Management Accounting Solutions: Detailed Financial Analysis

VerifiedAdded on 2021/04/24

|16

|3081

|23

Homework Assignment

AI Summary

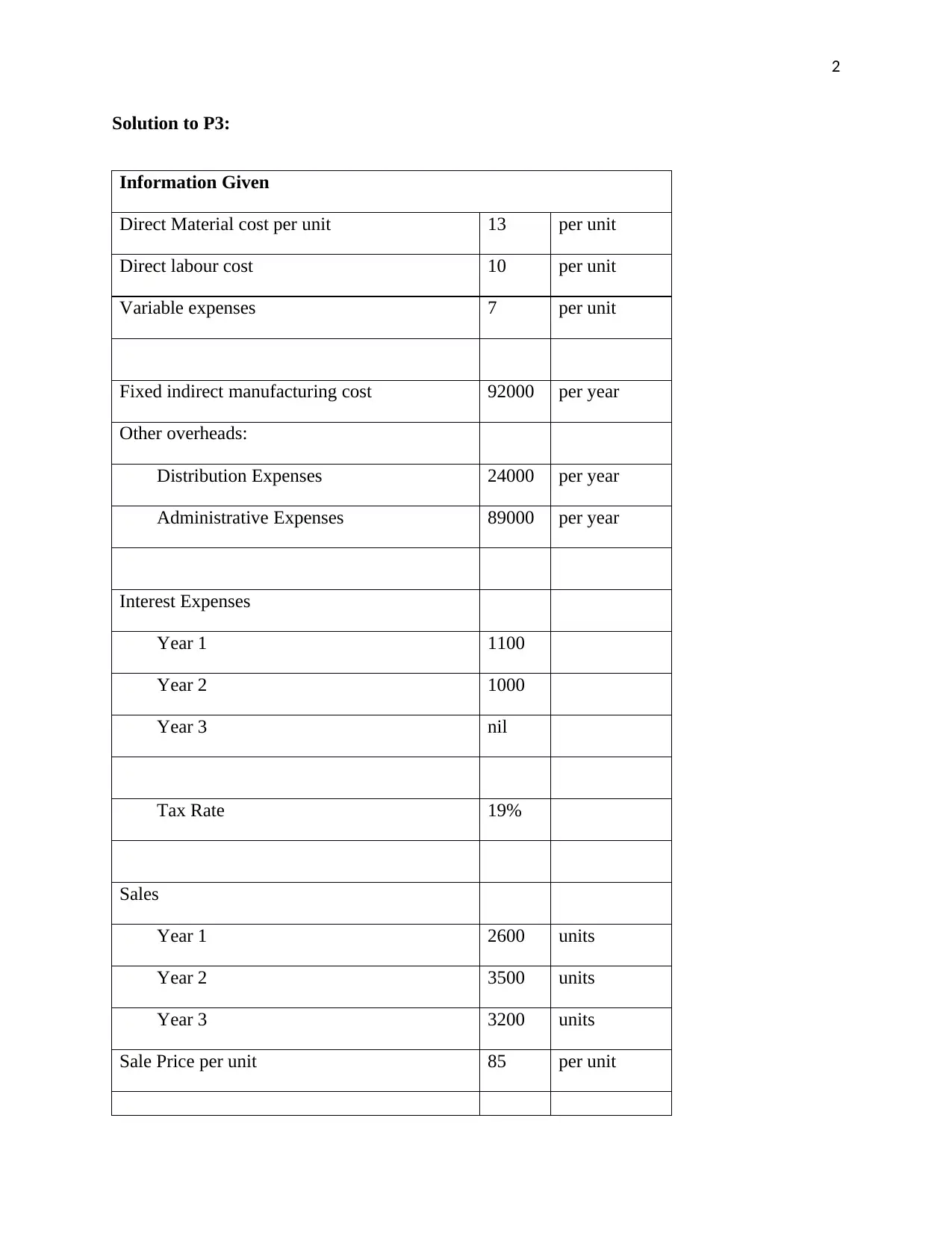

