management of Dell uses

this system and concentrates more on producing quality products so that sales volume of

the cited firm can get improved (Clark, Menifield and Stewart, 2017).

Transfer pricing accounting system: If entities are engaged in the import and export business

then it is necessary for them to follow legal guidance and they have to pay tax

accordingly (Bhimani and et.al, 2013). For example if Dell is US bases firm and it

imports some equipments from France then it will have to follow this management

accounting system and have to pay tax as per the norms of particular nation. It is applied

when business is run between two different countries (Clark, Menifield and Stewart,

2017).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Different methods used for management accounting reporting

Dell being a manufacturing firm has to follow the guidelines of the international

accounting norms and Dell can adopt any method for the growth of the cited firm

(Gullifer and Payne, 2015). Several methods are described as below:

Job cost reporting

It is considered as one of the important tool that helps in maintaining the organizational

job costing related details. In this section many information can be used such as period

sensitive accounts balance data, reviewing job information etc (Romano, 2015). It is

divided into subsections and information related to labor etc. is being used by the

management. By this way cited firm can generate good information for the well fare of

the entity. By this way Dell can compare the estimated cost with the actual. It is

beneficial tool that supports in tracking the cost and evaluating the job well (Clark,

Menifield and Stewart, 2017).

Sales reports

It is another method for management accounting reporting in which managers of Dell can

record sales information in specific time duration. It gives detail about the per item sales

volume so that company can estimate the profitable products and can reduce wastage.

Sales reports are evaluated by the higher authorities so that they can know about cost

attached with it and can minimize unnecessary expenditures soon (Hülle, Kaspar and

Möller, 2011). If there is big gap between estimated sales figures and capture volume

then company can take measures to enhance the sale performance. It will help in reducing

gap between estimated profit and actual revenue. After analyzing the sales report

managers of cited firm can identify threats and opportunities to the business. By this way

sales volume can be increased to great extent. This record shows that if sales is declining

continuously that shows Dell in not able to provide products as per the needs of clients,

so it is required to improve quality of the items (Romano, 2015). Declining sales shows

that firm are require to sell the existing products and it is required to modify it as per the

needs of consumers. By this way Dell will be able to achieve its sales goal and will be

able to sustain in the corporate market for longer duration. This management accounting

reports can give high profit to the firm in near future (Ball, Grubnic and Birchall, 2014 ).

5

Dell being a manufacturing firm has to follow the guidelines of the international

accounting norms and Dell can adopt any method for the growth of the cited firm

(Gullifer and Payne, 2015). Several methods are described as below:

Job cost reporting

It is considered as one of the important tool that helps in maintaining the organizational

job costing related details. In this section many information can be used such as period

sensitive accounts balance data, reviewing job information etc (Romano, 2015). It is

divided into subsections and information related to labor etc. is being used by the

management. By this way cited firm can generate good information for the well fare of

the entity. By this way Dell can compare the estimated cost with the actual. It is

beneficial tool that supports in tracking the cost and evaluating the job well (Clark,

Menifield and Stewart, 2017).

Sales reports

It is another method for management accounting reporting in which managers of Dell can

record sales information in specific time duration. It gives detail about the per item sales

volume so that company can estimate the profitable products and can reduce wastage.

Sales reports are evaluated by the higher authorities so that they can know about cost

attached with it and can minimize unnecessary expenditures soon (Hülle, Kaspar and

Möller, 2011). If there is big gap between estimated sales figures and capture volume

then company can take measures to enhance the sale performance. It will help in reducing

gap between estimated profit and actual revenue. After analyzing the sales report

managers of cited firm can identify threats and opportunities to the business. By this way

sales volume can be increased to great extent. This record shows that if sales is declining

continuously that shows Dell in not able to provide products as per the needs of clients,

so it is required to improve quality of the items (Romano, 2015). Declining sales shows

that firm are require to sell the existing products and it is required to modify it as per the

needs of consumers. By this way Dell will be able to achieve its sales goal and will be

able to sustain in the corporate market for longer duration. This management accounting

reports can give high profit to the firm in near future (Ball, Grubnic and Birchall, 2014 ).

