UGB253 Management Accounting Assignment: Budgeting Analysis

VerifiedAdded on 2023/06/01

|16

|3933

|248

Homework Assignment

AI Summary

This document provides a comprehensive solution to a management accounting assignment. It begins with an overview of budgetary control, emphasizing the differences between fixed and flexible budgets, and the advantages of flexible budgeting in adapting to changing circumstances. The solution then delves into the preparation of flexible budgets and discusses their strengths and weaknesses. It explores the behavioral aspects of budgeting, including motivation, participation, and group effects. The assignment also includes a case study involving Citrus Grove and a potential offer from Borges, requiring an analysis of relevant costs, and a recommendation on whether to accept the offer. Furthermore, it defines qualitative factors and their importance in decision-making. Finally, the document provides recommendations for Citrus Grove based on different scenarios, including outsourcing, and highlights the importance of considering both quantitative and qualitative aspects in business decisions.

UGB253

Management

Accounting for

Business

1

Management

Accounting for

Business

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Q1..........................................................................................................................................................2

1).......................................................................................................................................................2

Purpose of flexible Budgets..........................................................................................................2

Preparation of Flexible Budgets....................................................................................................2

2).......................................................................................................................................................3

Strengths and weaknesses of the flexible budgeting process........................................................3

Strengths of Flexible Budgeting....................................................................................................3

Weaknesses of Flexible Budgeting...............................................................................................3

3).......................................................................................................................................................4

Behavioral Aspects of Budgeting..................................................................................................4

Motivation.....................................................................................................................................4

Participation..................................................................................................................................4

Feedback.......................................................................................................................................4

Group effects.................................................................................................................................4

Budget slack..................................................................................................................................5

Q2..........................................................................................................................................................5

1).......................................................................................................................................................5

2).......................................................................................................................................................5

3).......................................................................................................................................................6

What are Qualitative Factors?.......................................................................................................6

4).......................................................................................................................................................6

Relevant cost.................................................................................................................................6

Reference...............................................................................................................................................8

2

Q1..........................................................................................................................................................2

1).......................................................................................................................................................2

Purpose of flexible Budgets..........................................................................................................2

Preparation of Flexible Budgets....................................................................................................2

2).......................................................................................................................................................3

Strengths and weaknesses of the flexible budgeting process........................................................3

Strengths of Flexible Budgeting....................................................................................................3

Weaknesses of Flexible Budgeting...............................................................................................3

3).......................................................................................................................................................4

Behavioral Aspects of Budgeting..................................................................................................4

Motivation.....................................................................................................................................4

Participation..................................................................................................................................4

Feedback.......................................................................................................................................4

Group effects.................................................................................................................................4

Budget slack..................................................................................................................................5

Q2..........................................................................................................................................................5

1).......................................................................................................................................................5

2).......................................................................................................................................................5

3).......................................................................................................................................................6

What are Qualitative Factors?.......................................................................................................6

4).......................................................................................................................................................6

Relevant cost.................................................................................................................................6

Reference...............................................................................................................................................8

2

Task 1

3

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Q1.

1)

Budgetary control is another term for the practice of using budgets to keep track of and oversee the

operations of a company. In order to ensure that goals are reached, budgets are created. It is feasible

to make meaningful comparisons between actual and expected outcomes by using the information

included in budget reports.

During the course of a fixed budgetary management system, a single prediction of sales volume or

any other activity level serves as the basis for the master budget. The budgeted amount for each cost

is calculated based on the number of sales that are expected to occur. In accounting jargon, a "fixed

budget" is a budget that is predicated on a certain quantity of sales or other operations being

completed. An important advantage of budgets is that they can be used to compare actual results to

expectations, which is a substantial benefit. A performance report contains information that may be

studied and compared with other data. Approximately 10,000 (composite) units were planned to be

sold in January of this year, based on Optel's fixed budget for the year 2009. Eyeglasses, frames,

4

1)

Budgetary control is another term for the practice of using budgets to keep track of and oversee the

operations of a company. In order to ensure that goals are reached, budgets are created. It is feasible

to make meaningful comparisons between actual and expected outcomes by using the information

included in budget reports.

During the course of a fixed budgetary management system, a single prediction of sales volume or

any other activity level serves as the basis for the master budget. The budgeted amount for each cost

is calculated based on the number of sales that are expected to occur. In accounting jargon, a "fixed

budget" is a budget that is predicated on a certain quantity of sales or other operations being

completed. An important advantage of budgets is that they can be used to compare actual results to

expectations, which is a substantial benefit. A performance report contains information that may be

studied and compared with other data. Approximately 10,000 (composite) units were planned to be

sold in January of this year, based on Optel's fixed budget for the year 2009. Eyeglasses, frames,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

contacts, and numerous accessories, such as sunglasses, are produced by this company at a

reasonable cost. The inventory levels (as well as the production volume) were unchanged for this

report.

