John Lewis Management Accounting: Financial Analysis and Risk Report

VerifiedAdded on 2020/07/23

|15

|4532

|85

Report

AI Summary

This report delves into the core principles of management accounting, emphasizing its significance in modern business operations. It explores various accounting systems, highlighting their role in organizing and analyzing financial transactions. The report provides a detailed examination of different accounting reports, including operational budgets, accounts receivable, and inventory management reports, and their impact on decision-making. Furthermore, it offers a comparative analysis of absorption and marginal costing techniques, illustrating their application in profit calculation. The report also addresses the importance of planning tools in budgetary control and discusses financial risks and their corresponding control measures. By providing a comprehensive overview of these key concepts, the report aims to equip readers with a solid understanding of management accounting and its practical applications. The report is a valuable resource for students seeking to enhance their knowledge of financial analysis and risk management.

MANAGEMENT

ACCOUNITNG

ACCOUNITNG

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

P1: Importance of management accounting and their various types of system use in an

organisation............................................................................................................................1

P2: Various accounting system reports .................................................................................3

P3 Calculation of profit by using absorption and marginal costing techniques.....................4

SECTION 2......................................................................................................................................7

P4: Advantage and disadvantage of using planning tools in order to control budget ...........7

P5: Different financial risk and their crucial control measures..............................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

P1: Importance of management accounting and their various types of system use in an

organisation............................................................................................................................1

P2: Various accounting system reports .................................................................................3

P3 Calculation of profit by using absorption and marginal costing techniques.....................4

SECTION 2......................................................................................................................................7

P4: Advantage and disadvantage of using planning tools in order to control budget ...........7

P5: Different financial risk and their crucial control measures..............................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is an essential aspect of every manufacturing business whether

small or large. They uses this in as primary tools for keeping their everyday business transactions

in well organise or systematic manner. The main motive of managers is to make effective plan so

that future aims and objectives can be attain in more easy and economical manner. Now a day’s

plenty of organisation are facing various issues associated with financial statements. They can be

resolve through using appropriate accounting and reporting systems (Abdelmoneim Mohamed

and Jones, 2014).

Understanding of different costing method which will be useful in evaluating net

profitability of an organisation. Further, this report is presenting various planning tools those are

being helpful in budgetary control. Apart from this, all those financial problems and its effective

measure to resolve them are discussed under this report. The overall project report, is providing

vital information about use of management accounting information those are assessing for the

betterment of an organisation.

SECTION 1

P1: Importance of management accounting and their various types of system use in an

organisation

In every manufacturing business, it is crucial to maintain their accounting detail in well

organise format so that proper detail information about actual gains and budgeted would be

analyse properly. The manager of John Lewis would hold responsible for making maximum

profit by using resources in effective ways. They need to take valuable decision regarding

increase their productivity as well as efficiency of the department (Management Accounting,

2017). Some other aspects for using accounting system regarding company’s partners such as

investors, shareholders, customer and so on. They are responsible for making crucial decision in

order to get positive results in coming time. By the help of using accounting system, it would

enable managers to focus on vital factors that should incur maximum gains to an organisation. It

is said to be an effective process of preparing management reports and accounts which will be

provide reliable and accurate financial and statistical information to concern managers of a

project (Akbar, 2010). There is various importance of using management accounting systems

those are discussed underneath:

1

Management accounting is an essential aspect of every manufacturing business whether

small or large. They uses this in as primary tools for keeping their everyday business transactions

in well organise or systematic manner. The main motive of managers is to make effective plan so

that future aims and objectives can be attain in more easy and economical manner. Now a day’s

plenty of organisation are facing various issues associated with financial statements. They can be

resolve through using appropriate accounting and reporting systems (Abdelmoneim Mohamed

and Jones, 2014).

Understanding of different costing method which will be useful in evaluating net

profitability of an organisation. Further, this report is presenting various planning tools those are

being helpful in budgetary control. Apart from this, all those financial problems and its effective

measure to resolve them are discussed under this report. The overall project report, is providing

vital information about use of management accounting information those are assessing for the

betterment of an organisation.

SECTION 1

P1: Importance of management accounting and their various types of system use in an

organisation

In every manufacturing business, it is crucial to maintain their accounting detail in well

organise format so that proper detail information about actual gains and budgeted would be

analyse properly. The manager of John Lewis would hold responsible for making maximum

profit by using resources in effective ways. They need to take valuable decision regarding

increase their productivity as well as efficiency of the department (Management Accounting,

2017). Some other aspects for using accounting system regarding company’s partners such as

investors, shareholders, customer and so on. They are responsible for making crucial decision in

order to get positive results in coming time. By the help of using accounting system, it would

enable managers to focus on vital factors that should incur maximum gains to an organisation. It

is said to be an effective process of preparing management reports and accounts which will be

provide reliable and accurate financial and statistical information to concern managers of a

project (Akbar, 2010). There is various importance of using management accounting systems

those are discussed underneath:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It would help in forecasting the future: A most crucial aspects for every business to

make appropriate forecasting which will assists in effective decision making and

searching for some useful information about the company. Like whether they are able to

invest in respect to generate maximum gains in coming time.

It will assists in making or buy decision: It happens to be one of the effective method

by which manufactures can make production of products as per the demand of customers.

Cost and productivity are the deciding aspects in this particular process of decision

making.

There are various types of management accounting system which would assists in the

betterment of an organisation. Those are being discussed underneath:

Cost accounting system: It is known as effective process of recoding, classifying and

summarising or evaluating alternative course of actions those are being used for the purpose of

controlling costs. Its primary motive is to advise owners on the most crucial action based on cost

efficiency and effectiveness (Belfo and Trigo, 2013).

Price optimisation system: Under this accounting system, a manager uses to make

numerical evaluation by a company to determine responses from customers about various prices

for its products and services. It is mostly used by the company to identify prices that John Lewis

Company has decided from their products.

Inventory management system: As per this system, manufacturing department can make

control over their opening and ending stock level during the year. This will help them to record

detail systematic detail of inventory position kept by the company. By this, managers can track

stock level, orders or any sales and deliveries. In production sector, this system is more effective

in creating a work order, bill of material and other important purpose. By the help of using

perfect stock management business can attain their target in more easy and fast manner.

Job costing system: This is valuable costing system which is useful in assigning production

costs to a single products or groups. Basically, the job order costing is mainly assessing only

when the products manufactured are relatively different from one another.

Benefits: It would deliver crucial benefits that set them from process costing. This system

delivers access the expenses those are incur on each job during production process.

2

make appropriate forecasting which will assists in effective decision making and

searching for some useful information about the company. Like whether they are able to

invest in respect to generate maximum gains in coming time.

