Management Accounting Report: Cost Analysis and Reporting Techniques

VerifiedAdded on 2022/12/15

|15

|4340

|446

Report

AI Summary

This report delves into the realm of management accounting, focusing on its systems, reporting methods, and cost calculation techniques, using Eastern Engineering Company Ltd (EECL) as a case study. The introduction provides a foundational understanding of management accounting's role in financial decision-making. Task 1 explores various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, outlining their essential requirements within the context of EECL. It also examines different management accounting reporting methods such as job costing reports, inventory management reports, accounts receivables aging reports, and budget reports. Task 2 focuses on the calculation of costs using marginal costing and absorption costing, highlighting their advantages, disadvantages, and providing justification for their use. The report concludes with a summary of the key findings and provides references to the sources used.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management Accounting Systems........................................................................................1

P2: Management Accounting Reporting......................................................................................3

TASK 2............................................................................................................................................4

P3: Calculation of costs...............................................................................................................4

TASK 3............................................................................................................................................7

P4: Advantages and Disadvantages of planning tools.................................................................7

TASK 4............................................................................................................................................9

P5: Comparison of organizations in adaptation of management accounting to solve financial

problems.......................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management Accounting Systems........................................................................................1

P2: Management Accounting Reporting......................................................................................3

TASK 2............................................................................................................................................4

P3: Calculation of costs...............................................................................................................4

TASK 3............................................................................................................................................7

P4: Advantages and Disadvantages of planning tools.................................................................7

TASK 4............................................................................................................................................9

P5: Comparison of organizations in adaptation of management accounting to solve financial

problems.......................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management Accounting refers to using of different types of financial provisions which

will help in deriving the right results for the future time period (Abernethy and Wallis, 2019). It

is quite helpful in deriving the advantage for the company. It helps the managers a lot by

ensuring that they are able to take short-term and long-term decisions. Through it, analysis and

interpretation can be done to derive conclusions and recommendations in an effective manner.

This report is based on EECL that is Eastern Engineering Company Ltd which operates as

medium sized venture within manufacturing field.

In this assignment, focus will be made on demonstration of understanding of

management accounting systems, methods for preparation of its reports. Additionally,

explanation of the use of planning tools and comparison of ways in which the companies can

make its use to respond to financial problems will be made as a part of this assignment.

TASK 1

P1: Management Accounting Systems

Concept of management accounting evolved during 1900s with the purpose of supplying

finance related information to management of entity together with other stakeholders that have

role to devise business decisions. Within EECL, management accounting information serves

objective of assisting administrators in devising well informed and reasoned decisions. Intended

aim of the accounting is to aid users for internal people in making effective determinations for

future. There are various types of systems which are used in management accounting. Some are

explained in context to EECL below:

Cost Accounting System- In this system, there is an estimation of various costs in the

company (Armitage, Webb and Glynn, 2016). Thus it can be very helpful for the purpose of

determining the costs. For the management of EECL it is essential that they are able to make its

use for segregating the costs and determining the overheads. These overheads can be allocated

according to the expenses which are made by the various departments such as Production,

Finance, HR, Sales and Marketing etc.

Essential requirements-

1

Management Accounting refers to using of different types of financial provisions which

will help in deriving the right results for the future time period (Abernethy and Wallis, 2019). It

is quite helpful in deriving the advantage for the company. It helps the managers a lot by

ensuring that they are able to take short-term and long-term decisions. Through it, analysis and

interpretation can be done to derive conclusions and recommendations in an effective manner.

This report is based on EECL that is Eastern Engineering Company Ltd which operates as

medium sized venture within manufacturing field.

In this assignment, focus will be made on demonstration of understanding of

management accounting systems, methods for preparation of its reports. Additionally,

explanation of the use of planning tools and comparison of ways in which the companies can

make its use to respond to financial problems will be made as a part of this assignment.

TASK 1

P1: Management Accounting Systems

Concept of management accounting evolved during 1900s with the purpose of supplying

finance related information to management of entity together with other stakeholders that have

role to devise business decisions. Within EECL, management accounting information serves

objective of assisting administrators in devising well informed and reasoned decisions. Intended

aim of the accounting is to aid users for internal people in making effective determinations for

future. There are various types of systems which are used in management accounting. Some are

explained in context to EECL below:

Cost Accounting System- In this system, there is an estimation of various costs in the

company (Armitage, Webb and Glynn, 2016). Thus it can be very helpful for the purpose of

determining the costs. For the management of EECL it is essential that they are able to make its

use for segregating the costs and determining the overheads. These overheads can be allocated

according to the expenses which are made by the various departments such as Production,

Finance, HR, Sales and Marketing etc.

Essential requirements-

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This system needs to ensure that the different types of costs are calculated in an effective

manner within the organization. Thus in the context of EECL it must be able to identify

and segregate the various costs and expenses which are being incurred.