Flexible Budgets:

In order to overcome the limits of a fixed budget performance report, such as the impact of changes

in sales volume, management may adopt a flexible budget. This will allow them to meet and exceed

their goals faster. With a variable budget, or flexible spending plan, the capacity to estimate both

income and expenditures is essential. Prior to and after the activities of a certain time, flexible

budgets may be advantageous. A flexible budget is usually designed prior to the time period in order

to handle fluctuating levels of activity. Budgets for each of these levels might provide a "what-if"

perspective on operations. The best- and worst-case scenarios are often included into the various

tiers. Averted or at least mitigated worst-case scenarios are possible as a result. Managers may better

assess their past performance with the use of after-period flexible budgeting. An good tool for this

kind of analysis, since it takes into account current activity levels to reflect future revenues and costs

in real time. The root causes of any discrepancies are more likely to be discovered via a comparison

of actual results with those predicted than through any other research strategy. Using this data,

managers may zero in on the most critical issues and devise solutions. Fixed budgets are intended to

help management forecast future operations since they are built on one predetermined amount of

projected sales or output.

Flexibility in Budget Preparation

It is possible to evaluate how varied levels of activity impact both revenues as well as expenditures

by using flexible budgeting. Budget flexibility is achieved by the use of distinctions between fixed

and variable expenses. A company's overall variable expenses fluctuate proportionally to variations

in activity levels, since the cost per unit of activity stays constant. Fixed costs are not affected by

variations in activity in a relevant (average) operating range. We presume that expenses may be

categorized as either variable or fixed within a relevant range in this discussion.

2)

Take Advantage of Opportunities

5

reasonable cost. The inventory levels (as well as the production volume) were unchanged for this

report.

Flexible Budgets:

In order to overcome the limits of a fixed budget performance report, such as the impact of changes

in sales volume, management may adopt a flexible budget. This will allow them to meet and exceed

their goals faster. With a variable budget, or flexible spending plan, the capacity to estimate both

income and expenditures is essential. Prior to and after the activities of a certain time, flexible

budgets may be advantageous. A flexible budget is usually designed prior to the time period in order

to handle fluctuating levels of activity. Budgets for each of these levels might provide a "what-if"

perspective on operations. The best- and worst-case scenarios are often included into the various

tiers. Averted or at least mitigated worst-case scenarios are possible as a result. Managers may better

assess their past performance with the use of after-period flexible budgeting. An good tool for this

kind of analysis, since it takes into account current activity levels to reflect future revenues and costs

in real time. The root causes of any discrepancies are more likely to be discovered via a comparison

of actual results with those predicted than through any other research strategy. Using this data,

managers may zero in on the most critical issues and devise solutions. Fixed budgets are intended to

help management forecast future operations since they are built on one predetermined amount of

projected sales or output.

Flexibility in Budget Preparation

It is possible to evaluate how varied levels of activity impact both revenues as well as expenditures

by using flexible budgeting. Budget flexibility is achieved by the use of distinctions between fixed

and variable expenses. A company's overall variable expenses fluctuate proportionally to variations

in activity levels, since the cost per unit of activity stays constant. Fixed costs are not affected by

variations in activity in a relevant (average) operating range. We presume that expenses may be

categorized as either variable or fixed within a relevant range in this discussion.

2)

Take Advantage of Opportunities

5

In flexible budgeting, variable expenditures are specified as a proportion of revenue. Flexible

budgets, for example, might be changed to raise marketing expenditures even more in order to take

advantage of unanticipated gains in revenues. Additionally, a more flexible budget would allow the

company to hire additional people to meet rising demand, rather than limiting it by keeping the

budget for payroll expenditures the same.

Adjust for Changing Costs and Profit Margins

Static budgets are those in which the expenses of operations and product profit margins are defined

at the beginning of the year on the basis of past data. Unfortunately, real life does not allow for the

continuation of the status quo. Budgets that are adaptable can deal with these changes. Consider the

following scenario: material prices for a product unexpectedly rise throughout the course of the year,

rendering this item unprofitable. A flexible budget would be able to detect this discrepancy, and

management would be able to take remedial action. Pricing changes may be implemented, or efforts

to identify cost reductions in production expenditures may be undertaken.

