Management Accounting Report: Analysis of DSA Manufacturing

VerifiedAdded on 2021/02/20

|17

|4367

|53

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within DSA Manufacturing, a UK-based clothing manufacturer. It delves into various management accounting systems, including cost accounting, inventory management, and price optimization. The report explores the origin, role, and principles of management accounting, highlighting the differences between management and financial accounting. It examines different types of management accounting reports, such as performance, budget, accounts receivable, and inventory management reports. Furthermore, the report discusses cost analysis techniques like direct and indirect costs, cost-volume-profit analysis, flexible budgeting, and cost variance. It also covers budgeting methods, including capital and operating budgets, zero-based budgeting, and priority-based budgeting, alongside the behavioral implications of budgeting like budgetary slack and participative budgeting. The report concludes with an overview of financial tools used for analysis and decision-making.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 ...........................................................................................................................................1

P2............................................................................................................................................3

TASK 2............................................................................................................................................5

P3............................................................................................................................................5

TASK 3............................................................................................................................................9

P4 ...........................................................................................................................................9

TASK 4..........................................................................................................................................12

P5 .........................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 ...........................................................................................................................................1

P2............................................................................................................................................3

TASK 2............................................................................................................................................5

P3............................................................................................................................................5

TASK 3............................................................................................................................................9

P4 ...........................................................................................................................................9

TASK 4..........................................................................................................................................12

P5 .........................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is a procedure to prepare management accounting reports and

accounts that provide reliable and timely financial and statistical information. It is required by

the managers to make daily routine and short term decisions (Chenhall and Moers, 2015).

Through the reports internal stakeholders like managers, employees etch determine the business

performance that weather it is well or not in the market. To better understand the concept of

report select manufacturing company, DSA manufacturing which is a clothing manufacturing

company based in the UK working with foreign factories.

In the report consist of different types of management accounting system and reporting

methods that provide advantage to organisation. These are helping to smoothly run their business

in efficient way. Calculate cost with the help of suitable techniques and analysis cost to produce

income statement. Along with applied different types of planning tools in the organisation to

predict financial problems and prepare effective strategy. Additionally, apply financial tool that

can help to identify problem with compare other organisation and find out suitable reason.

TASK 1

P1

Management Accounting: It is a method of examine as well as interacting

organizational information with executives in order to monitor business performance and

develop policies to improve it. DSA manufacturing apply management accounting to conduct

information on daily basis then analysis actual performance of company.

Management accounting system: The particular defined as inner system that is apply

through the manager as a reason to track business activities and record several sections of

company. By DSA manufacturing company utilise different types of management accounting

system to analyse actual performance of company.

Cost Accounting System: The particular system utilised by the company to know the cost

of different activities like manufacturing. It is applied by the DSA manufacturing in order to get

detail information of expenditure that are linked to producing clothes and other services.

Through this system add value to the business and help to get information of all the expenditure.

Inventory management system: It is applied by manufacturing company to analysis the

different stages of production in suitable way. It is applied by the DSA manufacturing company

1

Management accounting is a procedure to prepare management accounting reports and

accounts that provide reliable and timely financial and statistical information. It is required by

the managers to make daily routine and short term decisions (Chenhall and Moers, 2015).

Through the reports internal stakeholders like managers, employees etch determine the business

performance that weather it is well or not in the market. To better understand the concept of

report select manufacturing company, DSA manufacturing which is a clothing manufacturing

company based in the UK working with foreign factories.

In the report consist of different types of management accounting system and reporting

methods that provide advantage to organisation. These are helping to smoothly run their business

in efficient way. Calculate cost with the help of suitable techniques and analysis cost to produce

income statement. Along with applied different types of planning tools in the organisation to

predict financial problems and prepare effective strategy. Additionally, apply financial tool that

can help to identify problem with compare other organisation and find out suitable reason.

TASK 1

P1

Management Accounting: It is a method of examine as well as interacting

organizational information with executives in order to monitor business performance and

develop policies to improve it. DSA manufacturing apply management accounting to conduct

information on daily basis then analysis actual performance of company.

Management accounting system: The particular defined as inner system that is apply

through the manager as a reason to track business activities and record several sections of

company. By DSA manufacturing company utilise different types of management accounting

system to analyse actual performance of company.

Cost Accounting System: The particular system utilised by the company to know the cost

of different activities like manufacturing. It is applied by the DSA manufacturing in order to get

detail information of expenditure that are linked to producing clothes and other services.

Through this system add value to the business and help to get information of all the expenditure.

Inventory management system: It is applied by manufacturing company to analysis the

different stages of production in suitable way. It is applied by the DSA manufacturing company

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to track record of inventories at every stage of producing. There are three methods to calculate

inventory management such as LIFO, FIFO and AVCO.

LIFO – Last stock will be used for production procedure.

FIFO – Firstly purchased raw material utilised for production process.

AVCO – According to this methods

In DSA manufacturing company utilised FIFO method because through this method

properly utilise items in the company.

Price optimization system: As it names states, it is utilised by the manufacturing

company to set effective price structure for profit maximization. DSA manufacturing company

sell out different types of clothes and for this required set price structure as per the customer

requirement. It is important to determine the different reviews of customer regarding to product

that helps to attract them for purchase their products (Englund and Gerdin, 2014).