It will assists in making or buy decision: It happens to be one of the effective method

by which manufactures can make production of products as per the demand of customers.

Cost and productivity are the deciding aspects in this particular process of decision

making.

There are various types of management accounting system which would assists in the

betterment of an organisation. Those are being discussed underneath:

Cost accounting system: It is known as effective process of recoding, classifying and

summarising or evaluating alternative course of actions those are being used for the purpose of

controlling costs. Its primary motive is to advise owners on the most crucial action based on cost

efficiency and effectiveness (Belfo and Trigo, 2013).

Price optimisation system: Under this accounting system, a manager uses to make

numerical evaluation by a company to determine responses from customers about various prices

for its products and services. It is mostly used by the company to identify prices that John Lewis

Company has decided from their products.

Inventory management system: As per this system, manufacturing department can make

control over their opening and ending stock level during the year. This will help them to record

detail systematic detail of inventory position kept by the company. By this, managers can track

stock level, orders or any sales and deliveries. In production sector, this system is more effective

in creating a work order, bill of material and other important purpose. By the help of using

perfect stock management business can attain their target in more easy and fast manner.

Job costing system: This is valuable costing system which is useful in assigning production

costs to a single products or groups. Basically, the job order costing is mainly assessing only

when the products manufactured are relatively different from one another.

Benefits: It would deliver crucial benefits that set them from process costing. This system

delivers access the expenses those are incur on each job during production process.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2: Various accounting system reports

In order to generate more accurate outcomes company need to make use of reporting

systems. This will be prepared by collected various information from each department those are

associated with the company either directly or indirectly. Reporting system is an essential aspect

for every business because it consists of systematic detail of various accounting information

which is being helpful in evaluating present position of the company. Every organisation needs

to prepare report of their daily operations which is being done while producing a products and

services. By the help of reporting system, it would provide maximum advantages to organisation

which can be utilised during planning, organising and assigning vital roles to an individual

(Becker, Ulrich and Staffel, 2011).

This will be done at both the level as such internal or external level so the better decision

would be made to make improvement of performance and growth of the company. There are

various types of accounting system reporting which will be assessing an organisation to make

recoding of their financial and non-financial transaction on regular basis. Several reports are

having their own role and importance that is been beneficial for up-liftment of organisation

reputation. It would also assess in maintain proper communication and coordination between

various departments of “John Lewis” company. Some of the reports are used from the purpose of

making future budgets and standard to deliver perfect directions to employees in order to

perform their activities in more effective manner. By the help of this budget they can easily be

able to accomplish their aims as well as organisation objectives at the same point of time. Some

of them are discuss below:

Operational budget report: According to this particular budget, it has been seen that

every detail information total cost and expenses those are incur by the company while producing

products and services. By the help of this report, managers can easily evaluate their total cost

investment made in producing units during the time (Eierle and Schultze, 2013).

Account receivable report: As per this report, company would be identification of their

total lists of unpaid customers and credit memos. The primary motive of using this report is to

determine total credit recovery time duration which is still outstanding or does not recover.

Through these data management can take crucial decision about any changes or modification in

their credit policies and to make stronger their collection procedures.

3

In order to generate more accurate outcomes company need to make use of reporting

systems. This will be prepared by collected various information from each department those are

associated with the company either directly or indirectly. Reporting system is an essential aspect

for every business because it consists of systematic detail of various accounting information

which is being helpful in evaluating present position of the company. Every organisation needs

to prepare report of their daily operations which is being done while producing a products and

services. By the help of reporting system, it would provide maximum advantages to organisation

which can be utilised during planning, organising and assigning vital roles to an individual

(Becker, Ulrich and Staffel, 2011).

This will be done at both the level as such internal or external level so the better decision

would be made to make improvement of performance and growth of the company. There are

various types of accounting system reporting which will be assessing an organisation to make

recoding of their financial and non-financial transaction on regular basis. Several reports are

having their own role and importance that is been beneficial for up-liftment of organisation

reputation. It would also assess in maintain proper communication and coordination between

various departments of “John Lewis” company. Some of the reports are used from the purpose of

making future budgets and standard to deliver perfect directions to employees in order to

perform their activities in more effective manner. By the help of this budget they can easily be

able to accomplish their aims as well as organisation objectives at the same point of time. Some

of them are discuss below:

Operational budget report: According to this particular budget, it has been seen that

every detail information total cost and expenses those are incur by the company while producing

products and services. By the help of this report, managers can easily evaluate their total cost

investment made in producing units during the time (Eierle and Schultze, 2013).

Account receivable report: As per this report, company would be identification of their

total lists of unpaid customers and credit memos. The primary motive of using this report is to

determine total credit recovery time duration which is still outstanding or does not recover.

Through these data management can take crucial decision about any changes or modification in

their credit policies and to make stronger their collection procedures.

