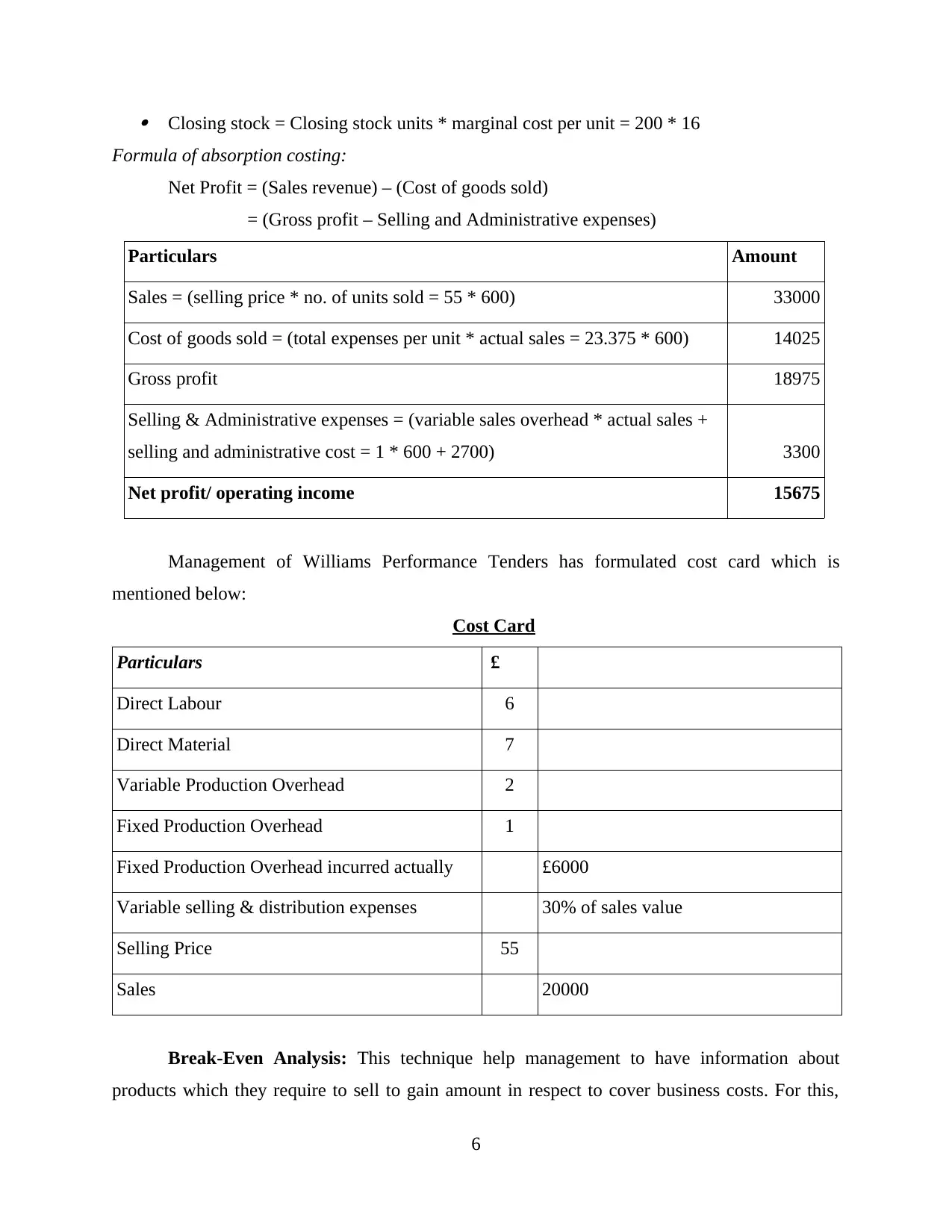

Management Accounting Report: Accounting Systems and Cost Analysis

VerifiedAdded on 2020/10/22

|18

|5435

|141

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their practical application within a business context, specifically using Williams Performance Tenders as a case study. The report begins by defining management accounting and its importance, differentiating it from other accounting systems, and exploring various management accounting systems such as inventory management, job costing, and cost accounting. It then delves into the benefits of these systems and their integration with organizational processes. The report further examines different methods used for management accounting reporting, including inventory and manufacturing reports, job cost reports, and performance reports. It also details cost calculation techniques, including fixed and variable costs, marginal costing, and absorption costing, with examples and working notes. The report also covers break-even analysis and planning tools for budgetary control, along with their advantages and disadvantages. Finally, the report addresses how management accounting systems can be adapted to respond to financial problems, highlighting how planning tools contribute to sustainable success. The report concludes with a discussion of the key findings and their implications for effective management accounting practices.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirement of different types of accounting

systems...................................................................................................................................1

P2 Different methods used for management accounting reporting........................................2

M1 Benefits of management accounting system and its application in organisation.............3

D1 Management accounting system and its reporting integration with organisational process. 4

TASK 2............................................................................................................................................4

P3 Calculate costs using appropriate techniques of cost analysis..........................................4

M2 Different types of accounting techniques to produce financial reporting documents.....8

