Management Accounting Report: AIRDRI Case Study Analysis

VerifiedAdded on 2021/02/22

|22

|4930

|76

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within an organizational context, using AIRDRI as a case study. It explores essential requirements for management accounting systems, different reporting methods, and the calculation of costs using marginal and absorption costing techniques to prepare income statements. The report further examines the advantages and disadvantages of planning tools used for budgetary control and analyzes how organizations adapt management accounting systems to respond to financial problems, ultimately leading to sustainable success. The integration of management accounting systems and reporting within organizational processes is critically evaluated, providing insights into effective financial management strategies. The report includes discussions on inventory management, cost accounting, price optimization, and job costing, highlighting the importance of these tools for informed decision-making and achieving organizational goals.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................4

P2 Explain different methods used for management accounting reporting................................6

M1 Evaluate the benefits of management accounting systems and their application within an

organisational context.................................................................................................................8

D1 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes..............................................................8

TASK 2............................................................................................................................................8

P 3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................8

M2 Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents...................................................................................................13

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities....................................................................................................................................13

TASK 3..........................................................................................................................................14

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control......................................................................................................................14

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets....................................................................................................................15

TASK 4..........................................................................................................................................16

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................16

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................4

P2 Explain different methods used for management accounting reporting................................6

M1 Evaluate the benefits of management accounting systems and their application within an

organisational context.................................................................................................................8

D1 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes..............................................................8

TASK 2............................................................................................................................................8

P 3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................8

M2 Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents...................................................................................................13

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities....................................................................................................................................13

TASK 3..........................................................................................................................................14

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control......................................................................................................................14

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets....................................................................................................................15

TASK 4..........................................................................................................................................16

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................16

M4 Analyse how, in responding to financial problems, management accounting can lead

organisations to sustainable success..........................................................................................17

D3 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success..............................................................17

CONCLUSION..............................................................................................................................18

REFERENCES .............................................................................................................................19

.........................................................................................................................................................1

organisations to sustainable success..........................................................................................17

D3 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success..............................................................17

CONCLUSION..............................................................................................................................18

REFERENCES .............................................................................................................................19

.........................................................................................................................................................1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting also known as managerial accounting is a chain of activities to

analyse cost of business and their operations to build financial reports, records and various kinds

of accounts to take appropriate decisions to achieve organisational goals and objectives. In other

words, it is an important act to make sense about financial and cost data for translate it into

meaning information and data in an organisation. This report is based on AIRDRI which is

founded in 1974 by significant advancement of hand drying industry by finding out gaps. This

report is based on management accounting and necessary requirements for management

accounting systems. It also includes kinds of methods used for management accounting reporting

to get fruitful for an organisation. It also includes calculation of various kinds of cost by

preparing income statement of both marginal and absorption cost. Further it includes advantages

and disadvantages of planning tools for budgetary control and in ways by organisation adopt

management accounting systems to resolve financial problems.

TASK 1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.

Management accounting is one of most important part of accounts in which application

of knowledge, tools and techniques with concept should be prepare to get accurate accounting

information (Banerjee, 2012). Accounting information proved helpful for organisation to

formulate plans and policies and to control organisational operations for making effective

Management accounting also known as managerial accounting is a chain of activities to

analyse cost of business and their operations to build financial reports, records and various kinds

of accounts to take appropriate decisions to achieve organisational goals and objectives. In other

words, it is an important act to make sense about financial and cost data for translate it into

meaning information and data in an organisation. This report is based on AIRDRI which is

founded in 1974 by significant advancement of hand drying industry by finding out gaps. This

report is based on management accounting and necessary requirements for management

accounting systems. It also includes kinds of methods used for management accounting reporting

to get fruitful for an organisation. It also includes calculation of various kinds of cost by

preparing income statement of both marginal and absorption cost. Further it includes advantages

and disadvantages of planning tools for budgetary control and in ways by organisation adopt

management accounting systems to resolve financial problems.

TASK 1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.