3

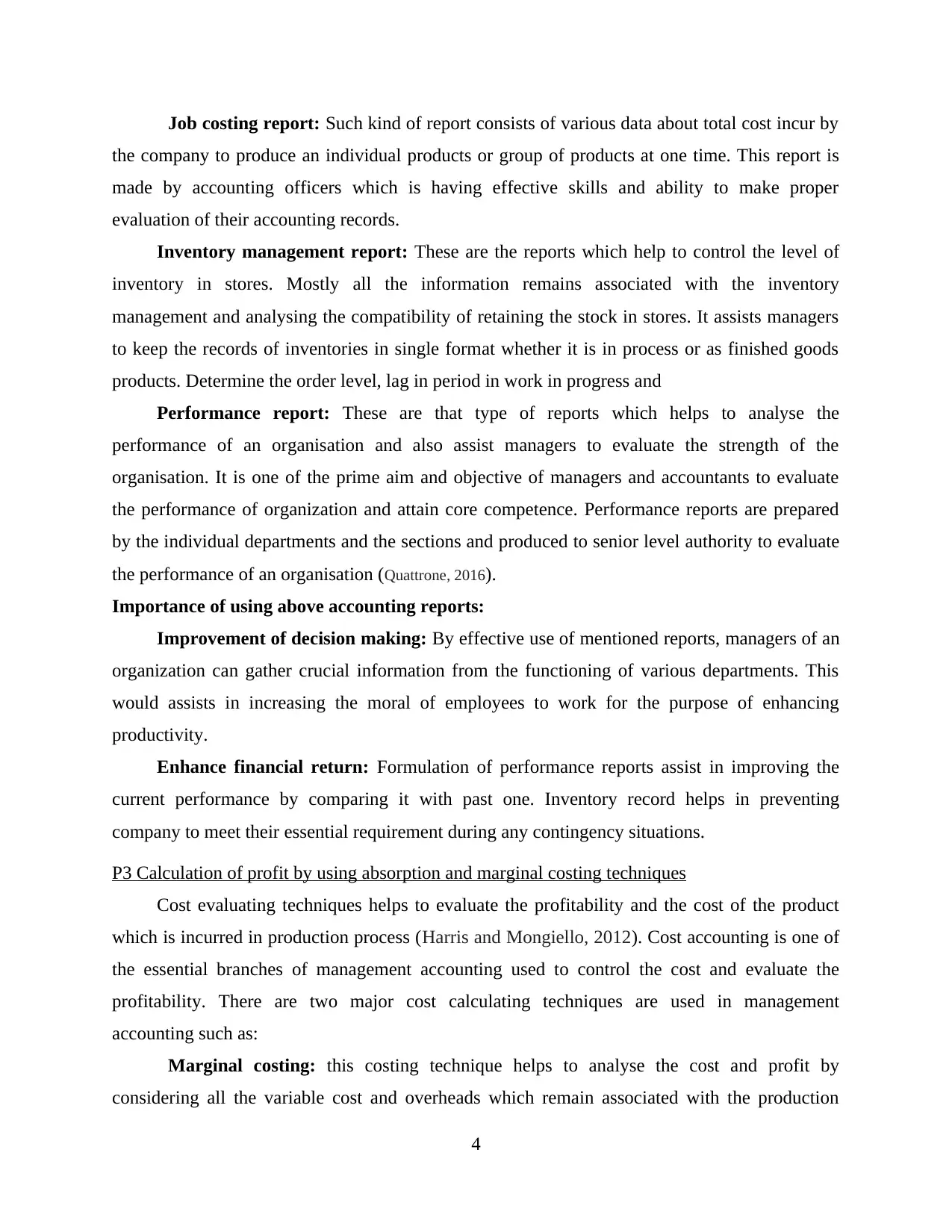

Job costing report: Such kind of report consists of various data about total cost incur by

the company to produce an individual products or group of products at one time. This report is

made by accounting officers which is having effective skills and ability to make proper

evaluation of their accounting records.

Inventory management report: These are the reports which help to control the level of

inventory in stores. Mostly all the information remains associated with the inventory

management and analysing the compatibility of retaining the stock in stores. It assists managers

to keep the records of inventories in single format whether it is in process or as finished goods

products. Determine the order level, lag in period in work in progress and

Performance report: These are that type of reports which helps to analyse the

performance of an organisation and also assist managers to evaluate the strength of the

organisation. It is one of the prime aim and objective of managers and accountants to evaluate

the performance of organization and attain core competence. Performance reports are prepared

by the individual departments and the sections and produced to senior level authority to evaluate

the performance of an organisation (Quattrone, 2016).

Importance of using above accounting reports:

Improvement of decision making: By effective use of mentioned reports, managers of an

organization can gather crucial information from the functioning of various departments. This

would assists in increasing the moral of employees to work for the purpose of enhancing

productivity.

Enhance financial return: Formulation of performance reports assist in improving the

current performance by comparing it with past one. Inventory record helps in preventing

company to meet their essential requirement during any contingency situations.

P3 Calculation of profit by using absorption and marginal costing techniques

Cost evaluating techniques helps to evaluate the profitability and the cost of the product

which is incurred in production process (Harris and Mongiello, 2012). Cost accounting is one of

the essential branches of management accounting used to control the cost and evaluate the

profitability. There are two major cost calculating techniques are used in management

accounting such as:

Marginal costing: this costing technique helps to analyse the cost and profit by

considering all the variable cost and overheads which remain associated with the production

4

the company to produce an individual products or group of products at one time. This report is

made by accounting officers which is having effective skills and ability to make proper

evaluation of their accounting records.

Inventory management report: These are the reports which help to control the level of

inventory in stores. Mostly all the information remains associated with the inventory

management and analysing the compatibility of retaining the stock in stores. It assists managers

to keep the records of inventories in single format whether it is in process or as finished goods

products. Determine the order level, lag in period in work in progress and

Performance report: These are that type of reports which helps to analyse the

performance of an organisation and also assist managers to evaluate the strength of the

organisation. It is one of the prime aim and objective of managers and accountants to evaluate

the performance of organization and attain core competence. Performance reports are prepared

by the individual departments and the sections and produced to senior level authority to evaluate

the performance of an organisation (Quattrone, 2016).

Importance of using above accounting reports:

Improvement of decision making: By effective use of mentioned reports, managers of an

organization can gather crucial information from the functioning of various departments. This

would assists in increasing the moral of employees to work for the purpose of enhancing

productivity.

Enhance financial return: Formulation of performance reports assist in improving the

current performance by comparing it with past one. Inventory record helps in preventing

company to meet their essential requirement during any contingency situations.

P3 Calculation of profit by using absorption and marginal costing techniques

Cost evaluating techniques helps to evaluate the profitability and the cost of the product

which is incurred in production process (Harris and Mongiello, 2012). Cost accounting is one of

the essential branches of management accounting used to control the cost and evaluate the

profitability. There are two major cost calculating techniques are used in management

accounting such as:

Marginal costing: this costing technique helps to analyse the cost and profit by

considering all the variable cost and overheads which remain associated with the production

