Analysing Management Accounting for Financial Problem Resolution

VerifiedAdded on 2023/01/18

|17

|4650

|28

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and their application in addressing financial problems. It begins by defining management accounting and its role in modern businesses, using Unilever as a case study. The report elaborates on various management accounting systems such as cost accounting, price optimization, job costing, and inventory management, detailing their benefits and critical evaluation within a company. It also covers different methods used in management accounting reporting, including budget reports, performance reports, and cost reports. Furthermore, the report applies absorption and marginal costing techniques to prepare income statements, demonstrating the accurate application and interpretation of data for various business activities. It also discusses the advantages and disadvantages of different planning tools used in budgetary control and how these tools can be used to prepare and forecast budgets. Finally, the report explores how management accounting systems can be used to respond to financial problems, highlighting the role of management accounting and planning tools in this context. Desklib offers more solved assignments and past papers for students.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

Understanding of management accounting systems....................................................................1

Different methods used in management accounting

reporting......................................................................................................................................2

Benefits of various kinds of systems...........................................................................................3

Critically evaluating

of MA systems and reporting integrated within company..........................................................4

TASK 2............................................................................................................................................4

Absorption and marginal costing to prepare income statements.................................................4

Accurate application of range of management accounting techniques........................................6

Accurate application and interpretation of data for a range of business activities......................7

TASK 3............................................................................................................................................7

Advantages and disadvantages of different

types of planning tools used in budgetary control......................................................................7

Analyse of planning tools and their

application to prepare and forecast budgets................................................................................9

TASK 4............................................................................................................................................9

Management accounting systems to respond to financial problems............................................9

Role of management accounting in responding to financial problems......................................11

Use of planning tools to respond financial problems.................................................................11

CONCLUSION..............................................................................................................................11

REFERENCERS ...........................................................................................................................12

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

Understanding of management accounting systems....................................................................1

Different methods used in management accounting

reporting......................................................................................................................................2

Benefits of various kinds of systems...........................................................................................3

Critically evaluating

of MA systems and reporting integrated within company..........................................................4

TASK 2............................................................................................................................................4

Absorption and marginal costing to prepare income statements.................................................4

Accurate application of range of management accounting techniques........................................6

Accurate application and interpretation of data for a range of business activities......................7

TASK 3............................................................................................................................................7

Advantages and disadvantages of different

types of planning tools used in budgetary control......................................................................7

Analyse of planning tools and their

application to prepare and forecast budgets................................................................................9

TASK 4............................................................................................................................................9

Management accounting systems to respond to financial problems............................................9

Role of management accounting in responding to financial problems......................................11

Use of planning tools to respond financial problems.................................................................11

CONCLUSION..............................................................................................................................11

REFERENCERS ...........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In modern business era, the procedures related with gathering, reporting, summarizing,

analysing and assessing the overall internal information of a company which facilitate the

manager in order to make precious decision is known as management accounting (Abernethy and

Wallis, 2018). In fact, it is the processes of identifying, calculating, analysing, assessing and

reporting financial information to meet organisation goals. This process is valuable in making

effective policies for company so that future performance of entire staff member and different

processes can be improved. In order to better know the importance of MA Unilever have been

selected that is basically going under reconstruction. The respective company is a oldest MNC

producing 400 brands that are delivered around 190 countries. Company products provide us

with a remarkable chance to bring about meaningful change, expand business and accomplish

main goal to make sustainable living place for entire customer.

In this report, different MAS and reports with their importance to company are

elaborated, costing techniques in order to improve the net profit, several planning tool which

help in controlling budgets and resolving financial problems. In addition report also cover the

comparison of crucial system of management accounting that are support in detecting the

financial issues and making effective plans to resolve these problems.

TASK 1

Understanding of management accounting systems

Management accounting is an information system connected with method of collecting

financial and non-financial data in order to produce inner reports of different aspects. The main

role of MA is that based on internal documents, corporate managers are able to take appropriate

action for corporate success in the appropriate time to attract more and more stakeholders. It also

help in making accurate planning, controlling and decision making which support in proper

utilisation of resources and employees. Manager properly plans about the activities and make

them profitable in order to increase the overall productivity of company. They usually makes

effective decision and tries to control excess usage of available resources, funds to increase

overall profit margin (Alawattage, Wickramasinghe and Uddin, 2017). There are number of

essential MA system that play a crucial role in making company productive and profitable. Some

of these are discussed below:

1

In modern business era, the procedures related with gathering, reporting, summarizing,

analysing and assessing the overall internal information of a company which facilitate the

manager in order to make precious decision is known as management accounting (Abernethy and

Wallis, 2018). In fact, it is the processes of identifying, calculating, analysing, assessing and

reporting financial information to meet organisation goals. This process is valuable in making

effective policies for company so that future performance of entire staff member and different

processes can be improved. In order to better know the importance of MA Unilever have been

selected that is basically going under reconstruction. The respective company is a oldest MNC

producing 400 brands that are delivered around 190 countries. Company products provide us

with a remarkable chance to bring about meaningful change, expand business and accomplish

main goal to make sustainable living place for entire customer.

In this report, different MAS and reports with their importance to company are

elaborated, costing techniques in order to improve the net profit, several planning tool which

help in controlling budgets and resolving financial problems. In addition report also cover the

comparison of crucial system of management accounting that are support in detecting the

financial issues and making effective plans to resolve these problems.

