Report on Management Accounting Techniques, GSK Costing Strategies

VerifiedAdded on 2023/01/12

|9

|1905

|25

Report

AI Summary

This report provides a comprehensive overview of management accounting practices at GlaxoSmithKline (GSK). It begins with an introduction to management accounting, highlighting its importance in planning, execution, and control of operations, with a focus on decision-making. The report examines various management accounting techniques employed by GSK, including cost accounting, inventory management, budgetary control, and break-even analysis. It then delves into the application of absorption costing and activity-based costing (ABC) techniques, providing detailed income statements for both methods. The analysis interprets the findings from these costing methods and recommends future costing strategies for GSK, advocating for the adoption of absorption costing. The report concludes by emphasizing the critical role of management accounting in achieving organizational growth and success.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

REPORT..........................................................................................................................................1

1. Management accounting and its importance of GSK..............................................................1

2. Management accounting available for GSK............................................................................2

3. Application of Absorption costing and activity based costing technique................................3

4. Interpretation of the findings and recommendation of the future costing strategy for GSK.. .4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

APPENDICES.................................................................................................................................7

Calculations.................................................................................................................................7

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

REPORT..........................................................................................................................................1

1. Management accounting and its importance of GSK..............................................................1

2. Management accounting available for GSK............................................................................2

3. Application of Absorption costing and activity based costing technique................................3

4. Interpretation of the findings and recommendation of the future costing strategy for GSK.. .4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

APPENDICES.................................................................................................................................7

Calculations.................................................................................................................................7

INTRODUTION

Management accounting is an accounting approach concerned with identifying, gathering,

analysing, interpreting and preparation of the financial reports. Management is concerned with

the objective of effectively managing the operations of company for increasing the productivity

keeping the costs to minimum. The report is based over GSK that is a manufacturer of innovative

pharmaceuticals medicines, vaccines and consumer health products. Company has the objective

of becoming the most innovative, best performing and the trusted healthcare products. The report

will provide the different management accounting techniques used by GSK. It will also provide

the costing strategy that could be used by company for achieving its objective.

REPORT

1. Management accounting and its importance of GSK

Management Accounting, its nature and scope.

Management accounting is concerned with task of planning, executions and controlling

the operating activities of enterprise. It works on the accounting information of the enterprise.

Management accounting provides information important for decision making of the enterprise.

Nature of management accounting is concerned with furnishing accounting information for

making management decisions. There are not set principles to be followed by the organisation

under management accounting like the financial accounting (Otley, 2016). Scope of

management accounting is concerned with the presentation of the accounting information useful

for management operations. It has a vast scope that includes almost every aspect of business

enterprise.

Importance of management accounting.

Management accounting is very essential as it assists the management for making

effective decisions. It provides accounting information serving vital source of the data in

management planning. Reports and accounts provided by MA forms bridge between financial

and other parts of business. Management accounting helps in pricing the products after

considering all the market conditions. Various cost accounting techniques are used for

calculating the cost of product to decide the profits margins. Manager using MA identifies the

area of improvements and take appropriate corrective strategies for achieving the growth of

GSK. It consists of various techniques used for monitoring and controlling the cost and

expenditures.

1

Management accounting is an accounting approach concerned with identifying, gathering,

analysing, interpreting and preparation of the financial reports. Management is concerned with

the objective of effectively managing the operations of company for increasing the productivity

keeping the costs to minimum. The report is based over GSK that is a manufacturer of innovative

pharmaceuticals medicines, vaccines and consumer health products. Company has the objective

of becoming the most innovative, best performing and the trusted healthcare products. The report

will provide the different management accounting techniques used by GSK. It will also provide

the costing strategy that could be used by company for achieving its objective.

REPORT

1. Management accounting and its importance of GSK

Management Accounting, its nature and scope.

Management accounting is concerned with task of planning, executions and controlling

the operating activities of enterprise. It works on the accounting information of the enterprise.

Management accounting provides information important for decision making of the enterprise.

Nature of management accounting is concerned with furnishing accounting information for

making management decisions. There are not set principles to be followed by the organisation

under management accounting like the financial accounting (Otley, 2016). Scope of

management accounting is concerned with the presentation of the accounting information useful

for management operations. It has a vast scope that includes almost every aspect of business

enterprise.

Importance of management accounting.