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

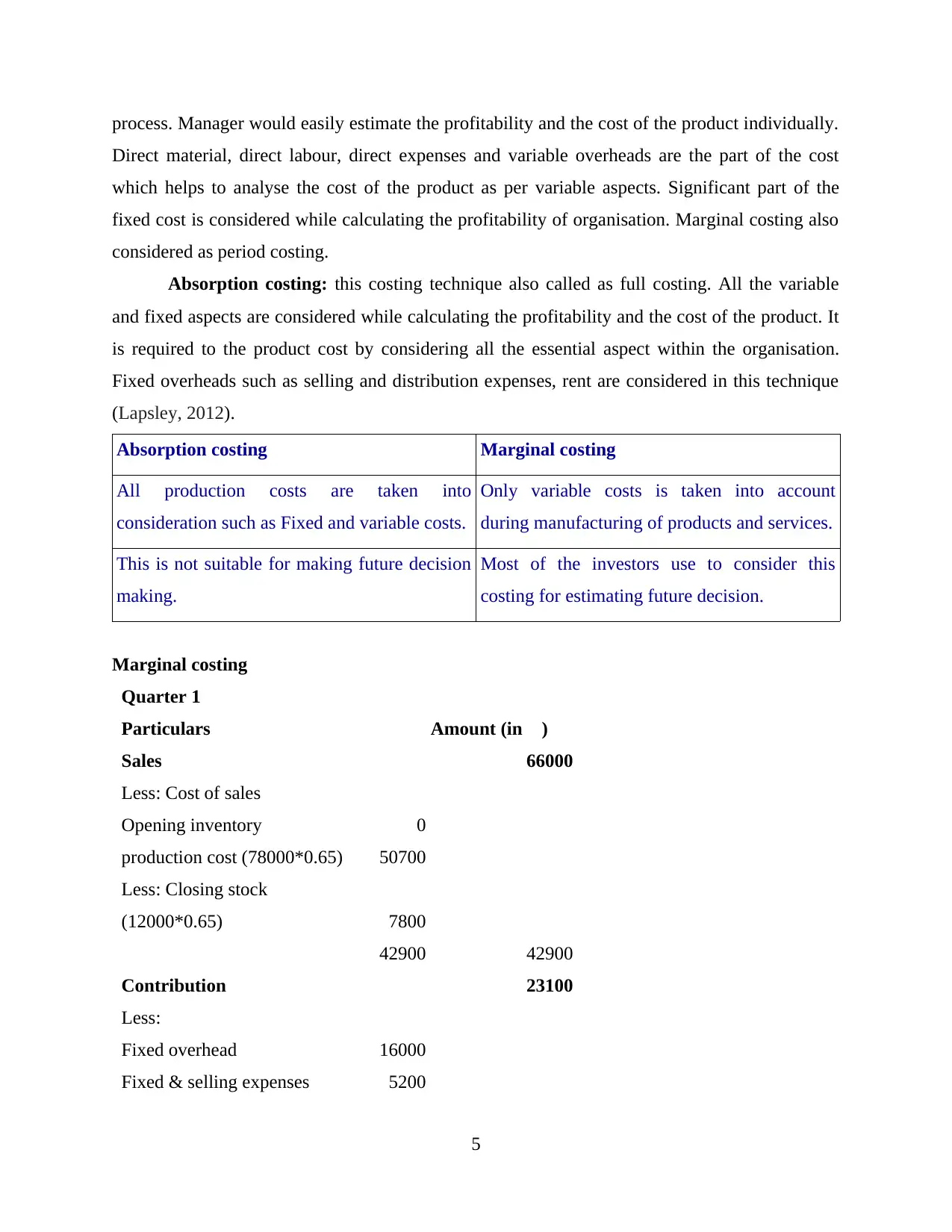

process. Manager would easily estimate the profitability and the cost of the product individually.

Direct material, direct labour, direct expenses and variable overheads are the part of the cost

which helps to analyse the cost of the product as per variable aspects. Significant part of the

fixed cost is considered while calculating the profitability of organisation. Marginal costing also

considered as period costing.

Absorption costing: this costing technique also called as full costing. All the variable

and fixed aspects are considered while calculating the profitability and the cost of the product. It

is required to the product cost by considering all the essential aspect within the organisation.

Fixed overheads such as selling and distribution expenses, rent are considered in this technique

(Lapsley, 2012).

Absorption costing Marginal costing

All production costs are taken into

consideration such as Fixed and variable costs.

Only variable costs is taken into account

during manufacturing of products and services.

This is not suitable for making future decision

making.

Most of the investors use to consider this

costing for estimating future decision.

Marginal costing

Quarter 1

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

5

Direct material, direct labour, direct expenses and variable overheads are the part of the cost

which helps to analyse the cost of the product as per variable aspects. Significant part of the

fixed cost is considered while calculating the profitability of organisation. Marginal costing also

considered as period costing.

Absorption costing: this costing technique also called as full costing. All the variable

and fixed aspects are considered while calculating the profitability and the cost of the product. It

is required to the product cost by considering all the essential aspect within the organisation.

Fixed overheads such as selling and distribution expenses, rent are considered in this technique

(Lapsley, 2012).

Absorption costing Marginal costing

All production costs are taken into

consideration such as Fixed and variable costs.

Only variable costs is taken into account

during manufacturing of products and services.

This is not suitable for making future decision

making.

Most of the investors use to consider this

costing for estimating future decision.

