Management Accounting Systems and Techniques at Creams Ltd.

VerifiedAdded on 2023/01/11

|18

|4349

|48

Report

AI Summary

This report provides a detailed analysis of management accounting systems and techniques applicable to Creams Ltd., a company specializing in ice-creams, waffles, and doughnuts. It explains various management accounting systems such as cost accounting, inventory management, job costing, and price optimization, highlighting their essential requirements and benefits. The report also discusses management accounting reporting methods, including budget reports, accounts receivables aging reports, cost managerial accounting reports, and performance reports, emphasizing their role in facilitating analysis and interpretation of organizational performance. Furthermore, it delves into costing techniques like marginal costing and absorption costing, outlining their advantages and disadvantages in the context of Creams Ltd. The report concludes by comparing organizations in their adoption of management accounting systems to solve financial problems, emphasizing the importance of effective management accounting in achieving organizational goals and objectives. Desklib offers this report, along with a wealth of study resources, to aid students in their academic pursuits.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1: Explanation of management accounting and its systems..................................................................3

P2: Methods for Management accounting reporting..............................................................................4

TASK 2..........................................................................................................................................................6

P3: Calculation of costs using appropriate techniques............................................................................6

TASK 3........................................................................................................................................................13

P4: Advantages and disadvantages of different types of planning tools...............................................13

TASK 4........................................................................................................................................................14

P5: Comparison of organizations in adoption of management accounting systems to solve financial

problems...............................................................................................................................................14

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1: Explanation of management accounting and its systems..................................................................3

P2: Methods for Management accounting reporting..............................................................................4

TASK 2..........................................................................................................................................................6

P3: Calculation of costs using appropriate techniques............................................................................6

TASK 3........................................................................................................................................................13

P4: Advantages and disadvantages of different types of planning tools...............................................13

TASK 4........................................................................................................................................................14

P5: Comparison of organizations in adoption of management accounting systems to solve financial

problems...............................................................................................................................................14

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

INTRODUCTION

Management accounting refers to the provision of financial data and advice to a company

which helps its managers in taking the decisions which are for its benefit (Armitage, Webb and

Glynn, 2016). It helps the managers to better inform themselves before they take decisions on

key matters concerning the company. Thus, overall its purpose is to aid them in decision-making

process. This helps in raising the overall efficiency, effectiveness and productivity in the

organizational context. Thus if the managers of the enterprise use it effectively then it will result

in achievement of short-term and long-term goals and objectives of the organization and will also

help in raising the level of profits. This project is based on Creams Ltd., which specializes in

selling of ice-creams, waffles and doughnuts. In this report, detailed analysis will be made on

types of systems used for management accounting, application of techniques of management

accounting to calculate the costs, use of planning tools. Additionally, the ways in which different

firms make use of management accounting systems will be discussed as a part of this report.

TASK 1

P1: Explanation of management accounting and its systems

Management accounting refers to using financial data and information in such a manner

so that it helps in taking of various decisions pertaining to the organization (Bromwich and

Scapens, 2016). Managers of Creams Ltd. can use this data in order to help them grow the

enterprise and to get ahead of the competitors through effective decision-making.

The various systems in management accounting are explained in the context of Creams

Ltd. as follows-

Cost accounting system- Cost accounting system is very helpful in order to find out and

analyze the costs pertaining to an organization. It can be used the managers of Creams Ltd. to

find out their various types of costs and segregating them according to requirements. Also, this

system helps in analyzing the overheads. Management can make use of this system to analyze

the costs and to find out the excessive costs incurring in the organization. This helps in reducing

these extra costs and maximizing the level of profits.

Essential requirements-

A good cost accounting system helps in analysis and interpretation of costs.

A good cost accounting system identified the extra costs in various departments of the

organization and helps in reducing them so that the profits can be maximized.

Inventory management system- Inventory management system helps a lot in proper and

effective management of the inventory level in the organization. Managers of Creams

Ltd. can use it so that they can manage the stock levels effectively and efficiently. It also

Management accounting refers to the provision of financial data and advice to a company

which helps its managers in taking the decisions which are for its benefit (Armitage, Webb and

Glynn, 2016). It helps the managers to better inform themselves before they take decisions on

key matters concerning the company. Thus, overall its purpose is to aid them in decision-making

process. This helps in raising the overall efficiency, effectiveness and productivity in the

organizational context. Thus if the managers of the enterprise use it effectively then it will result

in achievement of short-term and long-term goals and objectives of the organization and will also

help in raising the level of profits. This project is based on Creams Ltd., which specializes in

selling of ice-creams, waffles and doughnuts. In this report, detailed analysis will be made on

types of systems used for management accounting, application of techniques of management

accounting to calculate the costs, use of planning tools. Additionally, the ways in which different

firms make use of management accounting systems will be discussed as a part of this report.

