Management Accounting Report: Green Tech Budgetary Control Analysis

VerifiedAdded on 2020/10/05

|15

|4991

|169

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Green Tech, a company specializing in landscaping and garden supplies. It delves into various aspects of management accounting, including different types of accounting systems such as price optimization, job costing, cost accounting, and inventory management. The report examines the methods used for management accounting reporting, including budgeting, job cost, and inventory reports. It highlights the benefits of a management accounting system, such as aiding in decision-making and planning. Furthermore, the report explores cost calculation techniques, differentiating between fixed and variable costs, and explaining marginal and absorption costing methods. It also discusses the advantages and disadvantages of different planning tools for budgetary control and examines how Green Tech adapts its management accounting system to resolve financial problems. The report emphasizes the importance of management accounting in monitoring business performance and providing valuable insights for strategic decision-making.

Management Accounting

Table of Contents

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its different types................................................................1

P2 Methods for management accounting Reporting..............................................................3

M1 Benefits of management accounting system....................................................................4

D1 Critical evaluation on management accounting report integrated within organisational

process....................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Calculation of costs using techniques of cost analysis......................................................4

M2 Apply management accounting techniques to produce financial reporting documents. .8

D2 Produce financial reports that accurately apply and interpret data...................................8

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tools for budgetary control9

M3 Use of planning tools and application for preparing and forecasting budgets...............10

TASK 5..........................................................................................................................................11

P5 Comparison on how organizations are adapting management accounting system to resolve

financial problems................................................................................................................11

D3 Examine planning tools respond to lead organisation to sustainable success................12

M4 Examine planning tools respond to lead organisation to sustainable success...............12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

TASK 1............................................................................................................................................1

P1 Management accounting and its different types................................................................1

P2 Methods for management accounting Reporting..............................................................3

M1 Benefits of management accounting system....................................................................4

D1 Critical evaluation on management accounting report integrated within organisational

process....................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Calculation of costs using techniques of cost analysis......................................................4

M2 Apply management accounting techniques to produce financial reporting documents. .8

D2 Produce financial reports that accurately apply and interpret data...................................8

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tools for budgetary control9

M3 Use of planning tools and application for preparing and forecasting budgets...............10

TASK 5..........................................................................................................................................11

P5 Comparison on how organizations are adapting management accounting system to resolve

financial problems................................................................................................................11

D3 Examine planning tools respond to lead organisation to sustainable success................12

M4 Examine planning tools respond to lead organisation to sustainable success...............12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is a process of recording various transactions that takes place

within an organisation and then presenting them in an effective manner for the users of these

Accounting records for the purpose of decision making in the longer run. Management

Accounting plays a very important role in the monitoring the overall business performance in an

effective way over period of time. The current report will throw a light on the various

management accounting tools that are being used like planning and measurement tools. The

company is a leading supplier of various kinds of landscaping products, tree planting products

and at the same time is engaged in providing different garden supplies as well (Kumarasiri and

Jubb, 2016).

This particular report will emphasize on the different tools that are being used for

budgetary control. Different types of managerial accounting reports are budget; cost as well as

inventory etc. an income statement is prepared on the basis of calculations of costs by using

absorption and marginal costing methods. The importance of management accounting in the

business decision will also be discussed in detail in an effective manner under the current report.

TASK 1

P1 Management accounting and its different types

In a usual business operations there are various kinds of business transactions that takes

place and thus it becomes even more necessary to effectively record those transactions in a

manner that they can be used for the purpose of decision making of the users of these accounting

records. The users of this accounting information can be both internal as well as external in

nature; internal users can be management of the company, employees etc. while external users

can be investors,, government authorities etc. The Role of Management Accounting is basically

to take care of all the transactions and record them appropriately so that necessary reports can be

prepared for important business decisions like budgetary control etc.

Green Tech is a company which is engaged in the unique business of providing supplies

related to garden and planting trees. For this purpose the company comes across various kinds of

transactions that it decides to record through various kinds of management accounting system

that is in place, these includes:

1

Management accounting is a process of recording various transactions that takes place

within an organisation and then presenting them in an effective manner for the users of these

Accounting records for the purpose of decision making in the longer run. Management

Accounting plays a very important role in the monitoring the overall business performance in an

effective way over period of time. The current report will throw a light on the various

management accounting tools that are being used like planning and measurement tools. The

company is a leading supplier of various kinds of landscaping products, tree planting products

and at the same time is engaged in providing different garden supplies as well (Kumarasiri and

Jubb, 2016).

This particular report will emphasize on the different tools that are being used for

budgetary control. Different types of managerial accounting reports are budget; cost as well as

inventory etc. an income statement is prepared on the basis of calculations of costs by using

absorption and marginal costing methods. The importance of management accounting in the

business decision will also be discussed in detail in an effective manner under the current report.

TASK 1

P1 Management accounting and its different types

In a usual business operations there are various kinds of business transactions that takes

place and thus it becomes even more necessary to effectively record those transactions in a

manner that they can be used for the purpose of decision making of the users of these accounting

records. The users of this accounting information can be both internal as well as external in

nature; internal users can be management of the company, employees etc. while external users

can be investors,, government authorities etc. The Role of Management Accounting is basically

to take care of all the transactions and record them appropriately so that necessary reports can be

prepared for important business decisions like budgetary control etc.

Green Tech is a company which is engaged in the unique business of providing supplies

related to garden and planting trees. For this purpose the company comes across various kinds of

transactions that it decides to record through various kinds of management accounting system

that is in place, these includes:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price Optimisation System: It is quite obvious that demand of a particular goods or

service will fluctuate at different prices. This system is primarily used to determine the right kind

of prices that can be charged from customers that will enable higher profits and will also not

affect the sales of the organisation in the longer run. Therefore, the management of Green tech

uses this accounting system for pricing the various products of their company to compete

effectively in the market at competitive prices.