Management accounting is very essential as it assists the management for making

effective decisions. It provides accounting information serving vital source of the data in

management planning. Reports and accounts provided by MA forms bridge between financial

and other parts of business. Management accounting helps in pricing the products after

considering all the market conditions. Various cost accounting techniques are used for

calculating the cost of product to decide the profits margins. Manager using MA identifies the

area of improvements and take appropriate corrective strategies for achieving the growth of

GSK. It consists of various techniques used for monitoring and controlling the cost and

expenditures.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting is application of concepts and techniques for the projection of

projected and historical data for assisting the management to establish the plans for reasonable

economic objectives. This helps the management in taking rationale decisions for the attainment

of these objectives of the organisation. It is different from financial accounting that prepares for

external users that are known as financial statements mainly consisting of income statement,

balance sheet and cash flow. On the management accounting prepares report for the internal

users. This play a critical role in management of operations for achieving the desired goals and

objectives of GSK.

2. Management accounting available for GSK

Management accounting consists of various techniques used by GSK for managing its

operations.

Cost Accounting

Cost accounting is an important management accounting technique used by the

management for calculating the cost of product. It is concerned with ascertaining the cost of

different products manufactured by GSK for deciding the profit margins associated with the

product. It involves various costing techniques such as marginal costing, standard costing, direct

costing, activity based costing and other costing techniques for valuing its inventory and

recording the accounting transactions. Objective of cost accounting is to analyse the cost

associated with different products in detailed manner for identifying the areas of improvement.

On the basis of analysis done by GSK it takes operational and strategic decision for

improvements in the given areas

Inventory management

It is a management accounting technique used by GSK for having proper track of all the

inventory movements within the company. Inventory management is defined as the system used

by management for recording all the transactions and movements of enterprise. It contains

information elated to each and every type of inventory from company assets, raw materials, work

in progress and the finished goods. It is used by company for having detailed information

regarding the flow of inventory within and outside the firm. This provide important information

useful in decision making (Cooper,Ezzamel and Qu, 2017). It is possible to analyse the

frequency of inventory movements on the basis of which organisation place different purchase

orders for smooth running of productions and prevents from overstocking of raw materials or

2

projected and historical data for assisting the management to establish the plans for reasonable

economic objectives. This helps the management in taking rationale decisions for the attainment

of these objectives of the organisation. It is different from financial accounting that prepares for

external users that are known as financial statements mainly consisting of income statement,

balance sheet and cash flow. On the management accounting prepares report for the internal

users. This play a critical role in management of operations for achieving the desired goals and

objectives of GSK.

2. Management accounting available for GSK

Management accounting consists of various techniques used by GSK for managing its

operations.

Cost Accounting

Cost accounting is an important management accounting technique used by the

management for calculating the cost of product. It is concerned with ascertaining the cost of

different products manufactured by GSK for deciding the profit margins associated with the

product. It involves various costing techniques such as marginal costing, standard costing, direct

costing, activity based costing and other costing techniques for valuing its inventory and

recording the accounting transactions. Objective of cost accounting is to analyse the cost

associated with different products in detailed manner for identifying the areas of improvement.

On the basis of analysis done by GSK it takes operational and strategic decision for

improvements in the given areas

Inventory management

It is a management accounting technique used by GSK for having proper track of all the

inventory movements within the company. Inventory management is defined as the system used

by management for recording all the transactions and movements of enterprise. It contains

information elated to each and every type of inventory from company assets, raw materials, work

in progress and the finished goods. It is used by company for having detailed information

regarding the flow of inventory within and outside the firm. This provide important information

useful in decision making (Cooper,Ezzamel and Qu, 2017). It is possible to analyse the

frequency of inventory movements on the basis of which organisation place different purchase

orders for smooth running of productions and prevents from overstocking of raw materials or

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

finished goods.

Budgetary control

Budgetary is one of the important technique of management accounting that is concerned

with heading the company towards a defined direction. Management accounting uses this for

preparation of various budgets. Budgets are prepared by GSK on the basis of previous budgets.

Adjustments are made for preparation of the budgets of current year. These adjustments are

related with inflations, market conditions, consumer behaviours and such other factors. At the

end of periods budgeted figures are compared with the actual production figures for measuring

the variances. Management takes effective corrective steps for reducing the variances between

the budgeted and actual outputs (Weetman, 2019). Budgeting helps GSK in keeping control over

the cost and expenditures. It is also referred as the spending plan of the organisation that helps in

effective allocation of the resources among various departments.

