Management Accounting Report: Systems, Costs, and Planning

VerifiedAdded on 2023/01/23

|18

|5031

|55

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its role in identifying, measuring, analyzing, and communicating financial data to aid managerial decision-making within ABC Limited, a medium-sized manufacturing sector. The report explores various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, highlighting their importance in cost analysis, inventory control, and pricing strategies. It also details different methods used for management accounting reporting, such as cost reports, budgets, and performance reports, along with their integration within organizational processes. Furthermore, the report delves into cost calculation techniques like marginal and absorption costing, demonstrating their application through examples and profit and loss statements. Finally, it examines planning tools for budgetary control, comparing and contrasting how organizations adapt management accounting systems to address financial challenges, providing insights into strategic financial management.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1 Elaborate management accounting and requirement of various kind of management

accounting systems. ....................................................................................................................4

P2 Methods used for management accounting reporting............................................................6

TASK 2............................................................................................................................................8

P3 Calculate costs by using tools and techniques.......................................................................8

TASK 3..........................................................................................................................................11

P4 Explain advantages and disadvantages of various tools of planning for the purpose of

budgetary control......................................................................................................................11

TASK 4..........................................................................................................................................14

P5 Compare and contrast organisation adapting management accounting systems to respond

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1 Elaborate management accounting and requirement of various kind of management

accounting systems. ....................................................................................................................4

P2 Methods used for management accounting reporting............................................................6

TASK 2............................................................................................................................................8

P3 Calculate costs by using tools and techniques.......................................................................8

TASK 3..........................................................................................................................................11

P4 Explain advantages and disadvantages of various tools of planning for the purpose of

budgetary control......................................................................................................................11

TASK 4..........................................................................................................................................14

P5 Compare and contrast organisation adapting management accounting systems to respond

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting or managerial accounting or cost accounting, is the chain of

activities for identifying, measuring, analysing, interpreting and communicating data and

information to managers to achieve organisational goals and objectives in proper way.

Management accounting information helps to managers in an organisation to take decisions by

analysing each and every factor. This report is based on ABC limited which is an medium-sized

manufacturing sector. This report is based on management accounting and their various systems

that support to reach at desirable outcomes. It further elaborates various methods of management

accounting reporting and techniques for cost analysis by income statement. It also includes

advantages and disadvantages of kinds of planning tools that used in budgetary control by

comparing with other organisation by adapting management accounting systems to eliminate

financial problems.

Management accounting or managerial accounting or cost accounting, is the chain of

activities for identifying, measuring, analysing, interpreting and communicating data and

information to managers to achieve organisational goals and objectives in proper way.

Management accounting information helps to managers in an organisation to take decisions by

analysing each and every factor. This report is based on ABC limited which is an medium-sized

manufacturing sector. This report is based on management accounting and their various systems

that support to reach at desirable outcomes. It further elaborates various methods of management

accounting reporting and techniques for cost analysis by income statement. It also includes

advantages and disadvantages of kinds of planning tools that used in budgetary control by

comparing with other organisation by adapting management accounting systems to eliminate

financial problems.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

P1 Elaborate management accounting and requirement of various kind of management

accounting systems.

Management accounting is an significant internal function of organisation and

organisation use it to record and report internal financial information (A. Hammad, Jusoh and

Ghozali, 2013..). The role and responsibility of management accountant is to coordinate various

events around the whole business by considering the needs and wants of business in proper way.

The major result of management accounting is to prepare periodic reports for the role of

companies department managers and CEO. In management accounting reports includes details of

cash in an organisation,sales revenue of an organisation with current payables and receivables of

an organisation that are important factors to evaluate financial position of an organisation

(AlMaryani and Sadik, 2012.). Various kind of information found in management accounting

that are differ from financial accounting in various contexts as financial accounting based on

historical data and information and management reports that are future oriented. Management

accounting reports are usually confidential in nature and proved useful for internal usage of an

organisation. Management accounting based and relied on accounting practices that are based on

management informational needs and wants.

An effective management accounting system reach up to all kinds of departments of a business

in which finance, information technology, Human resource and operations with sales.

Various kinds of management accounting systems:

Management accounting systems vary and majorly depends on their usage that depends

on organisation and their functions. Each and every systems is designed to provide information

that based on the needs of management that assist in decision making. There are various kinds of

management accounting systems that are as follows:

Cost accounting system:

Cost accounting system that also known as product costing system which is an kind of

framework that helps in estimating cost of products for the motive of analysis of their

profitability, valuation of inventory with controlling cost (Belfo and Trigo, 2013.). In cost

accounting system majorly two kind of cost consist in it that are job order costing and process

costing. Estimating the accurate cost of products and services is very much critical to obtain

profitable operations. A product is profitable or not can be ascertained after analysing the cost of

P1 Elaborate management accounting and requirement of various kind of management

accounting systems.

Management accounting is an significant internal function of organisation and

organisation use it to record and report internal financial information (A. Hammad, Jusoh and

Ghozali, 2013..). The role and responsibility of management accountant is to coordinate various

events around the whole business by considering the needs and wants of business in proper way.

