Management Accounting: Unit 5 Report on Financial Strategies

VerifiedAdded on 2021/02/21

|18

|3694

|436

Report

AI Summary

This report delves into the realm of management accounting, exploring its systems, reporting methods, and application in financial analysis. The report begins with an introduction to management accounting and its importance, followed by a detailed examination of various accounting systems such as inventory management, cost accounting, price optimization, and job costing systems. The report further investigates different management accounting reporting methods, including cost accounting reports, inventory management reports, budget reports, and performance reports. It then discusses the benefits of management accounting systems and their integration within organizational processes. The report also covers the preparation of income statements using absorption and marginal costing methods. Furthermore, it analyzes the advantages and disadvantages of planning tools like budgetary control and compares the application of management accounting systems in responding to financial problems, using Alpha Financial and Brightstar as case studies. The report concludes by highlighting how management accounting can lead organizations to sustainable success and evaluating planning tools for accounting periods to address financial problems effectively.

Unit 5

Management Accounting

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting system and essential for various kind of accounting system.........3

P2. Different method of management accounting reporting........................................................5

M1 Benefits of management accounting systems........................................................................6

D1 Management accounting systems and reporting are integrated with the organisational

process..........................................................................................................................................7

TASK 2............................................................................................................................................7

P3. Preparation of income statements with the use of appropriate techniques............................7

M2 Management accounting techniques and financial reporting..............................................11

D2. Interpretation of prepared financial statements...................................................................11

TASK 3..........................................................................................................................................12

P4 Advantages and disadvantages of various kind of planning tools of budgetary control......12

M3 Use of different planning tools and their application for preparing the budgets. ...............14

TASK 4..........................................................................................................................................14

P5 Comparison of entity due to adapting management accounting systems to respond to

financial problems......................................................................................................................14

Comparison between Alpha Financial and Brightstar...............................................................15

M4 Responding to financial problems, management accounting can lead organisations to

sustainable success.....................................................................................................................16

D3 Evaluate planning tools for accounting period to respond financial problems appropriately

....................................................................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting system and essential for various kind of accounting system.........3

P2. Different method of management accounting reporting........................................................5

M1 Benefits of management accounting systems........................................................................6

D1 Management accounting systems and reporting are integrated with the organisational

process..........................................................................................................................................7

TASK 2............................................................................................................................................7

P3. Preparation of income statements with the use of appropriate techniques............................7

M2 Management accounting techniques and financial reporting..............................................11

D2. Interpretation of prepared financial statements...................................................................11

TASK 3..........................................................................................................................................12

P4 Advantages and disadvantages of various kind of planning tools of budgetary control......12

M3 Use of different planning tools and their application for preparing the budgets. ...............14

TASK 4..........................................................................................................................................14

P5 Comparison of entity due to adapting management accounting systems to respond to

financial problems......................................................................................................................14

Comparison between Alpha Financial and Brightstar...............................................................15

M4 Responding to financial problems, management accounting can lead organisations to

sustainable success.....................................................................................................................16

D3 Evaluate planning tools for accounting period to respond financial problems appropriately

....................................................................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is also known by the managerial accounting. This is so because

it is a kind of accounting system which is related to providing necessary information to the

managers of company so that they can manage their activities and operations in an effective way.

So basically, this accounting discipline is worth-full for internal stakeholders not for the

external. Herein, the project report various types of accounting system and accounting reports are

mentioned (Abdelmoneim Mohamed and Jones, 2014). Apart from it, different method of

costing are discussed to produce the income statements on given data as well as advantages and

disadvantages of planning tools are also included in project report. Along with use of

management accounting in overcoming the financial issues is also mentioned. To understand in

detail sense Brighstar financial limited company is selected. The company provides financial

consultancy services to multi-pal companies and their headquarters is at Essex UK. In the report

company's client company KEF manufacturing company is selected.

TASK 1

P1. Management accounting system and essential for various kind of accounting system

The management accounting system can be defined as a process of collecting, analysing

and presenting the quantitative and qualitative information to the users for the purpose of making

decisions about the best sourcing and use of funds in any business. Though this accounting

system is not mandatory to implement for the organisations, but it is becoming essential part of

the companies. There is various kind of accounting system which have their own importance.

The Bright-star financial limited company use various kind of accounting systems that are

mentioned below: Inventory management system- This is a type of accounting system which is associated

with the better management of the stock. Due to stock management system companies

can analyse the need of raw material as well as can take decision about the production.

As well as it informs about the availability of raw material in the stock. Eventually, it is

essential for having detailed proper record of inventories. Like the Bright star financial

company can suggest to their client KEF manufacturing company to manage their stock.

Management accounting is also known by the managerial accounting. This is so because

it is a kind of accounting system which is related to providing necessary information to the

managers of company so that they can manage their activities and operations in an effective way.

