Management Accounting Techniques, Planning, and Financial Problems

VerifiedAdded on 2023/01/12

|16

|3470

|91

Report

AI Summary

This report delves into the core principles of management accounting within a business context, focusing on the role of a managerial accountant. It includes detailed cost calculations using both marginal and absorption costing methods, highlighting their respective advantages and significance through the creation of income statements. The report also addresses common financial challenges faced by managerial accountants and proposes solutions using various costing management techniques. Furthermore, it explores accounting finance tools and techniques for budgeting and sales forecasting, emphasizing the importance of key performance indicators (KPIs) in measuring actual performance. The concept of sustainable success is discussed, underscoring its importance for firms and its contribution to net worth.

B09774

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

L0. 2: Apply a range of management accounting techniques..........................................................4

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................4

M2. Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents.....................................................................................................9

LO. 3: Explain the use of planning tools used in management accounting using budgets for

planning and control......................................................................................................................10

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................10

M3. Use of different planning tools and their application for preparing and forecasting budgets

...................................................................................................................................................12

LO.4: Compare ways in which organizations could use management accounting to respond to

financial problems.........................................................................................................................13

P5. Compare how organizations are adapting management accounting systems to respond

financial problems.....................................................................................................................13

M4. Analyze how, in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

L0. 2: Apply a range of management accounting techniques..........................................................4

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................4

M2. Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents.....................................................................................................9

LO. 3: Explain the use of planning tools used in management accounting using budgets for

planning and control......................................................................................................................10

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................10

M3. Use of different planning tools and their application for preparing and forecasting budgets

...................................................................................................................................................12

LO.4: Compare ways in which organizations could use management accounting to respond to

financial problems.........................................................................................................................13

P5. Compare how organizations are adapting management accounting systems to respond

financial problems.....................................................................................................................13

M4. Analyze how, in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

This project report is based on fundamentals of management accounting practice in business

environment by managerial accountant. Report consist calculation of costs on the basis of two

methods; marginal costing and absorption costing. Both costing methods have their advantage

and importance which is discussed by showing calculation of income statement through marginal

and absorption method. Some of the financial problems face by managerial accountant is also

discussed and how to solve these issues will reveal methods of costing management. Tools and

techniques of accounting finance will explore options which can be adopt by management to

budget or forecast its sales and also importance of key performance indicators to measure actual

performance has been shown in this project report. Sustainable success concept will show why it

is important to achieve by every firm and what value do it added to firm’s net worth.

This project report is based on fundamentals of management accounting practice in business

environment by managerial accountant. Report consist calculation of costs on the basis of two

methods; marginal costing and absorption costing. Both costing methods have their advantage

and importance which is discussed by showing calculation of income statement through marginal

and absorption method. Some of the financial problems face by managerial accountant is also

discussed and how to solve these issues will reveal methods of costing management. Tools and

techniques of accounting finance will explore options which can be adopt by management to

budget or forecast its sales and also importance of key performance indicators to measure actual

performance has been shown in this project report. Sustainable success concept will show why it

is important to achieve by every firm and what value do it added to firm’s net worth.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

L0. 2: Apply a range of management accounting techniques

P3. Calculate costs using appropriate techniques of cost analysis to prepare

an income statement using marginal and absorption costs

Cost: Also known as expenses and categories into two types; variable and fixed costs and

in income statement it further divided into two parts; direct and indirect expenses. Direct

expenses are those which are directly associated with production of finished goods;

indirect costs are not directly associated with manufacturing but it supports to reach

customers.

Different costs and cost analysis:

Variable costs: These are flexible expenses which increase with the increase in

production. Mostly it is calculated on per unit basis to decide price of product and also

known as marginal cost of the product.

Fixed costs: As per name it is fixed in nature and doesn’t change with production. It is

liability for every business and not tolerable for example; rent expenses, lighting and

salaries (Budgeting software, 2020).

Further classification of costs on the basis of method;

Marginal costing: This costing method also known as contribution margin. It concerns all

types of expenses which are variable in nature to calculate cost per unit. This variable per

costs deducts from selling price per unit to get contribution per unit.

Absorption costing: It absorbs all the expenses both fixed and variable associated with

production directly to absorb at the time of manufacturing.

Quarter 1 & 2

Calculation of product cost per unit:

Quarter Quarter

P3. Calculate costs using appropriate techniques of cost analysis to prepare

an income statement using marginal and absorption costs

Cost: Also known as expenses and categories into two types; variable and fixed costs and

in income statement it further divided into two parts; direct and indirect expenses. Direct

expenses are those which are directly associated with production of finished goods;

indirect costs are not directly associated with manufacturing but it supports to reach

customers.

Different costs and cost analysis:

Variable costs: These are flexible expenses which increase with the increase in

production. Mostly it is calculated on per unit basis to decide price of product and also

known as marginal cost of the product.

Fixed costs: As per name it is fixed in nature and doesn’t change with production. It is

liability for every business and not tolerable for example; rent expenses, lighting and

salaries (Budgeting software, 2020).

Further classification of costs on the basis of method;

Marginal costing: This costing method also known as contribution margin. It concerns all

types of expenses which are variable in nature to calculate cost per unit. This variable per

costs deducts from selling price per unit to get contribution per unit.

Absorption costing: It absorbs all the expenses both fixed and variable associated with

production directly to absorb at the time of manufacturing.

