Management Accounting Techniques: Reporting, Analysis & Planning

VerifiedAdded on 2023/01/03

|16

|3743

|32

Report

AI Summary

This report provides a comprehensive analysis of management accounting techniques, focusing on their application in business decision-making and profitability enhancement. It explores various types of management accounting, including product costing, cash flow analysis, inventory turnover, capital budgeting, financial leverage, trend analysis, and marginal analysis. The report also discusses methods of management account reporting, such as budget reports, accounts receivables, cost managerial accounting reports, and performance reports. Furthermore, it includes an income statement using marginal and absorption costing methods, along with financial analysis of cost and revenue, break-even point calculation, and margin of safety analysis. The report concludes with a discussion of planning tools for budgetary control, specifically variance analysis, highlighting its advantages and disadvantages, and illustrates how companies utilize management accounting to address financial challenges.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

P1 Management Accounting and its Types.................................................................................3

P2 Methods of Management account reporting...........................................................................6

P3 Income statement using marginal and absorption cost...........................................................7

P4 Planning Tools for Budgetary Control.................................................................................10

P5 Comparison of how companies are using management accounting to respond to financial

problems....................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

P1 Management Accounting and its Types.................................................................................3

P2 Methods of Management account reporting...........................................................................6

P3 Income statement using marginal and absorption cost...........................................................7

P4 Planning Tools for Budgetary Control.................................................................................10

P5 Comparison of how companies are using management accounting to respond to financial

problems....................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

The study is about management accounting and its techniques which can be defined as

accounting tools used by management in an organisation for making business decisions and

generate profits for the organisation. The different types of management accounting and tools

used for reporting are discussed. Cost analysis using costing types used in management

accounting have been done to elaborate difference in costing techniques. Planning tools for

budgetary control and their advantages and disadvantages have been highlighted. The ways

company has used management accounting techniques to respond to financial problems has been

illustrated.

P1 Management Accounting and its Types

Management accounting is the process of making reports after analysing, interpreting and

communicating decisions to the management. It helps in making short term and long-term

decision making and about projects which can give a better yield to the company. The main

functions of management accounting are:

a) Forecasting: It involves decisions like the type of equipment to be bought, which markets

to be diversified and which regions to be entered in. It makes use of its tools in

forecasting how the investment can get good returns for the company (Abdusalomova,

2019).

b) Cash flow estimation: Management accounting helps in creating budget and accordingly

estimate cash flows which will be required in investment projects. Also with methods like

NPV it takes consideration of time value of money. Budget thus made helps in financial

planning.

c) Performance variances: The performance estimated of a department, a project or the

productivity of an equipment is taken in consideration and compared with actual

performances. This helps in finding out where the parameters have mismatched or have

been up to the mark.

The study is about management accounting and its techniques which can be defined as

accounting tools used by management in an organisation for making business decisions and

generate profits for the organisation. The different types of management accounting and tools

used for reporting are discussed. Cost analysis using costing types used in management

accounting have been done to elaborate difference in costing techniques. Planning tools for

budgetary control and their advantages and disadvantages have been highlighted. The ways

company has used management accounting techniques to respond to financial problems has been

illustrated.

P1 Management Accounting and its Types

Management accounting is the process of making reports after analysing, interpreting and

communicating decisions to the management. It helps in making short term and long-term

decision making and about projects which can give a better yield to the company. The main

functions of management accounting are:

a) Forecasting: It involves decisions like the type of equipment to be bought, which markets

to be diversified and which regions to be entered in. It makes use of its tools in

forecasting how the investment can get good returns for the company (Abdusalomova,

2019).

b) Cash flow estimation: Management accounting helps in creating budget and accordingly

estimate cash flows which will be required in investment projects. Also with methods like

NPV it takes consideration of time value of money. Budget thus made helps in financial

planning.

c) Performance variances: The performance estimated of a department, a project or the

productivity of an equipment is taken in consideration and compared with actual

performances. This helps in finding out where the parameters have mismatched or have

been up to the mark.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Types of managerial accounting

Product Costing and Valuation

The cost of making products involving direct and indirect costs, variable and fixed costs with

other overhead expenses are calculated and divided by the total number of goods produced. This

helps to find out per unit cost of product turned out for the company and helps to fix the price for

the product (Alborov and et.al.,2017). This is done by calculating profit margin and then pricing

the product for sale. Thus it helps in realizing the profit. Innocent drinks will get help to know

their production costs and accordingly they will also get to know where to cut costs and how to

price their products and make profits.

Cash flow analysis

Managers examine the cash inflow and cash outflow of a business decision thus calculating the

money flow coming as funds and purchases and payments as cash outflow. It helps to take

decision whether investment has generated cash flows as per required standards (Abdusalomova,

2019). While maintaining cash flow managers try to control in such a way that company has

enough liquidity to pay off its current liabilities. Innocent drinks if researching on launching a

new drink will get benefitted by cash flow estimates on how much they need to invest and what

cash money they can realise at the present by this venture.

Inventory Turnover Analysis

Managers calculate the storage costs of inventory apart from how fast the inventory is sold. This

helps in making decisions regarding manufacturing number of units or purchasing more

inventory. If there are excess costs coming in storage company will have to find out a way to

deal with it and minimize it so as to use remaining cash in operational activity. Economic order

quantity wherein bringing the right amount of inventory has to be realised for minimizing excess

costs. Innocent drinks will be able to order as per demand with help of Economic Order quantity

and thus reduce costs of inventory storage. The cash surplus can then be used in research and

innovation.