D2 Financial report that accurately apply and interpret data for a range of business activities..8

TASK 3............................................................................................................................................9

P4 Advantage and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................9

M3 Applications of planning tools for preparing and forecasting budgets with its uses.....10

TASK 4..........................................................................................................................................11

P5 Adapting management accounting systems to respond to financial problems................11

M4 Management accounting lead organisation for sustainable success and financial problems

..............................................................................................................................................12

D3 Planning tools for accounting respond appropriately to resolve financial problems.....13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirement of different types of accounting

systems...................................................................................................................................1

P2 Different methods used for management accounting reporting........................................2

M1 Benefits of management accounting system and its application in organisation.............3

D1 Management accounting system and its reporting integration with organisational process. 4

TASK 2............................................................................................................................................4

P3 Calculate costs using appropriate techniques of cost analysis..........................................4

M2 Different types of accounting techniques to produce financial reporting documents.....8

D2 Financial report that accurately apply and interpret data for a range of business activities..8

TASK 3............................................................................................................................................9

P4 Advantage and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................9

M3 Applications of planning tools for preparing and forecasting budgets with its uses.....10

TASK 4..........................................................................................................................................11

P5 Adapting management accounting systems to respond to financial problems................11

M4 Management accounting lead organisation for sustainable success and financial problems

..............................................................................................................................................12

D3 Planning tools for accounting respond appropriately to resolve financial problems.....13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a procedure of preparing the accounts as well as reports which

give the timely and accurate statistical or financial information needed through managers to

make the short term and day- to- day decisions. It helps in analyse operations and business costs

in order to make internal financial report, account and records to assess process of decision

making of manager for attaining the business objectives. It is presentation of the accounting

information to prepare the effective policies and adopted through management and also help its

daily activities. Management accounting helps management of an organisation to perform all

functions consisting planning, staffing, organization, directing and also controlling. (Arroyo,

2012). This present report is based on Williams Performance Tenders. It is a boat manufacturer

business firm in Berinsfield. Under this given report will be discussed about management

accounting and its various kinds of management accounting systems. Benefits and limitations of

different kind of planning tool for the budgetary control will be discussed in mention assignment.

Planning tools which company used to solve the financial issues and lead business to sustainable

success will be given this report.

TASK 1

P1 Management accounting and essential requirement of different types of accounting systems

Management accounting refers to analysis, presentation, analysis, interpretation and

determination of accounting information that has been obtained through cost accounting and also

financial accounting. It helps the manager of company to prepare policies, conduct daily basis

operations and process of decision making of company. It is profession that consists the

partnering in devising planning, providing expertise, better decision making and also

performance management system in financial reporting and also control to help management in

develop and execution of strategy of company (Bodie, 2013). With the help of use management

accounting, Williams Performance Tenders can enhance its productivity along with

effectiveness. Thus, these are different management accounting system which are described

below:

Inventory management system: This system is related with management and

supervision of non-capitalized assets and stock of organisation. Williams Performance Tenders

provide boat to people, for which manager require to have sufficient material. For this, they

1

Management accounting is a procedure of preparing the accounts as well as reports which

give the timely and accurate statistical or financial information needed through managers to

make the short term and day- to- day decisions. It helps in analyse operations and business costs

in order to make internal financial report, account and records to assess process of decision

making of manager for attaining the business objectives. It is presentation of the accounting

information to prepare the effective policies and adopted through management and also help its

daily activities. Management accounting helps management of an organisation to perform all

functions consisting planning, staffing, organization, directing and also controlling. (Arroyo,

2012). This present report is based on Williams Performance Tenders. It is a boat manufacturer

business firm in Berinsfield. Under this given report will be discussed about management

accounting and its various kinds of management accounting systems. Benefits and limitations of

different kind of planning tool for the budgetary control will be discussed in mention assignment.

Planning tools which company used to solve the financial issues and lead business to sustainable

success will be given this report.

TASK 1

P1 Management accounting and essential requirement of different types of accounting systems

Management accounting refers to analysis, presentation, analysis, interpretation and

determination of accounting information that has been obtained through cost accounting and also

financial accounting. It helps the manager of company to prepare policies, conduct daily basis

operations and process of decision making of company. It is profession that consists the

partnering in devising planning, providing expertise, better decision making and also

performance management system in financial reporting and also control to help management in

develop and execution of strategy of company (Bodie, 2013). With the help of use management

accounting, Williams Performance Tenders can enhance its productivity along with

effectiveness. Thus, these are different management accounting system which are described

below:

Inventory management system: This system is related with management and

supervision of non-capitalized assets and stock of organisation. Williams Performance Tenders

provide boat to people, for which manager require to have sufficient material. For this, they

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maintain relations with suppliers which help top personnel to have flow of inventory in effective

manner. Along this, market forecast is conducted by management to have information about

future demands to arrange material in respect to order. Thus, firm's capital is utilised properly

and reduction of cost of storage and transportation.

