Management Accounting Techniques for Organizational Financial Problems

VerifiedAdded on 2024/05/23

|20

|4117

|475

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and techniques used by organizations to address financial problems. It begins by explaining management accounting and its essential requirements, including cost accounting, inventory management, job costing, and price optimization systems. The report then discusses various management accounting reporting methods such as budgeting, cost and sales, divisional, and investment appraisal reports. It highlights the benefits of management accounting systems in strategic planning, organizing, controlling, and decision-making, using the case of Waitrose as an example. Furthermore, it applies absorption costing and marginal costing techniques to prepare income statements. The report also explains planning tools for budgetary control, and compares how organizations adapt to respond to financial problems. The document is available on Desklib, a platform offering a wealth of study resources including past papers and solved assignments.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction.................................................................................................................................................3

LO1: Demonstrate an understanding of management accounting systems..................................................4

(P1) Explain management accounting and give the essential requirements of different types of

management accounting systems.............................................................................................................4

(P2) Explain different methods for management accounting reporting....................................................6

(M1) Benefits of management accounting systems and their application within an organisational

context.....................................................................................................................................................7

LO2: Apply a range of management accounting techniques......................................................................11

(P3) Calculate cost using appropriate techniques to prepare income statement.....................................11

LO3: Explain the use of planning tools used in management accounting..................................................14

(P4) Explain the advantages and disadvantages of different types of planning tools that can be used for

budgetary control for the chosen scenario.............................................................................................14

(M3) Advise to the CEO of M&S..........................................................................................................16

LO4: Compare ways in which organizations could use management accounting to respond to financial

problems....................................................................................................................................................17

(P5) Compare how organizations are adapting to respond to financial problems..................................17

Conclusion:...............................................................................................................................................18

References:................................................................................................................................................19

2

Introduction.................................................................................................................................................3

LO1: Demonstrate an understanding of management accounting systems..................................................4

(P1) Explain management accounting and give the essential requirements of different types of

management accounting systems.............................................................................................................4

(P2) Explain different methods for management accounting reporting....................................................6

(M1) Benefits of management accounting systems and their application within an organisational

context.....................................................................................................................................................7

LO2: Apply a range of management accounting techniques......................................................................11

(P3) Calculate cost using appropriate techniques to prepare income statement.....................................11

LO3: Explain the use of planning tools used in management accounting..................................................14

(P4) Explain the advantages and disadvantages of different types of planning tools that can be used for

budgetary control for the chosen scenario.............................................................................................14

(M3) Advise to the CEO of M&S..........................................................................................................16

LO4: Compare ways in which organizations could use management accounting to respond to financial

problems....................................................................................................................................................17

(P5) Compare how organizations are adapting to respond to financial problems..................................17

Conclusion:...............................................................................................................................................18

References:................................................................................................................................................19

2

Introduction

Management accounting is a type of reporting that is created solely for the management use. The

management accounting provides the manager with the insight about the present situation of

organization and way of improving it. The management accounting also provides comparison

between the expected and actual outcome of production. This function of management

accounting is referred to as budgetary control Management accounting is prepared for the short

term decision making of company. Management accounting estimates production cost in

different ways that is beneficial for the company strategy. Now a day’s management accounting

is integrated with environmental and social factors. This integration can reduce the financial

problems of companies (Huang, et al, 2010). Management accounting is an important concept in

the business operation and the management accountant performs the duty of this activities.

3

Management accounting is a type of reporting that is created solely for the management use. The

management accounting provides the manager with the insight about the present situation of

organization and way of improving it. The management accounting also provides comparison

between the expected and actual outcome of production. This function of management

accounting is referred to as budgetary control Management accounting is prepared for the short

term decision making of company. Management accounting estimates production cost in

different ways that is beneficial for the company strategy. Now a day’s management accounting

is integrated with environmental and social factors. This integration can reduce the financial

problems of companies (Huang, et al, 2010). Management accounting is an important concept in

the business operation and the management accountant performs the duty of this activities.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO1: Demonstrate an understanding of management accounting systems

(P1) Explain management accounting and give the essential requirements of different types

of management accounting systems

Management accounting can be defined as the critical component of operational function of

management in which various types of information are extracted and reported in an appropriate

report format which contains data that can be used by management for performing their decision

making function. The function of management accounting involves identifying, interpreting,

presenting and analyzing the data presented in the reports of management accounting (Bromwich

& Scapens, 2016).

Management accounting

system

Explanation Essentials

Cost accounting system The cost accounting system can

be seen as the function in which

various types and elements of

costs are recognized and

presented in an appropriate

format to the management of an

enterprise (Botes, et. al., 2017).

It must be ensured that there

exist an effective integration

between the financial accounting

and cost accounting system of

the enterprise.

The source and format of cost

data identified should be proper

and accurate.

Inventory management system The system of this type is

concerned with obtaining an

optimum level of inventory in

the production system of the

company. The inventory control

system helps in cost reduction

activities.

The factors which affect the

inventory levels should be given

more consideration.

The system should assist in

achieving the economies of scale

and appropriate inventory level

in the supply chain management

of company (Botes, et. al., 2017).