Job Costing System: Under this system, the cost of a particular job is calculated. This

kind of system helps in assigning manufacturing for each unit that is being provided to the

customers. But this type of system is basically used when the goods that are being provided are

quite different than other goods. Managers of Green Tech used this system for keeping track

record of cost of each job and maintaining data as well. It includes following procedure:- Receive Enquiry: The customer will first enquire about the product, its quality,, prices

etc. and then an order is given. Price Estimation: - Job costing is usually done by accountant who estimate price of each

unit by identifying taste and preference of customers. Order Receive: Once the customers are satisfied they will give order for the products or

service. Production Order: This order is being placed for the purpose of starting the process of

production in an effective manner. Recording of Cost: The cost of production and its every aspect are properly recorded for

the purpose of using the same for decision making purposes.

Completion of Job: Once the Job is complete, the report is being handed over to the

concerned accounts department of the company in the longer run.

Cost Accounting System: This is a comprehensive system of accounting that calculates

as well as records various costs that is being incurred by the company in the process of providing

goods and services to clients as well as customers in the longer run (Maskell, Baggaley and

Grasso, 2016).

Inventory Management System: This is also a very important system that helps an

organisation in managing the level of inventory in an efficient manner. Inventory management is

a very important part of cost management within the business and this system allows an

organisation to effectively ascertain the minimum cost that shall be incurred on inventory in

2

service will fluctuate at different prices. This system is primarily used to determine the right kind

of prices that can be charged from customers that will enable higher profits and will also not

affect the sales of the organisation in the longer run. Therefore, the management of Green tech

uses this accounting system for pricing the various products of their company to compete

effectively in the market at competitive prices.

Job Costing System: Under this system, the cost of a particular job is calculated. This

kind of system helps in assigning manufacturing for each unit that is being provided to the

customers. But this type of system is basically used when the goods that are being provided are

quite different than other goods. Managers of Green Tech used this system for keeping track

record of cost of each job and maintaining data as well. It includes following procedure:- Receive Enquiry: The customer will first enquire about the product, its quality,, prices

etc. and then an order is given. Price Estimation: - Job costing is usually done by accountant who estimate price of each

unit by identifying taste and preference of customers. Order Receive: Once the customers are satisfied they will give order for the products or

service. Production Order: This order is being placed for the purpose of starting the process of

production in an effective manner. Recording of Cost: The cost of production and its every aspect are properly recorded for

the purpose of using the same for decision making purposes.

Completion of Job: Once the Job is complete, the report is being handed over to the

concerned accounts department of the company in the longer run.

Cost Accounting System: This is a comprehensive system of accounting that calculates

as well as records various costs that is being incurred by the company in the process of providing

goods and services to clients as well as customers in the longer run (Maskell, Baggaley and

Grasso, 2016).

Inventory Management System: This is also a very important system that helps an

organisation in managing the level of inventory in an efficient manner. Inventory management is

a very important part of cost management within the business and this system allows an

organisation to effectively ascertain the minimum cost that shall be incurred on inventory in

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

order to remain profitable and competitive in the market. This system of management accounting

includes many methods like LIFO (Last in first out), FIFO (First-In First-Out) and prioritise with

ABC. Managers of Green Tech use ABC analysis in order to give more attention on those

products which give more profitability to business.

P2 Methods for management accounting Reporting

There are various sorts of reports that are being prepared by the management of Green

Tech for the purpose of presenting the financial information to users. Accounting Reports are a

very important part of the business; these are being used in determining the performance of an

organisation over longer period of time. Management of the company prepares various

accounting reports on weekly, quarterly as well as monthly basis in an effective manner. It will

help in getting accurate and reliable statistical information through major decisions can be taken.

The different types of Management accounting reports that are being prepared by the

management of Green tech are as follows: Budgeting report: Under this kind of report, the budgets are being set for different

departments that exist within an organisation. A proper cost budget is prepared for each

department and the same is represented through budget Report that will help in enhancing

the business decision and assessing the deviation in the budgeted as well as actual

performance in an effective way. Job Cost Report: It basically refers to ascertain the expenses, costs and profitability of a

particular job within the manufacturing process in an effective way. Through this report

the company can know the information about the current job and its progress that has

taken place till now. It contains information about labour cost, wastages as well as per

unit overhead costs. Therefore, employers of Green Tech prepare this report to see

opportunities in making considerable progress within the manufacturing progress in an

effective way (Banker, and et. al., 2014).

Inventory Report: It refers to the report that is prepared by the management of the

organisation for effectively in order to get a detailed view of the state of inventory within

the firm of its various products. The Report determines the quantity of the items, the

average rate of each item. The Standard quality of the same etc. It also include the cost of

inventory per unit, wastages that has taken place and the average holding period of the

inventory in an effective way.

3

includes many methods like LIFO (Last in first out), FIFO (First-In First-Out) and prioritise with

ABC. Managers of Green Tech use ABC analysis in order to give more attention on those

products which give more profitability to business.

P2 Methods for management accounting Reporting

There are various sorts of reports that are being prepared by the management of Green

Tech for the purpose of presenting the financial information to users. Accounting Reports are a

very important part of the business; these are being used in determining the performance of an

organisation over longer period of time. Management of the company prepares various

accounting reports on weekly, quarterly as well as monthly basis in an effective manner. It will

help in getting accurate and reliable statistical information through major decisions can be taken.