So basically, this accounting discipline is worth-full for internal stakeholders not for the

external. Herein, the project report various types of accounting system and accounting reports are

mentioned (Abdelmoneim Mohamed and Jones, 2014). Apart from it, different method of

costing are discussed to produce the income statements on given data as well as advantages and

disadvantages of planning tools are also included in project report. Along with use of

management accounting in overcoming the financial issues is also mentioned. To understand in

detail sense Brighstar financial limited company is selected. The company provides financial

consultancy services to multi-pal companies and their headquarters is at Essex UK. In the report

company's client company KEF manufacturing company is selected.

TASK 1

P1. Management accounting system and essential for various kind of accounting system

The management accounting system can be defined as a process of collecting, analysing

and presenting the quantitative and qualitative information to the users for the purpose of making

decisions about the best sourcing and use of funds in any business. Though this accounting

system is not mandatory to implement for the organisations, but it is becoming essential part of

the companies. There is various kind of accounting system which have their own importance.

The Bright-star financial limited company use various kind of accounting systems that are

mentioned below: Inventory management system- This is a type of accounting system which is associated

with the better management of the stock. Due to stock management system companies

can analyse the need of raw material as well as can take decision about the production.

As well as it informs about the availability of raw material in the stock. Eventually, it is

essential for having detailed proper record of inventories. Like the Bright star financial

company can suggest to their client KEF manufacturing company to manage their stock.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system- It is a kind of accounting system that enables effective cost

management in the organisations. As well as due to this accounting system, companies

can compute the cost of various activities separately. Basically, this accounting system is

essential for the companies in reducing and controlling the cost of different activities and

operations (Bagautdinova, Kundakchyan and Malakhov, 2013). The Bright-star financial

limited company can guide their client company to use this system so that their

expenditures can be managed. Price optimisation system- The price optimisation system is a part of management

accounting system which is related to the fixing the prices of products and services at an

effective level. As well as on the basis of this accounting system, organisations can

understand the behaviour of their customer on different pricing level. So it is essential for

the assigning the right price of products and services. Herein, the aspect of Bright-star

financial company, they give advice to the KEF manufacturing company to determine the

price of their manufacturing products.

Job costing system- The job costing system is a type of accounting system that evaluate

the cost or expenditures of revenue which occurs due to any specific job. So basically, it

is an accounting system which gives broad information regarding to the cost which is

related to any specific job. In other words, this accounting system is essential for the

computing the cost which is assigned to various jobs. This costing system includes

following information’s which are mentioned below:

Direct material cost- It is a kind of cost which can be traced with the unit of production. This cost

is being involved in the job costing system.

Direct labour cost- This cost is related to the labour involved in the manufacturing of products

and services. As well as this information is provided by the job costing system.

So the job costing system has valuable information regarding to the different kind of cost. Due to

this companies can aware about their overall expenditure related to each job assigned to different

activities. In Bright-star financial limited company, they suggest their client KEF manufacturing

company which can help in computing the cost of job.

management in the organisations. As well as due to this accounting system, companies

can compute the cost of various activities separately. Basically, this accounting system is

essential for the companies in reducing and controlling the cost of different activities and

operations (Bagautdinova, Kundakchyan and Malakhov, 2013). The Bright-star financial

limited company can guide their client company to use this system so that their

expenditures can be managed. Price optimisation system- The price optimisation system is a part of management

accounting system which is related to the fixing the prices of products and services at an

effective level. As well as on the basis of this accounting system, organisations can

understand the behaviour of their customer on different pricing level. So it is essential for

the assigning the right price of products and services. Herein, the aspect of Bright-star

financial company, they give advice to the KEF manufacturing company to determine the

price of their manufacturing products.

Job costing system- The job costing system is a type of accounting system that evaluate

the cost or expenditures of revenue which occurs due to any specific job. So basically, it

is an accounting system which gives broad information regarding to the cost which is

related to any specific job. In other words, this accounting system is essential for the

computing the cost which is assigned to various jobs. This costing system includes

following information’s which are mentioned below:

Direct material cost- It is a kind of cost which can be traced with the unit of production. This cost

is being involved in the job costing system.

Direct labour cost- This cost is related to the labour involved in the manufacturing of products

and services. As well as this information is provided by the job costing system.

So the job costing system has valuable information regarding to the different kind of cost. Due to

this companies can aware about their overall expenditure related to each job assigned to different

activities. In Bright-star financial limited company, they suggest their client KEF manufacturing

company which can help in computing the cost of job.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2. Different method of management accounting reporting

Management accounting reporting is based on recording information by managers at

workplace in order to communicate relevant information related to accounting system to

different departments as well as top level management. These reports are used while taking

critical decisions for the betterment of any organisation. In different company’s different

accounting reports are prepared and at the same time management accounting reports have their

unique role in any firm as these are significant for internal management for preparing strategies,

programmes as well as plans for future time period. Monetary along with non-monetary

information is used for the preparation of such reports. The client company of Bright-star

financial limited company prepares following reports:

Cost accounting report: It is a kind of report that includes information regarding to the

cost of different activities. Under such reporting system, information related to various costs is

recorded in systematic manner. It involves costs related to material costs, overhead costs, labour

costs and many more. This report is used for realizing prices of various items in order to estimate

profit margins (Bargate, 2012). This report provides a clear picture of associated costs of certain

items in production procedures. The aim of preparing this report is to control costs along with

improving efficiencies at workplace. In KEF manufacturing company, managers by using cost

accounting report identifies additional as well as unproductive costs in production or

manufacturing process which leads to assist organisation to optimise costs in order to increase

profit margins.

