Management Accounting Application at GSQ Limited: A Detailed Report

VerifiedAdded on 2023/01/12

|11

|2345

|88

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices at GSQ Limited, a UK-based company. It begins by defining management accounting and its importance, outlining various management accounting systems such as cost accounting, price optimization, inventory management, and job costing. The report details different types of management accounting reports, including budget reports, accounts receivable reports, cost management reports, and performance reports. It then presents an income statement using both marginal and absorption costing techniques, interpreting the results. Furthermore, the report discusses the advantages and disadvantages of different planning tools used for budgetary control, such as zero-based budgeting, activity-based budgeting, and rolling budgeting. Finally, it explores how management accounting systems can be used to solve financial problems, highlighting the use of key performance indicators, benchmarking, and financial governance. The conclusion emphasizes the essential role of management accounting in achieving organizational goals and improving resource utilization.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK1.............................................................................................................................................1

P1 Explanation of meaning of management accounting and importance of different types of

management accounting system..................................................................................................1

P2 Explanation of different types of management accounting reporting system........................1

TASK2.............................................................................................................................................1

P3Income statement using marginal and absorption costing.......................................................1

TASK3.............................................................................................................................................1

P4 Explanation of advantages and disadvantages of different types of planning tools used

for budgetary control...................................................................................................................1

TASK4.............................................................................................................................................1

P5 Uses of management accounting system to solve financial problem.....................................1

CONCLUSION................................................................................................................................1

REFRENCES...................................................................................................................................1

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK1.............................................................................................................................................1

P1 Explanation of meaning of management accounting and importance of different types of

management accounting system..................................................................................................1

P2 Explanation of different types of management accounting reporting system........................1

TASK2.............................................................................................................................................1

P3Income statement using marginal and absorption costing.......................................................1

TASK3.............................................................................................................................................1

P4 Explanation of advantages and disadvantages of different types of planning tools used

for budgetary control...................................................................................................................1

TASK4.............................................................................................................................................1

P5 Uses of management accounting system to solve financial problem.....................................1

CONCLUSION................................................................................................................................1

REFRENCES...................................................................................................................................1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a technique used by business organizations for better utilization

of accounting information. In other words it is used by manger to take effective decision for

achieving business organizations objective. To understand the concept of management

accounting in a better way GSQ limited has been taken, it is situated in United Kingdom. In

this report meaning of managerial accounting, and uses of management accounting system

in order to maintain sustainability in organization. This report also explain uses of

managerial accounting techniques , planning tools to control budget and how management

accounting tool s help in solve financial problems.

TASK1

P1 Explanation of meaning of management accounting and importance of different types of

management accounting system.

Definition of man

Management accounting: Management is an art of planning, organizing, coordinating,

directing and controlling business activites in a way which help in built strong position in

market. On the other side accounting is systematic procedure of recording, analysing,

collecting and submitting and communicating accounting data as information to mangers.

Management accounting the word is combination of management accounting, which

describe as uses of accounting information in managerial way to take effective decision for

attain future objective of business entity. In other words, management accounting is

(Carlsson-Wall, Kraus, and Lind, 2015).

branch of accounts which uses to analysis operational cost of business activites and

formulate financial reports in order to help mangers for their decision making procedure.

GSQ limited can be used different types of managerial accounting system to improve their

business performance, following are various types of management accounting system:

COST ACCOUNITNG SYSYEM: It is a framework which is used by business

organizations to identified cost of manufacturing products. Managers uses various

costing methods in order to analysis their cost, they uses standard costing, marginal

costing, job, costing, bench costing for calculation of cost rate. Manager of GSQ

limited use this cost accounting system in order to increase their profitability rate, it

1

Management accounting is a technique used by business organizations for better utilization

of accounting information. In other words it is used by manger to take effective decision for

achieving business organizations objective. To understand the concept of management

accounting in a better way GSQ limited has been taken, it is situated in United Kingdom. In

this report meaning of managerial accounting, and uses of management accounting system

in order to maintain sustainability in organization. This report also explain uses of

managerial accounting techniques , planning tools to control budget and how management

accounting tool s help in solve financial problems.

