Management Accounting Report for Excite Entertainment Ltd Analysis

VerifiedAdded on 2023/01/13

|17

|4491

|45

Report

AI Summary

This management accounting report provides a comprehensive analysis of the financial strategies and techniques applicable to Excite Entertainment Ltd., a UK-based company in the entertainment and leisure sector. The report begins with an introduction to management accounting and differentiates it from financial accounting, then delves into various cost accounting systems including cost accounting, inventory management, and job costing systems. It further explores the benefits of management accounting systems and different types of marginal accounting reports. The report also addresses the importance of accurate and timely information in management accounting, and how management accounting systems can be integrated into operational processes. Task 2 involves calculating costs using marginal and absorption costing techniques to prepare an income statement, followed by a discussion of planning tools used for budgetary control. Finally, the report compares how organizations adapt management accounting systems to respond to financial problems. The report concludes with a summary of the key findings and provides references to the sources used.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(a) Different between Management accounting and Financial Accounting................................1

(b) Cost accounting system.........................................................................................................2

(c) Inventory management systems.............................................................................................2

(d) Job costing systems...............................................................................................................3

(e) Benefits of management accounting systems........................................................................3

(a) Different types of marginal accounting reports.....................................................................3

(b) Explain why information presented should be accurate, relevant to the use, reliable up to

date and timely............................................................................................................................4

(c) Evaluate that how management accounting systems and management accounting reporting

should be integrated organisation operational process................................................................4

TASK 2............................................................................................................................................5

Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs...........................................................................................5

TASK 3............................................................................................................................................6

Advantages and disadvantages of different types of planning tools used for budgetary control6

TASK 4............................................................................................................................................9

Compare how organisations are adapting management accounting systems to respond

financial problems.......................................................................................................................9

CONCLUSION ...............................................................................................................................9

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(a) Different between Management accounting and Financial Accounting................................1

(b) Cost accounting system.........................................................................................................2

(c) Inventory management systems.............................................................................................2

(d) Job costing systems...............................................................................................................3

(e) Benefits of management accounting systems........................................................................3

(a) Different types of marginal accounting reports.....................................................................3

(b) Explain why information presented should be accurate, relevant to the use, reliable up to

date and timely............................................................................................................................4

(c) Evaluate that how management accounting systems and management accounting reporting

should be integrated organisation operational process................................................................4

TASK 2............................................................................................................................................5

Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs...........................................................................................5

TASK 3............................................................................................................................................6

Advantages and disadvantages of different types of planning tools used for budgetary control6

TASK 4............................................................................................................................................9

Compare how organisations are adapting management accounting systems to respond

financial problems.......................................................................................................................9

CONCLUSION ...............................................................................................................................9

REFERENCES................................................................................................................................9