Marginal costing

Quarter 1

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

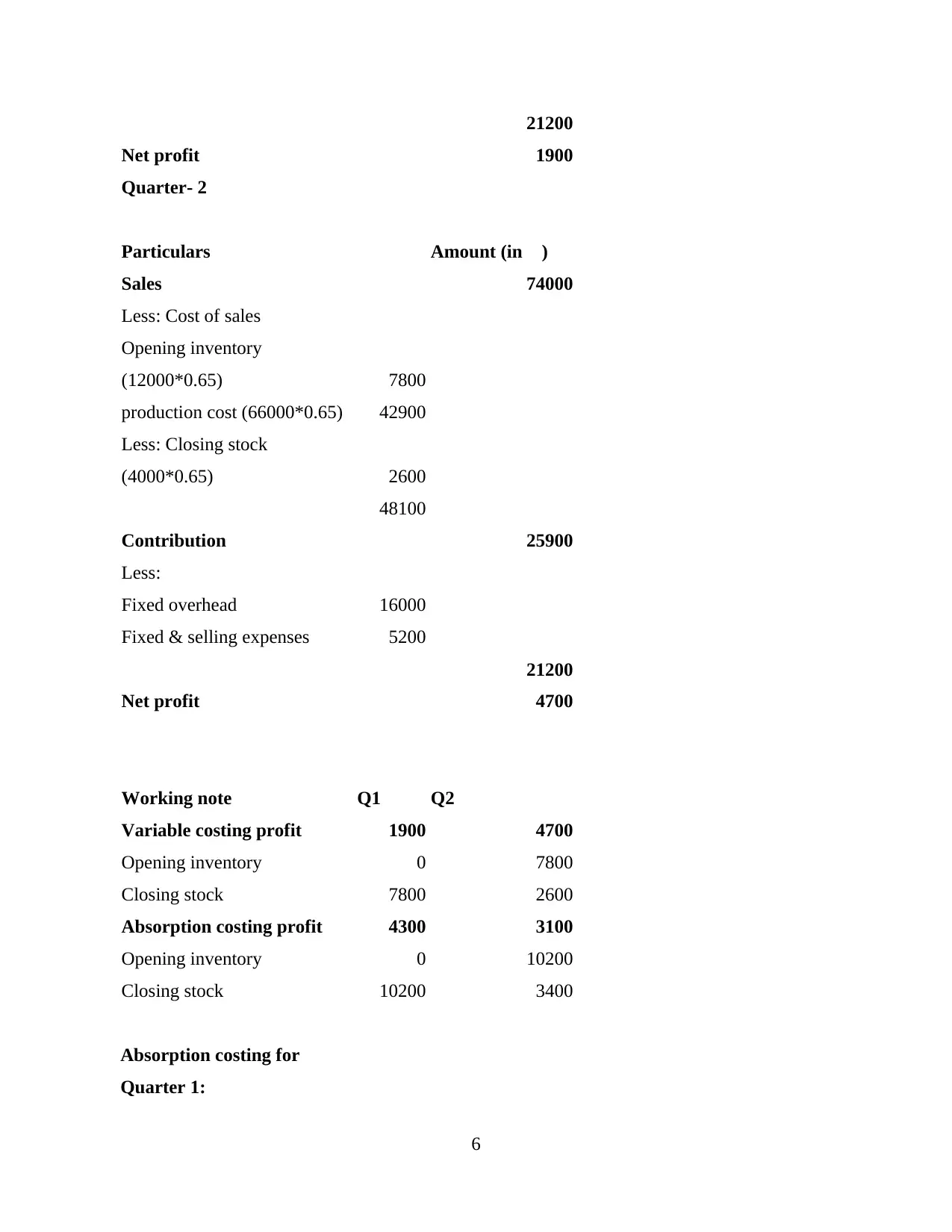

21200

Net profit 1900

Quarter- 2

Particulars Amount (in £)

Sales 74000

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Absorption costing for

Quarter 1:

6

Net profit 1900

Quarter- 2

Particulars Amount (in £)

Sales 74000

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Absorption costing for

Quarter 1:

6

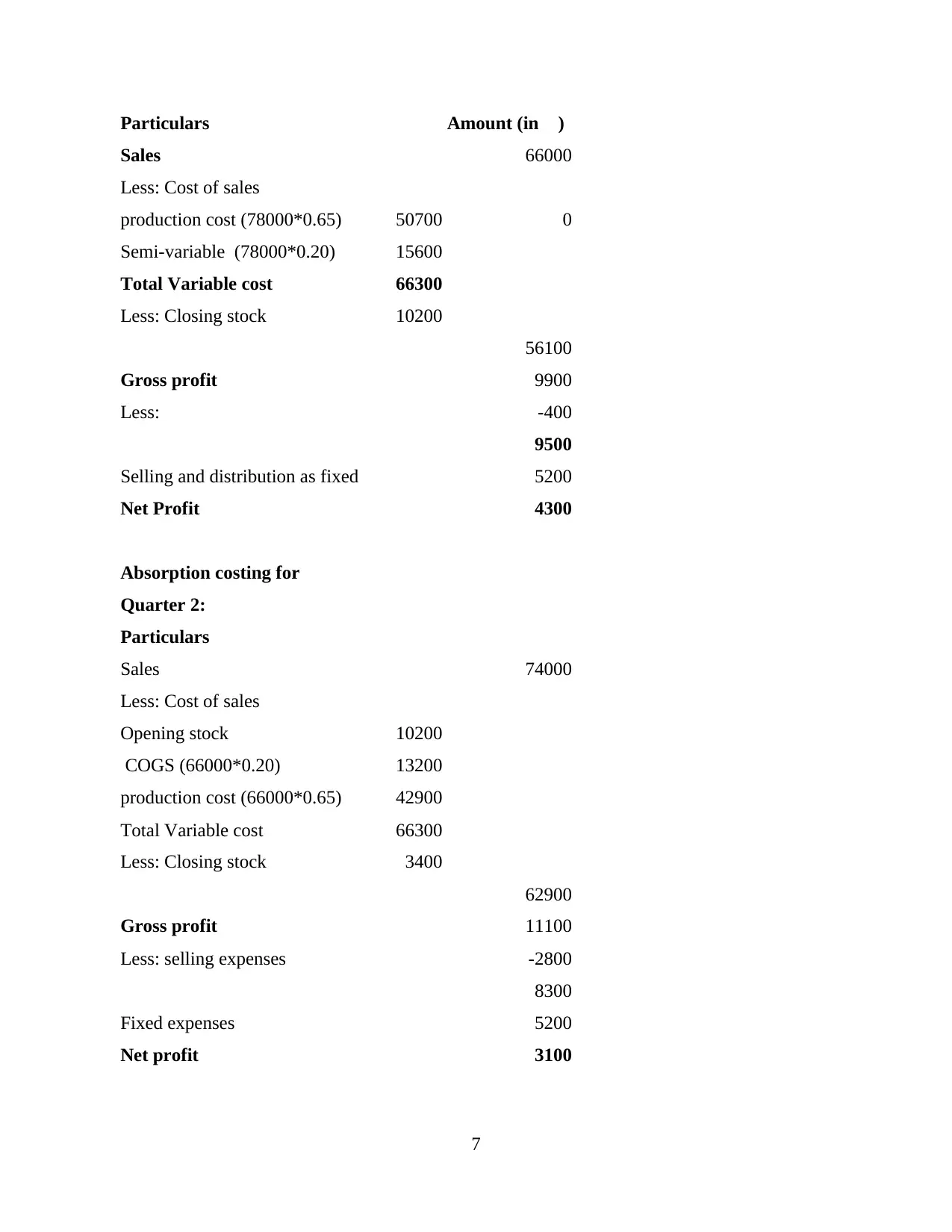

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for

Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

7

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for

Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

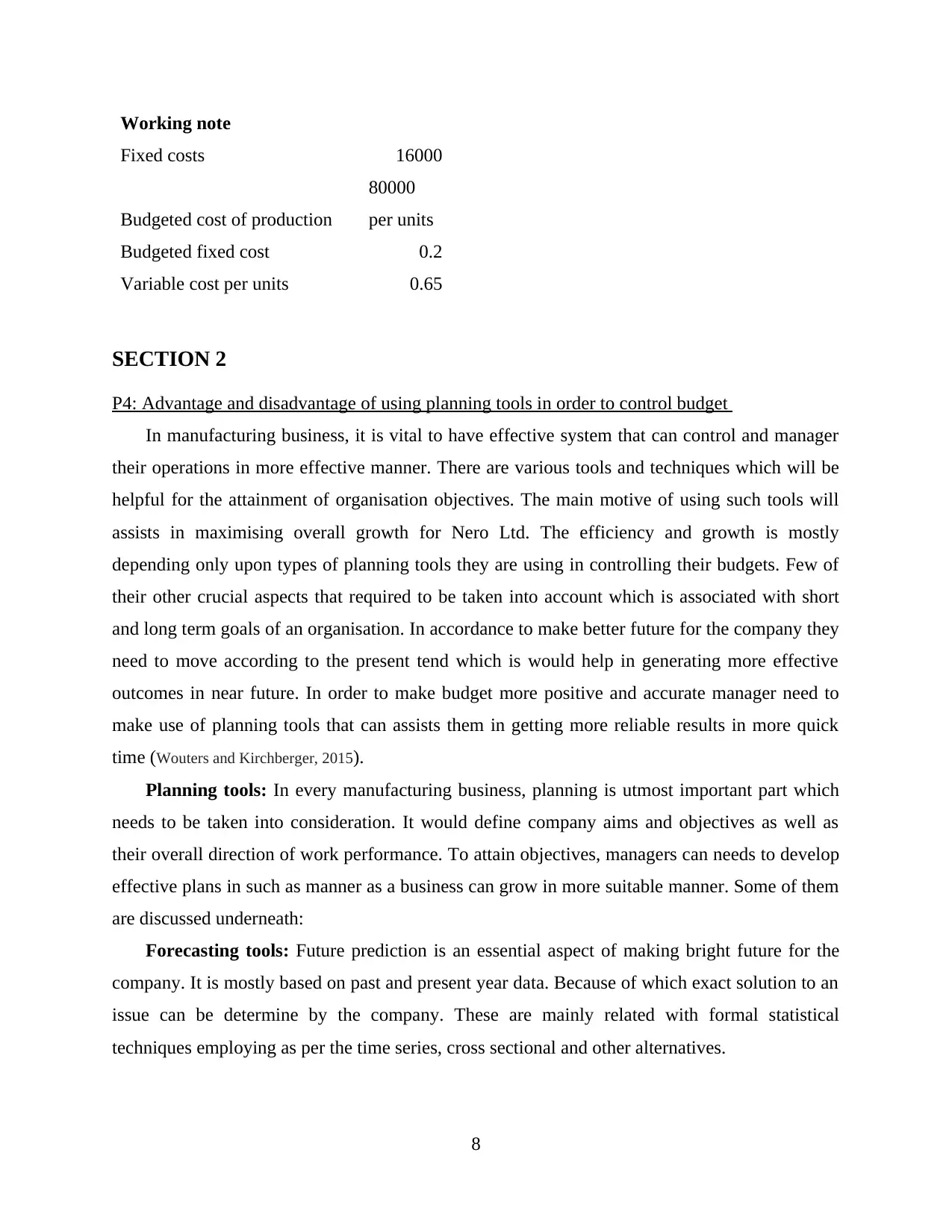

Working note

Fixed costs 16000

Budgeted cost of production

80000

per units

Budgeted fixed cost 0.2

Variable cost per units 0.65

SECTION 2

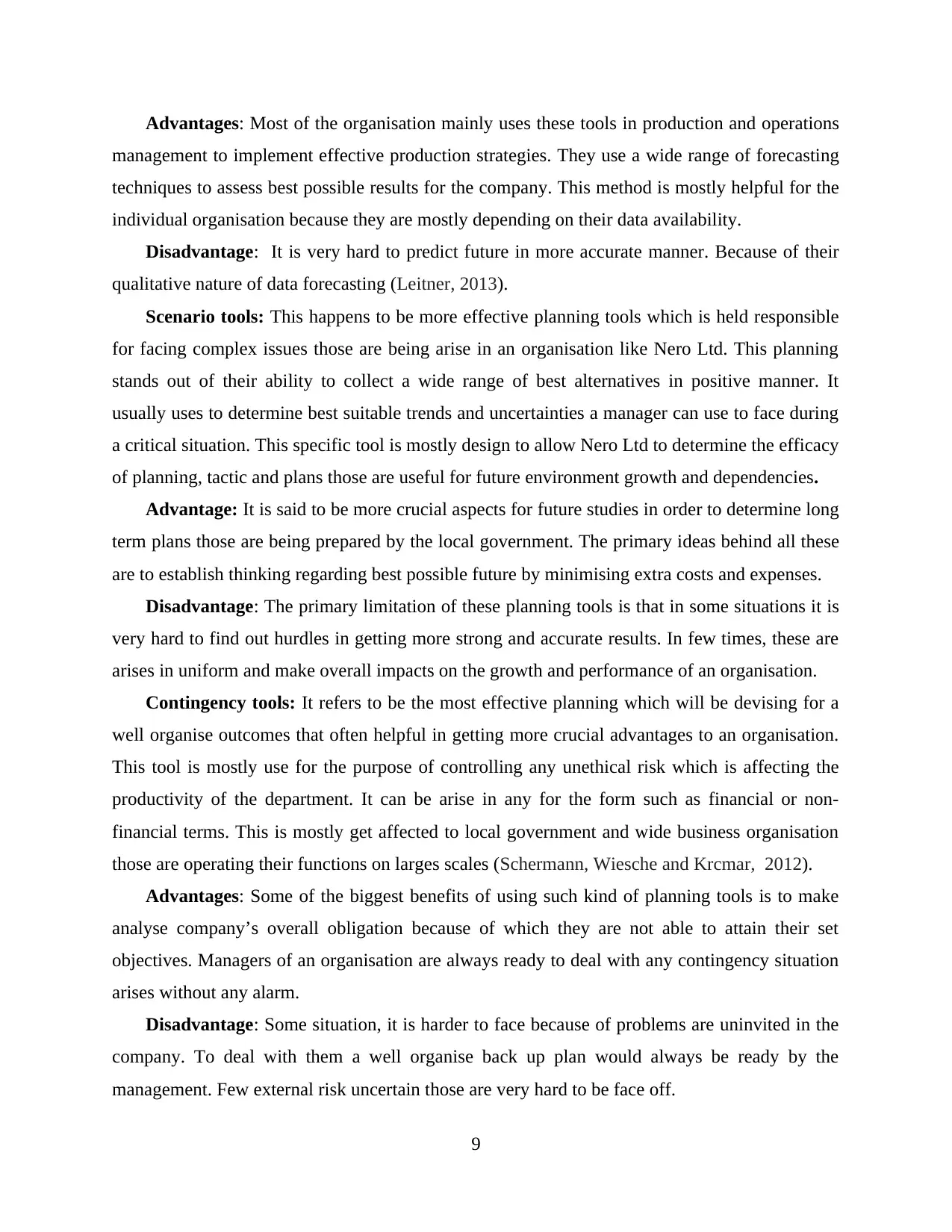

P4: Advantage and disadvantage of using planning tools in order to control budget

In manufacturing business, it is vital to have effective system that can control and manager

their operations in more effective manner. There are various tools and techniques which will be

helpful for the attainment of organisation objectives. The main motive of using such tools will

assists in maximising overall growth for Nero Ltd. The efficiency and growth is mostly

depending only upon types of planning tools they are using in controlling their budgets. Few of

their other crucial aspects that required to be taken into account which is associated with short

and long term goals of an organisation. In accordance to make better future for the company they

need to move according to the present tend which is would help in generating more effective

outcomes in near future. In order to make budget more positive and accurate manager need to

make use of planning tools that can assists them in getting more reliable results in more quick

time (Wouters and Kirchberger, 2015).