TASK1

P1 Explanation of meaning of management accounting and importance of different types of

management accounting system.

Definition of man

Management accounting: Management is an art of planning, organizing, coordinating,

directing and controlling business activites in a way which help in built strong position in

market. On the other side accounting is systematic procedure of recording, analysing,

collecting and submitting and communicating accounting data as information to mangers.

Management accounting the word is combination of management accounting, which

describe as uses of accounting information in managerial way to take effective decision for

attain future objective of business entity. In other words, management accounting is

(Carlsson-Wall, Kraus, and Lind, 2015).

branch of accounts which uses to analysis operational cost of business activites and

formulate financial reports in order to help mangers for their decision making procedure.

GSQ limited can be used different types of managerial accounting system to improve their

business performance, following are various types of management accounting system:

COST ACCOUNITNG SYSYEM: It is a framework which is used by business

organizations to identified cost of manufacturing products. Managers uses various

costing methods in order to analysis their cost, they uses standard costing, marginal

costing, job, costing, bench costing for calculation of cost rate. Manager of GSQ

limited use this cost accounting system in order to increase their profitability rate, it

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will help in identifying activites which incurred high cost, mangers make policies

through which they cut high cost generating activites.

1. Price optimization system: Business organizations use price optimization system

to determine price of their manufacturing products. It is a tool which included all

methods of calculating selling price of particular products. Managers decide their

products process after evaluate external market. Manager of GSQ limited uses

these policies related to price which fully satisfy their customer , they decide rate

of product through which they can attain financial gain by selling products at their

decided price rate. Mangers use various pricing policies they use price orientation,

price policies.

2. Inventory management system: This system is used to control inventory level of

an running organization in order to maintain their sustainability. Inventory

considered all raw material and goods use by business for manufacturing and

selling their products. In inventory management system, different kind of tools, and

techniques are adopted by mangers to identify maximum, minimum, an dangerous

level of stock. Manager of GSQ limited will be used EOQ, ABC analysis to

analysis their level of stock and t maintain their stock level. Inventory management

system will be help in optimum utilization of their resource and it will control

wastage activities (Wouters, and Kirchberger, 2015).

3. Job costing system: It is essential tool of managerial accounting system. It is a tool

which help in identify cost of each product manufacturing by business

organization. This type of system implemented in their organization which

produce product according to special demand of their customers. GSQ limited will

be used this technique when they produce special product the demand of their

potential customers.

2

through which they cut high cost generating activites.

1. Price optimization system: Business organizations use price optimization system

to determine price of their manufacturing products. It is a tool which included all

methods of calculating selling price of particular products. Managers decide their

products process after evaluate external market. Manager of GSQ limited uses

these policies related to price which fully satisfy their customer , they decide rate

of product through which they can attain financial gain by selling products at their

decided price rate. Mangers use various pricing policies they use price orientation,

price policies.

2. Inventory management system: This system is used to control inventory level of

an running organization in order to maintain their sustainability. Inventory

considered all raw material and goods use by business for manufacturing and

selling their products. In inventory management system, different kind of tools, and

techniques are adopted by mangers to identify maximum, minimum, an dangerous

level of stock. Manager of GSQ limited will be used EOQ, ABC analysis to

analysis their level of stock and t maintain their stock level. Inventory management

system will be help in optimum utilization of their resource and it will control

wastage activities (Wouters, and Kirchberger, 2015).

3. Job costing system: It is essential tool of managerial accounting system. It is a tool

which help in identify cost of each product manufacturing by business

organization. This type of system implemented in their organization which

produce product according to special demand of their customers. GSQ limited will

be used this technique when they produce special product the demand of their

potential customers.

