Management Accounting Report for Excite Entertainment Ltd: HND Unit 5

VerifiedAdded on 2023/01/13

|11

|2946

|75

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Excite Entertainment Ltd, focusing on the application of various accounting systems and techniques. The introduction outlines the report's objective to evaluate the importance and utilization of management accounting in the context of Excite Entertainment Ltd, a company involved in promoting concerts and festivals. Section A delves into the differences between management and financial accounting, explores cost accounting systems (including direct and standard costing), inventory management systems (ABC analysis and Just-in-time), and job costing systems. The benefits of these management accounting systems are also highlighted. Section B examines different types of managerial accounting reports (budgetary, performance, and cost reports), discusses the accuracy and reliability of information provided to users, and addresses the integration of management accounting reporting and systems. The report further includes scenarios that discuss financial reporting under marginal and absorption costing, planning tools used in management accounting (operational, cash, and sales budgets), and the application of management accounting techniques for solving financial issues. The report concludes by summarizing the key findings and their implications for Excite Entertainment Ltd, emphasizing how management accounting tools can enhance financial performance and decision-making.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................1

Scenario 1 ........................................................................................................................................1

Section A .....................................................................................................................................1

a) Difference between management and Financial accounting ........................................1

b) Cost Accounting System ..............................................................................................1

c) Inventory Management System ....................................................................................2

d) Job Costing System ......................................................................................................2

e) Benefits of management accounting systems................................................................2

Section B......................................................................................................................................3

a) Types of managerial accounting reports........................................................................3

b) Accuracy and reliability of information provided to the users......................................3

c) Integration of management accounting reporting and management accounting systems.. 4

Scenario 2 ........................................................................................................................................4

Financial report under marginal and absorption costing. ............................................................4

Scenario 3 ........................................................................................................................................5

Planning tools used in management accounting. ........................................................................5

Scenario 4 ........................................................................................................................................6

Use of management accounting techniques for solving the financial issues...............................6

CONCLUSION ...............................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION ..........................................................................................................................1

Scenario 1 ........................................................................................................................................1

Section A .....................................................................................................................................1

a) Difference between management and Financial accounting ........................................1

b) Cost Accounting System ..............................................................................................1

c) Inventory Management System ....................................................................................2

d) Job Costing System ......................................................................................................2

e) Benefits of management accounting systems................................................................2

Section B......................................................................................................................................3

a) Types of managerial accounting reports........................................................................3

b) Accuracy and reliability of information provided to the users......................................3

c) Integration of management accounting reporting and management accounting systems.. 4

Scenario 2 ........................................................................................................................................4

Financial report under marginal and absorption costing. ............................................................4

Scenario 3 ........................................................................................................................................5

Planning tools used in management accounting. ........................................................................5

Scenario 4 ........................................................................................................................................6

Use of management accounting techniques for solving the financial issues...............................6

CONCLUSION ...............................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Management accounting helps in preparation of different financial reports that help in

analysing the operation and performance of the business. Present report is based on Excite

Entertainment ltd. operating in entertainment and leisure industry. Company has main operations

of promoting festivals and concerts. The objective of this report is to provide understanding

about importance and use of management accounting in Excite ltd. This report will identify the

use of management accounting reports for ascertaining the financial performance and the

different types of management accounting systems that can be used (Endrikat, Hartmann and

Schreck, 2017). The report will also evaluate different budgetary options and conclude how the

management accounting tools can be used in an organization.

Scenario 1

Section A

a) Difference between management and Financial accounting

Management Accounting Financial Accounting

It is the accounting system that

provides information relevant for

management in making plans, policies

and strategies essential for running

business.

Management accounting provides

information for internal use for

executives and managers.

Management accounting has the focus

over present and on forecasts of future.

This system of accounting focuses over

preparation of the financial statements

of corporations for providing financial

information to interested parties.

Information provided by the financial

accounting is mainly for external users.

It focuses over historical reports, that

belong to the events and transactions

already occurred (Granlund and Lukka,

2017).

