Unit 5 Management Accounting Report: Cost Analysis and Budgeting

VerifiedAdded on 2022/12/28

|19

|4754

|67

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within the context of Connect Catering Services. It begins with an introduction to management accounting, differentiating it from financial accounting, and highlighting the essential requirements of various management accounting systems, including cost accounting and inventory management. The report then explores different methods used for management accounting reporting, such as budget reports and job cost reports. A significant portion of the report is dedicated to cost analysis, where income statements are prepared using both marginal and absorption costing techniques. Furthermore, the advantages and disadvantages of different planning tools used for budgetary control are examined. Finally, the report compares how companies adapt their management accounting systems to respond to financial issues, providing a holistic view of the subject matter.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1 Explanation of management accounting and providing the essential requirements of

various forms of management accounting system..................................................................4

P2 Explanation of different methods used for management accounting reporting................6

TASK 2............................................................................................................................................8

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................8

TASK 3............................................................................................................................................8

P4 Explanation of the advantages and disadvantages of various forms of planning tools used

for budgetary..........................................................................................................................8

TASK 4............................................................................................................................................9

P5 compare how companies are adapting management accounting system for responding to

financial issues........................................................................................................................9

Conclusion.....................................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1 Explanation of management accounting and providing the essential requirements of

various forms of management accounting system..................................................................4

P2 Explanation of different methods used for management accounting reporting................6

TASK 2............................................................................................................................................8

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................8

TASK 3............................................................................................................................................8

P4 Explanation of the advantages and disadvantages of various forms of planning tools used

for budgetary..........................................................................................................................8

TASK 4............................................................................................................................................9

P5 compare how companies are adapting management accounting system for responding to

financial issues........................................................................................................................9

Conclusion.....................................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is defined as the procedure of preparing reports about business

operations that assist higher authorities to make long term and short term decision. In addition to

this, management accounting is basically branch of accounting which refers to the execution of

professional understanding, tools, techniques, concepts and skills for the preparation of

accounting information in a manner which facilitate the development of plans as well as policies

by the management, utilization of resources optimally, control on the operations, satisfying

stakeholders, and taking effective decision. It is state that the users of accounting statements are

mainly the internal management committee of the company. Both the non-financial and financial

factors are involved in this type of information. Management accounting facilitates in identifying

the areas which health management committee do develop corrective measures in order to

overcome the issues and improve operational efficiency (Chaudhry and Amir, 2020). It is related

to the preparation of accounting in formation in relation to professional skills and knowledge do

too which the availability of funds is easily being provided. According to the American

Accounting Association, management accounting is the process as well as concept that is needed

for the successful procedure of planning which help a company in selecting the best alternative

among different available options, then controlling as well as interpreting its results.

The present report is based on the case study of connect catering services. It is a catering

business unit that is founded by John Herring in the year 1989 and its head office is located in

Oxfordshire, UK. The report will cover about the concept of management accounting and the

various type of accounting systems will stop in addition to this, there is description of various

methods used for management accounting reporting. Moreover, the cost is calculated by using

appropriate techniques of cost analysis in order to prepare income statement using absorption

cost and marginal cost. Furthermore, the advantages as well as disadvantages of different forms

of planning tools used for budgetary control is elaborated. In the last, there is comparison of how

companies are adapting management accounting system in order to respond financial issues or

problems.

Management accounting is defined as the procedure of preparing reports about business

operations that assist higher authorities to make long term and short term decision. In addition to

this, management accounting is basically branch of accounting which refers to the execution of

professional understanding, tools, techniques, concepts and skills for the preparation of

accounting information in a manner which facilitate the development of plans as well as policies

by the management, utilization of resources optimally, control on the operations, satisfying

stakeholders, and taking effective decision. It is state that the users of accounting statements are

mainly the internal management committee of the company. Both the non-financial and financial

factors are involved in this type of information. Management accounting facilitates in identifying

the areas which health management committee do develop corrective measures in order to

overcome the issues and improve operational efficiency (Chaudhry and Amir, 2020). It is related

to the preparation of accounting in formation in relation to professional skills and knowledge do

too which the availability of funds is easily being provided. According to the American

Accounting Association, management accounting is the process as well as concept that is needed

for the successful procedure of planning which help a company in selecting the best alternative

among different available options, then controlling as well as interpreting its results.

The present report is based on the case study of connect catering services. It is a catering

business unit that is founded by John Herring in the year 1989 and its head office is located in

Oxfordshire, UK. The report will cover about the concept of management accounting and the

various type of accounting systems will stop in addition to this, there is description of various

methods used for management accounting reporting. Moreover, the cost is calculated by using

appropriate techniques of cost analysis in order to prepare income statement using absorption

cost and marginal cost. Furthermore, the advantages as well as disadvantages of different forms

of planning tools used for budgetary control is elaborated. In the last, there is comparison of how

companies are adapting management accounting system in order to respond financial issues or

problems.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

P1 Explanation of management accounting and providing the essential requirements of various

forms of management accounting system

It is the process of creating organizational objectives and goals by quantifying,

interpreting, inspecting as well as communicating instruction to the managers is known as

management accounting. It also facilitates the decision-making for the higher authorities’ by

giving them the financial information and resources. It helps the management in efficiently and

effectively perform all the operations and monitored them in a proper manner. Management

accounting includes timely preparation and providing of financial statements of an organization

to the stakeholders (Englund and Gerdin, 2018). Moreover, this reports are generally developed

for the internal stakeholders of the organization that are not highly concerned towards report.