Job costing system: It is a system which define that management monitor cost by

assigning manufacturing expenses to each item. For this, products require to be similar in nature

than only proper accounting of them are possible. In Williams Performance Tenders, manager

first find communicate with customers to have information about quality of material. Along this,

rates are also fixed so that production process are conducted accordingly. Thus, now superior

responsibility is to asses cost which are involved in preparation of product to reduce unnecessary

expenses and utilise money properly (Hillier, Grinblatt and Titman, 2011).

Cost accounting system: This is another system which define that management analyse

profitability of firm and inventory by computing expenses of product. Manager of Williams

Performance Tenders coordinate all departments to have accurate information about cost which

are involved in production of boat. This help them to implement appropriate equipment and tools

in system for providing quality product to customers. Along this, management is even able to

reduce unnecessary cost in manufacturing process.

P2 Different methods used for management accounting reporting

Management accounting reporting is process which is conducted by top personnel to have

accurate information about statistical and financial information of company. This help them to

make appropriate decisions in respect to short-term and day-to-day business operations. Williams

Performance Tenders is small firm, so manager require to have sufficient funds for setting up

appropriate outlet in market. For this, businessperson examine different sources from which they

can get money to expand business to increase customer base, thereby enhance sales volume and

profitability. Management conduct financial reports that are profit and loss, balance sheet to have

information about availability of funds (Abugalia, 2011). Besides this, other statements that are

cash flow, sales report, item cost are prepared which help manager to have knowledge about net

worth of firm. Thus, these are various tools which are used for management accounting reporting

which are described below:

Inventory and manufacturing reporting: This is report which is formulated in firms

which are conducting production activities. This help management to have information about

2

manner. Along this, market forecast is conducted by management to have information about

future demands to arrange material in respect to order. Thus, firm's capital is utilised properly

and reduction of cost of storage and transportation.

Job costing system: It is a system which define that management monitor cost by

assigning manufacturing expenses to each item. For this, products require to be similar in nature

than only proper accounting of them are possible. In Williams Performance Tenders, manager

first find communicate with customers to have information about quality of material. Along this,

rates are also fixed so that production process are conducted accordingly. Thus, now superior

responsibility is to asses cost which are involved in preparation of product to reduce unnecessary

expenses and utilise money properly (Hillier, Grinblatt and Titman, 2011).

Cost accounting system: This is another system which define that management analyse

profitability of firm and inventory by computing expenses of product. Manager of Williams

Performance Tenders coordinate all departments to have accurate information about cost which

are involved in production of boat. This help them to implement appropriate equipment and tools

in system for providing quality product to customers. Along this, management is even able to

reduce unnecessary cost in manufacturing process.

P2 Different methods used for management accounting reporting

Management accounting reporting is process which is conducted by top personnel to have

accurate information about statistical and financial information of company. This help them to

make appropriate decisions in respect to short-term and day-to-day business operations. Williams

Performance Tenders is small firm, so manager require to have sufficient funds for setting up

appropriate outlet in market. For this, businessperson examine different sources from which they

can get money to expand business to increase customer base, thereby enhance sales volume and

profitability. Management conduct financial reports that are profit and loss, balance sheet to have

information about availability of funds (Abugalia, 2011). Besides this, other statements that are

cash flow, sales report, item cost are prepared which help manager to have knowledge about net

worth of firm. Thus, these are various tools which are used for management accounting reporting

which are described below:

Inventory and manufacturing reporting: This is report which is formulated in firms

which are conducting production activities. This help management to have information about

2

inventory and manufacturing processes to execute business operations in effective manner. It is

an appropriate report for Williams Performance Tenders, as company is manufacturing boat. For

this, labour expenses, wastage related with inventory and per unit overhead cost are various

constituents of this report. These are components which help manager to identify improvement

opportunities in system in respecty to workers and departments. For this, comparison of different

assembly line to have appropriate information about functioining of system.

Job cost reporting: It is another type of report which is related with acknowledgement

of expenses, cost and revenue in respect to each job. Management conduct examination of

earning of each project, so that they are able to choose appropriate one (Humphrey and Miller,

2012). This help executive of Williams Performance Tenders to safe their efforts and funds from

getting wasted in less valuable projects. Along this, manager is also able to have information

about cost that are conducted while progress time to make project profitable for firm.

Performance reporting: This is form of report which is formulated by management to

have information about business activities. For this, difference between budgeted performance

and actual outcomes is made. This help manager of Williams Performance Tenders to have

information about deviations and issues that have occured while production time.

M1 Benefits of management accounting system and its application in organisation

Management accounting system Advantages

Inventory management system This system help manager of Williams

Performance Tenders to save money and time

by maintaining an accurate inventory orders.

Job costing system Management of Williams Performance Tenders

use this system to save their efforts and get

appropriate results about cost that are incurred

in manufacture activity.

Cost accounting system This system help management of Williams

Performance Tenders to have measure

efficiency of business activities, thereby make

changes in system accordingly. Along this,

manager is also able to formulate plan about

3

an appropriate report for Williams Performance Tenders, as company is manufacturing boat. For

this, labour expenses, wastage related with inventory and per unit overhead cost are various

constituents of this report. These are components which help manager to identify improvement

opportunities in system in respecty to workers and departments. For this, comparison of different

assembly line to have appropriate information about functioining of system.