5

Cost accounting

It is the type of management accounting system in which firms collect, record information,

summarizes them in such manner so that it can make effective control over its cost. It is

beneficial tool that can support in capturing the production cost of the entity, fixed and

variable expenses. That can be advantage for the Dell because by this way cited firm will

be able to make comparison between input cost and output (Scapens and Bromwich 2010).

For example RL Maynard is using the cost accounting system , that helps in determining

the unit cost. By this way organization measures overall growth of the corporation.

Budgetary report

It is the type of the reporting tool in which performance of actual and estimated budget is

compared by the management. Dell uses this method in order to compare its budget

performance and show these details in its income statements (Romano, 2015). Variance

can be analyzed through this system and cited firm can make strategies in order to get

favorable results. It is beneficial tool that indicates the firms how much amount is

required to invest for further development (Clark, Menifield and Stewart, 2017).

TASK 2

P3 Calculating the costs under absorption & marginal costs and examining the difference

Absorption costing is a marginal costing technique which apportion all the fluctuating

and fixed variable production overheads to the goods(Surbhi, 2015).

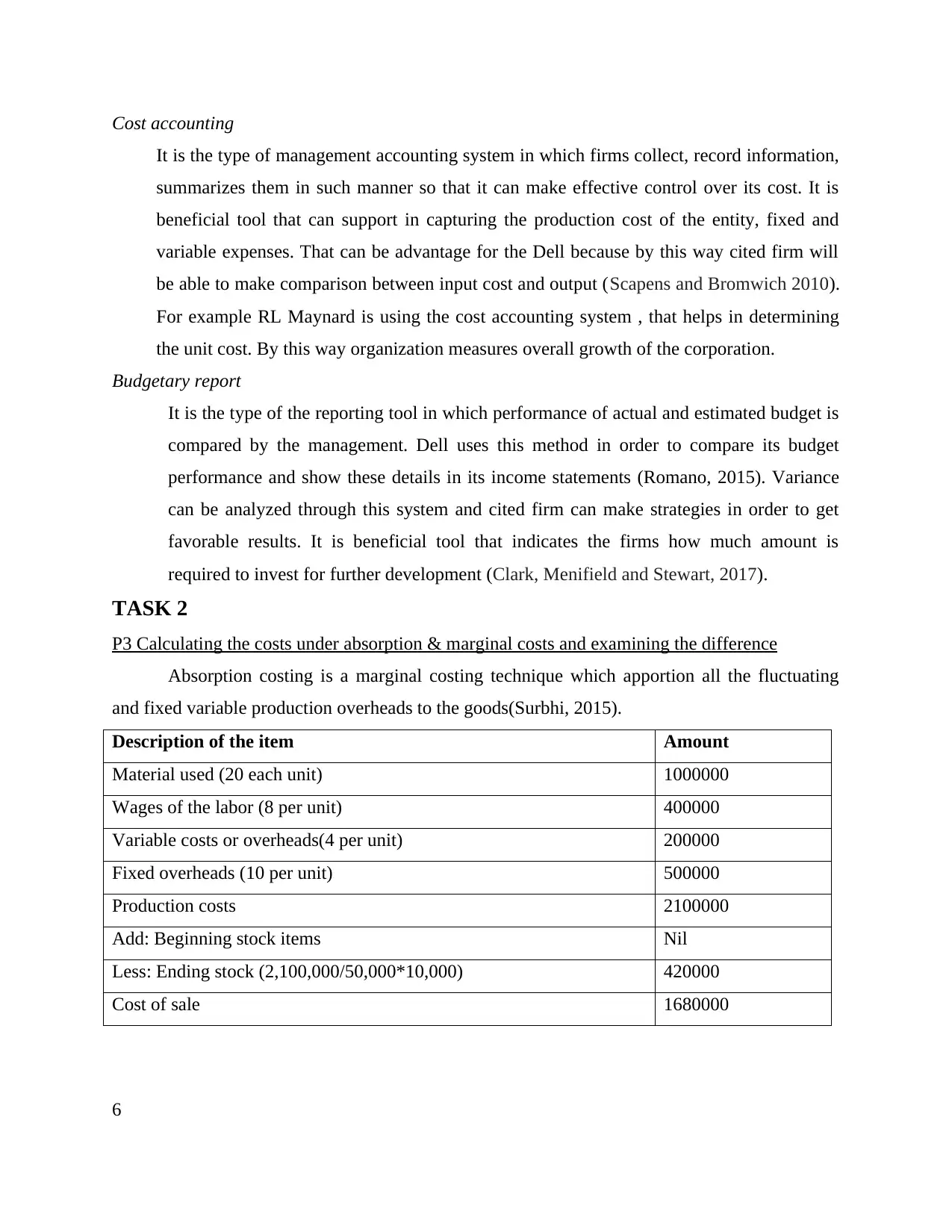

Description of the item Amount

Material used (20 each unit) 1000000

Wages of the labor (8 per unit) 400000

Variable costs or overheads(4 per unit) 200000

Fixed overheads (10 per unit) 500000

Production costs 2100000

Add: Beginning stock items Nil

Less: Ending stock (2,100,000/50,000*10,000) 420000

Cost of sale 1680000

6

It is the type of management accounting system in which firms collect, record information,

summarizes them in such manner so that it can make effective control over its cost. It is

beneficial tool that can support in capturing the production cost of the entity, fixed and

variable expenses. That can be advantage for the Dell because by this way cited firm will

be able to make comparison between input cost and output (Scapens and Bromwich 2010).

For example RL Maynard is using the cost accounting system , that helps in determining

the unit cost. By this way organization measures overall growth of the corporation.

Budgetary report

It is the type of the reporting tool in which performance of actual and estimated budget is

compared by the management. Dell uses this method in order to compare its budget

performance and show these details in its income statements (Romano, 2015). Variance

can be analyzed through this system and cited firm can make strategies in order to get

favorable results. It is beneficial tool that indicates the firms how much amount is

required to invest for further development (Clark, Menifield and Stewart, 2017).

TASK 2

P3 Calculating the costs under absorption & marginal costs and examining the difference

Absorption costing is a marginal costing technique which apportion all the fluctuating

and fixed variable production overheads to the goods(Surbhi, 2015).