Management accounting is one of most important part of accounts in which application

of knowledge, tools and techniques with concept should be prepare to get accurate accounting

information (Banerjee, 2012). Accounting information proved helpful for organisation to

formulate plans and policies and to control organisational operations for making effective

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decisions by using resources for safeguard assets. Management accounting is an process and

presentation of accounting and data related to economics that helps in evaluating performance of

management for building strategies, to compare things in better way with budgeting and

forecasting.

Essential requirement of management accounting systems:

Inventory management system:

Inventory management system helps in track goods in the whole supply chain that supply

goods and services to ultimate consumer base. Inventory management system covers from

production to retail, warehouse to shopping and includes movement of goods or stock in

between. Inventory management system proved helpful to track supply products and services

from which path goods passes through (Cadez and Guilding, 2012.). It is very much potential

for transfer management that helps to manage multiple sites simultaneously to coordinate each

and every activity in proper way while move products at place where it is important. So

inventory management is very much potential for an organisation to deal in effective manner.

Cost accounting system:

Cost accounting system also known as product costing system that is an framework used

by various firms or organisations to get estimate about cost of products and services to analyse

profitability, valuation of inventory by controlling cost in proper way. In context of AIRDRI they

use various kinds of cost accounting system to coordinate each and every activity to estimate

accurate cost of products and services that is an critical task for an organisation. It helps in

estimating closing values of materials, finished products and work in progress and many more in

positive way.

Price optimisation system:

Price optimisation is an accounting tool that proved helpful in pricing fields to evaluate

various applications that enables in set prices (DRURY, 2013. ). It helps to calculate in some

manner demand varies as price changes by combining data and information on basis of cost and

inventory levels to recommend best prices that enhance pricing. In context of AIRDRI with help

of price optimization system organisation can be able to set best price as per demand and supply

of goods and services in best way.

Job costing:

presentation of accounting and data related to economics that helps in evaluating performance of

management for building strategies, to compare things in better way with budgeting and

forecasting.

Essential requirement of management accounting systems:

Inventory management system:

Inventory management system helps in track goods in the whole supply chain that supply

goods and services to ultimate consumer base. Inventory management system covers from

production to retail, warehouse to shopping and includes movement of goods or stock in

between. Inventory management system proved helpful to track supply products and services

from which path goods passes through (Cadez and Guilding, 2012.). It is very much potential

for transfer management that helps to manage multiple sites simultaneously to coordinate each

and every activity in proper way while move products at place where it is important. So

inventory management is very much potential for an organisation to deal in effective manner.

Cost accounting system:

Cost accounting system also known as product costing system that is an framework used

by various firms or organisations to get estimate about cost of products and services to analyse

profitability, valuation of inventory by controlling cost in proper way. In context of AIRDRI they

use various kinds of cost accounting system to coordinate each and every activity to estimate

accurate cost of products and services that is an critical task for an organisation. It helps in

estimating closing values of materials, finished products and work in progress and many more in

positive way.

Price optimisation system:

Price optimisation is an accounting tool that proved helpful in pricing fields to evaluate

various applications that enables in set prices (DRURY, 2013. ). It helps to calculate in some

manner demand varies as price changes by combining data and information on basis of cost and

inventory levels to recommend best prices that enhance pricing. In context of AIRDRI with help

of price optimization system organisation can be able to set best price as per demand and supply

of goods and services in best way.

Job costing:

Job costing involves sum up of cost of materials, labour and overhead cost for a specific

job cost. This is an best tool and techniques that helps in tracing cost for an individual by

examining various factors in better way (Fullerton, Kennedy and Widener, 2014). It enables to

accumulate various kinds of cost and data at small unit such as materials, labour and overhead

associated within it. In context of AIRDRI they by using job costing can be evaluate various

factors that associated with their cost and their structures in better way.

Distinction between management and financial accounting:

There are difference in management and financial accounting that are as follows:

Aggregation:

Financial accounting depicts the whole or entire results about business on other hand

managerial accounting reports on detailed manner in which includes profits of products, product

line and geographical region of consumers.

Efficiency:

Financial accounting majorly related with complete profitability of a business on other

hand managerial accounting concerned with about factors that cause problems and ways to

resolve them in positive way.