Quarter 1 & 2

Calculation of product cost per unit:

Quarter Quarter

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 2

Variable Cost (78000 ×

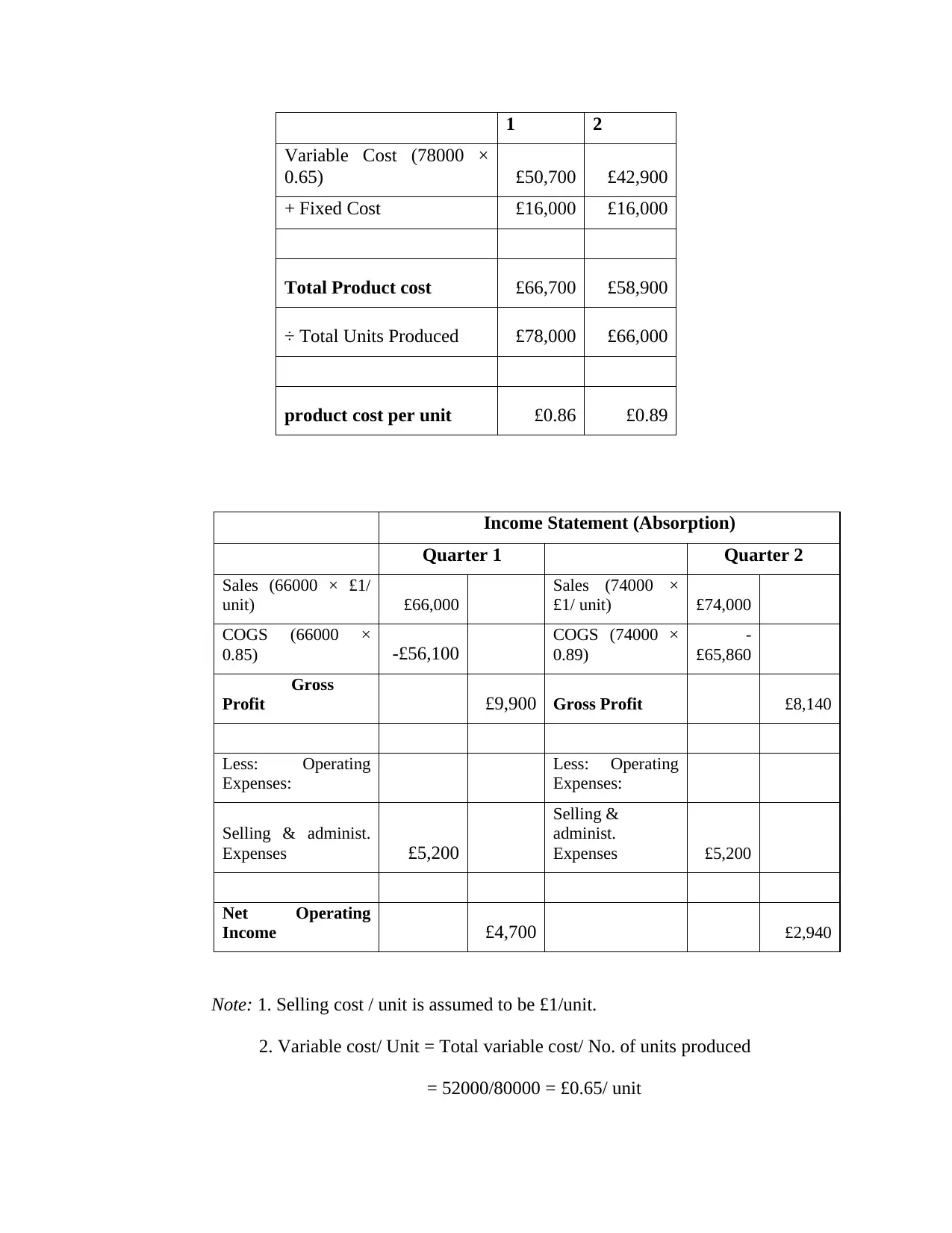

0.65) £50,700 £42,900

+ Fixed Cost £16,000 £16,000

Total Product cost £66,700 £58,900

÷ Total Units Produced £78,000 £66,000

product cost per unit £0.86 £0.89

Income Statement (Absorption)

Quarter 1 Quarter 2

Sales (66000 × £1/

unit) £66,000

Sales (74000 ×

£1/ unit) £74,000

COGS (66000 ×

0.85) -£56,100

COGS (74000 ×

0.89)

-

£65,860

Gross

Profit £9,900 Gross Profit £8,140

Less: Operating

Expenses:

Less: Operating

Expenses:

Selling & administ.

Expenses £5,200

Selling &

administ.

Expenses £5,200

Net Operating

Income £4,700 £2,940

Note: 1. Selling cost / unit is assumed to be £1/unit.

2. Variable cost/ Unit = Total variable cost/ No. of units produced

= 52000/80000 = £0.65/ unit

Variable Cost (78000 ×

0.65) £50,700 £42,900

+ Fixed Cost £16,000 £16,000

Total Product cost £66,700 £58,900

÷ Total Units Produced £78,000 £66,000

product cost per unit £0.86 £0.89

Income Statement (Absorption)

Quarter 1 Quarter 2

Sales (66000 × £1/

unit) £66,000

Sales (74000 ×

£1/ unit) £74,000

COGS (66000 ×

0.85) -£56,100

COGS (74000 ×

0.89)

-

£65,860

Gross

Profit £9,900 Gross Profit £8,140

Less: Operating

Expenses:

Less: Operating

Expenses:

Selling & administ.

Expenses £5,200

Selling &

administ.

Expenses £5,200

Net Operating

Income £4,700 £2,940

Note: 1. Selling cost / unit is assumed to be £1/unit.

