Management Accounting Application and Financial Solutions

VerifiedAdded on 2023/01/19

|19

|5485

|85

Report

AI Summary

This report provides a comprehensive overview of management accounting practices, focusing on their application within Excite Entertainment Ltd. It begins by defining management accounting and its essential need, detailing various management accounting systems such as cost accounting, job accounting, and inventory management. The report then explores different methods used in management accounting reporting, including inventory management reports, budget reports, performance reports, job cost reports, and accounts receivable aging reports. A significant portion of the analysis is dedicated to cost analysis methods, including cost volume profit analysis, flexible budgeting, cost variance, and absorption and marginal costing, with a practical application of these methods demonstrated through the preparation of an income statement. Furthermore, the report discusses the benefits and disadvantages of various planning tools in budgetary control and concludes by comparing how different organizations adapt management accounting systems to solve financial problems. The document is available on Desklib, offering students access to valuable study resources and solved assignments.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Meaning of management accounting with essential need of types of management

accounting systems. ...............................................................................................................1

P2 Various methods utilised in management accounting reporting......................................3

TASK 2............................................................................................................................................5

P3 Figuring costs with the usage of appropriate methods of cost analysis and preparing an

income statement by using marginal and absorption costs....................................................5

TASK3...........................................................................................................................................10

P4 The benefits and disadvantages of various kinds of planning tools in budgetary control. 10

TASK 4..........................................................................................................................................13

P5 Adaption of management accounting systems by different organisations in solving

financial problems................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Meaning of management accounting with essential need of types of management

accounting systems. ...............................................................................................................1

P2 Various methods utilised in management accounting reporting......................................3

TASK 2............................................................................................................................................5

P3 Figuring costs with the usage of appropriate methods of cost analysis and preparing an

income statement by using marginal and absorption costs....................................................5

TASK3...........................................................................................................................................10

P4 The benefits and disadvantages of various kinds of planning tools in budgetary control. 10

TASK 4..........................................................................................................................................13

P5 Adaption of management accounting systems by different organisations in solving

financial problems................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is the process of using the financial information of the company

to prepare management accounts and reports to make budget related decisions (Ali and Zhang,

2015). It prepares monthly and weekly reports for the management of the businesses. It is one of

the important element useful for running the organisation. It helps in assisting management to

achieve better control and efficient planning in the organization. It is applicable in every kind of

organization like not-for-profit administration, government organisation or sole proprietorship.

Management accounting is considered as a significant decision-making procedure utilised by the

internal management. This report is based on the company Excite Entertainment Ltd.

It is engaged in leisure and entertainment industry in the UK. This study alludes the

meaning of accounting system, explanation of need management accounting system in

enterprises, management accounting report methods. It also describes the usage of techniques of

cost analysis for preparation of income statement, merits and demerits of various types of

planning processes for controlling the budget. In the final part of the report the comparison

between different organisation's way of utilising this accounting system to solve financial

problems is discussed.

TASK 1

P1 Meaning of management accounting with essential need of types of management accounting

systems.

Management accounting- It make the necessary use of the data of the firm and make

valuation of the inflows and outflows (Arnaboldi, Lapsley and Steccolini, 2015). This

information can be used by the management to take important decisions about the product

manufactured, whether to make any changes in it or not. the applied strategies are improving the

sales; the estimated profit is earned or not. Management can conduct the planning for the future

and evaluate the overall performance of the concern. Management accounting helps in

identifying the risks associated in various fields. Hence, through this the company can take better

investment decisions.

Management accounting system- It involves the internal systems which the enterprise

utilises to figure out the processes for the organisational management. There are various types of

accounting system which different organisation uses in its operations. Excite Entertainment Ltd.

1

Management accounting is the process of using the financial information of the company

to prepare management accounts and reports to make budget related decisions (Ali and Zhang,

2015). It prepares monthly and weekly reports for the management of the businesses. It is one of

the important element useful for running the organisation. It helps in assisting management to

achieve better control and efficient planning in the organization. It is applicable in every kind of

organization like not-for-profit administration, government organisation or sole proprietorship.

Management accounting is considered as a significant decision-making procedure utilised by the

internal management. This report is based on the company Excite Entertainment Ltd.

It is engaged in leisure and entertainment industry in the UK. This study alludes the

meaning of accounting system, explanation of need management accounting system in

enterprises, management accounting report methods. It also describes the usage of techniques of

cost analysis for preparation of income statement, merits and demerits of various types of

planning processes for controlling the budget. In the final part of the report the comparison

between different organisation's way of utilising this accounting system to solve financial

problems is discussed.

TASK 1

P1 Meaning of management accounting with essential need of types of management accounting

systems.

Management accounting- It make the necessary use of the data of the firm and make

valuation of the inflows and outflows (Arnaboldi, Lapsley and Steccolini, 2015). This

information can be used by the management to take important decisions about the product

manufactured, whether to make any changes in it or not. the applied strategies are improving the

sales; the estimated profit is earned or not. Management can conduct the planning for the future

and evaluate the overall performance of the concern. Management accounting helps in

identifying the risks associated in various fields. Hence, through this the company can take better

investment decisions.

Management accounting system- It involves the internal systems which the enterprise

utilises to figure out the processes for the organisational management. There are various types of

accounting system which different organisation uses in its operations. Excite Entertainment Ltd.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

make use of this system in valuing assets, revenues and expenses. It helps in selecting finite

alternatives for the formulation of better decisions.

