Management Accounting Analysis: Excite Entertainment Ltd Report

VerifiedAdded on 2020/10/22

|22

|6233

|496

Report

AI Summary

This report provides a detailed analysis of management accounting practices, focusing on the case of Excite Entertainment Ltd, a UK-based leisure and entertainment company. It begins with an introduction to management accounting, emphasizing its role in internal decision-making compared to financial accounting. The report then explores key concepts such as cost accounting systems, inventory management systems, and job costing systems, illustrating their application within the context of Excite Entertainment Ltd. It highlights the benefits of management accounting, including improved profitability and waste reduction. Furthermore, the report delves into the planning tools used in management accounting and their effectiveness in addressing financial problems. Finally, it concludes with a discussion of various strategies for mitigating financial challenges and ensuring the company's long-term sustainability. The report leverages information to provide a comprehensive overview of how management accounting principles are applied in a real-world business scenario.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

Section A: Understanding management accounting Systems ....................................................1

Section B: Methods used for Management Accounting Reporting ...........................................6

LO2 Marginal and absorption costing method of Excite entertainment ltd................................7

LO 3 ..............................................................................................................................................10

Planning tool used in Management Accounting ......................................................................10

LO 4 Compare the ways in which management accounting will be used for reducing financial

problems....................................................................................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

Section A: Understanding management accounting Systems ....................................................1

Section B: Methods used for Management Accounting Reporting ...........................................6

LO2 Marginal and absorption costing method of Excite entertainment ltd................................7

LO 3 ..............................................................................................................................................10

Planning tool used in Management Accounting ......................................................................10

LO 4 Compare the ways in which management accounting will be used for reducing financial

problems....................................................................................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting is process that is used by the managers to prepared a report on

the basis of gathering information regarding to statistical and financial matters of the company.

This management helps the company to take longer and shorter decision for future growth and

perspective. To manage the accounts, it provides the stability to use the resource and make actual

and estimated budget to invest in any project or can take risk in market to achieve more

probability in business (Renz, 2016). Management accounting is prepared on the basis of

operational activities which can in terms of raw material utilized, inventory management, cash

flow budget and any other activities which help business to sustain their stability in market.

Present report is based on Excite Entertainment Ltd. which is leisure and entertainment industry

in UK. It conducts various promotional activities relating to concerts and festivals in UK. So to

mange their accounting department various facilities are required to address their effective and

sustainability in the market (Messner, 2016).

Report will include the difference between management accounting and financial

accounting and its various accounting concept and its different accounting reports. It also

includes the costs which are allocated in the business to identify the cost expenditure and income

in the management of business and its befits to be incurred in this system. Further it includes The

planning tools used in management accounting and its effectiveness in the business. Lastly the

report ends up with different ways to deal with financial problems and other relevant matters in

the organisation.

LO 1

Section A: Understanding management accounting Systems

Excite entertainment Ltd is one of the leading company engaged in promotion of their

concerts and festivals at different location throughout the United Kingdom. To manage their

business into large scale they have to organise their accounting systems in a systematic and

accurate manner (Management Accounting – Meaning, Advantages and Limitation, 2019). Thus,

management accounting is the process to manage the data and information of the company

internally so that they can take an appropriate decision for the growth of the business. Financial

accounting is that process which manages the finance of the business and transaction recorded

1

Management accounting is process that is used by the managers to prepared a report on

the basis of gathering information regarding to statistical and financial matters of the company.

This management helps the company to take longer and shorter decision for future growth and

perspective. To manage the accounts, it provides the stability to use the resource and make actual

and estimated budget to invest in any project or can take risk in market to achieve more

probability in business (Renz, 2016). Management accounting is prepared on the basis of

operational activities which can in terms of raw material utilized, inventory management, cash

flow budget and any other activities which help business to sustain their stability in market.

Present report is based on Excite Entertainment Ltd. which is leisure and entertainment industry

in UK. It conducts various promotional activities relating to concerts and festivals in UK. So to

mange their accounting department various facilities are required to address their effective and

sustainability in the market (Messner, 2016).

Report will include the difference between management accounting and financial

accounting and its various accounting concept and its different accounting reports. It also

includes the costs which are allocated in the business to identify the cost expenditure and income

in the management of business and its befits to be incurred in this system. Further it includes The

planning tools used in management accounting and its effectiveness in the business. Lastly the

report ends up with different ways to deal with financial problems and other relevant matters in

the organisation.

LO 1

Section A: Understanding management accounting Systems

Excite entertainment Ltd is one of the leading company engaged in promotion of their

concerts and festivals at different location throughout the United Kingdom. To manage their

business into large scale they have to organise their accounting systems in a systematic and

accurate manner (Management Accounting – Meaning, Advantages and Limitation, 2019). Thus,

management accounting is the process to manage the data and information of the company

internally so that they can take an appropriate decision for the growth of the business. Financial

accounting is that process which manages the finance of the business and transaction recorded