The different types of Management accounting reports that are being prepared by the

management of Green tech are as follows: Budgeting report: Under this kind of report, the budgets are being set for different

departments that exist within an organisation. A proper cost budget is prepared for each

department and the same is represented through budget Report that will help in enhancing

the business decision and assessing the deviation in the budgeted as well as actual

performance in an effective way. Job Cost Report: It basically refers to ascertain the expenses, costs and profitability of a

particular job within the manufacturing process in an effective way. Through this report

the company can know the information about the current job and its progress that has

taken place till now. It contains information about labour cost, wastages as well as per

unit overhead costs. Therefore, employers of Green Tech prepare this report to see

opportunities in making considerable progress within the manufacturing progress in an

effective way (Banker, and et. al., 2014).

Inventory Report: It refers to the report that is prepared by the management of the

organisation for effectively in order to get a detailed view of the state of inventory within

the firm of its various products. The Report determines the quantity of the items, the

average rate of each item. The Standard quality of the same etc. It also include the cost of

inventory per unit, wastages that has taken place and the average holding period of the

inventory in an effective way.

3

M1 Benefits of management accounting system

Management accounting system is internal management system in which organization

measures and analyse performance of management. Components of this system are budgets,

reports of return on investments, sales analysis, balance scorecard and activity based accounting.

This system is useful for management in efficient decision making, assists in planning process,

budgeting through focusing on specific costs and responsibilities, making work flows and

processes prompt, ease in find data by centralizes, organize and creating structure of it, ability to

generate useful trend analysis and special reports. Actual internal performance of management is

then compared with planned to find variances.

D1 Critical evaluation on management accounting report integrated within organisational process

Management accounting systems and management accounting reports are different in

context of reporting because former provides relevant information to internal users like

management but later to outsiders like stockholders, creditors, employees, government etc. Both

these are integrated in organizational context because both practices presents information in

report format so that they data can be easily compared between firms. Another similarity

between both these are that they requires specialized knowledge and expertise in accounting

field. Both these help organization to present health of business to take financial decisions and

present information more formally.

TASK 2

P3 Calculation of costs using techniques of cost analysis

Cost refer to process which is executed by management to have knowledge about value

of money incurred for conduction of business activities in company. It is essential that each and

every firm have adequate funds for having sufficient resources that is material and manpower in

firm. Executive of GreenTech uses cost analysis techniques to compute costs which are executed

while production of products and services. Thus, fixed and variable are two forms of costs which

are stated below (Kumarasiri and Jubb, 2016):

Fixed cost: It is tactic which includes expenses that remain unchanged till particular

production level. Depreciation, rent and other costs are part of fixed cost which even occur when

there is no manufacturing process occurring in firm.

4

Management accounting system is internal management system in which organization

measures and analyse performance of management. Components of this system are budgets,

reports of return on investments, sales analysis, balance scorecard and activity based accounting.

This system is useful for management in efficient decision making, assists in planning process,

budgeting through focusing on specific costs and responsibilities, making work flows and

processes prompt, ease in find data by centralizes, organize and creating structure of it, ability to

generate useful trend analysis and special reports. Actual internal performance of management is

then compared with planned to find variances.

D1 Critical evaluation on management accounting report integrated within organisational process

Management accounting systems and management accounting reports are different in

context of reporting because former provides relevant information to internal users like

management but later to outsiders like stockholders, creditors, employees, government etc. Both

these are integrated in organizational context because both practices presents information in

report format so that they data can be easily compared between firms. Another similarity

between both these are that they requires specialized knowledge and expertise in accounting

field. Both these help organization to present health of business to take financial decisions and

present information more formally.

TASK 2

P3 Calculation of costs using techniques of cost analysis

Cost refer to process which is executed by management to have knowledge about value

of money incurred for conduction of business activities in company. It is essential that each and

every firm have adequate funds for having sufficient resources that is material and manpower in

firm. Executive of GreenTech uses cost analysis techniques to compute costs which are executed

while production of products and services. Thus, fixed and variable are two forms of costs which

are stated below (Kumarasiri and Jubb, 2016):

Fixed cost: It is tactic which includes expenses that remain unchanged till particular

production level. Depreciation, rent and other costs are part of fixed cost which even occur when

there is no manufacturing process occurring in firm.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable cost: This is another form of cost which depend on business operations and

keeps on varying with production process. Employees, material, electricity, transportation, etc.

are variable expenses which rely on production level in company.

Marginal costing: It is an additional cost incurred for a production of extra unit of an

output. It indicates a rate at which total cost of a product changes as per increase in production

by one unit of product. It happens because fixed cost do not change as per increase in no. of

products. The marginal cost is generally influenced by variations in variable costs. It is mainly

important in decision-making process where management of a company has to take decisions

related to allocation of resources in the production process (Maskell, Baggaley and Grasso,

2016).

Absorption costing : It is a cost accounting method for valuing inventory which includes

all manufacturing cost of a product (both fixed and variable costs). It gives a more

comprehensive and accurate view on how much it really costs to produce your inventory. The

major components of absorption costing are: Direct material, direct labour, variable

manufacturing overhead and fixed manufacturing overhead. Therefore, absorption costing is

used to allocate overhead costs for inventory valuation purpose. It is a time-consuming and

expensive costing system.