TASK 1

Understanding of management accounting systems

Management accounting is an information system connected with method of collecting

financial and non-financial data in order to produce inner reports of different aspects. The main

role of MA is that based on internal documents, corporate managers are able to take appropriate

action for corporate success in the appropriate time to attract more and more stakeholders. It also

help in making accurate planning, controlling and decision making which support in proper

utilisation of resources and employees. Manager properly plans about the activities and make

them profitable in order to increase the overall productivity of company. They usually makes

effective decision and tries to control excess usage of available resources, funds to increase

overall profit margin (Alawattage, Wickramasinghe and Uddin, 2017). There are number of

essential MA system that play a crucial role in making company productive and profitable. Some

of these are discussed below:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

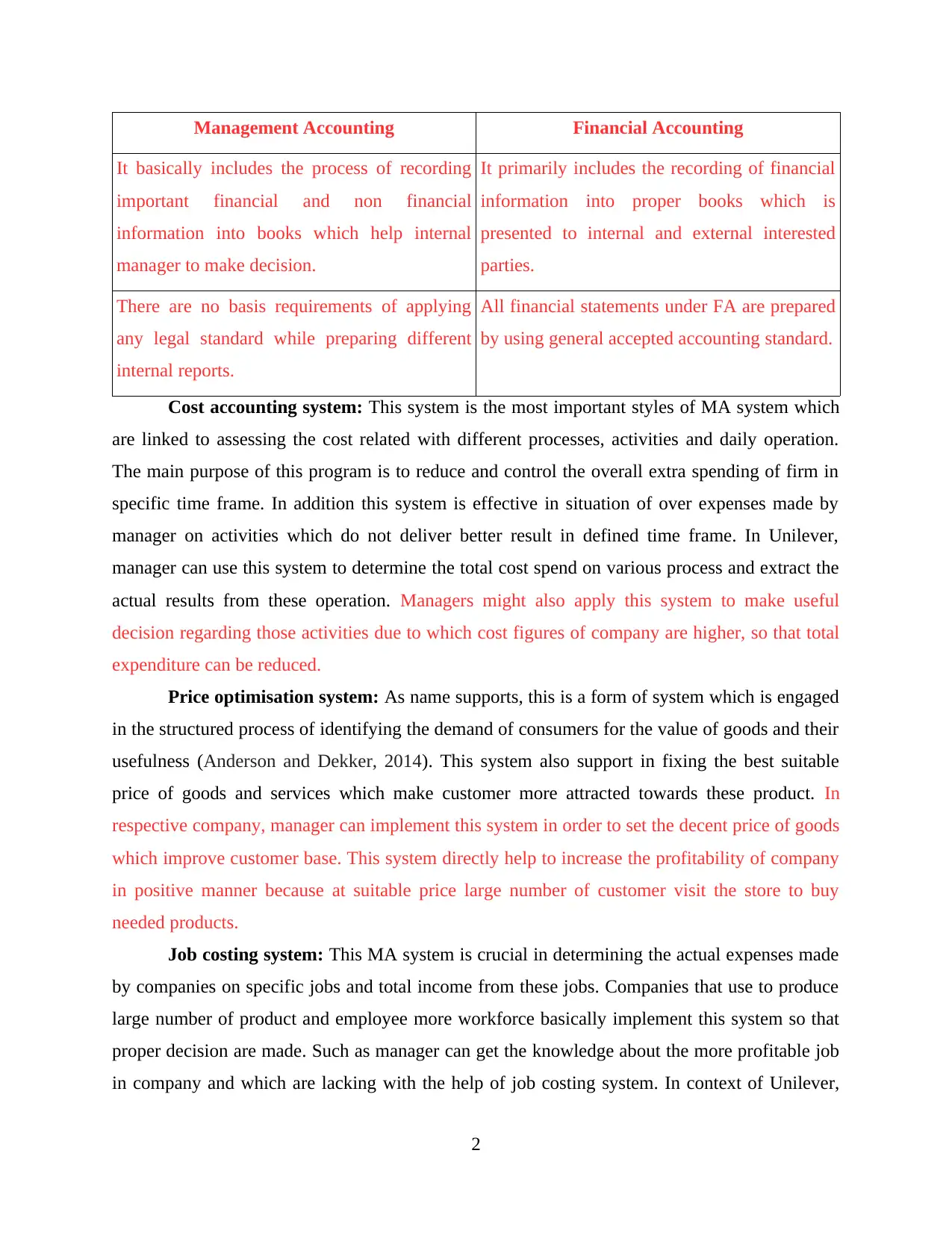

Management Accounting Financial Accounting

It basically includes the process of recording

important financial and non financial

information into books which help internal

manager to make decision.

It primarily includes the recording of financial

information into proper books which is

presented to internal and external interested

parties.

There are no basis requirements of applying

any legal standard while preparing different

internal reports.

All financial statements under FA are prepared

by using general accepted accounting standard.

Cost accounting system: This system is the most important styles of MA system which

are linked to assessing the cost related with different processes, activities and daily operation.

The main purpose of this program is to reduce and control the overall extra spending of firm in

specific time frame. In addition this system is effective in situation of over expenses made by

manager on activities which do not deliver better result in defined time frame. In Unilever,

manager can use this system to determine the total cost spend on various process and extract the

actual results from these operation. Managers might also apply this system to make useful

decision regarding those activities due to which cost figures of company are higher, so that total

expenditure can be reduced.

Price optimisation system: As name supports, this is a form of system which is engaged

in the structured process of identifying the demand of consumers for the value of goods and their

usefulness (Anderson and Dekker, 2014). This system also support in fixing the best suitable

price of goods and services which make customer more attracted towards these product. In

respective company, manager can implement this system in order to set the decent price of goods

which improve customer base. This system directly help to increase the profitability of company

in positive manner because at suitable price large number of customer visit the store to buy

needed products.

Job costing system: This MA system is crucial in determining the actual expenses made

by companies on specific jobs and total income from these jobs. Companies that use to produce

large number of product and employee more workforce basically implement this system so that

proper decision are made. Such as manager can get the knowledge about the more profitable job

in company and which are lacking with the help of job costing system. In context of Unilever,

2

It basically includes the process of recording

important financial and non financial

information into books which help internal

manager to make decision.

It primarily includes the recording of financial

information into proper books which is

presented to internal and external interested

parties.

There are no basis requirements of applying

any legal standard while preparing different

internal reports.

All financial statements under FA are prepared

by using general accepted accounting standard.

Cost accounting system: This system is the most important styles of MA system which

are linked to assessing the cost related with different processes, activities and daily operation.

The main purpose of this program is to reduce and control the overall extra spending of firm in

specific time frame. In addition this system is effective in situation of over expenses made by

manager on activities which do not deliver better result in defined time frame. In Unilever,

manager can use this system to determine the total cost spend on various process and extract the

actual results from these operation. Managers might also apply this system to make useful

decision regarding those activities due to which cost figures of company are higher, so that total

expenditure can be reduced.