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

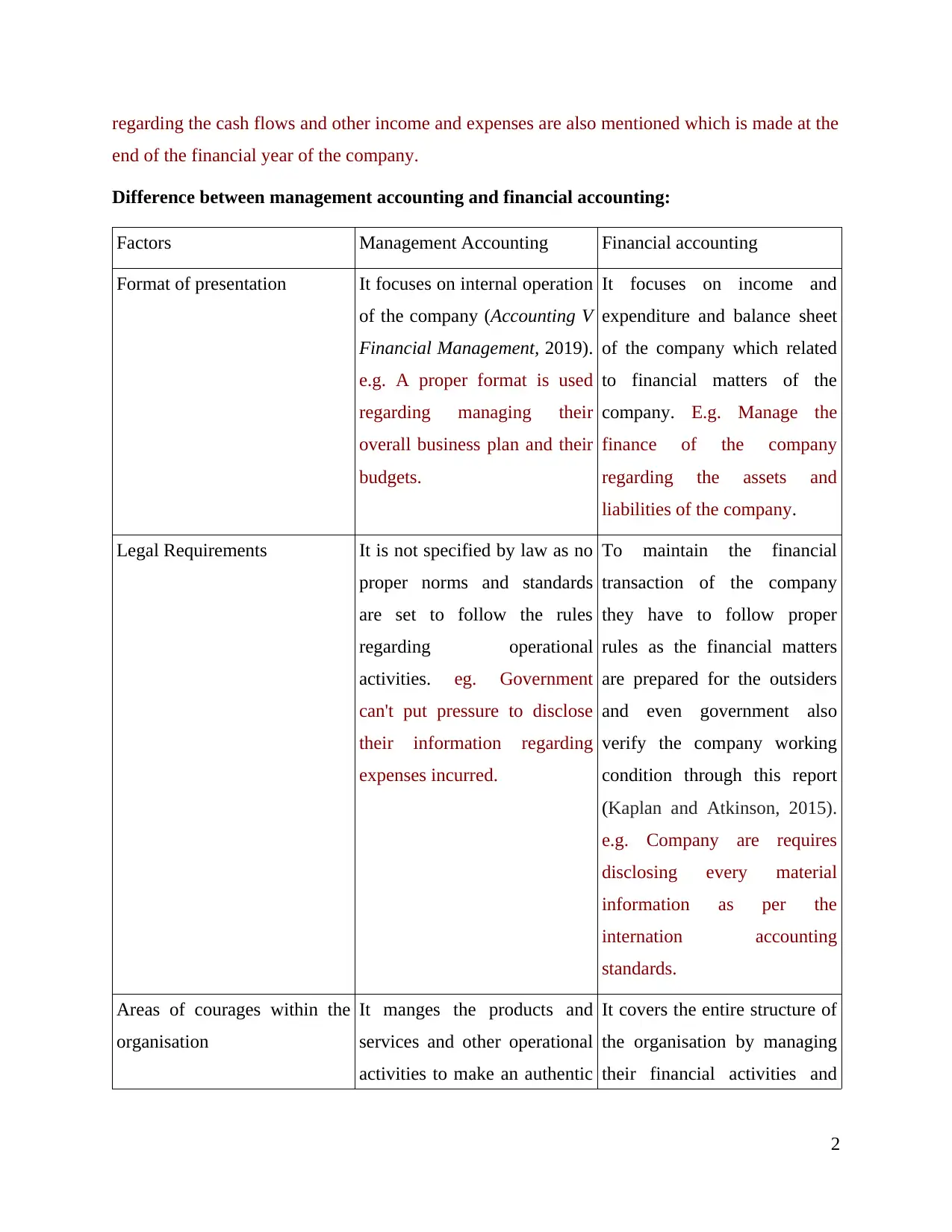

regarding the cash flows and other income and expenses are also mentioned which is made at the

end of the financial year of the company.