Types of Management accounting system:-

Cost accounting system- Manufacturers use this system to keep record of the production

exercise by using a everlasting inventory system. It helps in tracking the flow of stock during the

different stages of manufacturing (Ashraf and Uddin, 2015). This cost accounting system can be

applicable in all types of businesses like manufacturing, trading products and delivering services.

It needs five basic things for valuation. They are input measurement base, an inventory method

of valuation, cost assemblage methodology and recording of inventory cost cycle at particular

period.

Cost accounting system depends on variety of costs which are flowing in and through

with the inventory accounts. It selects any from among the pure historical costing, standard

costing and orderly historical costing. It is not possible for any business to perform without the

usage of cost accounting and it will cause in making of incorrect decision and thereby result in

suffering losses. Its objective is to minimize the business operation cost by controlling and

distinguishing them whenever required. Hence, the profits will be increased. Excite

Entertainment Ltd. exercises cost accounting system in verifying the products manufactured by

it are profitable or it requires some modification. It manages the costs and keeps balance between

the cash inflow and outflow.

Job accounting system- This system assigns the costs to specific job in which the

company is engaged. It is used majorly by the industries like construction where the costs are

allocated according to the various projects held by the business. Job accounting system is the

process of collecting subject matter about the various costs related with a particular production of

commodity and service job (Bedford, 2015). This data may be essential for submitting the

information of cost to the client for the fulfilment of contract where costs can be returned back. It

can be also useful for finding out the quality of enterprise’s estimating system to quote different

prices for earning a reasonable profit. The costs of inventory manufactured can also be

determined by this system. Excite Entertainment Ltd. management team operates this system to

investigate whether production cost surpasses the overheads, the ultimate price of products and

the quantity. The company also use this system in evaluating profits attained on particular

employee jobs.

2

alternatives for the formulation of better decisions.

Types of Management accounting system:-

Cost accounting system- Manufacturers use this system to keep record of the production

exercise by using a everlasting inventory system. It helps in tracking the flow of stock during the

different stages of manufacturing (Ashraf and Uddin, 2015). This cost accounting system can be

applicable in all types of businesses like manufacturing, trading products and delivering services.

It needs five basic things for valuation. They are input measurement base, an inventory method

of valuation, cost assemblage methodology and recording of inventory cost cycle at particular

period.

Cost accounting system depends on variety of costs which are flowing in and through

with the inventory accounts. It selects any from among the pure historical costing, standard

costing and orderly historical costing. It is not possible for any business to perform without the

usage of cost accounting and it will cause in making of incorrect decision and thereby result in

suffering losses. Its objective is to minimize the business operation cost by controlling and

distinguishing them whenever required. Hence, the profits will be increased. Excite

Entertainment Ltd. exercises cost accounting system in verifying the products manufactured by

it are profitable or it requires some modification. It manages the costs and keeps balance between

the cash inflow and outflow.

Job accounting system- This system assigns the costs to specific job in which the

company is engaged. It is used majorly by the industries like construction where the costs are

allocated according to the various projects held by the business. Job accounting system is the

process of collecting subject matter about the various costs related with a particular production of

commodity and service job (Bedford, 2015). This data may be essential for submitting the

information of cost to the client for the fulfilment of contract where costs can be returned back. It

can be also useful for finding out the quality of enterprise’s estimating system to quote different

prices for earning a reasonable profit. The costs of inventory manufactured can also be

determined by this system. Excite Entertainment Ltd. management team operates this system to

investigate whether production cost surpasses the overheads, the ultimate price of products and

the quantity. The company also use this system in evaluating profits attained on particular

employee jobs.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system- The requirement of this system can be felt at various

locations of the unit to carry out smooth performance of the daily stock production. An inventory

management system involves the processes which provides assistance in tracking products across

the supply chain of business. It makes the entire supply chain cycle effective from order

placement work with seller to delivery of order to the customer and processing the entire process

of product of the company (Brewer, Garrison and Noreen, 2015). This system is further divided

into periodic Inventory System, Radio Frequency Identification Inventory Systems and perpetual

system. Excite Entertainment Ltd. applies this type of system in improving the productivity and

efficiency in conducting entertainment events. It uses inventory management tools like radio

frequency identification and various software of inventory to manage stock.

Advantages of Management accounting systems: -

Basis Benefits

Cost accounting system With the use of this system, Excite Entertainment Ltd.

performs the task of evaluation of costs, calculations

of costs of various factors of manufacturing,

controlling costs, examining wastages and fixation of

goal-price.

Job costing system This system will benefit the Excite Entertainment Ltd.

in the estimation of different types of costs entangled

in the manufacturing processes. The quality of the

performed work can be also evaluated using this

system.

Inventory management system Excite Entertainment Ltd. can modify the inaccuracy

found in the orders of inventory through this system.

It is advantageous for the company in preventing

stock outs.