Reporting focus:

Financial reporting concerned with creation of financial statements that are distributed in

both internally and externally in an organisation. On other hand management accounting

concerned with operational reports that distributed within organisation.

As after observing the difference in both these terms useful for an organisation to gain important

insights and results out of it.

P2 Explain different methods used for management accounting reporting.

For an organisation there are various kinds of management accounting reporting that

helps in internal concentration of data in internal manner through financial accounting (.Herbert

and Seal, 2012). It helps in taking important decisions and planning with controlling data and

statistics. All these methods that use by an AIRDRI helps in management accounting reporting to

get desirable goals and objectives in proper way.

Budget Report:

Budget report is an kind of internal report proved useful for management by comparing

and estimating budget projections to achieve actual performance that received during a period of

job cost. This is an best tool and techniques that helps in tracing cost for an individual by

examining various factors in better way (Fullerton, Kennedy and Widener, 2014). It enables to

accumulate various kinds of cost and data at small unit such as materials, labour and overhead

associated within it. In context of AIRDRI they by using job costing can be evaluate various

factors that associated with their cost and their structures in better way.

Distinction between management and financial accounting:

There are difference in management and financial accounting that are as follows:

Aggregation:

Financial accounting depicts the whole or entire results about business on other hand

managerial accounting reports on detailed manner in which includes profits of products, product

line and geographical region of consumers.

Efficiency:

Financial accounting majorly related with complete profitability of a business on other

hand managerial accounting concerned with about factors that cause problems and ways to

resolve them in positive way.

Reporting focus:

Financial reporting concerned with creation of financial statements that are distributed in

both internally and externally in an organisation. On other hand management accounting

concerned with operational reports that distributed within organisation.

As after observing the difference in both these terms useful for an organisation to gain important

insights and results out of it.

P2 Explain different methods used for management accounting reporting.

For an organisation there are various kinds of management accounting reporting that

helps in internal concentration of data in internal manner through financial accounting (.Herbert

and Seal, 2012). It helps in taking important decisions and planning with controlling data and

statistics. All these methods that use by an AIRDRI helps in management accounting reporting to

get desirable goals and objectives in proper way.

Budget Report:

Budget report is an kind of internal report proved useful for management by comparing

and estimating budget projections to achieve actual performance that received during a period of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

time. It also proved useful in comparison of actual budgeted performance with actual

performance during a accounting period in best way. As budget are financial reports that helps in

estimation about future projects that are often in accurate in nature. During an accounting period

managers and others compare with budgeted numbers that prepared in beginning of a period for

actual results that incurs. In context of AIRDRI by preparing budget report organisation can be

able to predict about future projections in better way so that important measures should be

adopted.

Performance report:

Performance report refers to work performance to analysing, creating and sending to

respective stakeholders of an organisation that involved in performance reporting regarding a

project in better way (Hilton and Platt, 2013.). In other words performance report is an outcome

of an activity that helps in comparing actual results with budgeted or actual standards by

observing variance in these terms I positive way. That kind of report helps in taking appropriate

decisions in condition of unfavourable variance. There are some examples regarding

performance report that helps to AIRDRI that are as an personnel get annual performance report

to deal with various activities with appropriate action plan to achieve organisational goals and

objectives.

Accounts receivable report:

Accounts receivable report is one of most important aspect for an organisation that helps

in list out about unpaid consumer invoices and unused memos of credit as per data ranges

(Kaplan and Atkinson, 2015.). It is one of primary tool proved helpful for collection personnel

to evaluate various kinds of overdue that are undue in nature. That kind of report used by

management to evaluate effectiveness of various credit and collection functions takes place in an

organisation. That report also very much helpful in estimating bad debts that are build for

allowance for doubtful accounts in better way. In context of AIRDRI they use various kinds of

budget report to accumulate right kind of knowledge and information to reach at desirable

outcomes in proper way. There are various kinds of factors that help in evaluation of costing and

management of tools with techniques that helps in evaluation of inventory management to get

fruitful results.

Inventory management report:

performance during a accounting period in best way. As budget are financial reports that helps in

estimation about future projects that are often in accurate in nature. During an accounting period

managers and others compare with budgeted numbers that prepared in beginning of a period for

actual results that incurs. In context of AIRDRI by preparing budget report organisation can be

able to predict about future projections in better way so that important measures should be

adopted.