The major result of management accounting is to prepare periodic reports for the role of

companies department managers and CEO. In management accounting reports includes details of

cash in an organisation,sales revenue of an organisation with current payables and receivables of

an organisation that are important factors to evaluate financial position of an organisation

(AlMaryani and Sadik, 2012.). Various kind of information found in management accounting

that are differ from financial accounting in various contexts as financial accounting based on

historical data and information and management reports that are future oriented. Management

accounting reports are usually confidential in nature and proved useful for internal usage of an

organisation. Management accounting based and relied on accounting practices that are based on

management informational needs and wants.

An effective management accounting system reach up to all kinds of departments of a business

in which finance, information technology, Human resource and operations with sales.

Various kinds of management accounting systems:

Management accounting systems vary and majorly depends on their usage that depends

on organisation and their functions. Each and every systems is designed to provide information

that based on the needs of management that assist in decision making. There are various kinds of

management accounting systems that are as follows:

Cost accounting system:

Cost accounting system that also known as product costing system which is an kind of

framework that helps in estimating cost of products for the motive of analysis of their

profitability, valuation of inventory with controlling cost (Belfo and Trigo, 2013.). In cost

accounting system majorly two kind of cost consist in it that are job order costing and process

costing. Estimating the accurate cost of products and services is very much critical to obtain

profitable operations. A product is profitable or not can be ascertained after analysing the cost of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the product that is very much important role of it. In context of ABC Limited that introduce its

air dryers after analysing the cost and other attributes in right manner.

Inventory management system:

Inventory represents stocked goods or material and terms stock and inventory often used

interchangeably. An inventory management system amalgamate various systems and processes

in which desktop software, barcode printers, barcode scanners and various devices in which

mobile to streamline inventory of an organisation (Boučková, 2015.). The main function of

inventory control is to track majorly two main functions in which stock room by receiving and

shipping. The importance of inventory control that it helps in gathering current inventory level

to control both under stock and overstock situations. Effective tracking helps in get right

information about stocking locations that helps in taking effective decisions. In context of ABC

Limited that build their product after analysing needs and wants of consumers and demand in

proper way so that measurement of stock can be easily done.

Job costing system:

Job costing system used for assigning and accumulating cost of manufacturing for an

individual unit of output. It used when kinds of products should be produced that are sufficiently

differ from each other. It proved useful to submit the information of cost to a consumer under a

contract in which cost should be reimbursed. In job costing system majorly three kinds of

information consisted that are direct materials, direct labour and overhead costs. The another

function of job costing system is to tailored the requirements of consumers because some

consumers allow to charged certain costs on their jobs. In context of ABC limited they used it to

accumulate important knowledge and information to gather insights from various businesses in

proper way.

Price optimization system:

It is an mathematical program that helps in calculate factor that vary at various price

levels and after that combine data and information related to costs and level of inventory to select

best price that helps in enhance level of profit (Boyns and Edwards, 2013.). It used in three

pricing critical elements that are pricing strategy, value of products and services in perspective of

both buyer and sellers. Works and tactics that impacts on profitability level of an organisation. In

that context all management accounting systems are very much important to evaluate each and

every important attribute to evaluate cost, inventory level and many more factors that proved

air dryers after analysing the cost and other attributes in right manner.

Inventory management system:

Inventory represents stocked goods or material and terms stock and inventory often used

interchangeably. An inventory management system amalgamate various systems and processes

in which desktop software, barcode printers, barcode scanners and various devices in which

mobile to streamline inventory of an organisation (Boučková, 2015.). The main function of

inventory control is to track majorly two main functions in which stock room by receiving and

shipping. The importance of inventory control that it helps in gathering current inventory level

to control both under stock and overstock situations. Effective tracking helps in get right

information about stocking locations that helps in taking effective decisions. In context of ABC

Limited that build their product after analysing needs and wants of consumers and demand in

proper way so that measurement of stock can be easily done.

Job costing system:

Job costing system used for assigning and accumulating cost of manufacturing for an

individual unit of output. It used when kinds of products should be produced that are sufficiently

differ from each other. It proved useful to submit the information of cost to a consumer under a

contract in which cost should be reimbursed. In job costing system majorly three kinds of

information consisted that are direct materials, direct labour and overhead costs. The another

function of job costing system is to tailored the requirements of consumers because some

consumers allow to charged certain costs on their jobs. In context of ABC limited they used it to

accumulate important knowledge and information to gather insights from various businesses in

proper way.

Price optimization system:

It is an mathematical program that helps in calculate factor that vary at various price

levels and after that combine data and information related to costs and level of inventory to select

best price that helps in enhance level of profit (Boyns and Edwards, 2013.). It used in three

pricing critical elements that are pricing strategy, value of products and services in perspective of

both buyer and sellers. Works and tactics that impacts on profitability level of an organisation. In

that context all management accounting systems are very much important to evaluate each and

every important attribute to evaluate cost, inventory level and many more factors that proved

beneficial for ABC Limited. It proved useful in long term and short term planning to take

important decisions also it proved beneficial to manage information at every level of

organisational hierarchy.

P2 Methods used for management accounting reporting.