Inventory management report: Under this report, information related to available stock

at warehouses, products in transits as well as finished goods which are available for selling

purposes are recorded in appropriate manner. This report is prepared by production along with

warehouse managers to keep the record related with available and required stock in order to

provide strength to organisation so that they can supply products as per the demand in market.

The chosen client company prepares this report where all the necessary information in detailed

manner is provided related to stock of inventory. By providing such report managers can

improve inventory management by tracking cost of sold products as well as assist them to avoid

overselling along with underselling of products.

Budget report: Under this report, budget estimations are made on the basis of previous

experiences. These reports provide information related to all sources of expenditures or revenues.

Management accounting reporting is based on recording information by managers at

workplace in order to communicate relevant information related to accounting system to

different departments as well as top level management. These reports are used while taking

critical decisions for the betterment of any organisation. In different company’s different

accounting reports are prepared and at the same time management accounting reports have their

unique role in any firm as these are significant for internal management for preparing strategies,

programmes as well as plans for future time period. Monetary along with non-monetary

information is used for the preparation of such reports. The client company of Bright-star

financial limited company prepares following reports:

Cost accounting report: It is a kind of report that includes information regarding to the

cost of different activities. Under such reporting system, information related to various costs is

recorded in systematic manner. It involves costs related to material costs, overhead costs, labour

costs and many more. This report is used for realizing prices of various items in order to estimate

profit margins (Bargate, 2012). This report provides a clear picture of associated costs of certain

items in production procedures. The aim of preparing this report is to control costs along with

improving efficiencies at workplace. In KEF manufacturing company, managers by using cost

accounting report identifies additional as well as unproductive costs in production or

manufacturing process which leads to assist organisation to optimise costs in order to increase

profit margins.

Inventory management report: Under this report, information related to available stock

at warehouses, products in transits as well as finished goods which are available for selling

purposes are recorded in appropriate manner. This report is prepared by production along with

warehouse managers to keep the record related with available and required stock in order to

provide strength to organisation so that they can supply products as per the demand in market.

The chosen client company prepares this report where all the necessary information in detailed

manner is provided related to stock of inventory. By providing such report managers can

improve inventory management by tracking cost of sold products as well as assist them to avoid

overselling along with underselling of products.

Budget report: Under this report, budget estimations are made on the basis of previous

experiences. These reports provide information related to all sources of expenditures or revenues.

These reports are used by Bright-star managers to measure actual performance by comparing

standard targets with actual results. By analysing this report, managers management

organisational performances as well as certain issues which hampers achieving estimated targets.

On the basis of budget report, important decisions are taken for allocation of funds in various

departments along with serious activities for future time period. Like in the KEF manufacturing

company they prepare these reports to manage their performance.

Performance reports: This report includes performance of each employee along with

departmental performance and managers review such performances at the end of accounting

period. Apart from it, the performance report consist particular standard of performance for

measuring the actual performance (Bloomfield, 2015). Due to this companies can compare their

actual performance of employees and other activities and can take suitable decisions. This report

helps KEF manufacturing company to take key decisions as well as strategies for future time

period. Manager of selected business uses performance report to analyse strength as well as

weakness in order to make strategic decisions for the betterment of firm.

M1 Benefits of management accounting systems.

There are different kinds of management accounting system and each of them plays a

crucial role in the context of all kind of organisations. The KEF manufacturing limited company

implements various kind of accounting systems which are beneficial not only for them but also

for their clients. Herein, below advantage of these accounting systems mentioned:

Type of accounting system Benefits

Inventory management system This accounting system is useful in effective

management of the raw material and finished

goods. On the basis of it, companies take

decisions about purchasing and production. In

the KEF manufacturing limited company, they

suggest this accounting system to their clients

who operates in manufacture sector.

Cost accounting system As name assists, it is helpful in computing

overall cost of different operations and

standard targets with actual results. By analysing this report, managers management

organisational performances as well as certain issues which hampers achieving estimated targets.

On the basis of budget report, important decisions are taken for allocation of funds in various

departments along with serious activities for future time period. Like in the KEF manufacturing

company they prepare these reports to manage their performance.