Break Even Analysis

It is a financial tool used by organisation for determining the point where the product or

services of company will be profitable. This may also be referred as the financial calculation to

determines the number of products or service to be sold for covering the costs mainly the fixed

cost. This is very essential in decision making purposes.

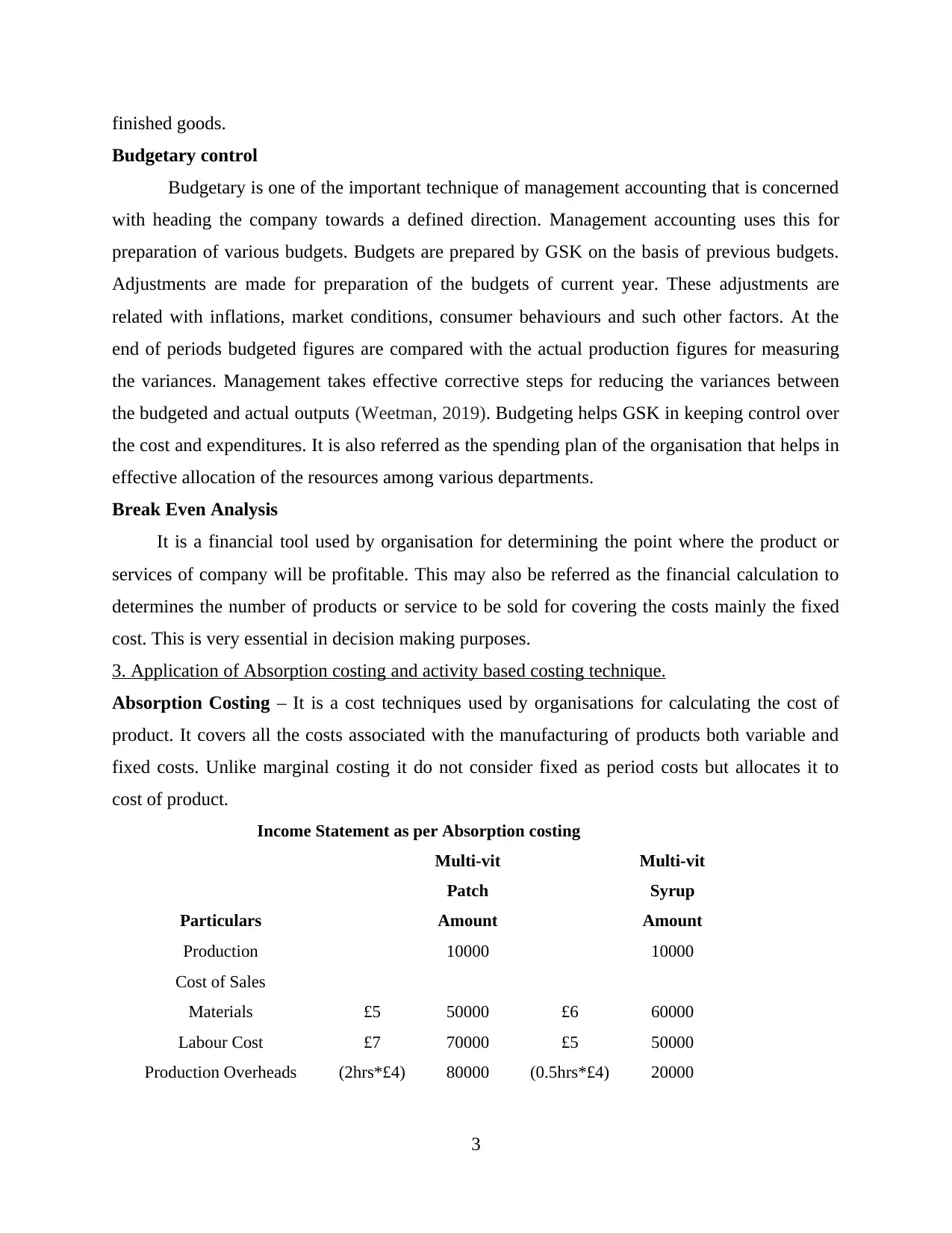

3. Application of Absorption costing and activity based costing technique.

Absorption Costing – It is a cost techniques used by organisations for calculating the cost of

product. It covers all the costs associated with the manufacturing of products both variable and

fixed costs. Unlike marginal costing it do not consider fixed as period costs but allocates it to

cost of product.