Performance report:

Performance report refers to work performance to analysing, creating and sending to

respective stakeholders of an organisation that involved in performance reporting regarding a

project in better way (Hilton and Platt, 2013.). In other words performance report is an outcome

of an activity that helps in comparing actual results with budgeted or actual standards by

observing variance in these terms I positive way. That kind of report helps in taking appropriate

decisions in condition of unfavourable variance. There are some examples regarding

performance report that helps to AIRDRI that are as an personnel get annual performance report

to deal with various activities with appropriate action plan to achieve organisational goals and

objectives.

Accounts receivable report:

Accounts receivable report is one of most important aspect for an organisation that helps

in list out about unpaid consumer invoices and unused memos of credit as per data ranges

(Kaplan and Atkinson, 2015.). It is one of primary tool proved helpful for collection personnel

to evaluate various kinds of overdue that are undue in nature. That kind of report used by

management to evaluate effectiveness of various credit and collection functions takes place in an

organisation. That report also very much helpful in estimating bad debts that are build for

allowance for doubtful accounts in better way. In context of AIRDRI they use various kinds of

budget report to accumulate right kind of knowledge and information to reach at desirable

outcomes in proper way. There are various kinds of factors that help in evaluation of costing and

management of tools with techniques that helps in evaluation of inventory management to get

fruitful results.

Inventory management report:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management report is very much essential for an organisation to deal in

effective manner to accumulate data and information regarding to manage stock in proper way.

One of best way to using and understand right kind of inventory management reports so that

accurate results should be accomplished. Accurate and up to date and appropriate inventory

management is very much important to find out trends, weaknesses and strengths to fill gaps to

gap the inefficiencies in better way (Kotas, 2014.). To get important knowledge and information

about profitable products by ensuring that each and every level performing well at optimum

level.

So all are the important tools and techniques for management accounting reporting to get

potential results in better way.

M1 Evaluate the benefits of management accounting systems and their application within an

organisational context.

Management accounting systems are very much important for an organisation with their

various systems that are cost accounting with help of it AIRDRI can easily estimate cost of

manufacturing products and services. With help of inventory management organisation can be

able to improve their efficiency and effectiveness in proper way by reducing cost. With help of

job costing duplication of work should be eliminated in proper way so that organisational results

should be accomplished in proper way. Job costing system also helps in knowing each and every

aspect related to product in better way.

D1 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes.

Integration of management accounting systems and management accounting is very much

important for an organisation to integrate both of them to achieve organisational goals and

objectives. In context of budget report

Budget report Budget report is very much important for an organisation to deal in

effective manner. With help of it organisation can be able to evaluate

ratio of income and expenditure in better way. In context of AIRDRI

by effective budget building can be able to take important decisions by

predict future in well manner.

Performance report Performance report is another crucial factor for organisation to

effective manner to accumulate data and information regarding to manage stock in proper way.

One of best way to using and understand right kind of inventory management reports so that

accurate results should be accomplished. Accurate and up to date and appropriate inventory

management is very much important to find out trends, weaknesses and strengths to fill gaps to

gap the inefficiencies in better way (Kotas, 2014.). To get important knowledge and information

about profitable products by ensuring that each and every level performing well at optimum

level.

So all are the important tools and techniques for management accounting reporting to get

potential results in better way.

M1 Evaluate the benefits of management accounting systems and their application within an

organisational context.

Management accounting systems are very much important for an organisation with their

various systems that are cost accounting with help of it AIRDRI can easily estimate cost of

manufacturing products and services. With help of inventory management organisation can be

able to improve their efficiency and effectiveness in proper way by reducing cost. With help of

job costing duplication of work should be eliminated in proper way so that organisational results

should be accomplished in proper way. Job costing system also helps in knowing each and every

aspect related to product in better way.

D1 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes.