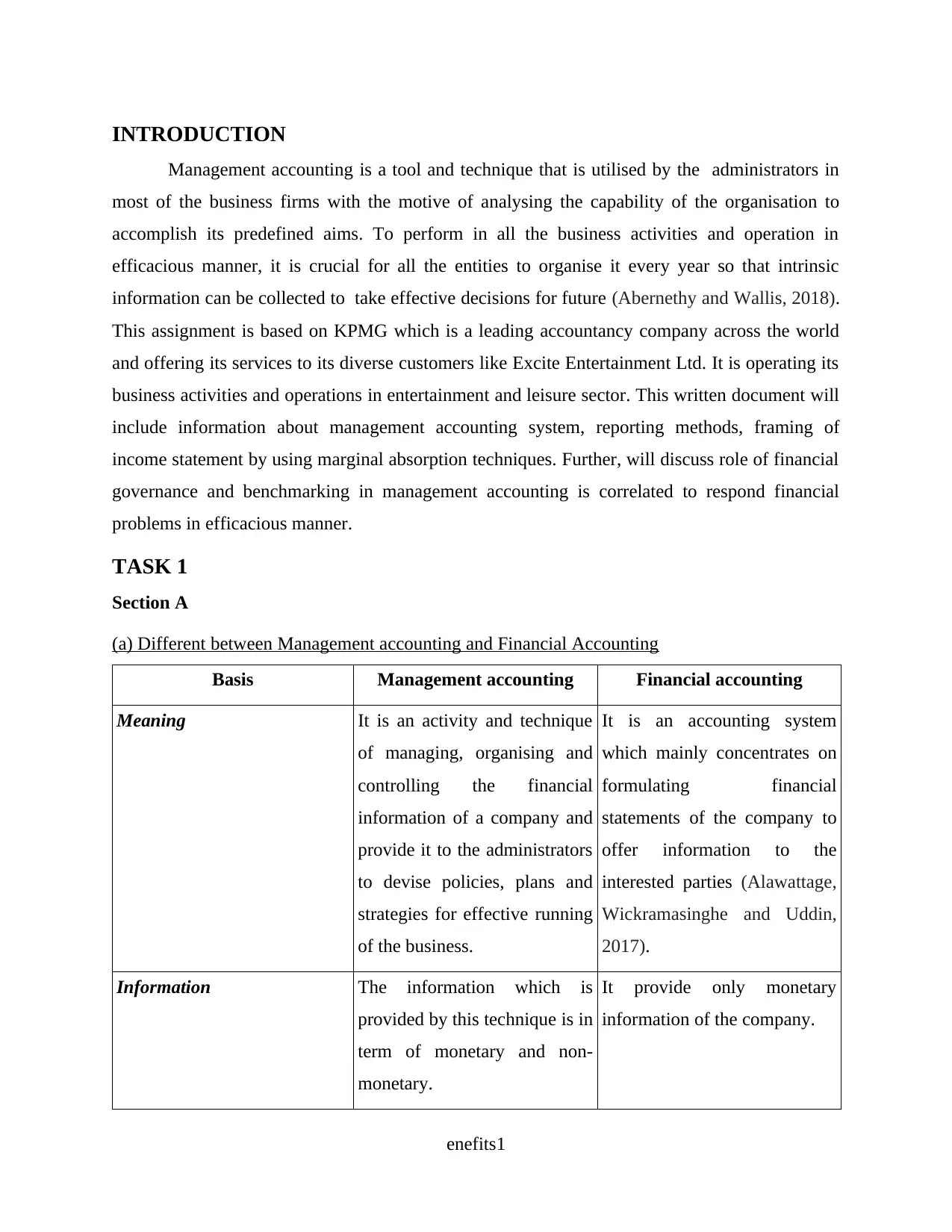

INTRODUCTION

Management accounting is a tool and technique that is utilised by the administrators in

most of the business firms with the motive of analysing the capability of the organisation to

accomplish its predefined aims. To perform in all the business activities and operation in

efficacious manner, it is crucial for all the entities to organise it every year so that intrinsic

information can be collected to take effective decisions for future (Abernethy and Wallis, 2018).

This assignment is based on KPMG which is a leading accountancy company across the world

and offering its services to its diverse customers like Excite Entertainment Ltd. It is operating its

business activities and operations in entertainment and leisure sector. This written document will

include information about management accounting system, reporting methods, framing of

income statement by using marginal absorption techniques. Further, will discuss role of financial

governance and benchmarking in management accounting is correlated to respond financial

problems in efficacious manner.

TASK 1

Section A

(a) Different between Management accounting and Financial Accounting

Basis Management accounting Financial accounting

Meaning It is an activity and technique

of managing, organising and

controlling the financial

information of a company and

provide it to the administrators

to devise policies, plans and

strategies for effective running

of the business.

It is an accounting system

which mainly concentrates on

formulating financial

statements of the company to

offer information to the

interested parties (Alawattage,

Wickramasinghe and Uddin,

2017).

Information The information which is

provided by this technique is in

term of monetary and non-

monetary.

It provide only monetary

information of the company.

enefits1

Management accounting is a tool and technique that is utilised by the administrators in

most of the business firms with the motive of analysing the capability of the organisation to

accomplish its predefined aims. To perform in all the business activities and operation in

efficacious manner, it is crucial for all the entities to organise it every year so that intrinsic

information can be collected to take effective decisions for future (Abernethy and Wallis, 2018).

This assignment is based on KPMG which is a leading accountancy company across the world

and offering its services to its diverse customers like Excite Entertainment Ltd. It is operating its

business activities and operations in entertainment and leisure sector. This written document will

include information about management accounting system, reporting methods, framing of

income statement by using marginal absorption techniques. Further, will discuss role of financial

governance and benchmarking in management accounting is correlated to respond financial

problems in efficacious manner.

TASK 1

Section A

(a) Different between Management accounting and Financial Accounting

Basis Management accounting Financial accounting

Meaning It is an activity and technique

of managing, organising and

controlling the financial

information of a company and

provide it to the administrators

to devise policies, plans and

strategies for effective running

of the business.

It is an accounting system

which mainly concentrates on

formulating financial

statements of the company to

offer information to the

interested parties (Alawattage,

Wickramasinghe and Uddin,

2017).

Information The information which is

provided by this technique is in

term of monetary and non-

monetary.

It provide only monetary

information of the company.