Description of the item Amount

Material used (20 each unit) 1000000

Wages of the labor (8 per unit) 400000

Variable costs or overheads(4 per unit) 200000

Fixed overheads (10 per unit) 500000

Production costs 2100000

Add: Beginning stock items Nil

Less: Ending stock (2,100,000/50,000*10,000) 420000

Cost of sale 1680000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

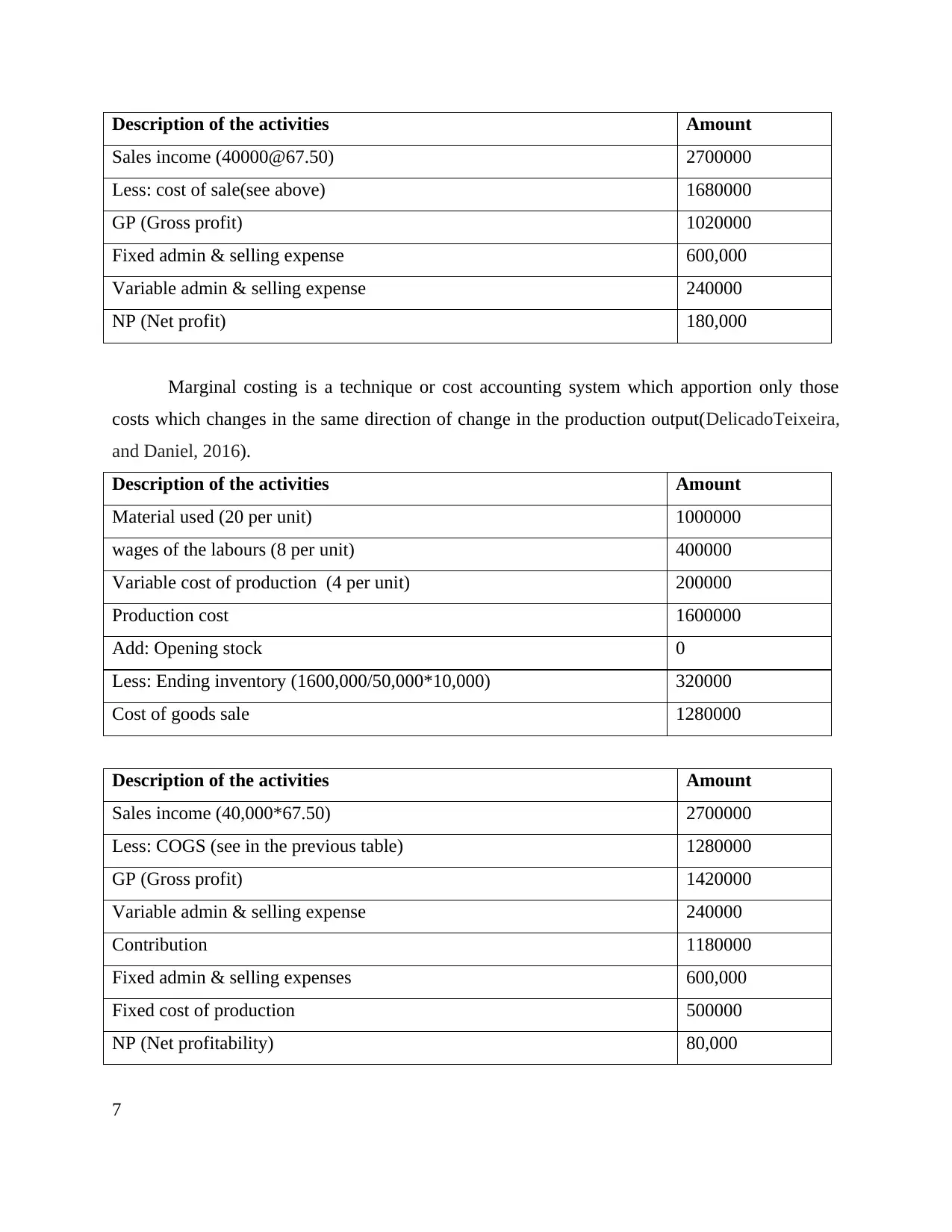

Description of the activities Amount

Sales income (40000@67.50) 2700000

Less: cost of sale(see above) 1680000

GP (Gross profit) 1020000

Fixed admin & selling expense 600,000

Variable admin & selling expense 240000

NP (Net profit) 180,000

Marginal costing is a technique or cost accounting system which apportion only those

costs which changes in the same direction of change in the production output(DelicadoTeixeira,

and Daniel, 2016).

Description of the activities Amount

Material used (20 per unit) 1000000

wages of the labours (8 per unit) 400000

Variable cost of production (4 per unit) 200000

Production cost 1600000

Add: Opening stock 0

Less: Ending inventory (1600,000/50,000*10,000) 320000

Cost of goods sale 1280000

Description of the activities Amount

Sales income (40,000*67.50) 2700000

Less: COGS (see in the previous table) 1280000

GP (Gross profit) 1420000

Variable admin & selling expense 240000

Contribution 1180000

Fixed admin & selling expenses 600,000

Fixed cost of production 500000

NP (Net profitability) 80,000

7

Sales income (40000@67.50) 2700000

Less: cost of sale(see above) 1680000

GP (Gross profit) 1020000