Performance reports: This report includes performance of each employee along with

departmental performance and managers review such performances at the end of accounting

period. Apart from it, the performance report consist particular standard of performance for

measuring the actual performance (Bloomfield, 2015). Due to this companies can compare their

actual performance of employees and other activities and can take suitable decisions. This report

helps KEF manufacturing company to take key decisions as well as strategies for future time

period. Manager of selected business uses performance report to analyse strength as well as

weakness in order to make strategic decisions for the betterment of firm.

M1 Benefits of management accounting systems.

There are different kinds of management accounting system and each of them plays a

crucial role in the context of all kind of organisations. The KEF manufacturing limited company

implements various kind of accounting systems which are beneficial not only for them but also

for their clients. Herein, below advantage of these accounting systems mentioned:

Type of accounting system Benefits

Inventory management system This accounting system is useful in effective

management of the raw material and finished

goods. On the basis of it, companies take

decisions about purchasing and production. In

the KEF manufacturing limited company, they

suggest this accounting system to their clients

who operates in manufacture sector.

Cost accounting system As name assists, it is helpful in computing

overall cost of different operations and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

activities. Like in the KEF manufacturing

limited company, this is beneficial in having

information about cost of their financial

services and products.

Price optimisation This accounting system is beneficial in the

analysing the customer's reaction on different

prices of products and services. For example,

in the KEF manufacturing limited company, it

helps in the fixing the prices of their financial

services and products (Collis and Hussey,

2017).

Job costing system It is beneficial in the computing the cost of

each job which is assigned to different

activities. Like in the KEF manufacturing

limited company, it is very beneficial in

providing information about the cost of job.

D1 Management accounting systems and reporting are integrated with the organisational process.

The management accounting systems and reporting are related with each other. This is

why because for the preparation of the management accounting reports, necessary information is

gathered from the different management accounting systems (Demerjian and et.al., 2012). Such

as in the Bright-star financial limited company's client company, they produce reports like

inventory reports, cost accounting reports with the help of inventory management system and

cost accounting system. So basically, both are aligned with each other and it is commonly

integrated within the organisational process.

limited company, this is beneficial in having

information about cost of their financial

services and products.

Price optimisation This accounting system is beneficial in the

analysing the customer's reaction on different

prices of products and services. For example,

in the KEF manufacturing limited company, it

helps in the fixing the prices of their financial

services and products (Collis and Hussey,

2017).

Job costing system It is beneficial in the computing the cost of

each job which is assigned to different

activities. Like in the KEF manufacturing

limited company, it is very beneficial in

providing information about the cost of job.

D1 Management accounting systems and reporting are integrated with the organisational process.

The management accounting systems and reporting are related with each other. This is

why because for the preparation of the management accounting reports, necessary information is

gathered from the different management accounting systems (Demerjian and et.al., 2012). Such

as in the Bright-star financial limited company's client company, they produce reports like

inventory reports, cost accounting reports with the help of inventory management system and

cost accounting system. So basically, both are aligned with each other and it is commonly

integrated within the organisational process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