Job order costing system: Such system applied by the manufacturing company to

estimate cost of every single unit in the business. Job order costing system applied by the DSA

manufacturing to analysis cost of each and every cloth before sell out to clients. It is essential for

business because this system provides specific information of direct labour, material and

overhead.

Origin, role and principle of management accounting

Management accounting was developed through accounting cost due to commercial

enterprise modification. It plays major role in every organisation like profit maximization, stock

arrangement, decision maker and many more. After apply it in the company, they get right

instruction for different policies. There are defined different types of principles of management

accounting such as - Influence: Through communication skills influence to customer for purchase their

products in company. Relevance: It provides actual and sufficient information to manager that utilise by the

company at right time (Honggowati and et.al., 2017).

Trust: Management accounting provides different types of reports which must be reliable

because on the basis of these reports stakeholders take appropriate decision for further

investment.

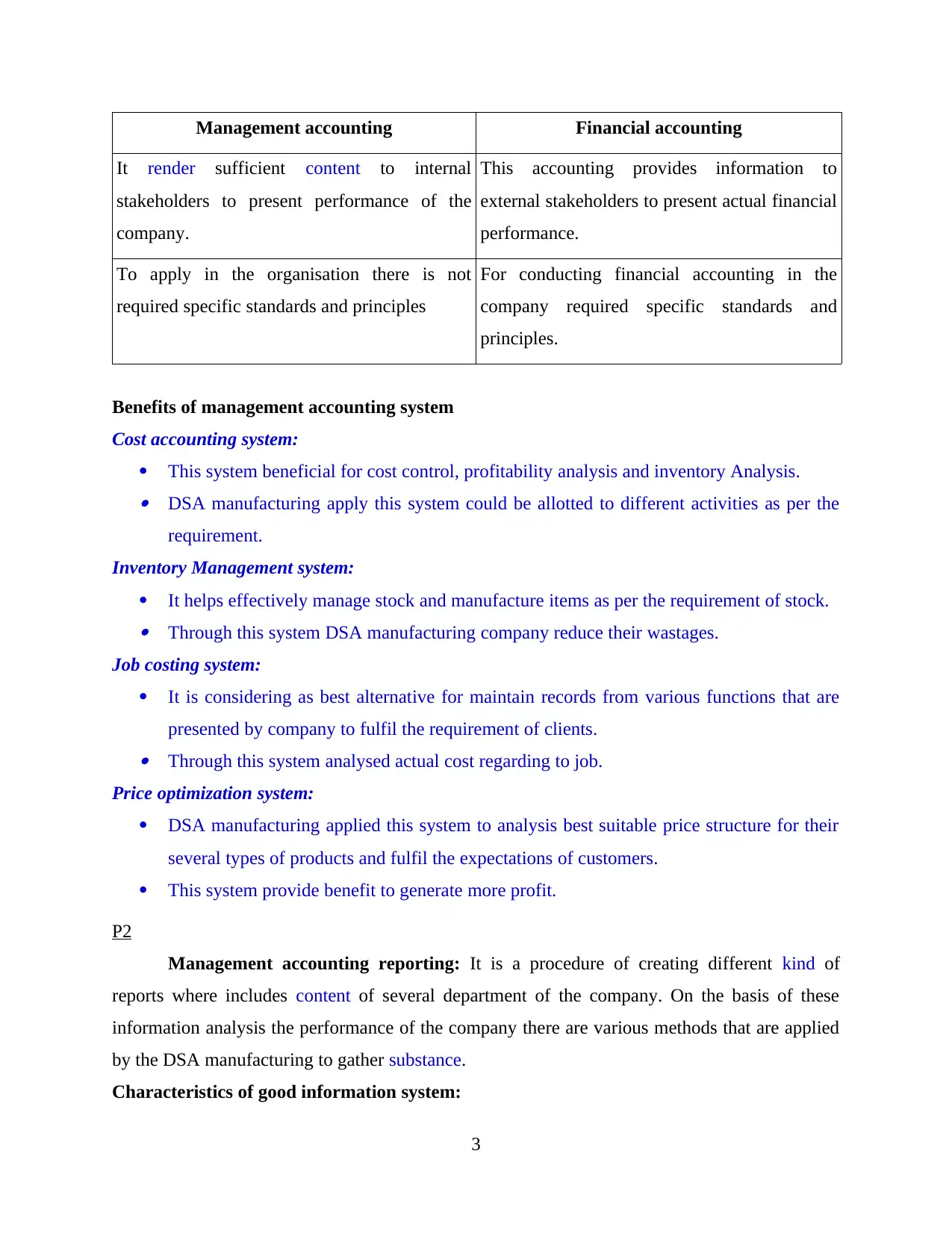

Difference between management and financial accounting

2

inventory management such as LIFO, FIFO and AVCO.

LIFO – Last stock will be used for production procedure.

FIFO – Firstly purchased raw material utilised for production process.

AVCO – According to this methods

In DSA manufacturing company utilised FIFO method because through this method

properly utilise items in the company.