Price optimisation system: As name supports, this is a form of system which is engaged

in the structured process of identifying the demand of consumers for the value of goods and their

usefulness (Anderson and Dekker, 2014). This system also support in fixing the best suitable

price of goods and services which make customer more attracted towards these product. In

respective company, manager can implement this system in order to set the decent price of goods

which improve customer base. This system directly help to increase the profitability of company

in positive manner because at suitable price large number of customer visit the store to buy

needed products.

Job costing system: This MA system is crucial in determining the actual expenses made

by companies on specific jobs and total income from these jobs. Companies that use to produce

large number of product and employee more workforce basically implement this system so that

proper decision are made. Such as manager can get the knowledge about the more profitable job

in company and which are lacking with the help of job costing system. In context of Unilever,

2

manage can apply this system to ascertain the total amount spend on different position in

production department and other operations. Thus this support in making decision regarding the

removal of jobs position which are not contributing in gaining the desired profit in the

meaningful time period.

Inventory management system: This is known as the combination of two practices such

as observing as well as the maintaining the storage house within company. Storage stuff can in

three form such as raw material, finished items and goods in production process. This is essential

in companies through production departments to develop effective manufacturing-related

decisions. In Unilever, this system can be useful in maintaining the total quantity of inventory

required to maintain the regular production of useful product that are more in demand. This can

also improve the supply chain of company in order to get the desired profitability in appropriate

time period. Such as FIFO system, allows company to use resources which comes first and sell

those product which arrived first within a specific period of time. On the other side LIFO, is used

to deliver goods first which arrive at last to the company.

Different methods used in management accounting reporting

In businesses, manager use to prepare number of valuable internal management

accounting reports so that overall performance can be analysed (Richardson, 2015). MA reports

are standard accounts provided by auditors to provide details on complex financial and non

monetary components. Several forms of documents are available like:

Budget report: This report is mainly related with preserving the detail information

related with estimated revenue and expenses within an appropriate time period. Budget reports

are meaningful for company in making comparison of actual and projected figures so that main

reason can be identified. It also support manager in making descriptive steps so that activities can

be managed and performed in desired manner to attain the aspected goals. Manager of Unilever

prepare budgets reports in every department so that actual expenses over these activities can be

predicted. This also support in estimating the total income generated through different operation

in company so that defined outcome can be gained.

Performance report: It is consider to be one of the most crucial report for company, as

it help in analysing the total performance of various business operation and total workforce

(Schaltegger, Burritt and Petersen, 2017). Manager can easily record the performance of worker

and make proper analyse to ascertain weather they are doing job as per company requirement or

3

production department and other operations. Thus this support in making decision regarding the

removal of jobs position which are not contributing in gaining the desired profit in the

meaningful time period.

Inventory management system: This is known as the combination of two practices such

as observing as well as the maintaining the storage house within company. Storage stuff can in

three form such as raw material, finished items and goods in production process. This is essential

in companies through production departments to develop effective manufacturing-related

decisions. In Unilever, this system can be useful in maintaining the total quantity of inventory

required to maintain the regular production of useful product that are more in demand. This can

also improve the supply chain of company in order to get the desired profitability in appropriate

time period. Such as FIFO system, allows company to use resources which comes first and sell

those product which arrived first within a specific period of time. On the other side LIFO, is used

to deliver goods first which arrive at last to the company.

Different methods used in management accounting reporting

In businesses, manager use to prepare number of valuable internal management

accounting reports so that overall performance can be analysed (Richardson, 2015). MA reports

are standard accounts provided by auditors to provide details on complex financial and non

monetary components. Several forms of documents are available like:

Budget report: This report is mainly related with preserving the detail information

related with estimated revenue and expenses within an appropriate time period. Budget reports

are meaningful for company in making comparison of actual and projected figures so that main

reason can be identified. It also support manager in making descriptive steps so that activities can

be managed and performed in desired manner to attain the aspected goals. Manager of Unilever

prepare budgets reports in every department so that actual expenses over these activities can be

predicted. This also support in estimating the total income generated through different operation

in company so that defined outcome can be gained.

Performance report: It is consider to be one of the most crucial report for company, as

it help in analysing the total performance of various business operation and total workforce

(Schaltegger, Burritt and Petersen, 2017). Manager can easily record the performance of worker

and make proper analyse to ascertain weather they are doing job as per company requirement or

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

not. With the support of this report manager of Unilever can record the overall performance of

total production process and number of worker working on these operation. In case of any

variance among expected and actual performance proper solution are can be made to improve the

entire performance of company.

Cost report: The actual use of cost report within an organisation is to record the total

cost being spend on several operating activities to acknowledge the total expenditure in specific

time period. Manager use to focus on every sudden variation arising the cost figures with the

support of this report and make better plans to reduce the cost. In respective company manager

can use this report to record the overall expenses made on various operation and entire

workforce. The detail information about cost expense support to make better effective steps in

order to decrease

Benefits of various kinds of systems

System Importance

Cost accounting system This is beneficial for businesses to effectively stop undesirable

operational expenses. In above mention company, managers can

use for the purpose of measuring the affectivity of every financial

aspect. By using important information through the accounting

system it enables them manage unnecessary expense burdens.

Stock management system It really is valuable for firms in controlling the buying, trading and

production operations of products. Like with the above-mentioned

company, the production department uses particular system to

optimize use the collected components in ware houses to increase

productivity (Seal and Mattimoe, 2014).

Job costing system It is desirable system for company because as it help in measuring

the expense input individual jobs. Manager gathers data about total

cost of work required and calculates this on the premise of each

unit's costs.

Price optimisation system The cost of goods and services at such an adequate level is

essential for firm to increase profit margin. Based on data obtained

from secondary research on customer requirements, manager in

4

total production process and number of worker working on these operation. In case of any

variance among expected and actual performance proper solution are can be made to improve the

entire performance of company.