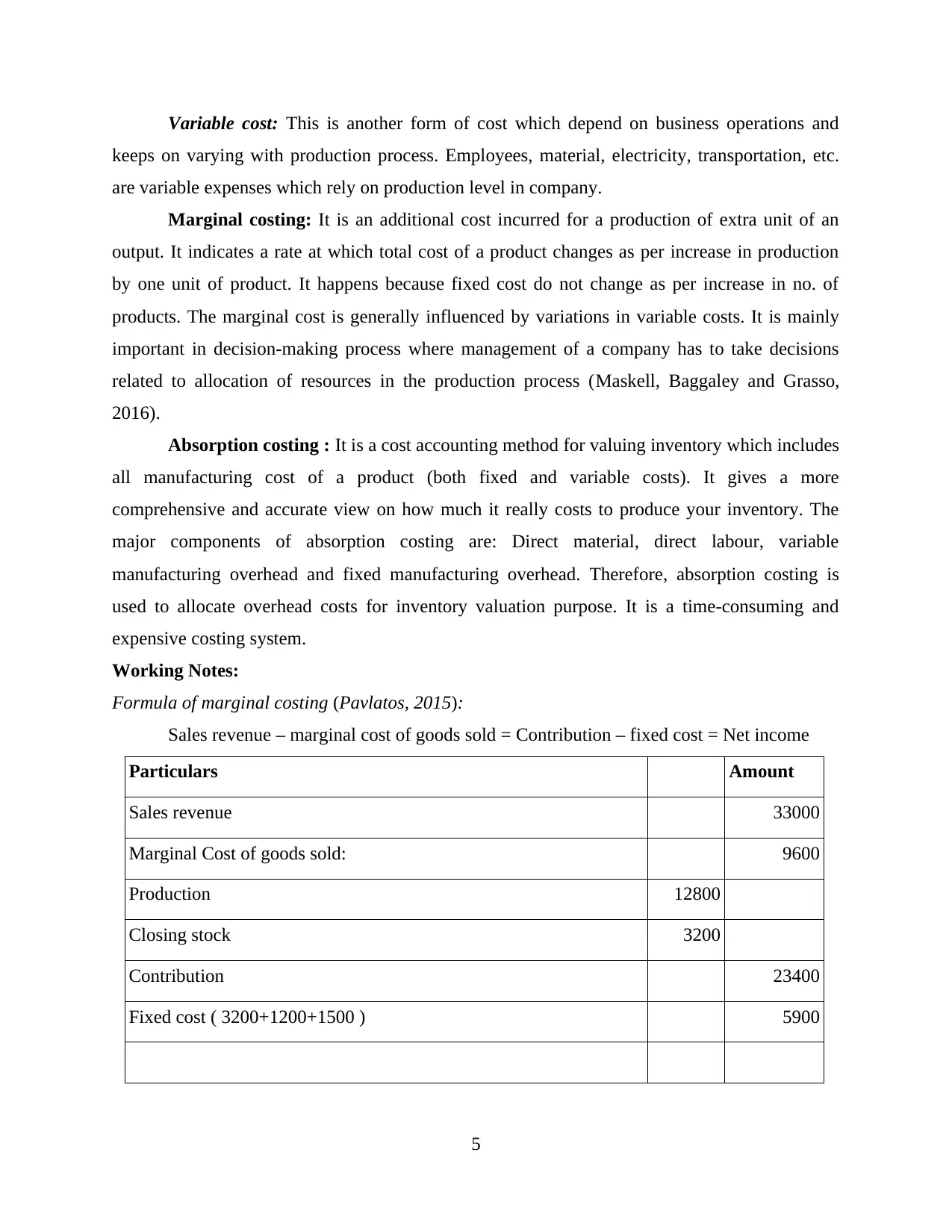

Working Notes:

Formula of marginal costing (Pavlatos, 2015):

Sales revenue – marginal cost of goods sold = Contribution – fixed cost = Net income

Particulars Amount

Sales revenue 33000

Marginal Cost of goods sold: 9600

Production 12800

Closing stock 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

5

keeps on varying with production process. Employees, material, electricity, transportation, etc.

are variable expenses which rely on production level in company.

Marginal costing: It is an additional cost incurred for a production of extra unit of an

output. It indicates a rate at which total cost of a product changes as per increase in production

by one unit of product. It happens because fixed cost do not change as per increase in no. of

products. The marginal cost is generally influenced by variations in variable costs. It is mainly

important in decision-making process where management of a company has to take decisions

related to allocation of resources in the production process (Maskell, Baggaley and Grasso,

2016).

Absorption costing : It is a cost accounting method for valuing inventory which includes

all manufacturing cost of a product (both fixed and variable costs). It gives a more

comprehensive and accurate view on how much it really costs to produce your inventory. The

major components of absorption costing are: Direct material, direct labour, variable

manufacturing overhead and fixed manufacturing overhead. Therefore, absorption costing is

used to allocate overhead costs for inventory valuation purpose. It is a time-consuming and

expensive costing system.

Working Notes:

Formula of marginal costing (Pavlatos, 2015):

Sales revenue – marginal cost of goods sold = Contribution – fixed cost = Net income