The management accounting report includes sales revenue generation, availability of cash,

present status of account receivable and payable and many more.

The origin of management accounting is in the form of financial accounting, also there is

high difference among these two. The management accounting is more advantages, therefore is

used widely. The difference among financial accounting and management accounting is given

below:

Basis Managerial Accounting Financial Accounting

Content It is associated to the both

forms of data that is financial

as well as non-financial.

Financial accounting is only

associated with the data that

consist of financial information.

Uses and Purposes Managerial accounting is

mainly used by the internal

stakeholders in order to take

appropriate decisions.

It gives information that are

essential for stakeholders of

organisation which facilitates

decision making associated to

interests.

Rules, Regulations and Laws It does not consist of any form

of law compliance as these are

developed only for the internal

management committee of the

The different rules as well as

regulations are to be monitored

and followed by the company

accountant at the time of

P1 Explanation of management accounting and providing the essential requirements of various

forms of management accounting system

It is the process of creating organizational objectives and goals by quantifying,

interpreting, inspecting as well as communicating instruction to the managers is known as

management accounting. It also facilitates the decision-making for the higher authorities’ by

giving them the financial information and resources. It helps the management in efficiently and

effectively perform all the operations and monitored them in a proper manner. Management

accounting includes timely preparation and providing of financial statements of an organization

to the stakeholders (Englund and Gerdin, 2018). Moreover, this reports are generally developed

for the internal stakeholders of the organization that are not highly concerned towards report.

The management accounting report includes sales revenue generation, availability of cash,

present status of account receivable and payable and many more.

The origin of management accounting is in the form of financial accounting, also there is

high difference among these two. The management accounting is more advantages, therefore is

used widely. The difference among financial accounting and management accounting is given

below:

Basis Managerial Accounting Financial Accounting

Content It is associated to the both

forms of data that is financial

as well as non-financial.

Financial accounting is only

associated with the data that

consist of financial information.

Uses and Purposes Managerial accounting is

mainly used by the internal

stakeholders in order to take

appropriate decisions.

It gives information that are

essential for stakeholders of

organisation which facilitates

decision making associated to

interests.

Rules, Regulations and Laws It does not consist of any form

of law compliance as these are

developed only for the internal

management committee of the

The different rules as well as

regulations are to be monitored

and followed by the company

accountant at the time of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

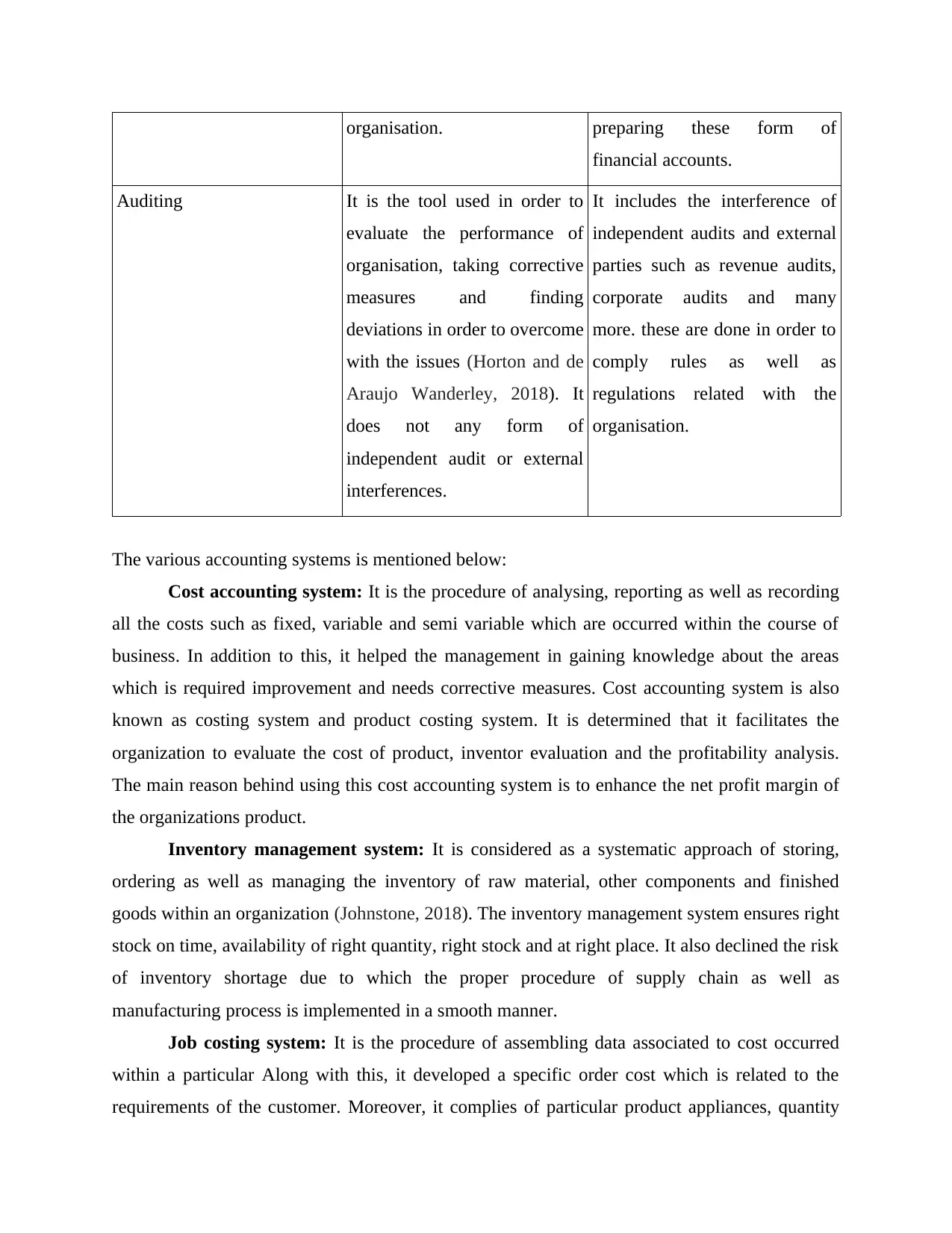

organisation. preparing these form of

financial accounts.