This system must be able to advise the management on the techniques which can be used

so that costs can be reduced and profits can be maximized. For EECL, it is important that

the company is able to consider it and reduce costs for enhancing the level of profits.

Inventory Management System- This system is used in order to track the stock levels and

manage them in an effective manner (Arunruangsirilert and Chonglerttham, 2017). By making its

use, inflows and outflows of various items can be tracked in a better manner. Thus for the

managers of EECL it is extremely helpful so that they are able to ensure that stock is properly

managed and there is not misplacement of the items.

Essential requirements-

In a good inventory management system, there should be identification of different items

and their related information. Thus the managers of EECL will be able to identify various

stock items by making appropriate use of it.

In an inventory management system, there must be the use of a software which can be

helpful in the tracking and managing of stock items. Thus in the context of EECL it can

be quite useful for ensuring that there is no misplacement of goods.

Job Costing System- In this method, there is an estimation of various job costs. It is

essential to be used in those companies which are indulged in the process of manufacturing

(Aureli and et.al., 2019). In the context of EECL, it can be very helpful to manage its job order

inflows and outflows effectively. In this way the firm will be able to make sure that it can attain a

higher level of efficiency and effectiveness.

Essential requirements-

In a good job costing system, there must be tracking of job performance. EECL will be

able to ensure that they can identify deviations and variances and remove them.

A good job costing system ensures that the level of profits can be enhanced effectively by

ensuring that the costs and expenses which are associated with them are reduced. In this

way, EECL will be able to maximize its level of profitability.

Price optimization system- In it, there is setting of price by the managers through the use

of appropriate methods and techniques (Bedford and Speklé, 2018). Therefore, for the managers

2

manner within the organization. Thus in the context of EECL it must be able to identify

and segregate the various costs and expenses which are being incurred.

This system must be able to advise the management on the techniques which can be used

so that costs can be reduced and profits can be maximized. For EECL, it is important that

the company is able to consider it and reduce costs for enhancing the level of profits.

Inventory Management System- This system is used in order to track the stock levels and

manage them in an effective manner (Arunruangsirilert and Chonglerttham, 2017). By making its

use, inflows and outflows of various items can be tracked in a better manner. Thus for the

managers of EECL it is extremely helpful so that they are able to ensure that stock is properly

managed and there is not misplacement of the items.

Essential requirements-

In a good inventory management system, there should be identification of different items

and their related information. Thus the managers of EECL will be able to identify various

stock items by making appropriate use of it.

In an inventory management system, there must be the use of a software which can be

helpful in the tracking and managing of stock items. Thus in the context of EECL it can

be quite useful for ensuring that there is no misplacement of goods.

Job Costing System- In this method, there is an estimation of various job costs. It is

essential to be used in those companies which are indulged in the process of manufacturing

(Aureli and et.al., 2019). In the context of EECL, it can be very helpful to manage its job order

inflows and outflows effectively. In this way the firm will be able to make sure that it can attain a

higher level of efficiency and effectiveness.

Essential requirements-

In a good job costing system, there must be tracking of job performance. EECL will be

able to ensure that they can identify deviations and variances and remove them.

A good job costing system ensures that the level of profits can be enhanced effectively by

ensuring that the costs and expenses which are associated with them are reduced. In this

way, EECL will be able to maximize its level of profitability.

Price optimization system- In it, there is setting of price by the managers through the use

of appropriate methods and techniques (Bedford and Speklé, 2018). Therefore, for the managers

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of EECL are required to ensure that they make the use of this system by forecasting the change

in prices in the market.

Essential requirements-

In a price optimization system, there must be use of mathematical methods to forecast the

changes in demand of goods. This will help EECL to set a right price.

A price optimization system must help the managers to be able to collect the historical

data related to the price of various products. In the context of EECL, it can be quite

helpful.

P2: Methods in management Accounting Reporting

Multiple kinds of reports of management accounting are prepared by managers so that

they are able to focus towards information about financial accounting. Within EECL, certain

kinds of methods related with management accounting report are used by administrators to plan,

regulate, make decision addition to measure performance. Either daily, weekly, monthly,

quarterly, half yearly or annually, management accounting reports are generated as per

requirements. There are different methods used by departmental managers of EECL for

management accounting reports. These are explained under:

Job Costing Reports- In these reports, there is an analysis and interpretation of job costs

in an effective manner (Ghasemi and et.al., 2019). It analyses the flow of job orders related

information in an effective manner. They are useful for those companies which deal in the

process of manufacturing. By preparing them they can identify the methods and techniques they

can use for the purpose of enhancement of the level of profits which is earned by completing the

orders of clients. For EECL, they are useful in the management of job orders so that they can

derive adequate information whenever required. All the records can be maintained in the desired

manner when the managers use them.

