Management Accounting Case Study of Exhibition Furniture - ACC203

VerifiedAdded on 2023/06/15

|11

|1526

|283

Case Study

AI Summary

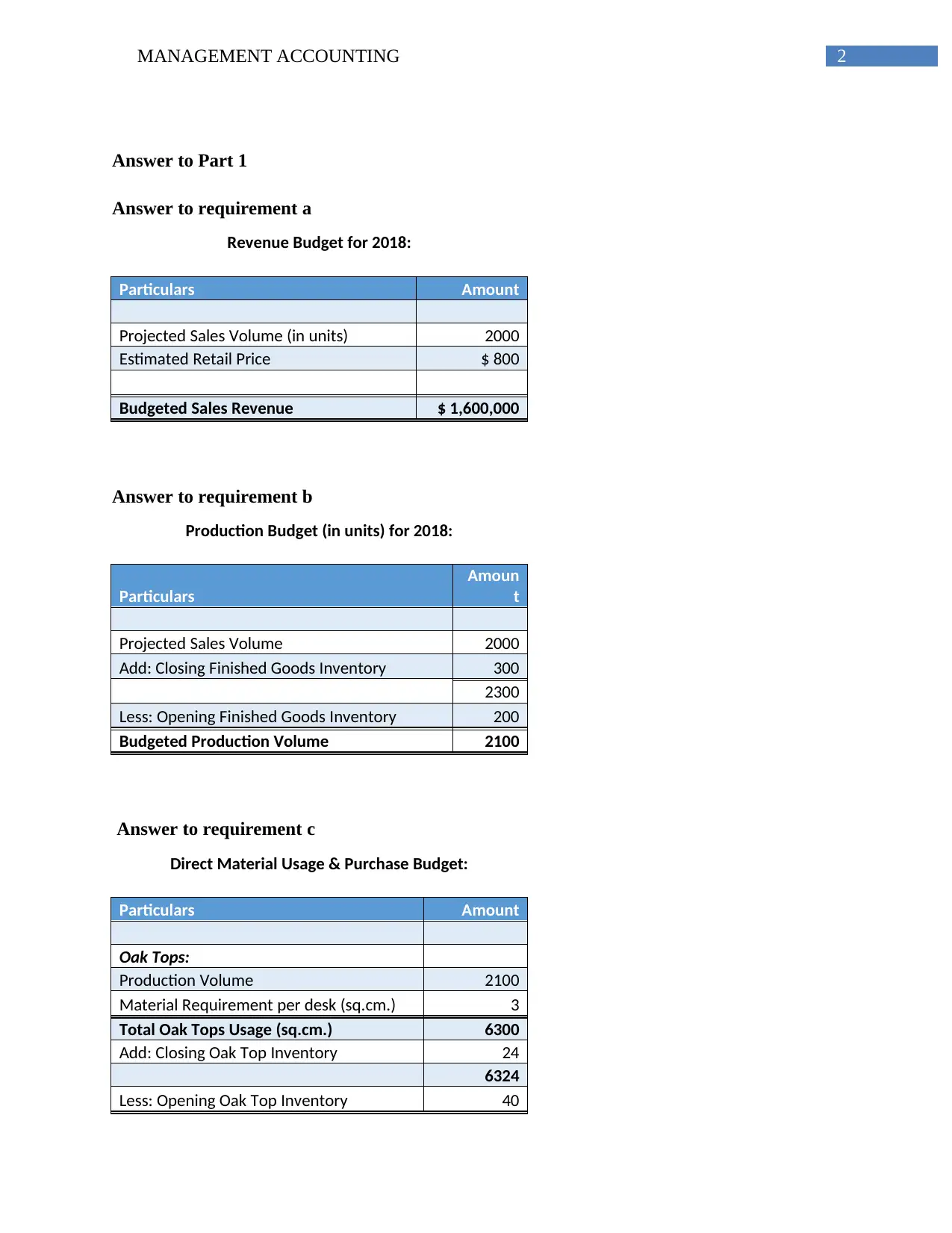

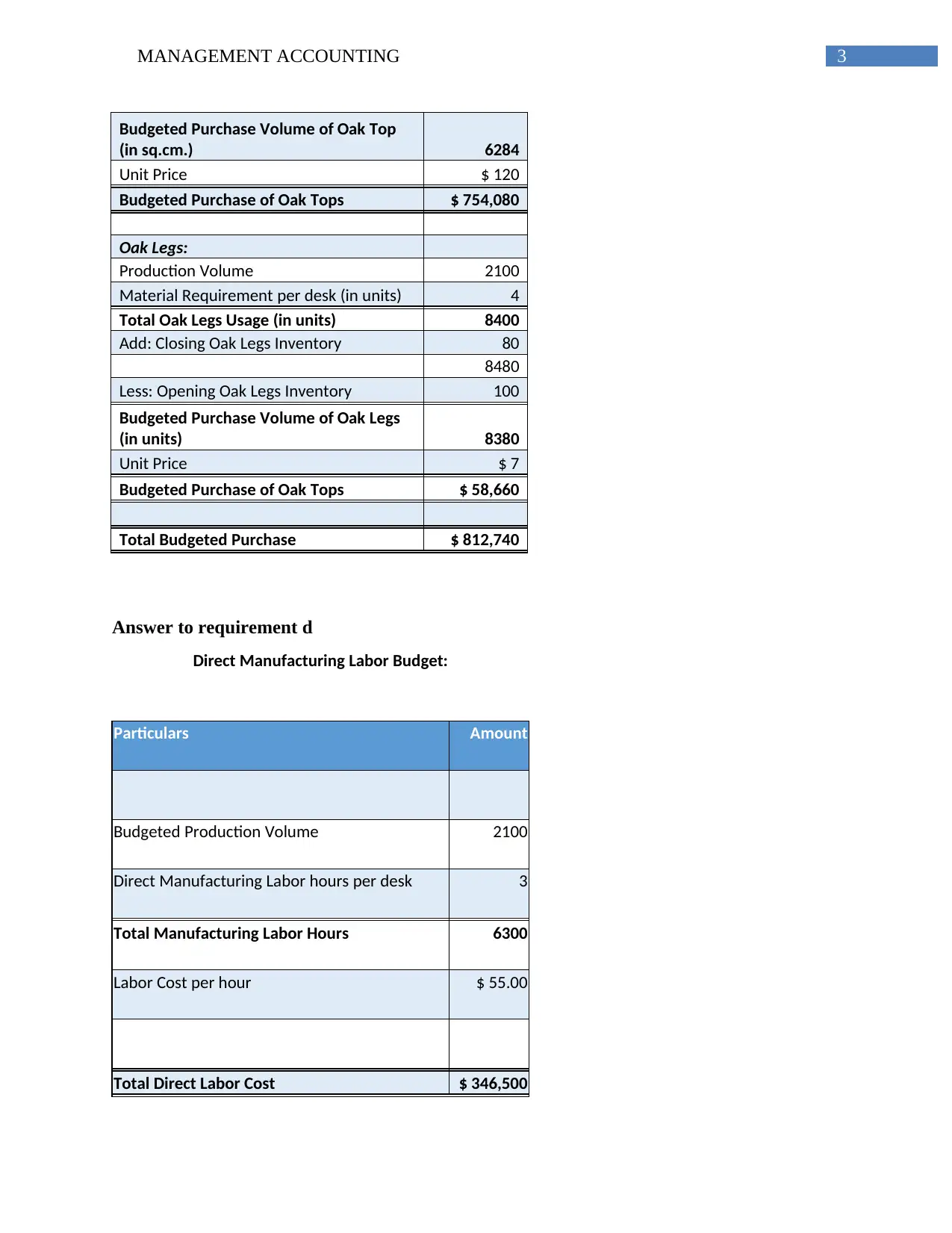