enefits1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

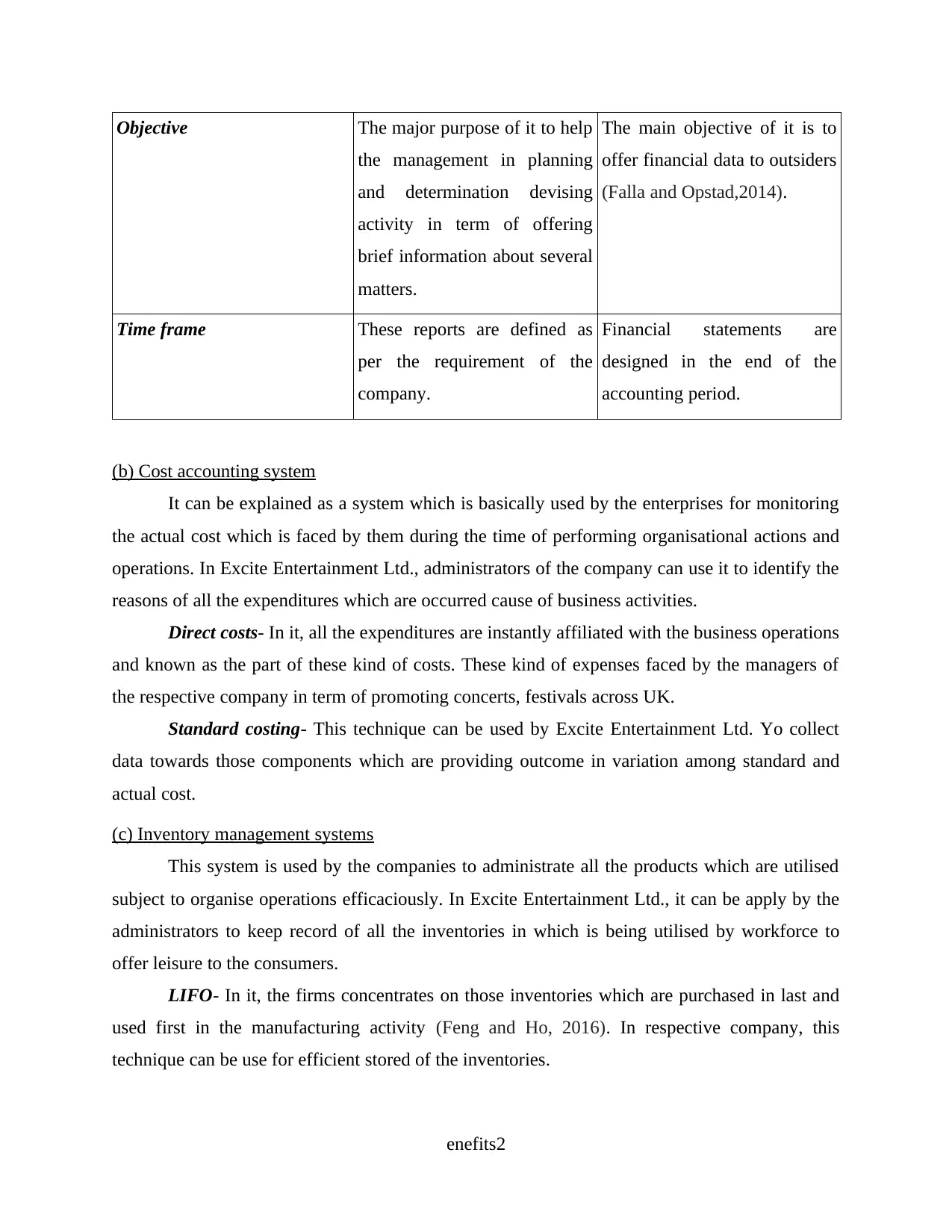

Objective The major purpose of it to help

the management in planning

and determination devising

activity in term of offering

brief information about several

matters.

The main objective of it is to

offer financial data to outsiders

(Falla and Opstad,2014).

Time frame These reports are defined as

per the requirement of the

company.

Financial statements are

designed in the end of the

accounting period.

(b) Cost accounting system

It can be explained as a system which is basically used by the enterprises for monitoring

the actual cost which is faced by them during the time of performing organisational actions and

operations. In Excite Entertainment Ltd., administrators of the company can use it to identify the

reasons of all the expenditures which are occurred cause of business activities.

Direct costs- In it, all the expenditures are instantly affiliated with the business operations

and known as the part of these kind of costs. These kind of expenses faced by the managers of

the respective company in term of promoting concerts, festivals across UK.

Standard costing- This technique can be used by Excite Entertainment Ltd. Yo collect

data towards those components which are providing outcome in variation among standard and

actual cost.

(c) Inventory management systems

This system is used by the companies to administrate all the products which are utilised

subject to organise operations efficaciously. In Excite Entertainment Ltd., it can be apply by the

administrators to keep record of all the inventories in which is being utilised by workforce to

offer leisure to the consumers.

LIFO- In it, the firms concentrates on those inventories which are purchased in last and

used first in the manufacturing activity (Feng and Ho, 2016). In respective company, this

technique can be use for efficient stored of the inventories.

enefits2

the management in planning

and determination devising

activity in term of offering

brief information about several

matters.

The main objective of it is to

offer financial data to outsiders

(Falla and Opstad,2014).

Time frame These reports are defined as

per the requirement of the

company.

Financial statements are

designed in the end of the

accounting period.

(b) Cost accounting system

It can be explained as a system which is basically used by the enterprises for monitoring

the actual cost which is faced by them during the time of performing organisational actions and

operations. In Excite Entertainment Ltd., administrators of the company can use it to identify the

reasons of all the expenditures which are occurred cause of business activities.

Direct costs- In it, all the expenditures are instantly affiliated with the business operations

and known as the part of these kind of costs. These kind of expenses faced by the managers of

the respective company in term of promoting concerts, festivals across UK.

Standard costing- This technique can be used by Excite Entertainment Ltd. Yo collect

data towards those components which are providing outcome in variation among standard and

actual cost.

(c) Inventory management systems

This system is used by the companies to administrate all the products which are utilised

subject to organise operations efficaciously. In Excite Entertainment Ltd., it can be apply by the

administrators to keep record of all the inventories in which is being utilised by workforce to

offer leisure to the consumers.

LIFO- In it, the firms concentrates on those inventories which are purchased in last and

used first in the manufacturing activity (Feng and Ho, 2016). In respective company, this

technique can be use for efficient stored of the inventories.

enefits2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AVCO- In Excite Entertainment Ltd., this technique can be used by the management of

the company for setting the price of their goods and services as per the basis of average cost of

the production.

FIFO- Within this inventory valuation system products which are purchased first are

utilised first in context of manufacturing.

(d) Job costing systems

This management accounting system is basically used by the large companies in order to

divide all the expenditures which are providing outcomes from various jobs (Giacomini, Sicilia

and Steccolini, 2016). In Excite entertainment Ltd., the administrators are utilising this method to

maintain the record of all the jobs which are executed as per the specification of the customers. It

is crucial for the firm because it can assist in segregating diverse expenditures accordant to the

clients.