Income Statement as per Absorption costing

Multi-vit

Patch

Multi-vit

Syrup

Particulars Amount Amount

Production 10000 10000

Cost of Sales

Materials £5 50000 £6 60000

Labour Cost £7 70000 £5 50000

Production Overheads (2hrs*£4) 80000 (0.5hrs*£4) 20000

3

Budgetary control

Budgetary is one of the important technique of management accounting that is concerned

with heading the company towards a defined direction. Management accounting uses this for

preparation of various budgets. Budgets are prepared by GSK on the basis of previous budgets.

Adjustments are made for preparation of the budgets of current year. These adjustments are

related with inflations, market conditions, consumer behaviours and such other factors. At the

end of periods budgeted figures are compared with the actual production figures for measuring

the variances. Management takes effective corrective steps for reducing the variances between

the budgeted and actual outputs (Weetman, 2019). Budgeting helps GSK in keeping control over

the cost and expenditures. It is also referred as the spending plan of the organisation that helps in

effective allocation of the resources among various departments.

Break Even Analysis

It is a financial tool used by organisation for determining the point where the product or

services of company will be profitable. This may also be referred as the financial calculation to

determines the number of products or service to be sold for covering the costs mainly the fixed

cost. This is very essential in decision making purposes.

3. Application of Absorption costing and activity based costing technique.

Absorption Costing – It is a cost techniques used by organisations for calculating the cost of

product. It covers all the costs associated with the manufacturing of products both variable and

fixed costs. Unlike marginal costing it do not consider fixed as period costs but allocates it to

cost of product.