TASK 1

P1: Explanation of management accounting and its systems

Management accounting refers to using financial data and information in such a manner

so that it helps in taking of various decisions pertaining to the organization (Bromwich and

Scapens, 2016). Managers of Creams Ltd. can use this data in order to help them grow the

enterprise and to get ahead of the competitors through effective decision-making.

The various systems in management accounting are explained in the context of Creams

Ltd. as follows-

Cost accounting system- Cost accounting system is very helpful in order to find out and

analyze the costs pertaining to an organization. It can be used the managers of Creams Ltd. to

find out their various types of costs and segregating them according to requirements. Also, this

system helps in analyzing the overheads. Management can make use of this system to analyze

the costs and to find out the excessive costs incurring in the organization. This helps in reducing

these extra costs and maximizing the level of profits.

Essential requirements-

A good cost accounting system helps in analysis and interpretation of costs.

A good cost accounting system identified the extra costs in various departments of the

organization and helps in reducing them so that the profits can be maximized.

Inventory management system- Inventory management system helps a lot in proper and

effective management of the inventory level in the organization. Managers of Creams

Ltd. can use it so that they can manage the stock levels effectively and efficiently. It also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

identifies the problems pertaining to the inventory in the organization and takes the

essential steps to resolve them. Thus overall it is very much helpful for taking decisions

related to the inventory.

Essential requirements-

An effective inventory management system must be able to identify the problems and

issues lying with the management of inventory level in the organization.

An effective inventory management system should be able to properly manage the stock

level in the organization.

Job costing system- Job costing system helps in proper management of orders and other

jobs undertaken in the organization (Bui and De Villiers, 2017). It is very useful for those

enterprises which are indulged in the process of manufacturing. The managers of Creams

Ltd. can make use of this system to properly track and manage their orders. This will help

them in completion of orders on time. Also the costs associated with the jobs in the

organization can be calculated using it and can be segregated across departments. This

helps in finding out the excessive costs incurred while completing the orders which helps

in reducing them and maximizing the level of profits.

Essential requirements-

An effective job costing system should help in properly maintaining the track of orders

received and given in the organization.

An effective job costing system should help the managers in reducing the costs associated

with the completion of orders by identifying unnecessary costs associated with the orders.

Price optimization system- Price optimization system helps in choosing a right price by

selecting a right pricing strategy according to the conditions prevalent in the market

(Christ, Burritt and Varsei, 2016). The managers of Creams Ltd. can make use of this

system in order to set a right price which helps them in raising profits and also getting

ahead of the competitors. It ascertains the problems related with the pricing strategy of

the organization and helps in resolving them so as to effectively raise the profits.

Essential requirements-

A good pricing optimization system should be able to find out the problems and issues

associated with the price set by the organization for its products.

A good price optimization system must be able to raise the level of profits and must help

the firm in getting ahead of the competition by helping management in framing an

effective strategy for the price.

P2: Methods for Management accounting reporting

Management accounting reports are prepared in order to facilitate the analysis and

interpretation of performance of various departments in the organization (Cooper, Ezzamel and

Qu, 2017). The explanation of these reports in the context of Creams Ltd. is as follows-

Budget report- A budget report is prepared with the help of budgets in the company

such as cash budget, operating budget, master budget etc. They are used to generate the overall

essential steps to resolve them. Thus overall it is very much helpful for taking decisions

related to the inventory.

Essential requirements-

An effective inventory management system must be able to identify the problems and

issues lying with the management of inventory level in the organization.

An effective inventory management system should be able to properly manage the stock

level in the organization.

Job costing system- Job costing system helps in proper management of orders and other

jobs undertaken in the organization (Bui and De Villiers, 2017). It is very useful for those

enterprises which are indulged in the process of manufacturing. The managers of Creams

Ltd. can make use of this system to properly track and manage their orders. This will help

them in completion of orders on time. Also the costs associated with the jobs in the

organization can be calculated using it and can be segregated across departments. This

helps in finding out the excessive costs incurred while completing the orders which helps

in reducing them and maximizing the level of profits.

Essential requirements-

An effective job costing system should help in properly maintaining the track of orders

received and given in the organization.

An effective job costing system should help the managers in reducing the costs associated

with the completion of orders by identifying unnecessary costs associated with the orders.