2

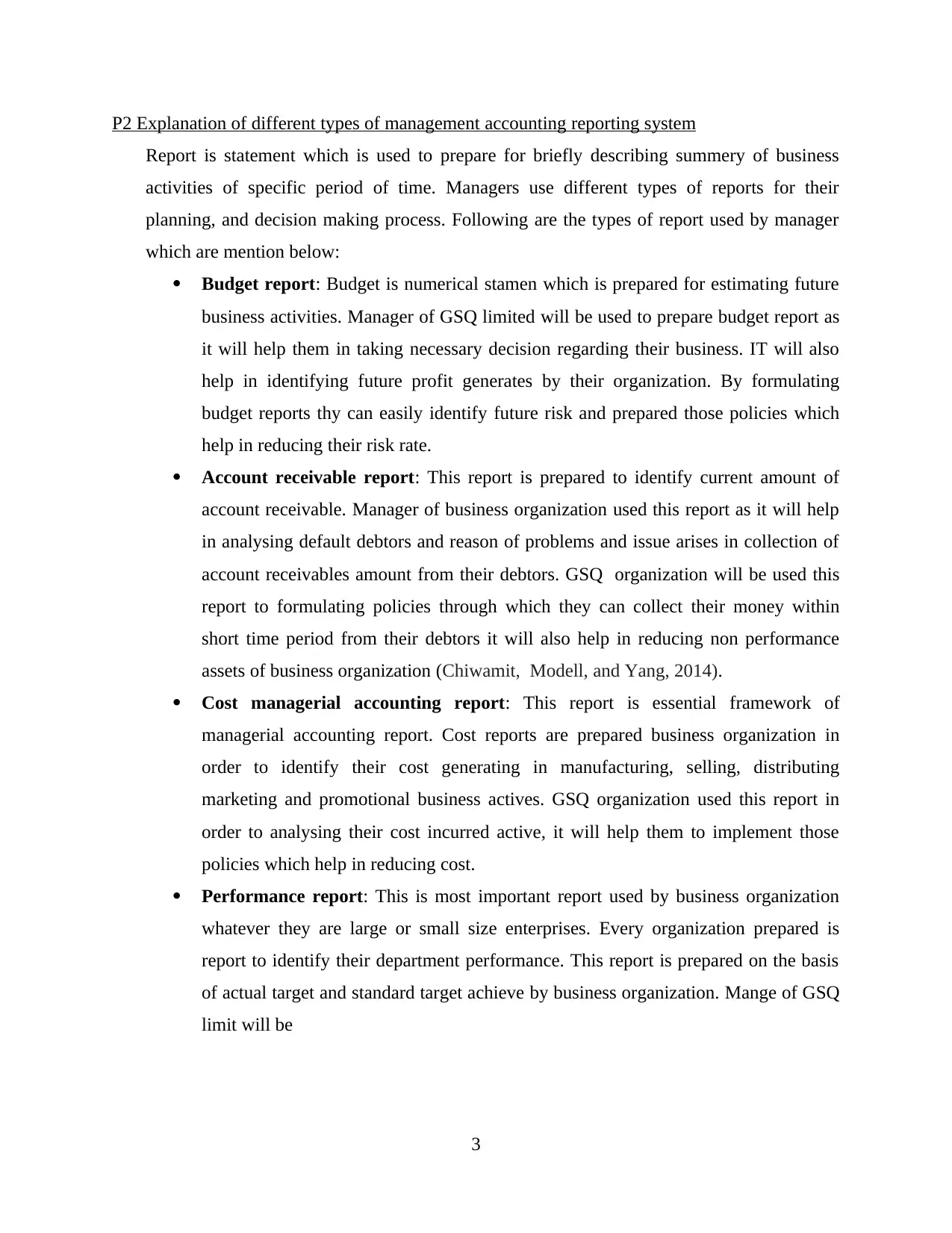

P2 Explanation of different types of management accounting reporting system

Report is statement which is used to prepare for briefly describing summery of business

activities of specific period of time. Managers use different types of reports for their

planning, and decision making process. Following are the types of report used by manager

which are mention below:

Budget report: Budget is numerical stamen which is prepared for estimating future

business activities. Manager of GSQ limited will be used to prepare budget report as

it will help them in taking necessary decision regarding their business. IT will also

help in identifying future profit generates by their organization. By formulating

budget reports thy can easily identify future risk and prepared those policies which

help in reducing their risk rate.