Inventory Management Reports- These reports are prepared in order to maintain the

desired information related to the stock items (Ghasemi and et.al., 2016). A detailed record of

stock items over the year can be maintained as a part of them. Thus for the management they

become quite useful and are required to be used in an appropriate manner. Effective analysis and

interpretation can be carried out by making them. In EECL, they can be used so that the

managers can identify any problems which are being faced while maintaining a detailed record

of inventory. Rectifying measures can be taken with immediate effect if required.

3

in prices in the market.

Essential requirements-

In a price optimization system, there must be use of mathematical methods to forecast the

changes in demand of goods. This will help EECL to set a right price.

A price optimization system must help the managers to be able to collect the historical

data related to the price of various products. In the context of EECL, it can be quite

helpful.

P2: Methods in management Accounting Reporting

Multiple kinds of reports of management accounting are prepared by managers so that

they are able to focus towards information about financial accounting. Within EECL, certain

kinds of methods related with management accounting report are used by administrators to plan,

regulate, make decision addition to measure performance. Either daily, weekly, monthly,

quarterly, half yearly or annually, management accounting reports are generated as per

requirements. There are different methods used by departmental managers of EECL for

management accounting reports. These are explained under:

Job Costing Reports- In these reports, there is an analysis and interpretation of job costs

in an effective manner (Ghasemi and et.al., 2019). It analyses the flow of job orders related

information in an effective manner. They are useful for those companies which deal in the

process of manufacturing. By preparing them they can identify the methods and techniques they

can use for the purpose of enhancement of the level of profits which is earned by completing the

orders of clients. For EECL, they are useful in the management of job orders so that they can

derive adequate information whenever required. All the records can be maintained in the desired

manner when the managers use them.

Inventory Management Reports- These reports are prepared in order to maintain the

desired information related to the stock items (Ghasemi and et.al., 2016). A detailed record of

stock items over the year can be maintained as a part of them. Thus for the management they

become quite useful and are required to be used in an appropriate manner. Effective analysis and

interpretation can be carried out by making them. In EECL, they can be used so that the

managers can identify any problems which are being faced while maintaining a detailed record

of inventory. Rectifying measures can be taken with immediate effect if required.

3

Accounts Receivables Ageing Reports- The managers of organizations prepare these

reports to maintain a track record of their trade receivables (Hariyati, Tjahjadi and Soewarno,

2019). Proper details regarding each and every debtor of the firm can be thus maintained. The

number of days for which the credit has been provided to them is included as a part of them.

Thus the debtors who have not paid their dues on time can be identified. In the context of EECL,

it is essential that the management manages the accounts receivables and identifies those debtors

who have not paid their dues since a long time in the organization. Thus a strategy can be framed

effectively for collecting the amount which is due with them.

Budget reports- In the companies, there is a specific requirement for the preparation of

these reports to maintain a record of the budgets which are made (Honggowati and et.al., 2017).

They are prepared specifically for a year and can be adjusted according to the change in the

requirements due to the prevailing situations and circumstances in the market according to which

the organizations can make the required adjustments. For the management of EECL, there is a

requirement to identify the detailed aspects related to the budgets so that deviations and

variances in the performance can be identified. This will help a lot to control the expenses and

forecast the incomes in a better manner. Thus higher-level of efficiency and effectiveness can be

maintained in the processes.

TASK 2

P3: Calculation of costs

In a firm, there can be use of various types of techniques through which costs can be

calculated. These are explained as follows-

Marginal Costing- It is a technique through which the organizations are able to

determine the level of profitability and the break-even point which is the level where the firms

neither earn profits nor incur losses (Maas, Schaltegger and Crutzen, 2016). The management of

EECL can use this method so that they are able to estimate the profits which they are earning.

Advantages-

With the use of this technique, the managers are able to ensure that they take short-term

decisions. Thus EECL will be able to make use of it to take the appropriate decisions

which will be very helpful in the short-term period of time.

4

reports to maintain a track record of their trade receivables (Hariyati, Tjahjadi and Soewarno,

2019). Proper details regarding each and every debtor of the firm can be thus maintained. The

number of days for which the credit has been provided to them is included as a part of them.

Thus the debtors who have not paid their dues on time can be identified. In the context of EECL,

it is essential that the management manages the accounts receivables and identifies those debtors

who have not paid their dues since a long time in the organization. Thus a strategy can be framed

effectively for collecting the amount which is due with them.

Budget reports- In the companies, there is a specific requirement for the preparation of

these reports to maintain a record of the budgets which are made (Honggowati and et.al., 2017).