Product Costing and Valuation

The cost of making products involving direct and indirect costs, variable and fixed costs with

other overhead expenses are calculated and divided by the total number of goods produced. This

helps to find out per unit cost of product turned out for the company and helps to fix the price for

the product (Alborov and et.al.,2017). This is done by calculating profit margin and then pricing

the product for sale. Thus it helps in realizing the profit. Innocent drinks will get help to know

their production costs and accordingly they will also get to know where to cut costs and how to

price their products and make profits.

Cash flow analysis

Managers examine the cash inflow and cash outflow of a business decision thus calculating the

money flow coming as funds and purchases and payments as cash outflow. It helps to take

decision whether investment has generated cash flows as per required standards (Abdusalomova,

2019). While maintaining cash flow managers try to control in such a way that company has

enough liquidity to pay off its current liabilities. Innocent drinks if researching on launching a

new drink will get benefitted by cash flow estimates on how much they need to invest and what

cash money they can realise at the present by this venture.

Inventory Turnover Analysis

Managers calculate the storage costs of inventory apart from how fast the inventory is sold. This

helps in making decisions regarding manufacturing number of units or purchasing more

inventory. If there are excess costs coming in storage company will have to find out a way to

deal with it and minimize it so as to use remaining cash in operational activity. Economic order

quantity wherein bringing the right amount of inventory has to be realised for minimizing excess

costs. Innocent drinks will be able to order as per demand with help of Economic Order quantity

and thus reduce costs of inventory storage. The cash surplus can then be used in research and

innovation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital Budgeting

Investment analysis is done on new projects and equipment purchase to calculate its rate of

return on the project. It takes into view time value of money and rate of return on the project

which helps to determine the cash flows coming in future will hold what amount of present

value. Innocent drinks can get benefitted if they are thinking of setting up a new plant in a

locality, they will know the rate of return and time value of future cash flows and thus decide

whether to go with the project or not.

Financial Leverage

It means the company uses or acquires debt to purchase new assets or carry forward its

operations. Through ratios it can be determined that whether company is taking right amount of

debt or in excess as it can hamper liquidity of the company (Alborov and et.al.,2017). A balance

of equity and debt is suggested by management accountants. Innocent drinks will be able to

maintain a balance between its equity and debt as it will be aware of the consequence of excess

debt and thus think of ways to generate more equity.

Trend Analysis

Company has to look out for historical parameters with demographic trends of customers. These

statistics performed by accounting helps management know where to put money and which

should be the target segment of customers. These statistics will help Innocent drinks to know its

target base of who is consuming its products more and which are the market trends among

customers; the sales volume can also be calculated of how each drink is doing in its own segment

(Ax and Greve, 2017).

Marginal Analysis

There is a certain stage where company realises its break even and the managers have to now

find out the cost of producing an additional unit which is known as incremental cost. Now the

company can find out the production cost which will be needed for a batch of production and

mark it as per market trends to sell the batch lot and thus gain profit. Management Accounting

Investment analysis is done on new projects and equipment purchase to calculate its rate of

return on the project. It takes into view time value of money and rate of return on the project

which helps to determine the cash flows coming in future will hold what amount of present

value. Innocent drinks can get benefitted if they are thinking of setting up a new plant in a

locality, they will know the rate of return and time value of future cash flows and thus decide

whether to go with the project or not.

Financial Leverage

It means the company uses or acquires debt to purchase new assets or carry forward its

operations. Through ratios it can be determined that whether company is taking right amount of

debt or in excess as it can hamper liquidity of the company (Alborov and et.al.,2017). A balance

of equity and debt is suggested by management accountants. Innocent drinks will be able to

maintain a balance between its equity and debt as it will be aware of the consequence of excess

debt and thus think of ways to generate more equity.

Trend Analysis

Company has to look out for historical parameters with demographic trends of customers. These

statistics performed by accounting helps management know where to put money and which

should be the target segment of customers. These statistics will help Innocent drinks to know its

target base of who is consuming its products more and which are the market trends among

customers; the sales volume can also be calculated of how each drink is doing in its own segment

(Ax and Greve, 2017).

Marginal Analysis

There is a certain stage where company realises its break even and the managers have to now

find out the cost of producing an additional unit which is known as incremental cost. Now the

company can find out the production cost which will be needed for a batch of production and

mark it as per market trends to sell the batch lot and thus gain profit. Management Accounting

helps the company gain profits by this method. Innocent drinks can get to know its break even

where the company has covered up its total cost on a project or itself and now it can go for

marginal costing where by calculating the incremental cost per drink can price its batch at a

profit margin with market survey and can gain profits.

P2 Methods of Management account reporting

Budget Reports

Budget is also known as financial planning as to how much money should be allocated to each

department viz. purchases, accounts, marketing etc. Production costs of previous years with

inflation are taken into consideration and budget is made according to the demand prevailing

(Ax, C. and Greve, J., 2017). Salaries of Employees with incentives is taken in consideration on

annual basis and a separate budget is made for each section. Previous year expenditures are taken

in consideration while making budget. Innocent drinks will be able to financially plan as to

which segment is doing well in its range of products and need to be allocated more budget,

which section needs more budget viz. marketing seeing today’s arena etc.

Accounts Receivables

A company when supplying orders does not get money instantly by the suppliers. It has to extend

credit to its suppliers sometimes and these pending payments are known as account receivables.

Management accounting has reports being made of these pending payments which finds out the

total amount with timeline to be received. Also it helps to find out defaulters in the collection

process and accordingly forms credit policy. This will help making a report for Innocent drinks

as to who are its debtors and the payment period given to debtors; also the defaulters will be

known and accordingly provisions can be made (Burritt and et.al.,2019).