Account receivable report: This report is prepared to identify current amount of

account receivable. Manager of business organization used this report as it will help

in analysing default debtors and reason of problems and issue arises in collection of

account receivables amount from their debtors. GSQ organization will be used this

report to formulating policies through which they can collect their money within

short time period from their debtors it will also help in reducing non performance

assets of business organization (Chiwamit, Modell, and Yang, 2014).

Cost managerial accounting report: This report is essential framework of

managerial accounting report. Cost reports are prepared business organization in

order to identify their cost generating in manufacturing, selling, distributing

marketing and promotional business actives. GSQ organization used this report in

order to analysing their cost incurred active, it will help them to implement those

policies which help in reducing cost.

Performance report: This is most important report used by business organization

whatever they are large or small size enterprises. Every organization prepared is

report to identify their department performance. This report is prepared on the basis

of actual target and standard target achieve by business organization. Mange of GSQ

limit will be

3

Report is statement which is used to prepare for briefly describing summery of business

activities of specific period of time. Managers use different types of reports for their

planning, and decision making process. Following are the types of report used by manager

which are mention below:

Budget report: Budget is numerical stamen which is prepared for estimating future

business activities. Manager of GSQ limited will be used to prepare budget report as

it will help them in taking necessary decision regarding their business. IT will also

help in identifying future profit generates by their organization. By formulating

budget reports thy can easily identify future risk and prepared those policies which

help in reducing their risk rate.

Account receivable report: This report is prepared to identify current amount of

account receivable. Manager of business organization used this report as it will help

in analysing default debtors and reason of problems and issue arises in collection of

account receivables amount from their debtors. GSQ organization will be used this

report to formulating policies through which they can collect their money within

short time period from their debtors it will also help in reducing non performance

assets of business organization (Chiwamit, Modell, and Yang, 2014).

Cost managerial accounting report: This report is essential framework of

managerial accounting report. Cost reports are prepared business organization in

order to identify their cost generating in manufacturing, selling, distributing

marketing and promotional business actives. GSQ organization used this report in

order to analysing their cost incurred active, it will help them to implement those

policies which help in reducing cost.

Performance report: This is most important report used by business organization

whatever they are large or small size enterprises. Every organization prepared is

report to identify their department performance. This report is prepared on the basis

of actual target and standard target achieve by business organization. Mange of GSQ