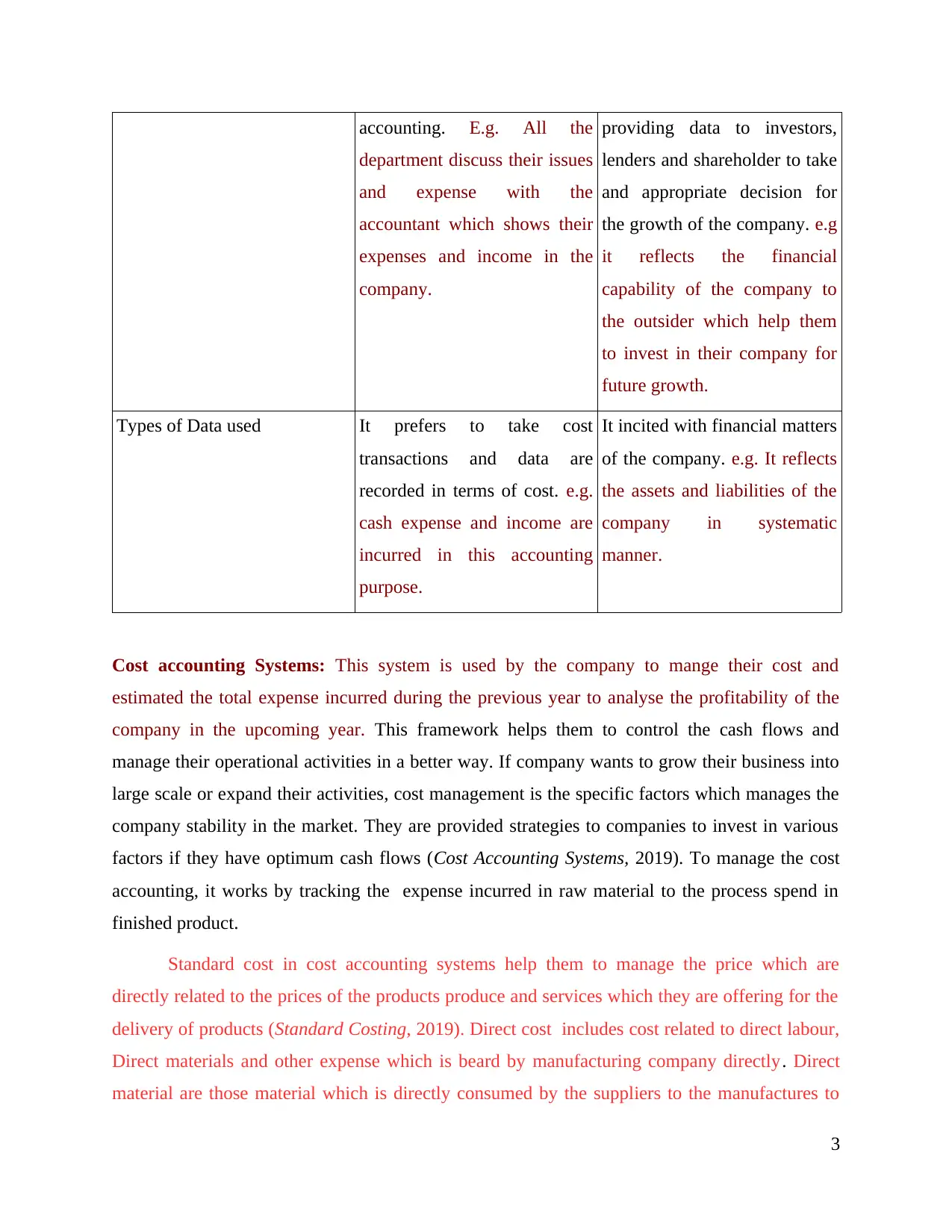

Difference between management accounting and financial accounting:

Factors Management Accounting Financial accounting

Format of presentation It focuses on internal operation

of the company (Accounting V

Financial Management, 2019).

e.g. A proper format is used

regarding managing their

overall business plan and their

budgets.

It focuses on income and

expenditure and balance sheet

of the company which related

to financial matters of the

company. E.g. Manage the

finance of the company

regarding the assets and

liabilities of the company.

Legal Requirements It is not specified by law as no

proper norms and standards

are set to follow the rules

regarding operational

activities. eg. Government

can't put pressure to disclose

their information regarding

expenses incurred.

To maintain the financial

transaction of the company

they have to follow proper

rules as the financial matters

are prepared for the outsiders

and even government also

verify the company working

condition through this report

(Kaplan and Atkinson, 2015).

e.g. Company are requires

disclosing every material

information as per the

internation accounting

standards.

Areas of courages within the

organisation

It manges the products and

services and other operational

activities to make an authentic

It covers the entire structure of

the organisation by managing

their financial activities and

2

end of the financial year of the company.

Difference between management accounting and financial accounting:

Factors Management Accounting Financial accounting

Format of presentation It focuses on internal operation

of the company (Accounting V

Financial Management, 2019).

e.g. A proper format is used

regarding managing their

overall business plan and their

budgets.

It focuses on income and

expenditure and balance sheet

of the company which related

to financial matters of the

company. E.g. Manage the

finance of the company

regarding the assets and

liabilities of the company.

Legal Requirements It is not specified by law as no

proper norms and standards

are set to follow the rules

regarding operational

activities. eg. Government

can't put pressure to disclose

their information regarding

expenses incurred.

To maintain the financial

transaction of the company

they have to follow proper

rules as the financial matters

are prepared for the outsiders

and even government also

verify the company working

condition through this report

(Kaplan and Atkinson, 2015).

e.g. Company are requires

disclosing every material

information as per the

internation accounting

standards.

Areas of courages within the

organisation

It manges the products and

services and other operational

activities to make an authentic

It covers the entire structure of

the organisation by managing

their financial activities and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting. E.g. All the

department discuss their issues

and expense with the

accountant which shows their

expenses and income in the

company.

providing data to investors,

lenders and shareholder to take

and appropriate decision for

the growth of the company. e.g

it reflects the financial

capability of the company to

the outsider which help them

to invest in their company for

future growth.

Types of Data used It prefers to take cost

transactions and data are

recorded in terms of cost. e.g.

cash expense and income are

incurred in this accounting

purpose.

It incited with financial matters

of the company. e.g. It reflects

the assets and liabilities of the

company in systematic

manner.

Cost accounting Systems: This system is used by the company to mange their cost and

estimated the total expense incurred during the previous year to analyse the profitability of the

company in the upcoming year. This framework helps them to control the cash flows and

manage their operational activities in a better way. If company wants to grow their business into

large scale or expand their activities, cost management is the specific factors which manages the

company stability in the market. They are provided strategies to companies to invest in various

factors if they have optimum cash flows (Cost Accounting Systems, 2019). To manage the cost

accounting, it works by tracking the expense incurred in raw material to the process spend in

finished product.

Standard cost in cost accounting systems help them to manage the price which are

directly related to the prices of the products produce and services which they are offering for the

delivery of products (Standard Costing, 2019). Direct cost includes cost related to direct labour,

Direct materials and other expense which is beard by manufacturing company directly. Direct

material are those material which is directly consumed by the suppliers to the manufactures to

3

department discuss their issues

and expense with the

accountant which shows their

expenses and income in the

company.

providing data to investors,

lenders and shareholder to take

and appropriate decision for

the growth of the company. e.g

it reflects the financial

capability of the company to

the outsider which help them

to invest in their company for

future growth.