Cost Managerial Accounting reports

The costs gone in manufacturing the products comprising of all direct and indirect costs with the

fixed and variable expenses are calculated and then divided by the total units produced. This

helps in determining per unit cost of production. With current market trends in view the pricing

of products is then done by keeping a profit margin over the cost. Thus, this method helps

where the company has covered up its total cost on a project or itself and now it can go for

marginal costing where by calculating the incremental cost per drink can price its batch at a

profit margin with market survey and can gain profits.

P2 Methods of Management account reporting

Budget Reports

Budget is also known as financial planning as to how much money should be allocated to each

department viz. purchases, accounts, marketing etc. Production costs of previous years with

inflation are taken into consideration and budget is made according to the demand prevailing

(Ax, C. and Greve, J., 2017). Salaries of Employees with incentives is taken in consideration on

annual basis and a separate budget is made for each section. Previous year expenditures are taken

in consideration while making budget. Innocent drinks will be able to financially plan as to

which segment is doing well in its range of products and need to be allocated more budget,

which section needs more budget viz. marketing seeing today’s arena etc.

Accounts Receivables

A company when supplying orders does not get money instantly by the suppliers. It has to extend

credit to its suppliers sometimes and these pending payments are known as account receivables.

Management accounting has reports being made of these pending payments which finds out the

total amount with timeline to be received. Also it helps to find out defaulters in the collection

process and accordingly forms credit policy. This will help making a report for Innocent drinks

as to who are its debtors and the payment period given to debtors; also the defaulters will be

known and accordingly provisions can be made (Burritt and et.al.,2019).

Cost Managerial Accounting reports

The costs gone in manufacturing the products comprising of all direct and indirect costs with the

fixed and variable expenses are calculated and then divided by the total units produced. This

helps in determining per unit cost of production. With current market trends in view the pricing

of products is then done by keeping a profit margin over the cost. Thus, this method helps

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company in realising profits. Inventory costs are also calculated in these reports which help to

realise the total amount of cost going in maintaining inventory. Innocent drinks can now have

accountability of all costs whether fixed or variable in determining the production costs.

Accordingly, it can do a market survey and set the profit margin for its products.

Performance reports

The performance of various departments in organisation is evaluated and compared with set

standards. It is seen whether the department has been able to meet its goals within the budget or

how much it has exceeded the budget. Managers use these reports to form a strategy for future

for the organisation. Innocent drinks can evaluate the performance of various departments and

also thus know the efficiency of their budget planning along with that of the department (Burritt

and et.al.,2019).