Price optimization system: As it names states, it is utilised by the manufacturing

company to set effective price structure for profit maximization. DSA manufacturing company

sell out different types of clothes and for this required set price structure as per the customer

requirement. It is important to determine the different reviews of customer regarding to product

that helps to attract them for purchase their products (Englund and Gerdin, 2014).

Job order costing system: Such system applied by the manufacturing company to

estimate cost of every single unit in the business. Job order costing system applied by the DSA

manufacturing to analysis cost of each and every cloth before sell out to clients. It is essential for

business because this system provides specific information of direct labour, material and

overhead.

Origin, role and principle of management accounting

Management accounting was developed through accounting cost due to commercial

enterprise modification. It plays major role in every organisation like profit maximization, stock

arrangement, decision maker and many more. After apply it in the company, they get right

instruction for different policies. There are defined different types of principles of management

accounting such as - Influence: Through communication skills influence to customer for purchase their

products in company. Relevance: It provides actual and sufficient information to manager that utilise by the

company at right time (Honggowati and et.al., 2017).

Trust: Management accounting provides different types of reports which must be reliable

because on the basis of these reports stakeholders take appropriate decision for further

investment.

Difference between management and financial accounting

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting Financial accounting

It render sufficient content to internal

stakeholders to present performance of the

company.

This accounting provides information to

external stakeholders to present actual financial

performance.

To apply in the organisation there is not

required specific standards and principles

For conducting financial accounting in the

company required specific standards and

principles.

Benefits of management accounting system

Cost accounting system:

This system beneficial for cost control, profitability analysis and inventory Analysis. DSA manufacturing apply this system could be allotted to different activities as per the

requirement.

Inventory Management system:

It helps effectively manage stock and manufacture items as per the requirement of stock. Through this system DSA manufacturing company reduce their wastages.

Job costing system:

It is considering as best alternative for maintain records from various functions that are

presented by company to fulfil the requirement of clients. Through this system analysed actual cost regarding to job.

Price optimization system:

DSA manufacturing applied this system to analysis best suitable price structure for their

several types of products and fulfil the expectations of customers.

This system provide benefit to generate more profit.

P2

Management accounting reporting: It is a procedure of creating different kind of

reports where includes content of several department of the company. On the basis of these

information analysis the performance of the company there are various methods that are applied

by the DSA manufacturing to gather substance.

Characteristics of good information system:

3

It render sufficient content to internal

stakeholders to present performance of the

company.

This accounting provides information to

external stakeholders to present actual financial

performance.

To apply in the organisation there is not

required specific standards and principles

For conducting financial accounting in the

company required specific standards and

principles.

Benefits of management accounting system

Cost accounting system:

This system beneficial for cost control, profitability analysis and inventory Analysis. DSA manufacturing apply this system could be allotted to different activities as per the

requirement.

Inventory Management system:

It helps effectively manage stock and manufacture items as per the requirement of stock. Through this system DSA manufacturing company reduce their wastages.

Job costing system:

It is considering as best alternative for maintain records from various functions that are

presented by company to fulfil the requirement of clients. Through this system analysed actual cost regarding to job.

Price optimization system:

DSA manufacturing applied this system to analysis best suitable price structure for their

several types of products and fulfil the expectations of customers.

This system provide benefit to generate more profit.

P2

Management accounting reporting: It is a procedure of creating different kind of

reports where includes content of several department of the company. On the basis of these

information analysis the performance of the company there are various methods that are applied

by the DSA manufacturing to gather substance.

Characteristics of good information system:

3

These systems provide faithful, reliable and updated data to manager through different

management reports. On the basis of these information takes appropriate decision and invest

money for the enterprise activities. Updated information helps to take objection and render good

result (Badolato, Donelson and Ege, 2014).

Different types of reports

Performance Report: According to particular report has been created for analysis the

performance of employees and company. It is utilised by the DSA manufacturing company in

order to get data of employees and company's performance. This report used by the company to

provide reward and bonus to employees as per their performance. It is advantageous for the

business to develop effective plan of action to enhance its execution.

Budget Report: It is prepared by every organisation in order to predict fund sources and

usage estimation to different functional and operational section of company. It is utilised by the

DSA manufacturing company to analyse existent and modular disbursement of company. On the

basis of result analysis its performance. It is beneficial to formulate all business practices in

allotted budget to meet their objectives.

Accounts Receivable report: In this report produced by the company to create list of

clients who take goods on credit. Accounts receivable report develop by those companies which

are providing commodity on credit to their clients. In DSA manufacturing company it prepared

by company to keep detail information of clients. It is important for company to analyse those

client who do not pay amount on time.

Inventory management report: The main reason of develop this report to provide

detailed information of inventories. It covers how much stock required on different stages of

manufacturing. It is developed by the DSA manufacturing company in order to track record of

material for make clothes. It is advantageous for company because it provides actual status and

fulfil the required resources on time (Kaplan and Atkinson, 2015).

TASK 2

P3

Cost: The particular sum has been paid by the purchaser to the seller to get something.

DSA Manufacturing set suitable cost of their clothes to centralised attention of huge way of

clients. It is categorised into different cost such as:

4

management reports. On the basis of these information takes appropriate decision and invest

money for the enterprise activities. Updated information helps to take objection and render good

result (Badolato, Donelson and Ege, 2014).