Management accounting that also known as managerial accounting that concentrates on

data and information from financial accounting. It proved useful in particularly to take important

decisions, planning and controlling various activities. Management accountants rely on financial

statements that contains earning statements, cash flows and balance sheets that helps in analyse

the information of an organisation regarding budgets, performance and reports and cost of a

product and services. There are various kinds of methods use for management accounting

reporting that are as follows:

Cost reports:

Managerial accounting helps in determining the prices of various products and services.

That can be possible by taking or adopting fresh prices, overhead cost, labour and any other kind

of prices that come into consideration (Chiwamit, Modell and Yang, 2014.). In that aspect total

cost should be divided as totals of items created. In that report data and information that consist

in it should be brief and that final report helps managers to evaluate prices of goods and their

selling cost. It also helps to managers to plan and manage limits related to income. In context of

ABC Limited they builds various reports that evaluate prices, cost and factors that influence

these prices in effective manner.

Budget:

One of the principal factor of management accounting that plans and coordinate spending

plans and policies. Budgets should be made by accumulating and utilizing various kinds financial

plans and relate with it future projections in proper way (DRURY, 2013.). In an organisation's

spending list consist of various sources of expenses and income. In context of ABC Limited that

tries to accomplish their goals and objectives in remaining budgeted amounts. Managers and

other higher authority find or search new sellers to avail as providers from raw resources to get

cash out of it. Organisation search various kinds of approaches with motive of diminishes cost.

Execution reports:

Management accounting is one of the most important tool or technique that helps in

evaluate spending plans by contrasting genuine uses and income by planned sums. Budget is one

important decisions also it proved beneficial to manage information at every level of

organisational hierarchy.

P2 Methods used for management accounting reporting.

Management accounting that also known as managerial accounting that concentrates on

data and information from financial accounting. It proved useful in particularly to take important

decisions, planning and controlling various activities. Management accountants rely on financial

statements that contains earning statements, cash flows and balance sheets that helps in analyse

the information of an organisation regarding budgets, performance and reports and cost of a

product and services. There are various kinds of methods use for management accounting

reporting that are as follows:

Cost reports:

Managerial accounting helps in determining the prices of various products and services.

That can be possible by taking or adopting fresh prices, overhead cost, labour and any other kind

of prices that come into consideration (Chiwamit, Modell and Yang, 2014.). In that aspect total

cost should be divided as totals of items created. In that report data and information that consist

in it should be brief and that final report helps managers to evaluate prices of goods and their

selling cost. It also helps to managers to plan and manage limits related to income. In context of

ABC Limited they builds various reports that evaluate prices, cost and factors that influence

these prices in effective manner.

Budget:

One of the principal factor of management accounting that plans and coordinate spending

plans and policies. Budgets should be made by accumulating and utilizing various kinds financial

plans and relate with it future projections in proper way (DRURY, 2013.). In an organisation's

spending list consist of various sources of expenses and income. In context of ABC Limited that

tries to accomplish their goals and objectives in remaining budgeted amounts. Managers and

other higher authority find or search new sellers to avail as providers from raw resources to get

cash out of it. Organisation search various kinds of approaches with motive of diminishes cost.

Execution reports:

Management accounting is one of the most important tool or technique that helps in

evaluate spending plans by contrasting genuine uses and income by planned sums. Budget is one

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of most important factor that helps to bring changes by analyse the entire data and information

that amount listed on the performance of the report in better way ( Farouk, Cherian and Jacob,

2012.). In ABC Limited each and every year the performance reports are calculated in better

way some organisations calculate it on monthly or quarterly basis that helps to directors to get

for future demand in production and cost additions in better way. Various kinds of reports are

utilized and get arranges by managerial accountant and other information such as orders placed

to receive orders are very much important. If the lots of orders of any particular order were

placed in that case particular report helps to summarises. A business opportunity reports are

build that helps managers to get settle their choices in respect of present and future business

choices.

Benefits of management accounting:

There are various benefits of management accounting that are very much important that

are as follows:

It helps to coordinate and manage all activities in proper way and setting up various budgets,

their requirements and expected performance that an organisation anticipated.

It helps in operate various cost centres and departments with efficiency and economy.

Management accounting helps in eliminate wastage that helps in enhance profitability in better

way.