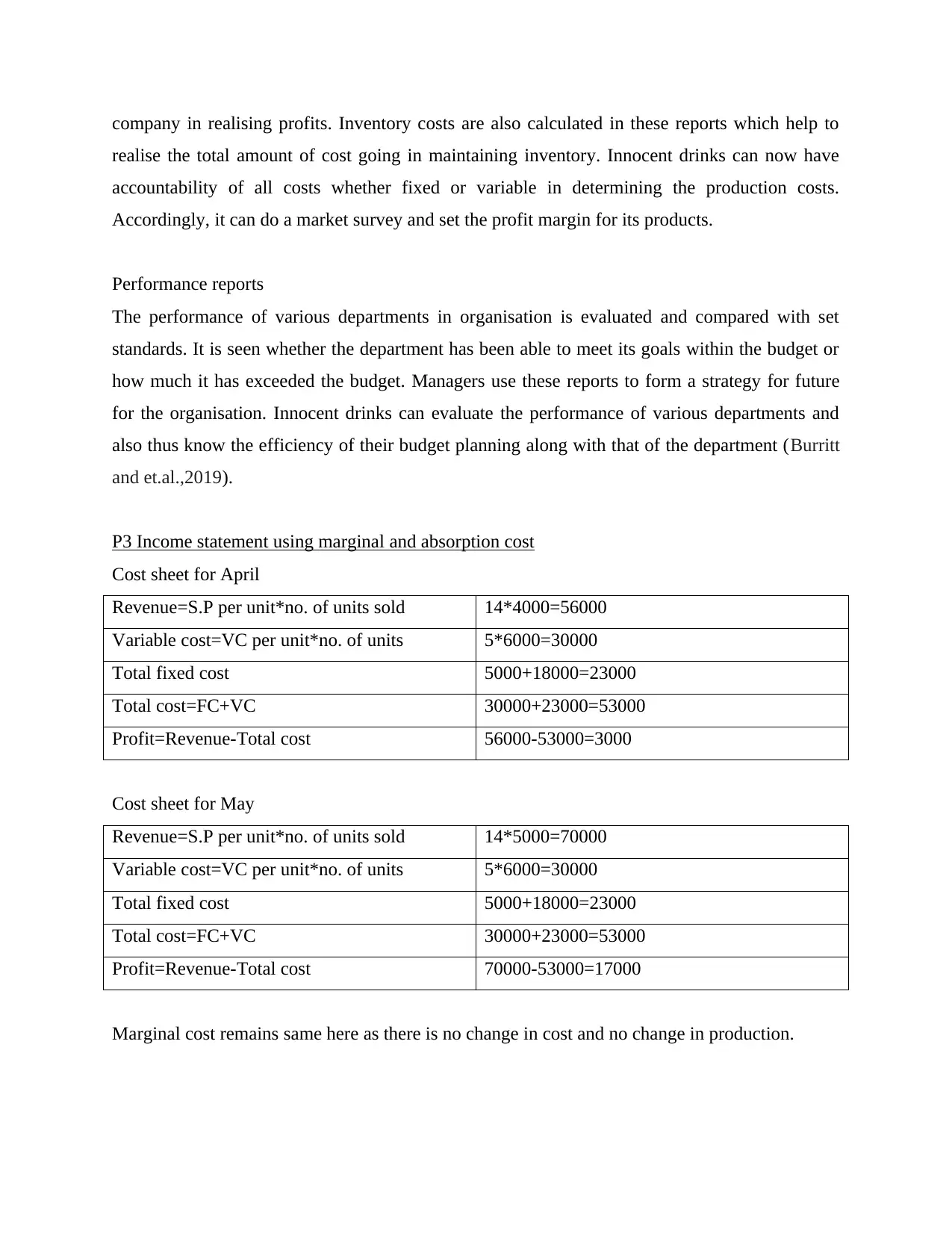

P3 Income statement using marginal and absorption cost

Cost sheet for April

Revenue=S.P per unit*no. of units sold 14*4000=56000

Variable cost=VC per unit*no. of units 5*6000=30000

Total fixed cost 5000+18000=23000

Total cost=FC+VC 30000+23000=53000

Profit=Revenue-Total cost 56000-53000=3000

Cost sheet for May

Revenue=S.P per unit*no. of units sold 14*5000=70000

Variable cost=VC per unit*no. of units 5*6000=30000

Total fixed cost 5000+18000=23000

Total cost=FC+VC 30000+23000=53000

Profit=Revenue-Total cost 70000-53000=17000

Marginal cost remains same here as there is no change in cost and no change in production.

realise the total amount of cost going in maintaining inventory. Innocent drinks can now have

accountability of all costs whether fixed or variable in determining the production costs.

Accordingly, it can do a market survey and set the profit margin for its products.

Performance reports

The performance of various departments in organisation is evaluated and compared with set

standards. It is seen whether the department has been able to meet its goals within the budget or

how much it has exceeded the budget. Managers use these reports to form a strategy for future

for the organisation. Innocent drinks can evaluate the performance of various departments and

also thus know the efficiency of their budget planning along with that of the department (Burritt

and et.al.,2019).

P3 Income statement using marginal and absorption cost

Cost sheet for April

Revenue=S.P per unit*no. of units sold 14*4000=56000

Variable cost=VC per unit*no. of units 5*6000=30000

Total fixed cost 5000+18000=23000

Total cost=FC+VC 30000+23000=53000

Profit=Revenue-Total cost 56000-53000=3000

Cost sheet for May

Revenue=S.P per unit*no. of units sold 14*5000=70000

Variable cost=VC per unit*no. of units 5*6000=30000

Total fixed cost 5000+18000=23000

Total cost=FC+VC 30000+23000=53000

Profit=Revenue-Total cost 70000-53000=17000

Marginal cost remains same here as there is no change in cost and no change in production.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