Job cost reporting: It is another type of report which is related with acknowledgement

of expenses, cost and revenue in respect to each job. Management conduct examination of

earning of each project, so that they are able to choose appropriate one (Humphrey and Miller,

2012). This help executive of Williams Performance Tenders to safe their efforts and funds from

getting wasted in less valuable projects. Along this, manager is also able to have information

about cost that are conducted while progress time to make project profitable for firm.

Performance reporting: This is form of report which is formulated by management to

have information about business activities. For this, difference between budgeted performance

and actual outcomes is made. This help manager of Williams Performance Tenders to have

information about deviations and issues that have occured while production time.

M1 Benefits of management accounting system and its application in organisation

Management accounting system Advantages

Inventory management system This system help manager of Williams

Performance Tenders to save money and time

by maintaining an accurate inventory orders.

Job costing system Management of Williams Performance Tenders

use this system to save their efforts and get

appropriate results about cost that are incurred

in manufacture activity.

Cost accounting system This system help management of Williams

Performance Tenders to have measure

efficiency of business activities, thereby make

changes in system accordingly. Along this,

manager is also able to formulate plan about

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

operations to reduce expenses of production of

boat.

D1 Management accounting system and its reporting integration with organisational process

Type of reporting Integration with organisational process

Inventory management system Management of Williams Performance Tenders

enhance inventory orders by using appropriate

technologies in respect to maintenance of

record of material in respect to demand of

people (Basel, 2012).

Job Costing system In Williams Performance Tenders, manager

compute expenses which will be incurred in

production of boat to reduce and eliminate

unnecessary cost.

Cost accounting system Management of Williams Performance Tenders

is to have information about orders of people to

arrange material accordingly. Along this,

expenses for production of boat is also

ascertained by manager to keep prices

appropriate in according to demands of people.

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis

Cost refer to activity which is conducted by management to have information about

money value which are incurred for execution of business operations in firm. Each and every

organisation require to have sufficient funds for having adequate material and manpower for

deliver of appropriate items and services to people. In business, there are two forms of cost

which are fixed and variable which are described below:-

Fixed cost: This tactic include expenses which doesn't change for a certain output level

that are rent, depreciation and many other. It has direct connection with production process, as

both increase or decreases in respect to items manufactured.

4

boat.

D1 Management accounting system and its reporting integration with organisational process

Type of reporting Integration with organisational process

Inventory management system Management of Williams Performance Tenders

enhance inventory orders by using appropriate

technologies in respect to maintenance of

record of material in respect to demand of

people (Basel, 2012).

Job Costing system In Williams Performance Tenders, manager

compute expenses which will be incurred in

production of boat to reduce and eliminate

unnecessary cost.

Cost accounting system Management of Williams Performance Tenders

is to have information about orders of people to

arrange material accordingly. Along this,

expenses for production of boat is also

ascertained by manager to keep prices

appropriate in according to demands of people.

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis

Cost refer to activity which is conducted by management to have information about

money value which are incurred for execution of business operations in firm. Each and every

organisation require to have sufficient funds for having adequate material and manpower for

deliver of appropriate items and services to people. In business, there are two forms of cost

which are fixed and variable which are described below:-

Fixed cost: This tactic include expenses which doesn't change for a certain output level

that are rent, depreciation and many other. It has direct connection with production process, as

both increase or decreases in respect to items manufactured.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