1

Management accounting helps in preparation of different financial reports that help in

analysing the operation and performance of the business. Present report is based on Excite

Entertainment ltd. operating in entertainment and leisure industry. Company has main operations

of promoting festivals and concerts. The objective of this report is to provide understanding

about importance and use of management accounting in Excite ltd. This report will identify the

use of management accounting reports for ascertaining the financial performance and the

different types of management accounting systems that can be used (Endrikat, Hartmann and

Schreck, 2017). The report will also evaluate different budgetary options and conclude how the

management accounting tools can be used in an organization.

Scenario 1

Section A

a) Difference between management and Financial accounting

Management Accounting Financial Accounting

It is the accounting system that

provides information relevant for

management in making plans, policies

and strategies essential for running

business.

Management accounting provides

information for internal use for

executives and managers.

Management accounting has the focus

over present and on forecasts of future.

This system of accounting focuses over

preparation of the financial statements

of corporations for providing financial

information to interested parties.

Information provided by the financial

accounting is mainly for external users.

It focuses over historical reports, that

belong to the events and transactions

already occurred (Granlund and Lukka,

2017).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Cost Accounting System

Cost accounting is referred as an accounting form aiming to improve the profitability of

company by controlling, managing & eliminating the expenses. It is used by management for

determining cost of product, project and process that shows company where it is losing and

earning money. It is used as an integral part of budgeting process of the Excite ltd that hepls in

arriving at accurate costs.

Direct Costing – It is used in cost analysis where only variable costs are considered for making

decisions. Fixed costs are considered to be associated with time periods.

Standard Costing – It is method used for comparing standard cost and revenues from product

with actual results for arriving at variances and informing management about deviations to take

corrective measures.

c) Inventory Management System

Inventory management refers to the management of inventory within organisation. This

ensures the availability of inventory for the production and keeps track record of all the finished

goods inventory (Konopczak and Welfe, 2017). Inventory management systems are installed in

the warehouse and production units of Excite Ltd which ensures that all the inventory is

available at time without affecting its operations.

ABC Analysis

Under this method Excite ltd. classifies inventory under three categories. A reflects the

most valuable inventory, B represents less valuable but generate profits and C reflects the least

valuable but have high sales.

Just-in-time

This approach ensures that Excite ltd is available with the materials required in

production as and when required without any delay. This approach do not focus over storing

materials which helps in reducing its carrying costs.

d) Job Costing System

System involves process of collecting information about all costs associated to

manufacturing or to service job. The information helps the company available with the cost

information related to particular job which is also sometime used for reimbursements. Job

2

Cost accounting is referred as an accounting form aiming to improve the profitability of

company by controlling, managing & eliminating the expenses. It is used by management for

determining cost of product, project and process that shows company where it is losing and

earning money. It is used as an integral part of budgeting process of the Excite ltd that hepls in

arriving at accurate costs.

Direct Costing – It is used in cost analysis where only variable costs are considered for making

decisions. Fixed costs are considered to be associated with time periods.

Standard Costing – It is method used for comparing standard cost and revenues from product

with actual results for arriving at variances and informing management about deviations to take

corrective measures.

c) Inventory Management System

Inventory management refers to the management of inventory within organisation. This

ensures the availability of inventory for the production and keeps track record of all the finished

goods inventory (Konopczak and Welfe, 2017). Inventory management systems are installed in

the warehouse and production units of Excite Ltd which ensures that all the inventory is

available at time without affecting its operations.

ABC Analysis

Under this method Excite ltd. classifies inventory under three categories. A reflects the

most valuable inventory, B represents less valuable but generate profits and C reflects the least

valuable but have high sales.