Different types of reports

Performance Report: According to particular report has been created for analysis the

performance of employees and company. It is utilised by the DSA manufacturing company in

order to get data of employees and company's performance. This report used by the company to

provide reward and bonus to employees as per their performance. It is advantageous for the

business to develop effective plan of action to enhance its execution.

Budget Report: It is prepared by every organisation in order to predict fund sources and

usage estimation to different functional and operational section of company. It is utilised by the

DSA manufacturing company to analyse existent and modular disbursement of company. On the

basis of result analysis its performance. It is beneficial to formulate all business practices in

allotted budget to meet their objectives.

Accounts Receivable report: In this report produced by the company to create list of

clients who take goods on credit. Accounts receivable report develop by those companies which

are providing commodity on credit to their clients. In DSA manufacturing company it prepared

by company to keep detail information of clients. It is important for company to analyse those

client who do not pay amount on time.

Inventory management report: The main reason of develop this report to provide

detailed information of inventories. It covers how much stock required on different stages of

manufacturing. It is developed by the DSA manufacturing company in order to track record of

material for make clothes. It is advantageous for company because it provides actual status and

fulfil the required resources on time (Kaplan and Atkinson, 2015).

TASK 2

P3

Cost: The particular sum has been paid by the purchaser to the seller to get something.

DSA Manufacturing set suitable cost of their clothes to centralised attention of huge way of

clients. It is categorised into different cost such as:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct cost: These types of cost are directly linked to manufacturing of products are

called as direct costs. Such as decrease, security, wage to senior etc.

Indirect cost: It is not directly present in the cost of products rather than it related to

production procedure (Lindholm, Laine and Suomala, 2017).

Cost Analysis: It can be defined as procedure of that is applied by the company to

measure the advantages of several activities that are done by the company to generate profit. It is

utilised by the DSA manufacturing company in order to take appropriate decision to execute

business activities and survive for long time in the market.

Cost Volume profit: The particular method related to cost accounting which is applied

by the manager of DSA manufacturing for the reason of determining the effect of changes in cost

as well as volume on organisational profit.

Flexible Budgeting: According to this method prepare budget with required

modifications or adjustments are made as per the requirement of organisation activities. It is

applied by the DSA manufacturing to apply modification in budget per the cost and volume.

Cost Variance: It is defined as a method that is utilised by the DSA manufacturing to

determine cost of different among the actual and budgeted cost of manufacturing. This method

applied by the company to executing strategical determination.

Marginal costing: It is a costing method where cost unit will not change and categorise

into fixed and variable cost. Through this method sort out the problem of over and under

absorption and fix the price, profit planning and other valuable decisions.