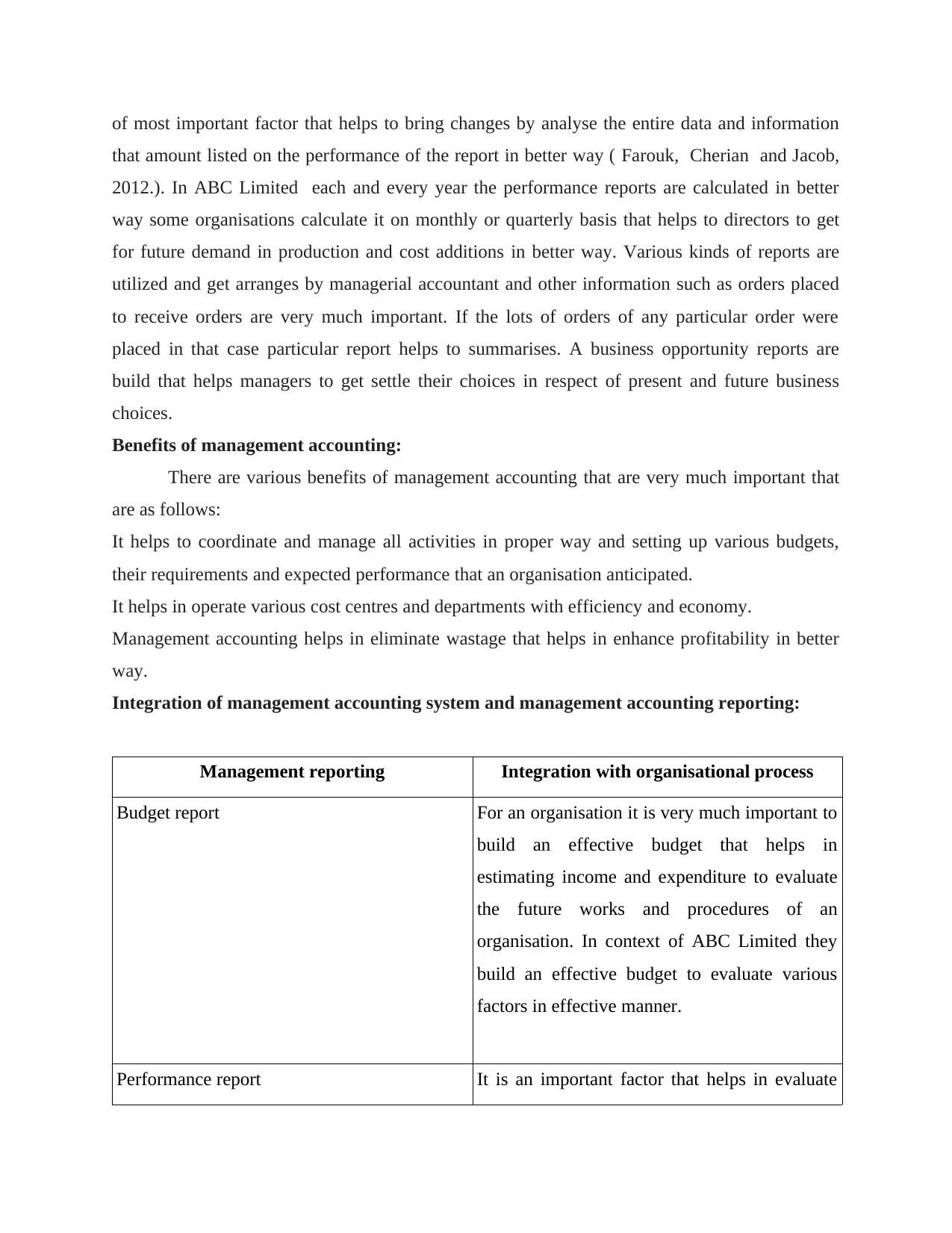

Integration of management accounting system and management accounting reporting:

Management reporting Integration with organisational process

Budget report For an organisation it is very much important to

build an effective budget that helps in

estimating income and expenditure to evaluate

the future works and procedures of an

organisation. In context of ABC Limited they

build an effective budget to evaluate various

factors in effective manner.

Performance report It is an important factor that helps in evaluate

that amount listed on the performance of the report in better way ( Farouk, Cherian and Jacob,

2012.). In ABC Limited each and every year the performance reports are calculated in better

way some organisations calculate it on monthly or quarterly basis that helps to directors to get

for future demand in production and cost additions in better way. Various kinds of reports are

utilized and get arranges by managerial accountant and other information such as orders placed

to receive orders are very much important. If the lots of orders of any particular order were

placed in that case particular report helps to summarises. A business opportunity reports are

build that helps managers to get settle their choices in respect of present and future business

choices.

Benefits of management accounting:

There are various benefits of management accounting that are very much important that

are as follows:

It helps to coordinate and manage all activities in proper way and setting up various budgets,

their requirements and expected performance that an organisation anticipated.

It helps in operate various cost centres and departments with efficiency and economy.

Management accounting helps in eliminate wastage that helps in enhance profitability in better

way.

Integration of management accounting system and management accounting reporting:

Management reporting Integration with organisational process

Budget report For an organisation it is very much important to

build an effective budget that helps in

estimating income and expenditure to evaluate

the future works and procedures of an

organisation. In context of ABC Limited they

build an effective budget to evaluate various

factors in effective manner.

Performance report It is an important factor that helps in evaluate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance of an individual by finding out

major strengths and weaknesses of an

individual that helps to evaluate their

contribution in organisational growth and

enhancement (Gond and et.al ., 2012.).

Inventory and manufacturing report In that aspect inventory is very much important

to evaluate the production as per the needs and

wants of consumers so that organisation can

build products accordingly. So there are close

relationship in both these factors.