Integration of management accounting systems and management accounting is very much

important for an organisation to integrate both of them to achieve organisational goals and

objectives. In context of budget report

Budget report Budget report is very much important for an organisation to deal in

effective manner. With help of it organisation can be able to evaluate

ratio of income and expenditure in better way. In context of AIRDRI

by effective budget building can be able to take important decisions by

predict future in well manner.

Performance report Performance report is another crucial factor for organisation to

evaluate performance of an individual by identifying strength and

weaknesses of an individual in positive way to get desirable outcomes.

TASK 2

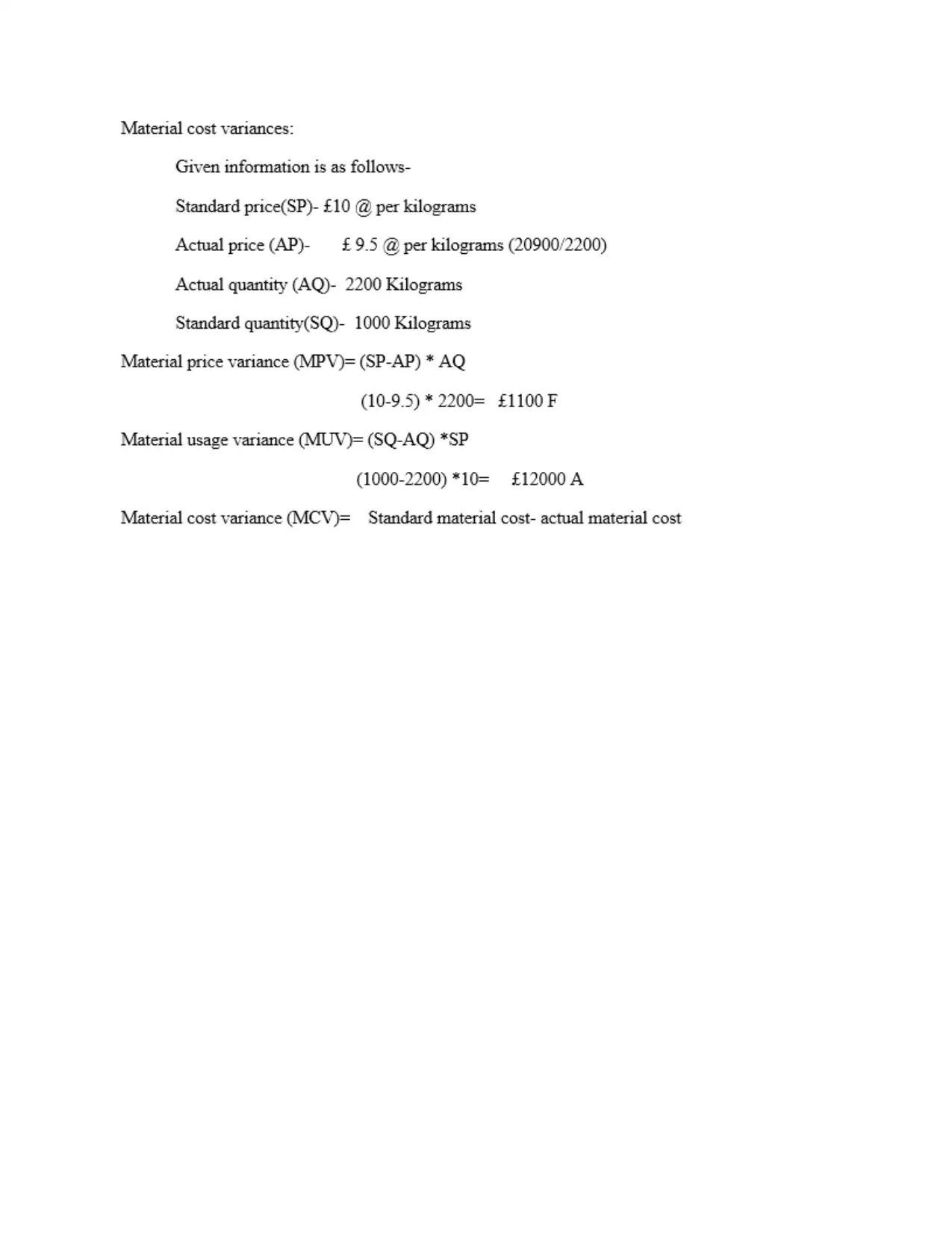

P 3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs

Marginal cost- It indicates to a accounting system in which variable costs are replaced to