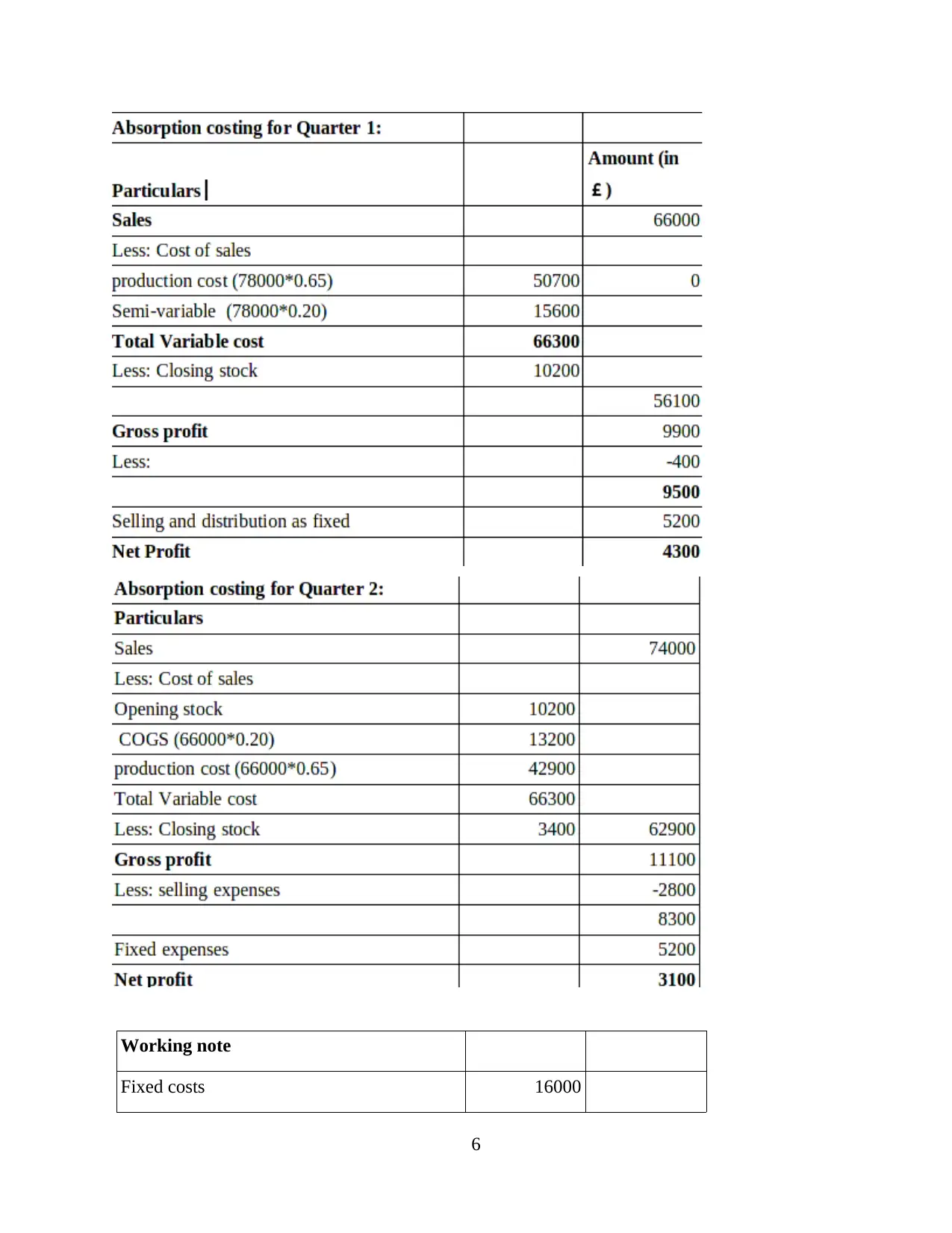

Absorption Costing: With the help of this method preparing financial records to present

gross profit and net profit. Absorption costing method allocate the fixed overhead to specific

section.

Fixed cost: There are including those cost that remain same after the changes other

things in the company. For DSA manufacturing defined these types of cost taxation, insurance,

interest etc.

Variable cost: The particular cost change as per the requirement of raw material is

known as variable cost. There are including wages, raw material and overhead.

5

called as direct costs. Such as decrease, security, wage to senior etc.

Indirect cost: It is not directly present in the cost of products rather than it related to

production procedure (Lindholm, Laine and Suomala, 2017).

Cost Analysis: It can be defined as procedure of that is applied by the company to

measure the advantages of several activities that are done by the company to generate profit. It is

utilised by the DSA manufacturing company in order to take appropriate decision to execute

business activities and survive for long time in the market.

Cost Volume profit: The particular method related to cost accounting which is applied

by the manager of DSA manufacturing for the reason of determining the effect of changes in cost

as well as volume on organisational profit.

Flexible Budgeting: According to this method prepare budget with required

modifications or adjustments are made as per the requirement of organisation activities. It is

applied by the DSA manufacturing to apply modification in budget per the cost and volume.

Cost Variance: It is defined as a method that is utilised by the DSA manufacturing to

determine cost of different among the actual and budgeted cost of manufacturing. This method

applied by the company to executing strategical determination.