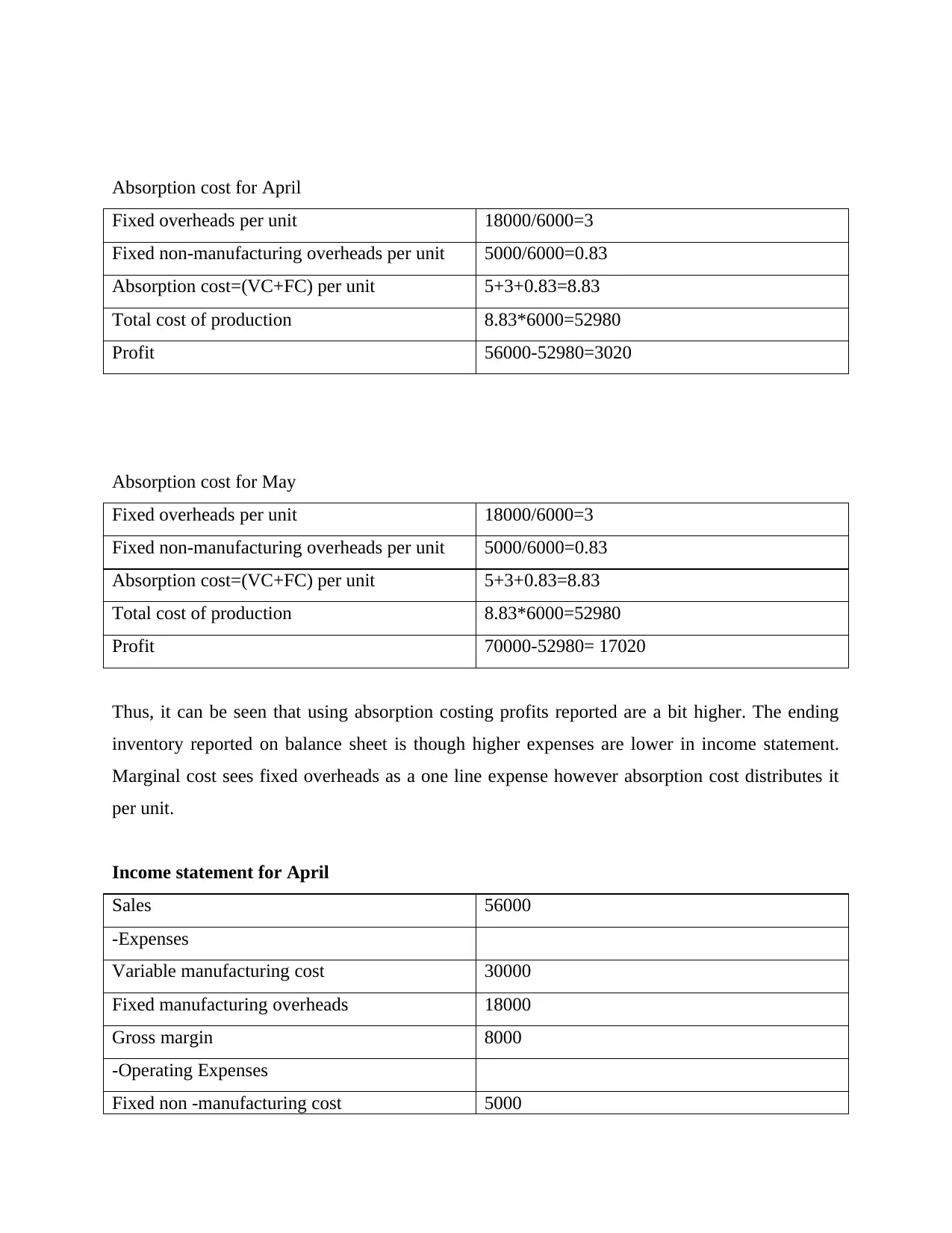

Absorption cost for April

Fixed overheads per unit 18000/6000=3

Fixed non-manufacturing overheads per unit 5000/6000=0.83

Absorption cost=(VC+FC) per unit 5+3+0.83=8.83

Total cost of production 8.83*6000=52980

Profit 56000-52980=3020

Absorption cost for May

Fixed overheads per unit 18000/6000=3

Fixed non-manufacturing overheads per unit 5000/6000=0.83

Absorption cost=(VC+FC) per unit 5+3+0.83=8.83

Total cost of production 8.83*6000=52980

Profit 70000-52980= 17020

Thus, it can be seen that using absorption costing profits reported are a bit higher. The ending

inventory reported on balance sheet is though higher expenses are lower in income statement.

Marginal cost sees fixed overheads as a one line expense however absorption cost distributes it

per unit.

Income statement for April

Sales 56000

-Expenses

Variable manufacturing cost 30000

Fixed manufacturing overheads 18000

Gross margin 8000

-Operating Expenses

Fixed non -manufacturing cost 5000

Fixed overheads per unit 18000/6000=3

Fixed non-manufacturing overheads per unit 5000/6000=0.83

Absorption cost=(VC+FC) per unit 5+3+0.83=8.83

Total cost of production 8.83*6000=52980

Profit 56000-52980=3020

Absorption cost for May

Fixed overheads per unit 18000/6000=3

Fixed non-manufacturing overheads per unit 5000/6000=0.83

Absorption cost=(VC+FC) per unit 5+3+0.83=8.83

Total cost of production 8.83*6000=52980

Profit 70000-52980= 17020

Thus, it can be seen that using absorption costing profits reported are a bit higher. The ending

inventory reported on balance sheet is though higher expenses are lower in income statement.

Marginal cost sees fixed overheads as a one line expense however absorption cost distributes it

per unit.