Particulars Amount

Sales revenue 33000

Marginal Cost of goods sold: 9600

Production 12800

Closing stock 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

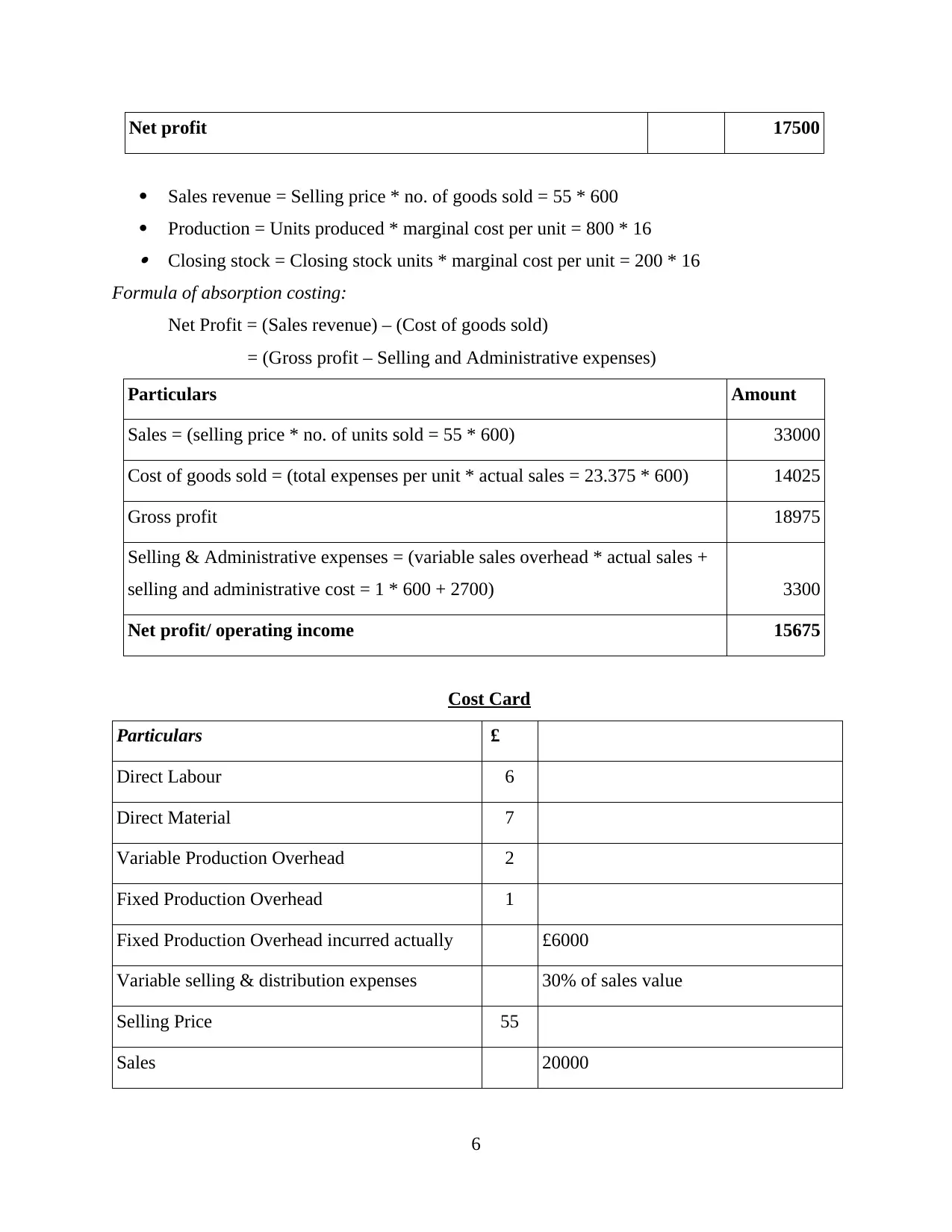

Net profit 17500

Sales revenue = Selling price * no. of goods sold = 55 * 600

Production = Units produced * marginal cost per unit = 800 * 16 Closing stock = Closing stock units * marginal cost per unit = 200 * 16

Formula of absorption costing:

Net Profit = (Sales revenue) – (Cost of goods sold)

= (Gross profit – Selling and Administrative expenses)

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Cost Card

Particulars £

Direct Labour 6

Direct Material 7

Variable Production Overhead 2

Fixed Production Overhead 1

Fixed Production Overhead incurred actually £6000

Variable selling & distribution expenses 30% of sales value

Selling Price 55

Sales 20000

6

Sales revenue = Selling price * no. of goods sold = 55 * 600

Production = Units produced * marginal cost per unit = 800 * 16 Closing stock = Closing stock units * marginal cost per unit = 200 * 16

Formula of absorption costing:

Net Profit = (Sales revenue) – (Cost of goods sold)

= (Gross profit – Selling and Administrative expenses)