P2 Various methods utilised in management accounting reporting

Inventory management report- This reports keeps the track of the inventory by the

scheduled time and the location. It determines the overall turnover during the period, demand

3

locations of the unit to carry out smooth performance of the daily stock production. An inventory

management system involves the processes which provides assistance in tracking products across

the supply chain of business. It makes the entire supply chain cycle effective from order

placement work with seller to delivery of order to the customer and processing the entire process

of product of the company (Brewer, Garrison and Noreen, 2015). This system is further divided

into periodic Inventory System, Radio Frequency Identification Inventory Systems and perpetual

system. Excite Entertainment Ltd. applies this type of system in improving the productivity and

efficiency in conducting entertainment events. It uses inventory management tools like radio

frequency identification and various software of inventory to manage stock.

Advantages of Management accounting systems: -

Basis Benefits

Cost accounting system With the use of this system, Excite Entertainment Ltd.

performs the task of evaluation of costs, calculations

of costs of various factors of manufacturing,

controlling costs, examining wastages and fixation of

goal-price.

Job costing system This system will benefit the Excite Entertainment Ltd.

in the estimation of different types of costs entangled

in the manufacturing processes. The quality of the

performed work can be also evaluated using this

system.

Inventory management system Excite Entertainment Ltd. can modify the inaccuracy

found in the orders of inventory through this system.

It is advantageous for the company in preventing

stock outs.

P2 Various methods utilised in management accounting reporting

Inventory management report- This reports keeps the track of the inventory by the

scheduled time and the location. It determines the overall turnover during the period, demand

3

and quantity delivered and the profitability produced by the stock. It helps in finding the

strengths and weaknesses involved in inventory management (Christ, Burritt and Varsei, 2016).

It is very vital in the businesses of manufacturing. This report keeps the information of the units

produced with quality and units wasted during holding of the inventory. Excite Entertainment

Ltd. put to use these reports in producing efficient manufacturing processes. Its keeps the record

of inventory scrap, per unit costs of overhead and timely labour costs in this report.

Budget Report- This kind of report is called as internal report. It is utilised by the

manager to make comparison between the estimated budget and the actual cost of the

performance during the specific period (Christopher, 2016). It is used to determine the factors

which are responsible for not working according to the budget. As the report is made on

estimation basis it is not accurate and hence, the large difference can be seen in the actual costs

incurred in performances.

The management of Excite Entertainment Ltd. utilises this report in managing future

costs and rendering incentives to skilled employees.

Performance report- This report assists in addressing the result of any particular project

or work. It makes comparison between the estimated performance and the actual performance

given on a work. It helps in planning, making decisions, regulating and controlling the

performances. Excite Entertainment Ltd. uses performance reports to interpret the accuracy of

the formulated strategy for attaining the company's objective. The company provides bonuses on

outstanding performances of the workforce through this reports.

Job Cost Report – It records the information about increase in total cost by a specific

product as compared with the estimated profit earned on that project. It assists in measuring the

profitableness of particular kinds of jobs and which jobs should be given importance to improve

profits (Cooper, 2017). The manager in Excite Entertainment Ltd. make analysis of progress of

projects with estimated time and costs through this report. If any weaknesses are found during

examination then they are corrected at that time only by the managers. It also helps the company

in finding out the gain in investment in particular jobs.

Accounts receivable ageing report- This report make the list of the non-paying

customer invoices and the credit memos which are not used. It is gainful in the businesses which

are involved in the activity of providing credit to its customers. Almost reports consists of

separated columns including invoices for late days as in 30, 60, 90 days. The accountant in

4

strengths and weaknesses involved in inventory management (Christ, Burritt and Varsei, 2016).

It is very vital in the businesses of manufacturing. This report keeps the information of the units

produced with quality and units wasted during holding of the inventory. Excite Entertainment

Ltd. put to use these reports in producing efficient manufacturing processes. Its keeps the record

of inventory scrap, per unit costs of overhead and timely labour costs in this report.

Budget Report- This kind of report is called as internal report. It is utilised by the

manager to make comparison between the estimated budget and the actual cost of the

performance during the specific period (Christopher, 2016). It is used to determine the factors

which are responsible for not working according to the budget. As the report is made on

estimation basis it is not accurate and hence, the large difference can be seen in the actual costs

incurred in performances.

The management of Excite Entertainment Ltd. utilises this report in managing future

costs and rendering incentives to skilled employees.

Performance report- This report assists in addressing the result of any particular project

or work. It makes comparison between the estimated performance and the actual performance

given on a work. It helps in planning, making decisions, regulating and controlling the

performances. Excite Entertainment Ltd. uses performance reports to interpret the accuracy of

the formulated strategy for attaining the company's objective. The company provides bonuses on

outstanding performances of the workforce through this reports.

Job Cost Report – It records the information about increase in total cost by a specific

product as compared with the estimated profit earned on that project. It assists in measuring the

profitableness of particular kinds of jobs and which jobs should be given importance to improve

profits (Cooper, 2017). The manager in Excite Entertainment Ltd. make analysis of progress of

projects with estimated time and costs through this report. If any weaknesses are found during

examination then they are corrected at that time only by the managers. It also helps the company

in finding out the gain in investment in particular jobs.

Accounts receivable ageing report- This report make the list of the non-paying

customer invoices and the credit memos which are not used. It is gainful in the businesses which

are involved in the activity of providing credit to its customers. Almost reports consists of

separated columns including invoices for late days as in 30, 60, 90 days. The accountant in

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Excite Entertainment Ltd. utilises this report in searching flaws in the present collection process

and managing the flow of cash. Credit policies are made in the company with the assistance of

this report.