2. Variable cost/ Unit = Total variable cost/ No. of units produced

= 52000/80000 = £0.65/ unit

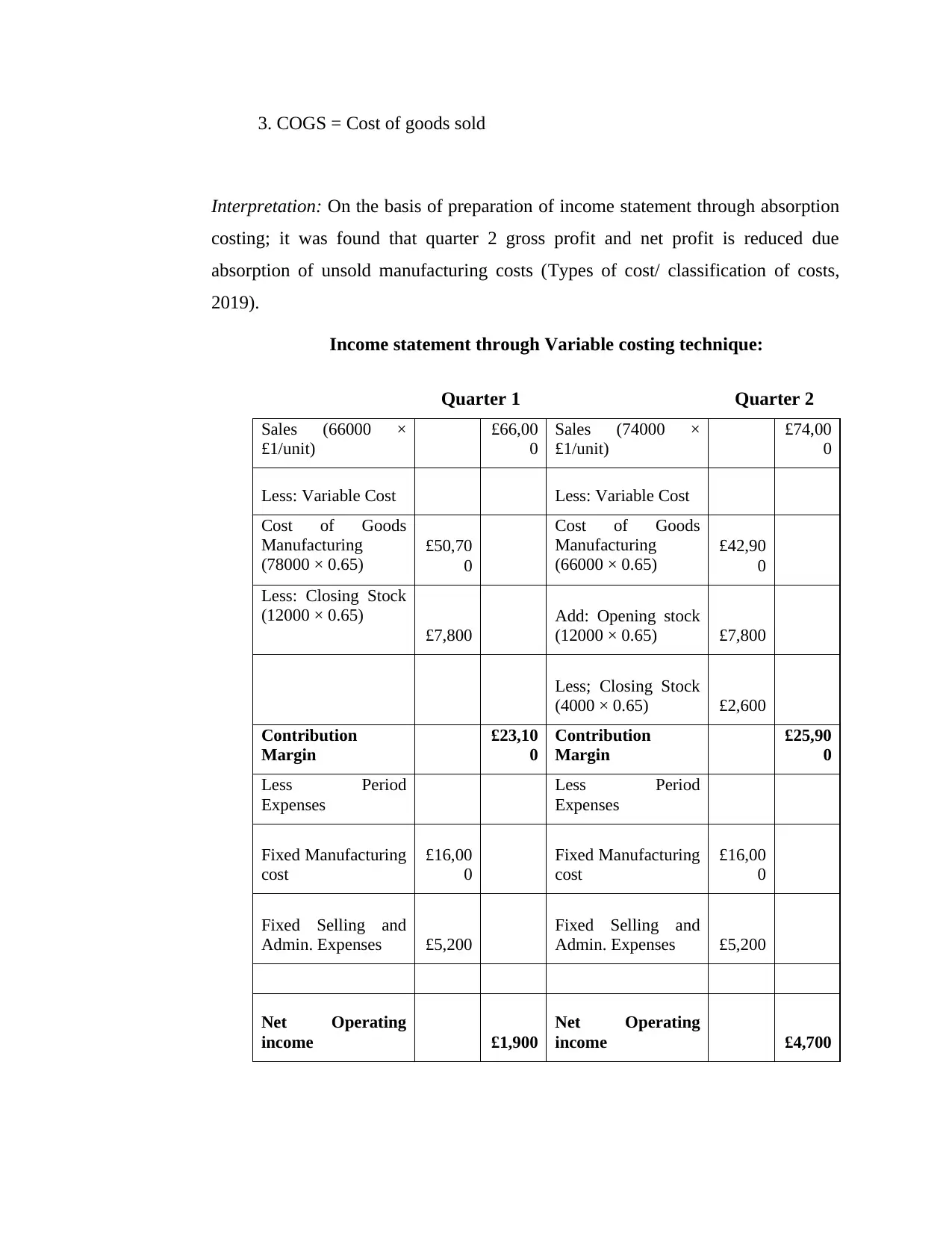

3. COGS = Cost of goods sold

Interpretation: On the basis of preparation of income statement through absorption

costing; it was found that quarter 2 gross profit and net profit is reduced due

absorption of unsold manufacturing costs (Types of cost/ classification of costs,

2019).

Income statement through Variable costing technique:

Quarter 1 Quarter 2

Sales (66000 ×

£1/unit)

£66,00

0

Sales (74000 ×

£1/unit)

£74,00

0

Less: Variable Cost Less: Variable Cost

Cost of Goods

Manufacturing

(78000 × 0.65)

£50,70

0

Cost of Goods

Manufacturing

(66000 × 0.65)

£42,90

0

Less: Closing Stock

(12000 × 0.65)

£7,800

Add: Opening stock

(12000 × 0.65) £7,800

Less; Closing Stock

(4000 × 0.65) £2,600

Contribution

Margin

£23,10

0

Contribution

Margin

£25,90

0

Less Period

Expenses

Less Period

Expenses

Fixed Manufacturing

cost

£16,00

0

Fixed Manufacturing

cost

£16,00

0

Fixed Selling and

Admin. Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Net Operating

income £1,900

Net Operating

income £4,700

Interpretation: On the basis of preparation of income statement through absorption

costing; it was found that quarter 2 gross profit and net profit is reduced due

absorption of unsold manufacturing costs (Types of cost/ classification of costs,

2019).

Income statement through Variable costing technique:

Quarter 1 Quarter 2

Sales (66000 ×

£1/unit)

£66,00

0

Sales (74000 ×

£1/unit)

£74,00

0

Less: Variable Cost Less: Variable Cost

Cost of Goods

Manufacturing

(78000 × 0.65)

£50,70

0

Cost of Goods

Manufacturing

(66000 × 0.65)

£42,90

0

Less: Closing Stock

(12000 × 0.65)