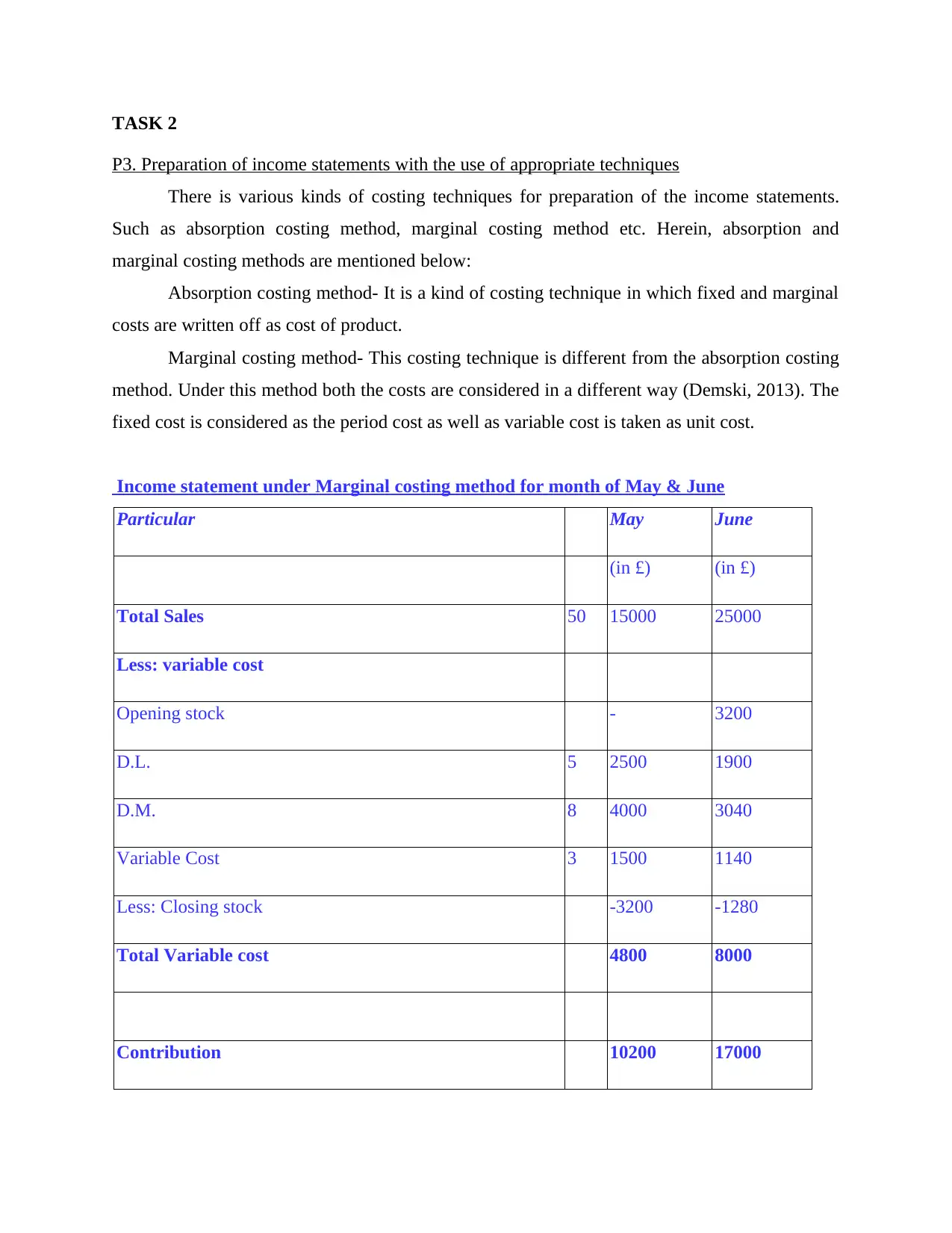

P3. Preparation of income statements with the use of appropriate techniques

There is various kinds of costing techniques for preparation of the income statements.

Such as absorption costing method, marginal costing method etc. Herein, absorption and

marginal costing methods are mentioned below:

Absorption costing method- It is a kind of costing technique in which fixed and marginal

costs are written off as cost of product.

Marginal costing method- This costing technique is different from the absorption costing

method. Under this method both the costs are considered in a different way (Demski, 2013). The

fixed cost is considered as the period cost as well as variable cost is taken as unit cost.

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

P3. Preparation of income statements with the use of appropriate techniques

There is various kinds of costing techniques for preparation of the income statements.

Such as absorption costing method, marginal costing method etc. Herein, absorption and

marginal costing methods are mentioned below:

Absorption costing method- It is a kind of costing technique in which fixed and marginal

costs are written off as cost of product.

Marginal costing method- This costing technique is different from the absorption costing

method. Under this method both the costs are considered in a different way (Demski, 2013). The

fixed cost is considered as the period cost as well as variable cost is taken as unit cost.