TASK 2

P3 Figuring costs with the usage of appropriate methods of cost analysis and preparing an

income statement by using marginal and absorption costs

Cost: It is overall costs of the resources exhausted in the operation of manufacturing a

product or on a particular product (Falkner and Hiebl, 2015). Fixed cost and variable costs are

the two basic basic kinds of costs incurred in organisations. Some of the examples of cost

incurred in Excite Entertainment Ltd. are payment of rent, purchase of materials, advertisement

costs, etc.

Cost volume profit analysis: It helps in understanding the activity of the profits in the

company as a result of change in volume of production and costs. For conducting cost volume

profit analysis it is essential to differentiate the costs of the organisation into fixed and variable

costs. Excite Entertainment Ltd. put to use this analysis in planning profit, controlling costs,

performance evaluation and making decisions.

Flexible budgeting: It assists the establishment in predicting the performance and level

of incomes at a different activity and sales levels (Gibassier, 2017). Flexible budget evaluates the

performance of the management in the firm. Excite Entertainment Ltd. can exert this budget in

controlling irregular payouts and use funds at needed time.

Cost variance: It is the cost of completed work after comparing with planned cost. It is

determined by the difference of earned value (EV) with actual cost (AC) incurred. Over

budgeting can be evaluated with the negative cost variance. It ensures that the task is delivered as

per budget. The manufacturing company Excite Entertainment Ltd. uses cost variance in

improving the budgeting activity.

Absorption & marginal costing:

Absorption costing: In this method while calculating profits any difference is not done

between variable and fixed cost. This type of costing presumes that fixed costs are related to

products hence, all the production costs either variable or fixed costs should become portion of

product cost. The overheads regarded by this costing statement are production, selling &

5

and managing the flow of cash. Credit policies are made in the company with the assistance of

this report.

TASK 2

P3 Figuring costs with the usage of appropriate methods of cost analysis and preparing an

income statement by using marginal and absorption costs

Cost: It is overall costs of the resources exhausted in the operation of manufacturing a

product or on a particular product (Falkner and Hiebl, 2015). Fixed cost and variable costs are

the two basic basic kinds of costs incurred in organisations. Some of the examples of cost

incurred in Excite Entertainment Ltd. are payment of rent, purchase of materials, advertisement

costs, etc.

Cost volume profit analysis: It helps in understanding the activity of the profits in the

company as a result of change in volume of production and costs. For conducting cost volume

profit analysis it is essential to differentiate the costs of the organisation into fixed and variable

costs. Excite Entertainment Ltd. put to use this analysis in planning profit, controlling costs,

performance evaluation and making decisions.

Flexible budgeting: It assists the establishment in predicting the performance and level

of incomes at a different activity and sales levels (Gibassier, 2017). Flexible budget evaluates the

performance of the management in the firm. Excite Entertainment Ltd. can exert this budget in

controlling irregular payouts and use funds at needed time.

Cost variance: It is the cost of completed work after comparing with planned cost. It is

determined by the difference of earned value (EV) with actual cost (AC) incurred. Over

budgeting can be evaluated with the negative cost variance. It ensures that the task is delivered as

per budget. The manufacturing company Excite Entertainment Ltd. uses cost variance in

improving the budgeting activity.

Absorption & marginal costing:

Absorption costing: In this method while calculating profits any difference is not done

between variable and fixed cost. This type of costing presumes that fixed costs are related to

products hence, all the production costs either variable or fixed costs should become portion of

product cost. The overheads regarded by this costing statement are production, selling &

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

administration and distribution overheads. It finds out the outlay of every unit. Excite

Entertainment Ltd. can use this statement in tracking accurate profits in various activities of the

production.

Marginal costing: This statement considers difference in both the costs fixed and

variable costs during calculations. There is no place of gross profit in the marginal costing

income statement. It makes consideration of fixed costs and variable costs overhead only. It uses

profit volume ratio to determine profits and calculates the cost of succeeding unit. To find out the

quantity of optimum production Excite Entertainment Ltd. can use this costing statement.

Cost allocation:

Fixed cost: This is the cost that is obtained for a particular period and remains unaffected

with the fluctuations in the different level of activity, turnover or production with definite

production and limits of turnover (Harrison and Lock, 2017). For instance in Excite

Entertainment Ltd. fixed costs are salaries of employees, rent, insurance charges, rates, etc.

Variable cost: This cost is the portion of the overall cost which changes with change in

production. Variable cost per unit of production changes with the increment in output and

decreases with the decrement in the overall output. Examples of variable costs in Excite

Entertainment Ltd. manufacturing can be seen as direct labour costs, direct expenses and direct

material.

Normal costing: This is the cost allocation methodology that apportions the costs to

commodity on the basis of material cost, labour cost and other overheads needed to produce that

product. Excite Entertainment Ltd. make use of this costing in deciding the cost of the

commodity. It makes the real costs for the components of the commodity.

Standard costing: It refers to estimated expenditure that generally occurs in the

production process of a product or carrying out of a particular service. The management in

Excite Entertainment Ltd. uses this costing to improve efficiencies and plan for the future

processes of the production.

Activity based costing: It is the methodology that is utilised for attributing costs to units

of products and services as per the profit received from that activity (Hirsch, Seubert and Sohn,

2015). The drivers of costs determines the behaviour of cost pattern in the production. In Excite

Entertainment Ltd. it is exercised to make correction in the inaccurate cost subject matter and to

distribute the overheads on the basis of activity.