£7,800

Add: Opening stock

(12000 × 0.65) £7,800

Less; Closing Stock

(4000 × 0.65) £2,600

Contribution

Margin

£23,10

0

Contribution

Margin

£25,90

0

Less Period

Expenses

Less Period

Expenses

Fixed Manufacturing

cost

£16,00

0

Fixed Manufacturing

cost

£16,00

0

Fixed Selling and

Admin. Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Net Operating

income £1,900

Net Operating

income £4,700

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

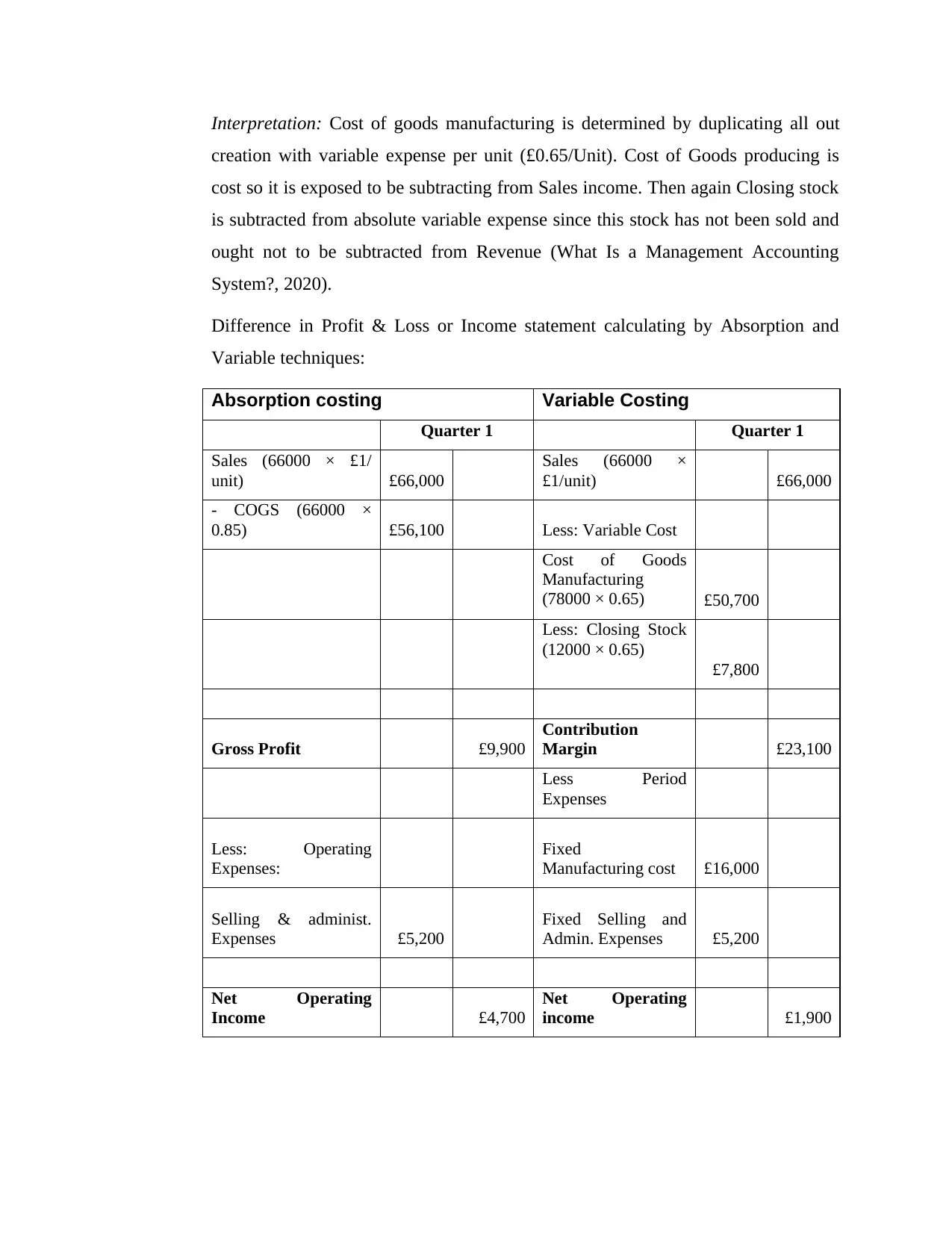

Interpretation: Cost of goods manufacturing is determined by duplicating all out

creation with variable expense per unit (£0.65/Unit). Cost of Goods producing is

cost so it is exposed to be subtracting from Sales income. Then again Closing stock

is subtracted from absolute variable expense since this stock has not been sold and

ought not to be subtracted from Revenue (What Is a Management Accounting

System?, 2020).

Difference in Profit & Loss or Income statement calculating by Absorption and

Variable techniques:

Absorption costing Variable Costing

Quarter 1 Quarter 1

Sales (66000 × £1/

unit) £66,000

Sales (66000 ×

£1/unit) £66,000

- COGS (66000 ×

0.85) £56,100 Less: Variable Cost

Cost of Goods

Manufacturing

(78000 × 0.65) £50,700

Less: Closing Stock

(12000 × 0.65)

£7,800

Gross Profit £9,900

Contribution

Margin £23,100

Less Period

Expenses

Less: Operating

Expenses:

Fixed

Manufacturing cost £16,000

Selling & administ.

Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Net Operating

Income £4,700

Net Operating

income £1,900

creation with variable expense per unit (£0.65/Unit). Cost of Goods producing is

cost so it is exposed to be subtracting from Sales income. Then again Closing stock

is subtracted from absolute variable expense since this stock has not been sold and

ought not to be subtracted from Revenue (What Is a Management Accounting

System?, 2020).

Difference in Profit & Loss or Income statement calculating by Absorption and

Variable techniques:

Absorption costing Variable Costing

Quarter 1 Quarter 1

Sales (66000 × £1/

unit) £66,000

Sales (66000 ×

£1/unit) £66,000

- COGS (66000 ×

0.85) £56,100 Less: Variable Cost

Cost of Goods

Manufacturing

(78000 × 0.65) £50,700

Less: Closing Stock

(12000 × 0.65)

£7,800

Gross Profit £9,900

Contribution

Margin £23,100

Less Period

Expenses

Less: Operating

Expenses:

Fixed

Manufacturing cost £16,000

Selling & administ.

Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Net Operating

Income £4,700

Net Operating

income £1,900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: Income through absorption costing shows less gross profit than

variable costing method; the main reason behind this difference is calculation of per

unit variable and fixed cost. Another reason for variance is variable cost of

manufacturing product; which is not considered by Variable costing method.