Auditing It is the tool used in order to

evaluate the performance of

organisation, taking corrective

measures and finding

deviations in order to overcome

with the issues (Horton and de

Araujo Wanderley, 2018). It

does not any form of

independent audit or external

interferences.

It includes the interference of

independent audits and external

parties such as revenue audits,

corporate audits and many

more. these are done in order to

comply rules as well as

regulations related with the

organisation.

The various accounting systems is mentioned below:

Cost accounting system: It is the procedure of analysing, reporting as well as recording

all the costs such as fixed, variable and semi variable which are occurred within the course of

business. In addition to this, it helped the management in gaining knowledge about the areas

which is required improvement and needs corrective measures. Cost accounting system is also

known as costing system and product costing system. It is determined that it facilitates the

organization to evaluate the cost of product, inventor evaluation and the profitability analysis.

The main reason behind using this cost accounting system is to enhance the net profit margin of

the organizations product.

Inventory management system: It is considered as a systematic approach of storing,

ordering as well as managing the inventory of raw material, other components and finished

goods within an organization (Johnstone, 2018). The inventory management system ensures right

stock on time, availability of right quantity, right stock and at right place. It also declined the risk

of inventory shortage due to which the proper procedure of supply chain as well as

manufacturing process is implemented in a smooth manner.

Job costing system: It is the procedure of assembling data associated to cost occurred

within a particular Along with this, it developed a specific order cost which is related to the

requirements of the customer. Moreover, it complies of particular product appliances, quantity

financial accounts.

Auditing It is the tool used in order to

evaluate the performance of

organisation, taking corrective

measures and finding

deviations in order to overcome

with the issues (Horton and de

Araujo Wanderley, 2018). It

does not any form of

independent audit or external

interferences.

It includes the interference of

independent audits and external

parties such as revenue audits,

corporate audits and many

more. these are done in order to

comply rules as well as

regulations related with the

organisation.

The various accounting systems is mentioned below:

Cost accounting system: It is the procedure of analysing, reporting as well as recording

all the costs such as fixed, variable and semi variable which are occurred within the course of

business. In addition to this, it helped the management in gaining knowledge about the areas

which is required improvement and needs corrective measures. Cost accounting system is also

known as costing system and product costing system. It is determined that it facilitates the

organization to evaluate the cost of product, inventor evaluation and the profitability analysis.

The main reason behind using this cost accounting system is to enhance the net profit margin of

the organizations product.

Inventory management system: It is considered as a systematic approach of storing,

ordering as well as managing the inventory of raw material, other components and finished

goods within an organization (Johnstone, 2018). The inventory management system ensures right

stock on time, availability of right quantity, right stock and at right place. It also declined the risk

of inventory shortage due to which the proper procedure of supply chain as well as

manufacturing process is implemented in a smooth manner.

Job costing system: It is the procedure of assembling data associated to cost occurred

within a particular Along with this, it developed a specific order cost which is related to the

requirements of the customer. Moreover, it complies of particular product appliances, quantity

and other connected expenses arrived within the production process. The main objective here is

to calculate as well as an ascertain the losses and profit made on the particular product or job.

Price optimizing system: It is considered as mathematical procedure to determine the

price of a particular product. In addition to this, it assists in predicting the alterations within the

price and also find out the desired price that a customer is willing to pay in order to gain product

as well as services. Moreover, price optimizing system facilitates the company for using the price

as a powerful profit lever.

P2 Explanation of different methods used for management accounting reporting

Accounting plays an important role in providing the complete picture of organization

performance in comparison to the other industry trends. It is determined that an extensive

accounting report are based on the particular period of time which gives an aggregate view of

business finances. Accounting report involves financial information from the accounting

transaction giving information about profitability, operational cost, sales revenue and many more

(Kastberg and Siverbo, 2016). It also assists higher authorities’ in taking the right decision and

instruct them towards the path for attaining objectives as well as goals of an organization. Some

of the reports developed by the higher authorities for management accounting reporting are given

below:

Budget report: It is one of the fundamental form of report that assist business owners in

controlling an acknowledging the cost occurred within the workplace. It is significant to measure

the performance of an organization and develop of budget report help in analysing it in an

effective manner. A budget is mainly prepared on the basis of past experiences and the

instruction of managers in order to offer employees incentive, negotiation with vendors and

suppliers, cost cutting and so on. Moreover, a budget gives an estimation of the company

earnings as well as expenditure and also prepare the connect catering service is to deal with the

unforeseen circumstances that can arise at any point of time.