(e) Benefits of management accounting systems

Cost accounting method is beneficial for measuring the cost of each individual group of

result. With the help of it, the respective company can assess its unit's cost. Inventory

management system help in storing material in warehouse which direct to efficacious control

upon over the storage cost. With the implication of this method, the respective firm can make

control over storage cost. Job costing system is crucial for calculating and offering information

about the cost of each production unit or aware about the cost of every product which they

consume in their actions.

Section B

(a) Different types of marginal accounting reports

It is an activity of formulating management reports which is used by all the organisations

for analysing the actual performance of the business of the firm. In Excite Entertainment Ltd.,

administrators are framing several kinds of reports in order to maintain brief data of business.

Account receivable report- It is the report which consists in depth material subject to the

unpaid amount which was not paid by consumers during the time of buy. In respective company,

the administrators of the firm are framing this report in order to monitor the amount which is

owned by their potential customers. It is crucial for the company because it assist the firm in

determine entire outstanding which will be accepted by the firm in future.

enefits3

the company for setting the price of their goods and services as per the basis of average cost of

the production.

FIFO- Within this inventory valuation system products which are purchased first are

utilised first in context of manufacturing.

(d) Job costing systems

This management accounting system is basically used by the large companies in order to

divide all the expenditures which are providing outcomes from various jobs (Giacomini, Sicilia

and Steccolini, 2016). In Excite entertainment Ltd., the administrators are utilising this method to

maintain the record of all the jobs which are executed as per the specification of the customers. It

is crucial for the firm because it can assist in segregating diverse expenditures accordant to the

clients.

(e) Benefits of management accounting systems

Cost accounting method is beneficial for measuring the cost of each individual group of

result. With the help of it, the respective company can assess its unit's cost. Inventory

management system help in storing material in warehouse which direct to efficacious control

upon over the storage cost. With the implication of this method, the respective firm can make

control over storage cost. Job costing system is crucial for calculating and offering information

about the cost of each production unit or aware about the cost of every product which they

consume in their actions.

Section B

(a) Different types of marginal accounting reports

It is an activity of formulating management reports which is used by all the organisations

for analysing the actual performance of the business of the firm. In Excite Entertainment Ltd.,

administrators are framing several kinds of reports in order to maintain brief data of business.

Account receivable report- It is the report which consists in depth material subject to the

unpaid amount which was not paid by consumers during the time of buy. In respective company,

the administrators of the firm are framing this report in order to monitor the amount which is

owned by their potential customers. It is crucial for the company because it assist the firm in

determine entire outstanding which will be accepted by the firm in future.

enefits3

Inventory management report- In is an written document which involve important

information of inventories that are utilised by the firms to execute all the operational actions and

activities (Hertati, and Sumantri, 2016). In respective company, the managers are designing the

aims and objectives of the business and the firm having effective inventory to provide

entertainment and leisure services of the organisation.

Performance report- These kind of reports are formulated by the companies to determine

that all the employees and business is executing in better manner or not. The administrators of

Excite Entertainment Ltd., are also generating it to analyse that workforce are performing in

effective manner in context of accomplishing the business objectives and aims (Jing and

DUMITRU, 2015). It offers several advantages to business which consists facilitation in offering

bonus to workers, taking decisions for upcoming time etc.

(b) Explain why information presented should be accurate, relevant to the use, reliable up to date

and timely

The data or information should be accurate, reliable and relevant up to date cause of

several mentioned reasons:

Accurate- The data is accurate because the administrators take effective and right

decision in context of business and business activities & operations.

Relevant- The accounting data should be relevant in context of firms financial

transactions because if the data will not be effective, it can be hard to rely on the information.

Reliable- The accounting data should be reliable because in the absence of this feature,

the firm can not make right or effective determination.

Timely- The accounting data should be provide ion correct time so that organisations can

devisee plans and strategies to beat the rivals.

(c) Evaluate that how management accounting systems and management accounting reporting

should be integrated organisation operational process

In Excite Entertainment Ltd., the administrators are obsessed with maximised execution

of the company for this motive, diverse systems and reports are utilised by them which are

affiliated to management accounting. The main motive of all them is to offer brief data in context

of execution and operational efficiency of business (Kihn and Näsi, S., 2017). For instant, cost

accounting method is utilised b y the administrators of the company to differentiate all

expenditures which are resulting from activities and operations. Apart from it, managers are

enefits4

information of inventories that are utilised by the firms to execute all the operational actions and

activities (Hertati, and Sumantri, 2016). In respective company, the managers are designing the

aims and objectives of the business and the firm having effective inventory to provide

entertainment and leisure services of the organisation.

Performance report- These kind of reports are formulated by the companies to determine

that all the employees and business is executing in better manner or not. The administrators of

Excite Entertainment Ltd., are also generating it to analyse that workforce are performing in

effective manner in context of accomplishing the business objectives and aims (Jing and

DUMITRU, 2015). It offers several advantages to business which consists facilitation in offering

bonus to workers, taking decisions for upcoming time etc.

(b) Explain why information presented should be accurate, relevant to the use, reliable up to date

and timely

The data or information should be accurate, reliable and relevant up to date cause of

several mentioned reasons:

Accurate- The data is accurate because the administrators take effective and right

decision in context of business and business activities & operations.