TASK 2

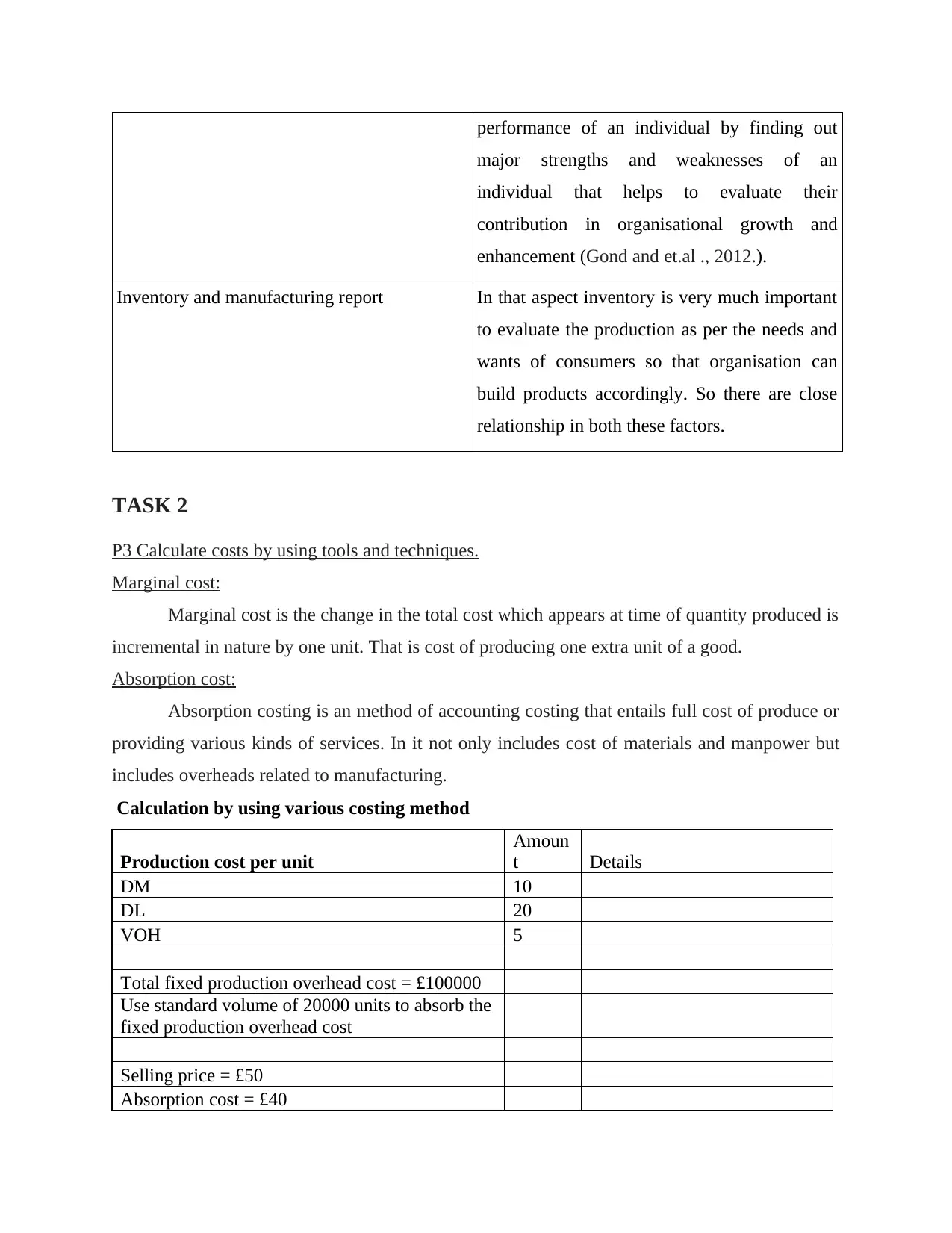

P3 Calculate costs by using tools and techniques.

Marginal cost:

Marginal cost is the change in the total cost which appears at time of quantity produced is

incremental in nature by one unit. That is cost of producing one extra unit of a good.

Absorption cost:

Absorption costing is an method of accounting costing that entails full cost of produce or

providing various kinds of services. In it not only includes cost of materials and manpower but

includes overheads related to manufacturing.

Calculation by using various costing method

Production cost per unit

Amoun

t Details

DM 10

DL 20

VOH 5

Total fixed production overhead cost = £100000

Use standard volume of 20000 units to absorb the

fixed production overhead cost

Selling price = £50

Absorption cost = £40

major strengths and weaknesses of an

individual that helps to evaluate their

contribution in organisational growth and

enhancement (Gond and et.al ., 2012.).

Inventory and manufacturing report In that aspect inventory is very much important

to evaluate the production as per the needs and

wants of consumers so that organisation can

build products accordingly. So there are close

relationship in both these factors.

TASK 2

P3 Calculate costs by using tools and techniques.

Marginal cost:

Marginal cost is the change in the total cost which appears at time of quantity produced is

incremental in nature by one unit. That is cost of producing one extra unit of a good.

Absorption cost:

Absorption costing is an method of accounting costing that entails full cost of produce or

providing various kinds of services. In it not only includes cost of materials and manpower but

includes overheads related to manufacturing.