Job cost report: This report gives a basic view of the overall cost arise on a specific task

or project and also compare it with the expected revenue yield for that particular project. Along

with this, it assists in analysing the profitability of the particular project and optimizing the

operational procedure in order to develop it more profitable. Moreover, it facilitated in

evaluating the highest earning business areas and providing less emphasize on the business

earning low returns. Job cost report also help in investigating the expenses that take place within

to calculate as well as an ascertain the losses and profit made on the particular product or job.

Price optimizing system: It is considered as mathematical procedure to determine the

price of a particular product. In addition to this, it assists in predicting the alterations within the

price and also find out the desired price that a customer is willing to pay in order to gain product

as well as services. Moreover, price optimizing system facilitates the company for using the price

as a powerful profit lever.

P2 Explanation of different methods used for management accounting reporting

Accounting plays an important role in providing the complete picture of organization

performance in comparison to the other industry trends. It is determined that an extensive

accounting report are based on the particular period of time which gives an aggregate view of

business finances. Accounting report involves financial information from the accounting

transaction giving information about profitability, operational cost, sales revenue and many more

(Kastberg and Siverbo, 2016). It also assists higher authorities’ in taking the right decision and

instruct them towards the path for attaining objectives as well as goals of an organization. Some

of the reports developed by the higher authorities for management accounting reporting are given

below:

Budget report: It is one of the fundamental form of report that assist business owners in

controlling an acknowledging the cost occurred within the workplace. It is significant to measure

the performance of an organization and develop of budget report help in analysing it in an

effective manner. A budget is mainly prepared on the basis of past experiences and the

instruction of managers in order to offer employees incentive, negotiation with vendors and

suppliers, cost cutting and so on. Moreover, a budget gives an estimation of the company

earnings as well as expenditure and also prepare the connect catering service is to deal with the

unforeseen circumstances that can arise at any point of time.

Job cost report: This report gives a basic view of the overall cost arise on a specific task

or project and also compare it with the expected revenue yield for that particular project. Along

with this, it assists in analysing the profitability of the particular project and optimizing the

operational procedure in order to develop it more profitable. Moreover, it facilitated in

evaluating the highest earning business areas and providing less emphasize on the business

earning low returns. Job cost report also help in investigating the expenses that take place within

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a project in order to decline waste and control it for making it profitable and productive for the

company.

Inventory & manufacturing budget: It is the report that summarizes the quality of

inventory used by the organization in a given period of time. In addition to this, it assists in

centralization of information associated to inventory cost, overheads included within the

production procedure and the cost of Labour related with optimally assembling of raw materials

and transforming them into the finished product (Kostyukova, 2018). The aim is to make the

prediction procedure more effective and efficient that involved labour cost, inventory wastage,

overhead costs arise per unit on other similar cost.

Order information report: It assist management committee to evaluate the business

trends that impact on the efficiency as well as effectiveness in a positive manner. The order in

formation report includes the information about multiple orders gained by the organization. It

also helps in integrating different management operations for attaining cost leadership on the

received and placed orders.

Accounts receivable aging report: It give data I thought she did to the credit balance of

customers and also involved different category items like 15 days, 60 days, 30 days and 90 days.

Along with this, it also facilitated the aligning of organizations credit policy with the customer

paying capacity. The account receivable aging report breakdown the customer balance and the

period they are owned with. It is mainly used by the higher authorities’ in order to find the issues

associated the organization credit collection procedure.

Performance report: This form of report addresses the end result of the task or the

performance of individuals in relation to the work performed by him. It also acts as a baseline for

the performance standard, analysing the variances and also take corrective measures in order to

overcome with such variances. It also involves performing indicators such as task accomplished,

goals achieved, achievements made by the organization.

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs

company.

Inventory & manufacturing budget: It is the report that summarizes the quality of

inventory used by the organization in a given period of time. In addition to this, it assists in

centralization of information associated to inventory cost, overheads included within the

production procedure and the cost of Labour related with optimally assembling of raw materials

and transforming them into the finished product (Kostyukova, 2018). The aim is to make the

prediction procedure more effective and efficient that involved labour cost, inventory wastage,

overhead costs arise per unit on other similar cost.

Order information report: It assist management committee to evaluate the business

trends that impact on the efficiency as well as effectiveness in a positive manner. The order in

formation report includes the information about multiple orders gained by the organization. It

also helps in integrating different management operations for attaining cost leadership on the

received and placed orders.

Accounts receivable aging report: It give data I thought she did to the credit balance of

customers and also involved different category items like 15 days, 60 days, 30 days and 90 days.

Along with this, it also facilitated the aligning of organizations credit policy with the customer

paying capacity. The account receivable aging report breakdown the customer balance and the

period they are owned with. It is mainly used by the higher authorities’ in order to find the issues

associated the organization credit collection procedure.

Performance report: This form of report addresses the end result of the task or the

performance of individuals in relation to the work performed by him. It also acts as a baseline for

the performance standard, analysing the variances and also take corrective measures in order to

overcome with such variances. It also involves performing indicators such as task accomplished,

goals achieved, achievements made by the organization.