Price optimization system- Price optimization system helps in choosing a right price by

selecting a right pricing strategy according to the conditions prevalent in the market

(Christ, Burritt and Varsei, 2016). The managers of Creams Ltd. can make use of this

system in order to set a right price which helps them in raising profits and also getting

ahead of the competitors. It ascertains the problems related with the pricing strategy of

the organization and helps in resolving them so as to effectively raise the profits.

Essential requirements-

A good pricing optimization system should be able to find out the problems and issues

associated with the price set by the organization for its products.

A good price optimization system must be able to raise the level of profits and must help

the firm in getting ahead of the competition by helping management in framing an

effective strategy for the price.

P2: Methods for Management accounting reporting

Management accounting reports are prepared in order to facilitate the analysis and

interpretation of performance of various departments in the organization (Cooper, Ezzamel and

Qu, 2017). The explanation of these reports in the context of Creams Ltd. is as follows-

Budget report- A budget report is prepared with the help of budgets in the company

such as cash budget, operating budget, master budget etc. They are used to generate the overall

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance and to check whether it matches the standards or not. The managers of Creams Ltd.

can use it for identifying whether there is a surplus or a deficit arising from the operations of the

company. Also comparison can be done by the managers using these reports as the data and

information of current year can be compared with that of the previous year. Therefore errors and

mistakes can be easily detected and the necessary steps can be taken with immediate effect to

rectify the same. This can help the management in raising the overall efficiency, effectiveness

and productivity. Thus, if used effectively budget reports will certainly help the management in

taking the right decisions in the context of the organization to help it achieve its short-term and

long-term goals and objectives.

Accounts receivables aging report- Accounts receivables aging report is prepared to

classify the different debtors in the organization. The managers of Creams Ltd. can use this

report for making a list of their debtors and segregating them according to their payment due

date. This helps in keeping a track on the debtors. Also, the potential bad debts can be easily

identified and a provision can be made for the same. The aging receivables that have not paid

their dues since a long time can also be identified. Thus overall tracking of debtors is facilitated

with this report in the organization. This report also tells the management whether it needs to

make its credit policy stricter or not. Flow of cash and liquidity position can be identified easily

by preparing it and thus it is quite useful for all the enterprises. Management can take the right

decisions by using it.

Cost managerial accounting report- Cost managerial accounting report is prepared in

order to compute the cost of articles that have been manufactured (Hall, 2016). All the raw

material, overhead, labor and any other added costs are taken into the consideration. A summary

is offered on all of this information. The managers of Creams Ltd. can make use of this report.

They can use it to identify the costs being incurred in the organization and comparing it with the

previous years to identify variances. If variances are there then they can be quickly rectified by

the use of various types of techniques. Also these reports help a lot in optimum utilization of

limited resources available in the organization. Inventory wastage, hourly labor costs and

overhead costs are all a part of this report. They provide an exact understanding of expenses

essential for optimum utilization of resources among all the departments.

Performance report- Performance report is prepared in order to find out the

performance of a company as a whole and of the workers working in different departments at the

end of the term (Honggowati and et.al., 2017). After finding out the performance a thorough

analysis, interpretation and review is done so that key strategic decisions can be taken by the

managers. The managers of Creams Ltd. can use these reports to get deep insights into the

working pattern of the organization. If by the use of this report they find out that the company is

still not performing to its full capacity then the necessary steps can be taken for improvement of

performance. Thus this report helps the managers in raising the overall efficiency, effectiveness

and productivity level in the organization which helps in attainment of several short-term and

can use it for identifying whether there is a surplus or a deficit arising from the operations of the

company. Also comparison can be done by the managers using these reports as the data and

information of current year can be compared with that of the previous year. Therefore errors and

mistakes can be easily detected and the necessary steps can be taken with immediate effect to

rectify the same. This can help the management in raising the overall efficiency, effectiveness

and productivity. Thus, if used effectively budget reports will certainly help the management in

taking the right decisions in the context of the organization to help it achieve its short-term and

long-term goals and objectives.

Accounts receivables aging report- Accounts receivables aging report is prepared to

classify the different debtors in the organization. The managers of Creams Ltd. can use this

report for making a list of their debtors and segregating them according to their payment due

date. This helps in keeping a track on the debtors. Also, the potential bad debts can be easily

identified and a provision can be made for the same. The aging receivables that have not paid

their dues since a long time can also be identified. Thus overall tracking of debtors is facilitated

with this report in the organization. This report also tells the management whether it needs to

make its credit policy stricter or not. Flow of cash and liquidity position can be identified easily

by preparing it and thus it is quite useful for all the enterprises. Management can take the right

decisions by using it.