Cost report: The actual use of cost report within an organisation is to record the total

cost being spend on several operating activities to acknowledge the total expenditure in specific

time period. Manager use to focus on every sudden variation arising the cost figures with the

support of this report and make better plans to reduce the cost. In respective company manager

can use this report to record the overall expenses made on various operation and entire

workforce. The detail information about cost expense support to make better effective steps in

order to decrease

Benefits of various kinds of systems

System Importance

Cost accounting system This is beneficial for businesses to effectively stop undesirable

operational expenses. In above mention company, managers can

use for the purpose of measuring the affectivity of every financial

aspect. By using important information through the accounting

system it enables them manage unnecessary expense burdens.

Stock management system It really is valuable for firms in controlling the buying, trading and

production operations of products. Like with the above-mentioned

company, the production department uses particular system to

optimize use the collected components in ware houses to increase

productivity (Seal and Mattimoe, 2014).

Job costing system It is desirable system for company because as it help in measuring

the expense input individual jobs. Manager gathers data about total

cost of work required and calculates this on the premise of each

unit's costs.

Price optimisation system The cost of goods and services at such an adequate level is

essential for firm to increase profit margin. Based on data obtained

from secondary research on customer requirements, manager in

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Unilever can regulate the cost of manufactured products. This will

directly increase the total sales for company and help in making

stronger brand image.

Critically evaluating of MA systems and reporting integrated within company

In present business era, management accounting system and reports play an important

role in maintaining and executing services according to the requirement. Different system and

reporting methods are beneficial in reaching the pre determined outcome as these are relevant to

one another. Such as cost management system in supportive in distribution of total cost involved

in various operation and process of company. On the other side, with the support of cost

accounting report manager of Unilever use to record the total cost used on various operation and

employees. This help in determining the overall expenditure and total revenue generation from

these activities in order to raise the total profit margin in specific year.

TASK 2

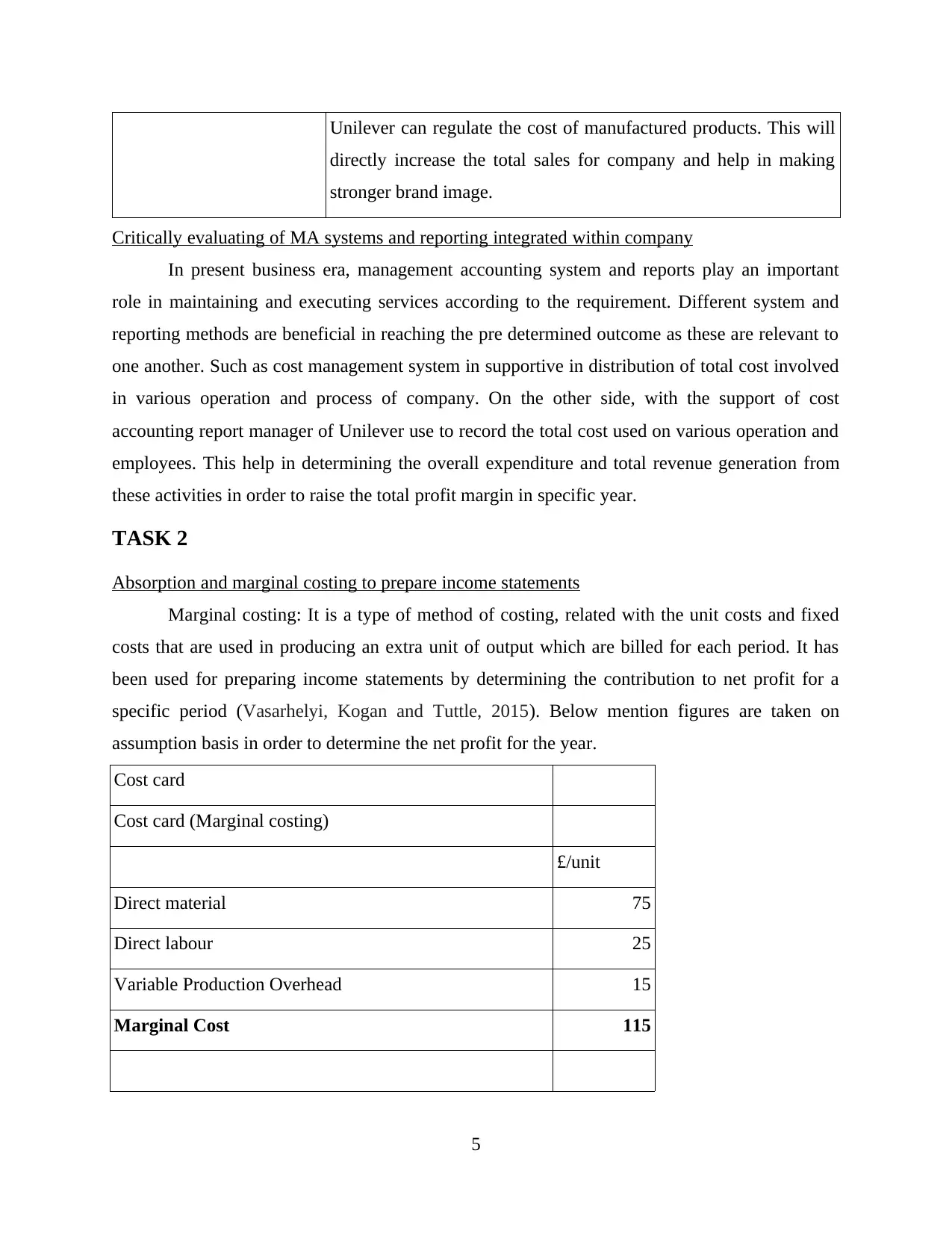

Absorption and marginal costing to prepare income statements

Marginal costing: It is a type of method of costing, related with the unit costs and fixed

costs that are used in producing an extra unit of output which are billed for each period. It has

been used for preparing income statements by determining the contribution to net profit for a

specific period (Vasarhelyi, Kogan and Tuttle, 2015). Below mention figures are taken on

assumption basis in order to determine the net profit for the year.

Cost card

Cost card (Marginal costing)

£/unit

Direct material 75

Direct labour 25

Variable Production Overhead 15

Marginal Cost 115

5

directly increase the total sales for company and help in making

stronger brand image.