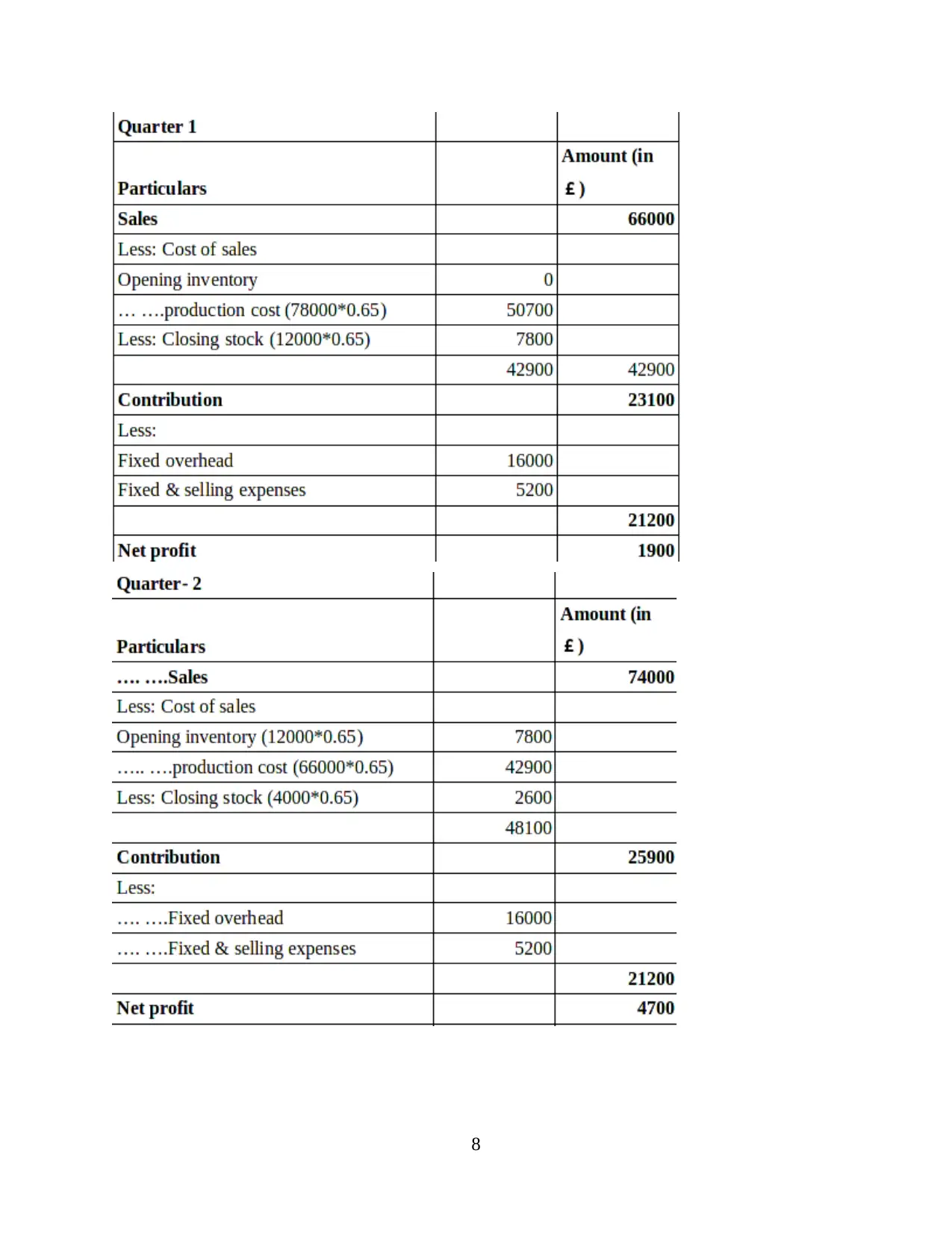

Marginal costing: It is a costing method where cost unit will not change and categorise

into fixed and variable cost. Through this method sort out the problem of over and under

absorption and fix the price, profit planning and other valuable decisions.

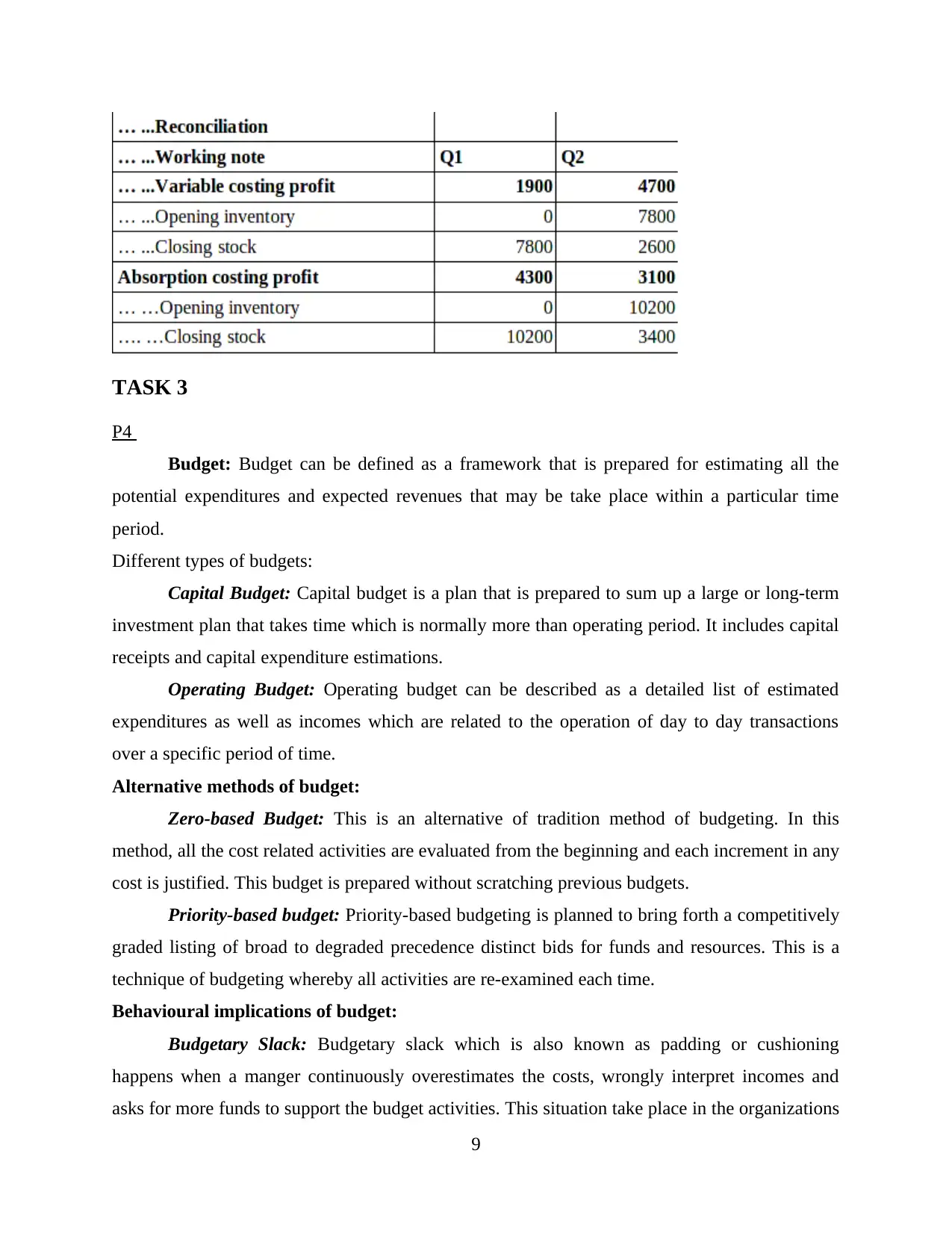

Absorption Costing: With the help of this method preparing financial records to present

gross profit and net profit. Absorption costing method allocate the fixed overhead to specific

section.