Types of Data used It prefers to take cost

transactions and data are

recorded in terms of cost. e.g.

cash expense and income are

incurred in this accounting

purpose.

It incited with financial matters

of the company. e.g. It reflects

the assets and liabilities of the

company in systematic

manner.

Cost accounting Systems: This system is used by the company to mange their cost and

estimated the total expense incurred during the previous year to analyse the profitability of the

company in the upcoming year. This framework helps them to control the cash flows and

manage their operational activities in a better way. If company wants to grow their business into

large scale or expand their activities, cost management is the specific factors which manages the

company stability in the market. They are provided strategies to companies to invest in various

factors if they have optimum cash flows (Cost Accounting Systems, 2019). To manage the cost

accounting, it works by tracking the expense incurred in raw material to the process spend in

finished product.

Standard cost in cost accounting systems help them to manage the price which are

directly related to the prices of the products produce and services which they are offering for the

delivery of products (Standard Costing, 2019). Direct cost includes cost related to direct labour,

Direct materials and other expense which is beard by manufacturing company directly. Direct

material are those material which is directly consumed by the suppliers to the manufactures to

3

produce such products. Direct expenses are such expense which directly charged on respect of

volumes of the cots incurred by the company. Variable cost are such cost which changes as per

changes in the prices of the products. It decreases in respect of decrease in prices or cost and

sxame increases with increases in cost. Company makes estimated cost before they deal in such

activities and after assembling all the matter they compare the actual cost with the estimated cost

which company bear at the time of production of products or services.

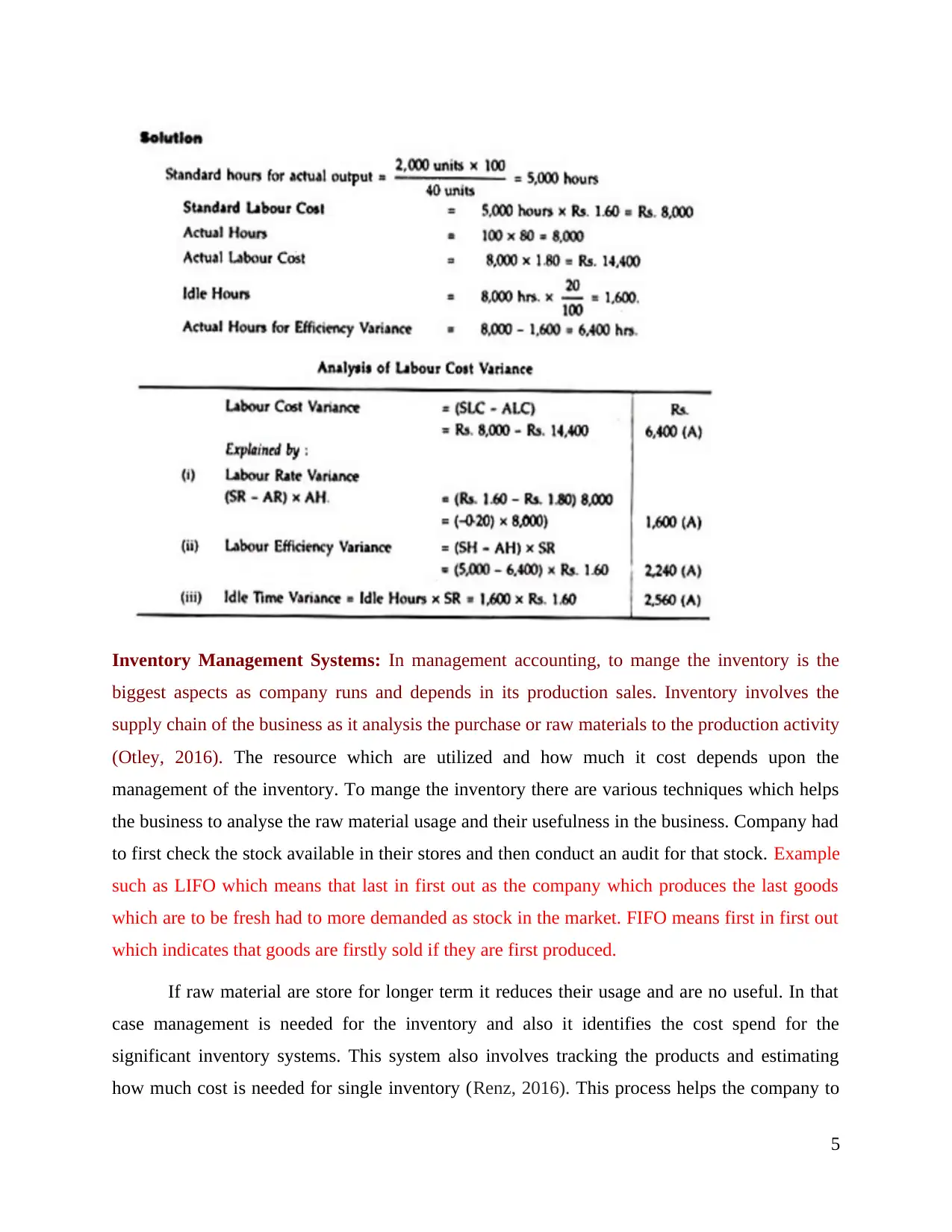

Steps used in standard accounting as firstly to set the standard in which the cost are

estimated or predetermined which is based on the targets of the company. e.g. in this the costs is

set for labour cost as 8000. Secondly to measure it with actual result as the cost which is set to be

measured with the actual cost which is disclosed. E.g. the actual cost arise is 8000.after

comparing both the results i.e. actuals and estimated the results arise the total cost which is

managed by the company. e.g. the actual labour cost is 14,400. After getting results the actual

results arises between the actuals and estimated cost is the variances. e.g. 6400 hrs. which is the

actual hours for efficiency variance. After that calculation, analyse the various from the available

data which gets the results in terms of cost of the company. After that various other factors which

is to incurred at the time of production or any process is also to be calculated which determined

during the work committed. Further lastly after gathering all the information calculated the

variance and make report regarding the standard costing of a particular product or management

of the company.