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

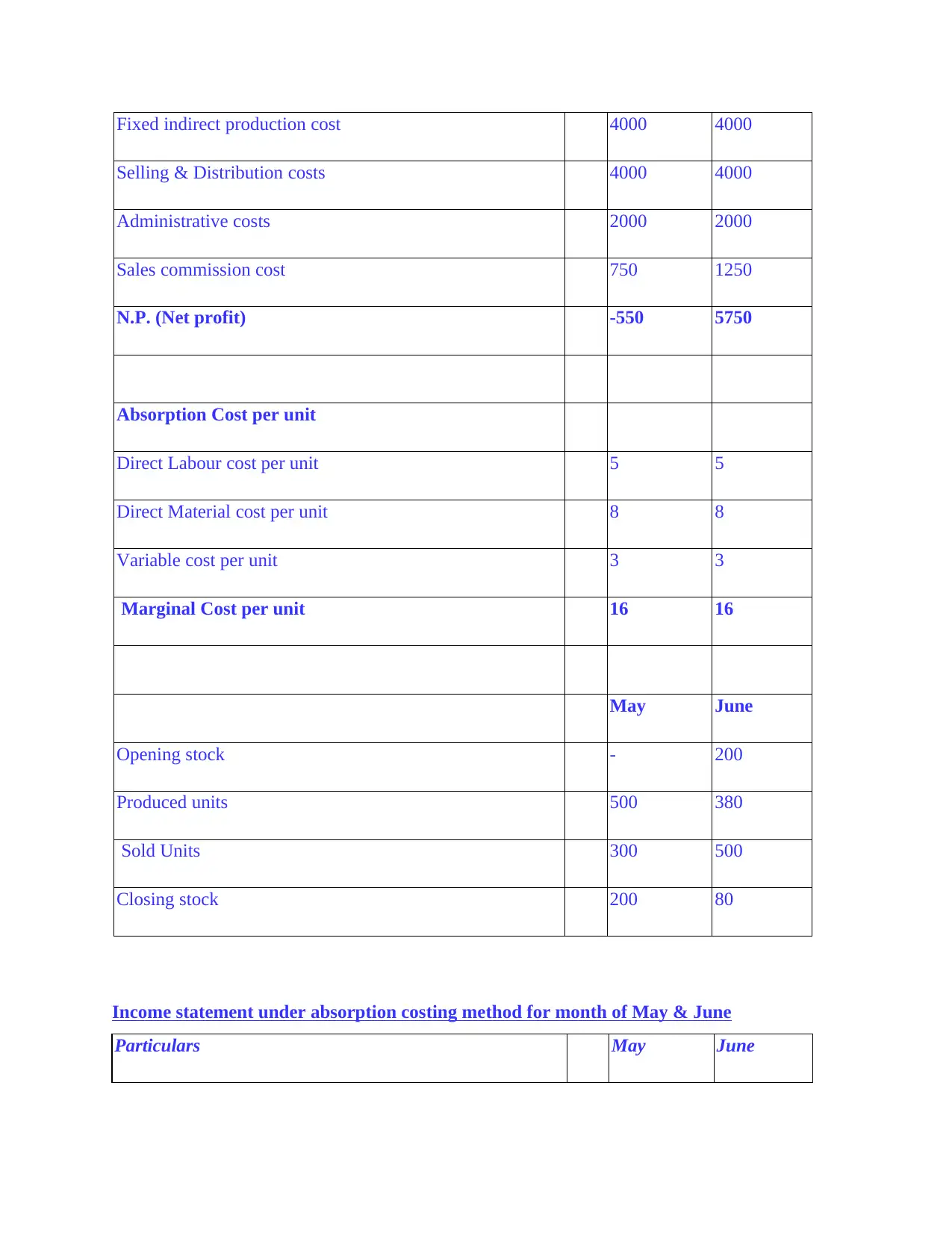

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Income statement under absorption costing method for month of May & June

Particulars May June

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Income statement under absorption costing method for month of May & June