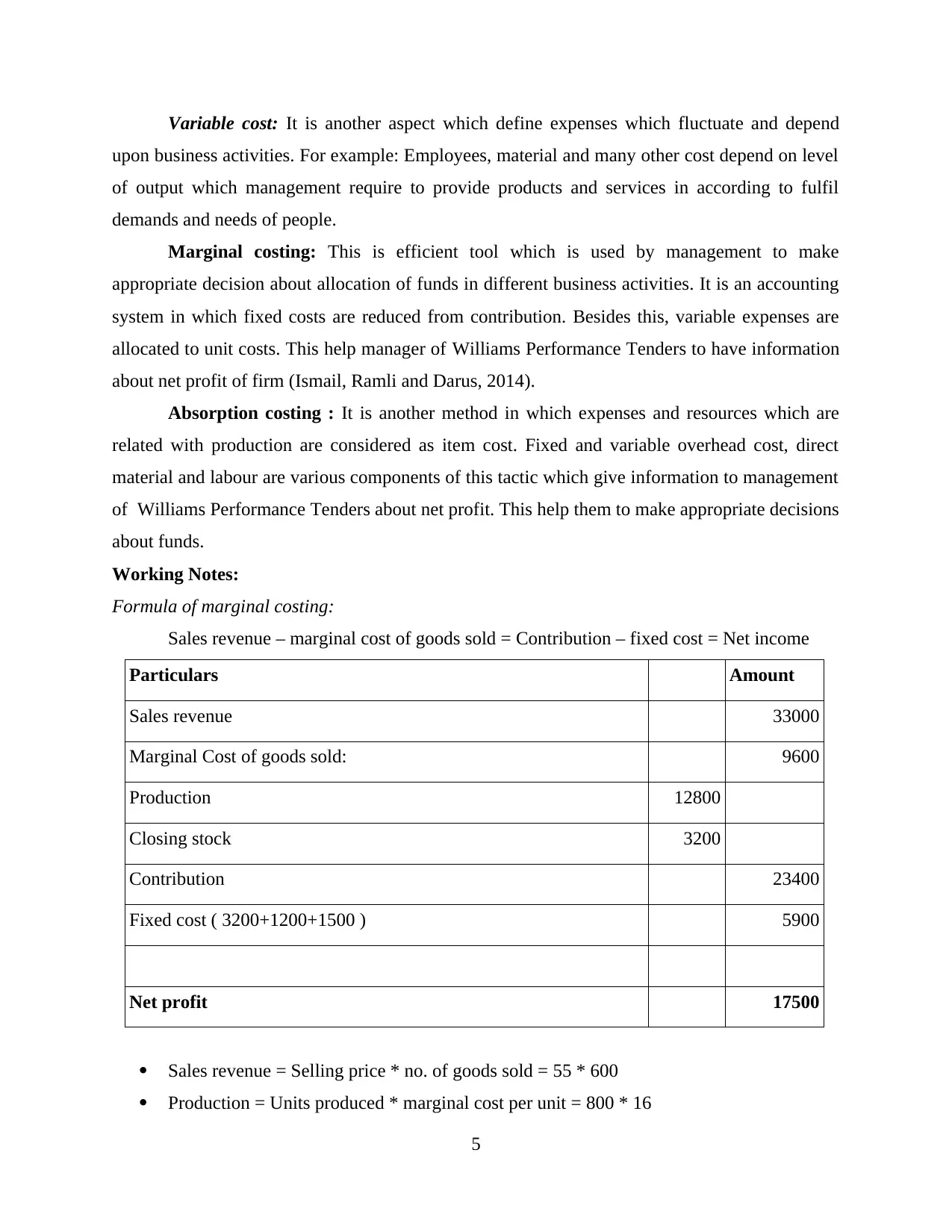

Variable cost: It is another aspect which define expenses which fluctuate and depend

upon business activities. For example: Employees, material and many other cost depend on level

of output which management require to provide products and services in according to fulfil

demands and needs of people.

Marginal costing: This is efficient tool which is used by management to make

appropriate decision about allocation of funds in different business activities. It is an accounting

system in which fixed costs are reduced from contribution. Besides this, variable expenses are

allocated to unit costs. This help manager of Williams Performance Tenders to have information

about net profit of firm (Ismail, Ramli and Darus, 2014).

Absorption costing : It is another method in which expenses and resources which are

related with production are considered as item cost. Fixed and variable overhead cost, direct

material and labour are various components of this tactic which give information to management

of Williams Performance Tenders about net profit. This help them to make appropriate decisions

about funds.

Working Notes:

Formula of marginal costing:

Sales revenue – marginal cost of goods sold = Contribution – fixed cost = Net income

Particulars Amount

Sales revenue 33000

Marginal Cost of goods sold: 9600

Production 12800

Closing stock 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Sales revenue = Selling price * no. of goods sold = 55 * 600

Production = Units produced * marginal cost per unit = 800 * 16

5

upon business activities. For example: Employees, material and many other cost depend on level

of output which management require to provide products and services in according to fulfil

demands and needs of people.

Marginal costing: This is efficient tool which is used by management to make

appropriate decision about allocation of funds in different business activities. It is an accounting

system in which fixed costs are reduced from contribution. Besides this, variable expenses are

allocated to unit costs. This help manager of Williams Performance Tenders to have information

about net profit of firm (Ismail, Ramli and Darus, 2014).

Absorption costing : It is another method in which expenses and resources which are

related with production are considered as item cost. Fixed and variable overhead cost, direct

material and labour are various components of this tactic which give information to management

of Williams Performance Tenders about net profit. This help them to make appropriate decisions

about funds.

Working Notes:

Formula of marginal costing:

Sales revenue – marginal cost of goods sold = Contribution – fixed cost = Net income

Particulars Amount

Sales revenue 33000

Marginal Cost of goods sold: 9600

Production 12800

Closing stock 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Sales revenue = Selling price * no. of goods sold = 55 * 600

Production = Units produced * marginal cost per unit = 800 * 16

5

Closing stock = Closing stock units * marginal cost per unit = 200 * 16

Formula of absorption costing:

Net Profit = (Sales revenue) – (Cost of goods sold)

= (Gross profit – Selling and Administrative expenses)

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Management of Williams Performance Tenders has formulated cost card which is

mentioned below:

Cost Card

Particulars £

Direct Labour 6

Direct Material 7

Variable Production Overhead 2

Fixed Production Overhead 1

Fixed Production Overhead incurred actually £6000

Variable selling & distribution expenses 30% of sales value

Selling Price 55

Sales 20000

Break-Even Analysis: This technique help management to have information about

products which they require to sell to gain amount in respect to cover business costs. For this,