Just-in-time

This approach ensures that Excite ltd is available with the materials required in

production as and when required without any delay. This approach do not focus over storing

materials which helps in reducing its carrying costs.

d) Job Costing System

System involves process of collecting information about all costs associated to

manufacturing or to service job. The information helps the company available with the cost

information related to particular job which is also sometime used for reimbursements. Job

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

costing records the cost incurred for job instead of process (Latan and et.al., 2018). Excite ltd.

keeps track and record of costs related to each job. For example the it helps in identifying the

cost associated with product A and B separately.

e) Benefits of management accounting systems

Cost Accounting – Cost accounting systems helps the Excite ltd in identifying the cost of

product or services specifically considering both variable and fixed costs.

Inventory management – Inventory management helps in keeping proper track record of all the

information about the movement of inventory in the company. This also makes the inventory

available on time.

Job Costing System – It is very useful to Excite ltd in identifying the the cost of each job

separately so that the profitability from every job could be identified.

Section B

a) Types of managerial accounting reports.

Budgetary Reports

Budgetary report are prepared by the organisation to have a well structured spending

plan to be followed for the given period. Budgets are prepared by the management based on

previous budgets by making adjustments required for current period. This helps Excite in proper

allocation of resources and expenses under control (Lopez-Valeiras, Gomez-Conde and

Naranjo-Gil, 2015). Budgets are forecast about revenues and expenses based on previous

information. It is not possible to forecast accurately but it provides a direction to be followed.

Performance Reports

These are the report prepared by management for measuring the performance of business

operations. These helps the Excite ltd in knowing the level of success achieved using the existing

policies and procedures. It also on individual basis helps in rewarding the performance of

employees achieving the targets (Maas, Schaltegger and Crutzen, 2016). Thorough performance

reports it can identify the areas of improvements.

3

keeps track and record of costs related to each job. For example the it helps in identifying the

cost associated with product A and B separately.

e) Benefits of management accounting systems

Cost Accounting – Cost accounting systems helps the Excite ltd in identifying the cost of

product or services specifically considering both variable and fixed costs.

Inventory management – Inventory management helps in keeping proper track record of all the

information about the movement of inventory in the company. This also makes the inventory

available on time.

Job Costing System – It is very useful to Excite ltd in identifying the the cost of each job

separately so that the profitability from every job could be identified.

Section B

a) Types of managerial accounting reports.

Budgetary Reports

Budgetary report are prepared by the organisation to have a well structured spending

plan to be followed for the given period. Budgets are prepared by the management based on

previous budgets by making adjustments required for current period. This helps Excite in proper

allocation of resources and expenses under control (Lopez-Valeiras, Gomez-Conde and

Naranjo-Gil, 2015). Budgets are forecast about revenues and expenses based on previous

information. It is not possible to forecast accurately but it provides a direction to be followed.

Performance Reports

These are the report prepared by management for measuring the performance of business

operations. These helps the Excite ltd in knowing the level of success achieved using the existing

policies and procedures. It also on individual basis helps in rewarding the performance of

employees achieving the targets (Maas, Schaltegger and Crutzen, 2016). Thorough performance

reports it can identify the areas of improvements.

3

Cost Reports

Cost reports are prepared by the organisation for identifying the cost of manufacturing a

product. It includes all costs that are related to the product like material, labour overheads and

other fixed costs. This helps Excite ltd in determining the profit margins for the product. These

reports are of great importance to the management for making comparisons between the

budgeted and actual outputs.

b) Accuracy and reliability of information provided to the users.

The information provided by the management accounting report must be accurate and

reliable as the decisions for organisation are framed on the information provided. Accurate and

reliable information will be steering the company towards right direction. Also relevance and

reliability are required to be complied as per the accounting standards and reporting frameworks.

Excite ltd uses these information critically in decisions for framing strategies and policies.

c) Integration of management accounting reporting and management accounting systems.

Excite ltd uses both management accounting systems for management of business

operation and transactions. At the same time management accounting reporting helps in

analysing the effectiveness of management systems (McLaren, Appleyard and Mitchell, 2016.).

Accounting systems and reporting are interrelated as Excite ltd uses information of accounting

systems for management reports. For example : Budgeted reports are prepared on the actual

information provided by the accounting systems like cost accounting, inventory management.