Examples:

4

volumes of the cots incurred by the company. Variable cost are such cost which changes as per

changes in the prices of the products. It decreases in respect of decrease in prices or cost and

sxame increases with increases in cost. Company makes estimated cost before they deal in such

activities and after assembling all the matter they compare the actual cost with the estimated cost

which company bear at the time of production of products or services.

Steps used in standard accounting as firstly to set the standard in which the cost are

estimated or predetermined which is based on the targets of the company. e.g. in this the costs is

set for labour cost as 8000. Secondly to measure it with actual result as the cost which is set to be

measured with the actual cost which is disclosed. E.g. the actual cost arise is 8000.after

comparing both the results i.e. actuals and estimated the results arise the total cost which is

managed by the company. e.g. the actual labour cost is 14,400. After getting results the actual

results arises between the actuals and estimated cost is the variances. e.g. 6400 hrs. which is the

actual hours for efficiency variance. After that calculation, analyse the various from the available

data which gets the results in terms of cost of the company. After that various other factors which

is to incurred at the time of production or any process is also to be calculated which determined

during the work committed. Further lastly after gathering all the information calculated the

variance and make report regarding the standard costing of a particular product or management

of the company.

Examples:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory Management Systems: In management accounting, to mange the inventory is the

biggest aspects as company runs and depends in its production sales. Inventory involves the

supply chain of the business as it analysis the purchase or raw materials to the production activity

(Otley, 2016). The resource which are utilized and how much it cost depends upon the

management of the inventory. To mange the inventory there are various techniques which helps

the business to analyse the raw material usage and their usefulness in the business. Company had

to first check the stock available in their stores and then conduct an audit for that stock. Example

such as LIFO which means that last in first out as the company which produces the last goods

which are to be fresh had to more demanded as stock in the market. FIFO means first in first out

which indicates that goods are firstly sold if they are first produced.

If raw material are store for longer term it reduces their usage and are no useful. In that

case management is needed for the inventory and also it identifies the cost spend for the

significant inventory systems. This system also involves tracking the products and estimating

how much cost is needed for single inventory (Renz, 2016). This process helps the company to

5

biggest aspects as company runs and depends in its production sales. Inventory involves the

supply chain of the business as it analysis the purchase or raw materials to the production activity

(Otley, 2016). The resource which are utilized and how much it cost depends upon the

management of the inventory. To mange the inventory there are various techniques which helps

the business to analyse the raw material usage and their usefulness in the business. Company had

to first check the stock available in their stores and then conduct an audit for that stock. Example

such as LIFO which means that last in first out as the company which produces the last goods

which are to be fresh had to more demanded as stock in the market. FIFO means first in first out

which indicates that goods are firstly sold if they are first produced.

If raw material are store for longer term it reduces their usage and are no useful. In that

case management is needed for the inventory and also it identifies the cost spend for the

significant inventory systems. This system also involves tracking the products and estimating

how much cost is needed for single inventory (Renz, 2016). This process helps the company to

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manage their productivity in the market and also take appropriate decision for taking risk in the

business.

Job Costing systems: It is the system which is involves the process of accumulating the

information in respect of cost assigned for specific products and services. This involves costing

of each cost recorded in terms of direct labour, Direct material and manufacturing overhead in

the manufacturing company and also helps them to assigned various cost in respect for future

perspective (Maas, Schaltegger and Crutzen, 2016). Usually this system is implemented on

individual to identify the unit of output spent in producing a product in the company.

Thus, it involves a separate record for each items produce or each individual person

worked to achieve that targets or special order which are passed by company requires the cost

procedure to be systematically mannered (Messner, 2016). Thus, in simple words job costing

method helps the companies to records and track the cost of manufacturing engaged in job rather

than the process which is used by the company to produce a product.

Benefits of Management Accounting Systems:

To manage the accounting concept there are various benefits which helps companies to

stable their business in the emerging world and stand the chance to face the risk without affecting

their reputation and goodwill of the company. First benefits is related to identifying the

profitability in the business. To manage the accounts and other operational activities of the

company this is the major benefits to analyse the company stability and integrity to produce

more products in the market (Quattrone, 2016). If company manage their internal activities in the

systematics and effective manner and clear their matter which can raise the defects and damages

in the near futures than company can raise more profits in the next year.

The second benefits is regarding controlling the wastage from the products. As

accounting management manages the internal operational activities so through this process is

helps them to reuse or save the products from wastage. They can control and estimates the results

through which the wastages occurs (Chenhall and Moers, 2015). They can coordinate with the

other department and also analyse the results relating to the matters which occurring losses in the

company regarding to that department.

6

business.