Calculation by using various costing method

Production cost per unit

Amoun

t Details

DM 10

DL 20

VOH 5

Total fixed production overhead cost = £100000

Use standard volume of 20000 units to absorb the

fixed production overhead cost

Selling price = £50

Absorption cost = £40

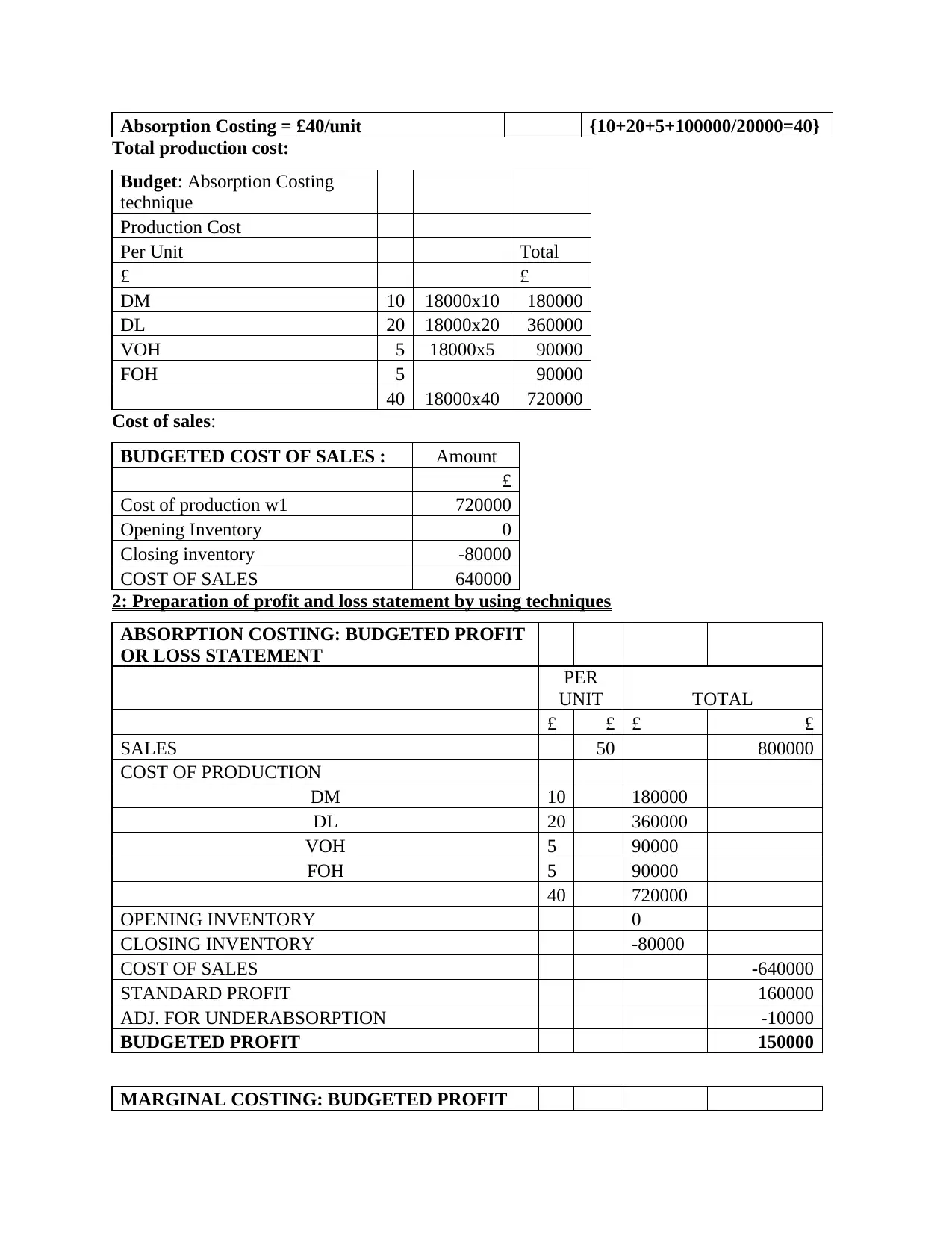

Absorption Costing = £40/unit {10+20+5+100000/20000=40}

Total production cost:

Budget: Absorption Costing

technique

Production Cost

Per Unit Total

£ £

DM 10 18000x10 180000

DL 20 18000x20 360000

VOH 5 18000x5 90000

FOH 5 90000

40 18000x40 720000

Cost of sales:

BUDGETED COST OF SALES : Amount

£

Cost of production w1 720000

Opening Inventory 0

Closing inventory -80000

COST OF SALES 640000

2: Preparation of profit and loss statement by using techniques

ABSORPTION COSTING: BUDGETED PROFIT

OR LOSS STATEMENT

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

40 720000

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

MARGINAL COSTING: BUDGETED PROFIT

Total production cost:

Budget: Absorption Costing

technique

Production Cost

Per Unit Total

£ £

DM 10 18000x10 180000

DL 20 18000x20 360000

VOH 5 18000x5 90000

FOH 5 90000

40 18000x40 720000

Cost of sales:

BUDGETED COST OF SALES : Amount

£

Cost of production w1 720000

Opening Inventory 0

Closing inventory -80000

COST OF SALES 640000

2: Preparation of profit and loss statement by using techniques

ABSORPTION COSTING: BUDGETED PROFIT

OR LOSS STATEMENT

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

40 720000

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

MARGINAL COSTING: BUDGETED PROFIT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