Scenario 2

Financial report under marginal and absorption costing.

Interpretation

The profits under absorption costing and marginal costing differ because the marginal

system do not consider the fixed costs in valuation of closing inventory. While in other case in

valuing closing inventory fixed costs are considered that increases the cost of closing inventory.

This results in higher profits under absorption costing and lower in marginal costing.

4

Cost reports are prepared by the organisation for identifying the cost of manufacturing a

product. It includes all costs that are related to the product like material, labour overheads and

other fixed costs. This helps Excite ltd in determining the profit margins for the product. These

reports are of great importance to the management for making comparisons between the

budgeted and actual outputs.

b) Accuracy and reliability of information provided to the users.

The information provided by the management accounting report must be accurate and

reliable as the decisions for organisation are framed on the information provided. Accurate and

reliable information will be steering the company towards right direction. Also relevance and

reliability are required to be complied as per the accounting standards and reporting frameworks.

Excite ltd uses these information critically in decisions for framing strategies and policies.

c) Integration of management accounting reporting and management accounting systems.

Excite ltd uses both management accounting systems for management of business

operation and transactions. At the same time management accounting reporting helps in

analysing the effectiveness of management systems (McLaren, Appleyard and Mitchell, 2016.).

Accounting systems and reporting are interrelated as Excite ltd uses information of accounting

systems for management reports. For example : Budgeted reports are prepared on the actual

information provided by the accounting systems like cost accounting, inventory management.

Scenario 2

Financial report under marginal and absorption costing.

Interpretation

The profits under absorption costing and marginal costing differ because the marginal

system do not consider the fixed costs in valuation of closing inventory. While in other case in

valuing closing inventory fixed costs are considered that increases the cost of closing inventory.

This results in higher profits under absorption costing and lower in marginal costing.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