Job Costing systems: It is the system which is involves the process of accumulating the

information in respect of cost assigned for specific products and services. This involves costing

of each cost recorded in terms of direct labour, Direct material and manufacturing overhead in

the manufacturing company and also helps them to assigned various cost in respect for future

perspective (Maas, Schaltegger and Crutzen, 2016). Usually this system is implemented on

individual to identify the unit of output spent in producing a product in the company.

Thus, it involves a separate record for each items produce or each individual person

worked to achieve that targets or special order which are passed by company requires the cost

procedure to be systematically mannered (Messner, 2016). Thus, in simple words job costing

method helps the companies to records and track the cost of manufacturing engaged in job rather

than the process which is used by the company to produce a product.

Benefits of Management Accounting Systems:

To manage the accounting concept there are various benefits which helps companies to

stable their business in the emerging world and stand the chance to face the risk without affecting

their reputation and goodwill of the company. First benefits is related to identifying the

profitability in the business. To manage the accounts and other operational activities of the

company this is the major benefits to analyse the company stability and integrity to produce

more products in the market (Quattrone, 2016). If company manage their internal activities in the

systematics and effective manner and clear their matter which can raise the defects and damages

in the near futures than company can raise more profits in the next year.

The second benefits is regarding controlling the wastage from the products. As

accounting management manages the internal operational activities so through this process is

helps them to reuse or save the products from wastage. They can control and estimates the results

through which the wastages occurs (Chenhall and Moers, 2015). They can coordinate with the

other department and also analyse the results relating to the matters which occurring losses in the

company regarding to that department.

6

The Third benefits is related to Organising the work schedule and the persons are

responsible for their own defects. As in managing the accounts, everyone is assigned to assist

and complete the specific work and they are not responsible for the other work to be completed if

they are not assigned to them (Bromwich and Scapens, 2016). So if any mistakes occurs the

person is easily identifies and they are responsible for the damages which incurred in managing

the accounts or conducting any fraud in manipulating the data and information.

Section B: Methods used for Management Accounting Reporting

Different types of managerial accounting reports -

Managerial accounting reports helps the companies to evaluate their performance and

budgets in the upcoming year which can be analysed in appropriate manner. This report helps the

companies to take decision and analyse the factors which is most expensive and which bring

losses to the company. There are various types of managerial accounting reports.

11 Budget: Budgets is a tool that uses by company managers to plan and execute them in

effective way. Time and money is the biggest aspect which helps company to maintain

stability in market and this can only be achieved by making a proper budget (Ax and

Greve, 2017). Report involves the proper and authentic transaction which describes the

company working structure and it can only be achieved by adopting the budget technique.

11 Performance report: This report is prepared to analyse the budget and performance of the

line managers and employees working in the business. This report is prepared so that

employees who engages more time and bring more productivity in the company are

appreciated and motivated through appraisal and incentives (Nitzl, 2016). Report includes

the list of employees and their incentives to be given under the profits identified through

them in company internal matters.

11 Cost Reports: It helps the company to manage their resource utilized in manufacturing

the products and services (Malina, 2018). In this report it includes the cost spend in raw

materials and payment to labour and also added other cost which analyses the complete

review of the company. It helps the company to plan their future plans and also manages

their cost to expand their activities in near future.

The information presented should be accurate, relevant to user so that they can easily

finance and take interest in the internal matters of the company. As company can easily run if

7

responsible for their own defects. As in managing the accounts, everyone is assigned to assist

and complete the specific work and they are not responsible for the other work to be completed if

they are not assigned to them (Bromwich and Scapens, 2016). So if any mistakes occurs the

person is easily identifies and they are responsible for the damages which incurred in managing

the accounts or conducting any fraud in manipulating the data and information.

Section B: Methods used for Management Accounting Reporting

Different types of managerial accounting reports -

Managerial accounting reports helps the companies to evaluate their performance and

budgets in the upcoming year which can be analysed in appropriate manner. This report helps the

companies to take decision and analyse the factors which is most expensive and which bring

losses to the company. There are various types of managerial accounting reports.

11 Budget: Budgets is a tool that uses by company managers to plan and execute them in

effective way. Time and money is the biggest aspect which helps company to maintain

stability in market and this can only be achieved by making a proper budget (Ax and

Greve, 2017). Report involves the proper and authentic transaction which describes the

company working structure and it can only be achieved by adopting the budget technique.

11 Performance report: This report is prepared to analyse the budget and performance of the

line managers and employees working in the business. This report is prepared so that

employees who engages more time and bring more productivity in the company are

appreciated and motivated through appraisal and incentives (Nitzl, 2016). Report includes

the list of employees and their incentives to be given under the profits identified through

them in company internal matters.

11 Cost Reports: It helps the company to manage their resource utilized in manufacturing

the products and services (Malina, 2018). In this report it includes the cost spend in raw

materials and payment to labour and also added other cost which analyses the complete

review of the company. It helps the company to plan their future plans and also manages

their cost to expand their activities in near future.

The information presented should be accurate, relevant to user so that they can easily

finance and take interest in the internal matters of the company. As company can easily run if

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

shareholder, investors and lender have interest in their internal matter and they can provide

finance to the company to maintain their reputation in the market. As government can also

demand the company financial management report to identify the stability of the company and

how they run to achieve targets (van Helden and Uddin, 2016). They have to manage and present

their report in the systematic manner as it can be demand at any time. Even customers can also

demand their report and it's the duty of the mangers team to keep them up to date and also timely

rectify the errors if any incurred. Its advantages is that to provide timely details in internal factors

they can prepare the financial statement and also examine the budget to be used for internals

growth of the company. For external stakeholder is helps to know the status of the company and

their working criteria to secure their funds in the company.