Fixed admin & selling expense 600,000

Variable admin & selling expense 240000

NP (Net profit) 180,000

Marginal costing is a technique or cost accounting system which apportion only those

costs which changes in the same direction of change in the production output(DelicadoTeixeira,

and Daniel, 2016).

Description of the activities Amount

Material used (20 per unit) 1000000

wages of the labours (8 per unit) 400000

Variable cost of production (4 per unit) 200000

Production cost 1600000

Add: Opening stock 0

Less: Ending inventory (1600,000/50,000*10,000) 320000

Cost of goods sale 1280000

Description of the activities Amount

Sales income (40,000*67.50) 2700000

Less: COGS (see in the previous table) 1280000

GP (Gross profit) 1420000

Variable admin & selling expense 240000

Contribution 1180000

Fixed admin & selling expenses 600,000

Fixed cost of production 500000

NP (Net profitability) 80,000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Findings and analysis: Under marginal cost, unit cost is 32 whereas in full costing

method, it is 42. The difference caused because absorption costing method apportioned fixed

costs of 10 per unit also to the cost measurement. Due to these differences in the cost treatment,

cost of production & COGS also quantified differences, as in full costing, these are measured at

2,100,000 and 1,680,000 whilst under variable costing, the data has been reported less to

1,600,000 & 1,280,000 respectively, as a result, gross profit under full & variable costing

reported different results to 1,020,000 & 1,420,000 (Clark, Menifield and Stewart, 2017).