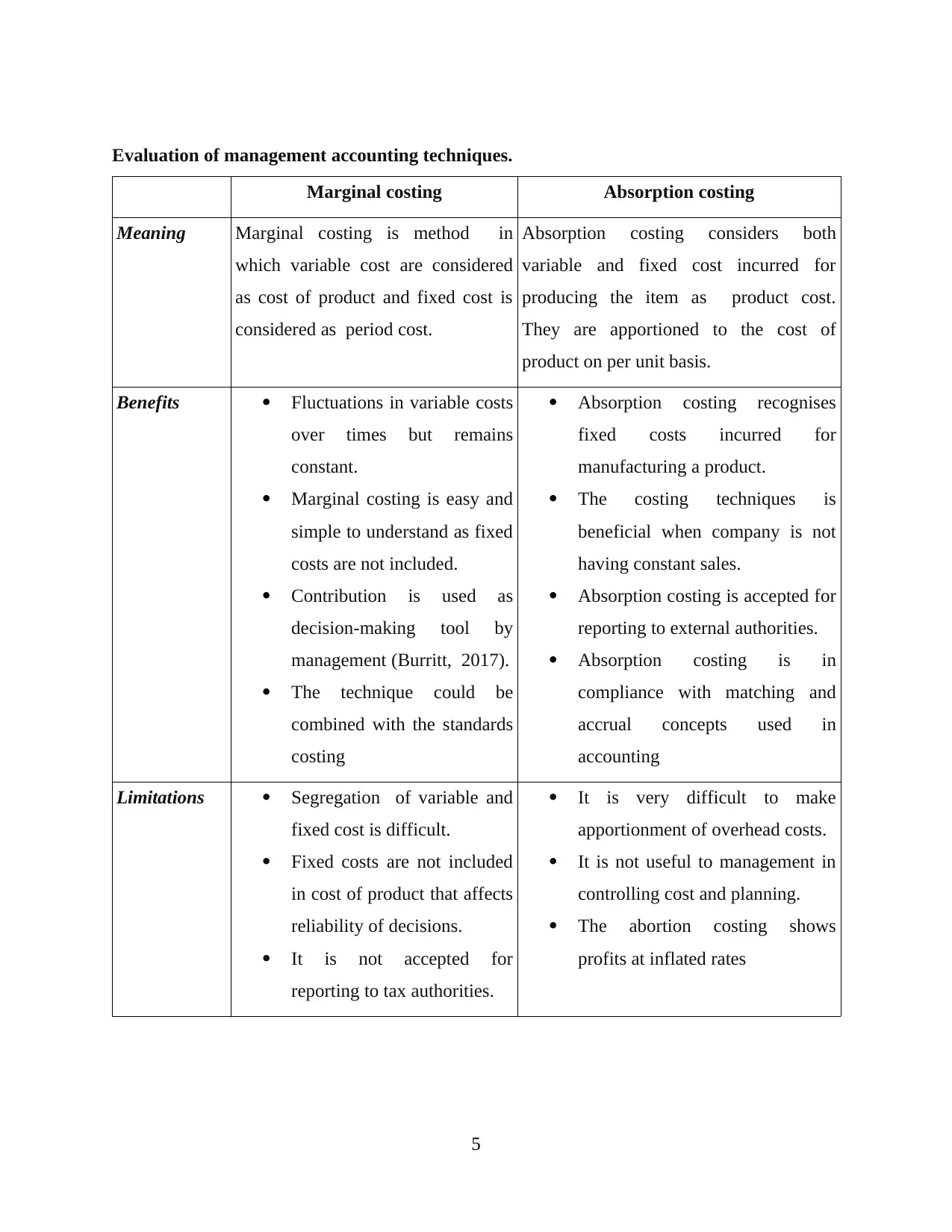

Evaluation of management accounting techniques.

Marginal costing Absorption costing

Meaning Marginal costing is method in

which variable cost are considered

as cost of product and fixed cost is

considered as period cost.

Absorption costing considers both

variable and fixed cost incurred for

producing the item as product cost.

They are apportioned to the cost of

product on per unit basis.

Benefits Fluctuations in variable costs

over times but remains

constant.

Marginal costing is easy and

simple to understand as fixed

costs are not included.

Contribution is used as

decision-making tool by

management (Burritt, 2017).

The technique could be

combined with the standards

costing

Absorption costing recognises

fixed costs incurred for

manufacturing a product.

The costing techniques is

beneficial when company is not

having constant sales.

Absorption costing is accepted for

reporting to external authorities.

Absorption costing is in

compliance with matching and

accrual concepts used in

accounting

Limitations Segregation of variable and

fixed cost is difficult.

Fixed costs are not included

in cost of product that affects

reliability of decisions.

It is not accepted for

reporting to tax authorities.

It is very difficult to make

apportionment of overhead costs.

It is not useful to management in

controlling cost and planning.

The abortion costing shows

profits at inflated rates

5

Marginal costing Absorption costing

Meaning Marginal costing is method in

which variable cost are considered

as cost of product and fixed cost is

considered as period cost.

Absorption costing considers both

variable and fixed cost incurred for

producing the item as product cost.

They are apportioned to the cost of

product on per unit basis.

Benefits Fluctuations in variable costs

over times but remains

constant.

Marginal costing is easy and

simple to understand as fixed

costs are not included.

Contribution is used as

decision-making tool by

management (Burritt, 2017).

The technique could be

combined with the standards

costing

Absorption costing recognises

fixed costs incurred for

manufacturing a product.

The costing techniques is

beneficial when company is not

having constant sales.

Absorption costing is accepted for

reporting to external authorities.

Absorption costing is in

compliance with matching and

accrual concepts used in

accounting

Limitations Segregation of variable and

fixed cost is difficult.

Fixed costs are not included

in cost of product that affects

reliability of decisions.

It is not accepted for

reporting to tax authorities.

It is very difficult to make

apportionment of overhead costs.

It is not useful to management in

controlling cost and planning.

The abortion costing shows

profits at inflated rates

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Scenario 3

Planning tools used in management accounting.