They are prepared specifically for a year and can be adjusted according to the change in the

requirements due to the prevailing situations and circumstances in the market according to which

the organizations can make the required adjustments. For the management of EECL, there is a

requirement to identify the detailed aspects related to the budgets so that deviations and

variances in the performance can be identified. This will help a lot to control the expenses and

forecast the incomes in a better manner. Thus higher-level of efficiency and effectiveness can be

maintained in the processes.

TASK 2

P3: Calculation of costs

In a firm, there can be use of various types of techniques through which costs can be

calculated. These are explained as follows-

Marginal Costing- It is a technique through which the organizations are able to

determine the level of profitability and the break-even point which is the level where the firms

neither earn profits nor incur losses (Maas, Schaltegger and Crutzen, 2016). The management of

EECL can use this method so that they are able to estimate the profits which they are earning.

Advantages-

With the use of this technique, the managers are able to ensure that they take short-term

decisions. Thus EECL will be able to make use of it to take the appropriate decisions

which will be very helpful in the short-term period of time.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The use of this method is very useful for the comparison purposes. It can be facilitated

either with the set industrial standards or with the previous data of the company.

Disadvantages-

In this method, there is an use of different assumptions. Thus the management of EECL

will face a disadvantage if any of these assumptions prove out to be wrong.

Through this technique, effective control cannot be exercised. Thus for the managers of

EECL this can result in a disadvantage if they are not able to control the various aspects

in the organization.

Absorption Costing- It is a method through which the overall level of costs can be

calculated in the organization (Messner, 2016). By making its use, the organizations will be able

to make sure that they can estimate the costs in a highly effective manner. In the context of

EECL it can be very useful so that it can estimate the level of profitability.

Advantages-

When this method is used by the organizations it can be quite helpful in bringing a

higher-level of responsibility in the managers for their respective departments. If their

department is having excessive costs then the reasons for the same can be identified. This

can initiate rectifying actions to be taken for reducing them effectively and efficiently.

Thus in EECL an advantage can be created.

The use of this technique by the companies can ensure that inefficient utilization of

resources can be avoided in the organization. Thus in this way under-utilization and over-

utilization of resources can be prevented and their optimum-utilization can be ensured so

that the best results can be derived from them which can be highly beneficial for the

company in the future time period. For EECL, this can be quite helpful in creating an

advantage.

Disadvantages-

The right use of this method is dependent upon the accurate apportionment of overhead

costs. Thus in EECL this can lead towards a disadvantage.

This technique is not helpful for preparing flexible budget and also does not helps in

segregation between fixed and variable costs. In the context of EECL, this can create a

disadvantage.

5

either with the set industrial standards or with the previous data of the company.

Disadvantages-

In this method, there is an use of different assumptions. Thus the management of EECL

will face a disadvantage if any of these assumptions prove out to be wrong.

Through this technique, effective control cannot be exercised. Thus for the managers of

EECL this can result in a disadvantage if they are not able to control the various aspects

in the organization.

Absorption Costing- It is a method through which the overall level of costs can be

calculated in the organization (Messner, 2016). By making its use, the organizations will be able

to make sure that they can estimate the costs in a highly effective manner. In the context of

EECL it can be very useful so that it can estimate the level of profitability.

Advantages-

When this method is used by the organizations it can be quite helpful in bringing a

higher-level of responsibility in the managers for their respective departments. If their

department is having excessive costs then the reasons for the same can be identified. This

can initiate rectifying actions to be taken for reducing them effectively and efficiently.

Thus in EECL an advantage can be created.

The use of this technique by the companies can ensure that inefficient utilization of

resources can be avoided in the organization. Thus in this way under-utilization and over-

utilization of resources can be prevented and their optimum-utilization can be ensured so

that the best results can be derived from them which can be highly beneficial for the

company in the future time period. For EECL, this can be quite helpful in creating an

advantage.

Disadvantages-

The right use of this method is dependent upon the accurate apportionment of overhead

costs. Thus in EECL this can lead towards a disadvantage.

This technique is not helpful for preparing flexible budget and also does not helps in

segregation between fixed and variable costs. In the context of EECL, this can create a