Better Cost Controls

Budgets that are more adaptable respond more swiftly to changing circumstances. Consider the

following scenario: the budget was created with the idea that sales would be $200,000 per month,

and labor costs were budgeted at $50,000 per month, or 25 percent of sales, as a result of this

expectation. If sales fall to $150,000 per month, then labor costs should be cut to $37,500 (25

percent of $150,000), which is $37,500 per month. A static budget would not be able to respond to a

decrease in income and would retain labor expenses at the same level as they were before.

Updated With Current Data

When operating in a dynamic environment, revenues and expenses are continually adjusted in

flexible budgets to account for the changes in conditions. It is probable that new environmental

regulations may increase the costs of production in the future, necessitating the procurement of new

types of equipment to meet the requirements. Shipments to customers may be delayed as a result of

weather conditions, which may boost shipping rates and create delays in delivery charges. When

managers have flexible budgets, they are constantly updating their forecasts and spending controls to

reflect the most up-to-date information available. Most importantly, the ability of a flexible budget

6

budgets, for example, might be changed to raise marketing expenditures even more in order to take

advantage of unanticipated gains in revenues. Additionally, a more flexible budget would allow the

company to hire additional people to meet rising demand, rather than limiting it by keeping the

budget for payroll expenditures the same.

Adjust for Changing Costs and Profit Margins

Static budgets are those in which the expenses of operations and product profit margins are defined

at the beginning of the year on the basis of past data. Unfortunately, real life does not allow for the

continuation of the status quo. Budgets that are adaptable can deal with these changes. Consider the

following scenario: material prices for a product unexpectedly rise throughout the course of the year,

rendering this item unprofitable. A flexible budget would be able to detect this discrepancy, and

management would be able to take remedial action. Pricing changes may be implemented, or efforts

to identify cost reductions in production expenditures may be undertaken.

Better Cost Controls

Budgets that are more adaptable respond more swiftly to changing circumstances. Consider the

following scenario: the budget was created with the idea that sales would be $200,000 per month,

and labor costs were budgeted at $50,000 per month, or 25 percent of sales, as a result of this

expectation. If sales fall to $150,000 per month, then labor costs should be cut to $37,500 (25

percent of $150,000), which is $37,500 per month. A static budget would not be able to respond to a

decrease in income and would retain labor expenses at the same level as they were before.

Updated With Current Data

When operating in a dynamic environment, revenues and expenses are continually adjusted in

flexible budgets to account for the changes in conditions. It is probable that new environmental

regulations may increase the costs of production in the future, necessitating the procurement of new

types of equipment to meet the requirements. Shipments to customers may be delayed as a result of

weather conditions, which may boost shipping rates and create delays in delivery charges. When

managers have flexible budgets, they are constantly updating their forecasts and spending controls to

reflect the most up-to-date information available. Most importantly, the ability of a flexible budget

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to adapt to changing conditions in the actual world is the most significant advantage it has over a

static one. Because nothing ever stays the same, management is accountable for reacting to

unexpected negative circumstances and grasping unanticipated opportunities when they arise.

3)

Behavioral Aspects of Budgeting

It is essential that all stakeholders engaged in the budget-setting process be involved at every stage

of the process. If it were feasible, the perfect result would be achieved. Despite the fact that the

world isn't flawless, it's probable that not everyone will be able to attain exactly what they want

from the beginning of their journey. In order to maximize your good points and limit your negative

points, you must be aware of behavioral components if you are in charge of budgeting. Aspects of

organizational behavior that might be characterized include motivation, participation, feedback,

group effects, budget slack, and organizational politics, to name a few examples. Several studies

have been conducted on each of these themes, with results that are, at best, ambiguous.

7

static one. Because nothing ever stays the same, management is accountable for reacting to

unexpected negative circumstances and grasping unanticipated opportunities when they arise.

3)

Behavioral Aspects of Budgeting

It is essential that all stakeholders engaged in the budget-setting process be involved at every stage

of the process. If it were feasible, the perfect result would be achieved. Despite the fact that the

world isn't flawless, it's probable that not everyone will be able to attain exactly what they want

from the beginning of their journey. In order to maximize your good points and limit your negative

points, you must be aware of behavioral components if you are in charge of budgeting. Aspects of

organizational behavior that might be characterized include motivation, participation, feedback,

group effects, budget slack, and organizational politics, to name a few examples. Several studies

have been conducted on each of these themes, with results that are, at best, ambiguous.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Getting Buy-In

A budget may be quickly and easily created by top-down decision-making without considering those

at the bottom of the organizational hierarchy. Corporate decision-making often takes this route,

although it has its drawbacks. Workers and lower-level supervisors may detest being advised to live

within the budget because they believe it sets an unattainable expectation. It takes longer when

management asks for employee participation and feedback. Those workers, on the other hand, who

believe they had a hand in creating the budget, are more inclined to see it through.