6

Entertainment Ltd. can use this statement in tracking accurate profits in various activities of the

production.

Marginal costing: This statement considers difference in both the costs fixed and

variable costs during calculations. There is no place of gross profit in the marginal costing

income statement. It makes consideration of fixed costs and variable costs overhead only. It uses

profit volume ratio to determine profits and calculates the cost of succeeding unit. To find out the

quantity of optimum production Excite Entertainment Ltd. can use this costing statement.

Cost allocation:

Fixed cost: This is the cost that is obtained for a particular period and remains unaffected

with the fluctuations in the different level of activity, turnover or production with definite

production and limits of turnover (Harrison and Lock, 2017). For instance in Excite

Entertainment Ltd. fixed costs are salaries of employees, rent, insurance charges, rates, etc.

Variable cost: This cost is the portion of the overall cost which changes with change in

production. Variable cost per unit of production changes with the increment in output and

decreases with the decrement in the overall output. Examples of variable costs in Excite

Entertainment Ltd. manufacturing can be seen as direct labour costs, direct expenses and direct

material.

Normal costing: This is the cost allocation methodology that apportions the costs to

commodity on the basis of material cost, labour cost and other overheads needed to produce that

product. Excite Entertainment Ltd. make use of this costing in deciding the cost of the

commodity. It makes the real costs for the components of the commodity.

Standard costing: It refers to estimated expenditure that generally occurs in the

production process of a product or carrying out of a particular service. The management in

Excite Entertainment Ltd. uses this costing to improve efficiencies and plan for the future

processes of the production.

Activity based costing: It is the methodology that is utilised for attributing costs to units

of products and services as per the profit received from that activity (Hirsch, Seubert and Sohn,

2015). The drivers of costs determines the behaviour of cost pattern in the production. In Excite

Entertainment Ltd. it is exercised to make correction in the inaccurate cost subject matter and to

distribute the overheads on the basis of activity.

6

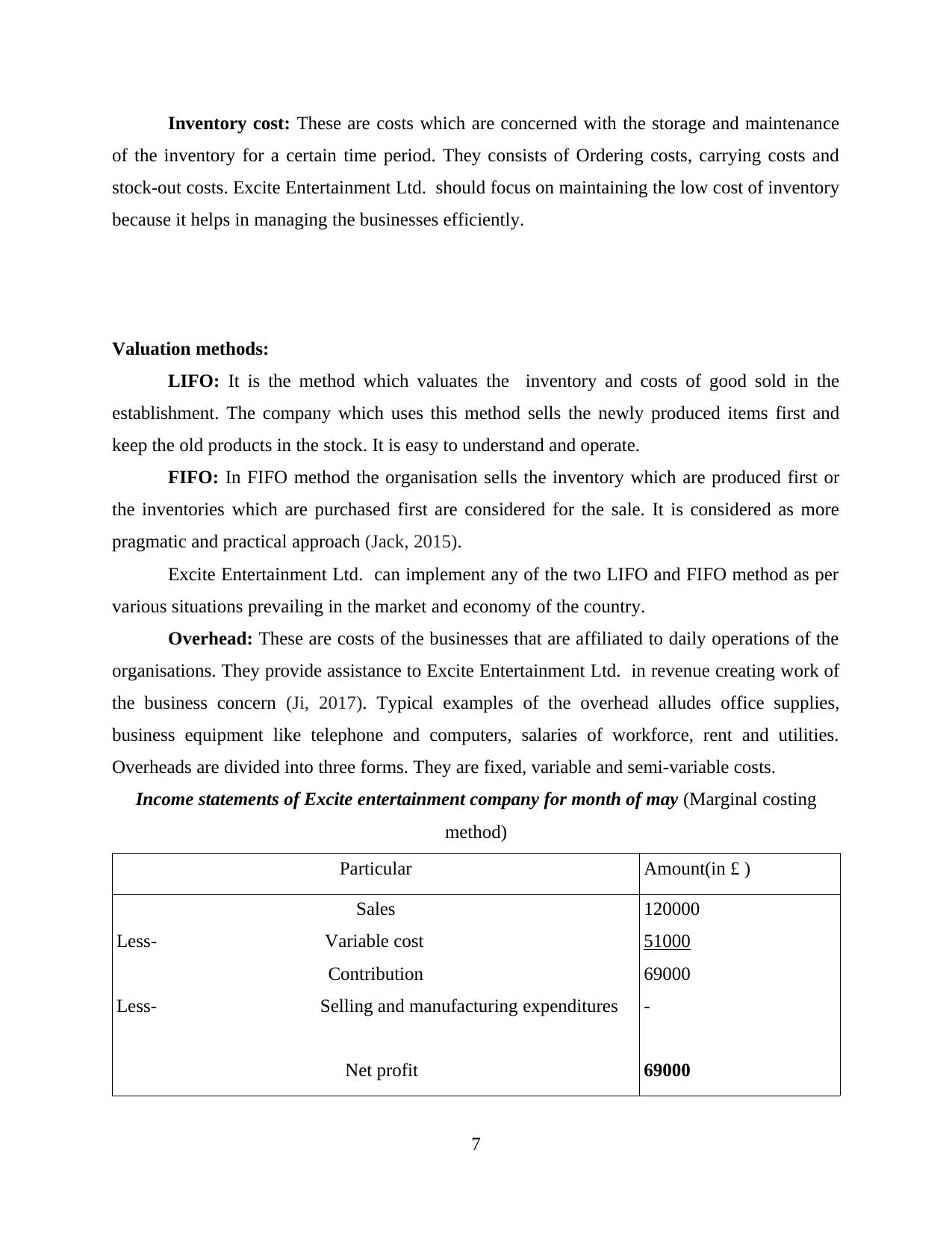

Inventory cost: These are costs which are concerned with the storage and maintenance