disadvantage.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

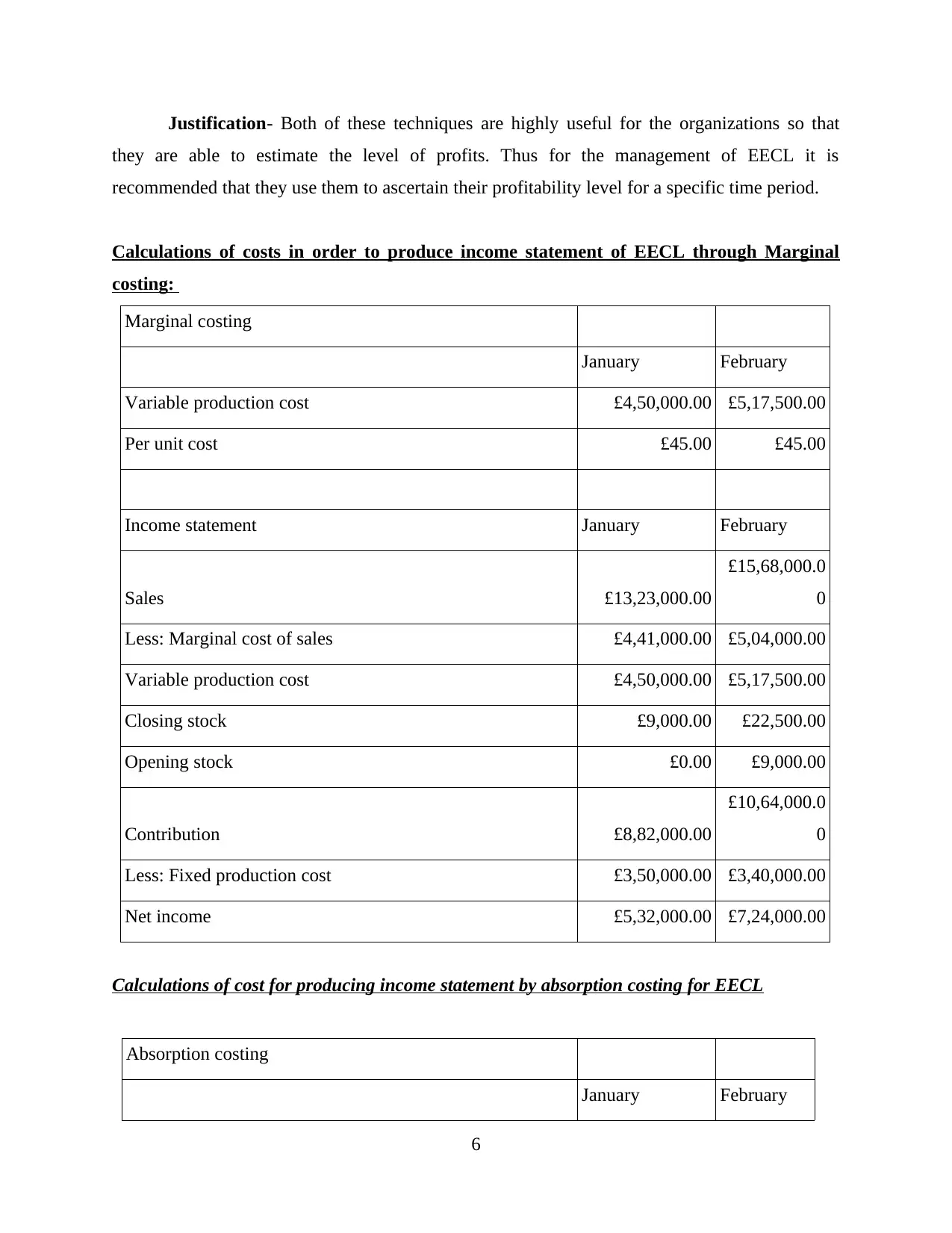

Justification- Both of these techniques are highly useful for the organizations so that

they are able to estimate the level of profits. Thus for the management of EECL it is

recommended that they use them to ascertain their profitability level for a specific time period.

Calculations of costs in order to produce income statement of EECL through Marginal

costing:

Marginal costing

January February

Variable production cost £4,50,000.00 £5,17,500.00

Per unit cost £45.00 £45.00

Income statement January February

Sales £13,23,000.00

£15,68,000.0

0

Less: Marginal cost of sales £4,41,000.00 £5,04,000.00

Variable production cost £4,50,000.00 £5,17,500.00

Closing stock £9,000.00 £22,500.00

Opening stock £0.00 £9,000.00

Contribution £8,82,000.00

£10,64,000.0

0

Less: Fixed production cost £3,50,000.00 £3,40,000.00

Net income £5,32,000.00 £7,24,000.00

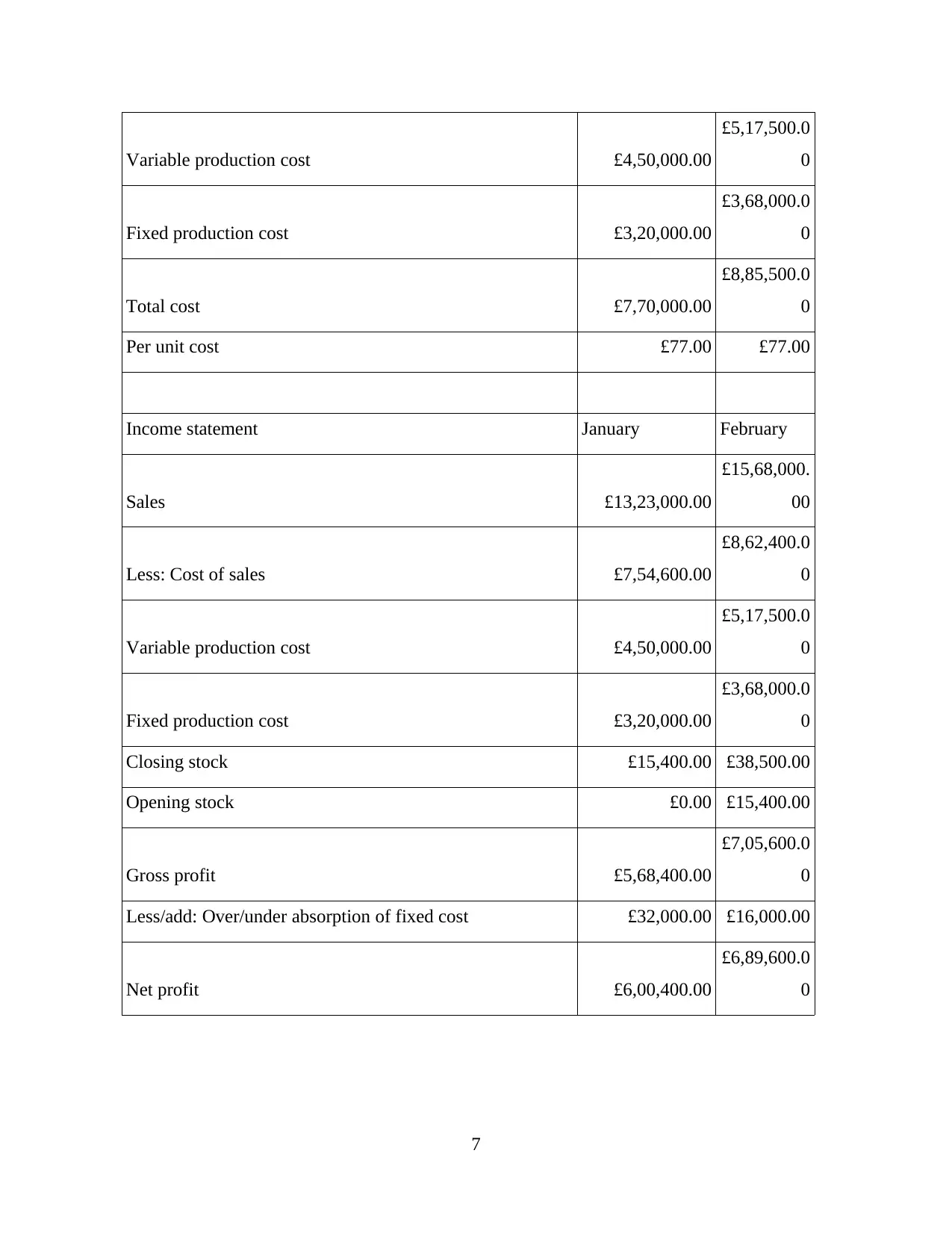

Calculations of cost for producing income statement by absorption costing for EECL

Absorption costing

January February

6

they are able to estimate the level of profits. Thus for the management of EECL it is

recommended that they use them to ascertain their profitability level for a specific time period.

Calculations of costs in order to produce income statement of EECL through Marginal

costing:

Marginal costing

January February

Variable production cost £4,50,000.00 £5,17,500.00

Per unit cost £45.00 £45.00

Income statement January February

Sales £13,23,000.00

£15,68,000.0

0

Less: Marginal cost of sales £4,41,000.00 £5,04,000.00

Variable production cost £4,50,000.00 £5,17,500.00

Closing stock £9,000.00 £22,500.00

Opening stock £0.00 £9,000.00

Contribution £8,82,000.00

£10,64,000.0

0

Less: Fixed production cost £3,50,000.00 £3,40,000.00

Net income £5,32,000.00 £7,24,000.00

Calculations of cost for producing income statement by absorption costing for EECL

Absorption costing

January February

6

Variable production cost £4,50,000.00

£5,17,500.0

0

Fixed production cost £3,20,000.00

£3,68,000.0

0

Total cost £7,70,000.00

£8,85,500.0

0

Per unit cost £77.00 £77.00

Income statement January February

Sales £13,23,000.00

£15,68,000.

00

Less: Cost of sales £7,54,600.00

£8,62,400.0

0

Variable production cost £4,50,000.00

£5,17,500.0

0

Fixed production cost £3,20,000.00

£3,68,000.0

0

Closing stock £15,400.00 £38,500.00

Opening stock £0.00 £15,400.00

Gross profit £5,68,400.00

£7,05,600.0

0

Less/add: Over/under absorption of fixed cost £32,000.00 £16,000.00

Net profit £6,00,400.00

£6,89,600.0

0

7

£5,17,500.0

0

Fixed production cost £3,20,000.00

£3,68,000.0

0

Total cost £7,70,000.00

£8,85,500.0

0

Per unit cost £77.00 £77.00

Income statement January February

Sales £13,23,000.00

£15,68,000.