Self-Interested Managers

Budgets are not always objective as a result of the fact that management is not objective. A hidden

agenda may be at work among those who are engaged in the budget-making process. The

department head of an employee has a vested interest in making the case for greater resources and

more money to be provided to her department. That might lead to his overestimating the amount of

money the department demands or the amount of money the department sends to the company. In

order to create a good budget, objective analysis must be performed that is independent of human

influence.

Constraints and Resentment

It is not unusual for employees to see a budget as a kind of punishment. Managers may utilize

budgets to decline even legitimate requests as long as they don't go overboard with spending.

Employees who are subjected to restrictions may come to think that they are unable to do their tasks

properly. Employees may grow even more disgruntled as a result of the fact that meeting budget

requirements is an essential element of the appraisal process. According to an article in the

"Accounting Historians Journal," in order to get around a tight budget, workers would exaggerate

estimates and fabricate figures, according to the article. What to Do in Order to Make It Happen

Employees may be more willing to comply with a budget if the process is more open to them,

according to research. Budgeting should be portrayed by managers as a joint activity between

themselves and their staff. Participating employees demands a degree of seriousness that cannot be

faked, and this is essential.

8

A budget may be quickly and easily created by top-down decision-making without considering those

at the bottom of the organizational hierarchy. Corporate decision-making often takes this route,

although it has its drawbacks. Workers and lower-level supervisors may detest being advised to live

within the budget because they believe it sets an unattainable expectation. It takes longer when

management asks for employee participation and feedback. Those workers, on the other hand, who

believe they had a hand in creating the budget, are more inclined to see it through.

Self-Interested Managers

Budgets are not always objective as a result of the fact that management is not objective. A hidden

agenda may be at work among those who are engaged in the budget-making process. The

department head of an employee has a vested interest in making the case for greater resources and

more money to be provided to her department. That might lead to his overestimating the amount of

money the department demands or the amount of money the department sends to the company. In

order to create a good budget, objective analysis must be performed that is independent of human

influence.

Constraints and Resentment

It is not unusual for employees to see a budget as a kind of punishment. Managers may utilize

budgets to decline even legitimate requests as long as they don't go overboard with spending.

Employees who are subjected to restrictions may come to think that they are unable to do their tasks

properly. Employees may grow even more disgruntled as a result of the fact that meeting budget

requirements is an essential element of the appraisal process. According to an article in the

"Accounting Historians Journal," in order to get around a tight budget, workers would exaggerate

estimates and fabricate figures, according to the article. What to Do in Order to Make It Happen

Employees may be more willing to comply with a budget if the process is more open to them,

according to research. Budgeting should be portrayed by managers as a joint activity between

themselves and their staff. Participating employees demands a degree of seriousness that cannot be

faked, and this is essential.