Besides this, marginal costing method measured a contribution of 1,180,000 GBP. Further, in

order to find out the net profit, marginal costing method subtracts all the fixed expenses whereas

absorption costing method subtracts other expenses either fixed or variable which are not the part

of operations. Due to this reason, both method computed net profit differently at 180,000 &

80,000.

TASK 3

P4 Explaining advantages & drawbacks of the budgetary planning techniques

Budgeting can be defined as a process wherein managers express their plan into monetary

terms which aims at fulfilling long-term goals of the enterprise (Clark, Menifield and Stewart,

2017). It is a plan which is designed for the desired future outcome and finding out the effective

ways of bringing success. It is a plan that express the possible results or outcome of the future

activities and functions and helps in coordinating the business functionality of all the divisions.

Dell Corporation’s managers construct budget to aid in business planning, performance

evaluation, coordination, motivation and implement control over the organizational functions.

Budgeting methods:

Incremental budgeting: It is the oldest technique that Dell’s managerial team can use as

a traditional budgeting. Under this method, budget is created in five stages, first defining the

broad activities, finding out their essential & lastly, quantifying their prospective outcome. This

method does not question the past year’s budget and targeted at managing sufficient cash so as to

sustain it at previous level and adding more expense for the new items (Clark, Menifield and

Stewart, 2017).

Advantage:

It is easy to understand and facilitates inexperienced managers to operate it.

8

method, it is 42. The difference caused because absorption costing method apportioned fixed

costs of 10 per unit also to the cost measurement. Due to these differences in the cost treatment,

cost of production & COGS also quantified differences, as in full costing, these are measured at

2,100,000 and 1,680,000 whilst under variable costing, the data has been reported less to

1,600,000 & 1,280,000 respectively, as a result, gross profit under full & variable costing

reported different results to 1,020,000 & 1,420,000 (Clark, Menifield and Stewart, 2017).

Besides this, marginal costing method measured a contribution of 1,180,000 GBP. Further, in

order to find out the net profit, marginal costing method subtracts all the fixed expenses whereas

absorption costing method subtracts other expenses either fixed or variable which are not the part

of operations. Due to this reason, both method computed net profit differently at 180,000 &

80,000.

TASK 3

P4 Explaining advantages & drawbacks of the budgetary planning techniques

Budgeting can be defined as a process wherein managers express their plan into monetary

terms which aims at fulfilling long-term goals of the enterprise (Clark, Menifield and Stewart,

2017). It is a plan which is designed for the desired future outcome and finding out the effective

ways of bringing success. It is a plan that express the possible results or outcome of the future

activities and functions and helps in coordinating the business functionality of all the divisions.

Dell Corporation’s managers construct budget to aid in business planning, performance

evaluation, coordination, motivation and implement control over the organizational functions.

Budgeting methods:

Incremental budgeting: It is the oldest technique that Dell’s managerial team can use as

a traditional budgeting. Under this method, budget is created in five stages, first defining the

broad activities, finding out their essential & lastly, quantifying their prospective outcome. This

method does not question the past year’s budget and targeted at managing sufficient cash so as to

sustain it at previous level and adding more expense for the new items (Clark, Menifield and

Stewart, 2017).

Advantage:

It is easy to understand and facilitates inexperienced managers to operate it.

8

It helps in making the statistical comparison over the period easily, because, past year’s

budgeted items are still not questioned in the current year.

Drawbacks:

It uses last year budget and does not question the existing period’s budget validity.

Being a budgetee, Dell is not required to justify the elements and only the new items that

has been added into PY’s budget must be justified (de Campos and Rodrigues, 2016).

It ignores the total production volume or activity and also does not considers the input-

output relationship.

Zero-based budgeting:

In case where company’s costs is excessively discretionary then in such situation, zero

based budgeting is founded really suitable. This technique requires for the departmental

managers to carry out an investigation to analyse the external market environment and thereby

make the projection about possible future course of activities (Sehgal, 2017).