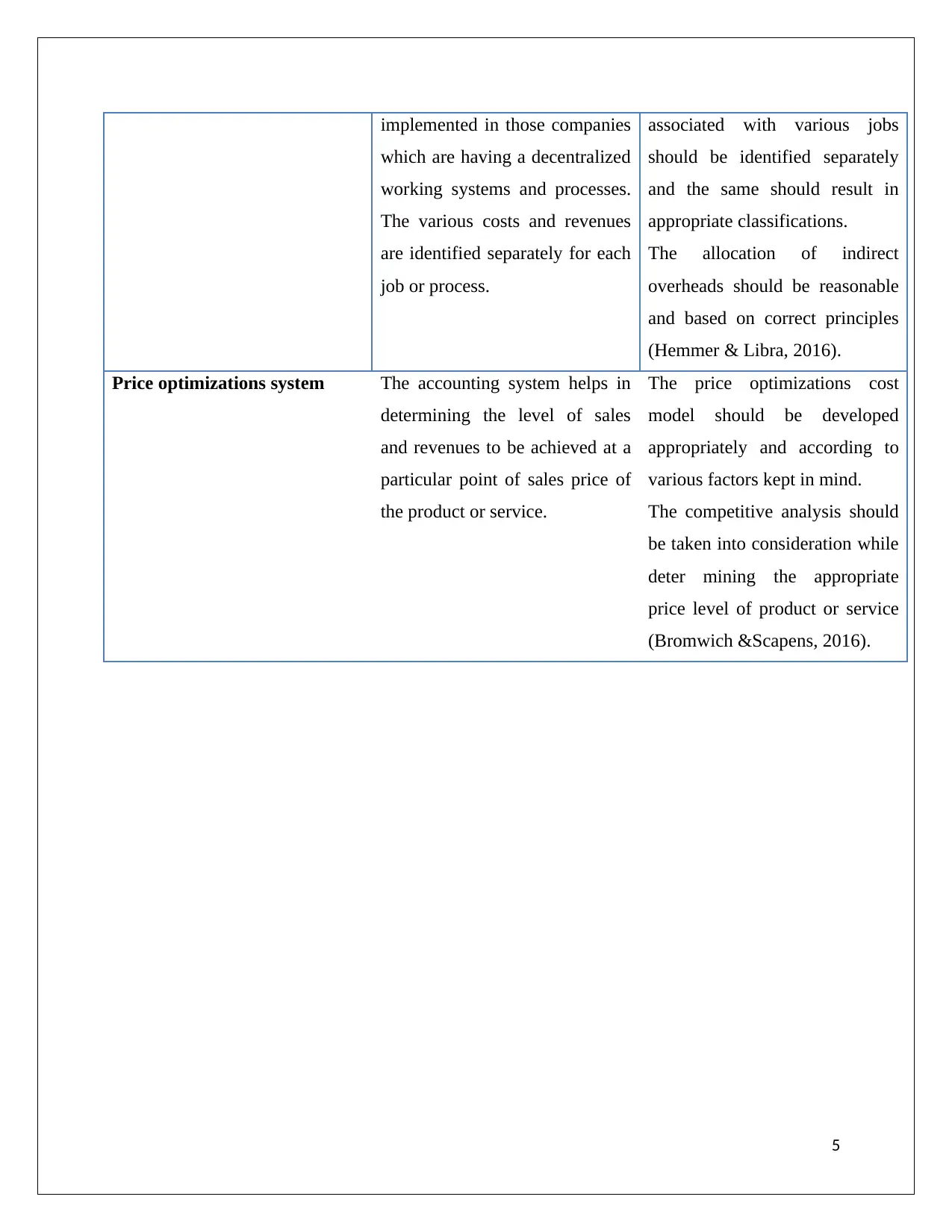

Job costing system The type of costing system is The different types of costs

4

(P1) Explain management accounting and give the essential requirements of different types

of management accounting systems

Management accounting can be defined as the critical component of operational function of

management in which various types of information are extracted and reported in an appropriate

report format which contains data that can be used by management for performing their decision

making function. The function of management accounting involves identifying, interpreting,

presenting and analyzing the data presented in the reports of management accounting (Bromwich

& Scapens, 2016).

Management accounting

system

Explanation Essentials

Cost accounting system The cost accounting system can

be seen as the function in which

various types and elements of

costs are recognized and

presented in an appropriate

format to the management of an

enterprise (Botes, et. al., 2017).

It must be ensured that there

exist an effective integration

between the financial accounting

and cost accounting system of

the enterprise.

The source and format of cost

data identified should be proper

and accurate.

Inventory management system The system of this type is

concerned with obtaining an

optimum level of inventory in

the production system of the

company. The inventory control

system helps in cost reduction

activities.

The factors which affect the

inventory levels should be given

more consideration.

The system should assist in

achieving the economies of scale

and appropriate inventory level

in the supply chain management

of company (Botes, et. al., 2017).

Job costing system The type of costing system is The different types of costs

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

implemented in those companies

which are having a decentralized

working systems and processes.

The various costs and revenues

are identified separately for each

job or process.

associated with various jobs

should be identified separately

and the same should result in

appropriate classifications.

The allocation of indirect

overheads should be reasonable

and based on correct principles

(Hemmer & Libra, 2016).

Price optimizations system The accounting system helps in

determining the level of sales

and revenues to be achieved at a

particular point of sales price of

the product or service.

The price optimizations cost

model should be developed

appropriately and according to

various factors kept in mind.

The competitive analysis should

be taken into consideration while

deter mining the appropriate

price level of product or service

(Bromwich &Scapens, 2016).

5

which are having a decentralized

working systems and processes.