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

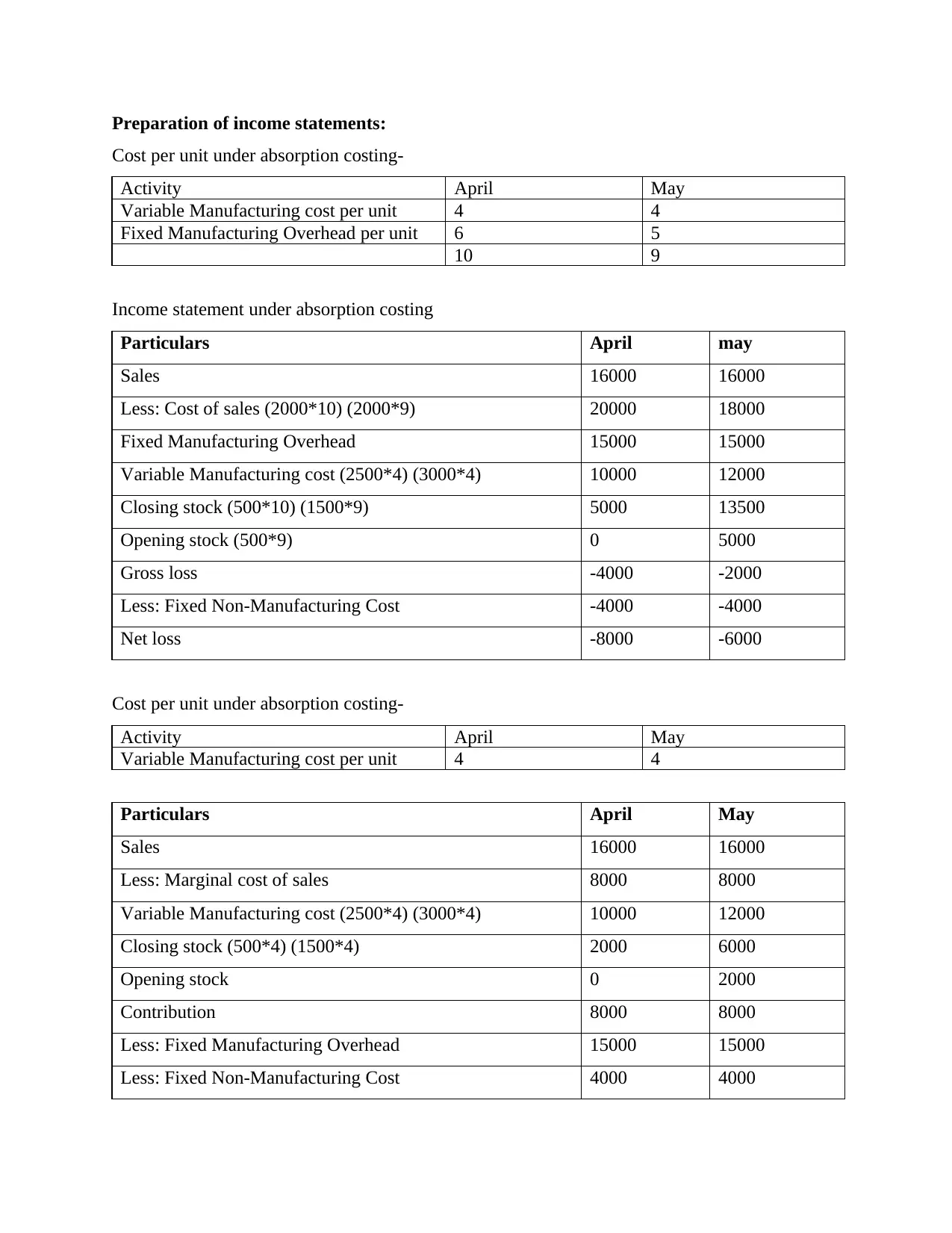

Preparation of income statements:

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

10 9

Income statement under absorption costing

Particulars April may

Sales 16000 16000

Less: Cost of sales (2000*10) (2000*9) 20000 18000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*10) (1500*9) 5000 13500

Opening stock (500*9) 0 5000

Gross loss -4000 -2000

Less: Fixed Non-Manufacturing Cost -4000 -4000

Net loss -8000 -6000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Particulars April May

Sales 16000 16000

Less: Marginal cost of sales 8000 8000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*4) (1500*4) 2000 6000

Opening stock 0 2000

Contribution 8000 8000

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non-Manufacturing Cost 4000 4000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

10 9

Income statement under absorption costing

Particulars April may

Sales 16000 16000

Less: Cost of sales (2000*10) (2000*9) 20000 18000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*10) (1500*9) 5000 13500

Opening stock (500*9) 0 5000

Gross loss -4000 -2000

Less: Fixed Non-Manufacturing Cost -4000 -4000

Net loss -8000 -6000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Particulars April May

Sales 16000 16000

Less: Marginal cost of sales 8000 8000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*4) (1500*4) 2000 6000

Opening stock 0 2000

Contribution 8000 8000

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non-Manufacturing Cost 4000 4000