8

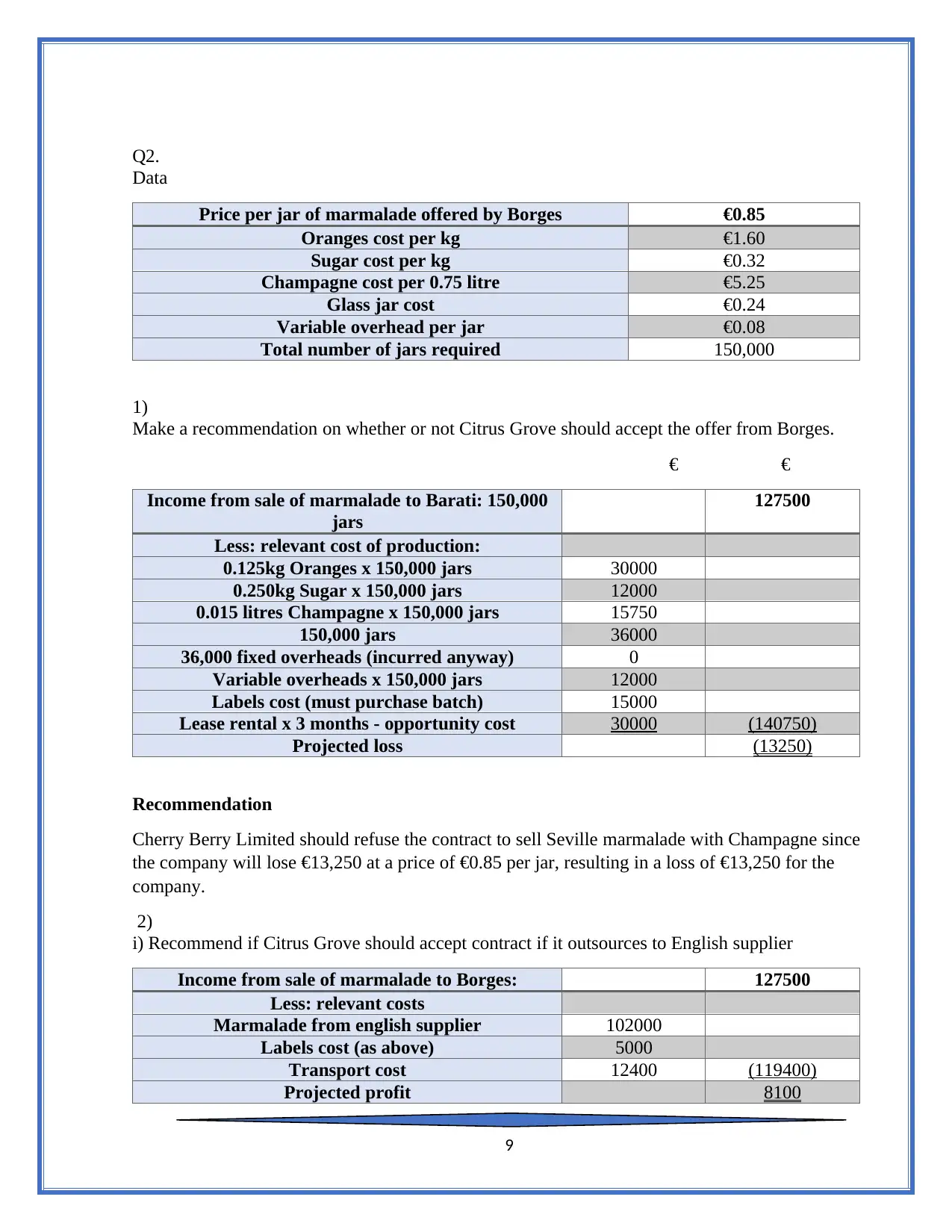

Q2.

Data

Price per jar of marmalade offered by Borges €0.85

Oranges cost per kg €1.60

Sugar cost per kg €0.32

Champagne cost per 0.75 litre €5.25

Glass jar cost €0.24

Variable overhead per jar €0.08

Total number of jars required 150,000

1)

Make a recommendation on whether or not Citrus Grove should accept the offer from Borges.

€ €

Income from sale of marmalade to Barati: 150,000

jars

127500

Less: relevant cost of production:

0.125kg Oranges x 150,000 jars 30000

0.250kg Sugar x 150,000 jars 12000

0.015 litres Champagne x 150,000 jars 15750

150,000 jars 36000

36,000 fixed overheads (incurred anyway) 0

Variable overheads x 150,000 jars 12000

Labels cost (must purchase batch) 15000

Lease rental x 3 months - opportunity cost 30000 (140750)

Projected loss (13250)

Recommendation

Cherry Berry Limited should refuse the contract to sell Seville marmalade with Champagne since

the company will lose €13,250 at a price of €0.85 per jar, resulting in a loss of €13,250 for the

company.

2)

i) Recommend if Citrus Grove should accept contract if it outsources to English supplier

Income from sale of marmalade to Borges: 127500

Less: relevant costs

Marmalade from english supplier 102000

Labels cost (as above) 5000

Transport cost 12400 (119400)

Projected profit 8100

9

Data

Price per jar of marmalade offered by Borges €0.85

Oranges cost per kg €1.60

Sugar cost per kg €0.32

Champagne cost per 0.75 litre €5.25

Glass jar cost €0.24

Variable overhead per jar €0.08

Total number of jars required 150,000

1)

Make a recommendation on whether or not Citrus Grove should accept the offer from Borges.

€ €

Income from sale of marmalade to Barati: 150,000

jars

127500

Less: relevant cost of production:

0.125kg Oranges x 150,000 jars 30000

0.250kg Sugar x 150,000 jars 12000

0.015 litres Champagne x 150,000 jars 15750

150,000 jars 36000

36,000 fixed overheads (incurred anyway) 0

Variable overheads x 150,000 jars 12000

Labels cost (must purchase batch) 15000

Lease rental x 3 months - opportunity cost 30000 (140750)

Projected loss (13250)

Recommendation

Cherry Berry Limited should refuse the contract to sell Seville marmalade with Champagne since

the company will lose €13,250 at a price of €0.85 per jar, resulting in a loss of €13,250 for the

company.