of the inventory for a certain time period. They consists of Ordering costs, carrying costs and

stock-out costs. Excite Entertainment Ltd. should focus on maintaining the low cost of inventory

because it helps in managing the businesses efficiently.

Valuation methods:

LIFO: It is the method which valuates the inventory and costs of good sold in the

establishment. The company which uses this method sells the newly produced items first and

keep the old products in the stock. It is easy to understand and operate.

FIFO: In FIFO method the organisation sells the inventory which are produced first or

the inventories which are purchased first are considered for the sale. It is considered as more

pragmatic and practical approach (Jack, 2015).

Excite Entertainment Ltd. can implement any of the two LIFO and FIFO method as per

various situations prevailing in the market and economy of the country.

Overhead: These are costs of the businesses that are affiliated to daily operations of the

organisations. They provide assistance to Excite Entertainment Ltd. in revenue creating work of

the business concern (Ji, 2017). Typical examples of the overhead alludes office supplies,

business equipment like telephone and computers, salaries of workforce, rent and utilities.

Overheads are divided into three forms. They are fixed, variable and semi-variable costs.

Income statements of Excite entertainment company for month of may (Marginal costing

method)

Particular Amount(in £ )

Sales

Less- Variable cost

Contribution

Less- Selling and manufacturing expenditures

Net profit

120000

51000

69000

-

69000

7

of the inventory for a certain time period. They consists of Ordering costs, carrying costs and

stock-out costs. Excite Entertainment Ltd. should focus on maintaining the low cost of inventory

because it helps in managing the businesses efficiently.

Valuation methods:

LIFO: It is the method which valuates the inventory and costs of good sold in the

establishment. The company which uses this method sells the newly produced items first and

keep the old products in the stock. It is easy to understand and operate.

FIFO: In FIFO method the organisation sells the inventory which are produced first or

the inventories which are purchased first are considered for the sale. It is considered as more

pragmatic and practical approach (Jack, 2015).

Excite Entertainment Ltd. can implement any of the two LIFO and FIFO method as per

various situations prevailing in the market and economy of the country.

Overhead: These are costs of the businesses that are affiliated to daily operations of the

organisations. They provide assistance to Excite Entertainment Ltd. in revenue creating work of

the business concern (Ji, 2017). Typical examples of the overhead alludes office supplies,

business equipment like telephone and computers, salaries of workforce, rent and utilities.

Overheads are divided into three forms. They are fixed, variable and semi-variable costs.

Income statements of Excite entertainment company for month of may (Marginal costing

method)

Particular Amount(in £ )