Income Statement as per Absorption costing

Multi-vit

Patch

Multi-vit

Syrup

Particulars Amount Amount

Production 10000 10000

Cost of Sales

Materials £5 50000 £6 60000

Labour Cost £7 70000 £5 50000

Production Overheads (2hrs*£4) 80000 (0.5hrs*£4) 20000

3

Cost of Production 200000 130000

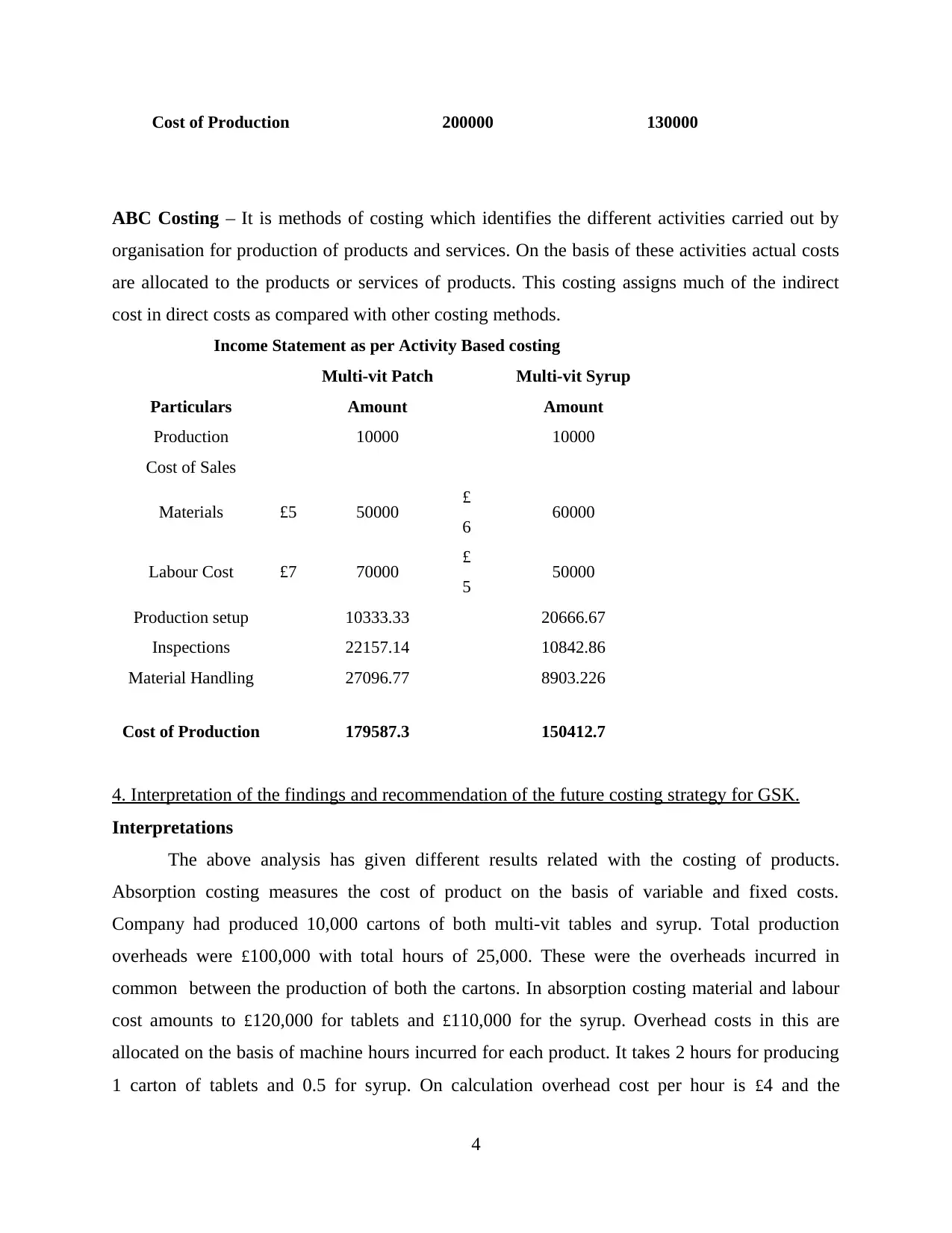

ABC Costing – It is methods of costing which identifies the different activities carried out by

organisation for production of products and services. On the basis of these activities actual costs

are allocated to the products or services of products. This costing assigns much of the indirect

cost in direct costs as compared with other costing methods.

Income Statement as per Activity Based costing

Multi-vit Patch Multi-vit Syrup

Particulars Amount Amount

Production 10000 10000

Cost of Sales

Materials £5 50000 £

6 60000

Labour Cost £7 70000 £

5 50000

Production setup 10333.33 20666.67

Inspections 22157.14 10842.86

Material Handling 27096.77 8903.226

Cost of Production 179587.3 150412.7

4. Interpretation of the findings and recommendation of the future costing strategy for GSK.

Interpretations

The above analysis has given different results related with the costing of products.

Absorption costing measures the cost of product on the basis of variable and fixed costs.

Company had produced 10,000 cartons of both multi-vit tables and syrup. Total production

overheads were £100,000 with total hours of 25,000. These were the overheads incurred in

common between the production of both the cartons. In absorption costing material and labour

cost amounts to £120,000 for tablets and £110,000 for the syrup. Overhead costs in this are

allocated on the basis of machine hours incurred for each product. It takes 2 hours for producing

1 carton of tablets and 0.5 for syrup. On calculation overhead cost per hour is £4 and the

4

ABC Costing – It is methods of costing which identifies the different activities carried out by

organisation for production of products and services. On the basis of these activities actual costs

are allocated to the products or services of products. This costing assigns much of the indirect

cost in direct costs as compared with other costing methods.

Income Statement as per Activity Based costing

Multi-vit Patch Multi-vit Syrup

Particulars Amount Amount

Production 10000 10000

Cost of Sales

Materials £5 50000 £

6 60000

Labour Cost £7 70000 £

5 50000

Production setup 10333.33 20666.67

Inspections 22157.14 10842.86

Material Handling 27096.77 8903.226

Cost of Production 179587.3 150412.7

4. Interpretation of the findings and recommendation of the future costing strategy for GSK.

Interpretations

The above analysis has given different results related with the costing of products.

Absorption costing measures the cost of product on the basis of variable and fixed costs.

Company had produced 10,000 cartons of both multi-vit tables and syrup. Total production

overheads were £100,000 with total hours of 25,000. These were the overheads incurred in

common between the production of both the cartons. In absorption costing material and labour

cost amounts to £120,000 for tablets and £110,000 for the syrup. Overhead costs in this are

allocated on the basis of machine hours incurred for each product. It takes 2 hours for producing

1 carton of tablets and 0.5 for syrup. On calculation overhead cost per hour is £4 and the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

allocation of total overhead is done on the basis of time taken for the production of each carton.