Critically evaluating of MA systems and reporting integrated within company

In present business era, management accounting system and reports play an important

role in maintaining and executing services according to the requirement. Different system and

reporting methods are beneficial in reaching the pre determined outcome as these are relevant to

one another. Such as cost management system in supportive in distribution of total cost involved

in various operation and process of company. On the other side, with the support of cost

accounting report manager of Unilever use to record the total cost used on various operation and

employees. This help in determining the overall expenditure and total revenue generation from

these activities in order to raise the total profit margin in specific year.

TASK 2

Absorption and marginal costing to prepare income statements

Marginal costing: It is a type of method of costing, related with the unit costs and fixed

costs that are used in producing an extra unit of output which are billed for each period. It has

been used for preparing income statements by determining the contribution to net profit for a

specific period (Vasarhelyi, Kogan and Tuttle, 2015). Below mention figures are taken on

assumption basis in order to determine the net profit for the year.

Cost card

Cost card (Marginal costing)

£/unit

Direct material 75

Direct labour 25

Variable Production Overhead 15

Marginal Cost 115

5

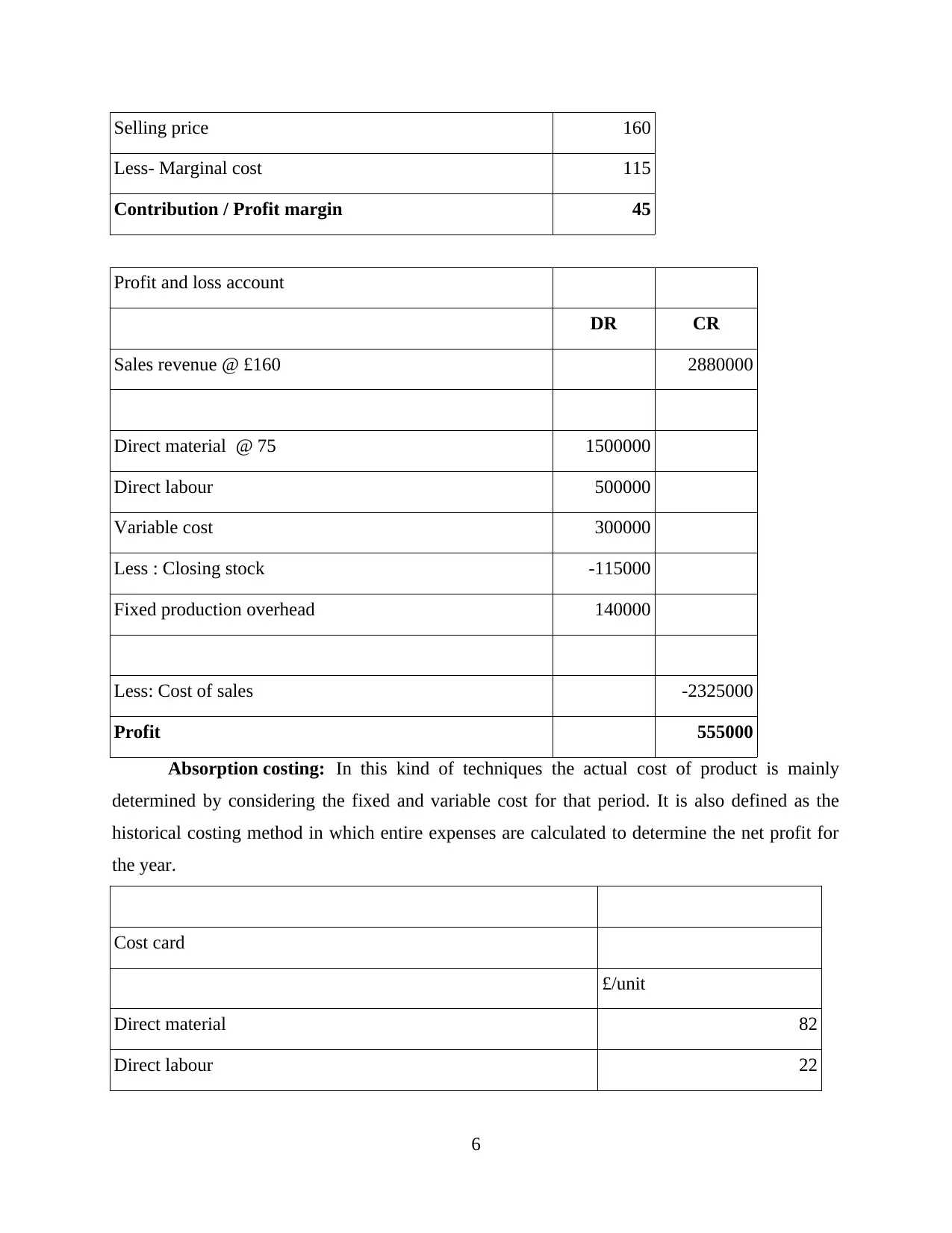

Selling price 160

Less- Marginal cost 115

Contribution / Profit margin 45

Profit and loss account

DR CR

Sales revenue @ £160 2880000

Direct material @ 75 1500000

Direct labour 500000

Variable cost 300000

Less : Closing stock -115000

Fixed production overhead 140000

Less: Cost of sales -2325000

Profit 555000

Absorption costing: In this kind of techniques the actual cost of product is mainly

determined by considering the fixed and variable cost for that period. It is also defined as the

historical costing method in which entire expenses are calculated to determine the net profit for

the year.

Cost card

£/unit

Direct material 82

Direct labour 22

6

Less- Marginal cost 115

Contribution / Profit margin 45

Profit and loss account

DR CR

Sales revenue @ £160 2880000

Direct material @ 75 1500000

Direct labour 500000

Variable cost 300000

Less : Closing stock -115000

Fixed production overhead 140000

Less: Cost of sales -2325000

Profit 555000

Absorption costing: In this kind of techniques the actual cost of product is mainly

determined by considering the fixed and variable cost for that period. It is also defined as the

historical costing method in which entire expenses are calculated to determine the net profit for

the year.