00

Less: Cost of sales £7,54,600.00

£8,62,400.0

0

Variable production cost £4,50,000.00

£5,17,500.0

0

Fixed production cost £3,20,000.00

£3,68,000.0

0

Closing stock £15,400.00 £38,500.00

Opening stock £0.00 £15,400.00

Gross profit £5,68,400.00

£7,05,600.0

0

Less/add: Over/under absorption of fixed cost £32,000.00 £16,000.00

Net profit £6,00,400.00

£6,89,600.0

0

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P4: Advantages and Disadvantages of planning tools

Sum of finances that are allocated for some specific purpose along with summary of

intended proposals addition to expenditure is said to budget. It generally comprises budget

surplus, deficit in expenses than revenues and providing financial resources for usage at some

future duration. With budget, financial managers of EECL are able to control spendings, save

money along with track expenses. There are several planning tools used in EECL that facilitates

budgetary control. These tools are explained as follows-

Cash budget- It is an estimation of the overall receipts and payments in cash over a

specific period of time (Otley, 2016). In EECL, its use can be made so that the managers are able

to properly estimate the cash requirements in an effective manner.

Advantages-

The use of this budget is quite helpful in the organizations for the purpose of maintenance

of liquidity. Therefore this is highly beneficial for the managers of EECL.

By making this budget the management can determine the best way to manage their cash

and other liquid resources to optimize their use. In the context of EECL, this can create

an advantage.

Disadvantages-

This budget can create an impact on flexibility. For EECL this can result in a

disadvantage.

Preparation of this budget consumes a lot of time in the organization. In EECL, this can

lead towards a disadvantage.

Overhead budget- In this budget, there is an estimation of various types of overheads

within the organization (Quinn and et.al., 2018). It can be very helpful for the management in

ensuring that proper segregation of overheads can be made. For the managers of EECL this can

be helpful in controlling of the expenses in an effective manner.

Advantages-

Better segregation of overheads can be made when these reports are used. In EECL this

can create an advantage.

8

P4: Advantages and Disadvantages of planning tools

Sum of finances that are allocated for some specific purpose along with summary of

intended proposals addition to expenditure is said to budget. It generally comprises budget

surplus, deficit in expenses than revenues and providing financial resources for usage at some

future duration. With budget, financial managers of EECL are able to control spendings, save

money along with track expenses. There are several planning tools used in EECL that facilitates

budgetary control. These tools are explained as follows-

Cash budget- It is an estimation of the overall receipts and payments in cash over a

specific period of time (Otley, 2016). In EECL, its use can be made so that the managers are able

to properly estimate the cash requirements in an effective manner.

Advantages-

The use of this budget is quite helpful in the organizations for the purpose of maintenance

of liquidity. Therefore this is highly beneficial for the managers of EECL.

By making this budget the management can determine the best way to manage their cash

and other liquid resources to optimize their use. In the context of EECL, this can create

an advantage.

Disadvantages-

This budget can create an impact on flexibility. For EECL this can result in a

disadvantage.

Preparation of this budget consumes a lot of time in the organization. In EECL, this can

lead towards a disadvantage.

Overhead budget- In this budget, there is an estimation of various types of overheads

within the organization (Quinn and et.al., 2018). It can be very helpful for the management in

ensuring that proper segregation of overheads can be made. For the managers of EECL this can

be helpful in controlling of the expenses in an effective manner.

Advantages-

Better segregation of overheads can be made when these reports are used. In EECL this

can create an advantage.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

When this budget is used within the companies it can ensure that they are able to exercise

greater control over the operations in an effective manner. For EECL, this can result in an

advantage.

Disadvantages-

Preparation of this budget within the companies requires the application of higher-level

of skills. For EECL this can create a disadvantage if its workers do not have these skills.

In this budget, there can be an over-allocation or under-allocation of the overheads. In

EECL this can result in a disadvantage if the overheads are not allocated in a proper

manner.

Master budget- It is a budget which includes several types of smaller-level budgets in

the company and is inclusive of cash flow forecasts, financial statements and financial plan

(What Is a Master Budget, 2020). For EECL, it is quite important that they are able to properly

estimate the requirements in an effective manner with the use of this budget.

Advantages-

With the preparation of a master budget a comprehensive overview of the organization

can be obtained. EECL can ensure that overall estimation of a business's earnings and

expenses can be made by preparing it.

Deviations and Variations in the different processes of a firm can be identified

effectively. For the management of EECL, this can result in an advantage.

Disadvantages-

Preparation of this budget is quite time-consuming for the firms. In the context of EECL

this can create a disadvantage.