Relevant- The accounting data should be relevant in context of firms financial

transactions because if the data will not be effective, it can be hard to rely on the information.

Reliable- The accounting data should be reliable because in the absence of this feature,

the firm can not make right or effective determination.

Timely- The accounting data should be provide ion correct time so that organisations can

devisee plans and strategies to beat the rivals.

(c) Evaluate that how management accounting systems and management accounting reporting

should be integrated organisation operational process

In Excite Entertainment Ltd., the administrators are obsessed with maximised execution

of the company for this motive, diverse systems and reports are utilised by them which are

affiliated to management accounting. The main motive of all them is to offer brief data in context

of execution and operational efficiency of business (Kihn and Näsi, S., 2017). For instant, cost

accounting method is utilised b y the administrators of the company to differentiate all

expenditures which are resulting from activities and operations. Apart from it, managers are

enefits4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

framing administration reports like inventory management report, performance report etc. These

reports are crucial to analysing or assessing the actual performance or the employees and the

business of the company.

TASK 2

Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs

Absorption costing- It is an accounting technique which utilised in cost accounting to

analyse the cost of absorption. In Excite Entertainment Ltd., the administrator usage it for

identifying the best method to formulate the income statement so that effective data can be

collected in context of business (Nimtrakoon, S. and Tayles, M., 2015). The major advantage of

this technique is that it provide direction to the manager to formulate plan of actions to maximise

operating incomes for for the firm for a particular time frame. The limitation of it is that the issue

which is suffered by the analysers during the time of comparing outcomes as all the expenditures

which are considering at the time of utilisation it to calculate profitability.

Marginal costing- It is another technique of accounting which is utilised by the firm to

identify the cost and fund which gets modify when the units in entire manufacturing is changed

by senior mangers. At time of usage of this technique, the administrators of the respective

company write off all the fixed costs. This technique is beneficial because it is easy to

acknowledge so assist in designing the plan of actions for the growth and development. The

drawback of it is that there is high level of problem which is suffered by the analysers at the time

of classifying costs.

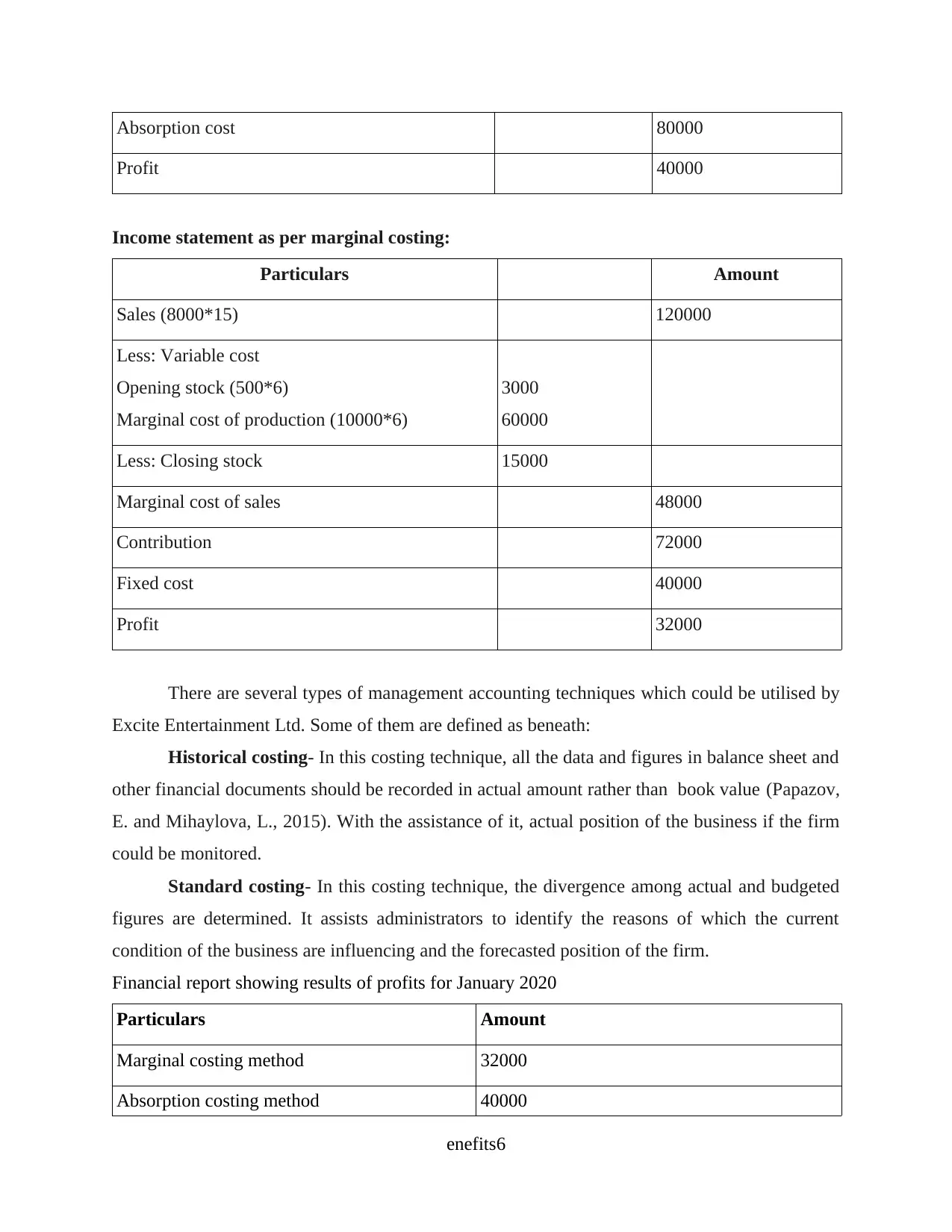

Income statement as per absorption costing:

Particulars Amount

Sales (8000*5) 120000

Less : Cost of good sold:

Opening stock (500*10)

Production (10000*10)

5000

100000

Less- Closing stock (2500*10) 25000

enefits5

reports are crucial to analysing or assessing the actual performance or the employees and the

business of the company.