6

Formula of absorption costing:

Net Profit = (Sales revenue) – (Cost of goods sold)

= (Gross profit – Selling and Administrative expenses)

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Management of Williams Performance Tenders has formulated cost card which is

mentioned below:

Cost Card

Particulars £

Direct Labour 6

Direct Material 7

Variable Production Overhead 2

Fixed Production Overhead 1

Fixed Production Overhead incurred actually £6000

Variable selling & distribution expenses 30% of sales value

Selling Price 55

Sales 20000

Break-Even Analysis: This technique help management to have information about

products which they require to sell to gain amount in respect to cover business costs. For this,

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

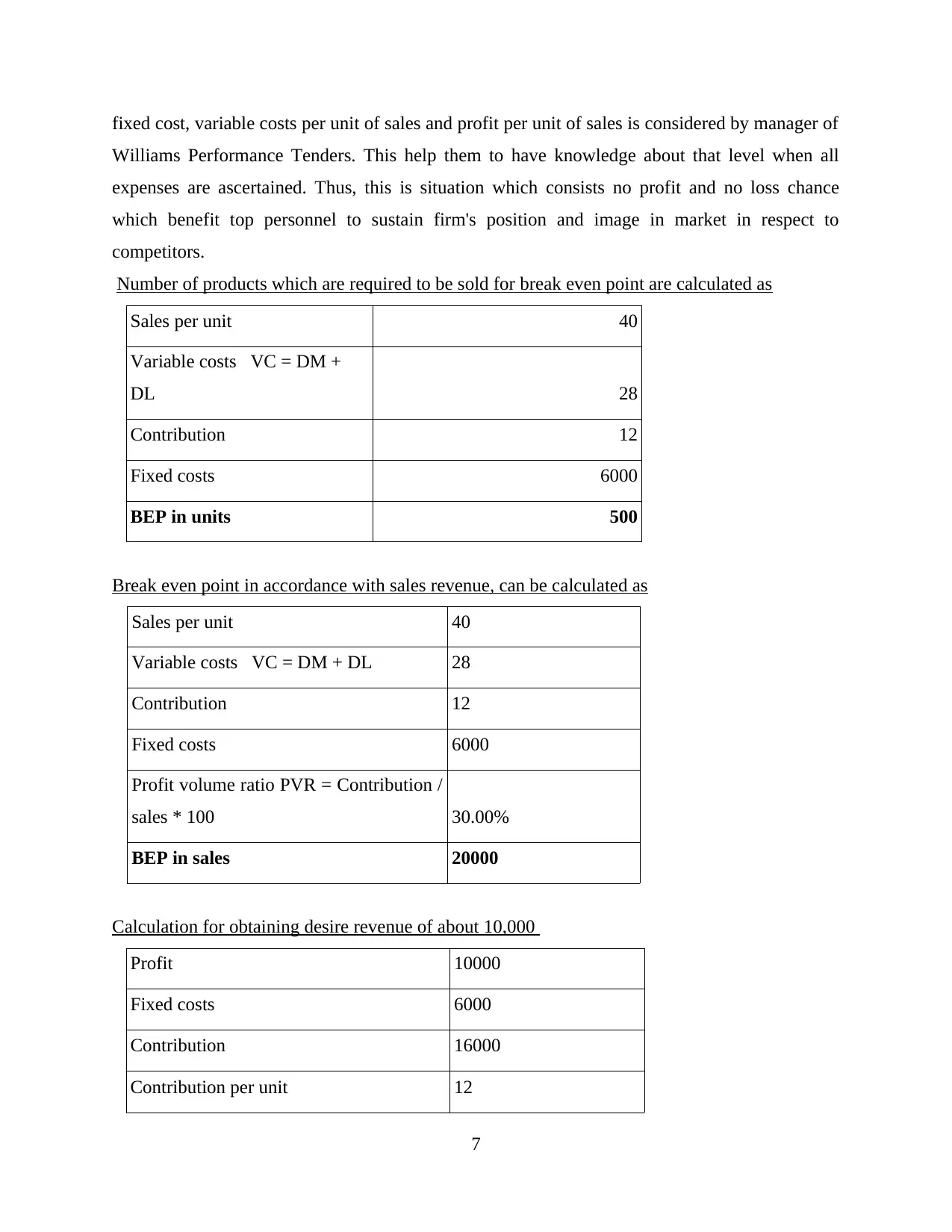

fixed cost, variable costs per unit of sales and profit per unit of sales is considered by manager of

Williams Performance Tenders. This help them to have knowledge about that level when all

expenses are ascertained. Thus, this is situation which consists no profit and no loss chance

which benefit top personnel to sustain firm's position and image in market in respect to

competitors.

Number of products which are required to be sold for break even point are calculated as

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

Break even point in accordance with sales revenue, can be calculated as

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

Calculation for obtaining desire revenue of about 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

7

Williams Performance Tenders. This help them to have knowledge about that level when all

expenses are ascertained. Thus, this is situation which consists no profit and no loss chance

which benefit top personnel to sustain firm's position and image in market in respect to

competitors.