The various costs and revenues

are identified separately for each

job or process.

associated with various jobs

should be identified separately

and the same should result in

appropriate classifications.

The allocation of indirect

overheads should be reasonable

and based on correct principles

(Hemmer & Libra, 2016).

Price optimizations system The accounting system helps in

determining the level of sales

and revenues to be achieved at a

particular point of sales price of

the product or service.

The price optimizations cost

model should be developed

appropriately and according to

various factors kept in mind.

The competitive analysis should

be taken into consideration while

deter mining the appropriate

price level of product or service

(Bromwich &Scapens, 2016).

5

(P2) Explain different methods for management accounting reporting

The various types of reporting methods which can be used by the management of Waitrose are as

under:

Budgeting reports – As the company is in the phase of development and initial stage of

executing new plans there is need to develop a budgeting plan for future course of action for the

company. The plans developed for the strategic direction of the company Waitrose will be

reported in budgeting reports appropriately (Hemmer & Libra, 2016).

Cost and sales reports – The type of reports will be used by the company Waitrose in order to

record and maintain the data about the various types of costs and sales revenues obtained during

the period. The same will help in analyzing the current financial position of company in respect

of market and other industry factors.

Divisional and segmental reports – The Company has decentralized system of performing the

operations and managing its business affairs and therefore there is a need to develop a proper

reporting system separately for each and every department of the company which will include all

its items related to costs and revenues of the company.

Investment appraisal reports – The type of reports are concerned with taking long term

decisions for the company and the various proposals for investment to be made by the company

are critically evaluated and analyzed through this type of reporting. The various results obtained

by applying the investment appraisal techniques like NPV, IRR etc. will be identified and the

results obtained will be reported as per the norms by the company (Granlund & Lukka, 2017).

6

The various types of reporting methods which can be used by the management of Waitrose are as

under:

Budgeting reports – As the company is in the phase of development and initial stage of

executing new plans there is need to develop a budgeting plan for future course of action for the

company. The plans developed for the strategic direction of the company Waitrose will be

reported in budgeting reports appropriately (Hemmer & Libra, 2016).

Cost and sales reports – The type of reports will be used by the company Waitrose in order to

record and maintain the data about the various types of costs and sales revenues obtained during

the period. The same will help in analyzing the current financial position of company in respect

of market and other industry factors.

Divisional and segmental reports – The Company has decentralized system of performing the

operations and managing its business affairs and therefore there is a need to develop a proper

reporting system separately for each and every department of the company which will include all

its items related to costs and revenues of the company.

Investment appraisal reports – The type of reports are concerned with taking long term

decisions for the company and the various proposals for investment to be made by the company

are critically evaluated and analyzed through this type of reporting. The various results obtained

by applying the investment appraisal techniques like NPV, IRR etc. will be identified and the

results obtained will be reported as per the norms by the company (Granlund & Lukka, 2017).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(M1) Benefits of management accounting systems and their application within an

organisational context

It can be observed form the above case study that the company Waitrose is currently facing a

financial crunch and the customers are not satisfied with the services of the company. Also the

company has been operating in highly competitive environment which requires innovation and

sound business practices. The various benefits in context of Waitrose are describes as below:

Strategic planning – The company is in the phase where it is introducing various exciting

offers for attracting its customers in order to increase the revenue of the company. The

management accounting function will provide strategic direction to the company for

making suitable action plans to be executed in the company (Granlund & Lukka, 2017).

Organizing – It can be observed that there is required a proper security system and

supervision system in Waitrose to check whether the customer has purchased the item

before taking the delivery of coffee and the function of management accounting will

provide adequate options for managing and organizing these affairs in the company.

Controlling – The Company needs to control its costs and expenditures in order to

achieve the highest profitability and growth in future and therefore the costing techniques

like standard costing, responsibility accounting will assist the company in planning and

executing the cost control and cost reduction activities in company.

Decision making – The function of management accounting will help significantly the

management of Waitrose to take critical business decision efficiently and effectively. The

use of various management accounting tools and techniques will assure that proper

decisions are taken at appropriate time (Botes, et. al., 2017).