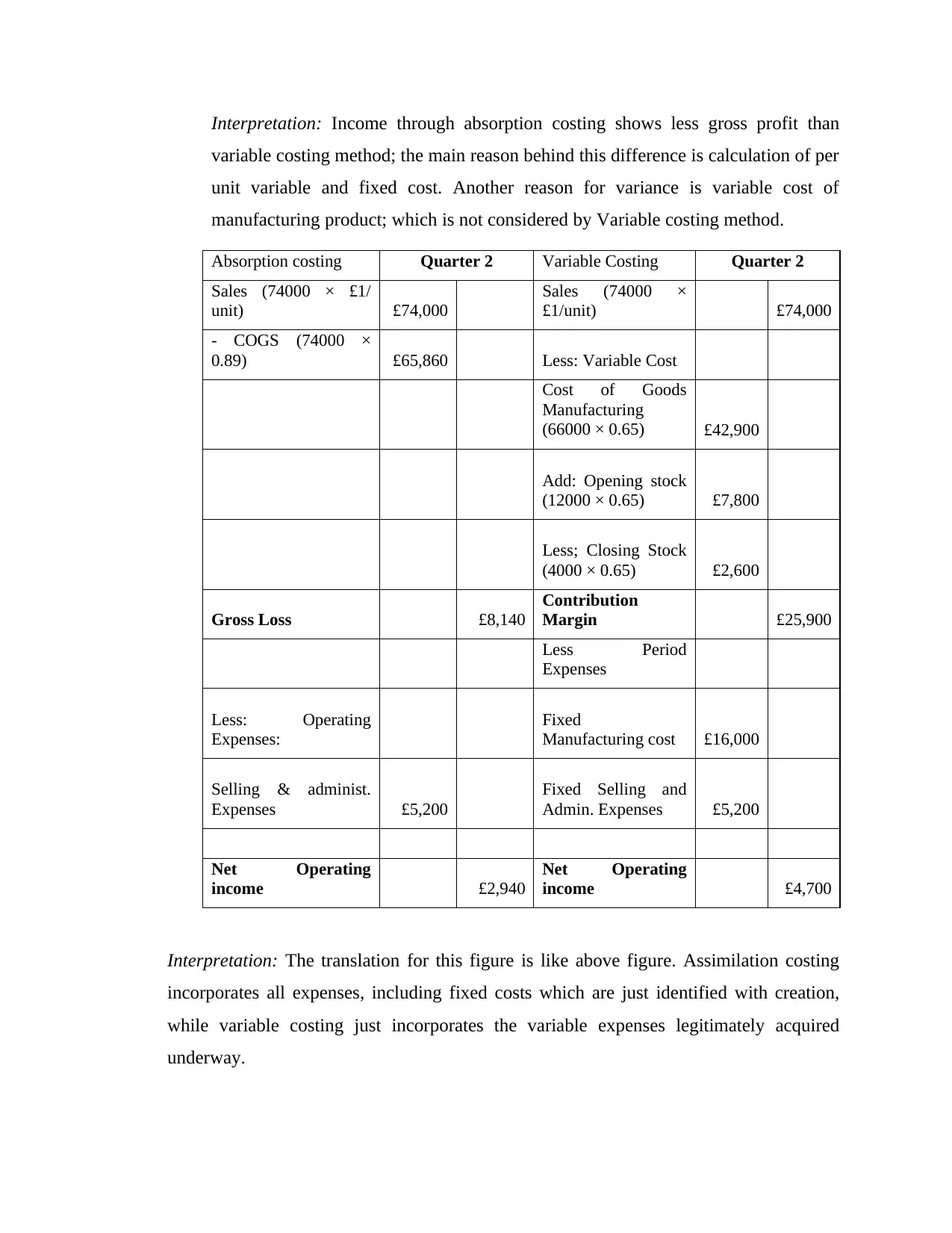

Absorption costing Quarter 2 Variable Costing Quarter 2

Sales (74000 × £1/

unit) £74,000

Sales (74000 ×

£1/unit) £74,000

- COGS (74000 ×

0.89) £65,860 Less: Variable Cost

Cost of Goods

Manufacturing

(66000 × 0.65) £42,900

Add: Opening stock

(12000 × 0.65) £7,800

Less; Closing Stock

(4000 × 0.65) £2,600

Gross Loss £8,140

Contribution

Margin £25,900

Less Period

Expenses

Less: Operating

Expenses:

Fixed

Manufacturing cost £16,000

Selling & administ.

Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Net Operating

income £2,940

Net Operating

income £4,700

Interpretation: The translation for this figure is like above figure. Assimilation costing

incorporates all expenses, including fixed costs which are just identified with creation,

while variable costing just incorporates the variable expenses legitimately acquired

underway.

variable costing method; the main reason behind this difference is calculation of per

unit variable and fixed cost. Another reason for variance is variable cost of

manufacturing product; which is not considered by Variable costing method.

Absorption costing Quarter 2 Variable Costing Quarter 2

Sales (74000 × £1/

unit) £74,000

Sales (74000 ×

£1/unit) £74,000

- COGS (74000 ×

0.89) £65,860 Less: Variable Cost

Cost of Goods

Manufacturing

(66000 × 0.65) £42,900

Add: Opening stock

(12000 × 0.65) £7,800

Less; Closing Stock

(4000 × 0.65) £2,600

Gross Loss £8,140

Contribution

Margin £25,900

Less Period

Expenses

Less: Operating

Expenses:

Fixed

Manufacturing cost £16,000

Selling & administ.

Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Net Operating

income £2,940

Net Operating

income £4,700

Interpretation: The translation for this figure is like above figure. Assimilation costing

incorporates all expenses, including fixed costs which are just identified with creation,

while variable costing just incorporates the variable expenses legitimately acquired

underway.

M2. Accurately apply a range of management accounting techniques and

produce appropriate financial reporting documents

Management accounting techniques are the tools for achieving business success and

objectives. Analyses of techniques will help to identify which tools best suits the Prime

Furniture. Some of these methods are mentioned below:

1. Financial planning: It is the advance planning of sources and applications of funds to

fill the gap between them. Components of financial planning are budgeting, return on

investment, payback period and sales forecasting. Prime furniture can apply this tool

to get budgeted income statement, balance sheet and cash flow statement.