Planning tools are used by the organisation for planning the objectives and targets to be

achieved by the organisation. There are different types of planning tools that are used in

management accounting. These planning tool helps in effective planning and making the

required accurate decisions. Excite ltd. in its management accounting uses following planning

tools.

Operational Budget

Operational budgets are used as planning tool for making estimates of all the incomes

and expenses related to a given period. Operational budgets helps Excite to plan in advance

about the revenues and expenses by making detailed analysis of the previous budgets and trends.

The operational budgets are given as objectives to the departments for achieving in the given

period of time (Ameen, Ahmed and Hafez, 2018).

Advantages

This is used by Excite ltd in projecting the future incomes and expenses and planning its policies

and strategies accordingly.

Disadvantage

It is prepared considering all the budgets therefore the errors in one budget will be carried to this

budget also.

Cash Budgets

Cash budgets are prepared on estimates of cash inflow and outflow from different

activities and business operations. The cash budget enables the Excite ltd. to identify whether it

will be available with sufficient monetary funds for carrying out its business. It estimates

revenues from the sales and required expenses to be incurred for the business. This helps in

estimating the cash that will be available at the end of the period (Järvinen, 2016). On the basis

of estimates Excite ltd makes arrangement of required funds so that operations are not

interrupted due to insufficient funds.

Advantages

Cash budgets helps the management in identifying the availability of sufficient funds for

carrying out the operations.

6

Planning tools used in management accounting.

Planning tools are used by the organisation for planning the objectives and targets to be

achieved by the organisation. There are different types of planning tools that are used in

management accounting. These planning tool helps in effective planning and making the

required accurate decisions. Excite ltd. in its management accounting uses following planning

tools.

Operational Budget

Operational budgets are used as planning tool for making estimates of all the incomes

and expenses related to a given period. Operational budgets helps Excite to plan in advance

about the revenues and expenses by making detailed analysis of the previous budgets and trends.

The operational budgets are given as objectives to the departments for achieving in the given

period of time (Ameen, Ahmed and Hafez, 2018).

Advantages

This is used by Excite ltd in projecting the future incomes and expenses and planning its policies

and strategies accordingly.

Disadvantage

It is prepared considering all the budgets therefore the errors in one budget will be carried to this

budget also.

Cash Budgets

Cash budgets are prepared on estimates of cash inflow and outflow from different

activities and business operations. The cash budget enables the Excite ltd. to identify whether it

will be available with sufficient monetary funds for carrying out its business. It estimates

revenues from the sales and required expenses to be incurred for the business. This helps in

estimating the cash that will be available at the end of the period (Järvinen, 2016). On the basis

of estimates Excite ltd makes arrangement of required funds so that operations are not

interrupted due to insufficient funds.

Advantages

Cash budgets helps the management in identifying the availability of sufficient funds for

carrying out the operations.

6

Disadvantage

Errors in estimates of cash budgets may affect the production as funds may not be available for

carrying out the operations.

Sales Budget

Sales budget is the estimate of sales that will be generated by the business during the

period. The sales estimates are to be made by management after incurring deep study of all the

factors that influence the sales. This gives the company further targets. Sales budget role in

decision making process of Excite as all the budgets and expenses revolve around the sales

estimation. All the budgets will be affected like, expenses, operational if proper estimates of

sales are not made. Sales budgets helps Excite ltd. in planning the incomes and expenses for the

business. This also helps in managing the cost of production.

Advantages

Sales budget helps in allocation of resources based on the revenues estimated in sales budget.

Disadvantage

It is not possible to make accurate forecasts which can affect the completes budget on wrong

forecasts.

Comparison and Contrast

All the above three planning tools are prepared by Excite ltd for having effective control

and management of the organisation. On comparison among all the three tools it was outlined

that cash budget are being used by the Excite for calculating the cash flow from all the three

activities that is operating, financing and investing activities. But in contrast to this the sales

budget is used by the company to maintain and monitor that whether the set target for sales will

be able to achieved with given resources. In the end of comparison it was outlined that operating

budget is used in order to plan for the future by estimating the income and the expenses which

may be accrued by the company (Latan and et.al., 2018). But all the three budgets need to be

prepared by the company because all the three budgets are different form one another and has

their own utility and importance in attaining the objectives of the business.