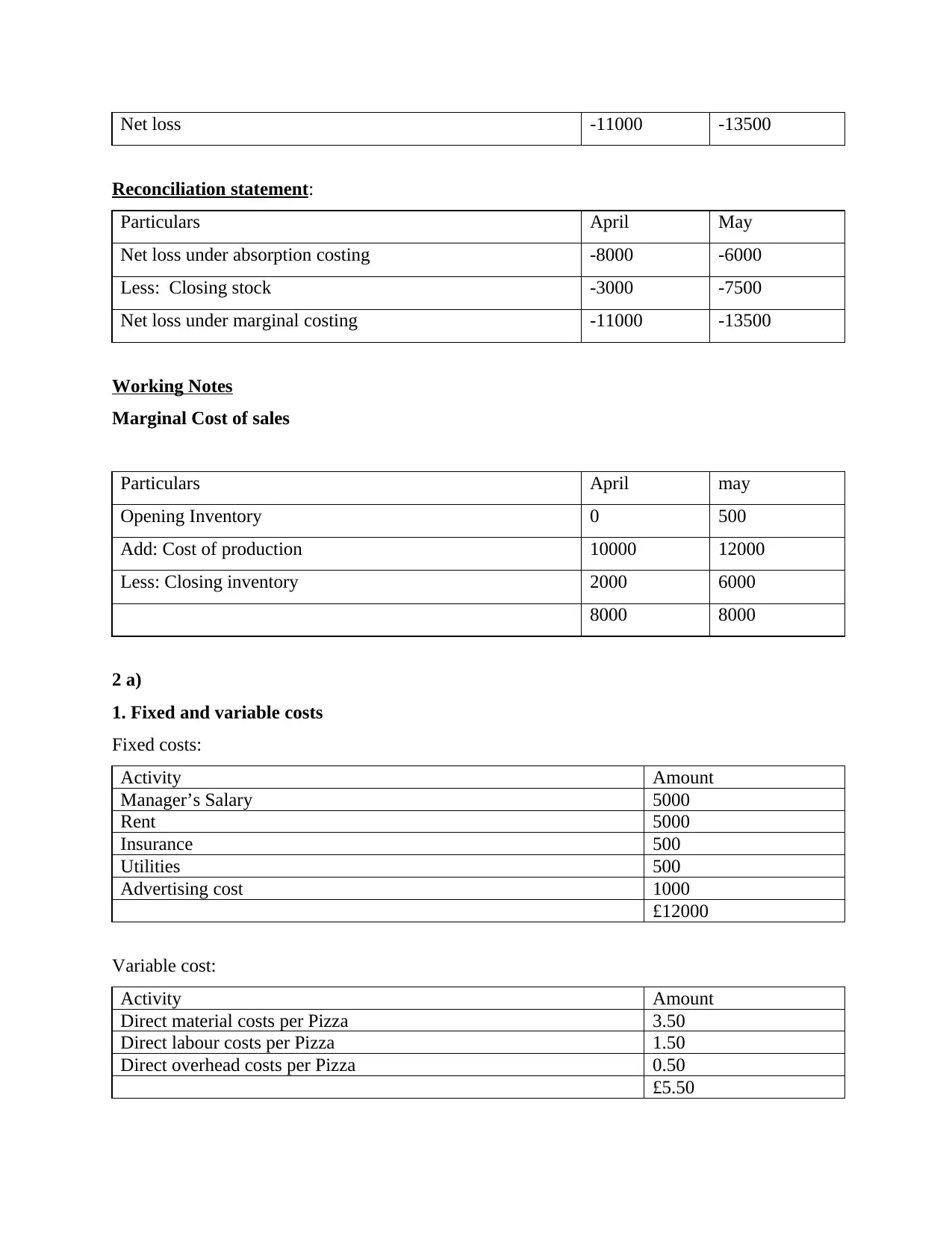

Net loss -11000 -13500

Reconciliation statement:

Particulars April May

Net loss under absorption costing -8000 -6000

Less: Closing stock -3000 -7500

Net loss under marginal costing -11000 -13500

Working Notes

Marginal Cost of sales

Particulars April may

Opening Inventory 0 500

Add: Cost of production 10000 12000

Less: Closing inventory 2000 6000

8000 8000

2 a)

1. Fixed and variable costs

Fixed costs:

Activity Amount

Manager’s Salary 5000

Rent 5000

Insurance 500

Utilities 500

Advertising cost 1000

£12000

Variable cost:

Activity Amount

Direct material costs per Pizza 3.50

Direct labour costs per Pizza 1.50

Direct overhead costs per Pizza 0.50

£5.50

Reconciliation statement:

Particulars April May

Net loss under absorption costing -8000 -6000

Less: Closing stock -3000 -7500

Net loss under marginal costing -11000 -13500

Working Notes

Marginal Cost of sales

Particulars April may

Opening Inventory 0 500

Add: Cost of production 10000 12000

Less: Closing inventory 2000 6000

8000 8000

2 a)

1. Fixed and variable costs

Fixed costs:

Activity Amount

Manager’s Salary 5000

Rent 5000

Insurance 500

Utilities 500

Advertising cost 1000

£12000

Variable cost:

Activity Amount

Direct material costs per Pizza 3.50

Direct labour costs per Pizza 1.50

Direct overhead costs per Pizza 0.50

£5.50

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

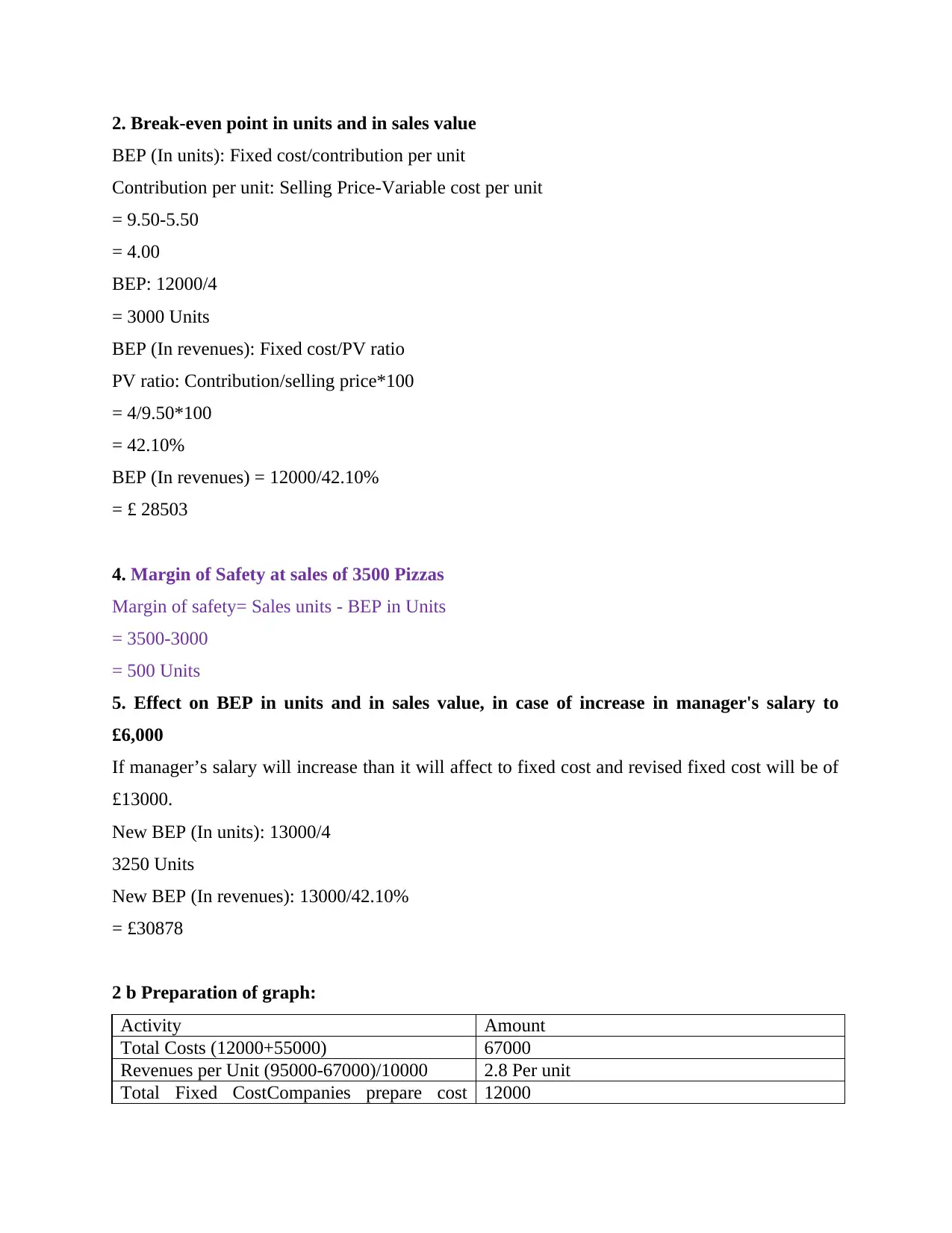

2. Break-even point in units and in sales value

BEP (In units): Fixed cost/contribution per unit

Contribution per unit: Selling Price-Variable cost per unit

= 9.50-5.50

= 4.00

BEP: 12000/4

= 3000 Units

BEP (In revenues): Fixed cost/PV ratio

PV ratio: Contribution/selling price*100

= 4/9.50*100

= 42.10%

BEP (In revenues) = 12000/42.10%

= £ 28503

4. Margin of Safety at sales of 3500 Pizzas

Margin of safety= Sales units - BEP in Units

= 3500-3000

= 500 Units

5. Effect on BEP in units and in sales value, in case of increase in manager's salary to

£6,000

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New BEP (In units): 13000/4

3250 Units

New BEP (In revenues): 13000/42.10%

= £30878

2 b Preparation of graph:

Activity Amount

Total Costs (12000+55000) 67000

Revenues per Unit (95000-67000)/10000 2.8 Per unit

Total Fixed CostCompanies prepare cost 12000

BEP (In units): Fixed cost/contribution per unit

Contribution per unit: Selling Price-Variable cost per unit

= 9.50-5.50

= 4.00

BEP: 12000/4

= 3000 Units

BEP (In revenues): Fixed cost/PV ratio

PV ratio: Contribution/selling price*100

= 4/9.50*100

= 42.10%

BEP (In revenues) = 12000/42.10%

= £ 28503

4. Margin of Safety at sales of 3500 Pizzas

Margin of safety= Sales units - BEP in Units

= 3500-3000

= 500 Units

5. Effect on BEP in units and in sales value, in case of increase in manager's salary to

£6,000

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New BEP (In units): 13000/4

3250 Units

New BEP (In revenues): 13000/42.10%

= £30878

2 b Preparation of graph:

Activity Amount

Total Costs (12000+55000) 67000

Revenues per Unit (95000-67000)/10000 2.8 Per unit

Total Fixed CostCompanies prepare cost 12000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budget which is used to find variance in

actual cost incurred and budgeted target. Cost

budgets shall be flexible enough to

incorporate changes in targets as and when

they arise.

BEP point 28503

TASK 3

P4 Explanation of the advantages and disadvantages of various forms of planning tools used for

budgetary

The management accounting tools involved the procedure as well as techniques which

assist organizations managing committee to take effective and appropriate decisions. The Main

objective here is to enhance an improved performance, attaining strategic aims and objectives,

adding value within the organizational procedure and many more. there are different functions

executed by the management committee such as controlling, price fixing, planning and many

more that required different form of tools.

Firstly, planning of business activities is taking place on the basis of supervision and

observing functions. The tool which is used by the management is budgeting for the same.