The use of this budget can lead to an increase in the overall costs and expenses. Thus for

the management of EECL, this can lead towards a disadvantage.

Justification- All of these planning tools are quite helpful for the managers in order to

create plans suiting their needs and requirements. This will allow them to be able to take

decisions for the future time period.

9

greater control over the operations in an effective manner. For EECL, this can result in an

advantage.

Disadvantages-

Preparation of this budget within the companies requires the application of higher-level

of skills. For EECL this can create a disadvantage if its workers do not have these skills.

In this budget, there can be an over-allocation or under-allocation of the overheads. In

EECL this can result in a disadvantage if the overheads are not allocated in a proper

manner.

Master budget- It is a budget which includes several types of smaller-level budgets in

the company and is inclusive of cash flow forecasts, financial statements and financial plan

(What Is a Master Budget, 2020). For EECL, it is quite important that they are able to properly

estimate the requirements in an effective manner with the use of this budget.

Advantages-

With the preparation of a master budget a comprehensive overview of the organization

can be obtained. EECL can ensure that overall estimation of a business's earnings and

expenses can be made by preparing it.

Deviations and Variations in the different processes of a firm can be identified

effectively. For the management of EECL, this can result in an advantage.

Disadvantages-

Preparation of this budget is quite time-consuming for the firms. In the context of EECL

this can create a disadvantage.

The use of this budget can lead to an increase in the overall costs and expenses. Thus for

the management of EECL, this can lead towards a disadvantage.

Justification- All of these planning tools are quite helpful for the managers in order to

create plans suiting their needs and requirements. This will allow them to be able to take

decisions for the future time period.

9

TASK 4

P5: Comparison of organizations in adaptation of management accounting to solve financial

problems

Financial problem- It is a situation where creates an impact on the financial situation of

the firm. Thus it can lead towards losses for the organization (Shields and Shelleman, 2016).

Thus it is required from the companies that they are able to find a solution to the problem. Like

other organizations EECL also faces financial problems. The problems which it faces are as

follows-

Segregation of overheads- In EECL the overheads are not segregated in a proper

manner. This can result in an increase in the overall level of expenses and thus an impact

can be created on the profitability of the organization.

Mismanagement of job orders- In EECL, there is a problem which has been created in

the management of job orders. This has lead towards issues because the costs to complete

job orders has increased and thus this can create an overall impact on the level of profits.

Techniques for solving financial problems-

KPIs- These are Key Performance Indicators. They are Financial as well as Non-

Financial. Their use can be made by the managers to identify and assess the overall

performance in a highly effective manner. Their use can be made by EECL to solve the

problem of overheads as by using them it can be judged whether there has been a

substantial increase in the overheads and the techniques which can be used to reduce

them.

Balanced scorecard- In it, there is a constant monitoring by the managers on the staff

members in various departments and the tasks which are performed by them (Soderstrom,

Soderstrom and Stewart, 2017). Thus the overall performance of the organization can be

judged easily through it. In the context of EECL, it can be used so that the management is

able to solve the problem related to job orders.

Comparison between organizations-

Basis Asda Aldi

Financial problem It is facing the problem of

increase in the overall costs

It is facing the problem of

management of stock items

10

P5: Comparison of organizations in adaptation of management accounting to solve financial

problems

Financial problem- It is a situation where creates an impact on the financial situation of

the firm. Thus it can lead towards losses for the organization (Shields and Shelleman, 2016).

Thus it is required from the companies that they are able to find a solution to the problem. Like

other organizations EECL also faces financial problems. The problems which it faces are as

follows-

Segregation of overheads- In EECL the overheads are not segregated in a proper

manner. This can result in an increase in the overall level of expenses and thus an impact

can be created on the profitability of the organization.

Mismanagement of job orders- In EECL, there is a problem which has been created in

the management of job orders. This has lead towards issues because the costs to complete

job orders has increased and thus this can create an overall impact on the level of profits.

Techniques for solving financial problems-

KPIs- These are Key Performance Indicators. They are Financial as well as Non-

Financial. Their use can be made by the managers to identify and assess the overall

performance in a highly effective manner. Their use can be made by EECL to solve the

problem of overheads as by using them it can be judged whether there has been a

substantial increase in the overheads and the techniques which can be used to reduce

them.

Balanced scorecard- In it, there is a constant monitoring by the managers on the staff

members in various departments and the tasks which are performed by them (Soderstrom,

Soderstrom and Stewart, 2017). Thus the overall performance of the organization can be

judged easily through it. In the context of EECL, it can be used so that the management is

able to solve the problem related to job orders.

Comparison between organizations-

Basis Asda Aldi

Financial problem It is facing the problem of

increase in the overall costs

It is facing the problem of

management of stock items

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.