Cost managerial accounting report- Cost managerial accounting report is prepared in

order to compute the cost of articles that have been manufactured (Hall, 2016). All the raw

material, overhead, labor and any other added costs are taken into the consideration. A summary

is offered on all of this information. The managers of Creams Ltd. can make use of this report.

They can use it to identify the costs being incurred in the organization and comparing it with the

previous years to identify variances. If variances are there then they can be quickly rectified by

the use of various types of techniques. Also these reports help a lot in optimum utilization of

limited resources available in the organization. Inventory wastage, hourly labor costs and

overhead costs are all a part of this report. They provide an exact understanding of expenses

essential for optimum utilization of resources among all the departments.

Performance report- Performance report is prepared in order to find out the

performance of a company as a whole and of the workers working in different departments at the

end of the term (Honggowati and et.al., 2017). After finding out the performance a thorough

analysis, interpretation and review is done so that key strategic decisions can be taken by the

managers. The managers of Creams Ltd. can use these reports to get deep insights into the

working pattern of the organization. If by the use of this report they find out that the company is

still not performing to its full capacity then the necessary steps can be taken for improvement of

performance. Thus this report helps the managers in raising the overall efficiency, effectiveness

and productivity level in the organization which helps in attainment of several short-term and

long-term goals and objectives. Therefore the management has to make the best use of these

reports.