Income statement for April

Sales 56000

-Expenses

Variable manufacturing cost 30000

Fixed manufacturing overheads 18000

Gross margin 8000

-Operating Expenses

Fixed non -manufacturing cost 5000

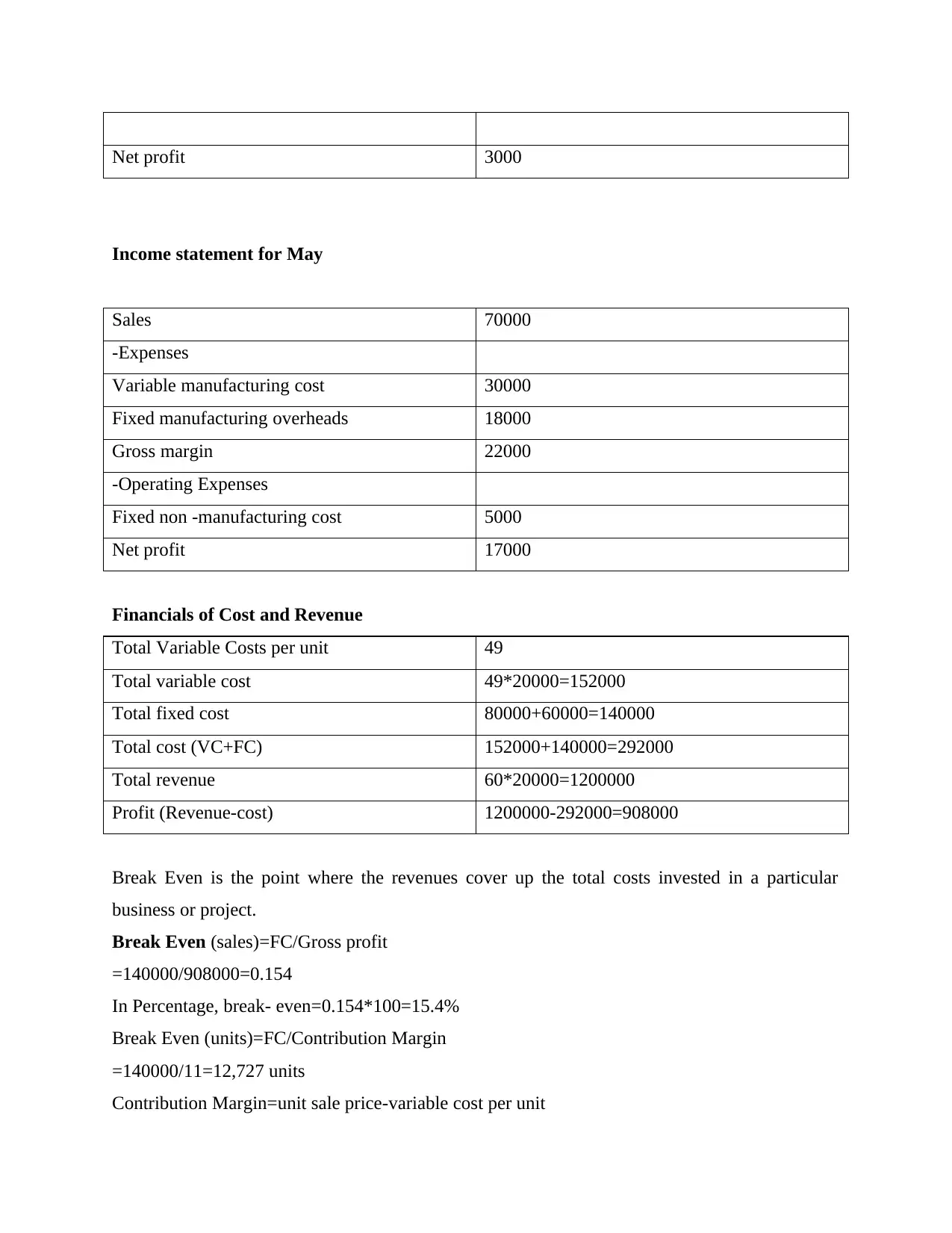

Net profit 3000

Income statement for May

Sales 70000

-Expenses

Variable manufacturing cost 30000

Fixed manufacturing overheads 18000

Gross margin 22000

-Operating Expenses

Fixed non -manufacturing cost 5000

Net profit 17000

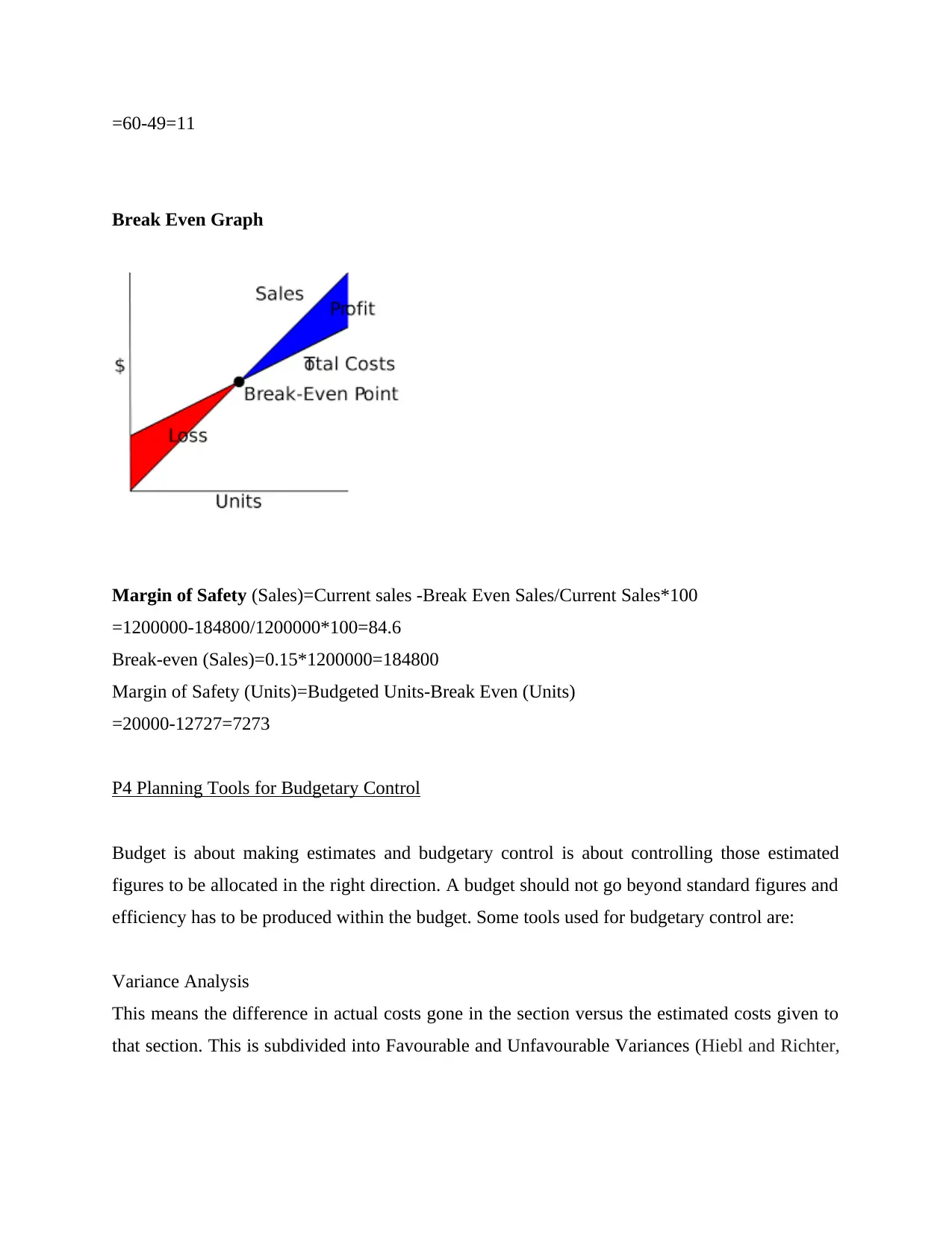

Financials of Cost and Revenue

Total Variable Costs per unit 49

Total variable cost 49*20000=152000

Total fixed cost 80000+60000=140000

Total cost (VC+FC) 152000+140000=292000

Total revenue 60*20000=1200000

Profit (Revenue-cost) 1200000-292000=908000

Break Even is the point where the revenues cover up the total costs invested in a particular

business or project.