Particulars May June

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

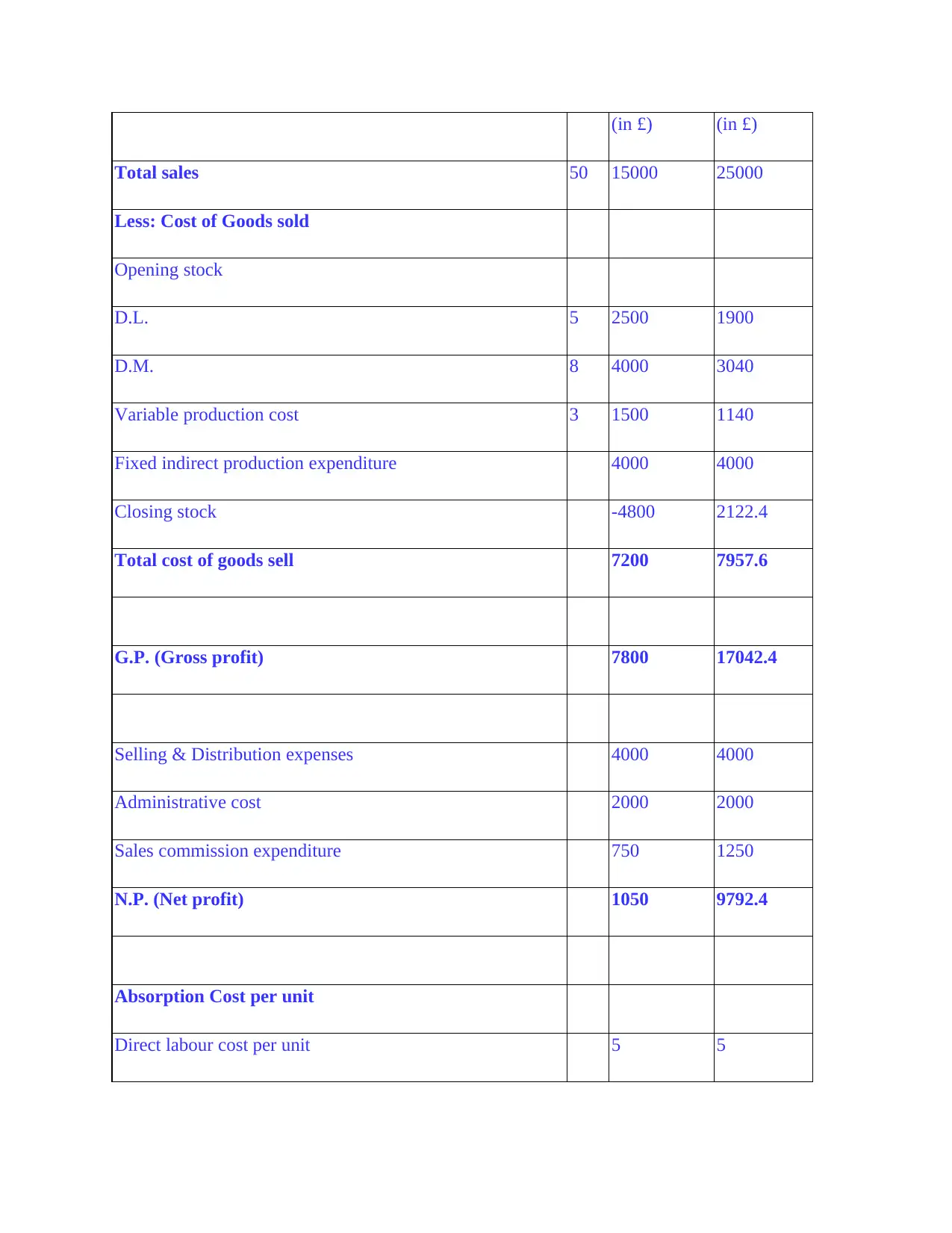

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

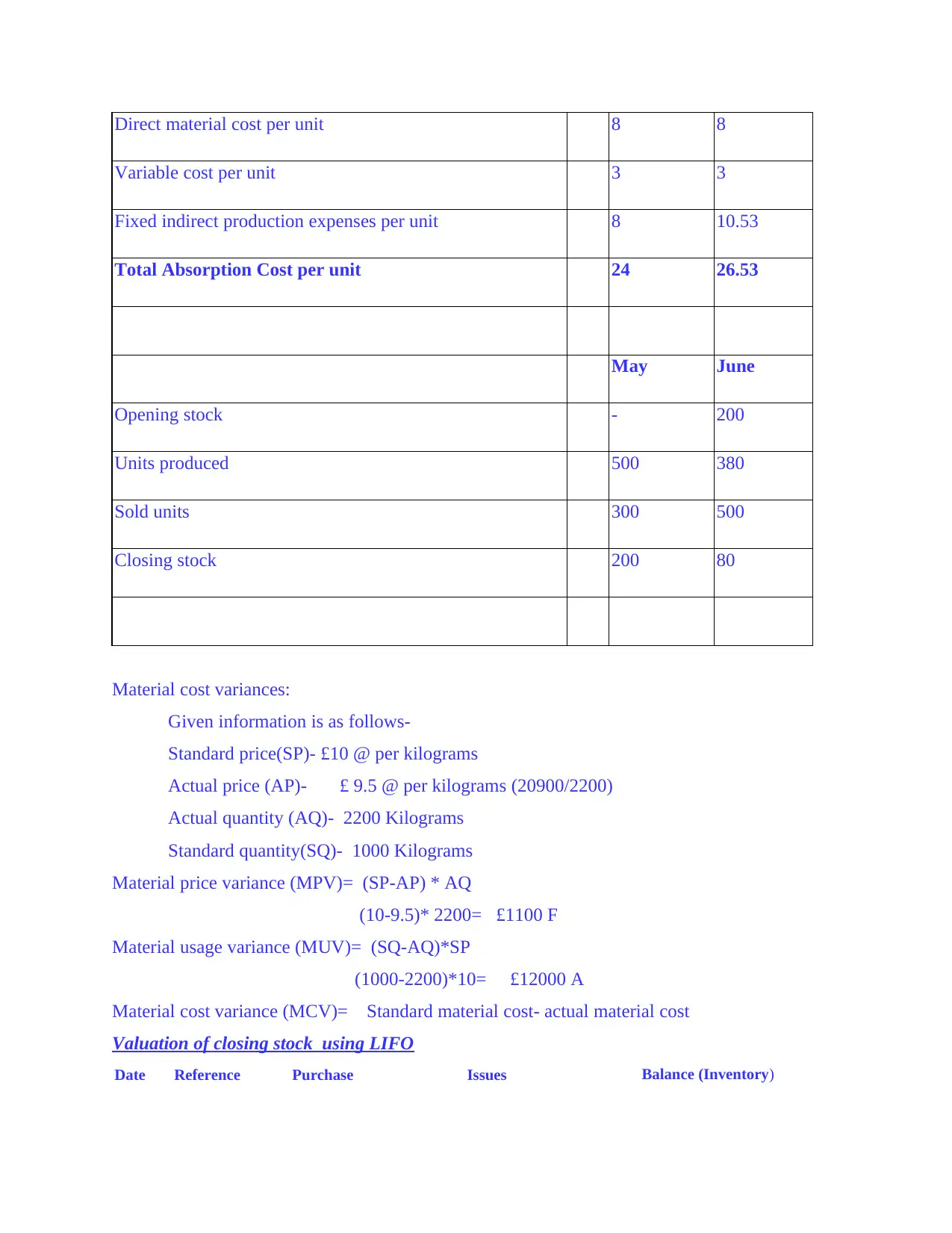

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

(10-9.5)* 2200= £1100 F

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

Valuation of closing stock using LIFO

Date Reference Purchase Issues Balance (Inventory)