2. Cost accounting: This costing method includes distribution of information’s related to

cost on basis of nature of product, department head and value based. Prime furniture

can apply this method for effective cost management and controlling costs to increase

gross profit.

3. Fund flow analysis: It contains the statement explaining what are the sources of fund

and where they applied by business. It is the best tool which will help Prime Furniture

to keep tracking its fund and resources within business.

4. Standard costing: It is the overall expenses which are concerned by management for

preparing budgets and forecasting sales. The application of this method will help

Prime furniture in price optimization of its product.

5. Decision making accounting: This method will support Prime Furniture in taking

effective decisions based on accurate data provided to managerial accountant.

Decisions made by higher authorities are based on reports produced by accountants.

Hence, result of decisions is based on accuracy of reports present by junior

accountants.

6. Management Information System: This system oriented method has major role in

integrating various systems of company. It gathers information’s from different

departments through setting up interconnectivity between them. This helps

management in maintaining real time information and accuracy of data.

produce appropriate financial reporting documents

Management accounting techniques are the tools for achieving business success and

objectives. Analyses of techniques will help to identify which tools best suits the Prime

Furniture. Some of these methods are mentioned below:

1. Financial planning: It is the advance planning of sources and applications of funds to

fill the gap between them. Components of financial planning are budgeting, return on

investment, payback period and sales forecasting. Prime furniture can apply this tool

to get budgeted income statement, balance sheet and cash flow statement.

2. Cost accounting: This costing method includes distribution of information’s related to

cost on basis of nature of product, department head and value based. Prime furniture

can apply this method for effective cost management and controlling costs to increase

gross profit.

3. Fund flow analysis: It contains the statement explaining what are the sources of fund

and where they applied by business. It is the best tool which will help Prime Furniture

to keep tracking its fund and resources within business.

4. Standard costing: It is the overall expenses which are concerned by management for

preparing budgets and forecasting sales. The application of this method will help

Prime furniture in price optimization of its product.

5. Decision making accounting: This method will support Prime Furniture in taking

effective decisions based on accurate data provided to managerial accountant.

Decisions made by higher authorities are based on reports produced by accountants.

Hence, result of decisions is based on accuracy of reports present by junior

accountants.

6. Management Information System: This system oriented method has major role in

integrating various systems of company. It gathers information’s from different

departments through setting up interconnectivity between them. This helps

management in maintaining real time information and accuracy of data.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7. Management reporting: It is the effective tool which produces timely report to be used

by management to get at certain conclusions and recommend changes important to get

desired results.

LO. 3: Explain the use of planning tools used in management accounting

using budgets for planning and control

P4. Explain the advantages and disadvantages of different types of planning

tools used for budgetary control

Budgeting: It is the process of estimating future costs and revenues of the business based

on current financial documents and trend analysis. It is one of the components of

financial performance indicators which sets milestone for each and every departments to

be achieved in the terms of cost cutting and increasing sales (Management Accounting –

Meaning, Advantages & Functions, 2020).

Importance of Budget:

Sets milestone which has to be achieved by business.

Used as performance indicator tool.

Effective in cost controlling and monitoring.

Alerts business for any shortage of working capital in future.

Making projection for cash flow statement, income statement and balance sheet.

Comparison tool which shows what factors need to be improved to get projected

result.

Types of Budgets:

1. Cash flow budget: Budget which projects future cash inflows and outflows within

company is known as cash flow budget. It estimates all expenses and incomes in

advance to fulfill cash requirement.

2. Operating budget: Projection related to operations of the business is known as

operating budget. Activities like paying salary, office expenses and payment of

by management to get at certain conclusions and recommend changes important to get

desired results.

LO. 3: Explain the use of planning tools used in management accounting

using budgets for planning and control

P4. Explain the advantages and disadvantages of different types of planning

tools used for budgetary control

Budgeting: It is the process of estimating future costs and revenues of the business based

on current financial documents and trend analysis. It is one of the components of

financial performance indicators which sets milestone for each and every departments to

be achieved in the terms of cost cutting and increasing sales (Management Accounting –

Meaning, Advantages & Functions, 2020).

Importance of Budget:

Sets milestone which has to be achieved by business.

Used as performance indicator tool.

Effective in cost controlling and monitoring.

Alerts business for any shortage of working capital in future.

Making projection for cash flow statement, income statement and balance sheet.

Comparison tool which shows what factors need to be improved to get projected

result.

Types of Budgets:

1. Cash flow budget: Budget which projects future cash inflows and outflows within

company is known as cash flow budget. It estimates all expenses and incomes in

advance to fulfill cash requirement.

2. Operating budget: Projection related to operations of the business is known as

operating budget. Activities like paying salary, office expenses and payment of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interest lays under operation and estimation for these factors known as operating

budget.