Number of products which are required to be sold for break even point are calculated as

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

Break even point in accordance with sales revenue, can be calculated as

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

Calculation for obtaining desire revenue of about 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

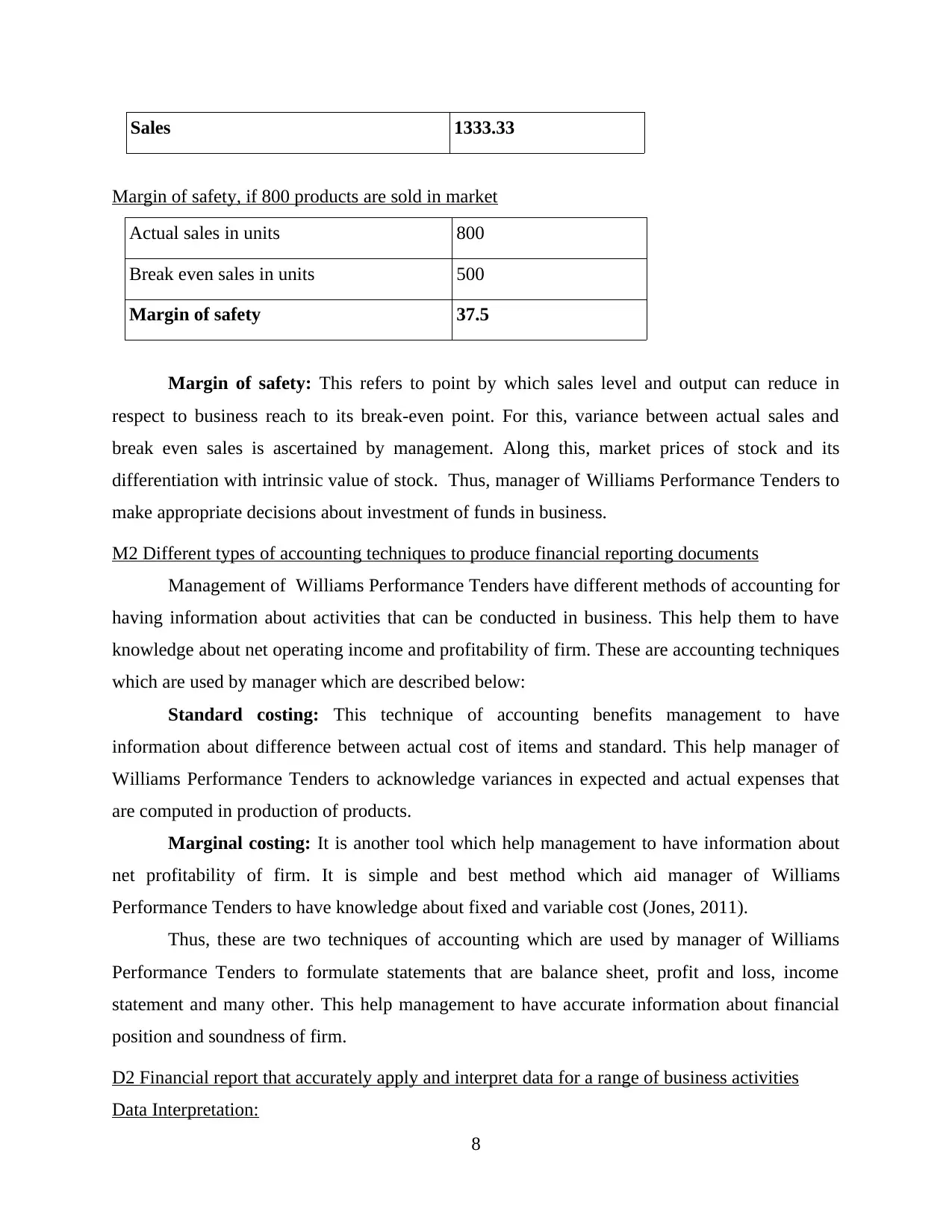

Sales 1333.33

Margin of safety, if 800 products are sold in market

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety: This refers to point by which sales level and output can reduce in

respect to business reach to its break-even point. For this, variance between actual sales and

break even sales is ascertained by management. Along this, market prices of stock and its

differentiation with intrinsic value of stock. Thus, manager of Williams Performance Tenders to

make appropriate decisions about investment of funds in business.

M2 Different types of accounting techniques to produce financial reporting documents

Management of Williams Performance Tenders have different methods of accounting for

having information about activities that can be conducted in business. This help them to have

knowledge about net operating income and profitability of firm. These are accounting techniques

which are used by manager which are described below:

Standard costing: This technique of accounting benefits management to have

information about difference between actual cost of items and standard. This help manager of

Williams Performance Tenders to acknowledge variances in expected and actual expenses that

are computed in production of products.

Marginal costing: It is another tool which help management to have information about

net profitability of firm. It is simple and best method which aid manager of Williams

Performance Tenders to have knowledge about fixed and variable cost (Jones, 2011).