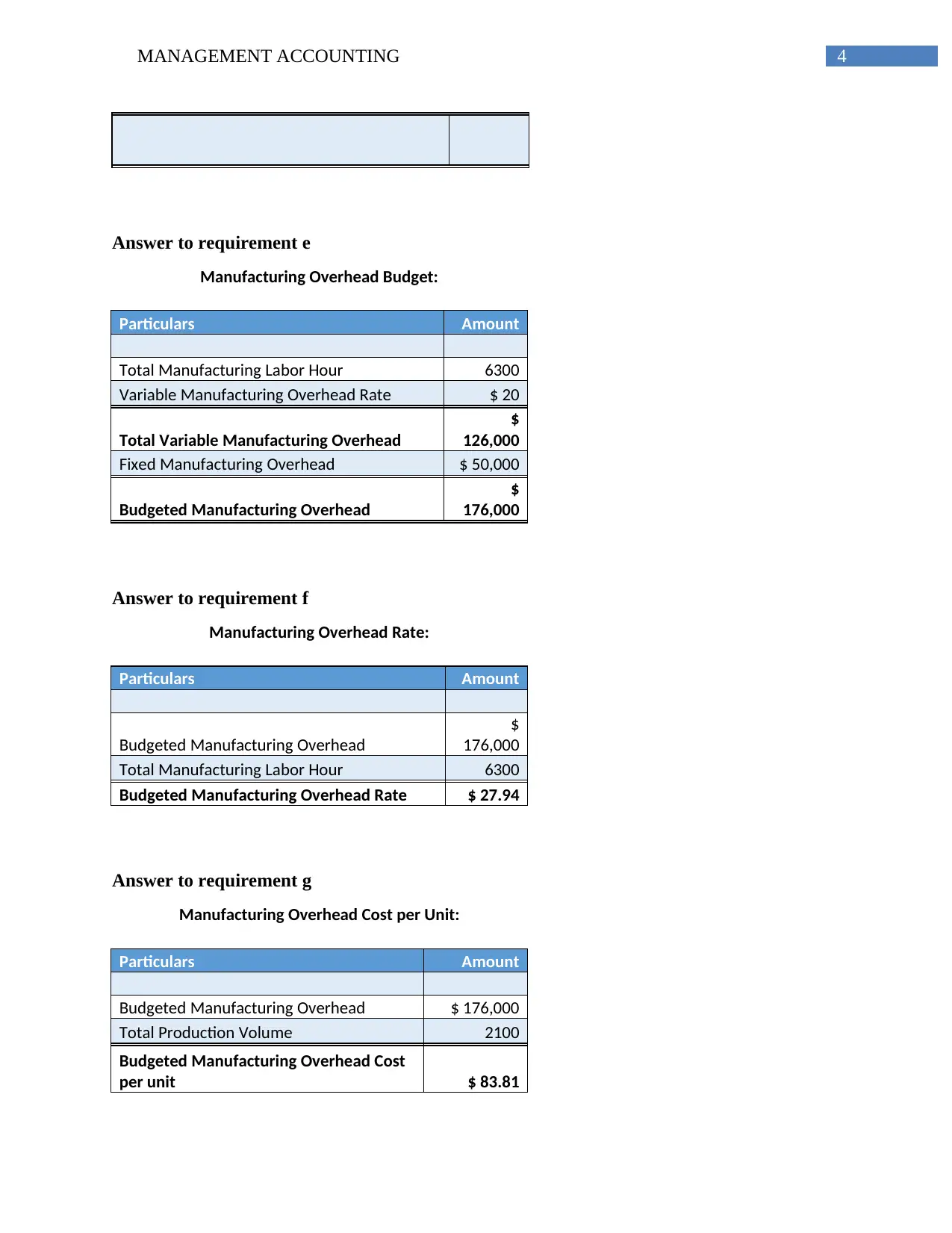

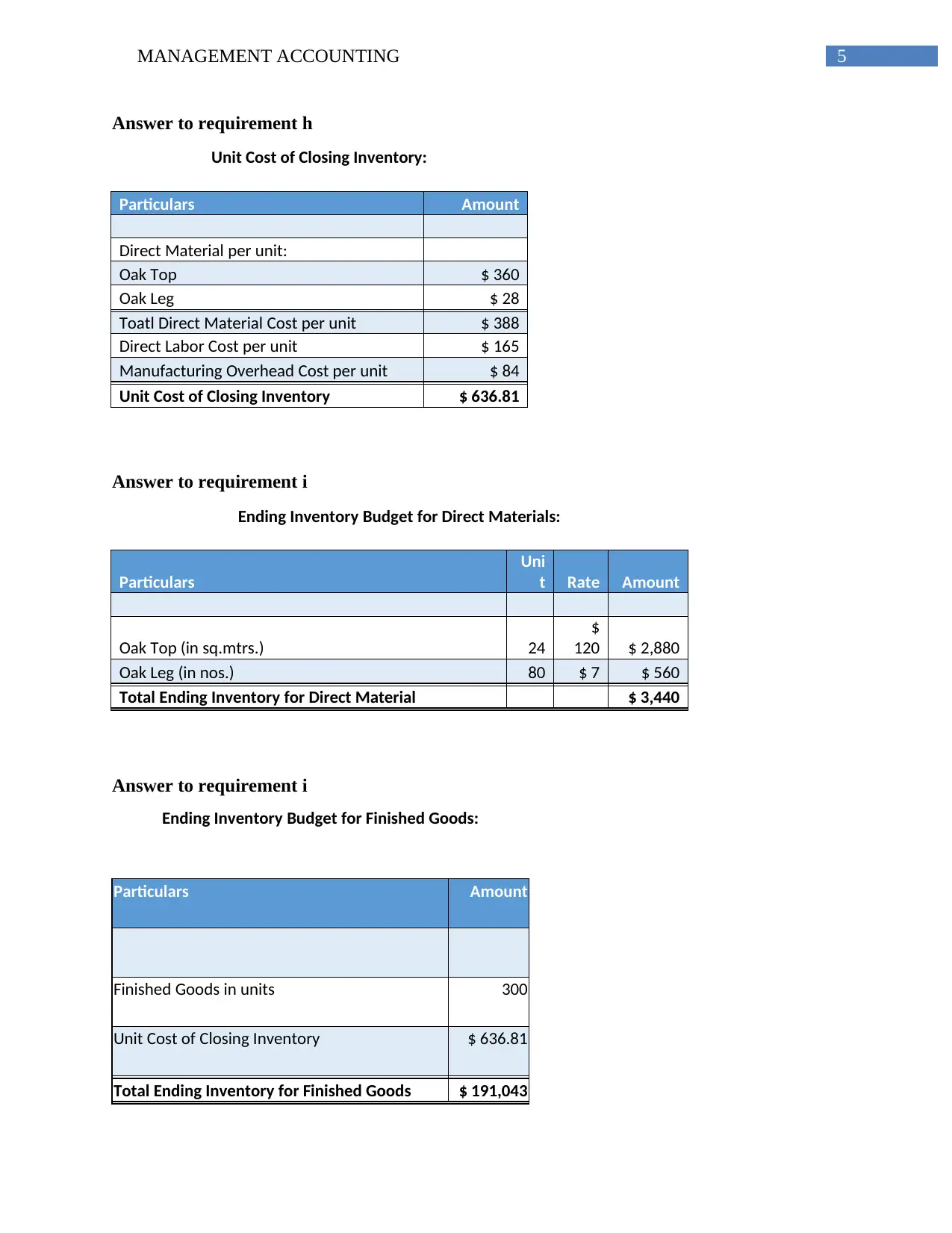

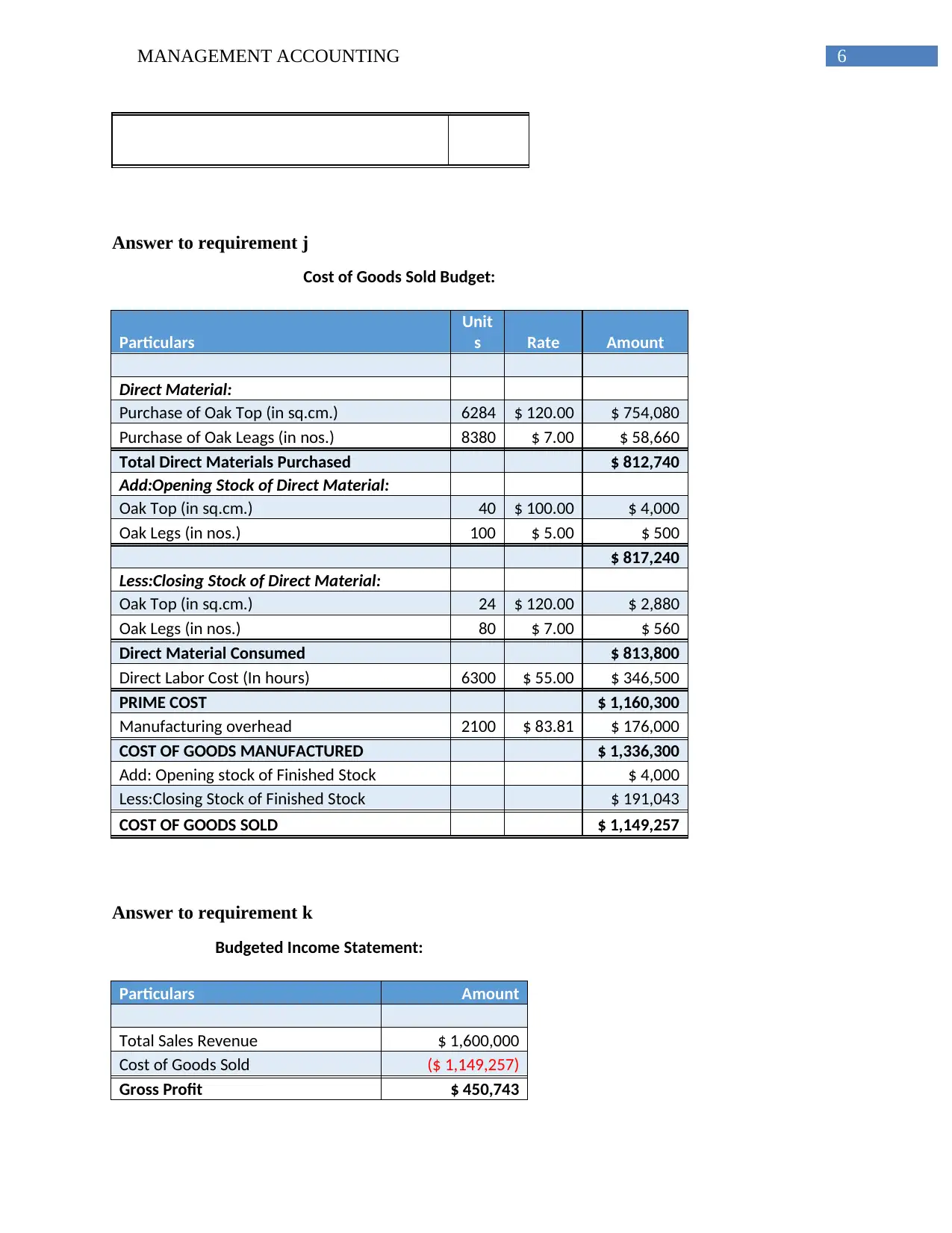

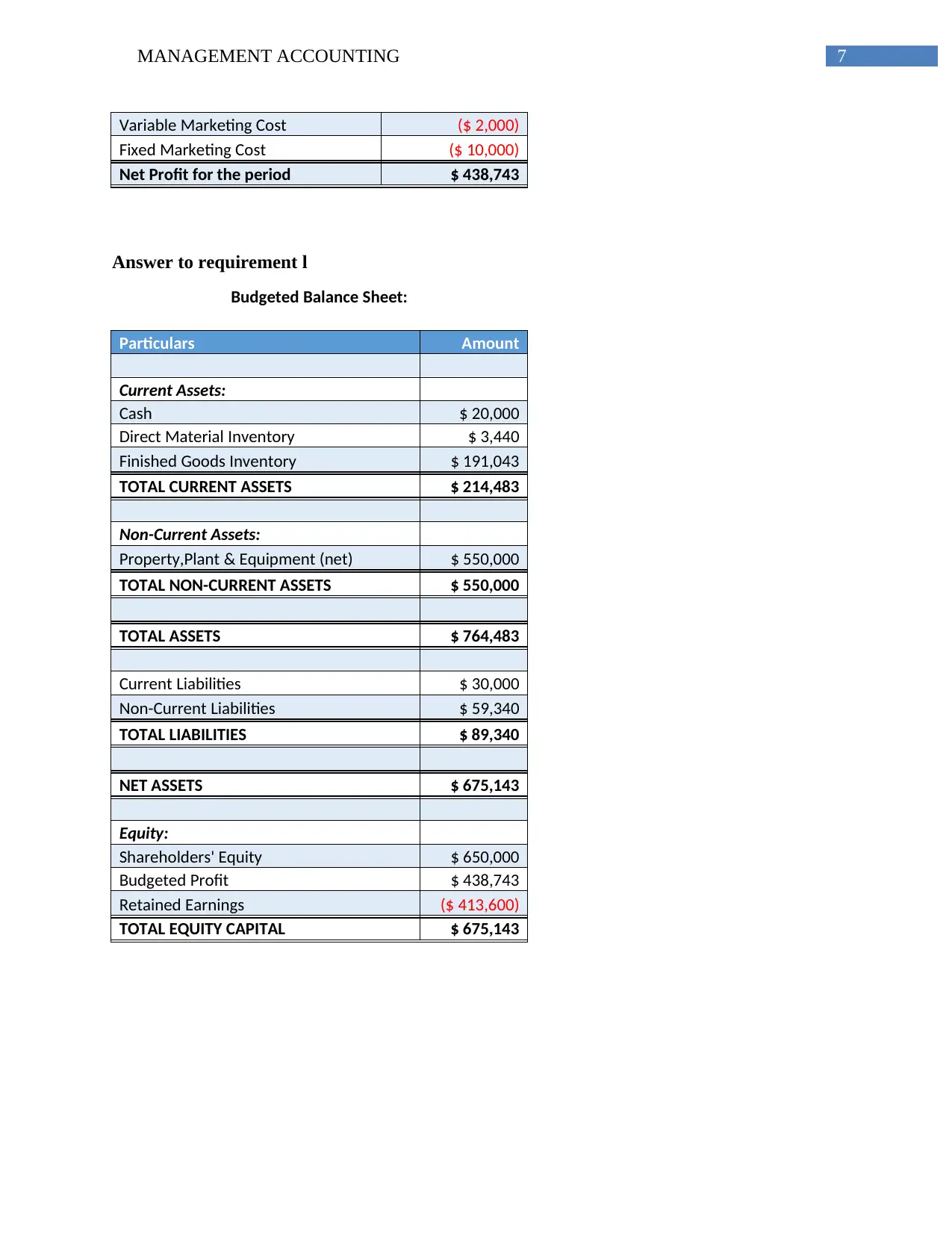

This document presents a comprehensive solution to a management accounting case study focused on Exhibition Furniture, a desk manufacturer. The solution includes a detailed revenue budget, production budget, direct material usage and purchase budget, direct manufacturing labor budget, manufacturing overhead budget, and a cost of goods sold budget. It further provides a budgeted income statement and balance sheet. The analysis covers key financial aspects such as sales forecasting, inventory management, cost control, and profitability assessment. Part two consists of a business memorandum offering recommendations for continuous improvement in budget schedules, emphasizing quarterly budgeting and variance analysis to enhance performance and strategic decision-making. The document also includes relevant calculations and justifications for the presented financial figures.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.