Sales

Less- Variable cost

Contribution

Less- Selling and manufacturing expenditures

Net profit

120000

51000

69000

-

69000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

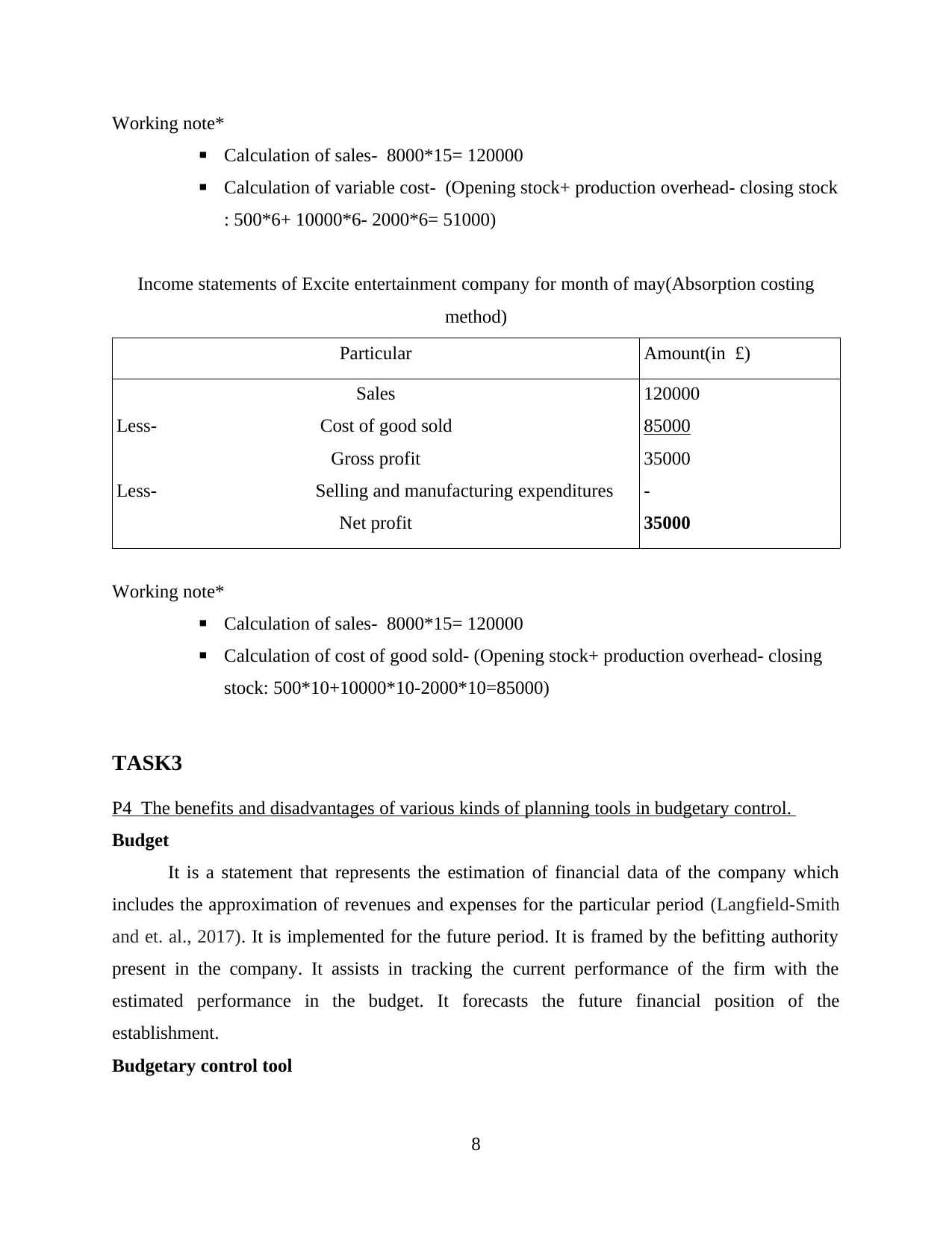

Working note*

▪ Calculation of sales- 8000*15= 120000

▪ Calculation of variable cost- (Opening stock+ production overhead- closing stock

: 500*6+ 10000*6- 2000*6= 51000)

Income statements of Excite entertainment company for month of may(Absorption costing

method)

Particular Amount(in £)

Sales

Less- Cost of good sold

Gross profit

Less- Selling and manufacturing expenditures

Net profit

120000

85000

35000

-

35000

Working note*

▪ Calculation of sales- 8000*15= 120000

▪ Calculation of cost of good sold- (Opening stock+ production overhead- closing

stock: 500*10+10000*10-2000*10=85000)

TASK3

P4 The benefits and disadvantages of various kinds of planning tools in budgetary control.

Budget

It is a statement that represents the estimation of financial data of the company which

includes the approximation of revenues and expenses for the particular period (Langfield-Smith

and et. al., 2017). It is implemented for the future period. It is framed by the befitting authority

present in the company. It assists in tracking the current performance of the firm with the

estimated performance in the budget. It forecasts the future financial position of the

establishment.

Budgetary control tool

8

▪ Calculation of sales- 8000*15= 120000

▪ Calculation of variable cost- (Opening stock+ production overhead- closing stock

: 500*6+ 10000*6- 2000*6= 51000)

Income statements of Excite entertainment company for month of may(Absorption costing

method)

Particular Amount(in £)

Sales

Less- Cost of good sold

Gross profit

Less- Selling and manufacturing expenditures

Net profit

120000

85000

35000

-

35000

Working note*

▪ Calculation of sales- 8000*15= 120000

▪ Calculation of cost of good sold- (Opening stock+ production overhead- closing

stock: 500*10+10000*10-2000*10=85000)

TASK3

P4 The benefits and disadvantages of various kinds of planning tools in budgetary control.

Budget

It is a statement that represents the estimation of financial data of the company which

includes the approximation of revenues and expenses for the particular period (Langfield-Smith

and et. al., 2017). It is implemented for the future period. It is framed by the befitting authority

present in the company. It assists in tracking the current performance of the firm with the

estimated performance in the budget. It forecasts the future financial position of the

establishment.

Budgetary control tool

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is a technique in which the differences in the actual outcomes and estimated results

from the budget are recovered. It helps in taking necessary actions at the required time. This tool

assists the manager in the company in making proper plans and co-ordinating the activities. It

controls costs by preparing budgets, assigning responsibilities and organising departments to

attain maximum gains in businesses.

Forms of Planning tools utilised for budget control:-

Sales budget- This budget provides a complete sales strategy for a particular time period.

Sales budget sets the sales estimation with product, quantity, quality, beliefs and time

(Schneider, 2015). It is important budget from among other budges as provides base for the

preparation of rest budgets in the organisation. In Excite Entertainment Ltd. sales manager

constructs sales budget by taking help of sales supervisor, market researchers, sales officer and

other employees related to sales. Trends in the price of the product, customer's trends, purchasing

power of consumer, content of advertising, previous year sales, current competition in the

market, economic conditions in the location of marketplace are regarded for formulating the

sales budget.

Merits-

It provide assistance to the organisation in aligning the employees with the activities of

sales.

Several costs like equipment cost, travel costs, marketing costs for functioning of the

sales objective can be determined by the Sales budget. It frames clear-cut goals for the sales function in the establishment.

Demerits-

It consumes much of the time of management in preparing budget after considering

modifications, additions, etc.