Fixed cost: There are including those cost that remain same after the changes other

things in the company. For DSA manufacturing defined these types of cost taxation, insurance,

interest etc.

Variable cost: The particular cost change as per the requirement of raw material is

known as variable cost. There are including wages, raw material and overhead.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working note

Fixed costs 16000

6

Fixed costs 16000

6

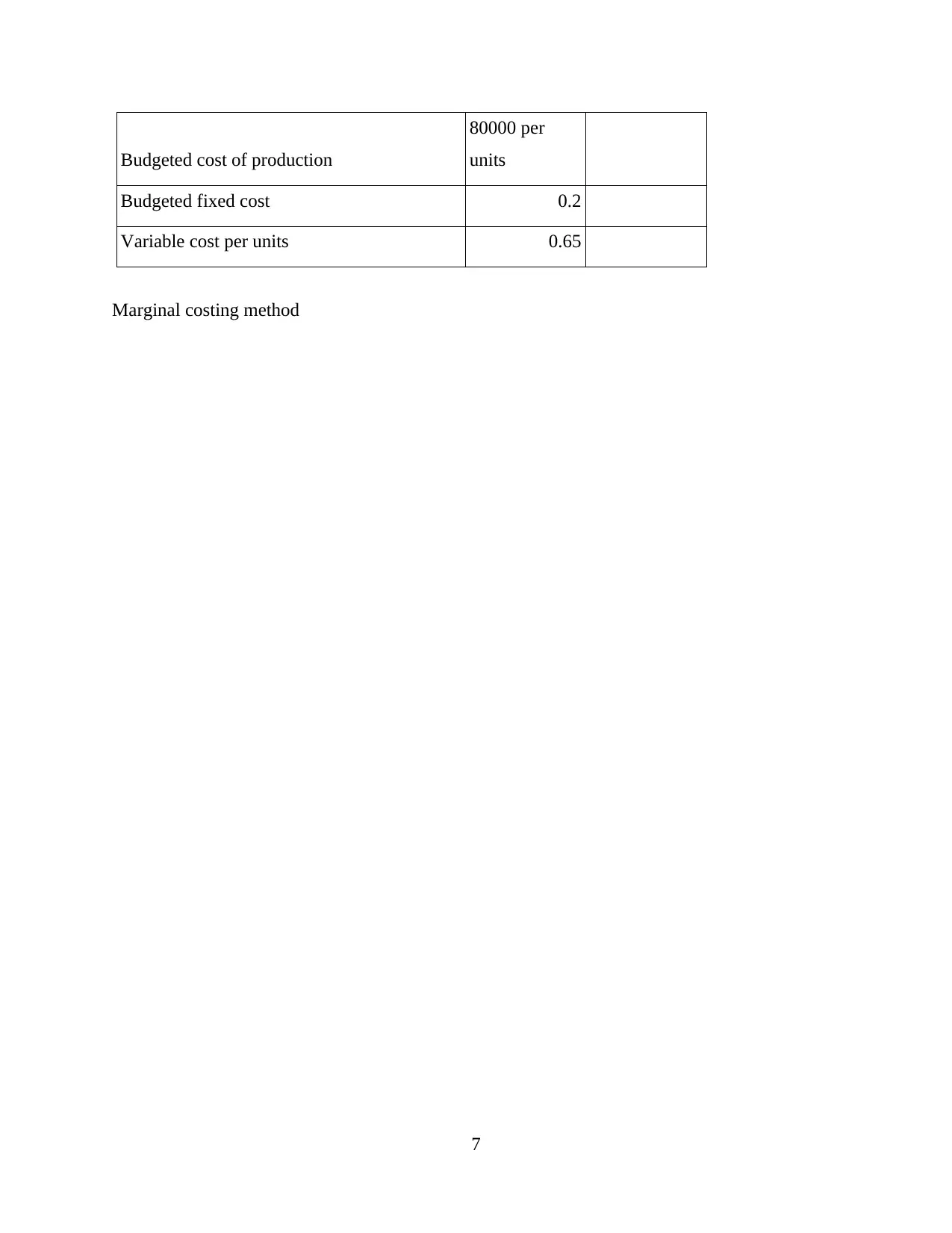

Budgeted cost of production

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

Marginal costing method

7

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

Marginal costing method

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4

Budget: Budget can be defined as a framework that is prepared for estimating all the

potential expenditures and expected revenues that may be take place within a particular time

period.

Different types of budgets:

Capital Budget: Capital budget is a plan that is prepared to sum up a large or long-term

investment plan that takes time which is normally more than operating period. It includes capital

receipts and capital expenditure estimations.

Operating Budget: Operating budget can be described as a detailed list of estimated

expenditures as well as incomes which are related to the operation of day to day transactions

over a specific period of time.