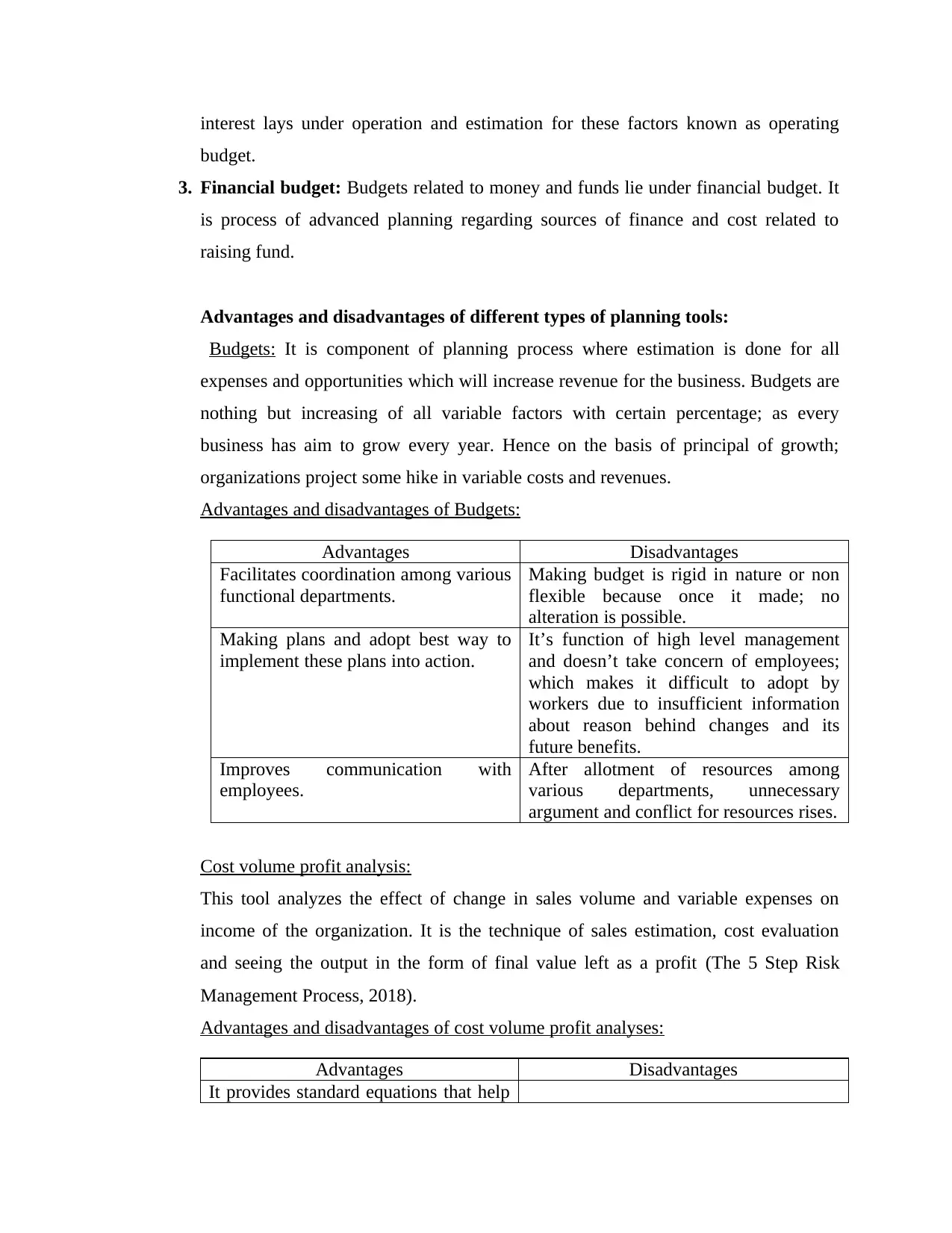

3. Financial budget: Budgets related to money and funds lie under financial budget. It

is process of advanced planning regarding sources of finance and cost related to

raising fund.

Advantages and disadvantages of different types of planning tools:

Budgets: It is component of planning process where estimation is done for all

expenses and opportunities which will increase revenue for the business. Budgets are

nothing but increasing of all variable factors with certain percentage; as every

business has aim to grow every year. Hence on the basis of principal of growth;

organizations project some hike in variable costs and revenues.

Advantages and disadvantages of Budgets:

Advantages Disadvantages

Facilitates coordination among various

functional departments.

Making budget is rigid in nature or non

flexible because once it made; no

alteration is possible.

Making plans and adopt best way to

implement these plans into action.

It’s function of high level management

and doesn’t take concern of employees;

which makes it difficult to adopt by

workers due to insufficient information

about reason behind changes and its

future benefits.

Improves communication with

employees.

After allotment of resources among

various departments, unnecessary

argument and conflict for resources rises.

Cost volume profit analysis:

This tool analyzes the effect of change in sales volume and variable expenses on

income of the organization. It is the technique of sales estimation, cost evaluation

and seeing the output in the form of final value left as a profit (The 5 Step Risk

Management Process, 2018).

Advantages and disadvantages of cost volume profit analyses:

Advantages Disadvantages

It provides standard equations that help

budget.

3. Financial budget: Budgets related to money and funds lie under financial budget. It

is process of advanced planning regarding sources of finance and cost related to

raising fund.

Advantages and disadvantages of different types of planning tools:

Budgets: It is component of planning process where estimation is done for all

expenses and opportunities which will increase revenue for the business. Budgets are

nothing but increasing of all variable factors with certain percentage; as every

business has aim to grow every year. Hence on the basis of principal of growth;

organizations project some hike in variable costs and revenues.

Advantages and disadvantages of Budgets:

Advantages Disadvantages

Facilitates coordination among various

functional departments.

Making budget is rigid in nature or non

flexible because once it made; no

alteration is possible.

Making plans and adopt best way to

implement these plans into action.

It’s function of high level management

and doesn’t take concern of employees;

which makes it difficult to adopt by

workers due to insufficient information

about reason behind changes and its

future benefits.

Improves communication with

employees.

After allotment of resources among

various departments, unnecessary

argument and conflict for resources rises.

Cost volume profit analysis:

This tool analyzes the effect of change in sales volume and variable expenses on

income of the organization. It is the technique of sales estimation, cost evaluation

and seeing the output in the form of final value left as a profit (The 5 Step Risk

Management Process, 2018).