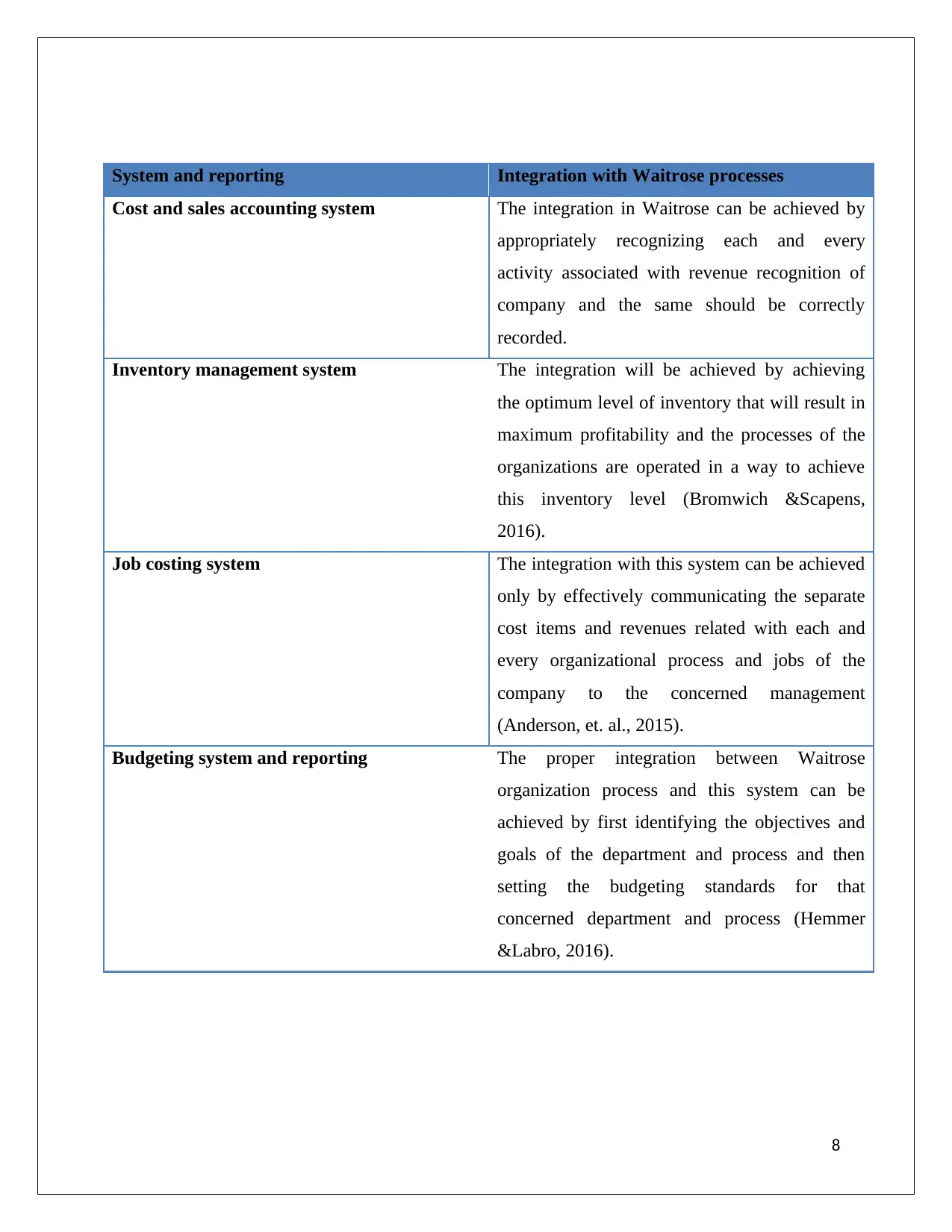

Management accounting systems and reporting is integration with organisational

processes.

In Waitrose the management accounting system will play a crucial role in achieving the

organization objectives and goals. However there is a need to achieve integration with

organizational processes that can be achieved as following:

7

organisational context

It can be observed form the above case study that the company Waitrose is currently facing a

financial crunch and the customers are not satisfied with the services of the company. Also the

company has been operating in highly competitive environment which requires innovation and

sound business practices. The various benefits in context of Waitrose are describes as below:

Strategic planning – The company is in the phase where it is introducing various exciting

offers for attracting its customers in order to increase the revenue of the company. The

management accounting function will provide strategic direction to the company for

making suitable action plans to be executed in the company (Granlund & Lukka, 2017).

Organizing – It can be observed that there is required a proper security system and

supervision system in Waitrose to check whether the customer has purchased the item

before taking the delivery of coffee and the function of management accounting will

provide adequate options for managing and organizing these affairs in the company.

Controlling – The Company needs to control its costs and expenditures in order to

achieve the highest profitability and growth in future and therefore the costing techniques

like standard costing, responsibility accounting will assist the company in planning and

executing the cost control and cost reduction activities in company.

Decision making – The function of management accounting will help significantly the

management of Waitrose to take critical business decision efficiently and effectively. The

use of various management accounting tools and techniques will assure that proper

decisions are taken at appropriate time (Botes, et. al., 2017).

Management accounting systems and reporting is integration with organisational

processes.

In Waitrose the management accounting system will play a crucial role in achieving the

organization objectives and goals. However there is a need to achieve integration with

organizational processes that can be achieved as following:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

System and reporting Integration with Waitrose processes

Cost and sales accounting system The integration in Waitrose can be achieved by

appropriately recognizing each and every

activity associated with revenue recognition of

company and the same should be correctly

recorded.

Inventory management system The integration will be achieved by achieving

the optimum level of inventory that will result in

maximum profitability and the processes of the

organizations are operated in a way to achieve

this inventory level (Bromwich &Scapens,

2016).

Job costing system The integration with this system can be achieved

only by effectively communicating the separate

cost items and revenues related with each and

every organizational process and jobs of the

company to the concerned management

(Anderson, et. al., 2015).

Budgeting system and reporting The proper integration between Waitrose

organization process and this system can be

achieved by first identifying the objectives and

goals of the department and process and then

setting the budgeting standards for that

concerned department and process (Hemmer

&Labro, 2016).

8

Cost and sales accounting system The integration in Waitrose can be achieved by

appropriately recognizing each and every

activity associated with revenue recognition of

company and the same should be correctly

recorded.

Inventory management system The integration will be achieved by achieving

the optimum level of inventory that will result in

maximum profitability and the processes of the

organizations are operated in a way to achieve

this inventory level (Bromwich &Scapens,

2016).