Overheads are allocated as 80,000 for tablets and 20,000 for syrup amounting to 100,000 in

total.

Under ABC costs are allocated as per different activities not on the variable and fixed.

Cost of material and labour remains same under both the methods that amount to 120000 for

tablets and 110000 for the syrup. Overhead costs are not allocated on the basis of machine hours

but on the basis of cost driver associated with different cost of activities (Hopper and Bui, 2016).

It carries out set up for machines, inspections and the material movements. Allocations are

segregated on the basis of separate cost drivers that caused cost of production to tablets to reduce

and for syrups to increase.

Recommendation of the cost strategy.

GSK should adopt for absorption costing as its cost strategy. Absorption costing makes

proper allocation of the overheads on the basis of machine hours that are incurred for the

production of both the cartons. ABC costing includes indirect costs like material handling into

direct costs that are indirect in actual that do not give clear bifurcation of the costs between

variable and fixed costs. Absorption costing is accepted by the accounting standards and

reporting frameworks for valuation of the inventory also. Therefore GSK should adopt for

absorption costing as the costing strategy for achieving the goal of organisation.

CONCLUSION

From the above study it could be concluded that management accounting plays an important

role in the growth and success of organisation. It concludes various concepts and techniques that

helps the managers in keeping its costs and expenditures under control for increasing the

productivity and efficiency.

5

Overheads are allocated as 80,000 for tablets and 20,000 for syrup amounting to 100,000 in

total.

Under ABC costs are allocated as per different activities not on the variable and fixed.

Cost of material and labour remains same under both the methods that amount to 120000 for

tablets and 110000 for the syrup. Overhead costs are not allocated on the basis of machine hours

but on the basis of cost driver associated with different cost of activities (Hopper and Bui, 2016).

It carries out set up for machines, inspections and the material movements. Allocations are

segregated on the basis of separate cost drivers that caused cost of production to tablets to reduce

and for syrups to increase.

Recommendation of the cost strategy.

GSK should adopt for absorption costing as its cost strategy. Absorption costing makes

proper allocation of the overheads on the basis of machine hours that are incurred for the

production of both the cartons. ABC costing includes indirect costs like material handling into

direct costs that are indirect in actual that do not give clear bifurcation of the costs between

variable and fixed costs. Absorption costing is accepted by the accounting standards and

reporting frameworks for valuation of the inventory also. Therefore GSK should adopt for

absorption costing as the costing strategy for achieving the goal of organisation.

CONCLUSION

From the above study it could be concluded that management accounting plays an important

role in the growth and success of organisation. It concludes various concepts and techniques that

helps the managers in keeping its costs and expenditures under control for increasing the

productivity and efficiency.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research.31.pp.45-62.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a management accounting idea: The

case of the balanced scorecard. Contemporary Accounting Research.34(2).pp.991-1025.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research.31. pp.10-30.

6

Books and Journals

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research.31.pp.45-62.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a management accounting idea: The

case of the balanced scorecard. Contemporary Accounting Research.34(2).pp.991-1025.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research.31. pp.10-30.