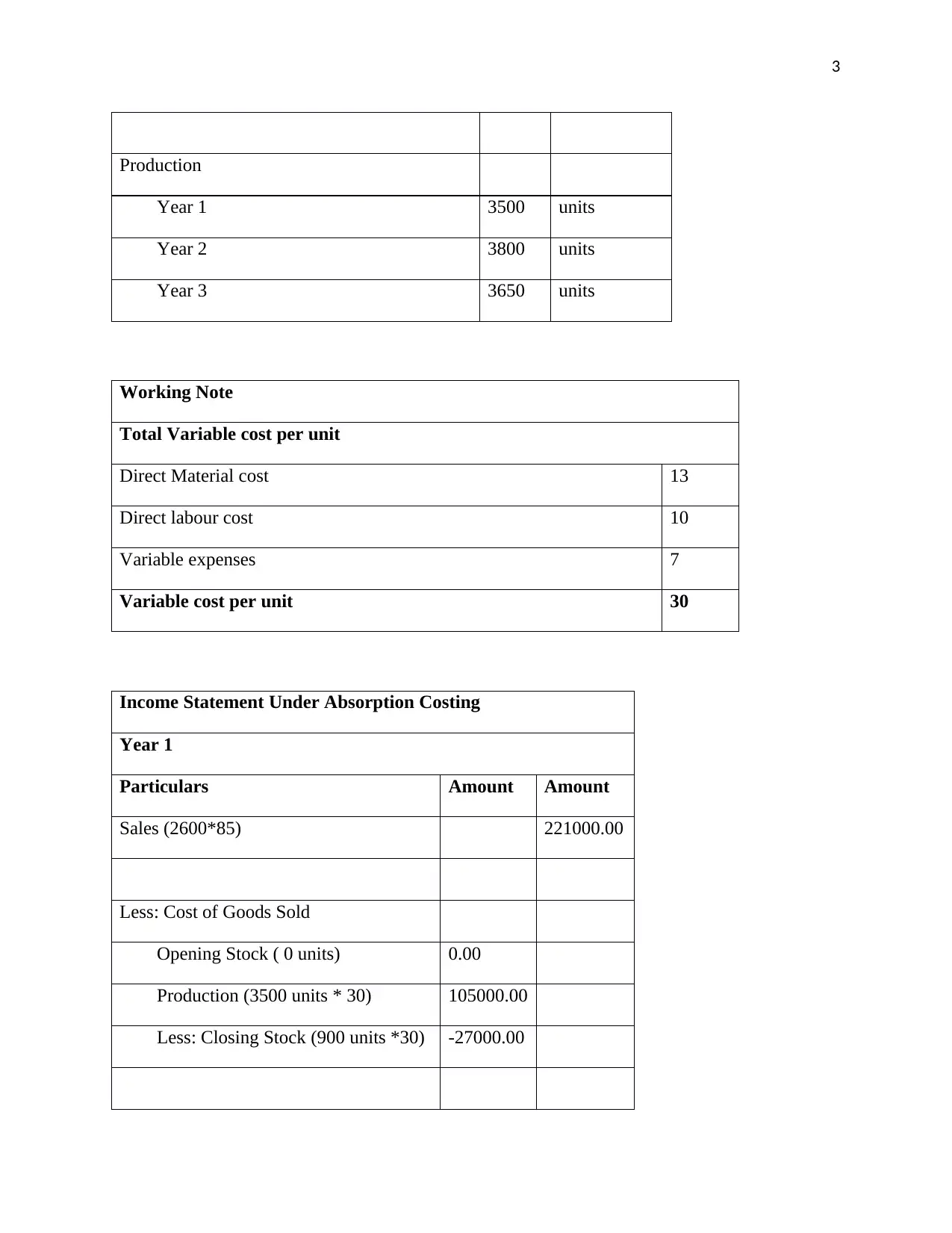

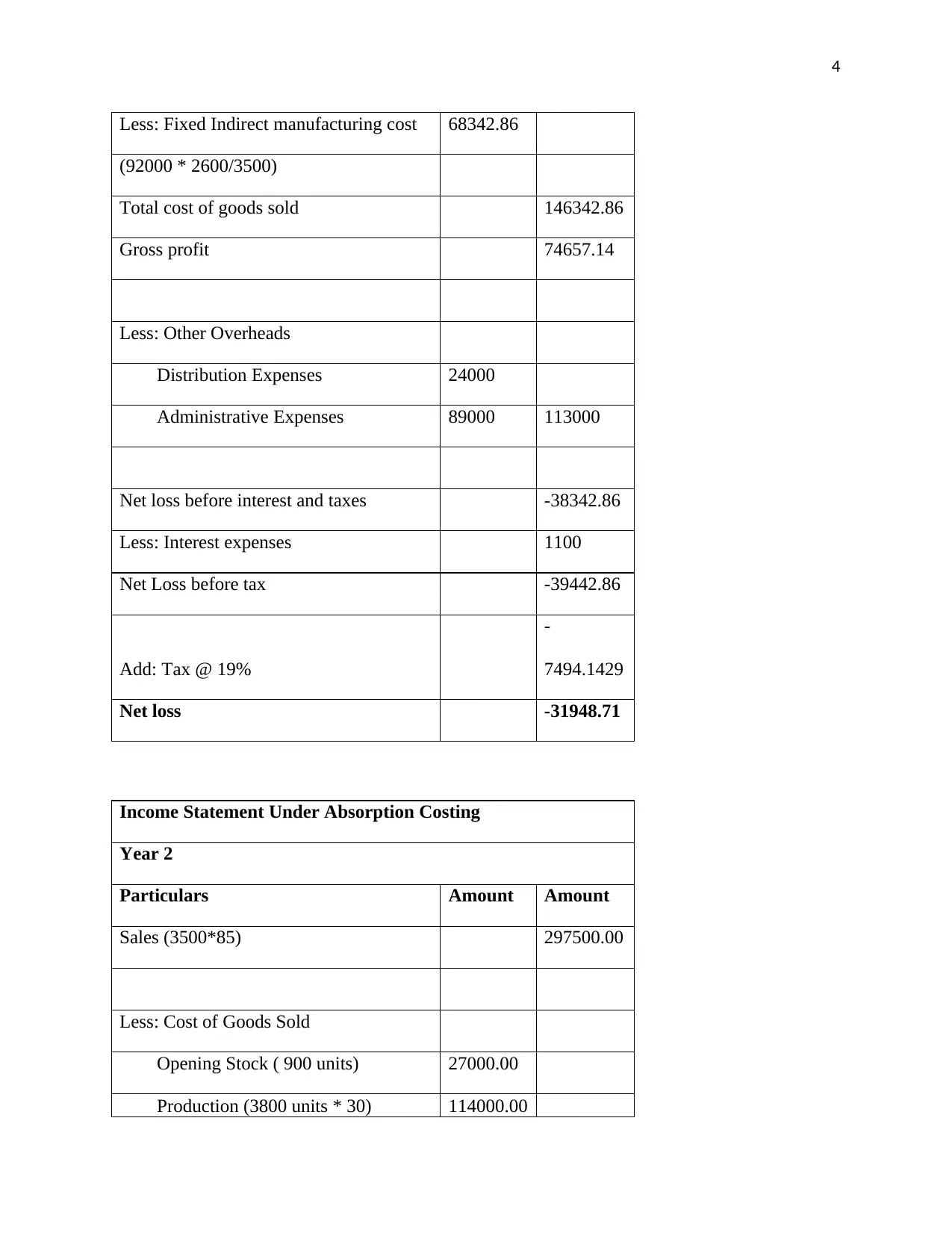

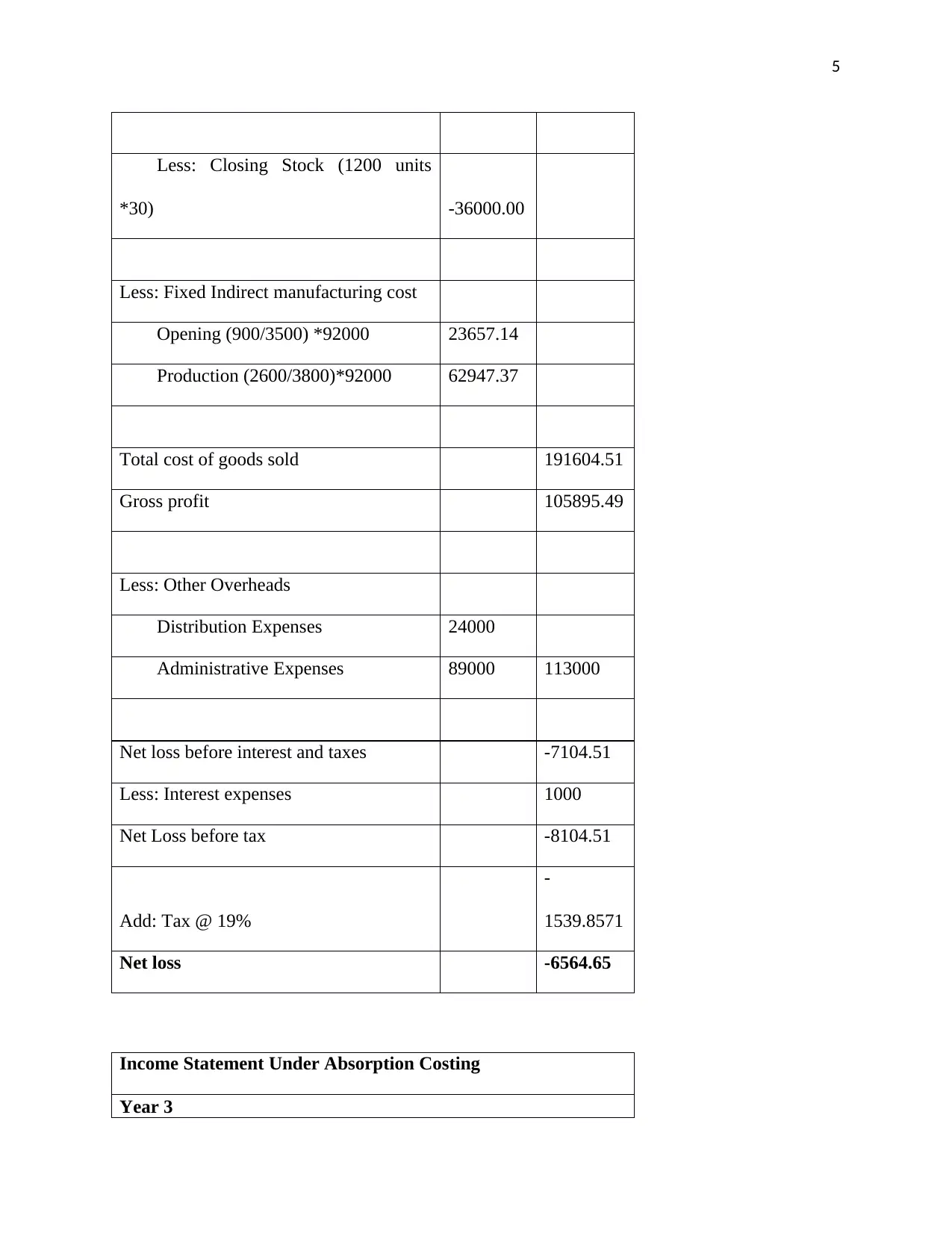

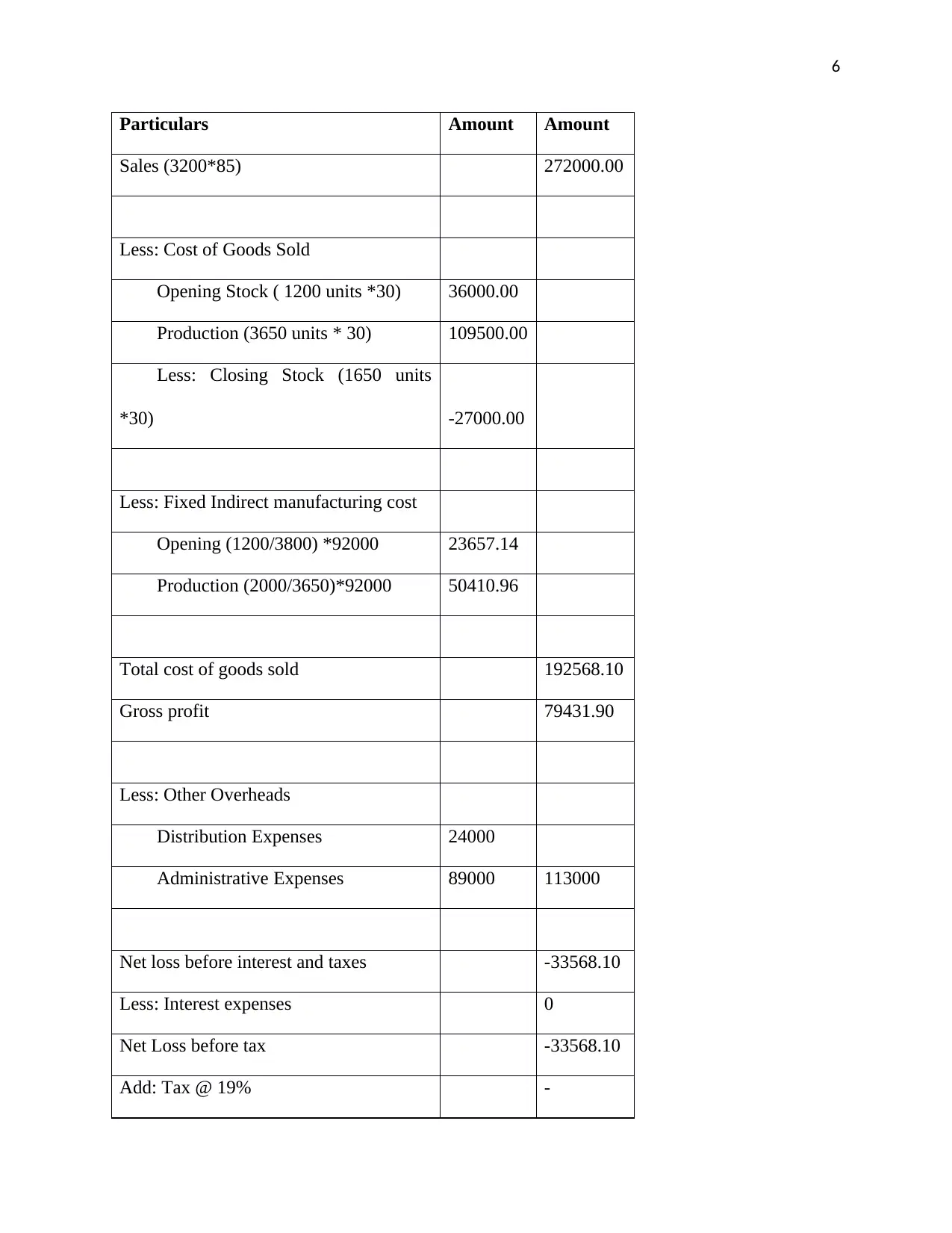