Job costing system The integration with this system can be achieved

only by effectively communicating the separate

cost items and revenues related with each and

every organizational process and jobs of the

company to the concerned management

(Anderson, et. al., 2015).

Budgeting system and reporting The proper integration between Waitrose

organization process and this system can be

achieved by first identifying the objectives and

goals of the department and process and then

setting the budgeting standards for that

concerned department and process (Hemmer

&Labro, 2016).

8

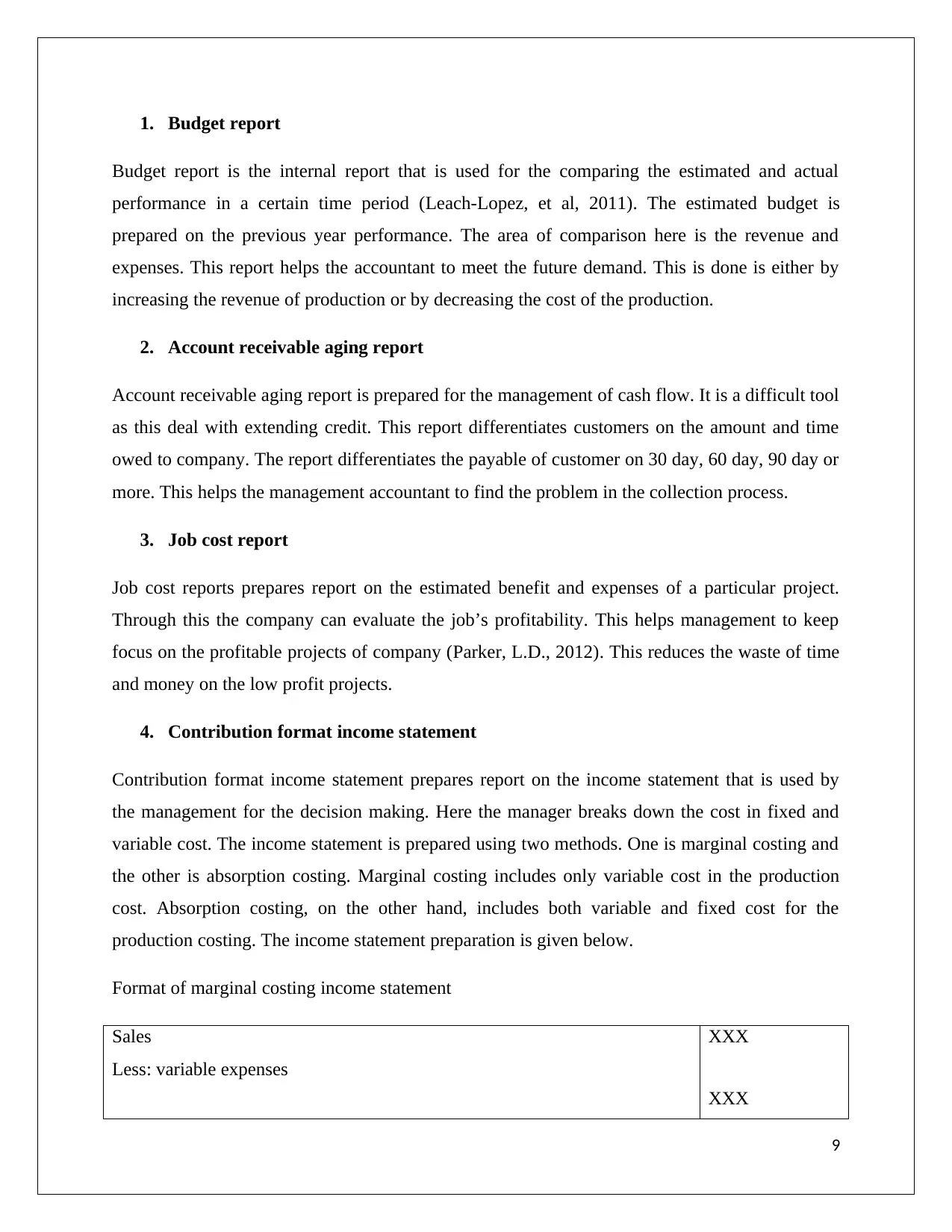

1. Budget report

Budget report is the internal report that is used for the comparing the estimated and actual

performance in a certain time period (Leach-Lopez, et al, 2011). The estimated budget is

prepared on the previous year performance. The area of comparison here is the revenue and

expenses. This report helps the accountant to meet the future demand. This is done is either by

increasing the revenue of production or by decreasing the cost of the production.

2. Account receivable aging report

Account receivable aging report is prepared for the management of cash flow. It is a difficult tool

as this deal with extending credit. This report differentiates customers on the amount and time

owed to company. The report differentiates the payable of customer on 30 day, 60 day, 90 day or

more. This helps the management accountant to find the problem in the collection process.

3. Job cost report

Job cost reports prepares report on the estimated benefit and expenses of a particular project.

Through this the company can evaluate the job’s profitability. This helps management to keep

focus on the profitable projects of company (Parker, L.D., 2012). This reduces the waste of time

and money on the low profit projects.