2)

i) Recommend if Citrus Grove should accept contract if it outsources to English supplier

Income from sale of marmalade to Borges: 127500

Less: relevant costs

Marmalade from english supplier 102000

Labels cost (as above) 5000

Transport cost 12400 (119400)

Projected profit 8100

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Recommendation

Cherry Berry Limited should accept the contract to manufacture Seville marmalade with

Champagne based on the financial data because outsourcing manufacturing to an English supplier

would result in a profit of €8,100. Cherry Berry Limited should reject the contract to manufacture

Seville marmalade with Champagne based on the financial data.

3)

What are Qualitative Factors?

Qualitative factors are decision outcomes that cannot be measured. Examples of qualitative factors

are

noted below:

Morale. The impact on employee morale of adding a break room to the production area.

Customers. The impact on customer opinions of a business if an investment is made in answering

their

phone calls in less time by adding customer support staff.

Investors. The impact on investors of conducting a road show to meet as many of them as possible.

Community. The impact on the local community of allowing employees to spend a few hours of

paid

time assisting with community projects.

Products. It may be possible to use somewhat cheaper components in products. However, if this is

done

too much, it may create an overall impression of reduced quality, which may lead customers to buy

fewer products.

A manager should consider qualitative factors as part of his or her analysis of a decision. Depending

on

the manager and the level of investment involved, qualitative factors can be the deciding point in

whether to engage in a certain activity. For example, if a large investment of funds is involved, the

key

decision factors are more likely to be quantitative, since the investing business has a great deal at

stake

in the decision. However, if the investment of funds is minor, the impact of qualitative factors could

play

a more important role in the decision.

From a branding perspective, qualitative factors can be particularly important. Proper branding

requires

high expenditure levels to establish and maintain an aura of quality, which a purely quantitative

analysis

might not justify

What are Qualitative Factors?

Qualitative factors are decision outcomes that cannot be measured. Examples of qualitative factors

are

noted below:

Morale. The impact on employee morale of adding a break room to the production area.

10

Cherry Berry Limited should accept the contract to manufacture Seville marmalade with

Champagne based on the financial data because outsourcing manufacturing to an English supplier

would result in a profit of €8,100. Cherry Berry Limited should reject the contract to manufacture

Seville marmalade with Champagne based on the financial data.

3)

What are Qualitative Factors?

Qualitative factors are decision outcomes that cannot be measured. Examples of qualitative factors

are

noted below:

Morale. The impact on employee morale of adding a break room to the production area.

Customers. The impact on customer opinions of a business if an investment is made in answering

their

phone calls in less time by adding customer support staff.

Investors. The impact on investors of conducting a road show to meet as many of them as possible.

Community. The impact on the local community of allowing employees to spend a few hours of

paid

time assisting with community projects.

Products. It may be possible to use somewhat cheaper components in products. However, if this is

done

too much, it may create an overall impression of reduced quality, which may lead customers to buy

fewer products.

A manager should consider qualitative factors as part of his or her analysis of a decision. Depending

on

the manager and the level of investment involved, qualitative factors can be the deciding point in

whether to engage in a certain activity. For example, if a large investment of funds is involved, the

key

decision factors are more likely to be quantitative, since the investing business has a great deal at

stake

in the decision. However, if the investment of funds is minor, the impact of qualitative factors could

play

a more important role in the decision.

From a branding perspective, qualitative factors can be particularly important. Proper branding

requires

high expenditure levels to establish and maintain an aura of quality, which a purely quantitative

analysis

might not justify

What are Qualitative Factors?

Qualitative factors are decision outcomes that cannot be measured. Examples of qualitative factors

are

noted below:

Morale. The impact on employee morale of adding a break room to the production area.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Customers. The impact on customer opinions of a business if an investment is made in answering

their

phone calls in less time by adding customer support staff.

Investors. The impact on investors of conducting a road show to meet as many of them as possible.

Community. The impact on the local community of allowing employees to spend a few hours of

paid

time assisting with community projects.

Products. It may be possible to use somewhat cheaper components in products. However, if this is

done

too much, it may create an overall impression of reduced quality, which may lead customers to buy

fewer products.

A manager should consider qualitative factors as part of his or her analysis of a decision. Depending

on

the manager and the level of investment involved, qualitative factors can be the deciding point in

whether to engage in a certain activity. For example, if a large investment of funds is involved, the

key

decision factors are more likely to be quantitative, since the investing business has a great deal at

stake

in the decision. However, if the investment of funds is minor, the impact of qualitative factors could

play

a more important role in the decision.