Alternative methods of budget:

Zero-based Budget: This is an alternative of tradition method of budgeting. In this

method, all the cost related activities are evaluated from the beginning and each increment in any

cost is justified. This budget is prepared without scratching previous budgets.

Priority-based budget: Priority-based budgeting is planned to bring forth a competitively

graded listing of broad to degraded precedence distinct bids for funds and resources. This is a

technique of budgeting whereby all activities are re-examined each time.

Behavioural implications of budget:

Budgetary Slack: Budgetary slack which is also known as padding or cushioning

happens when a manger continuously overestimates the costs, wrongly interpret incomes and

asks for more funds to support the budget activities. This situation take place in the organizations

9

P4

Budget: Budget can be defined as a framework that is prepared for estimating all the

potential expenditures and expected revenues that may be take place within a particular time

period.

Different types of budgets:

Capital Budget: Capital budget is a plan that is prepared to sum up a large or long-term

investment plan that takes time which is normally more than operating period. It includes capital

receipts and capital expenditure estimations.

Operating Budget: Operating budget can be described as a detailed list of estimated

expenditures as well as incomes which are related to the operation of day to day transactions

over a specific period of time.

Alternative methods of budget:

Zero-based Budget: This is an alternative of tradition method of budgeting. In this

method, all the cost related activities are evaluated from the beginning and each increment in any

cost is justified. This budget is prepared without scratching previous budgets.

Priority-based budget: Priority-based budgeting is planned to bring forth a competitively

graded listing of broad to degraded precedence distinct bids for funds and resources. This is a

technique of budgeting whereby all activities are re-examined each time.

Behavioural implications of budget:

Budgetary Slack: Budgetary slack which is also known as padding or cushioning

happens when a manger continuously overestimates the costs, wrongly interpret incomes and

asks for more funds to support the budget activities. This situation take place in the organizations

9

when subordinate managers when they know their budget proposals may be cut or senior

managers avoid the padding habit of their juniors.

Participative budgeting: The participative budgeting process is a bottom-up approach in

which the lower level employees that may be affected by the budget are involved in budget

preparation process. This approach helps in increasing employees' morale and conflicts between

managers and employees can be reduced.

Common Costing Systems:

Actual Costing: Actual costing is a cost accounting technique that includes direct cost

rates, actual cost and real qualities utilised in manufacturing to ascertain the cost of particular

products. An actual costing system allots direct costs to a cost object or something that can be

measure.

Normal Costing: Normal costing is a costing method that used actual cost of labour,

actual cost of material and standard overheads in order to derive the cost of the production. This

method is used where there sudden increase in standard rates are absent.

Standard Costing: This costing method is used to find out the variances between actual

and standard costs for a product manufacturing. This costing method uses standard rates for

direct expenditures and overheads and find their variances by using actual costs at the same time.

Job Costing: Job costing method is used to find out the cost of manufacturing a specific

product. This method used direct labour, direct material and overheads in order to find out the

cost of a particular product or specific job.

Process Costing: Process costing method is used where there mass production of similar

units take place and cost associated with an individual unit can not be separated.

Batch Costing: Batch costing can be described as the cluster of costs incurred when a

batch or group of services or products is manufactured or rendered that can not be determined to

particular product or service.

PEST Analysis: PEST Analysis is a technique of evaluating the external factors of an economy

that may affect the business of the organization either favourably or adversely. A brief PEST

analysis of DSA Manufacturing is presented below:

Political Factors: Political factors are the policies and components related to the

governmental rules and laws exist in an economy. Funding, grants and subsidy provided by the

10

managers avoid the padding habit of their juniors.

Participative budgeting: The participative budgeting process is a bottom-up approach in

which the lower level employees that may be affected by the budget are involved in budget

preparation process. This approach helps in increasing employees' morale and conflicts between

managers and employees can be reduced.

Common Costing Systems:

Actual Costing: Actual costing is a cost accounting technique that includes direct cost

rates, actual cost and real qualities utilised in manufacturing to ascertain the cost of particular

products. An actual costing system allots direct costs to a cost object or something that can be

measure.

Normal Costing: Normal costing is a costing method that used actual cost of labour,

actual cost of material and standard overheads in order to derive the cost of the production. This

method is used where there sudden increase in standard rates are absent.

Standard Costing: This costing method is used to find out the variances between actual

and standard costs for a product manufacturing. This costing method uses standard rates for

direct expenditures and overheads and find their variances by using actual costs at the same time.

Job Costing: Job costing method is used to find out the cost of manufacturing a specific

product. This method used direct labour, direct material and overheads in order to find out the

cost of a particular product or specific job.

Process Costing: Process costing method is used where there mass production of similar

units take place and cost associated with an individual unit can not be separated.

Batch Costing: Batch costing can be described as the cluster of costs incurred when a

batch or group of services or products is manufactured or rendered that can not be determined to

particular product or service.

PEST Analysis: PEST Analysis is a technique of evaluating the external factors of an economy

that may affect the business of the organization either favourably or adversely. A brief PEST

analysis of DSA Manufacturing is presented below:

Political Factors: Political factors are the policies and components related to the

governmental rules and laws exist in an economy. Funding, grants and subsidy provided by the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.