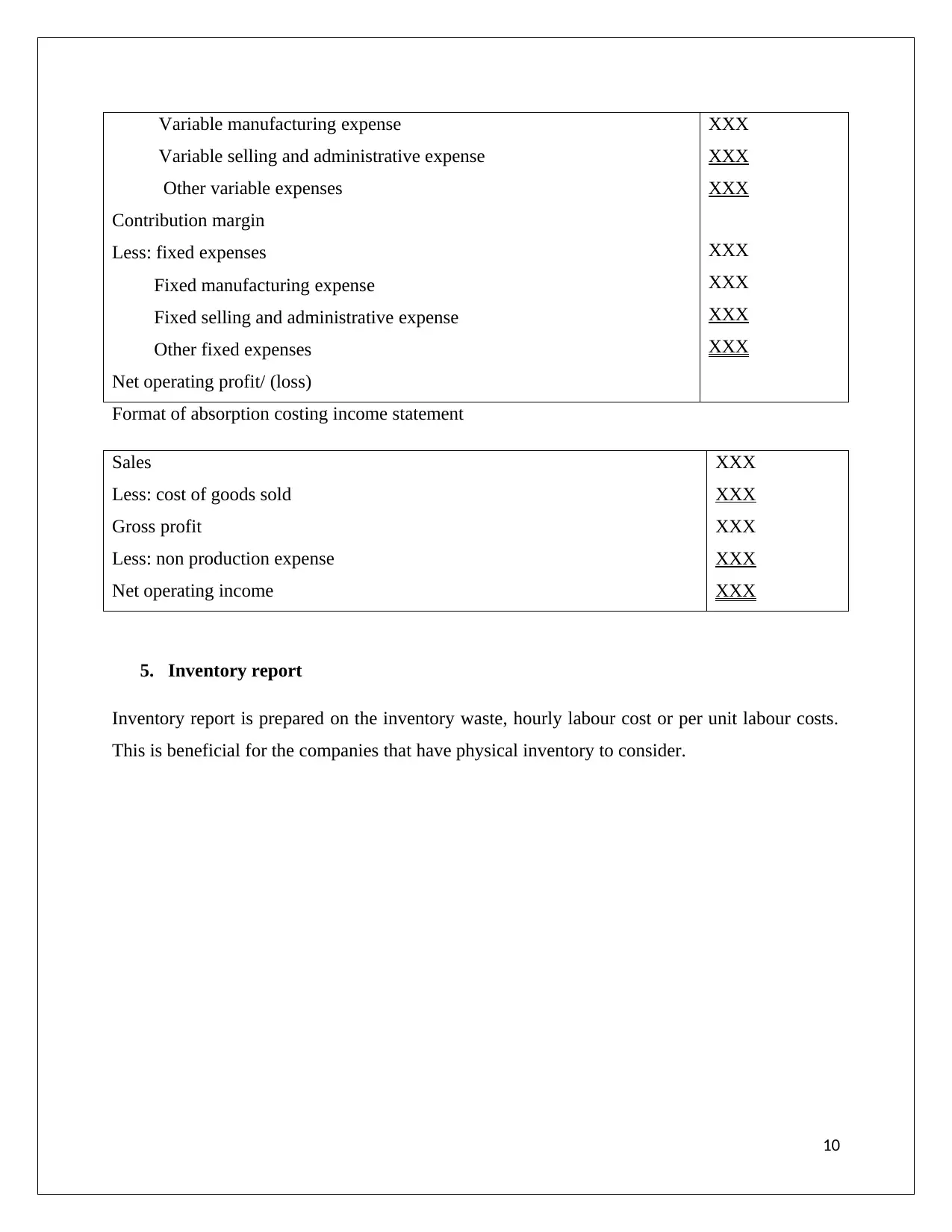

4. Contribution format income statement

Contribution format income statement prepares report on the income statement that is used by

the management for the decision making. Here the manager breaks down the cost in fixed and

variable cost. The income statement is prepared using two methods. One is marginal costing and

the other is absorption costing. Marginal costing includes only variable cost in the production

cost. Absorption costing, on the other hand, includes both variable and fixed cost for the

production costing. The income statement preparation is given below.

Format of marginal costing income statement

Sales

Less: variable expenses

XXX

XXX

9

Budget report is the internal report that is used for the comparing the estimated and actual

performance in a certain time period (Leach-Lopez, et al, 2011). The estimated budget is

prepared on the previous year performance. The area of comparison here is the revenue and

expenses. This report helps the accountant to meet the future demand. This is done is either by

increasing the revenue of production or by decreasing the cost of the production.

2. Account receivable aging report

Account receivable aging report is prepared for the management of cash flow. It is a difficult tool

as this deal with extending credit. This report differentiates customers on the amount and time

owed to company. The report differentiates the payable of customer on 30 day, 60 day, 90 day or

more. This helps the management accountant to find the problem in the collection process.

3. Job cost report

Job cost reports prepares report on the estimated benefit and expenses of a particular project.

Through this the company can evaluate the job’s profitability. This helps management to keep

focus on the profitable projects of company (Parker, L.D., 2012). This reduces the waste of time

and money on the low profit projects.

4. Contribution format income statement

Contribution format income statement prepares report on the income statement that is used by

the management for the decision making. Here the manager breaks down the cost in fixed and

variable cost. The income statement is prepared using two methods. One is marginal costing and

the other is absorption costing. Marginal costing includes only variable cost in the production

cost. Absorption costing, on the other hand, includes both variable and fixed cost for the

production costing. The income statement preparation is given below.