7

Errors in estimates of cash budgets may affect the production as funds may not be available for

carrying out the operations.

Sales Budget

Sales budget is the estimate of sales that will be generated by the business during the

period. The sales estimates are to be made by management after incurring deep study of all the

factors that influence the sales. This gives the company further targets. Sales budget role in

decision making process of Excite as all the budgets and expenses revolve around the sales

estimation. All the budgets will be affected like, expenses, operational if proper estimates of

sales are not made. Sales budgets helps Excite ltd. in planning the incomes and expenses for the

business. This also helps in managing the cost of production.

Advantages

Sales budget helps in allocation of resources based on the revenues estimated in sales budget.

Disadvantage

It is not possible to make accurate forecasts which can affect the completes budget on wrong

forecasts.

Comparison and Contrast

All the above three planning tools are prepared by Excite ltd for having effective control

and management of the organisation. On comparison among all the three tools it was outlined

that cash budget are being used by the Excite for calculating the cash flow from all the three

activities that is operating, financing and investing activities. But in contrast to this the sales

budget is used by the company to maintain and monitor that whether the set target for sales will

be able to achieved with given resources. In the end of comparison it was outlined that operating

budget is used in order to plan for the future by estimating the income and the expenses which

may be accrued by the company (Latan and et.al., 2018). But all the three budgets need to be

prepared by the company because all the three budgets are different form one another and has

their own utility and importance in attaining the objectives of the business.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Scenario 4

Use of management accounting techniques for solving the financial issues.

An organisation while operating any business has to face various problems which

influence its performance. The financial issues faced by the organisation are raising production

costs, variances between actual and budgeted costs, scarcity resources to achieve the goals and

many more. These are managed by using the tools such as ;

Variance analysis – Variance analysis helps Excite ltd in identifying the areas where the

deviations are occurring. Once the areas are identified, company focus over identifying the

reasons of variations. Company adopt new policies and procedures for reducing the variances.

Benchmarking – Benchmarking is the tool used for setting realistic and attainable targets. This

motivates employees to increase their efficiency for reaching the set targets (Konopczak and

Welfe, 2017). Benchmarking helps Excite ltd in identifying whether the targets are being

achieved with the available resources or further arrangements are required to be made.

Financial governance – Financial governance refers to the monitoring and controlling business

activities and operations. Excite ltd implement proper monitoring procedure keeps track over all

the costs and expenses. This helps in keeping the costs under control.

CONCLUSION

Management accounting plays a critical role in Excite ltd. A business cannot be run

successfully without using the management accounting tools and techniques. Management

accounting is different from that of financial accounting. Management accounting is useful for

internal management of organisation. Different management accounting systems like inventory

management, cost accounting and job costing helps it to properly record and track costs.

Planning tools used by Excite ltd helps in achieving the organisational goals and objectives

keeping the cost under control. The management accounting reports helps the management in

improving and enhancing the performance of company. Using the management accounting

Excite ltd can achieve a sustainable growth and success.

8

Use of management accounting techniques for solving the financial issues.

An organisation while operating any business has to face various problems which

influence its performance. The financial issues faced by the organisation are raising production

costs, variances between actual and budgeted costs, scarcity resources to achieve the goals and

many more. These are managed by using the tools such as ;

Variance analysis – Variance analysis helps Excite ltd in identifying the areas where the

deviations are occurring. Once the areas are identified, company focus over identifying the

reasons of variations. Company adopt new policies and procedures for reducing the variances.

Benchmarking – Benchmarking is the tool used for setting realistic and attainable targets. This

motivates employees to increase their efficiency for reaching the set targets (Konopczak and

Welfe, 2017). Benchmarking helps Excite ltd in identifying whether the targets are being

achieved with the available resources or further arrangements are required to be made.