TASK 2

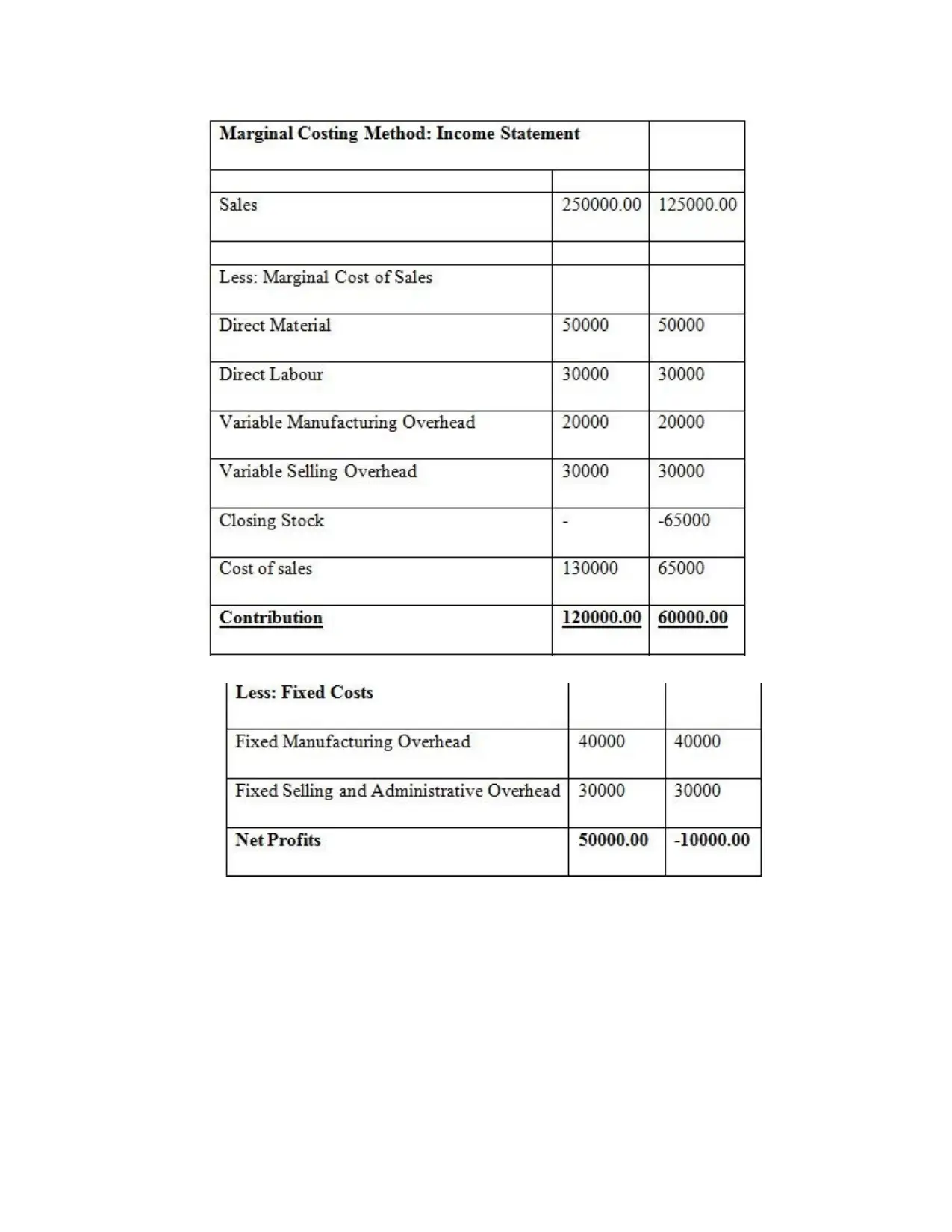

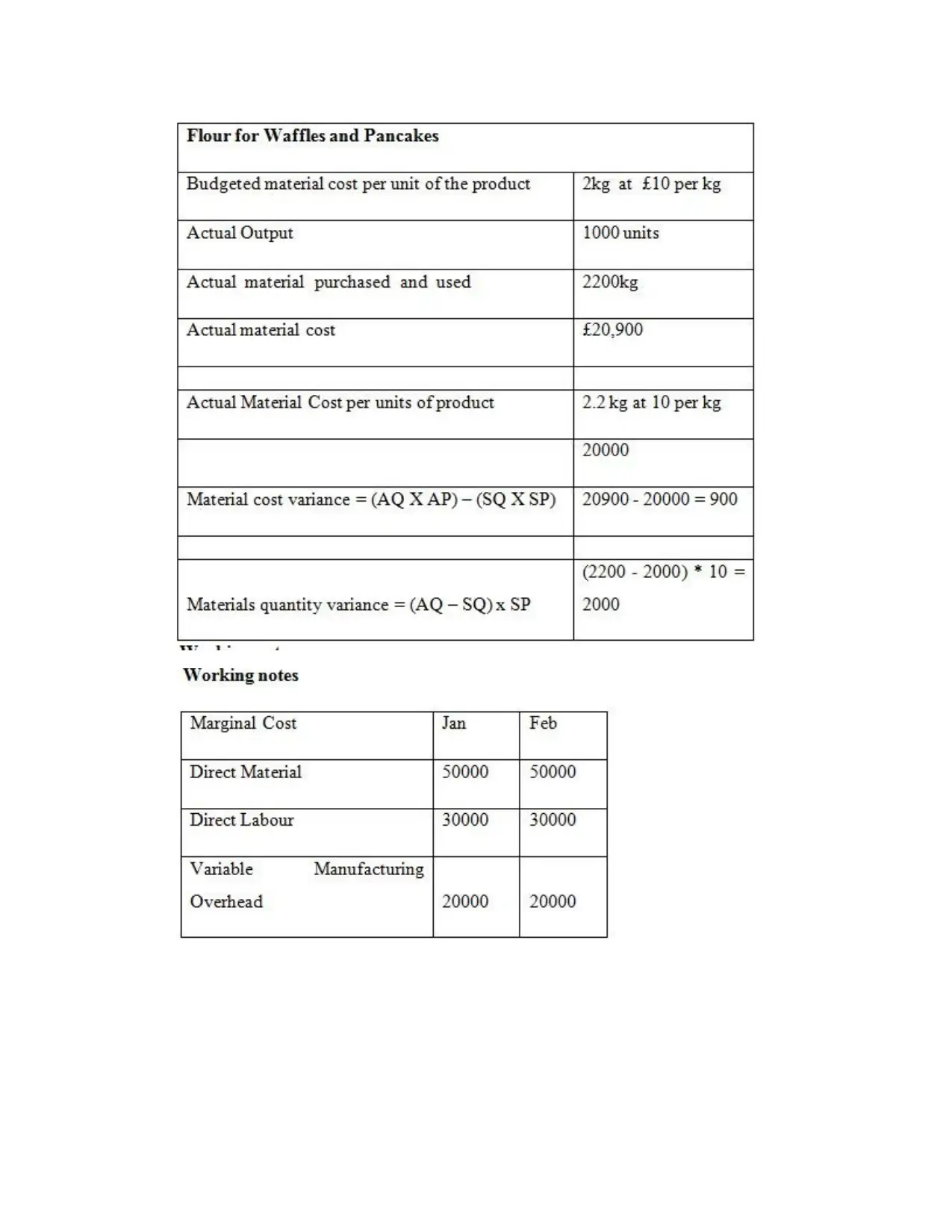

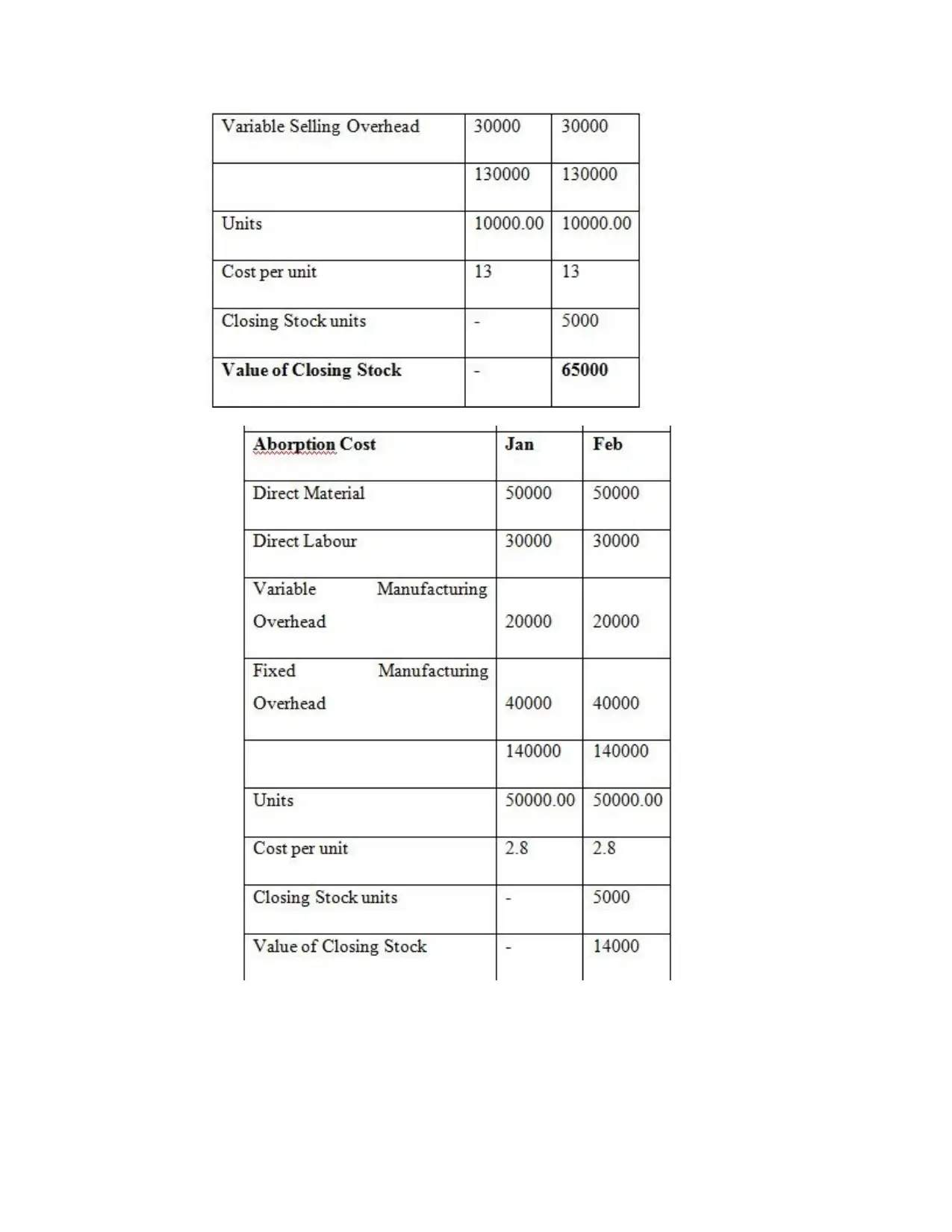

P3: Calculation of costs using appropriate techniques

Costs can be calculated by using several techniques (Hopper and Bui, 2016). The most

popular of these techniques are marginal costing and absorption costing. Explanation of these

techniques in the context of Creams Ltd. is as follows-

Marginal costing-

Marginal costing is a technique used in costing wherein variable costs are charged to the

units of cost and fixed costs are completely written off against the contribution (Horton and de

Araujo Wanderley, 2018). The managers of Creams Ltd. can make use of this technique as it will

help them in analyzing the break-even point.

Advantages-

Marginal costing is very helpful in production planning as it shows the amount of profit

at every level of output with the help of cost-volume relationship. Break-even chart can

be used for this purpose.