cost units and fixed costs of the time period are written off in full against the accumulation

endeavour. This coat is also known as variable cost that include labour and material cost and an

computation portion of fixed costs (Banerjee, 2012).. In organisation where average cost are

fairly invariable, marginal cost is normally equal to average cost. It is the most common kind of

costing method that underline on a organized categorization of expenditure in to fixed and

variable. Fixed and variable endeavour per unit which is calculated to consider only variable

production overheads, within this method after categorisation of expenditures or costs.

Absorption cost- It is a method of accounting which demesne the whole and entire cost

of producing and manufacturing a service (Kotas, 2014.).. It can be a method of analysing and

calculating the cost of a good and service that are manufacture by a company to take into account

indirect expenditures as well as direct costs. Within this method, all the overheads related to the

process of manufacturing which is regardless of their nature are replaced ton unit cosy of the

goods. In AIRDRI, this cost can be calculated by the management of the company. Within it, the

cost per unit is direct substantial, direct labour, changeable overheads and determinate

overheads. Fixed overheads per unit is deliberate by dividing total fixed operating cost by the

number of units produced.

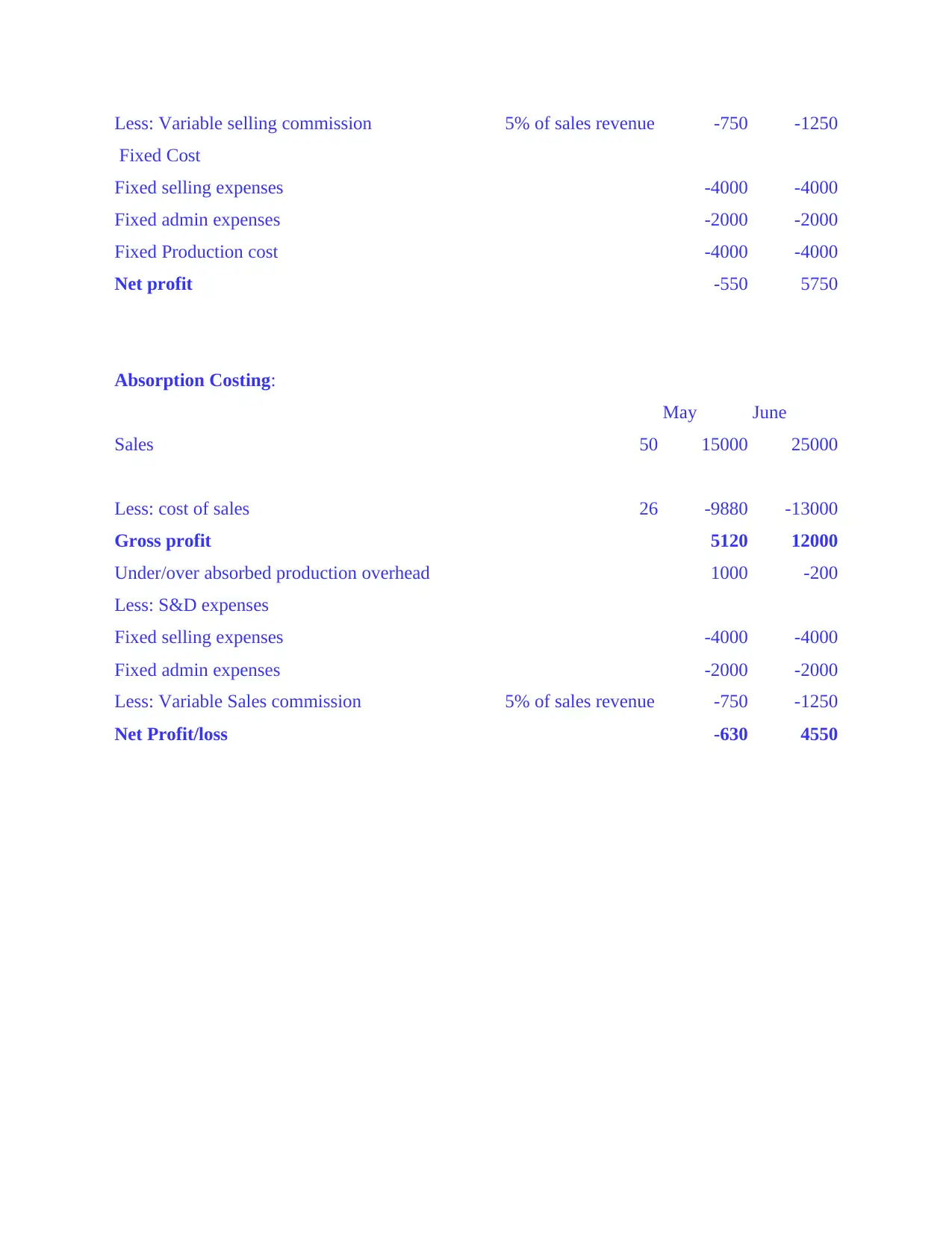

Marginal costing

Selling per unit price 50 15000 25000

Less: Various Marginal Costs

Per unit Direct materials cost -8 -2400 -4000

Per unit Direct labour cost -5 -1500 -2500

Per unit variable production overheads cost -3 -900 -1500

Contribution 10200 17000

weaknesses of an individual in positive way to get desirable outcomes.

TASK 2

P 3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs

Marginal cost- It indicates to a accounting system in which variable costs are replaced to

cost units and fixed costs of the time period are written off in full against the accumulation

endeavour. This coat is also known as variable cost that include labour and material cost and an

computation portion of fixed costs (Banerjee, 2012).. In organisation where average cost are

fairly invariable, marginal cost is normally equal to average cost. It is the most common kind of