Evaluating the management accounting Systems and management accounting report

within Excite Entertainment Ltd.

In Excite Entertainment Ltd. the accounting concepts helps them, to plan their activities

in a systematic and accurate manner. They can plan their internal activities and operational

process to gain more profitability in their business. They plan their budget and other expense

which company may incurred in the future and they can estimate the cost incurred which help to

take appropriate decision. The report is prepared in systematic manner with this planning and the

investors can easily invest in the business for future growth (Honggowati and et.al., 2017). To

commit a proper report it involves planning from all the department and their technique which

they used to achieve goal. As there are various advantages for planning tools as it helps company

to analyst the cost incurred and earned and can take risk in the business but the disadvantages is

that due to incorrect planning it results in huge losses to the company strategy to achieve targets

and they can be presentable to the investors to invest in their company.

LO2 Marginal and absorption costing method of Excite entertainment ltd.

Absorption costing basically indicates that all the manufacturing costs has to assigned to

the units produced by the company that is cost of the finished goods include the all cost of direct

materials, direct labour, variable manufacturing overheads and fixed manufacturing overhead.

This cost is generally required for the external financial reporting and for the income tax

reporting by the company.

Advantages:

8

finance to the company to maintain their reputation in the market. As government can also

demand the company financial management report to identify the stability of the company and

how they run to achieve targets (van Helden and Uddin, 2016). They have to manage and present

their report in the systematic manner as it can be demand at any time. Even customers can also

demand their report and it's the duty of the mangers team to keep them up to date and also timely

rectify the errors if any incurred. Its advantages is that to provide timely details in internal factors

they can prepare the financial statement and also examine the budget to be used for internals

growth of the company. For external stakeholder is helps to know the status of the company and

their working criteria to secure their funds in the company.

Evaluating the management accounting Systems and management accounting report

within Excite Entertainment Ltd.

In Excite Entertainment Ltd. the accounting concepts helps them, to plan their activities

in a systematic and accurate manner. They can plan their internal activities and operational

process to gain more profitability in their business. They plan their budget and other expense

which company may incurred in the future and they can estimate the cost incurred which help to

take appropriate decision. The report is prepared in systematic manner with this planning and the

investors can easily invest in the business for future growth (Honggowati and et.al., 2017). To

commit a proper report it involves planning from all the department and their technique which

they used to achieve goal. As there are various advantages for planning tools as it helps company

to analyst the cost incurred and earned and can take risk in the business but the disadvantages is

that due to incorrect planning it results in huge losses to the company strategy to achieve targets

and they can be presentable to the investors to invest in their company.

LO2 Marginal and absorption costing method of Excite entertainment ltd.

Absorption costing basically indicates that all the manufacturing costs has to assigned to

the units produced by the company that is cost of the finished goods include the all cost of direct

materials, direct labour, variable manufacturing overheads and fixed manufacturing overhead.

This cost is generally required for the external financial reporting and for the income tax

reporting by the company.

Advantages:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It takes in account all the cost that is fixed overheads as well as variable overhead costs.

It is the most suitable method for preparation of accounts to ascertain actual financial

performance of the business.

It shows the decreased cost of sales and increases revenue of the company than the

marginal or variable costing especially when the inventory level is rising.

Disadvantage:

This method cannot be used as effective monitoring tool to evaluate the profitability of

the business

in this the cost is considered the both fixed and variable cost of product this method

cannot be used for further decision making and planning like budgeting and forecasting.

The profits for period are required to adjusted for under and over absorption of the fixed

cost.

Marginal costing is that cost technique in which only the variable cost is charged on the

units produced while the fixed cots for the particular period is completely written off against the

contribution. The increase or decrease in the cost of producing one more unit is also referred to

the marginal costing.

Advantages:

It facilitates short teem decision making process.

Cost control can be used in better and effective way by putting more efforts in

maintaining the consistent marginal cost as fixed cost which is assumed to e constant.

There is no requirement of calculating the overhead absorption rate which helps in

making the calculations easy

It avoids complication of under or over absorption of overheads'

inventories carried forwards to next year does not include the elements of current periods

foxed overheads,

Disadvantages:

It ignores fixed costs of products

9

It is the most suitable method for preparation of accounts to ascertain actual financial

performance of the business.

It shows the decreased cost of sales and increases revenue of the company than the

marginal or variable costing especially when the inventory level is rising.

Disadvantage:

This method cannot be used as effective monitoring tool to evaluate the profitability of

the business

in this the cost is considered the both fixed and variable cost of product this method

cannot be used for further decision making and planning like budgeting and forecasting.

The profits for period are required to adjusted for under and over absorption of the fixed

cost.

Marginal costing is that cost technique in which only the variable cost is charged on the

units produced while the fixed cots for the particular period is completely written off against the

contribution. The increase or decrease in the cost of producing one more unit is also referred to

the marginal costing.

Advantages:

It facilitates short teem decision making process.

Cost control can be used in better and effective way by putting more efforts in

maintaining the consistent marginal cost as fixed cost which is assumed to e constant.

There is no requirement of calculating the overhead absorption rate which helps in

making the calculations easy

It avoids complication of under or over absorption of overheads'

inventories carried forwards to next year does not include the elements of current periods

foxed overheads,

Disadvantages:

It ignores fixed costs of products

9

it fails to recognize the fixed cost become variable in long run

It makes the use of the historical data while decision by management related to the future

events.