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Cost Card

Particulars £

Direct Labour 6

Direct Material 7

Variable Production Overhead 2

Fixed Production Overhead 1

Fixed Production Overhead incurred actually £6000

Variable selling & distribution expenses 30% of sales value

Selling Price 55

Sales 20000

6

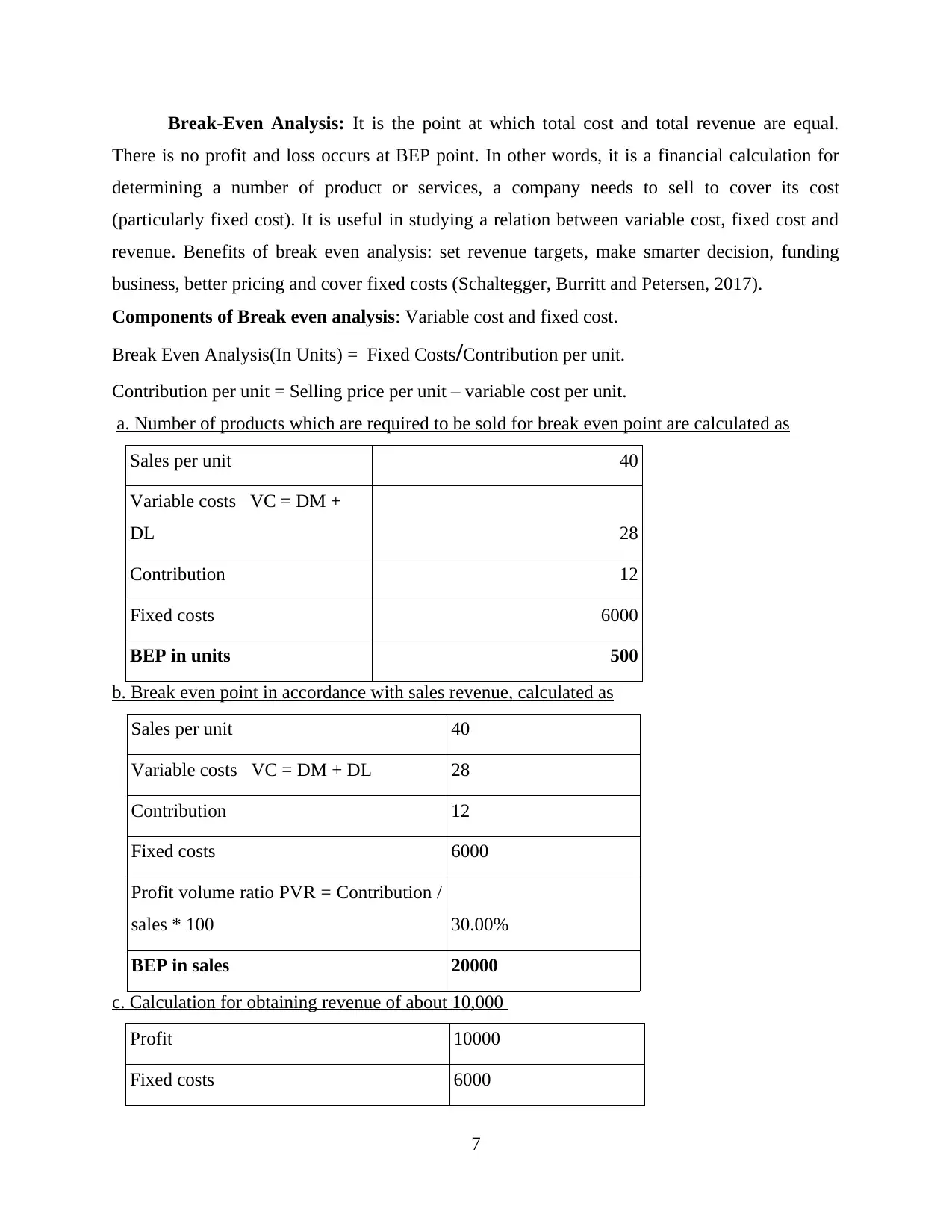

Break-Even Analysis: It is the point at which total cost and total revenue are equal.

There is no profit and loss occurs at BEP point. In other words, it is a financial calculation for

determining a number of product or services, a company needs to sell to cover its cost

(particularly fixed cost). It is useful in studying a relation between variable cost, fixed cost and

revenue. Benefits of break even analysis: set revenue targets, make smarter decision, funding

business, better pricing and cover fixed costs (Schaltegger, Burritt and Petersen, 2017).

Components of Break even analysis: Variable cost and fixed cost.

Break Even Analysis(In Units) = Fixed Costs/Contribution per unit.

Contribution per unit = Selling price per unit – variable cost per unit.

a. Number of products which are required to be sold for break even point are calculated as

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Break even point in accordance with sales revenue, calculated as

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. Calculation for obtaining revenue of about 10,000

Profit 10000

Fixed costs 6000

7

There is no profit and loss occurs at BEP point. In other words, it is a financial calculation for

determining a number of product or services, a company needs to sell to cover its cost

(particularly fixed cost). It is useful in studying a relation between variable cost, fixed cost and

revenue. Benefits of break even analysis: set revenue targets, make smarter decision, funding

business, better pricing and cover fixed costs (Schaltegger, Burritt and Petersen, 2017).

Components of Break even analysis: Variable cost and fixed cost.

Break Even Analysis(In Units) = Fixed Costs/Contribution per unit.

Contribution per unit = Selling price per unit – variable cost per unit.

a. Number of products which are required to be sold for break even point are calculated as

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Break even point in accordance with sales revenue, calculated as

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. Calculation for obtaining revenue of about 10,000