Advantages:

It is really a better way & suitable approach of allocating resources. It is because, the

method question each and every item of the budget & aims at eliminating unnecessary

operations that will contribute to success.

It provides a base to the management for achieving measurements, which in turn, leads to

staff involvement (Kaplan and Anderson, 2013).

Drawbacks:

It needs excessive paperwork & too-much time consuming.

Every item of the budget needs to be justified with the enough amount of evidences.

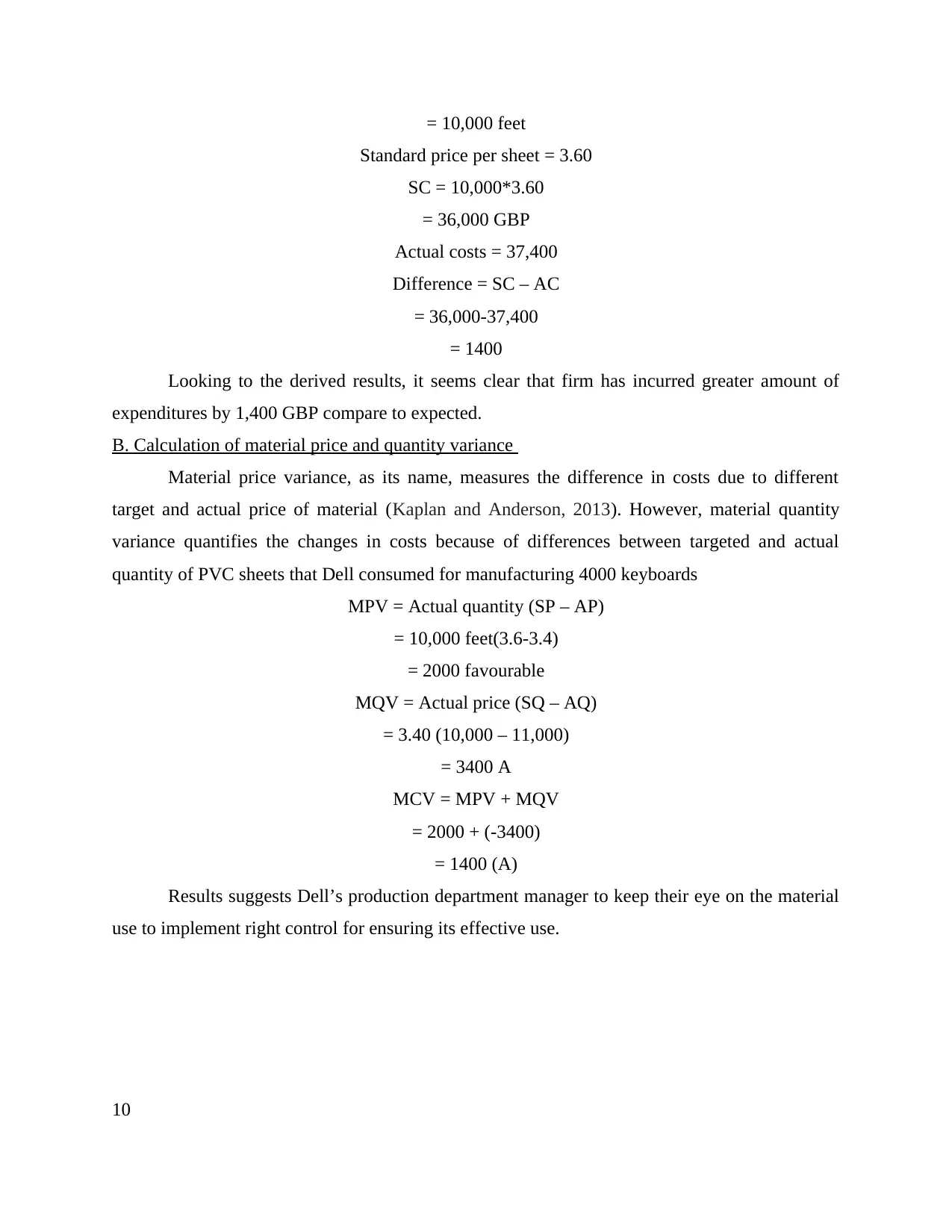

A. Computation of standards cost of PVC sheets

Standard costing is the practice that is applied in the establishment to substitute an

expected or possible cost for the actual expenditures & also record the variances or deviations

showing the differences in actual & targeted results.