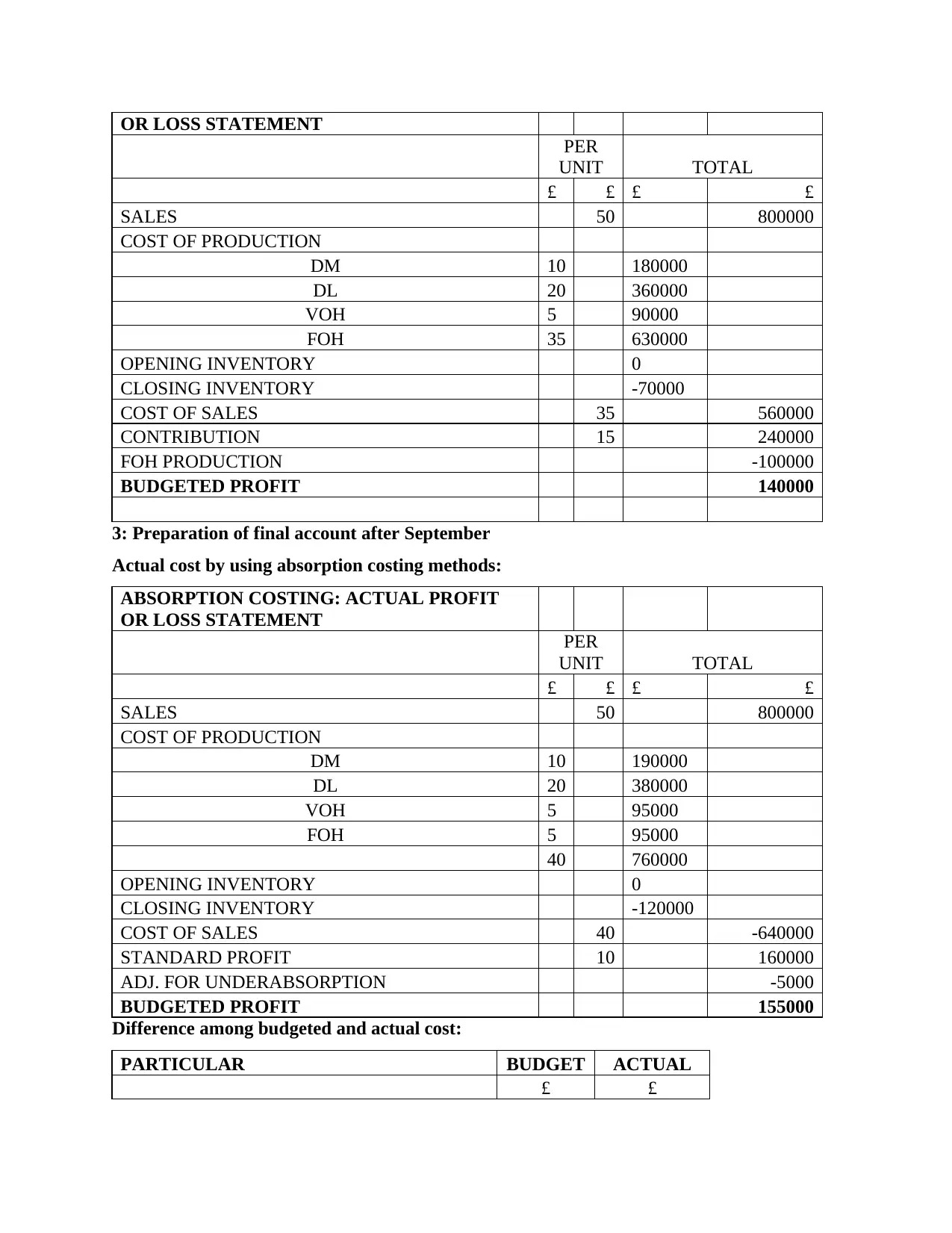

OR LOSS STATEMENT

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

OPENING INVENTORY 0

CLOSING INVENTORY -70000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

3: Preparation of final account after September

Actual cost by using absorption costing methods:

ABSORPTION COSTING: ACTUAL PROFIT

OR LOSS STATEMENT

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 5 95000

40 760000

OPENING INVENTORY 0

CLOSING INVENTORY -120000

COST OF SALES 40 -640000

STANDARD PROFIT 10 160000

ADJ. FOR UNDERABSORPTION -5000

BUDGETED PROFIT 155000

Difference among budgeted and actual cost:

PARTICULAR BUDGET ACTUAL

£ £

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

OPENING INVENTORY 0

CLOSING INVENTORY -70000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

3: Preparation of final account after September

Actual cost by using absorption costing methods:

ABSORPTION COSTING: ACTUAL PROFIT

OR LOSS STATEMENT

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 5 95000

40 760000

OPENING INVENTORY 0

CLOSING INVENTORY -120000

COST OF SALES 40 -640000

STANDARD PROFIT 10 160000

ADJ. FOR UNDERABSORPTION -5000

BUDGETED PROFIT 155000

Difference among budgeted and actual cost:

PARTICULAR BUDGET ACTUAL

£ £

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FOH CHARGED TO PRODUCTION COST 90000 95000

under FOH charged to Profit or Loss account 10000 5000

FOH CHARGED IN THE MONTH 100000 100000

FOH TRANSFERRED THROUGH CLOSING

INVENTORY TO NEXT MONTH OCT 2018 10000 15000

FOH CHARGED 90000 85000

From the above data and information it has been summarised that financial planning, balance

sheet and other various measures proved beneficial for organisation to reach at desirable goals

and objectives in proper way.