Financial governance – Financial governance refers to the monitoring and controlling business

activities and operations. Excite ltd implement proper monitoring procedure keeps track over all

the costs and expenses. This helps in keeping the costs under control.

CONCLUSION

Management accounting plays a critical role in Excite ltd. A business cannot be run

successfully without using the management accounting tools and techniques. Management

accounting is different from that of financial accounting. Management accounting is useful for

internal management of organisation. Different management accounting systems like inventory

management, cost accounting and job costing helps it to properly record and track costs.

Planning tools used by Excite ltd helps in achieving the organisational goals and objectives

keeping the cost under control. The management accounting reports helps the management in

improving and enhancing the performance of company. Using the management accounting

Excite ltd can achieve a sustainable growth and success.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ameen, A.M., Ahmed, M.F. and Hafez, M.A.A., 2018. The Impact of Management Accounting

and How It Can Be Implemented into the Organizational Culture. Dutch Journal of

Finance and Management. 2(1).p.02.

Burritt, R.L., 2017. Cost Allocation: An Active Tool for Environmental Management

Accounting?. In The green bottom line (pp. 152-161). Routledge.

Endrikat, J., Hartmann, F. and Schreck, P., 2017. Social and ethical issues in management

accounting and control: an editorial.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting

research. Critical Perspectives on Accounting. 45. pp.63-80.

Järvinen, J.T., 2016. Role of management accounting in applying new institutional

logics. Accounting, Auditing & Accountability Journal.

Konopczak, K. and Welfe, A., 2017. Convergence-driven inflation and the channels of its

absorption. Journal of Policy Modeling. 39(6). pp.1019-1034.

Latan, H. and et.al., 2018. Effects of environmental strategy, environmental uncertainty and top

management's commitment on corporate environmental performance: The role of

environmental management accounting. Journal of cleaner production. 180. pp.297-306.

Lopez-Valeiras, E., Gomez-Conde, J. and Naranjo-Gil, D., 2015. Sustainable innovation,

management accounting and control systems, and international performance.

Sustainability. 7(3). pp.3479-3492.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

McLaren, J., Appleyard, T. and Mitchell, F., 2016. The rise and fall of management accounting

systems: A case study investigation of EVA™. The British Accounting

Review. 48(3).pp.341-358.

9

Books and Journals

Ameen, A.M., Ahmed, M.F. and Hafez, M.A.A., 2018. The Impact of Management Accounting

and How It Can Be Implemented into the Organizational Culture. Dutch Journal of

Finance and Management. 2(1).p.02.

Burritt, R.L., 2017. Cost Allocation: An Active Tool for Environmental Management

Accounting?. In The green bottom line (pp. 152-161). Routledge.

Endrikat, J., Hartmann, F. and Schreck, P., 2017. Social and ethical issues in management

accounting and control: an editorial.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting

research. Critical Perspectives on Accounting. 45. pp.63-80.

Järvinen, J.T., 2016. Role of management accounting in applying new institutional

logics. Accounting, Auditing & Accountability Journal.

Konopczak, K. and Welfe, A., 2017. Convergence-driven inflation and the channels of its

absorption. Journal of Policy Modeling. 39(6). pp.1019-1034.

Latan, H. and et.al., 2018. Effects of environmental strategy, environmental uncertainty and top

management's commitment on corporate environmental performance: The role of

environmental management accounting. Journal of cleaner production. 180. pp.297-306.

Lopez-Valeiras, E., Gomez-Conde, J. and Naranjo-Gil, D., 2015. Sustainable innovation,

management accounting and control systems, and international performance.

Sustainability. 7(3). pp.3479-3492.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

McLaren, J., Appleyard, T. and Mitchell, F., 2016. The rise and fall of management accounting

systems: A case study investigation of EVA™. The British Accounting

Review. 48(3).pp.341-358.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.