Break Even (sales)=FC/Gross profit

=140000/908000=0.154

In Percentage, break- even=0.154*100=15.4%

Break Even (units)=FC/Contribution Margin

=140000/11=12,727 units

Contribution Margin=unit sale price-variable cost per unit

Income statement for May

Sales 70000

-Expenses

Variable manufacturing cost 30000

Fixed manufacturing overheads 18000

Gross margin 22000

-Operating Expenses

Fixed non -manufacturing cost 5000

Net profit 17000

Financials of Cost and Revenue

Total Variable Costs per unit 49

Total variable cost 49*20000=152000

Total fixed cost 80000+60000=140000

Total cost (VC+FC) 152000+140000=292000

Total revenue 60*20000=1200000

Profit (Revenue-cost) 1200000-292000=908000

Break Even is the point where the revenues cover up the total costs invested in a particular

business or project.

Break Even (sales)=FC/Gross profit

=140000/908000=0.154

In Percentage, break- even=0.154*100=15.4%

Break Even (units)=FC/Contribution Margin

=140000/11=12,727 units

Contribution Margin=unit sale price-variable cost per unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

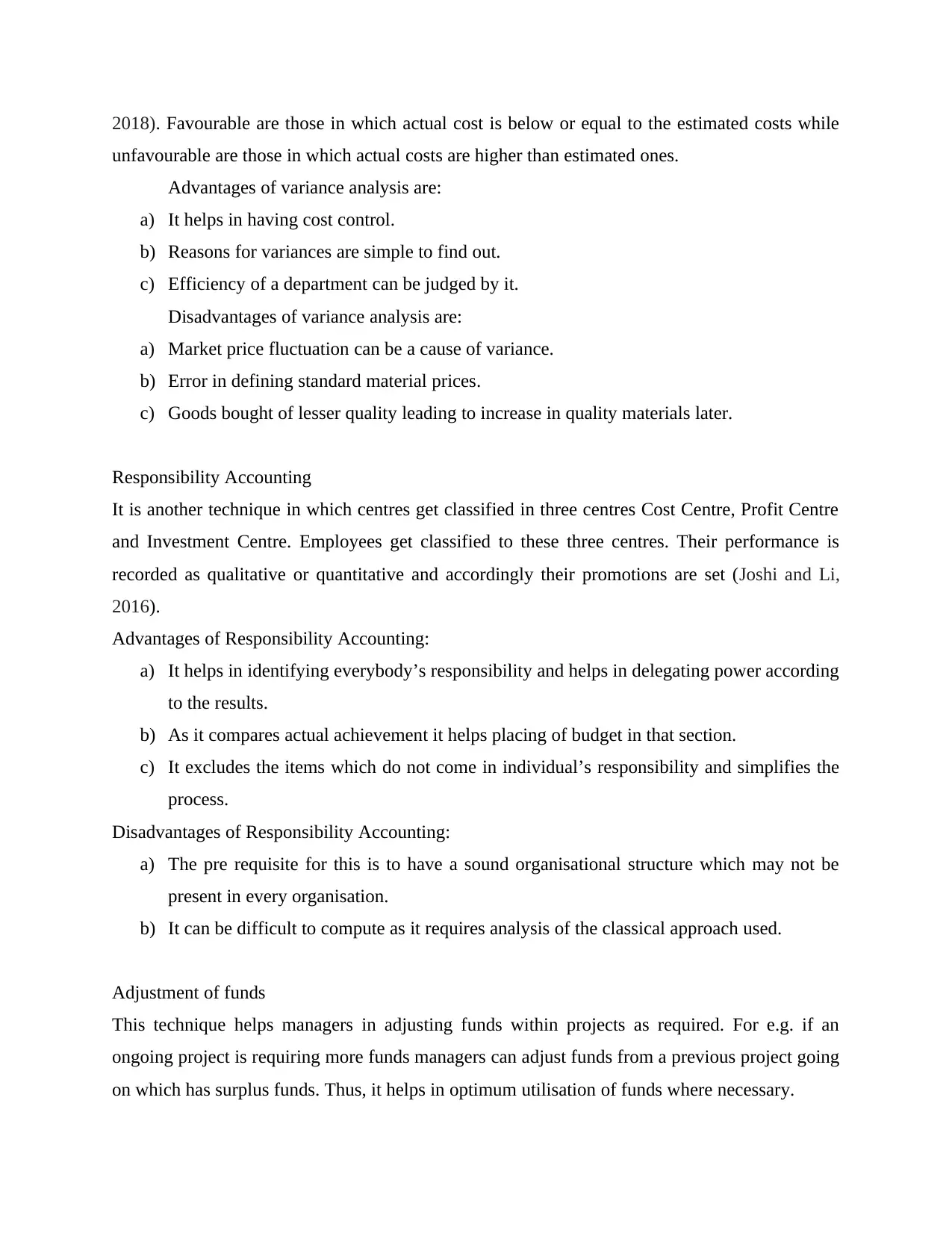

=60-49=11

Break Even Graph

Margin of Safety (Sales)=Current sales -Break Even Sales/Current Sales*100

=1200000-184800/1200000*100=84.6

Break-even (Sales)=0.15*1200000=184800

Margin of Safety (Units)=Budgeted Units-Break Even (Units)

=20000-12727=7273

P4 Planning Tools for Budgetary Control

Budget is about making estimates and budgetary control is about controlling those estimated

figures to be allocated in the right direction. A budget should not go beyond standard figures and

efficiency has to be produced within the budget. Some tools used for budgetary control are:

Variance Analysis

This means the difference in actual costs gone in the section versus the estimated costs given to

that section. This is subdivided into Favourable and Unfavourable Variances (Hiebl and Richter,

Break Even Graph

Margin of Safety (Sales)=Current sales -Break Even Sales/Current Sales*100

=1200000-184800/1200000*100=84.6

Break-even (Sales)=0.15*1200000=184800

Margin of Safety (Units)=Budgeted Units-Break Even (Units)

=20000-12727=7273

P4 Planning Tools for Budgetary Control

Budget is about making estimates and budgetary control is about controlling those estimated

figures to be allocated in the right direction. A budget should not go beyond standard figures and

efficiency has to be produced within the budget. Some tools used for budgetary control are:

Variance Analysis

This means the difference in actual costs gone in the section versus the estimated costs given to

that section. This is subdivided into Favourable and Unfavourable Variances (Hiebl and Richter,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018). Favourable are those in which actual cost is below or equal to the estimated costs while

unfavourable are those in which actual costs are higher than estimated ones.