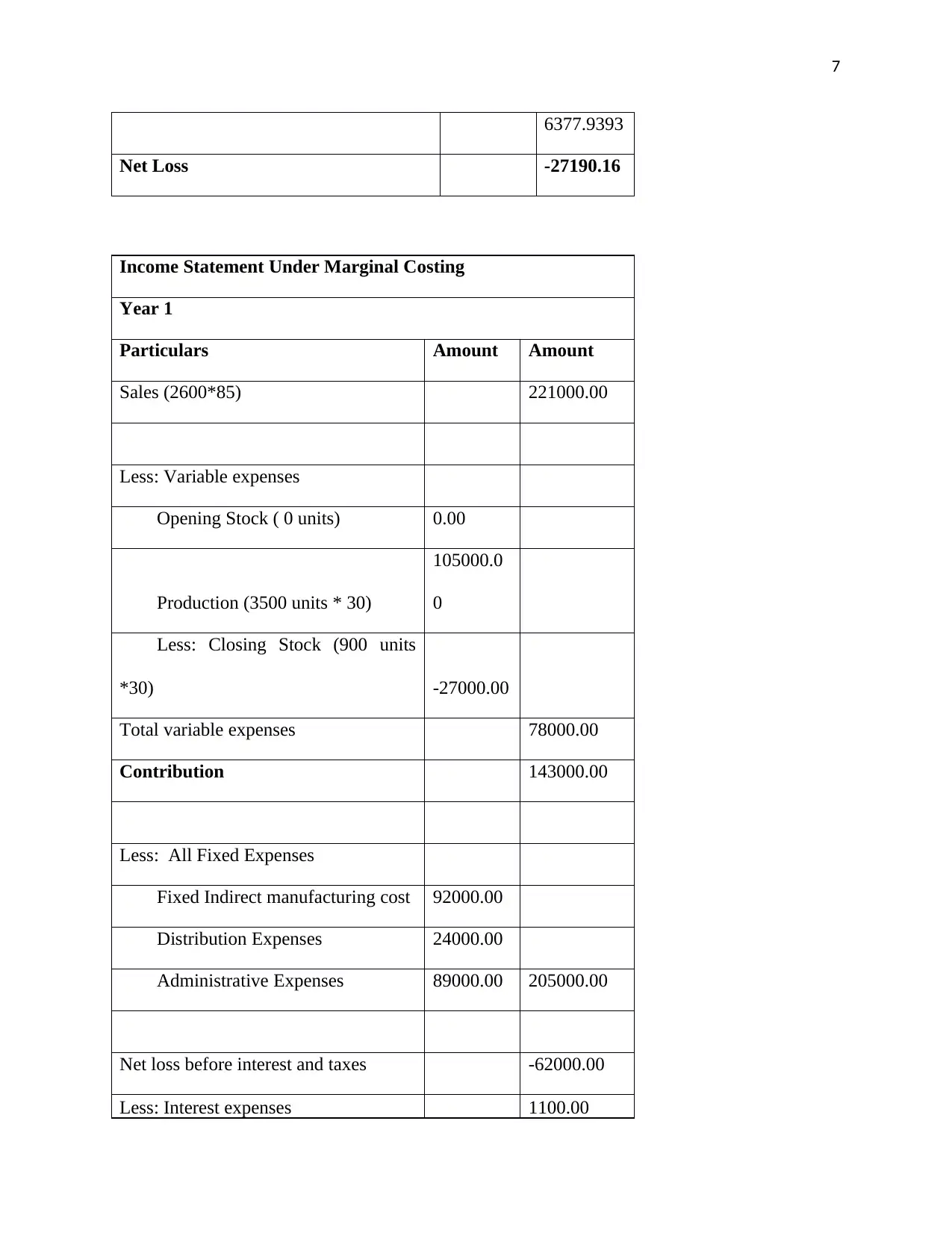

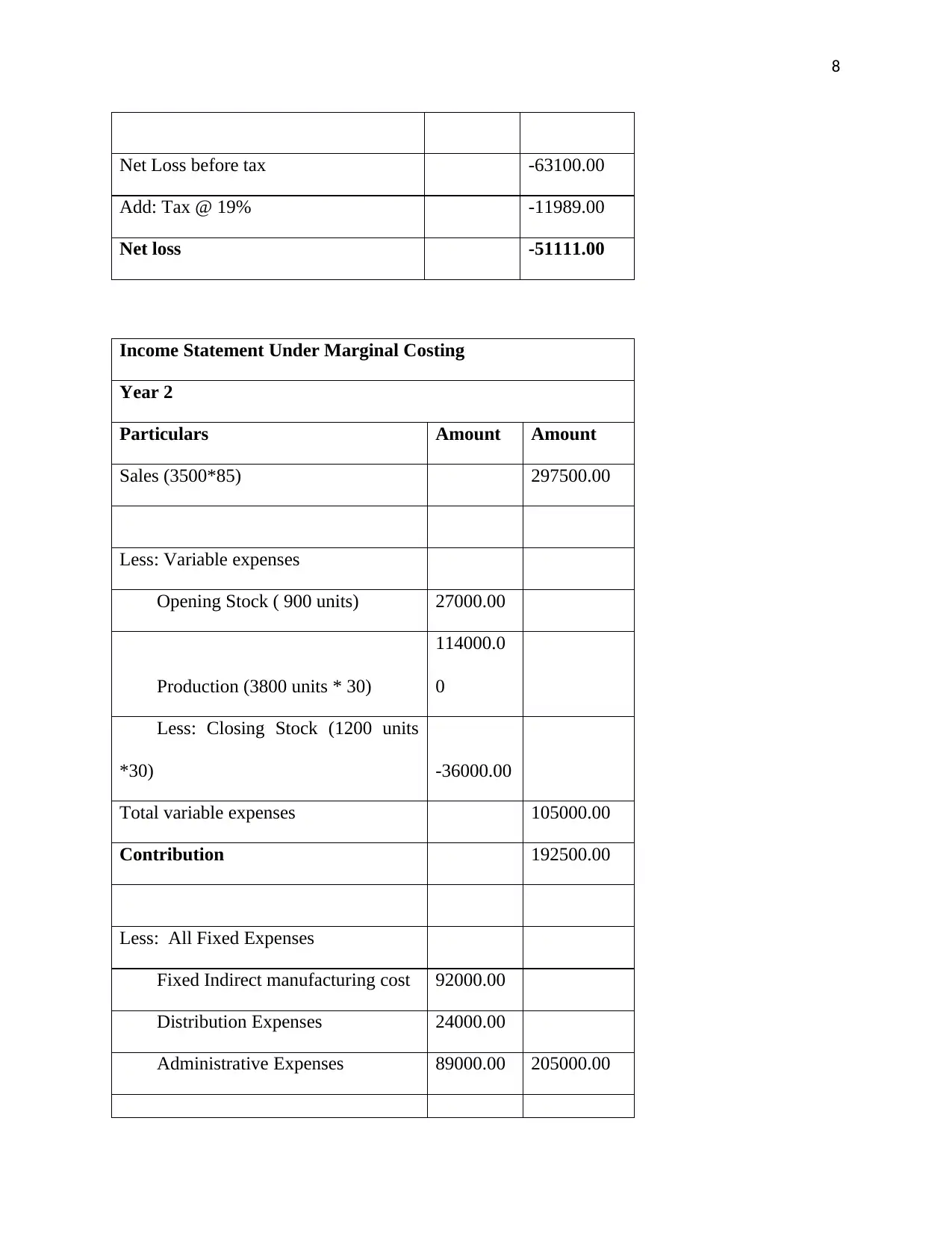

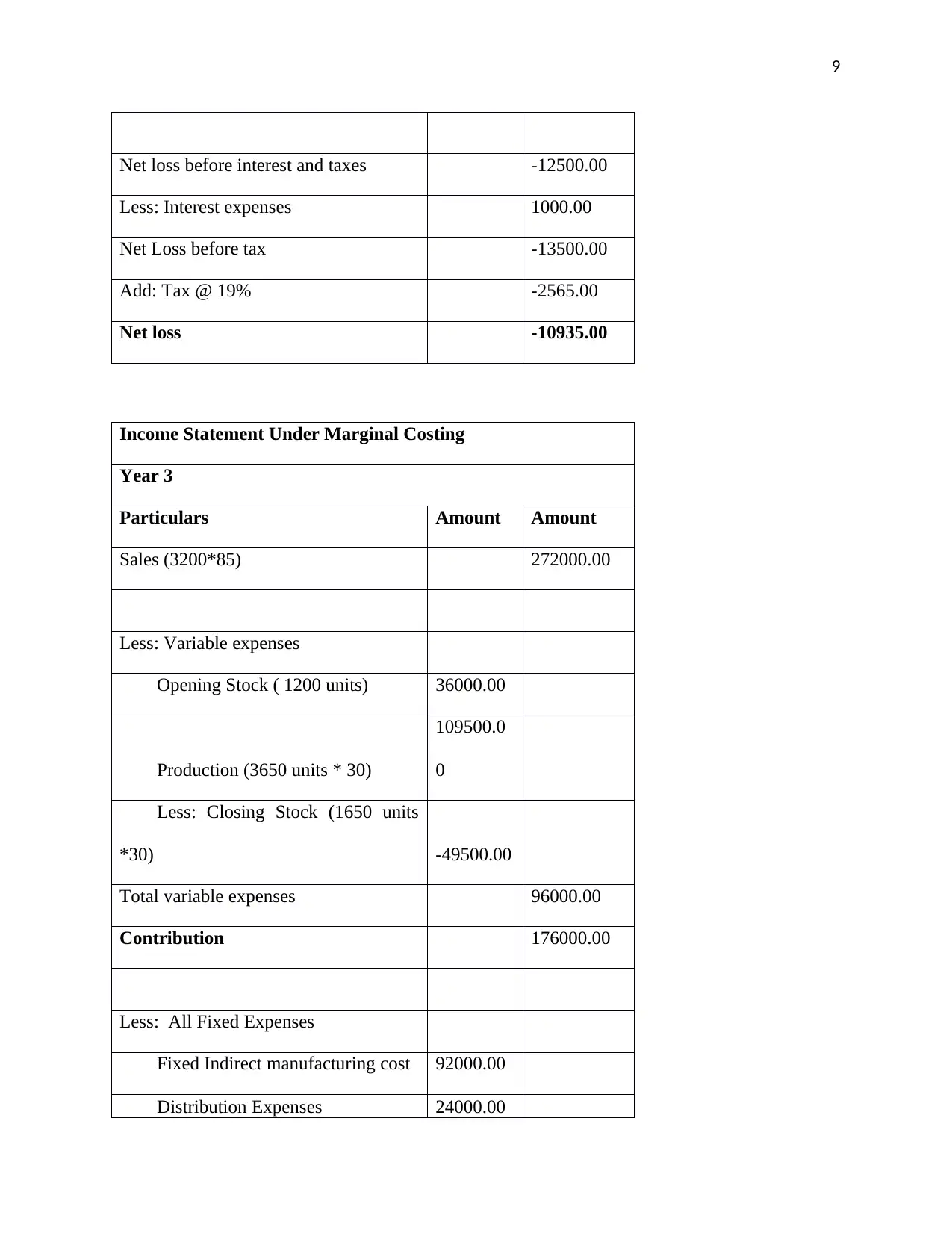

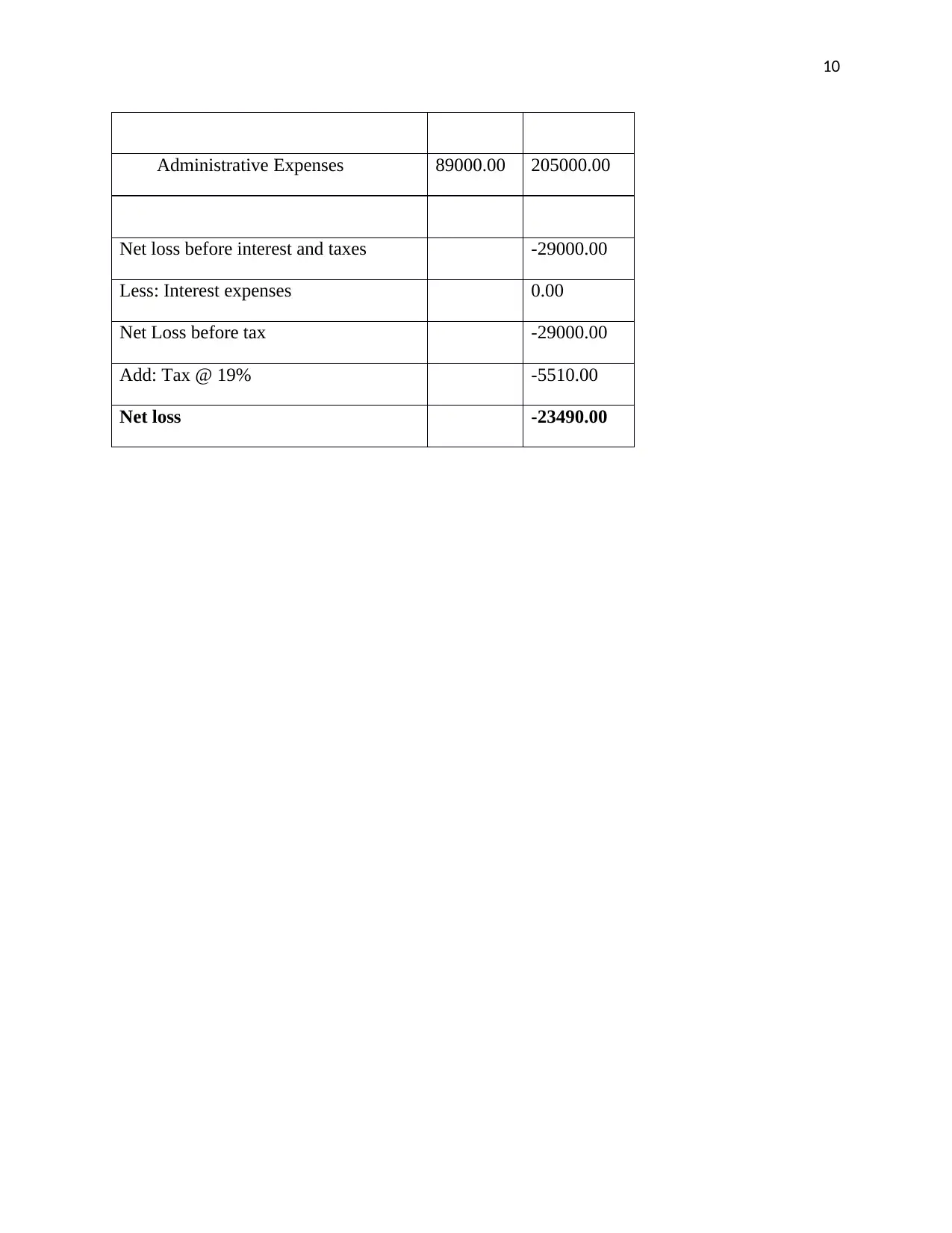

This document provides comprehensive solutions to management accounting problems P3, P4, and P5. The solution to P3 includes income statements under both absorption and marginal costing methods, analyzing sales, cost of goods sold, and various overheads over three years. P4 delves into budgeting, explaining its purpose in planning and performance measurement, along with the advantages and disadvantages of budgeting, variance analysis, and ratio analysis. P5 explores the application of management accounting systems, such as cost accounting, inventory management, and job costing, in addressing financial problems within business organizations. The document offers a detailed financial analysis, including the use of management accounting systems for responding to financial problems in business organizations.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.