TASK 3

P4 Explain advantages and disadvantages of various tools of planning for the purpose of

budgetary control.

There are various kinds of planning tools that helps to organisation to control various

activities that proved beneficial to lead in market that are as follows:

Flexible Budget:

Flexible Budget may be defined a financial plan which is based on revenues and expenses

of current amount and output. With the help of revenues and expenses in the current production

taking as a base, future revenues and expenses can be estimated (Huang, Teoh and Zhang,

2013.).

Advantages:

Easy Differentiation: Flexible budget helps in differentiating between actual

performance with standard performance.

Flexible: Flexible budget can easily be modified according to the dynamic environment

in the market.

Disadvantages:

Confusing: Flexible Budgets are quite confusing as it require more planning to adjust

expenses of different periods and this may lead the user in confusion to understand the

data.

Zero-based Budget:

under FOH charged to Profit or Loss account 10000 5000

FOH CHARGED IN THE MONTH 100000 100000

FOH TRANSFERRED THROUGH CLOSING

INVENTORY TO NEXT MONTH OCT 2018 10000 15000

FOH CHARGED 90000 85000

From the above data and information it has been summarised that financial planning, balance

sheet and other various measures proved beneficial for organisation to reach at desirable goals

and objectives in proper way.

TASK 3

P4 Explain advantages and disadvantages of various tools of planning for the purpose of

budgetary control.

There are various kinds of planning tools that helps to organisation to control various

activities that proved beneficial to lead in market that are as follows:

Flexible Budget:

Flexible Budget may be defined a financial plan which is based on revenues and expenses

of current amount and output. With the help of revenues and expenses in the current production

taking as a base, future revenues and expenses can be estimated (Huang, Teoh and Zhang,

2013.).

Advantages:

Easy Differentiation: Flexible budget helps in differentiating between actual

performance with standard performance.

Flexible: Flexible budget can easily be modified according to the dynamic environment

in the market.

Disadvantages:

Confusing: Flexible Budgets are quite confusing as it require more planning to adjust

expenses of different periods and this may lead the user in confusion to understand the

data.

Zero-based Budget:

Zero-based budgeting is refer as management accounting which helps in preparing

budget from starting. Cash flow statement should be evaluated again and all the expenses must

be justified that is incurred in the department (Lavia López and Hiebl, 2014.).

Zero-based budget record the expenses of new period which are calculated on the basis of

actual expenses.

Advantages:

Efficiency: Zero-based budgeting helps in efficient allocation of department-wise

resources and it focus more on actual numbers rather than historical numbers.

Co-ordination and communication: Zero-based budgeting helps in co-ordinating and

communicating within the department and involves employees in decision making to

share their views and ideas which helps them to keep them motivated.

Disadvantages of Zero-based budgeting:

Lack of expertise: Zero-based budgeting lack in expertise as it becomes difficult to

explain every line and cost and for this training of managers is required.

High-manpower requirement: As zero-based budget need to be started from the base, it

requires large number of employees due to which department lack in time and human

resources.

Activity-based Budgeting:

Activity-based Budgeting may be defined as budget which is prepared after considering

the overhead cost (Lee, 2012.). In other words, it is a management accounting tool which is not

concerned with the past year budget but analyse and research the cost incurred and based on that

allocate resources to an activity in ABC Limited.

Advantages:

Evaluation: Activity based budgeting helps in evaluation of cost driver and takes into

consideration involved in the activity. It eliminates the irrelevant activities and focus only

on necessary activities.

Elimination of gridlock: Activity based budget are prepared after analysis and reseach

which helps in eliminating unnecessary activities through which business function are

carried smoothly.

Disadvantages:

budget from starting. Cash flow statement should be evaluated again and all the expenses must

be justified that is incurred in the department (Lavia López and Hiebl, 2014.).

Zero-based budget record the expenses of new period which are calculated on the basis of

actual expenses.

Advantages:

Efficiency: Zero-based budgeting helps in efficient allocation of department-wise

resources and it focus more on actual numbers rather than historical numbers.

Co-ordination and communication: Zero-based budgeting helps in co-ordinating and

communicating within the department and involves employees in decision making to

share their views and ideas which helps them to keep them motivated.

Disadvantages of Zero-based budgeting:

Lack of expertise: Zero-based budgeting lack in expertise as it becomes difficult to

explain every line and cost and for this training of managers is required.

High-manpower requirement: As zero-based budget need to be started from the base, it

requires large number of employees due to which department lack in time and human

resources.

Activity-based Budgeting:

Activity-based Budgeting may be defined as budget which is prepared after considering

the overhead cost (Lee, 2012.). In other words, it is a management accounting tool which is not

concerned with the past year budget but analyse and research the cost incurred and based on that

allocate resources to an activity in ABC Limited.

Advantages:

Evaluation: Activity based budgeting helps in evaluation of cost driver and takes into

consideration involved in the activity. It eliminates the irrelevant activities and focus only

on necessary activities.

Elimination of gridlock: Activity based budget are prepared after analysis and reseach

which helps in eliminating unnecessary activities through which business function are

carried smoothly.

Disadvantages:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.