Standard costs of PVC sheets for manufacturing 4000 keyboards

= Standard quantity * standard price per sheet

Standard quantity = quantity per unit * 4000 key boards

= 2.5 feet * 4,000

9

budgeted items are still not questioned in the current year.

Drawbacks:

It uses last year budget and does not question the existing period’s budget validity.

Being a budgetee, Dell is not required to justify the elements and only the new items that

has been added into PY’s budget must be justified (de Campos and Rodrigues, 2016).

It ignores the total production volume or activity and also does not considers the input-

output relationship.

Zero-based budgeting:

In case where company’s costs is excessively discretionary then in such situation, zero

based budgeting is founded really suitable. This technique requires for the departmental

managers to carry out an investigation to analyse the external market environment and thereby

make the projection about possible future course of activities (Sehgal, 2017).

Advantages:

It is really a better way & suitable approach of allocating resources. It is because, the

method question each and every item of the budget & aims at eliminating unnecessary

operations that will contribute to success.

It provides a base to the management for achieving measurements, which in turn, leads to

staff involvement (Kaplan and Anderson, 2013).

Drawbacks:

It needs excessive paperwork & too-much time consuming.

Every item of the budget needs to be justified with the enough amount of evidences.

A. Computation of standards cost of PVC sheets

Standard costing is the practice that is applied in the establishment to substitute an

expected or possible cost for the actual expenditures & also record the variances or deviations

showing the differences in actual & targeted results.

Standard costs of PVC sheets for manufacturing 4000 keyboards

= Standard quantity * standard price per sheet

Standard quantity = quantity per unit * 4000 key boards

= 2.5 feet * 4,000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 10,000 feet

Standard price per sheet = 3.60

SC = 10,000*3.60

= 36,000 GBP

Actual costs = 37,400

Difference = SC – AC

= 36,000-37,400

= 1400

Looking to the derived results, it seems clear that firm has incurred greater amount of

expenditures by 1,400 GBP compare to expected.

B. Calculation of material price and quantity variance

Material price variance, as its name, measures the difference in costs due to different

target and actual price of material (Kaplan and Anderson, 2013). However, material quantity

variance quantifies the changes in costs because of differences between targeted and actual

quantity of PVC sheets that Dell consumed for manufacturing 4000 keyboards

MPV = Actual quantity (SP – AP)

= 10,000 feet(3.6-3.4)

= 2000 favourable

MQV = Actual price (SQ – AQ)

= 3.40 (10,000 – 11,000)

= 3400 A

MCV = MPV + MQV

= 2000 + (-3400)

= 1400 (A)

Results suggests Dell’s production department manager to keep their eye on the material

use to implement right control for ensuring its effective use.

10

Standard price per sheet = 3.60

SC = 10,000*3.60

= 36,000 GBP

Actual costs = 37,400

Difference = SC – AC

= 36,000-37,400

= 1400

Looking to the derived results, it seems clear that firm has incurred greater amount of

expenditures by 1,400 GBP compare to expected.

B. Calculation of material price and quantity variance

Material price variance, as its name, measures the difference in costs due to different

target and actual price of material (Kaplan and Anderson, 2013). However, material quantity

variance quantifies the changes in costs because of differences between targeted and actual

quantity of PVC sheets that Dell consumed for manufacturing 4000 keyboards

MPV = Actual quantity (SP – AP)

= 10,000 feet(3.6-3.4)

= 2000 favourable

MQV = Actual price (SQ – AQ)

= 3.40 (10,000 – 11,000)

= 3400 A

MCV = MPV + MQV

= 2000 + (-3400)

= 1400 (A)

Results suggests Dell’s production department manager to keep their eye on the material

use to implement right control for ensuring its effective use.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

P5 Effectiveness of management accounting system in resolving financial problems

Management accounting is the tool that is used by the entities in order to track the cots so

that they can make control over wastage and can enhance revenues (Banerjee and Das,

2017).