costing method that underline on a organized categorization of expenditure in to fixed and

variable. Fixed and variable endeavour per unit which is calculated to consider only variable

production overheads, within this method after categorisation of expenditures or costs.

Absorption cost- It is a method of accounting which demesne the whole and entire cost

of producing and manufacturing a service (Kotas, 2014.).. It can be a method of analysing and

calculating the cost of a good and service that are manufacture by a company to take into account

indirect expenditures as well as direct costs. Within this method, all the overheads related to the

process of manufacturing which is regardless of their nature are replaced ton unit cosy of the

goods. In AIRDRI, this cost can be calculated by the management of the company. Within it, the

cost per unit is direct substantial, direct labour, changeable overheads and determinate

overheads. Fixed overheads per unit is deliberate by dividing total fixed operating cost by the

number of units produced.

Marginal costing

Selling per unit price 50 15000 25000

Less: Various Marginal Costs

Per unit Direct materials cost -8 -2400 -4000

Per unit Direct labour cost -5 -1500 -2500

Per unit variable production overheads cost -3 -900 -1500

Contribution 10200 17000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Variable selling commission 5% of sales revenue -750 -1250

Fixed Cost

Fixed selling expenses -4000 -4000

Fixed admin expenses -2000 -2000

Fixed Production cost -4000 -4000

Net profit -550 5750

Absorption Costing:

May June

Sales 50 15000 25000

Less: cost of sales 26 -9880 -13000

Gross profit 5120 12000

Under/over absorbed production overhead 1000 -200

Less: S&D expenses

Fixed selling expenses -4000 -4000

Fixed admin expenses -2000 -2000

Less: Variable Sales commission 5% of sales revenue -750 -1250

Net Profit/loss -630 4550

Fixed Cost

Fixed selling expenses -4000 -4000

Fixed admin expenses -2000 -2000

Fixed Production cost -4000 -4000

Net profit -550 5750

Absorption Costing:

May June

Sales 50 15000 25000

Less: cost of sales 26 -9880 -13000

Gross profit 5120 12000

Under/over absorbed production overhead 1000 -200

Less: S&D expenses

Fixed selling expenses -4000 -4000

Fixed admin expenses -2000 -2000

Less: Variable Sales commission 5% of sales revenue -750 -1250

Net Profit/loss -630 4550

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.