From a branding perspective, qualitative factors can be particularly important. Proper branding

requires

high expenditure levels to establish and maintain an aura of quality, which a purely quantitative

analysis

might not justify

What are Qualitative Factors?

To put it another way: Qualitative elements are results that can't be quantified. The following are

some examples of qualitative factors:

Morale. The impact of introducing a break room to the workplace is investigated.

Customers. Increasing the number of customer service representatives may have a significant impact

on how consumers see a company's customer service.

Investors. The effect of a road show on the investing community.

Community. Employees that donate a few hours of their paid time to help out in the community will

be covered in length in the next section.

Products. To save money on items, you might use cheaper components. Customers may buy fewer

items if they have the sense that the product is of poorer quality if this happens too often.

When making a choice, managers should take into account both quantitative and qualitative factors.

Whether or not to participate in a certain activity may be influenced by qualitative characteristics

that rely on the management and the amount of investment necessary. Suppose you're in this

situation: Due to the high stakes involved, the major decision factors are more likely to be

11

their

phone calls in less time by adding customer support staff.

Investors. The impact on investors of conducting a road show to meet as many of them as possible.

Community. The impact on the local community of allowing employees to spend a few hours of

paid

time assisting with community projects.

Products. It may be possible to use somewhat cheaper components in products. However, if this is

done

too much, it may create an overall impression of reduced quality, which may lead customers to buy

fewer products.

A manager should consider qualitative factors as part of his or her analysis of a decision. Depending

on

the manager and the level of investment involved, qualitative factors can be the deciding point in

whether to engage in a certain activity. For example, if a large investment of funds is involved, the

key

decision factors are more likely to be quantitative, since the investing business has a great deal at

stake

in the decision. However, if the investment of funds is minor, the impact of qualitative factors could

play

a more important role in the decision.

From a branding perspective, qualitative factors can be particularly important. Proper branding

requires

high expenditure levels to establish and maintain an aura of quality, which a purely quantitative

analysis

might not justify

What are Qualitative Factors?

To put it another way: Qualitative elements are results that can't be quantified. The following are

some examples of qualitative factors:

Morale. The impact of introducing a break room to the workplace is investigated.

Customers. Increasing the number of customer service representatives may have a significant impact

on how consumers see a company's customer service.

Investors. The effect of a road show on the investing community.

Community. Employees that donate a few hours of their paid time to help out in the community will

be covered in length in the next section.

Products. To save money on items, you might use cheaper components. Customers may buy fewer

items if they have the sense that the product is of poorer quality if this happens too often.

When making a choice, managers should take into account both quantitative and qualitative factors.

Whether or not to participate in a certain activity may be influenced by qualitative characteristics

that rely on the management and the amount of investment necessary. Suppose you're in this

situation: Due to the high stakes involved, the major decision factors are more likely to be

11

quantitative in nature when a large quantity of money is being put at risk. It is possible that

qualitative factors will have a greater influence on results even when the investment is little.

When it comes to branding from a marketing perspective, quality qualities may be extremely

important. Impossible to justify with merely financial facts, high levels of expenditure are necessary

for good branding in order to create and sustain an air of quality.

4)