Budget is basically an approximately forecasting of expenses occurred & revenue earned

through the organization within stipulated time period (Maas, Schaltegger and Crutzen, 2016). It

is a form of financial plan that defines the period, and also involved the money given or a sign in

order to attain particular object. The budget is mainly categorized into two forms that is

operational budget as well as capital budget. The few different budgets developed by the higher

authorities’ of connect catering services artist follows:

Cash budget: It is the estimated amount which involves the cash inflow as well as

outflow within a given time frame. In addition to this, it helps manage are in analyzing the nature

and source of flows. It also determines the cash availability and the allocation of it over a

particular time period.

Advantages: It assist in avoiding the situation that is under or over liquidity which

impact on the flow of business operations.

actual cost incurred and budgeted target. Cost

budgets shall be flexible enough to

incorporate changes in targets as and when

they arise.

BEP point 28503

TASK 3

P4 Explanation of the advantages and disadvantages of various forms of planning tools used for

budgetary

The management accounting tools involved the procedure as well as techniques which

assist organizations managing committee to take effective and appropriate decisions. The Main

objective here is to enhance an improved performance, attaining strategic aims and objectives,

adding value within the organizational procedure and many more. there are different functions

executed by the management committee such as controlling, price fixing, planning and many

more that required different form of tools.

Firstly, planning of business activities is taking place on the basis of supervision and

observing functions. The tool which is used by the management is budgeting for the same.

Budget is basically an approximately forecasting of expenses occurred & revenue earned

through the organization within stipulated time period (Maas, Schaltegger and Crutzen, 2016). It

is a form of financial plan that defines the period, and also involved the money given or a sign in

order to attain particular object. The budget is mainly categorized into two forms that is

operational budget as well as capital budget. The few different budgets developed by the higher

authorities’ of connect catering services artist follows:

Cash budget: It is the estimated amount which involves the cash inflow as well as

outflow within a given time frame. In addition to this, it helps manage are in analyzing the nature

and source of flows. It also determines the cash availability and the allocation of it over a

particular time period.

Advantages: It assist in avoiding the situation that is under or over liquidity which

impact on the flow of business operations.

Disadvantages: It is determined that cash budget is prepared on the estimation and is not

accurate at every time. Along with this, it is rigid in nature and did not undertaken

uncertainty of the changing business environment.

Sales Budget: This form of Buzzard assists in forecasting the sales of organizations good

and services within a financial year or within a specified time period. In addition to this, it

assists in formulation of strategies that help in improving sales and enhancing profitability.

Advantages: It is important to prepared sales budget as it helps in formulation and

execution of master budget within an organization. It also assists management in

estimating revenue earned by the sales of its goods as well as services.

Disadvantages: It is stated that the business environment is uncertain and dynamic,

also the demand as well as supply of product and services is unpredictable, therefore

there is high probability of inaccurate sales forecast that results in over and under

production that may arise high loss to the organization (Messner, 2016).

TASK 4

P5 compare how companies are adapting management accounting system for responding to

financial issues

Financial problems are mainly the circumstances in which the company is not able to fulfil

its financial obligations because of insufficient funds or money is available to them. In addition

to this, it can happen because of high fixed operational cost, revenue sensitive the cause of

economic downfall, high level of non-liquid funds, poor busting and many more. Financial

problem is also an indicator of company's bankruptcy and causing a damage on its brand image

and credibility. The financial management involves effective capital structure development,

budget formulation and so on. If the higher authorities fail in managing any of the financial

management factors, then it may develop financial problems within an organization. Some of the

financial problems that arise are given below:

Unwanted high cost: This issue is associated with the alteration in the cost occurred, that

results in decline in profit margin of organization. In addition to this, increase in cost can

be arise due to employee execution of activities not as per the requirements, uninterrupted

use of technology, non-execution of business operations and many more. All such

conditions can be hazardous and negative for the survival of company at marketplace. In

accurate at every time. Along with this, it is rigid in nature and did not undertaken

uncertainty of the changing business environment.

Sales Budget: This form of Buzzard assists in forecasting the sales of organizations good

and services within a financial year or within a specified time period. In addition to this, it

assists in formulation of strategies that help in improving sales and enhancing profitability.

Advantages: It is important to prepared sales budget as it helps in formulation and

execution of master budget within an organization. It also assists management in

estimating revenue earned by the sales of its goods as well as services.

Disadvantages: It is stated that the business environment is uncertain and dynamic,

also the demand as well as supply of product and services is unpredictable, therefore

there is high probability of inaccurate sales forecast that results in over and under

production that may arise high loss to the organization (Messner, 2016).

TASK 4

P5 compare how companies are adapting management accounting system for responding to

financial issues

Financial problems are mainly the circumstances in which the company is not able to fulfil

its financial obligations because of insufficient funds or money is available to them. In addition

to this, it can happen because of high fixed operational cost, revenue sensitive the cause of

economic downfall, high level of non-liquid funds, poor busting and many more. Financial

problem is also an indicator of company's bankruptcy and causing a damage on its brand image

and credibility. The financial management involves effective capital structure development,

budget formulation and so on. If the higher authorities fail in managing any of the financial

management factors, then it may develop financial problems within an organization. Some of the

financial problems that arise are given below:

Unwanted high cost: This issue is associated with the alteration in the cost occurred, that

results in decline in profit margin of organization. In addition to this, increase in cost can

be arise due to employee execution of activities not as per the requirements, uninterrupted

use of technology, non-execution of business operations and many more. All such

conditions can be hazardous and negative for the survival of company at marketplace. In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.