It assumes constant total fixed costs, per unit sales price and variable cost but in reality

they all vary which leads to inappropriate result of financial position of the business.

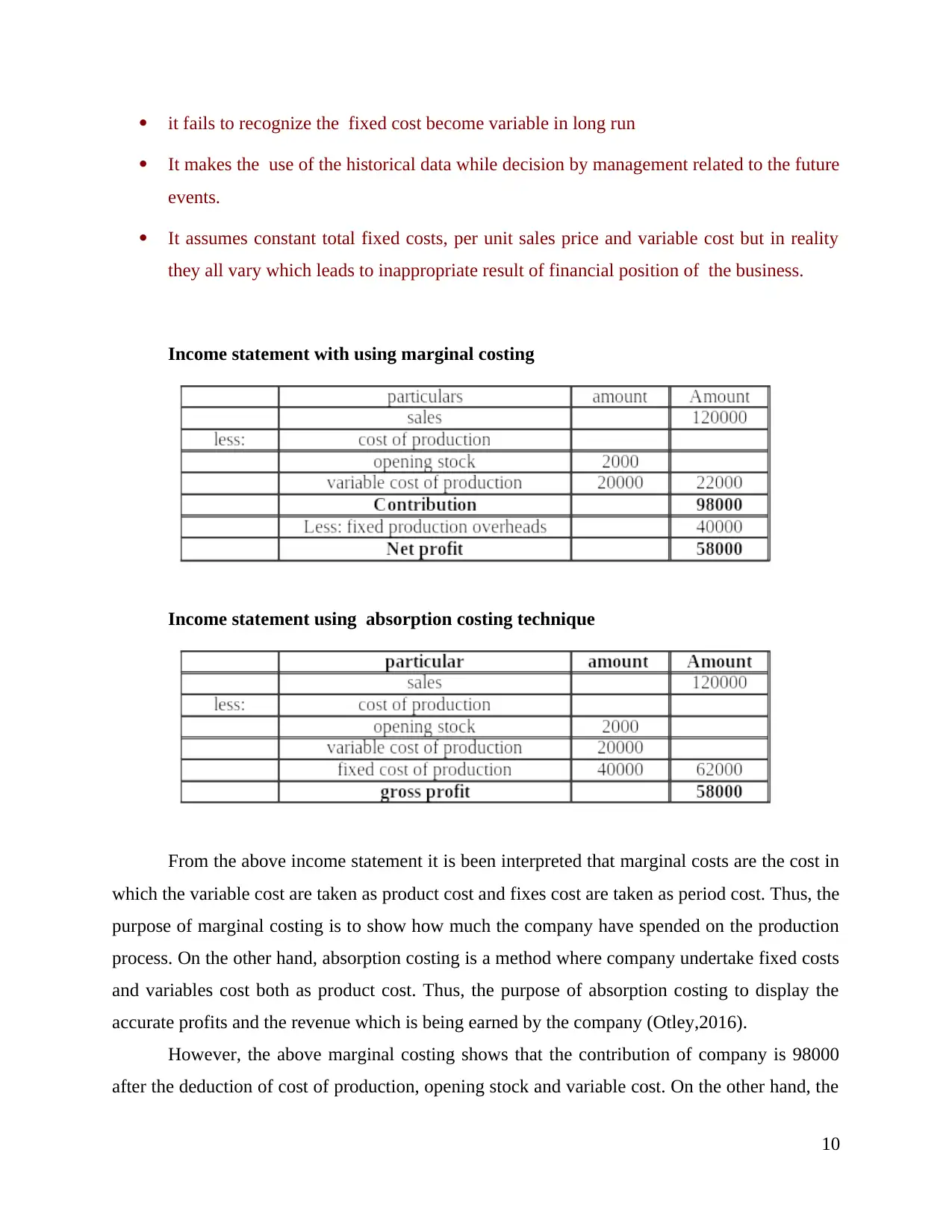

Income statement with using marginal costing

Income statement using absorption costing technique

From the above income statement it is been interpreted that marginal costs are the cost in

which the variable cost are taken as product cost and fixes cost are taken as period cost. Thus, the

purpose of marginal costing is to show how much the company have spended on the production

process. On the other hand, absorption costing is a method where company undertake fixed costs

and variables cost both as product cost. Thus, the purpose of absorption costing to display the

accurate profits and the revenue which is being earned by the company (Otley,2016).

However, the above marginal costing shows that the contribution of company is 98000

after the deduction of cost of production, opening stock and variable cost. On the other hand, the

10

It makes the use of the historical data while decision by management related to the future

events.

It assumes constant total fixed costs, per unit sales price and variable cost but in reality

they all vary which leads to inappropriate result of financial position of the business.

Income statement with using marginal costing

Income statement using absorption costing technique

From the above income statement it is been interpreted that marginal costs are the cost in

which the variable cost are taken as product cost and fixes cost are taken as period cost. Thus, the

purpose of marginal costing is to show how much the company have spended on the production

process. On the other hand, absorption costing is a method where company undertake fixed costs

and variables cost both as product cost. Thus, the purpose of absorption costing to display the

accurate profits and the revenue which is being earned by the company (Otley,2016).

However, the above marginal costing shows that the contribution of company is 98000

after the deduction of cost of production, opening stock and variable cost. On the other hand, the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.