TASK 2

Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs

Absorption costing- It is an accounting technique which utilised in cost accounting to

analyse the cost of absorption. In Excite Entertainment Ltd., the administrator usage it for

identifying the best method to formulate the income statement so that effective data can be

collected in context of business (Nimtrakoon, S. and Tayles, M., 2015). The major advantage of

this technique is that it provide direction to the manager to formulate plan of actions to maximise

operating incomes for for the firm for a particular time frame. The limitation of it is that the issue

which is suffered by the analysers during the time of comparing outcomes as all the expenditures

which are considering at the time of utilisation it to calculate profitability.

Marginal costing- It is another technique of accounting which is utilised by the firm to

identify the cost and fund which gets modify when the units in entire manufacturing is changed

by senior mangers. At time of usage of this technique, the administrators of the respective

company write off all the fixed costs. This technique is beneficial because it is easy to

acknowledge so assist in designing the plan of actions for the growth and development. The

drawback of it is that there is high level of problem which is suffered by the analysers at the time

of classifying costs.

Income statement as per absorption costing:

Particulars Amount

Sales (8000*5) 120000

Less : Cost of good sold:

Opening stock (500*10)

Production (10000*10)

5000

100000

Less- Closing stock (2500*10) 25000

enefits5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption cost 80000

Profit 40000

Income statement as per marginal costing:

Particulars Amount

Sales (8000*15) 120000

Less: Variable cost

Opening stock (500*6)

Marginal cost of production (10000*6)

3000

60000

Less: Closing stock 15000

Marginal cost of sales 48000

Contribution 72000

Fixed cost 40000

Profit 32000

There are several types of management accounting techniques which could be utilised by

Excite Entertainment Ltd. Some of them are defined as beneath:

Historical costing- In this costing technique, all the data and figures in balance sheet and

other financial documents should be recorded in actual amount rather than book value (Papazov,

E. and Mihaylova, L., 2015). With the assistance of it, actual position of the business if the firm

could be monitored.

Standard costing- In this costing technique, the divergence among actual and budgeted

figures are determined. It assists administrators to identify the reasons of which the current

condition of the business are influencing and the forecasted position of the firm.

Financial report showing results of profits for January 2020

Particulars Amount

Marginal costing method 32000

Absorption costing method 40000

enefits6

Profit 40000

Income statement as per marginal costing:

Particulars Amount

Sales (8000*15) 120000

Less: Variable cost

Opening stock (500*6)

Marginal cost of production (10000*6)

3000

60000

Less: Closing stock 15000

Marginal cost of sales 48000

Contribution 72000

Fixed cost 40000

Profit 32000

There are several types of management accounting techniques which could be utilised by

Excite Entertainment Ltd. Some of them are defined as beneath:

Historical costing- In this costing technique, all the data and figures in balance sheet and

other financial documents should be recorded in actual amount rather than book value (Papazov,

E. and Mihaylova, L., 2015). With the assistance of it, actual position of the business if the firm

could be monitored.

Standard costing- In this costing technique, the divergence among actual and budgeted

figures are determined. It assists administrators to identify the reasons of which the current

condition of the business are influencing and the forecasted position of the firm.

Financial report showing results of profits for January 2020

Particulars Amount

Marginal costing method 32000

Absorption costing method 40000

enefits6

From the income statements which are formulated for Excite Entertainment Ltd., it has

been summarised that marginal costing is providing outcomes in term of profits of 69000 and

absorption method is reflecting the net income of 35000. The major reason of the differentiation

is ignorance of fixed cost in marginal costing. By determining the current situation , it has been

suggested to the company to utilise the first method and technique which is showing or

indicating net profit of 69000.