Marginal costing also helps in fixation of selling price of products and services of the

organization. Sometimes, different prices can be charged for the same article in different

markets for meeting varying degrees of competition. Thus fixation of selling price helps

in determining the profitability level of the enterprise. Any variance or deviation in the

profits can be easily identified. If a variance or deviation is found in profitability then

rectifying steps can be immediately taken by the management to correct them so that

operations and functioning of the enterprise is not affected at all. Therefore, it can be said

that this acts like an advantage in the context of the company.

Disadvantages-

Marginal costing technique is based on certain assumptions which may not always be

true in all the situations and circumstances in the company. Practically, they may change

and therefore different results can be obtained. This can affect the level of accuracy of

results obtained in the organization.

Marginal costing technique overcomes the problems of over and under-absorption of the

fixed overheads. However, the problems related with the absorption of variable

overheads still persist within the organization. Thus it again affects the accuracy of

calculations and can give wrong results, conclusions and judgments. Managers may take

wrong decisions if accuracy is affected.

Absorption costing-

reports.

TASK 2

P3: Calculation of costs using appropriate techniques

Costs can be calculated by using several techniques (Hopper and Bui, 2016). The most

popular of these techniques are marginal costing and absorption costing. Explanation of these

techniques in the context of Creams Ltd. is as follows-

Marginal costing-

Marginal costing is a technique used in costing wherein variable costs are charged to the

units of cost and fixed costs are completely written off against the contribution (Horton and de

Araujo Wanderley, 2018). The managers of Creams Ltd. can make use of this technique as it will

help them in analyzing the break-even point.

Advantages-

Marginal costing is very helpful in production planning as it shows the amount of profit

at every level of output with the help of cost-volume relationship. Break-even chart can

be used for this purpose.

Marginal costing also helps in fixation of selling price of products and services of the

organization. Sometimes, different prices can be charged for the same article in different

markets for meeting varying degrees of competition. Thus fixation of selling price helps

in determining the profitability level of the enterprise. Any variance or deviation in the

profits can be easily identified. If a variance or deviation is found in profitability then

rectifying steps can be immediately taken by the management to correct them so that

operations and functioning of the enterprise is not affected at all. Therefore, it can be said

that this acts like an advantage in the context of the company.

Disadvantages-

Marginal costing technique is based on certain assumptions which may not always be

true in all the situations and circumstances in the company. Practically, they may change

and therefore different results can be obtained. This can affect the level of accuracy of

results obtained in the organization.

Marginal costing technique overcomes the problems of over and under-absorption of the

fixed overheads. However, the problems related with the absorption of variable

overheads still persist within the organization. Thus it again affects the accuracy of

calculations and can give wrong results, conclusions and judgments. Managers may take

wrong decisions if accuracy is affected.