Cost card

£/unit

Direct material 82

Direct labour 22

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

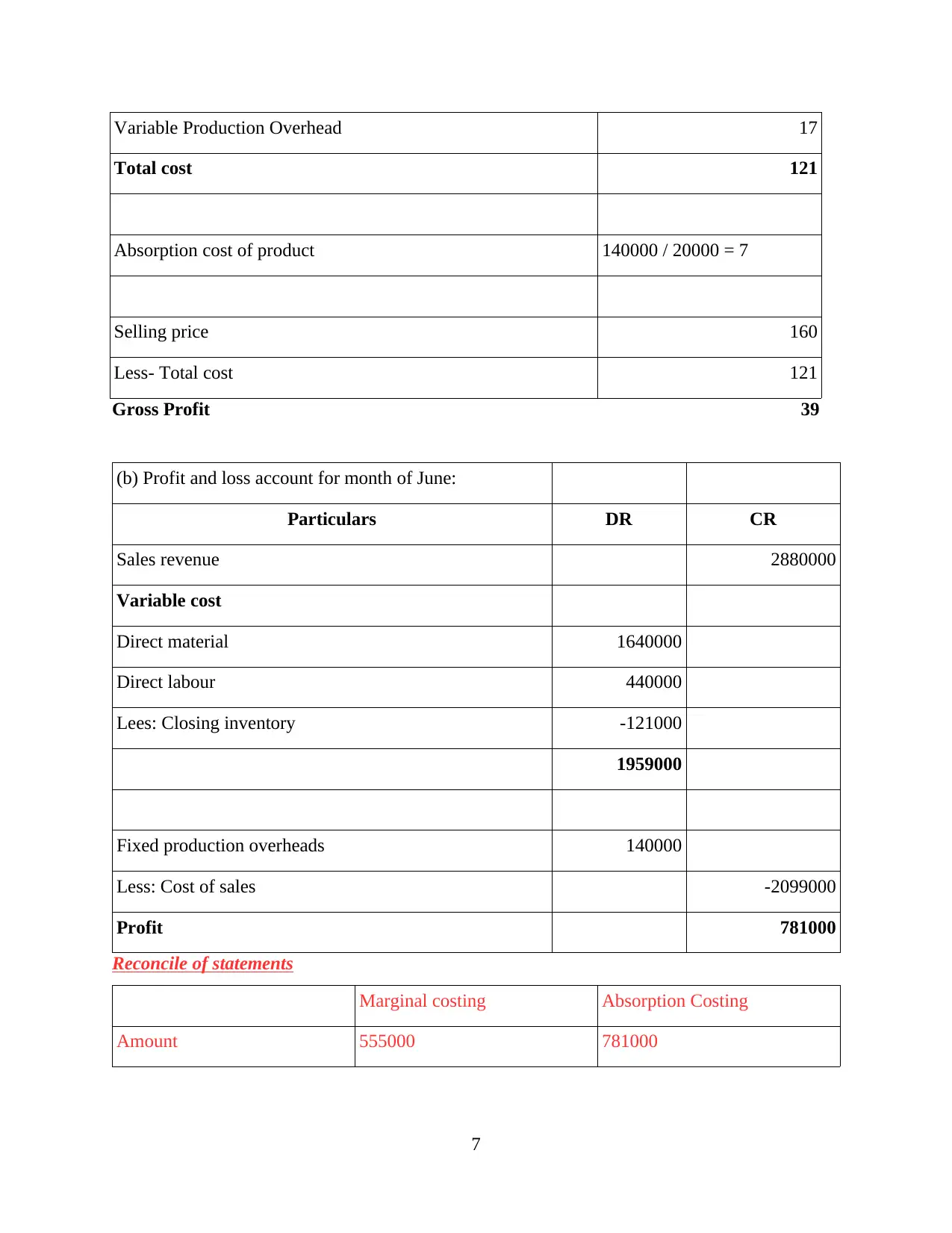

Variable Production Overhead 17

Total cost 121

Absorption cost of product 140000 / 20000 = 7

Selling price 160

Less- Total cost 121

Gross Profit 39

(b) Profit and loss account for month of June:

Particulars DR CR

Sales revenue 2880000

Variable cost

Direct material 1640000

Direct labour 440000

Lees: Closing inventory -121000

1959000

Fixed production overheads 140000

Less: Cost of sales -2099000

Profit 781000

Reconcile of statements

Marginal costing Absorption Costing

Amount 555000 781000

7

Total cost 121

Absorption cost of product 140000 / 20000 = 7

Selling price 160

Less- Total cost 121

Gross Profit 39

(b) Profit and loss account for month of June:

Particulars DR CR

Sales revenue 2880000

Variable cost

Direct material 1640000

Direct labour 440000

Lees: Closing inventory -121000

1959000

Fixed production overheads 140000

Less: Cost of sales -2099000

Profit 781000

Reconcile of statements

Marginal costing Absorption Costing

Amount 555000 781000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

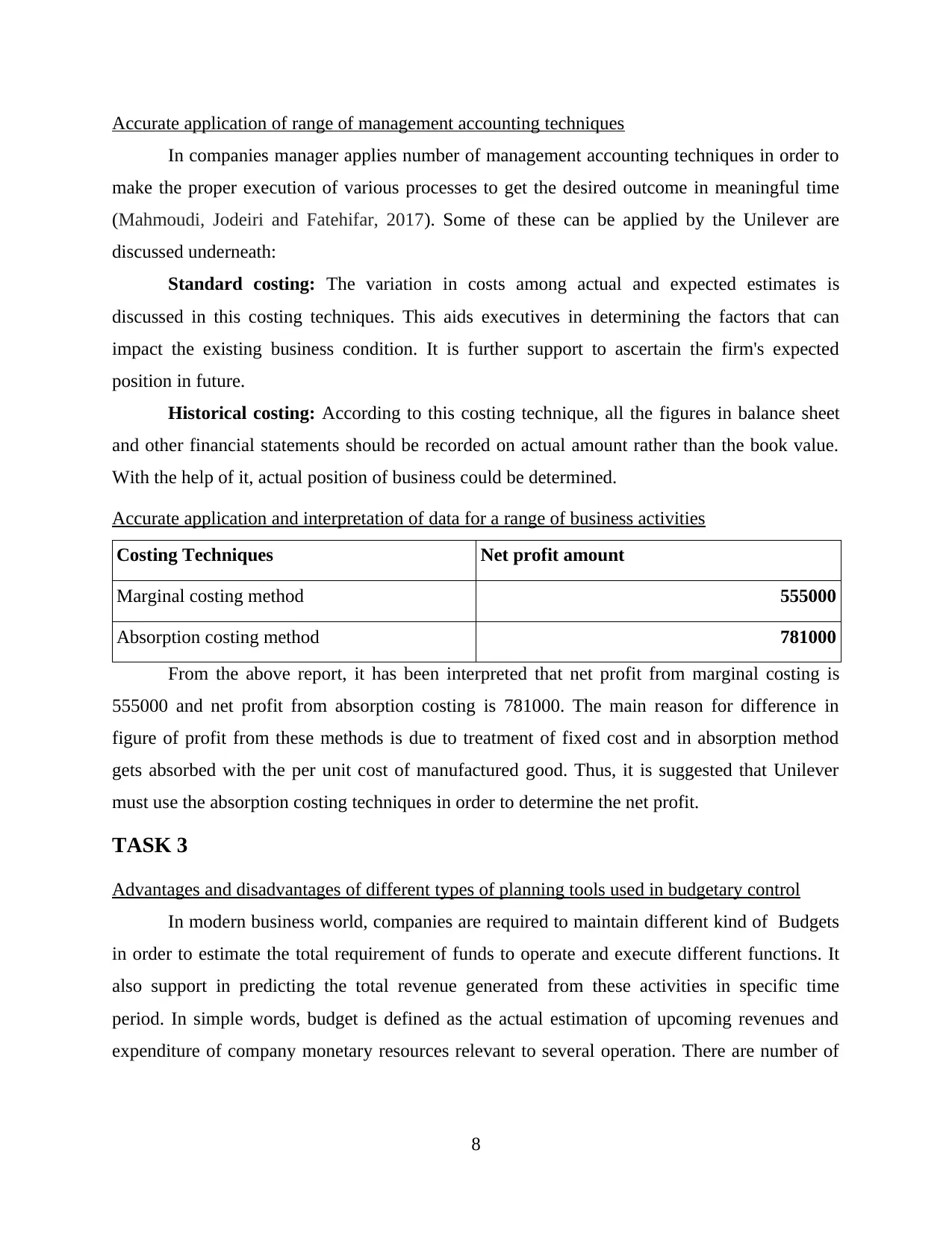

Accurate application of range of management accounting techniques

In companies manager applies number of management accounting techniques in order to

make the proper execution of various processes to get the desired outcome in meaningful time

(Mahmoudi, Jodeiri and Fatehifar, 2017). Some of these can be applied by the Unilever are

discussed underneath:

Standard costing: The variation in costs among actual and expected estimates is

discussed in this costing techniques. This aids executives in determining the factors that can

impact the existing business condition. It is further support to ascertain the firm's expected

position in future.

Historical costing: According to this costing technique, all the figures in balance sheet

and other financial statements should be recorded on actual amount rather than the book value.

With the help of it, actual position of business could be determined.

Accurate application and interpretation of data for a range of business activities

Costing Techniques Net profit amount

Marginal costing method 555000

Absorption costing method 781000

From the above report, it has been interpreted that net profit from marginal costing is

555000 and net profit from absorption costing is 781000. The main reason for difference in

figure of profit from these methods is due to treatment of fixed cost and in absorption method

gets absorbed with the per unit cost of manufactured good. Thus, it is suggested that Unilever

must use the absorption costing techniques in order to determine the net profit.