Thus, these are two techniques of accounting which are used by manager of Williams

Performance Tenders to formulate statements that are balance sheet, profit and loss, income

statement and many other. This help management to have accurate information about financial

position and soundness of firm.

D2 Financial report that accurately apply and interpret data for a range of business activities

Data Interpretation:

8

Margin of safety, if 800 products are sold in market

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety: This refers to point by which sales level and output can reduce in

respect to business reach to its break-even point. For this, variance between actual sales and

break even sales is ascertained by management. Along this, market prices of stock and its

differentiation with intrinsic value of stock. Thus, manager of Williams Performance Tenders to

make appropriate decisions about investment of funds in business.

M2 Different types of accounting techniques to produce financial reporting documents

Management of Williams Performance Tenders have different methods of accounting for

having information about activities that can be conducted in business. This help them to have

knowledge about net operating income and profitability of firm. These are accounting techniques

which are used by manager which are described below:

Standard costing: This technique of accounting benefits management to have

information about difference between actual cost of items and standard. This help manager of

Williams Performance Tenders to acknowledge variances in expected and actual expenses that

are computed in production of products.

Marginal costing: It is another tool which help management to have information about

net profitability of firm. It is simple and best method which aid manager of Williams

Performance Tenders to have knowledge about fixed and variable cost (Jones, 2011).

Thus, these are two techniques of accounting which are used by manager of Williams

Performance Tenders to formulate statements that are balance sheet, profit and loss, income

statement and many other. This help management to have accurate information about financial

position and soundness of firm.

D2 Financial report that accurately apply and interpret data for a range of business activities

Data Interpretation:

8

From the above data, it is interpreted that marginal costing is technique which is used by

management of Williams Performance Tenders. This is an effective accounting method which

aid manager to have information about profitability of business. Net profit of company which is

computed through marginal costing is about £17500, while absorption technique result is

£15675. These are tools which define that difference in cost are due to fluctuations in variable

costs. Besides this, BEP analysis state that company require to sold 500 units to attain break-

even point of 20,000. Management earn around £10,000 of profit, for which sales of nearly 1333

units to be made by firm. Thus, this results in obtaining margin of safety of 37.5 when this

company sold 800 units.

TASK 3

P4 Advantage and disadvantages of different types of planning tools used for budgetary control

Budget planning tools which are used by management to predict, frame plan and manage

capital properly. It is essential that funds are properly utilised by top personnel for which they

formulate a budget that is allocate money in different business activities. This help them to

execute operations to attain targeted results and objectives. With technological advancements,

manager of Williams Performance Tenders shifted from traditional budgeting tools to cloud

based software. This help executive to maintain records appropriately which aid them to have

accurate knowledge about funds.

Budgetary control: This is a financial process which is conducted by management to

manage expenditures and income of organisation. For this, financial and performance goals in

respect to budget are set by top personnel. This help management to compare actual outcomes to

make adjustments in performance of firm to execute business activities in respect to market. This

technique is used by management of Williams Performance Tenders to keep track of financial

information of company. Thus, executive have knowledge about requirement of investments for

making alteration in system in according to future market situations (Christopher, 2016).

Manager of Williams Performance Tenders used budgetary control as an coordination

instrument. This tool help management to formulate plan for future that is set budget for each

and every business activity. By this, technique they are able to reduce wastage of funds and

enhance profitability. Thus, these are various budgetary control planning tools which are

described below:

9

management of Williams Performance Tenders. This is an effective accounting method which

aid manager to have information about profitability of business. Net profit of company which is

computed through marginal costing is about £17500, while absorption technique result is

£15675. These are tools which define that difference in cost are due to fluctuations in variable

costs. Besides this, BEP analysis state that company require to sold 500 units to attain break-

even point of 20,000. Management earn around £10,000 of profit, for which sales of nearly 1333

units to be made by firm. Thus, this results in obtaining margin of safety of 37.5 when this

company sold 800 units.

TASK 3

P4 Advantage and disadvantages of different types of planning tools used for budgetary control

Budget planning tools which are used by management to predict, frame plan and manage

capital properly. It is essential that funds are properly utilised by top personnel for which they

formulate a budget that is allocate money in different business activities. This help them to

execute operations to attain targeted results and objectives. With technological advancements,

manager of Williams Performance Tenders shifted from traditional budgeting tools to cloud

based software. This help executive to maintain records appropriately which aid them to have

accurate knowledge about funds.

Budgetary control: This is a financial process which is conducted by management to

manage expenditures and income of organisation. For this, financial and performance goals in

respect to budget are set by top personnel. This help management to compare actual outcomes to

make adjustments in performance of firm to execute business activities in respect to market. This

technique is used by management of Williams Performance Tenders to keep track of financial

information of company. Thus, executive have knowledge about requirement of investments for

making alteration in system in according to future market situations (Christopher, 2016).

Manager of Williams Performance Tenders used budgetary control as an coordination

instrument. This tool help management to formulate plan for future that is set budget for each

and every business activity. By this, technique they are able to reduce wastage of funds and

enhance profitability. Thus, these are various budgetary control planning tools which are

described below:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.