BE Formula

Formula=TFc + TP / SPpv - VCpv

=£500 + £700 / £30 - £10

=£1.200/ £20

= 600,000 Units

Budget is plan for a future period in economic terms

Q= £10* £40= £400

R= £8* £36 = £288

S= £11* £20= £ 220

= £908

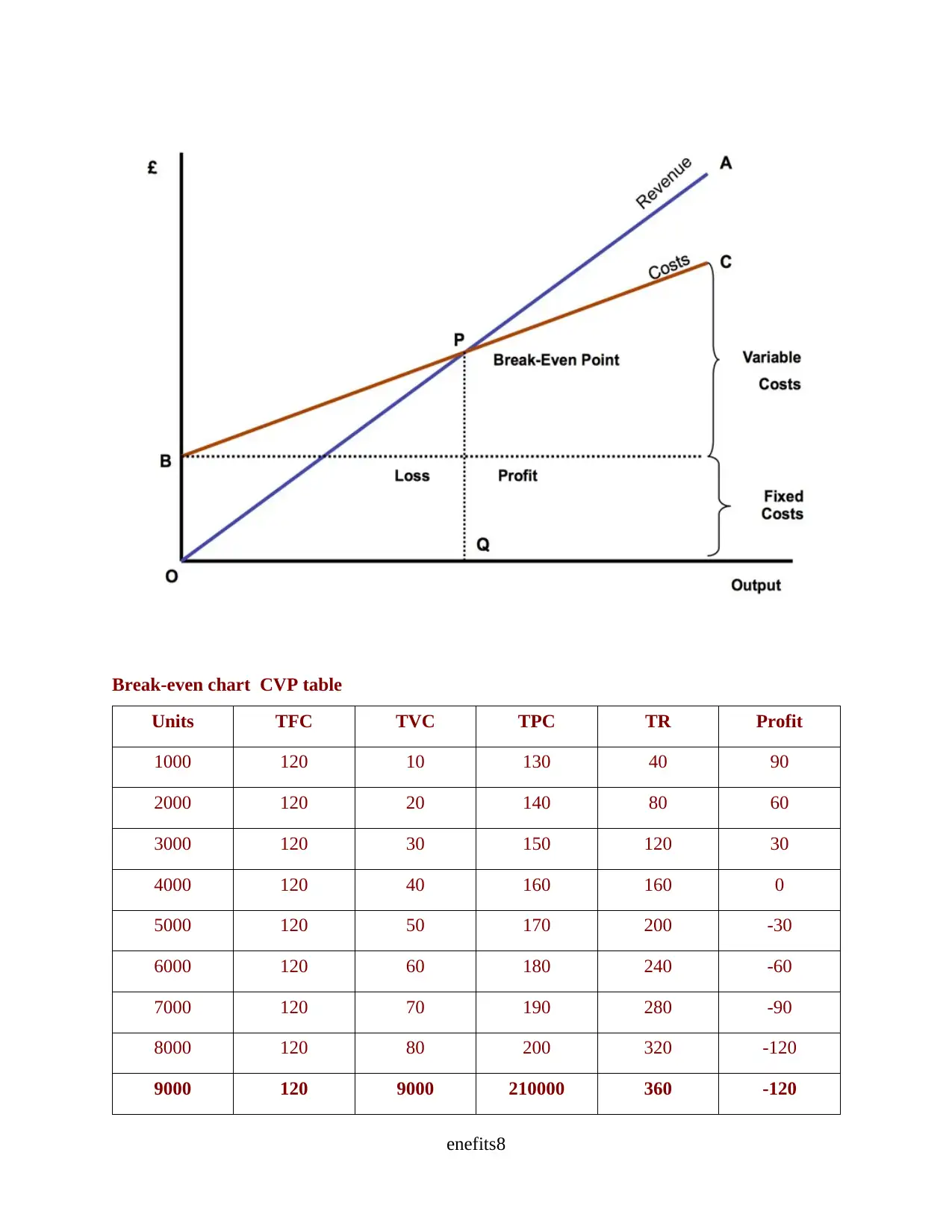

BREAK-EVEN CHART

enefits7

been summarised that marginal costing is providing outcomes in term of profits of 69000 and

absorption method is reflecting the net income of 35000. The major reason of the differentiation

is ignorance of fixed cost in marginal costing. By determining the current situation , it has been

suggested to the company to utilise the first method and technique which is showing or

indicating net profit of 69000.

BE Formula

Formula=TFc + TP / SPpv - VCpv

=£500 + £700 / £30 - £10

=£1.200/ £20

= 600,000 Units

Budget is plan for a future period in economic terms

Q= £10* £40= £400

R= £8* £36 = £288

S= £11* £20= £ 220

= £908

BREAK-EVEN CHART

enefits7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Break-even chart CVP table

Units TFC TVC TPC TR Profit

1000 120 10 130 40 90

2000 120 20 140 80 60

3000 120 30 150 120 30

4000 120 40 160 160 0

5000 120 50 170 200 -30

6000 120 60 180 240 -60

7000 120 70 190 280 -90

8000 120 80 200 320 -120

9000 120 9000 210000 360 -120

enefits8

Units TFC TVC TPC TR Profit

1000 120 10 130 40 90

2000 120 20 140 80 60

3000 120 30 150 120 30

4000 120 40 160 160 0

5000 120 50 170 200 -30

6000 120 60 180 240 -60

7000 120 70 190 280 -90

8000 120 80 200 320 -120

9000 120 9000 210000 360 -120

enefits8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

VCpv= 10

TPpv= 40

TFC= 120

TFC= Total fixed cost

TVC= Total variable cost

TPC= Total price cost

TR= Total revenue

SR= Sales revenue

TP= Target profit

TASK 3

Advantages and disadvantages of different types of planning tools used for budgetary control

Budgeting

It is an activity of designing a plan to spend the finance. It can be an estimation of

expenses and revenue over a specified forthcoming time period which is basically complied and

re-measured on a periodic basis (Revellino and Mouritsen, 2015). In term of companies, it is an

internal too, which is used by the administration to have the information about future expenses

and profits.

Budgetary control

Budgets are financial documents that consists estimations about the expenses or profits

which are formulated after determining aims and objectives of the firm. Methods and systems

which are adopted by the enterprise for controlling fiscal execution by preparing addition to

applying distinct budgets is known as budgetary control. Finance function of Excite

Entertainment Ltd. Design several budgets and examine the outcomes with the help of this

mechanisms and with the assistance of it they can comparison among actual performance with

the approximation.