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

(10-9.5)* 2200= £1100 F

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

Valuation of closing stock using LIFO

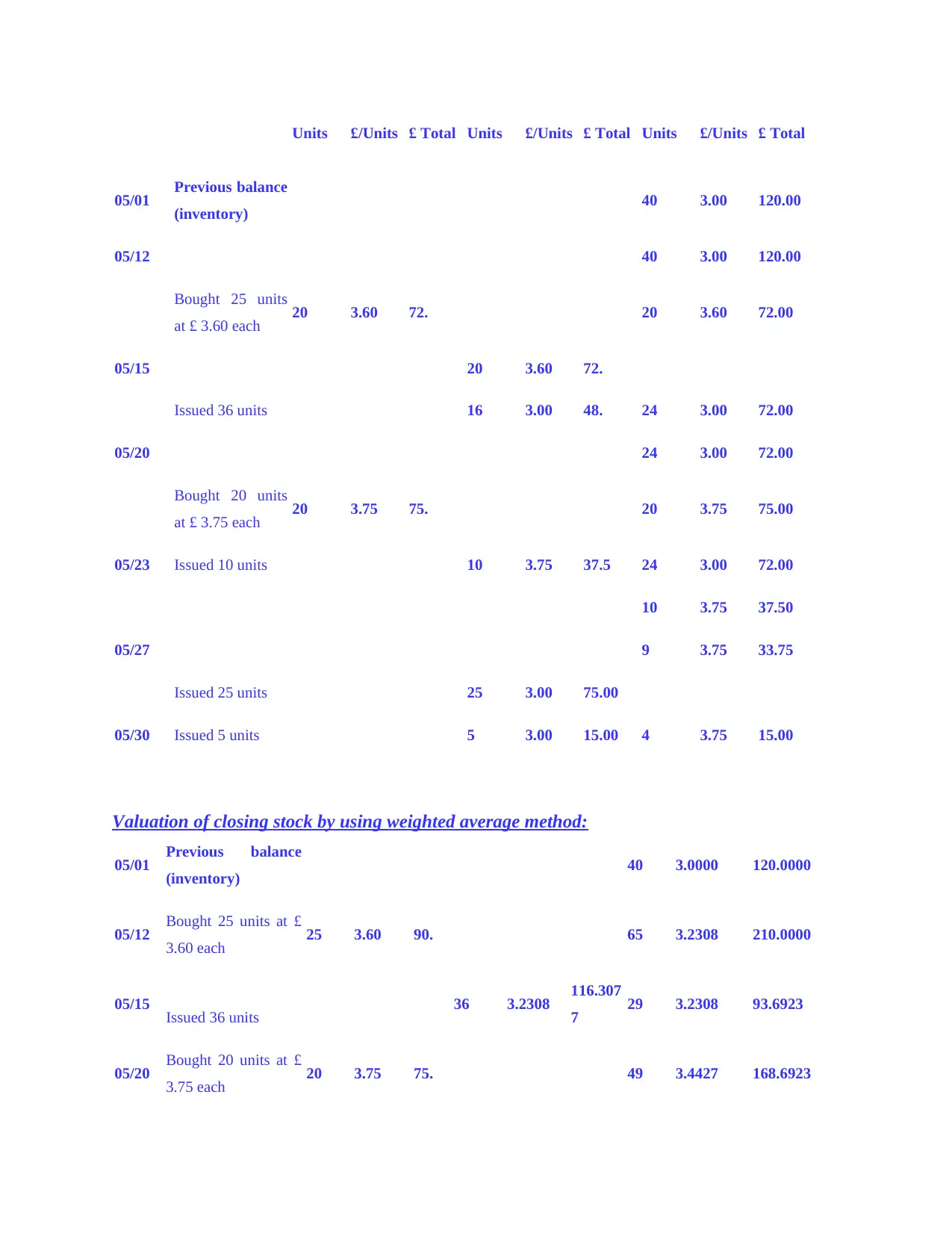

Date Reference Purchase Issues Balance (Inventory)

Units £/Units £ Total Units £/Units £ Total Units £/Units £ Total

05/01 Previous balance

(inventory) 40 3.00 120.00

05/12 40 3.00 120.00

Bought 25 units

at £ 3.60 each 20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units

at £ 3.75 each 20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.0000

05/12 Bought 25 units at £

3.60 each 25 3.60 90. 65 3.2308 210.0000

05/15 Issued 36 units 36 3.2308 116.307

7 29 3.2308 93.6923

05/20 Bought 20 units at £

3.75 each 20 3.75 75. 49 3.4427 168.6923

05/01 Previous balance

(inventory) 40 3.00 120.00

05/12 40 3.00 120.00

Bought 25 units

at £ 3.60 each 20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units

at £ 3.75 each 20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.0000

05/12 Bought 25 units at £

3.60 each 25 3.60 90. 65 3.2308 210.0000

05/15 Issued 36 units 36 3.2308 116.307

7 29 3.2308 93.6923

05/20 Bought 20 units at £

3.75 each 20 3.75 75. 49 3.4427 168.6923

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.