It cannot forecast the trends in the future events that arises due to unpredictable calamity

and market situations. Sales budget is not always accurate and it may provide unfavourable results.

Cash Budget- It furnishes the firm estimated statement of receipts and expenses for the

period fixed in budget and discloses the current situation of cash valued from it. This budget

displays the requirements of cash at various period of the budget and thereby helps the manager

in arranging to satisfy the demands of business concern (Schuster, 2015). Hence, it gives

9

from the budget are recovered. It helps in taking necessary actions at the required time. This tool

assists the manager in the company in making proper plans and co-ordinating the activities. It

controls costs by preparing budgets, assigning responsibilities and organising departments to

attain maximum gains in businesses.

Forms of Planning tools utilised for budget control:-

Sales budget- This budget provides a complete sales strategy for a particular time period.

Sales budget sets the sales estimation with product, quantity, quality, beliefs and time

(Schneider, 2015). It is important budget from among other budges as provides base for the

preparation of rest budgets in the organisation. In Excite Entertainment Ltd. sales manager

constructs sales budget by taking help of sales supervisor, market researchers, sales officer and

other employees related to sales. Trends in the price of the product, customer's trends, purchasing

power of consumer, content of advertising, previous year sales, current competition in the

market, economic conditions in the location of marketplace are regarded for formulating the

sales budget.

Merits-

It provide assistance to the organisation in aligning the employees with the activities of

sales.

Several costs like equipment cost, travel costs, marketing costs for functioning of the

sales objective can be determined by the Sales budget. It frames clear-cut goals for the sales function in the establishment.

Demerits-

It consumes much of the time of management in preparing budget after considering

modifications, additions, etc.

It cannot forecast the trends in the future events that arises due to unpredictable calamity

and market situations. Sales budget is not always accurate and it may provide unfavourable results.

Cash Budget- It furnishes the firm estimated statement of receipts and expenses for the

period fixed in budget and discloses the current situation of cash valued from it. This budget

displays the requirements of cash at various period of the budget and thereby helps the manager

in arranging to satisfy the demands of business concern (Schuster, 2015). Hence, it gives

9

assurance that a firm will never face shortage of finances. It also encourage the management to

control and coordinate the activities involved with payments as well as receipts. Excite

Entertainment Ltd. uses this budget to keep a control on the usage of funds in less productive

activities and maintaining the required liquidity or cash balance. Maintenance of excess cash in

the firm is essential so as to manage the situations of selling on credit and meeting short term

liabilities. Cash budget helped the company in boosting the sales and increasing profitability.

Merits-

Cash budget helps in acquiring financial assistance from lenders and financial institution

by providing projected cash flow report to them. It aids the management in devising efficient and effectual ways for handling the resources

of the company.

Demerits-

Cash budget do not provide significance to the non-financial factors which may be

responsible for the non-performance of plan.

It may be manipulated by the top authority according to their interests.

Production Budget-This budget is also referred as output budget. This budget is largely

based on the sales budget and reveals the estimated units quantities which are to be produced

throughout the time of budget (Solovida and Latan, 2017). This budget assists in keeping

optimum balance among production and sales stock position in the manufacturing unit. The task

of preparing this budget is given to production manager in the company. The production team in

Excite Entertainment Ltd. exercises this budget to identify the appropriate factors responsible

for lowering the sales of the businesses. The company make the necessary strategy to meet the

requirements of the stock to serve the customers and therefore plan the chronological sequence

of various operations to produce estimated production. It helped the company in controlling the

supply of raw materials, stock of finished goods and unfinished work.

Merits-

It enables optimum utilisation of labour hours in the production and maximum use of the

plant and machinery. It keeps a check on the expenses of the production as there is consistent production in the

unit.

Demerits-

10

control and coordinate the activities involved with payments as well as receipts. Excite

Entertainment Ltd. uses this budget to keep a control on the usage of funds in less productive

activities and maintaining the required liquidity or cash balance. Maintenance of excess cash in

the firm is essential so as to manage the situations of selling on credit and meeting short term

liabilities. Cash budget helped the company in boosting the sales and increasing profitability.

Merits-

Cash budget helps in acquiring financial assistance from lenders and financial institution

by providing projected cash flow report to them. It aids the management in devising efficient and effectual ways for handling the resources

of the company.

Demerits-

Cash budget do not provide significance to the non-financial factors which may be

responsible for the non-performance of plan.

It may be manipulated by the top authority according to their interests.

Production Budget-This budget is also referred as output budget. This budget is largely

based on the sales budget and reveals the estimated units quantities which are to be produced

throughout the time of budget (Solovida and Latan, 2017). This budget assists in keeping

optimum balance among production and sales stock position in the manufacturing unit. The task

of preparing this budget is given to production manager in the company. The production team in

Excite Entertainment Ltd. exercises this budget to identify the appropriate factors responsible

for lowering the sales of the businesses. The company make the necessary strategy to meet the

requirements of the stock to serve the customers and therefore plan the chronological sequence

of various operations to produce estimated production. It helped the company in controlling the

supply of raw materials, stock of finished goods and unfinished work.

Merits-

It enables optimum utilisation of labour hours in the production and maximum use of the

plant and machinery. It keeps a check on the expenses of the production as there is consistent production in the

unit.

Demerits-

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.