Advantages of variance analysis are:

a) It helps in having cost control.

b) Reasons for variances are simple to find out.

c) Efficiency of a department can be judged by it.

Disadvantages of variance analysis are:

a) Market price fluctuation can be a cause of variance.

b) Error in defining standard material prices.

c) Goods bought of lesser quality leading to increase in quality materials later.

Responsibility Accounting

It is another technique in which centres get classified in three centres Cost Centre, Profit Centre

and Investment Centre. Employees get classified to these three centres. Their performance is

recorded as qualitative or quantitative and accordingly their promotions are set (Joshi and Li,

2016).

Advantages of Responsibility Accounting:

a) It helps in identifying everybody’s responsibility and helps in delegating power according

to the results.

b) As it compares actual achievement it helps placing of budget in that section.

c) It excludes the items which do not come in individual’s responsibility and simplifies the

process.

Disadvantages of Responsibility Accounting:

a) The pre requisite for this is to have a sound organisational structure which may not be

present in every organisation.

b) It can be difficult to compute as it requires analysis of the classical approach used.

Adjustment of funds

This technique helps managers in adjusting funds within projects as required. For e.g. if an

ongoing project is requiring more funds managers can adjust funds from a previous project going

on which has surplus funds. Thus, it helps in optimum utilisation of funds where necessary.

unfavourable are those in which actual costs are higher than estimated ones.

Advantages of variance analysis are:

a) It helps in having cost control.

b) Reasons for variances are simple to find out.

c) Efficiency of a department can be judged by it.

Disadvantages of variance analysis are:

a) Market price fluctuation can be a cause of variance.

b) Error in defining standard material prices.

c) Goods bought of lesser quality leading to increase in quality materials later.

Responsibility Accounting

It is another technique in which centres get classified in three centres Cost Centre, Profit Centre

and Investment Centre. Employees get classified to these three centres. Their performance is

recorded as qualitative or quantitative and accordingly their promotions are set (Joshi and Li,

2016).

Advantages of Responsibility Accounting:

a) It helps in identifying everybody’s responsibility and helps in delegating power according

to the results.

b) As it compares actual achievement it helps placing of budget in that section.

c) It excludes the items which do not come in individual’s responsibility and simplifies the

process.

Disadvantages of Responsibility Accounting:

a) The pre requisite for this is to have a sound organisational structure which may not be

present in every organisation.

b) It can be difficult to compute as it requires analysis of the classical approach used.

Adjustment of funds

This technique helps managers in adjusting funds within projects as required. For e.g. if an

ongoing project is requiring more funds managers can adjust funds from a previous project going

on which has surplus funds. Thus, it helps in optimum utilisation of funds where necessary.

Advantages :

a) It helps in utilisation of funds optimally.

b) It helps in saving further use of capital by adjusting as per the need.

Disadvantages:

a) The calculations may go wrong sometimes as the surplus fund to a project may be

required by that project later on.

b) Adjusting of entries have to be done carefully beforehand to avoid discrepancies.

Zero based budgeting

It states that budget of next year can be zero if estimated revenues are equal to estimated

expenses. This technique helps in having control over amount of money spent during the year

(Hiebl and Richter, 2018).

Advantages of zero-based budgeting:

a) It is efficient in allocation of resources as it does not take traditional numbers but the

actual numbers in cash flow statement.

b) It has accuracy as it looks in each cash flow of every department to form the budget.

c) It computes operational costs and thus helps in a way to reduce costs.

Disadvantages of zero-based budgeting:

a) It is time consuming as each and every line of cash flow has to be interpreted.

b) It requires expertise to calculate every line item and thus requires special training.

c) A high manpower is required to compute so many costs.

P5 Comparison of how companies are using management accounting to respond to financial

problems

Management accounting in organisations have helped companies deal with problems regarding

financial matters and also achieve financial goals with profitability (Joshi and Li,2016). Here is a

comparison of two companies who have used management accounting to their benefits:

a) It helps in utilisation of funds optimally.

b) It helps in saving further use of capital by adjusting as per the need.

Disadvantages:

a) The calculations may go wrong sometimes as the surplus fund to a project may be

required by that project later on.

b) Adjusting of entries have to be done carefully beforehand to avoid discrepancies.

Zero based budgeting

It states that budget of next year can be zero if estimated revenues are equal to estimated

expenses. This technique helps in having control over amount of money spent during the year

(Hiebl and Richter, 2018).

Advantages of zero-based budgeting:

a) It is efficient in allocation of resources as it does not take traditional numbers but the

actual numbers in cash flow statement.

b) It has accuracy as it looks in each cash flow of every department to form the budget.

c) It computes operational costs and thus helps in a way to reduce costs.

Disadvantages of zero-based budgeting:

a) It is time consuming as each and every line of cash flow has to be interpreted.

b) It requires expertise to calculate every line item and thus requires special training.

c) A high manpower is required to compute so many costs.

P5 Comparison of how companies are using management accounting to respond to financial

problems

Management accounting in organisations have helped companies deal with problems regarding

financial matters and also achieve financial goals with profitability (Joshi and Li,2016). Here is a

comparison of two companies who have used management accounting to their benefits:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.