Throughput accounting system: It is the type of system which is used by the Dell in order to

measure the performance. It is the method which concentrates on the cash element that

means it pays attention on cash generated by the firm over a period of time. This model is

very effective because by this way economic issues can be identified and firm can make

suitable strategies to reduce these problems (Tucker and Parker, 2014).

Lean accounting: It is another type of system in which overall manufacturing environment is

managed by the Dell well so that it can achieve its target. In this more focus on managers

are on the direct and indirect cost. These costs can enhance the operational cost of the

cited firm so management try to minimize these expenditures. It is the simple tool and

works to increase productivity of the organization (Banerjee and Das, 2017). It is

beneficial tool that supports in managing the manufacturing process well so that it can

make effective control over production inventory and can gain good profit.

Transfer pricing: It is the type of accounting system in which firms transact with other firms. It is

time consuming process and it enhances cost of the corporation because for that extra

labor is required by the entity in order to run its business well. Though it is kind of

expensive tool but by this way entities can provide raw material to its subsidiary firm on

time (Ball, Grubnic and Birchall, 2014 ). HP is using is method and running is business

well. It increases sales volume of the firm and company became able to make effective

strategies which can increase its profitability.

Traditional accounting system: It is the effective through which entities can produce more goods

and can satisfy the needs of consumers. It takes into consideration to various factors such

as costing, budgets, cash flow etc. It is beneficial tool that supports in the improvement of

11

P5 Effectiveness of management accounting system in resolving financial problems

Management accounting is the tool that is used by the entities in order to track the cots so

that they can make control over wastage and can enhance revenues (Banerjee and Das,

2017).

Throughput accounting system: It is the type of system which is used by the Dell in order to

measure the performance. It is the method which concentrates on the cash element that

means it pays attention on cash generated by the firm over a period of time. This model is

very effective because by this way economic issues can be identified and firm can make

suitable strategies to reduce these problems (Tucker and Parker, 2014).

Lean accounting: It is another type of system in which overall manufacturing environment is

managed by the Dell well so that it can achieve its target. In this more focus on managers

are on the direct and indirect cost. These costs can enhance the operational cost of the

cited firm so management try to minimize these expenditures. It is the simple tool and

works to increase productivity of the organization (Banerjee and Das, 2017). It is

beneficial tool that supports in managing the manufacturing process well so that it can

make effective control over production inventory and can gain good profit.

Transfer pricing: It is the type of accounting system in which firms transact with other firms. It is

time consuming process and it enhances cost of the corporation because for that extra

labor is required by the entity in order to run its business well. Though it is kind of

expensive tool but by this way entities can provide raw material to its subsidiary firm on

time (Ball, Grubnic and Birchall, 2014 ). HP is using is method and running is business

well. It increases sales volume of the firm and company became able to make effective

strategies which can increase its profitability.

Traditional accounting system: It is the effective through which entities can produce more goods

and can satisfy the needs of consumers. It takes into consideration to various factors such

as costing, budgets, cash flow etc. It is beneficial tool that supports in the improvement of

11

reporting system and helps in increasing the volume to great extent (Scapens and

Bromwich 2010).

CONCLUSION

From the above report it can be concluded that Management accounting is the effective

tool by this way managers can gather essential information and can make sound business

decisions. For making the judgments firms have to look upon the several costs and have to make

strategies so that they can make effective control over unnecessary expenditures. It helps in

increasing overall revenues and performance of the entity to great extent. From the study it is

found that absorption costing is far better than marginal, it helps in calculating the net profit.

With the help of management accounting Dell and resolve its economic problems and can run its

business well. It will help in sustaining in the market for longer duration.

12

Bromwich 2010).

CONCLUSION

From the above report it can be concluded that Management accounting is the effective

tool by this way managers can gather essential information and can make sound business

decisions. For making the judgments firms have to look upon the several costs and have to make

strategies so that they can make effective control over unnecessary expenditures. It helps in

increasing overall revenues and performance of the entity to great extent. From the study it is

found that absorption costing is far better than marginal, it helps in calculating the net profit.

With the help of management accounting Dell and resolve its economic problems and can run its

business well. It will help in sustaining in the market for longer duration.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.