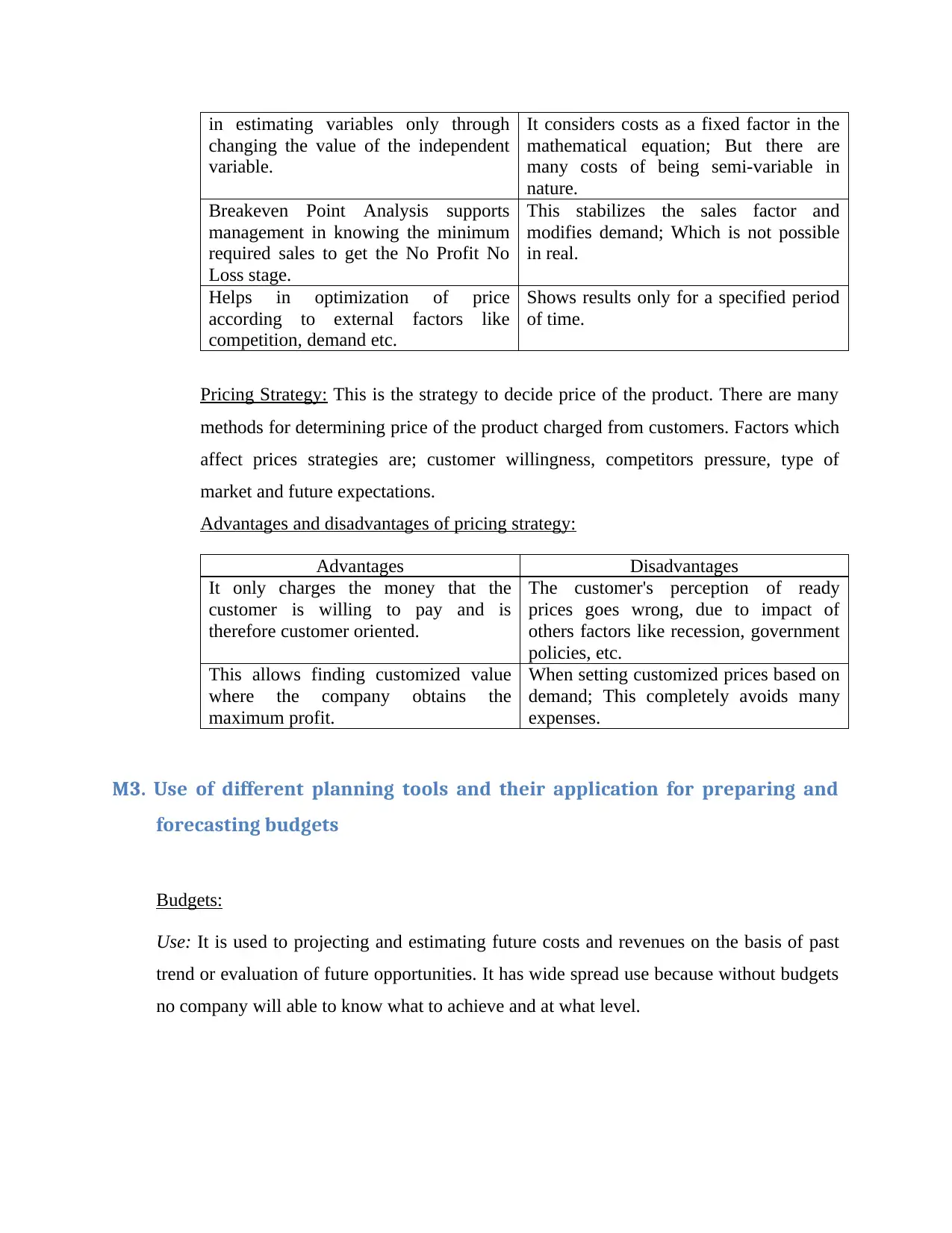

Advantages and disadvantages of cost volume profit analyses:

Advantages Disadvantages

It provides standard equations that help

in estimating variables only through

changing the value of the independent

variable.

It considers costs as a fixed factor in the

mathematical equation; But there are

many costs of being semi-variable in

nature.

Breakeven Point Analysis supports

management in knowing the minimum

required sales to get the No Profit No

Loss stage.

This stabilizes the sales factor and

modifies demand; Which is not possible

in real.

Helps in optimization of price

according to external factors like

competition, demand etc.

Shows results only for a specified period

of time.

Pricing Strategy: This is the strategy to decide price of the product. There are many

methods for determining price of the product charged from customers. Factors which

affect prices strategies are; customer willingness, competitors pressure, type of

market and future expectations.

Advantages and disadvantages of pricing strategy:

Advantages Disadvantages

It only charges the money that the

customer is willing to pay and is

therefore customer oriented.

The customer's perception of ready

prices goes wrong, due to impact of

others factors like recession, government

policies, etc.

This allows finding customized value

where the company obtains the

maximum profit.

When setting customized prices based on

demand; This completely avoids many

expenses.

M3. Use of different planning tools and their application for preparing and

forecasting budgets

Budgets:

Use: It is used to projecting and estimating future costs and revenues on the basis of past

trend or evaluation of future opportunities. It has wide spread use because without budgets

no company will able to know what to achieve and at what level.

changing the value of the independent

variable.

It considers costs as a fixed factor in the

mathematical equation; But there are

many costs of being semi-variable in

nature.

Breakeven Point Analysis supports

management in knowing the minimum

required sales to get the No Profit No

Loss stage.

This stabilizes the sales factor and

modifies demand; Which is not possible

in real.

Helps in optimization of price

according to external factors like

competition, demand etc.

Shows results only for a specified period

of time.

Pricing Strategy: This is the strategy to decide price of the product. There are many

methods for determining price of the product charged from customers. Factors which

affect prices strategies are; customer willingness, competitors pressure, type of

market and future expectations.

Advantages and disadvantages of pricing strategy:

Advantages Disadvantages

It only charges the money that the

customer is willing to pay and is

therefore customer oriented.

The customer's perception of ready

prices goes wrong, due to impact of

others factors like recession, government

policies, etc.

This allows finding customized value

where the company obtains the

maximum profit.

When setting customized prices based on

demand; This completely avoids many

expenses.

M3. Use of different planning tools and their application for preparing and

forecasting budgets

Budgets:

Use: It is used to projecting and estimating future costs and revenues on the basis of past

trend or evaluation of future opportunities. It has wide spread use because without budgets

no company will able to know what to achieve and at what level.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.