6

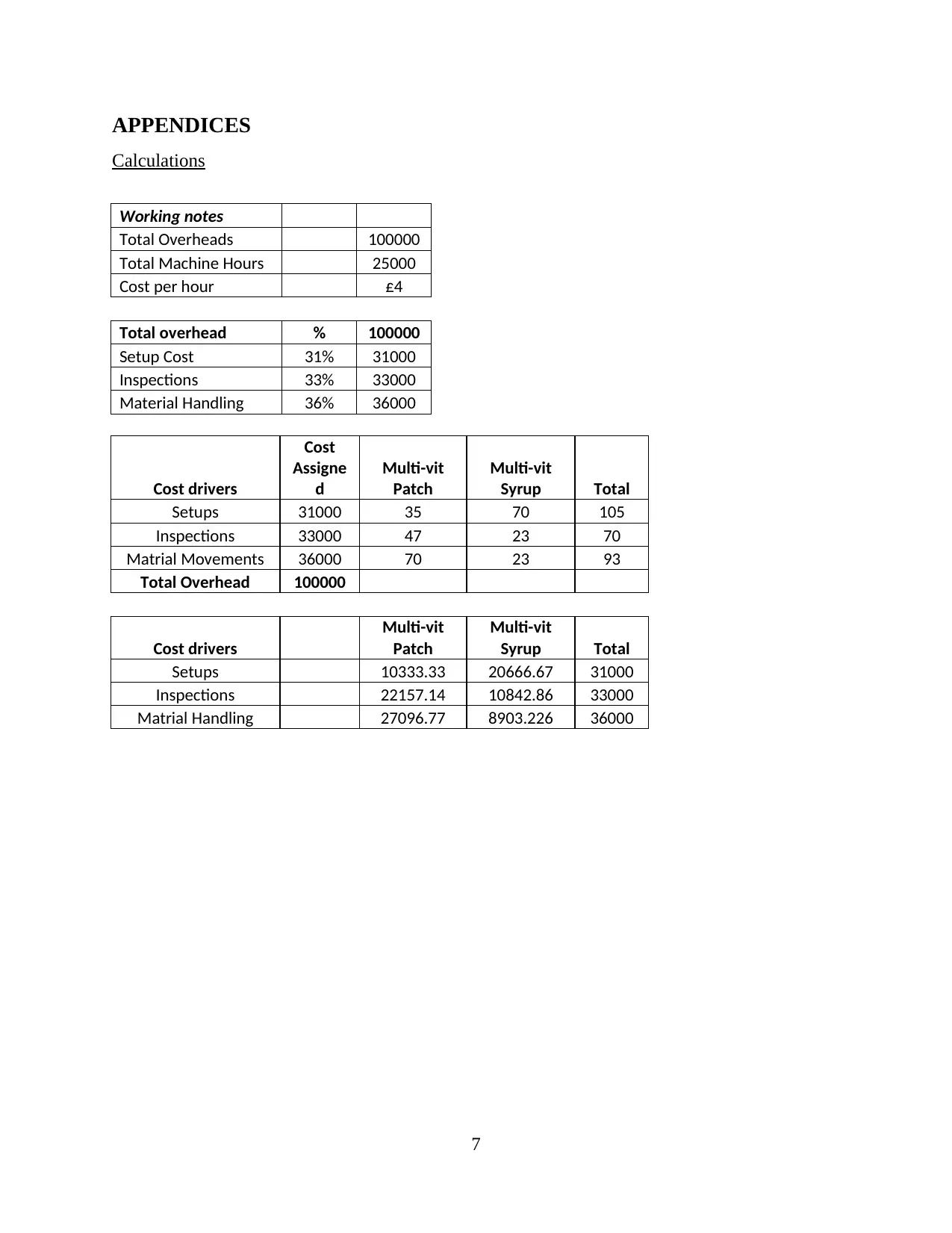

APPENDICES

Calculations

Working notes

Total Overheads 100000

Total Machine Hours 25000

Cost per hour £4

Total overhead % 100000

Setup Cost 31% 31000

Inspections 33% 33000

Material Handling 36% 36000

Cost drivers

Cost

Assigne

d

Multi-vit

Patch

Multi-vit

Syrup Total

Setups 31000 35 70 105

Inspections 33000 47 23 70

Matrial Movements 36000 70 23 93

Total Overhead 100000

Cost drivers

Multi-vit

Patch

Multi-vit

Syrup Total

Setups 10333.33 20666.67 31000

Inspections 22157.14 10842.86 33000

Matrial Handling 27096.77 8903.226 36000

7

Calculations

Working notes

Total Overheads 100000

Total Machine Hours 25000

Cost per hour £4

Total overhead % 100000

Setup Cost 31% 31000

Inspections 33% 33000

Material Handling 36% 36000

Cost drivers

Cost

Assigne

d

Multi-vit

Patch

Multi-vit

Syrup Total

Setups 31000 35 70 105

Inspections 33000 47 23 70

Matrial Movements 36000 70 23 93

Total Overhead 100000

Cost drivers

Multi-vit

Patch

Multi-vit

Syrup Total

Setups 10333.33 20666.67 31000

Inspections 22157.14 10842.86 33000

Matrial Handling 27096.77 8903.226 36000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.