TASK 3

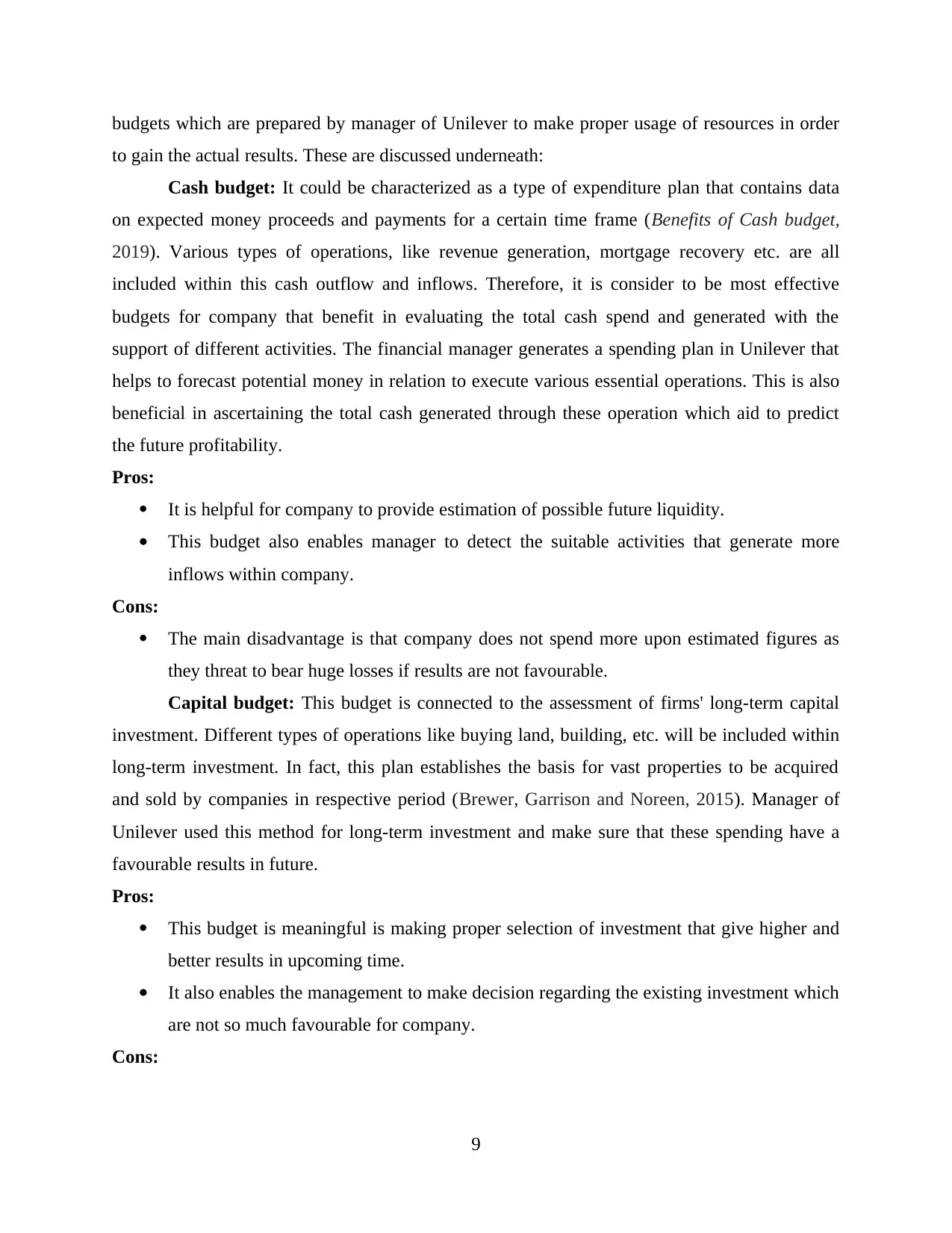

Advantages and disadvantages of different types of planning tools used in budgetary control

In modern business world, companies are required to maintain different kind of Budgets

in order to estimate the total requirement of funds to operate and execute different functions. It

also support in predicting the total revenue generated from these activities in specific time

period. In simple words, budget is defined as the actual estimation of upcoming revenues and

expenditure of company monetary resources relevant to several operation. There are number of

8

In companies manager applies number of management accounting techniques in order to

make the proper execution of various processes to get the desired outcome in meaningful time

(Mahmoudi, Jodeiri and Fatehifar, 2017). Some of these can be applied by the Unilever are

discussed underneath:

Standard costing: The variation in costs among actual and expected estimates is

discussed in this costing techniques. This aids executives in determining the factors that can

impact the existing business condition. It is further support to ascertain the firm's expected

position in future.

Historical costing: According to this costing technique, all the figures in balance sheet

and other financial statements should be recorded on actual amount rather than the book value.

With the help of it, actual position of business could be determined.

Accurate application and interpretation of data for a range of business activities

Costing Techniques Net profit amount

Marginal costing method 555000

Absorption costing method 781000

From the above report, it has been interpreted that net profit from marginal costing is

555000 and net profit from absorption costing is 781000. The main reason for difference in

figure of profit from these methods is due to treatment of fixed cost and in absorption method

gets absorbed with the per unit cost of manufactured good. Thus, it is suggested that Unilever

must use the absorption costing techniques in order to determine the net profit.

TASK 3

Advantages and disadvantages of different types of planning tools used in budgetary control

In modern business world, companies are required to maintain different kind of Budgets

in order to estimate the total requirement of funds to operate and execute different functions. It

also support in predicting the total revenue generated from these activities in specific time

period. In simple words, budget is defined as the actual estimation of upcoming revenues and

expenditure of company monetary resources relevant to several operation. There are number of

8

budgets which are prepared by manager of Unilever to make proper usage of resources in order

to gain the actual results. These are discussed underneath:

Cash budget: It could be characterized as a type of expenditure plan that contains data

on expected money proceeds and payments for a certain time frame (Benefits of Cash budget,

2019). Various types of operations, like revenue generation, mortgage recovery etc. are all

included within this cash outflow and inflows. Therefore, it is consider to be most effective

budgets for company that benefit in evaluating the total cash spend and generated with the

support of different activities. The financial manager generates a spending plan in Unilever that

helps to forecast potential money in relation to execute various essential operations. This is also

beneficial in ascertaining the total cash generated through these operation which aid to predict

the future profitability.

Pros:

It is helpful for company to provide estimation of possible future liquidity.

This budget also enables manager to detect the suitable activities that generate more

inflows within company.

Cons:

The main disadvantage is that company does not spend more upon estimated figures as

they threat to bear huge losses if results are not favourable.

Capital budget: This budget is connected to the assessment of firms' long-term capital

investment. Different types of operations like buying land, building, etc. will be included within

long-term investment. In fact, this plan establishes the basis for vast properties to be acquired

and sold by companies in respective period (Brewer, Garrison and Noreen, 2015). Manager of

Unilever used this method for long-term investment and make sure that these spending have a

favourable results in future.

Pros:

This budget is meaningful is making proper selection of investment that give higher and

better results in upcoming time.

It also enables the management to make decision regarding the existing investment which

are not so much favourable for company.

Cons:

9

to gain the actual results. These are discussed underneath:

Cash budget: It could be characterized as a type of expenditure plan that contains data

on expected money proceeds and payments for a certain time frame (Benefits of Cash budget,

2019). Various types of operations, like revenue generation, mortgage recovery etc. are all

included within this cash outflow and inflows. Therefore, it is consider to be most effective

budgets for company that benefit in evaluating the total cash spend and generated with the

support of different activities. The financial manager generates a spending plan in Unilever that

helps to forecast potential money in relation to execute various essential operations. This is also

beneficial in ascertaining the total cash generated through these operation which aid to predict

the future profitability.

Pros:

It is helpful for company to provide estimation of possible future liquidity.

This budget also enables manager to detect the suitable activities that generate more

inflows within company.

Cons:

The main disadvantage is that company does not spend more upon estimated figures as

they threat to bear huge losses if results are not favourable.

Capital budget: This budget is connected to the assessment of firms' long-term capital

investment. Different types of operations like buying land, building, etc. will be included within

long-term investment. In fact, this plan establishes the basis for vast properties to be acquired

and sold by companies in respective period (Brewer, Garrison and Noreen, 2015). Manager of

Unilever used this method for long-term investment and make sure that these spending have a

favourable results in future.

Pros:

This budget is meaningful is making proper selection of investment that give higher and

better results in upcoming time.

It also enables the management to make decision regarding the existing investment which

are not so much favourable for company.

Cons:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.