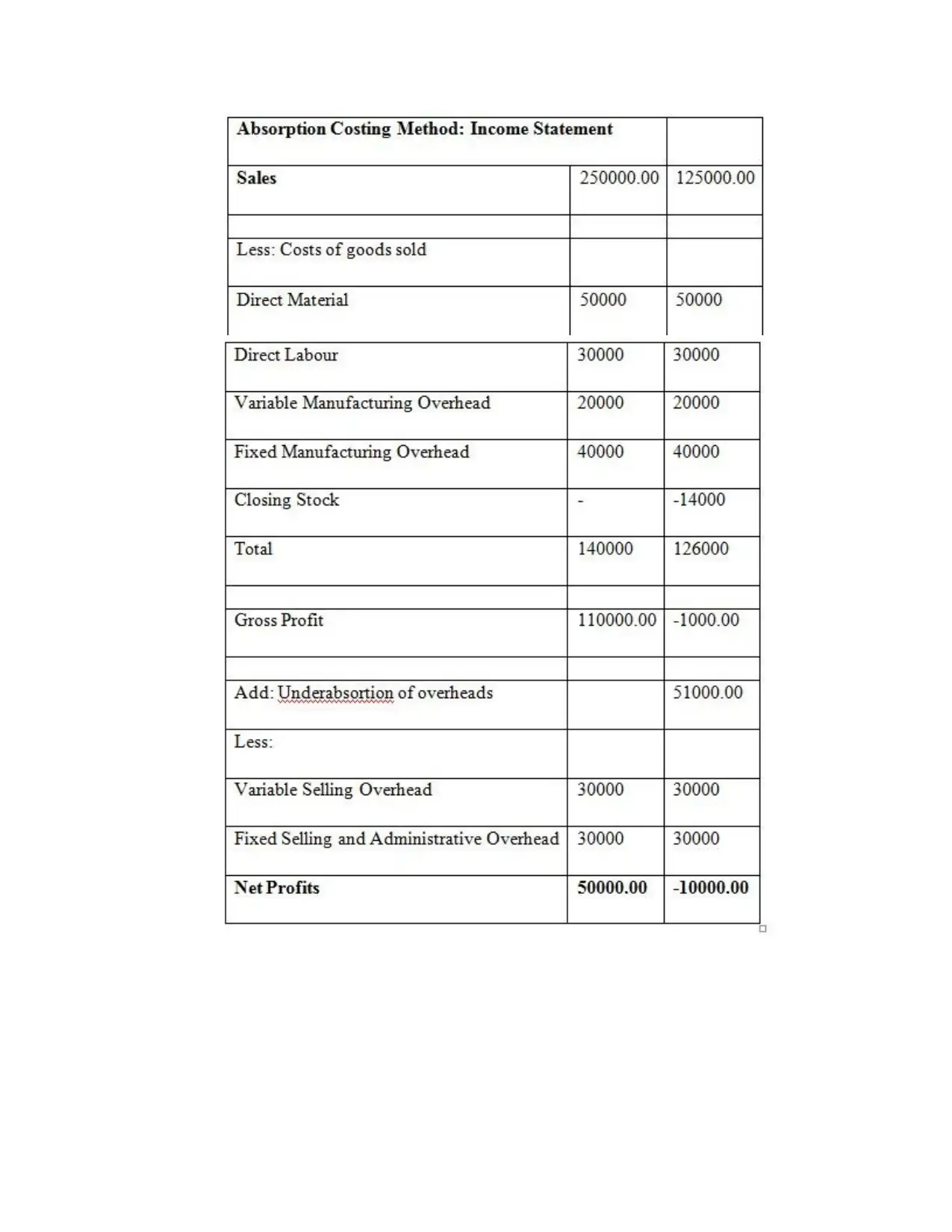

Absorption costing-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is a method of accounting of costs which takes into account all the expenses and

overheads incurring within an organization (Malmi, 2016). The managers of Creams Ltd. may

make use of this technique which helps in getting accurate results within the company.

Advantages-

It works according to the accrual and matching concept of accounting by helping to

match costs and revenues for a particular accounting period. Thus it ensures compilation

with the accounting standards set. This also helps in maintaining the accuracy in

calculations.

It can disclose whether the overheads pertaining to various departments are being

absorbed properly or not. Thus it is very much useful for manufacturing organizations. If

the overheads are not being absorbed properly it can indicate that easily and thus the

necessary steps can be taken within the organization for the same.

Disadvantages-

There is an argument by many accountants that fixed manufacturing, administration,

selling and distribution overheads do not produce future benefits and therefore must not

be included in the cost of the product.

It is not helpful for preparing a flexible budget as there is no distinction made between

fixed and variable costs of the product.

From the above discussion, it can be concluded that both marginal and absorption costing

techniques can be used by a company. A company like Creams Ltd. which deals in

production process should make use of both these techniques. This will help it in

determining the costs accurately and getting the desired results. Also the efficiency and

effectiveness will improve and thus the profits can be maximized easily. The goals and

objectives related to the organization can also be achieved if both these techniques are

used in the right manner by the management by ensuring accuracy and therefore this will

reflect in the results obtained in the organization.

overheads incurring within an organization (Malmi, 2016). The managers of Creams Ltd. may

make use of this technique which helps in getting accurate results within the company.

Advantages-

It works according to the accrual and matching concept of accounting by helping to

match costs and revenues for a particular accounting period. Thus it ensures compilation

with the accounting standards set. This also helps in maintaining the accuracy in

calculations.

It can disclose whether the overheads pertaining to various departments are being

absorbed properly or not. Thus it is very much useful for manufacturing organizations. If

the overheads are not being absorbed properly it can indicate that easily and thus the

necessary steps can be taken within the organization for the same.

Disadvantages-

There is an argument by many accountants that fixed manufacturing, administration,

selling and distribution overheads do not produce future benefits and therefore must not

be included in the cost of the product.

It is not helpful for preparing a flexible budget as there is no distinction made between

fixed and variable costs of the product.

From the above discussion, it can be concluded that both marginal and absorption costing

techniques can be used by a company. A company like Creams Ltd. which deals in

production process should make use of both these techniques. This will help it in

determining the costs accurately and getting the desired results. Also the efficiency and

effectiveness will improve and thus the profits can be maximized easily. The goals and

objectives related to the organization can also be achieved if both these techniques are

used in the right manner by the management by ensuring accuracy and therefore this will

reflect in the results obtained in the organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.