Profit 10000

Fixed costs 6000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

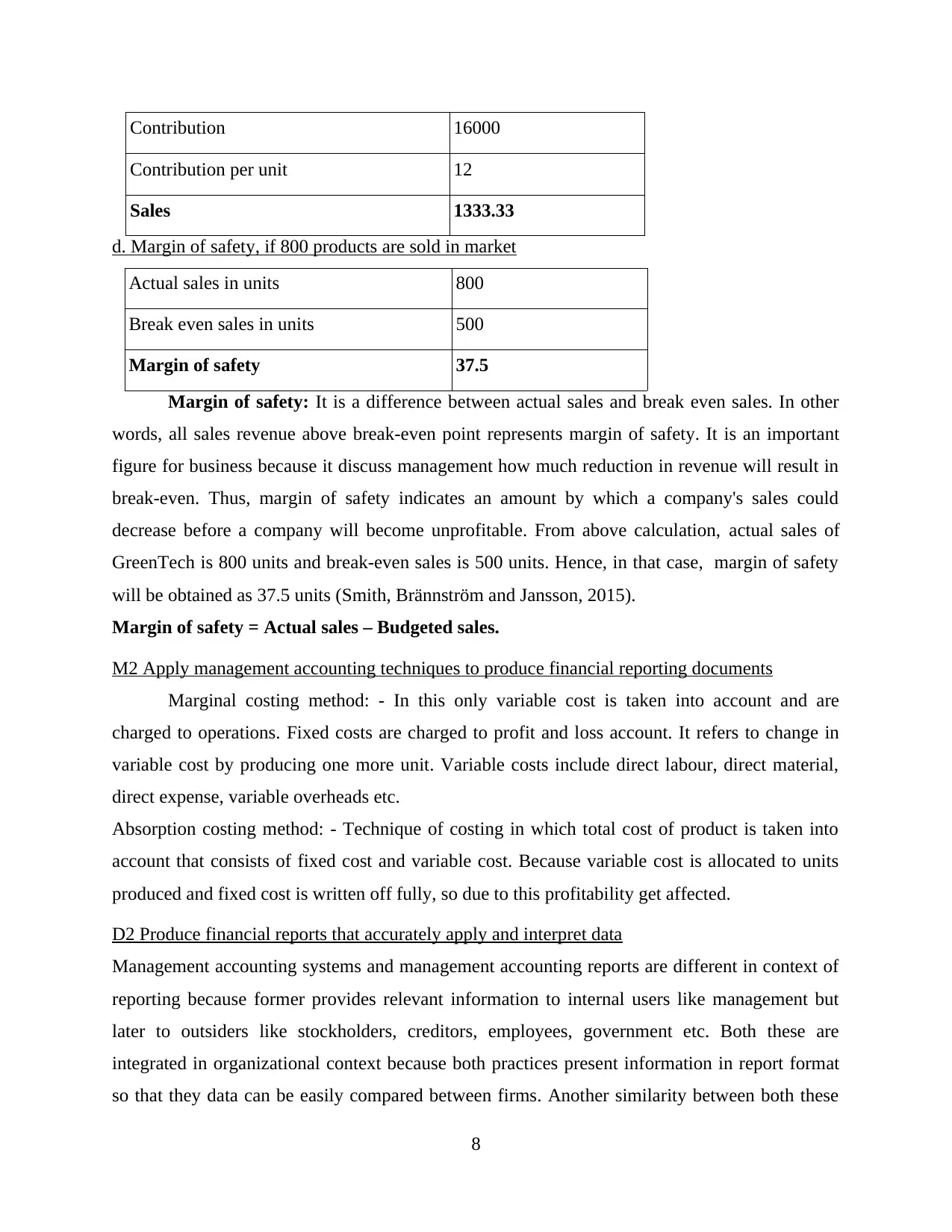

Contribution 16000

Contribution per unit 12

Sales 1333.33

d. Margin of safety, if 800 products are sold in market

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety: It is a difference between actual sales and break even sales. In other

words, all sales revenue above break-even point represents margin of safety. It is an important

figure for business because it discuss management how much reduction in revenue will result in

break-even. Thus, margin of safety indicates an amount by which a company's sales could

decrease before a company will become unprofitable. From above calculation, actual sales of

GreenTech is 800 units and break-even sales is 500 units. Hence, in that case, margin of safety

will be obtained as 37.5 units (Smith, Brännström and Jansson, 2015).

Margin of safety = Actual sales – Budgeted sales.

M2 Apply management accounting techniques to produce financial reporting documents

Marginal costing method: - In this only variable cost is taken into account and are

charged to operations. Fixed costs are charged to profit and loss account. It refers to change in

variable cost by producing one more unit. Variable costs include direct labour, direct material,

direct expense, variable overheads etc.

Absorption costing method: - Technique of costing in which total cost of product is taken into

account that consists of fixed cost and variable cost. Because variable cost is allocated to units

produced and fixed cost is written off fully, so due to this profitability get affected.

D2 Produce financial reports that accurately apply and interpret data

Management accounting systems and management accounting reports are different in context of

reporting because former provides relevant information to internal users like management but

later to outsiders like stockholders, creditors, employees, government etc. Both these are

integrated in organizational context because both practices present information in report format

so that they data can be easily compared between firms. Another similarity between both these

8

Contribution per unit 12

Sales 1333.33

d. Margin of safety, if 800 products are sold in market

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety: It is a difference between actual sales and break even sales. In other

words, all sales revenue above break-even point represents margin of safety. It is an important

figure for business because it discuss management how much reduction in revenue will result in

break-even. Thus, margin of safety indicates an amount by which a company's sales could

decrease before a company will become unprofitable. From above calculation, actual sales of

GreenTech is 800 units and break-even sales is 500 units. Hence, in that case, margin of safety

will be obtained as 37.5 units (Smith, Brännström and Jansson, 2015).

Margin of safety = Actual sales – Budgeted sales.

M2 Apply management accounting techniques to produce financial reporting documents

Marginal costing method: - In this only variable cost is taken into account and are

charged to operations. Fixed costs are charged to profit and loss account. It refers to change in

variable cost by producing one more unit. Variable costs include direct labour, direct material,

direct expense, variable overheads etc.

Absorption costing method: - Technique of costing in which total cost of product is taken into

account that consists of fixed cost and variable cost. Because variable cost is allocated to units

produced and fixed cost is written off fully, so due to this profitability get affected.

D2 Produce financial reports that accurately apply and interpret data

Management accounting systems and management accounting reports are different in context of

reporting because former provides relevant information to internal users like management but

later to outsiders like stockholders, creditors, employees, government etc. Both these are

integrated in organizational context because both practices present information in report format

so that they data can be easily compared between firms. Another similarity between both these

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are that they require specialized knowledge and expertise in accounting field. Both these help

organizations to present health of business to take financial decisions and present information

more formally.

TASK 3

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Budgetary control is process by which organization's finance and expenses are controlled

by management. Actual outcomes are compared with budgeted figures which help them to have

information about variances. This helps executive to utilise money efficiently and save funds for

future uses. In GreenTech, budgetary control system aid business person to enhance profitability

of firm. For this, budget is prepared, coordination of departments and its activities, comparison

of actual performance with standard are undertaken (Trucco, 2015). This aid them to control

activities which can affect on accomplishment of business objectives and targets. Besides this,

management is also able to make changes in system to utilise market opportunities. Thus, they

are able to expand business to higher level and make success in respect to competitors.