Planning tools: In every manufacturing business, planning is utmost important part which

needs to be taken into consideration. It would define company aims and objectives as well as

their overall direction of work performance. To attain objectives, managers can needs to develop

effective plans in such as manner as a business can grow in more suitable manner. Some of them

are discussed underneath:

Forecasting tools: Future prediction is an essential aspect of making bright future for the

company. It is mostly based on past and present year data. Because of which exact solution to an

issue can be determine by the company. These are mainly related with formal statistical

techniques employing as per the time series, cross sectional and other alternatives.

8

Fixed costs 16000

Budgeted cost of production

80000

per units

Budgeted fixed cost 0.2

Variable cost per units 0.65

SECTION 2

P4: Advantage and disadvantage of using planning tools in order to control budget

In manufacturing business, it is vital to have effective system that can control and manager

their operations in more effective manner. There are various tools and techniques which will be

helpful for the attainment of organisation objectives. The main motive of using such tools will

assists in maximising overall growth for Nero Ltd. The efficiency and growth is mostly

depending only upon types of planning tools they are using in controlling their budgets. Few of

their other crucial aspects that required to be taken into account which is associated with short

and long term goals of an organisation. In accordance to make better future for the company they

need to move according to the present tend which is would help in generating more effective

outcomes in near future. In order to make budget more positive and accurate manager need to

make use of planning tools that can assists them in getting more reliable results in more quick

time (Wouters and Kirchberger, 2015).

Planning tools: In every manufacturing business, planning is utmost important part which

needs to be taken into consideration. It would define company aims and objectives as well as

their overall direction of work performance. To attain objectives, managers can needs to develop

effective plans in such as manner as a business can grow in more suitable manner. Some of them

are discussed underneath:

Forecasting tools: Future prediction is an essential aspect of making bright future for the

company. It is mostly based on past and present year data. Because of which exact solution to an

issue can be determine by the company. These are mainly related with formal statistical

techniques employing as per the time series, cross sectional and other alternatives.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages: Most of the organisation mainly uses these tools in production and operations

management to implement effective production strategies. They use a wide range of forecasting

techniques to assess best possible results for the company. This method is mostly helpful for the

individual organisation because they are mostly depending on their data availability.

Disadvantage: It is very hard to predict future in more accurate manner. Because of their

qualitative nature of data forecasting (Leitner, 2013).

Scenario tools: This happens to be more effective planning tools which is held responsible

for facing complex issues those are being arise in an organisation like Nero Ltd. This planning

stands out of their ability to collect a wide range of best alternatives in positive manner. It

usually uses to determine best suitable trends and uncertainties a manager can use to face during

a critical situation. This specific tool is mostly design to allow Nero Ltd to determine the efficacy

of planning, tactic and plans those are useful for future environment growth and dependencies.

Advantage: It is said to be more crucial aspects for future studies in order to determine long

term plans those are being prepared by the local government. The primary ideas behind all these

are to establish thinking regarding best possible future by minimising extra costs and expenses.

Disadvantage: The primary limitation of these planning tools is that in some situations it is

very hard to find out hurdles in getting more strong and accurate results. In few times, these are

arises in uniform and make overall impacts on the growth and performance of an organisation.

Contingency tools: It refers to be the most effective planning which will be devising for a

well organise outcomes that often helpful in getting more crucial advantages to an organisation.

This tool is mostly use for the purpose of controlling any unethical risk which is affecting the

productivity of the department. It can be arise in any for the form such as financial or non-

financial terms. This is mostly get affected to local government and wide business organisation

those are operating their functions on larges scales (Schermann, Wiesche and Krcmar, 2012).

Advantages: Some of the biggest benefits of using such kind of planning tools is to make

analyse company’s overall obligation because of which they are not able to attain their set

objectives. Managers of an organisation are always ready to deal with any contingency situation

arises without any alarm.

Disadvantage: Some situation, it is harder to face because of problems are uninvited in the

company. To deal with them a well organise back up plan would always be ready by the

management. Few external risk uncertain those are very hard to be face off.

9

management to implement effective production strategies. They use a wide range of forecasting

techniques to assess best possible results for the company. This method is mostly helpful for the

individual organisation because they are mostly depending on their data availability.

Disadvantage: It is very hard to predict future in more accurate manner. Because of their

qualitative nature of data forecasting (Leitner, 2013).

Scenario tools: This happens to be more effective planning tools which is held responsible

for facing complex issues those are being arise in an organisation like Nero Ltd. This planning

stands out of their ability to collect a wide range of best alternatives in positive manner. It

usually uses to determine best suitable trends and uncertainties a manager can use to face during

a critical situation. This specific tool is mostly design to allow Nero Ltd to determine the efficacy

of planning, tactic and plans those are useful for future environment growth and dependencies.

Advantage: It is said to be more crucial aspects for future studies in order to determine long

term plans those are being prepared by the local government. The primary ideas behind all these

are to establish thinking regarding best possible future by minimising extra costs and expenses.

Disadvantage: The primary limitation of these planning tools is that in some situations it is

very hard to find out hurdles in getting more strong and accurate results. In few times, these are

arises in uniform and make overall impacts on the growth and performance of an organisation.

Contingency tools: It refers to be the most effective planning which will be devising for a

well organise outcomes that often helpful in getting more crucial advantages to an organisation.

This tool is mostly use for the purpose of controlling any unethical risk which is affecting the

productivity of the department. It can be arise in any for the form such as financial or non-

financial terms. This is mostly get affected to local government and wide business organisation

those are operating their functions on larges scales (Schermann, Wiesche and Krcmar, 2012).

Advantages: Some of the biggest benefits of using such kind of planning tools is to make

analyse company’s overall obligation because of which they are not able to attain their set

objectives. Managers of an organisation are always ready to deal with any contingency situation

arises without any alarm.

Disadvantage: Some situation, it is harder to face because of problems are uninvited in the

company. To deal with them a well organise back up plan would always be ready by the

management. Few external risk uncertain those are very hard to be face off.