Relevant cost

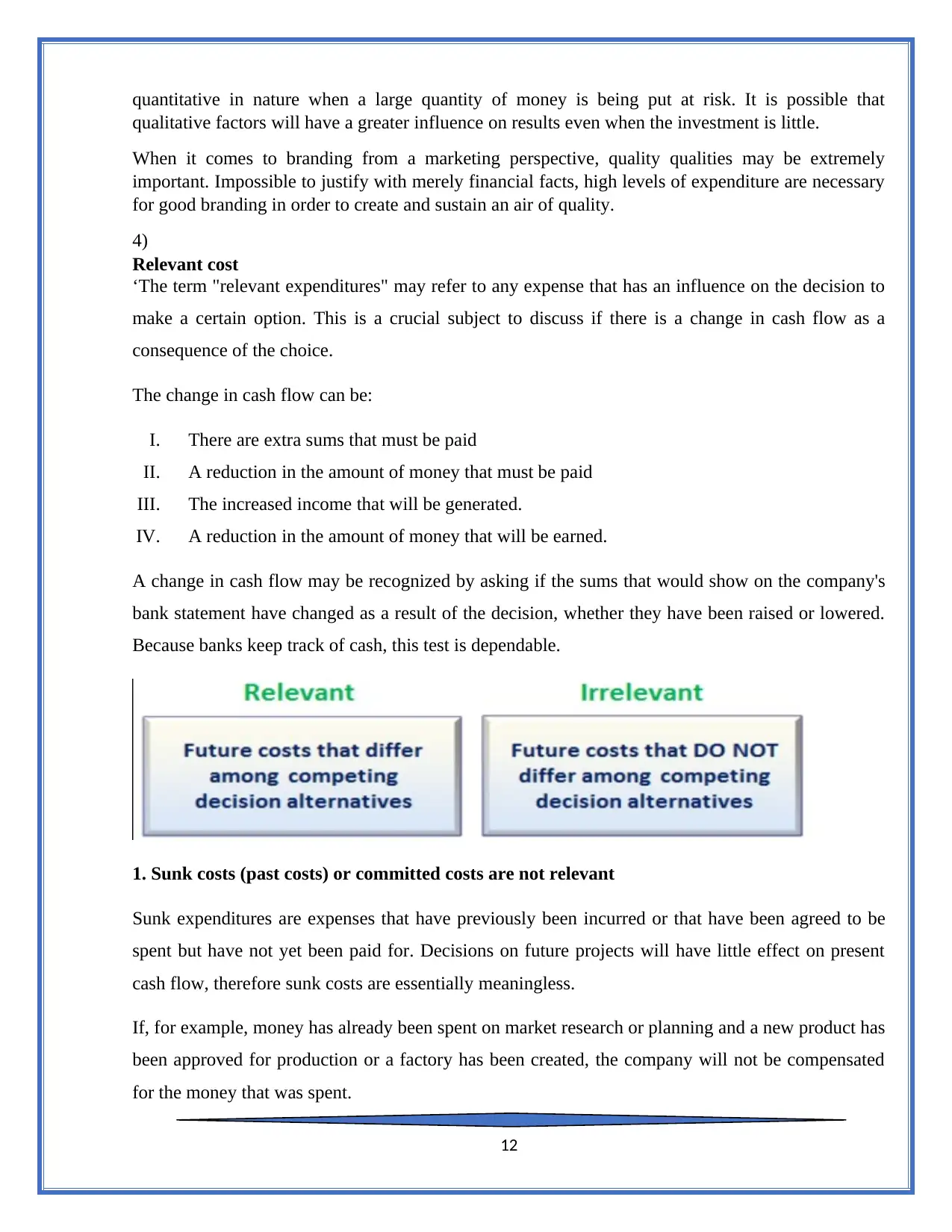

‘The term "relevant expenditures" may refer to any expense that has an influence on the decision to

make a certain option. This is a crucial subject to discuss if there is a change in cash flow as a

consequence of the choice.

The change in cash flow can be:

I. There are extra sums that must be paid

II. A reduction in the amount of money that must be paid

III. The increased income that will be generated.

IV. A reduction in the amount of money that will be earned.

A change in cash flow may be recognized by asking if the sums that would show on the company's

bank statement have changed as a result of the decision, whether they have been raised or lowered.

Because banks keep track of cash, this test is dependable.

1. Sunk costs (past costs) or committed costs are not relevant

Sunk expenditures are expenses that have previously been incurred or that have been agreed to be

spent but have not yet been paid for. Decisions on future projects will have little effect on present

cash flow, therefore sunk costs are essentially meaningless.

If, for example, money has already been spent on market research or planning and a new product has

been approved for production or a factory has been created, the company will not be compensated

for the money that was spent.

12

qualitative factors will have a greater influence on results even when the investment is little.

When it comes to branding from a marketing perspective, quality qualities may be extremely

important. Impossible to justify with merely financial facts, high levels of expenditure are necessary

for good branding in order to create and sustain an air of quality.

4)

Relevant cost

‘The term "relevant expenditures" may refer to any expense that has an influence on the decision to

make a certain option. This is a crucial subject to discuss if there is a change in cash flow as a

consequence of the choice.

The change in cash flow can be:

I. There are extra sums that must be paid

II. A reduction in the amount of money that must be paid

III. The increased income that will be generated.

IV. A reduction in the amount of money that will be earned.

A change in cash flow may be recognized by asking if the sums that would show on the company's

bank statement have changed as a result of the decision, whether they have been raised or lowered.

Because banks keep track of cash, this test is dependable.

1. Sunk costs (past costs) or committed costs are not relevant

Sunk expenditures are expenses that have previously been incurred or that have been agreed to be

spent but have not yet been paid for. Decisions on future projects will have little effect on present

cash flow, therefore sunk costs are essentially meaningless.

If, for example, money has already been spent on market research or planning and a new product has

been approved for production or a factory has been created, the company will not be compensated

for the money that was spent.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.