Different planning tool

Zero based budgeting- It is a budgeting tool in which all transactions are justified for the

starting of new accounting period. In Excite Entertainment Ltd., it can be utilise to scratch all

expenditures to zero every time in context of justify the fund according to the business aims.

enefits9

TPpv= 40

TFC= 120

TFC= Total fixed cost

TVC= Total variable cost

TPC= Total price cost

TR= Total revenue

SR= Sales revenue

TP= Target profit

TASK 3

Advantages and disadvantages of different types of planning tools used for budgetary control

Budgeting

It is an activity of designing a plan to spend the finance. It can be an estimation of

expenses and revenue over a specified forthcoming time period which is basically complied and

re-measured on a periodic basis (Revellino and Mouritsen, 2015). In term of companies, it is an

internal too, which is used by the administration to have the information about future expenses

and profits.

Budgetary control

Budgets are financial documents that consists estimations about the expenses or profits

which are formulated after determining aims and objectives of the firm. Methods and systems

which are adopted by the enterprise for controlling fiscal execution by preparing addition to

applying distinct budgets is known as budgetary control. Finance function of Excite

Entertainment Ltd. Design several budgets and examine the outcomes with the help of this

mechanisms and with the assistance of it they can comparison among actual performance with

the approximation.

Different planning tool

Zero based budgeting- It is a budgeting tool in which all transactions are justified for the

starting of new accounting period. In Excite Entertainment Ltd., it can be utilise to scratch all

expenditures to zero every time in context of justify the fund according to the business aims.

enefits9

Advantages- These kind of budgets generates growth options to the administrators and it

assist in capitalising resources on inefficiencies addition to identifying creations for minimising

costs.

Disadvantages- The main draw back of this tool is to prepare budget at at company

which take more time as the process of designing consists new aspects in each cycle that takes

more duration in analysing the actions for devising estimation.

Cost budget- It is another planning tool in which expected cash receipts together with cash

disbursements are recorded for accounting period (Richardson, 2015). In Excite entertainment,

with the help of it, the administrators can gets total information about cash status so that further

critical determinations in term of creating reserves and uses in effective way are designed.

Advantages- The major benefit of this tool is that it make realistic predictions and

monitors financial statements so to look into expenses that are devised in the period.

Disadvantages- The limitation of it is that it limits the areas of spending that providing

outcomes in term of preventing growth options to make future investments by the firm.

Break even analysis

It is a financial tool which assists the company in determining at hat stage the firm or a

new service or a product will be profitable (Schaltegger, Burritt and Petersen, 2017). In context

of respective firm, it is an financial analysis or calculation for monitoring the number of products

services an organisation should sell to cover its costs. It is a situation where the firm can neither

making fund and nor losing cost but all the costs have been covered. This analysis is beneficial to

examine the relation among the variable and fixed cost and revenue. This analysis is beneficial

because it help in monitoring the impact on profit on modifying to automation from manual.

Fixed cost-It is also known as overhead cost and fixed cost also consist interest, taxes,

salaries, rent, labour cost, energy costs and others. These all cost are fixed because no matter

how much the firm sell.

Variable cost- It is the cost that will maximise or minimise in direct relation to the

manufacturing volume. In excite Entertainment, it consist raw material, fuel and other costs that

are directly connected with the production.

Limiting factor analysis

It refers to any resource which the business requires to manufacture the products it sells.

There is no point in forecasting high unit sales if the business is not able to manufacture the

enefits10

assist in capitalising resources on inefficiencies addition to identifying creations for minimising

costs.

Disadvantages- The main draw back of this tool is to prepare budget at at company

which take more time as the process of designing consists new aspects in each cycle that takes

more duration in analysing the actions for devising estimation.

Cost budget- It is another planning tool in which expected cash receipts together with cash

disbursements are recorded for accounting period (Richardson, 2015). In Excite entertainment,

with the help of it, the administrators can gets total information about cash status so that further

critical determinations in term of creating reserves and uses in effective way are designed.

Advantages- The major benefit of this tool is that it make realistic predictions and

monitors financial statements so to look into expenses that are devised in the period.

Disadvantages- The limitation of it is that it limits the areas of spending that providing

outcomes in term of preventing growth options to make future investments by the firm.

Break even analysis

It is a financial tool which assists the company in determining at hat stage the firm or a

new service or a product will be profitable (Schaltegger, Burritt and Petersen, 2017). In context

of respective firm, it is an financial analysis or calculation for monitoring the number of products

services an organisation should sell to cover its costs. It is a situation where the firm can neither

making fund and nor losing cost but all the costs have been covered. This analysis is beneficial to

examine the relation among the variable and fixed cost and revenue. This analysis is beneficial

because it help in monitoring the impact on profit on modifying to automation from manual.

Fixed cost-It is also known as overhead cost and fixed cost also consist interest, taxes,

salaries, rent, labour cost, energy costs and others. These all cost are fixed because no matter

how much the firm sell.

Variable cost- It is the cost that will maximise or minimise in direct relation to the

manufacturing volume. In excite Entertainment, it consist raw material, fuel and other costs that

are directly connected with the production.

Limiting factor analysis

It refers to any resource which the business requires to manufacture the products it sells.

There is no point in forecasting high unit sales if the business is not able to manufacture the

enefits10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.