9

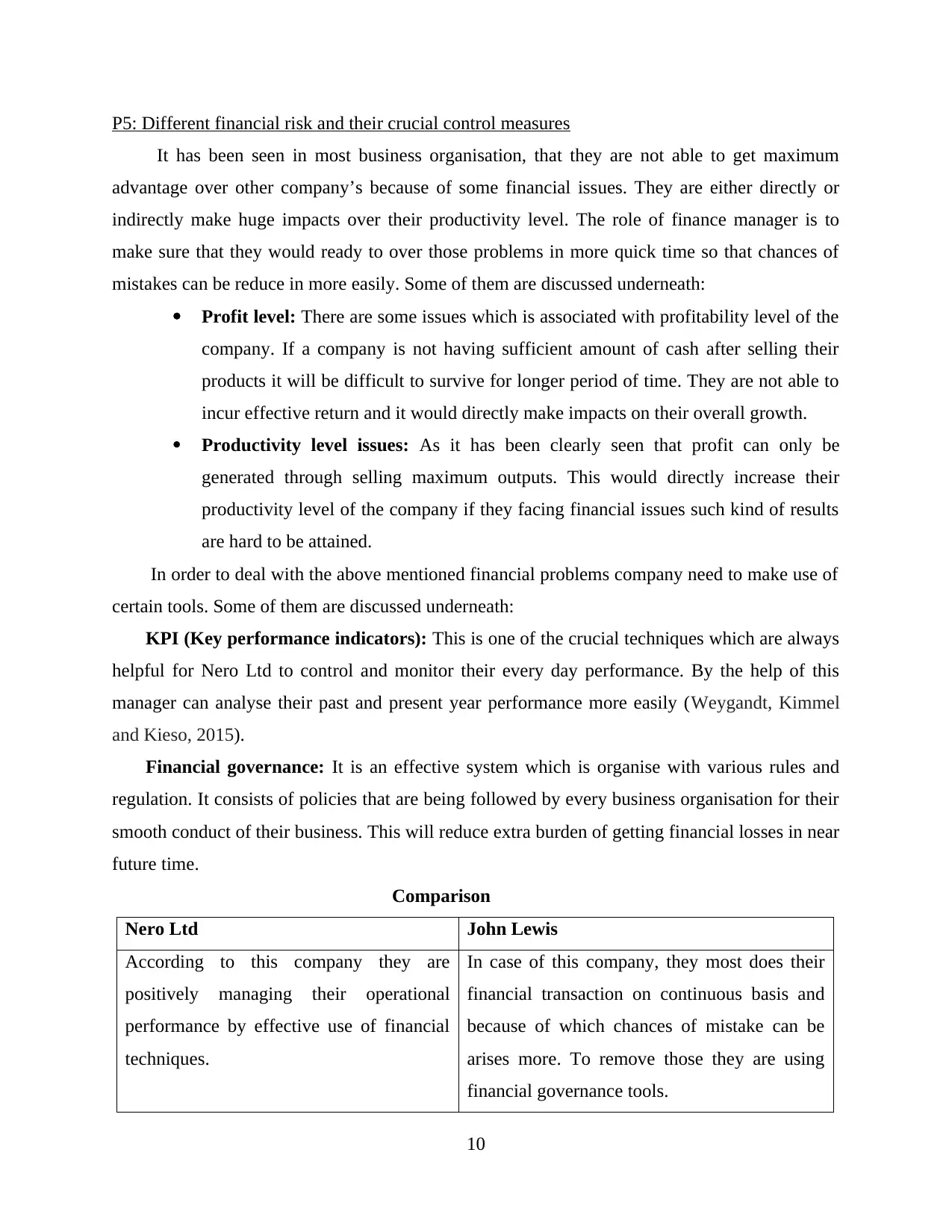

P5: Different financial risk and their crucial control measures

It has been seen in most business organisation, that they are not able to get maximum

advantage over other company’s because of some financial issues. They are either directly or

indirectly make huge impacts over their productivity level. The role of finance manager is to

make sure that they would ready to over those problems in more quick time so that chances of

mistakes can be reduce in more easily. Some of them are discussed underneath:

Profit level: There are some issues which is associated with profitability level of the

company. If a company is not having sufficient amount of cash after selling their

products it will be difficult to survive for longer period of time. They are not able to

incur effective return and it would directly make impacts on their overall growth.

Productivity level issues: As it has been clearly seen that profit can only be

generated through selling maximum outputs. This would directly increase their

productivity level of the company if they facing financial issues such kind of results

are hard to be attained.

In order to deal with the above mentioned financial problems company need to make use of

certain tools. Some of them are discussed underneath:

KPI (Key performance indicators): This is one of the crucial techniques which are always

helpful for Nero Ltd to control and monitor their every day performance. By the help of this

manager can analyse their past and present year performance more easily (Weygandt, Kimmel

and Kieso, 2015).

Financial governance: It is an effective system which is organise with various rules and

regulation. It consists of policies that are being followed by every business organisation for their

smooth conduct of their business. This will reduce extra burden of getting financial losses in near

future time.

Comparison

Nero Ltd John Lewis

According to this company they are

positively managing their operational

performance by effective use of financial

techniques.

In case of this company, they most does their

financial transaction on continuous basis and

because of which chances of mistake can be

arises more. To remove those they are using

financial governance tools.

10

It has been seen in most business organisation, that they are not able to get maximum

advantage over other company’s because of some financial issues. They are either directly or

indirectly make huge impacts over their productivity level. The role of finance manager is to

make sure that they would ready to over those problems in more quick time so that chances of

mistakes can be reduce in more easily. Some of them are discussed underneath:

Profit level: There are some issues which is associated with profitability level of the

company. If a company is not having sufficient amount of cash after selling their

products it will be difficult to survive for longer period of time. They are not able to

incur effective return and it would directly make impacts on their overall growth.

Productivity level issues: As it has been clearly seen that profit can only be

generated through selling maximum outputs. This would directly increase their

productivity level of the company if they facing financial issues such kind of results

are hard to be attained.

In order to deal with the above mentioned financial problems company need to make use of

certain tools. Some of them are discussed underneath:

KPI (Key performance indicators): This is one of the crucial techniques which are always

helpful for Nero Ltd to control and monitor their every day performance. By the help of this

manager can analyse their past and present year performance more easily (Weygandt, Kimmel

and Kieso, 2015).

Financial governance: It is an effective system which is organise with various rules and

regulation. It consists of policies that are being followed by every business organisation for their

smooth conduct of their business. This will reduce extra burden of getting financial losses in near

future time.

Comparison

Nero Ltd John Lewis

According to this company they are

positively managing their operational

performance by effective use of financial

techniques.

In case of this company, they most does their

financial transaction on continuous basis and

because of which chances of mistake can be

arises more. To remove those they are using

financial governance tools.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.