Businesses are present in dynamic environment so there are different forms of risks that

occur at workplace and affect on budget of firm. Natural disasters, climatic changes, global

events such as pandemic (influenza, swine flu), technology failure and many other are factors

which danger which influence on sales and profitability. GreenTech is small company which

require to sustain its position and image in market. It is necessary that business person handle

upcomin risks and factors to manage business functionality. For this, budget controlling are used

by management to execute operations effectively. Thus, these are different planning tools are

mentioned below (Agrawal and Cooper, 2017):

Forecasting planning tool: This technique aid executive to use present and past data for

overcome from future uncertainties. It is process in which management make assumptions which

are based on their experience, judgement and knowledge. Potential issues and problems which

have possibility of occurrence in future are ascertained by executive of GreenTech. For this,

qualitative observation and quantitative data are used by them to collect information (Definition

of forecasting, 2018). Beside this, operations management techniques are used by seniors to

acknowledge actions through which favourable outcomes are gained by firm. Development in

9

organizations to present health of business to take financial decisions and present information

more formally.

TASK 3

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Budgetary control is process by which organization's finance and expenses are controlled

by management. Actual outcomes are compared with budgeted figures which help them to have

information about variances. This helps executive to utilise money efficiently and save funds for

future uses. In GreenTech, budgetary control system aid business person to enhance profitability

of firm. For this, budget is prepared, coordination of departments and its activities, comparison

of actual performance with standard are undertaken (Trucco, 2015). This aid them to control

activities which can affect on accomplishment of business objectives and targets. Besides this,

management is also able to make changes in system to utilise market opportunities. Thus, they

are able to expand business to higher level and make success in respect to competitors.

Businesses are present in dynamic environment so there are different forms of risks that

occur at workplace and affect on budget of firm. Natural disasters, climatic changes, global

events such as pandemic (influenza, swine flu), technology failure and many other are factors

which danger which influence on sales and profitability. GreenTech is small company which

require to sustain its position and image in market. It is necessary that business person handle

upcomin risks and factors to manage business functionality. For this, budget controlling are used

by management to execute operations effectively. Thus, these are different planning tools are

mentioned below (Agrawal and Cooper, 2017):

Forecasting planning tool: This technique aid executive to use present and past data for

overcome from future uncertainties. It is process in which management make assumptions which

are based on their experience, judgement and knowledge. Potential issues and problems which

have possibility of occurrence in future are ascertained by executive of GreenTech. For this,

qualitative observation and quantitative data are used by them to collect information (Definition

of forecasting, 2018). Beside this, operations management techniques are used by seniors to

acknowledge actions through which favourable outcomes are gained by firm. Development in

9

existing and new items and services are conducted to fulfil demands and needs of people. Thus,

company is able to recover from situations which might happen in future.

Advantage Disadvantages

Forecasting helps management of GreenTech

to protect firm from future uncertainties. It is

efficient method as past data are used to

acknowledge strengths of system. Besides this,

investigator have good experience and

qualification which help them to make accurate

results about future conditions.

This method have certain demerit which are

related with correct prediction of future.

GreenTech is small firm so management is not

able to properly predict changes which are

occurring in market (Banker and et. al., 2014).

Contingency Planning Tools: This is another technique which is used by organisation to

respond to situation which may happen in future. It is tactic through which risk management,

disaster recovery and business continuity are maintained. GreenTech is small firm which require

to sustain in its market reputation and create brand value. For this, executive need to make

policies and design system through which they are able to maintain sustainability of company.

Advantage Disadvantage

Contingency planning helps management of

GreenTech to inform staff members about

tasks and duties required to be conducted by

them. This aid them to encourage subordinates

to handle and work effectively in disaster

situation (Christ and Burritt, 2017).

Since this type of plan require much time and

cost, it is not affordable for small firms.

Therefore, this plan is appropriate to be used by

manager of GreenTech.

M3 Use of planning tools and application for preparing and forecasting budgets

Different planning tools like costing tools, pricing tools, budgeting tools, profitability analysis

tool, investment decision making, and other operational tools help in preparing budgets. As from

costing tool, company can analyse costs. Flexible and fixed budget assists in analysing costs

related to budgets. Flexible budget does not change with output of goods produced and fixed

budget changes with production level.

10

company is able to recover from situations which might happen in future.

Advantage Disadvantages

Forecasting helps management of GreenTech

to protect firm from future uncertainties. It is

efficient method as past data are used to

acknowledge strengths of system. Besides this,

investigator have good experience and

qualification which help them to make accurate

results about future conditions.

This method have certain demerit which are

related with correct prediction of future.

GreenTech is small firm so management is not

able to properly predict changes which are

occurring in market (Banker and et. al., 2014).

Contingency Planning Tools: This is another technique which is used by organisation to

respond to situation which may happen in future. It is tactic through which risk management,

disaster recovery and business continuity are maintained. GreenTech is small firm which require

to sustain in its market reputation and create brand value. For this, executive need to make

policies and design system through which they are able to maintain sustainability of company.

Advantage Disadvantage

Contingency planning helps management of

GreenTech to inform staff members about

tasks and duties required to be conducted by

them. This aid them to encourage subordinates

to handle and work effectively in disaster

situation (Christ and Burritt, 2017).

Since this type of plan require much time and

cost, it is not affordable for small firms.

Therefore, this plan is appropriate to be used by

manager of GreenTech.

M3 Use of planning tools and application for preparing and forecasting budgets

Different planning tools like costing tools, pricing tools, budgeting tools, profitability analysis

tool, investment decision making, and other operational tools help in preparing budgets. As from

costing tool, company can analyse costs. Flexible and fixed budget assists in analysing costs

related to budgets. Flexible budget does not change with output of goods produced and fixed

budget changes with production level.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.