Format of marginal costing income statement

Sales

Less: variable expenses

XXX

XXX

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable manufacturing expense

Variable selling and administrative expense

Other variable expenses

Contribution margin

Less: fixed expenses

Fixed manufacturing expense

Fixed selling and administrative expense

Other fixed expenses

Net operating profit/ (loss)

XXX

XXX

XXX

XXX

XXX

XXX

XXX

Format of absorption costing income statement

Sales

Less: cost of goods sold

Gross profit

Less: non production expense

Net operating income

XXX

XXX

XXX

XXX

XXX

5. Inventory report

Inventory report is prepared on the inventory waste, hourly labour cost or per unit labour costs.

This is beneficial for the companies that have physical inventory to consider.

10

Variable selling and administrative expense

Other variable expenses

Contribution margin

Less: fixed expenses

Fixed manufacturing expense

Fixed selling and administrative expense

Other fixed expenses

Net operating profit/ (loss)

XXX

XXX

XXX

XXX

XXX

XXX

XXX

Format of absorption costing income statement

Sales

Less: cost of goods sold

Gross profit

Less: non production expense

Net operating income

XXX

XXX

XXX

XXX

XXX

5. Inventory report

Inventory report is prepared on the inventory waste, hourly labour cost or per unit labour costs.

This is beneficial for the companies that have physical inventory to consider.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

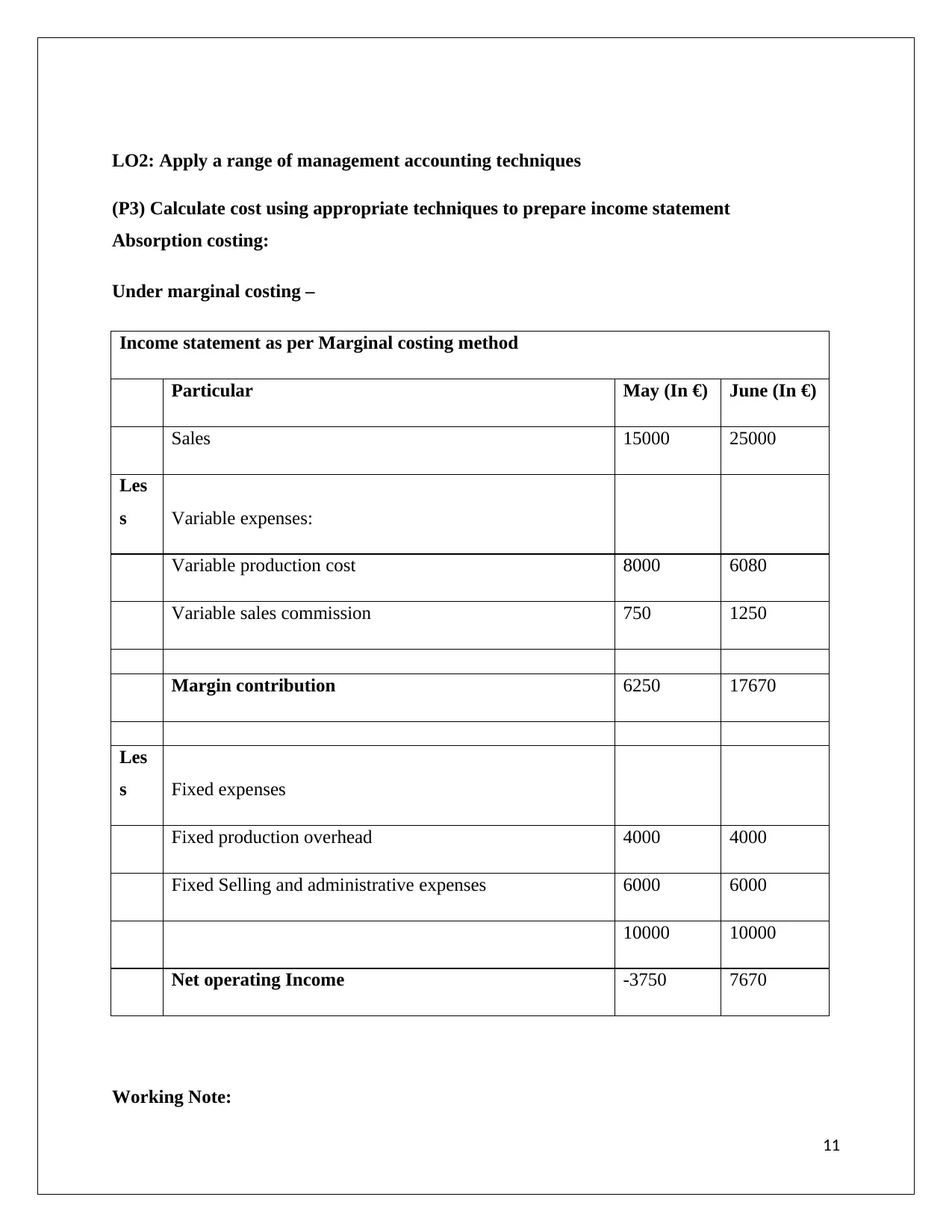

LO2: Apply a range of management accounting techniques

(P3) Calculate cost using appropriate techniques to prepare income statement

Absorption costing:

Under marginal costing –

Income statement as per Marginal costing method

Particular May (In €) June (In €)

Sales 15000 25000

Les

s Variable expenses:

Variable production cost 8000 6080

Variable sales commission 750 1250

Margin contribution 6250 17670

Les

s Fixed expenses

Fixed production overhead 4000 4000

Fixed Selling and administrative expenses 6000 6000

10000 10000

Net operating Income -3750 7670

Working Note:

11

(P3) Calculate cost using appropriate techniques to prepare income statement

Absorption costing:

Under marginal costing –

Income statement as per Marginal costing method

Particular May (In €) June (In €)

Sales 15000 25000

Les

s Variable expenses:

Variable production cost 8000 6080

Variable sales commission 750 1250

Margin contribution 6250 17670

Les

s Fixed expenses

Fixed production overhead 4000 4000

Fixed Selling and administrative expenses 6000 6000

10000 10000

Net operating Income -3750 7670

Working Note:

11

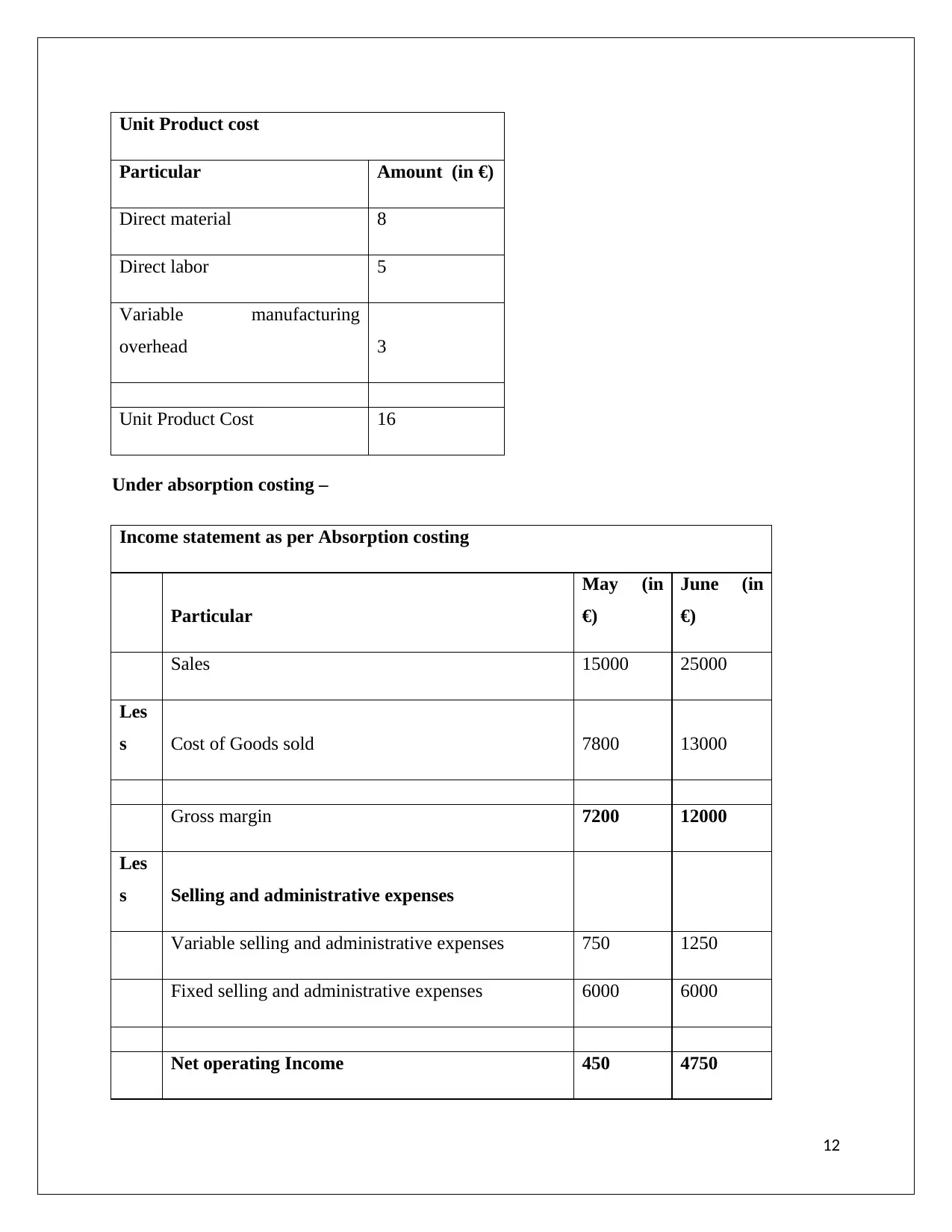

Unit Product cost

Particular Amount (in €)

Direct material 8

Direct labor 5

Variable manufacturing

overhead 3

Unit Product Cost 16

Under absorption costing –

Income statement as per Absorption costing

Particular

May (in

€)

June (in

€)

Sales 15000 25000

Les

s Cost of Goods sold 7800 13000

Gross margin 7200 12000

Les

s Selling and administrative expenses

Variable selling and administrative expenses 750 1250

Fixed selling and administrative expenses 6000 6000

Net operating Income 450 4750

12

Particular Amount (in €)

Direct material 8

Direct labor 5

Variable manufacturing

overhead 3

Unit Product Cost 16

Under absorption costing –

Income statement as per Absorption costing

Particular

May (in

€)

June (in

€)

Sales 15000 25000

Les

s Cost of Goods sold 7800 13000

Gross margin 7200 12000

Les

s Selling and administrative expenses

Variable selling and administrative expenses 750 1250

Fixed selling and administrative expenses 6000 6000

Net operating Income 450 4750

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.