limit will be

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

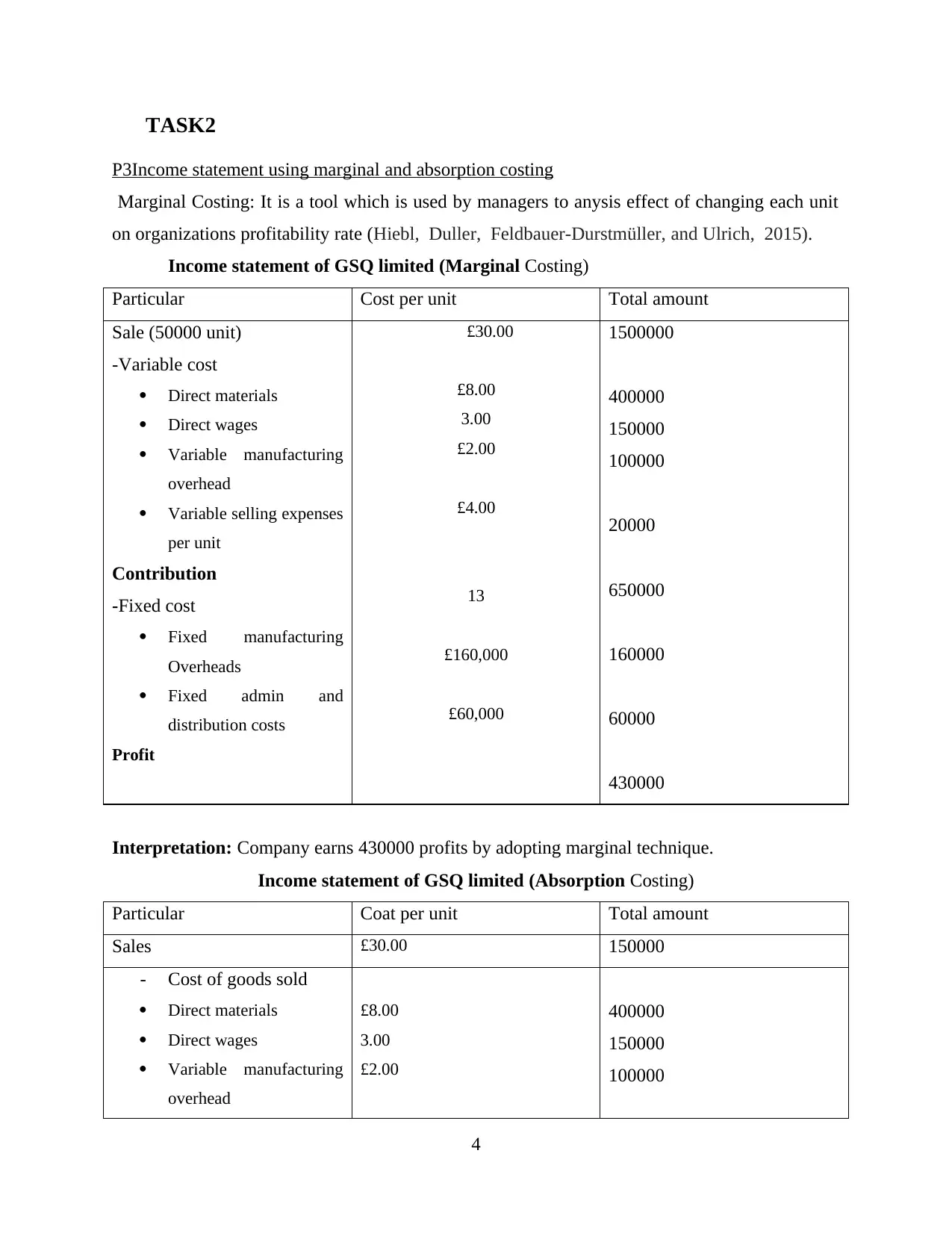

TASK2

P3Income statement using marginal and absorption costing

Marginal Costing: It is a tool which is used by managers to anysis effect of changing each unit

on organizations profitability rate (Hiebl, Duller, Feldbauer-Durstmüller, and Ulrich, 2015).

Income statement of GSQ limited (Marginal Costing)

Particular Cost per unit Total amount

Sale (50000 unit)

-Variable cost

Direct materials

Direct wages

Variable manufacturing

overhead

Variable selling expenses

per unit

Contribution

-Fixed cost

Fixed manufacturing

Overheads

Fixed admin and

distribution costs

Profit

£30.00

£8.00

3.00

£2.00

£4.00

13

£160,000

£60,000

1500000

400000

150000

100000

20000

650000

160000

60000

430000

Interpretation: Company earns 430000 profits by adopting marginal technique.

Income statement of GSQ limited (Absorption Costing)

Particular Coat per unit Total amount

Sales £30.00 150000

- Cost of goods sold

Direct materials

Direct wages

Variable manufacturing

overhead

£8.00

3.00

£2.00

400000

150000

100000

4

P3Income statement using marginal and absorption costing

Marginal Costing: It is a tool which is used by managers to anysis effect of changing each unit

on organizations profitability rate (Hiebl, Duller, Feldbauer-Durstmüller, and Ulrich, 2015).

Income statement of GSQ limited (Marginal Costing)

Particular Cost per unit Total amount

Sale (50000 unit)

-Variable cost

Direct materials

Direct wages

Variable manufacturing

overhead

Variable selling expenses

per unit

Contribution

-Fixed cost

Fixed manufacturing

Overheads

Fixed admin and

distribution costs

Profit

£30.00

£8.00

3.00

£2.00

£4.00

13

£160,000

£60,000

1500000

400000

150000

100000

20000

650000

160000

60000

430000

Interpretation: Company earns 430000 profits by adopting marginal technique.

Income statement of GSQ limited (Absorption Costing)

Particular Coat per unit Total amount

Sales £30.00 150000

- Cost of goods sold

Direct materials

Direct wages

Variable manufacturing

overhead

£8.00

3.00

£2.00

400000

150000

100000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

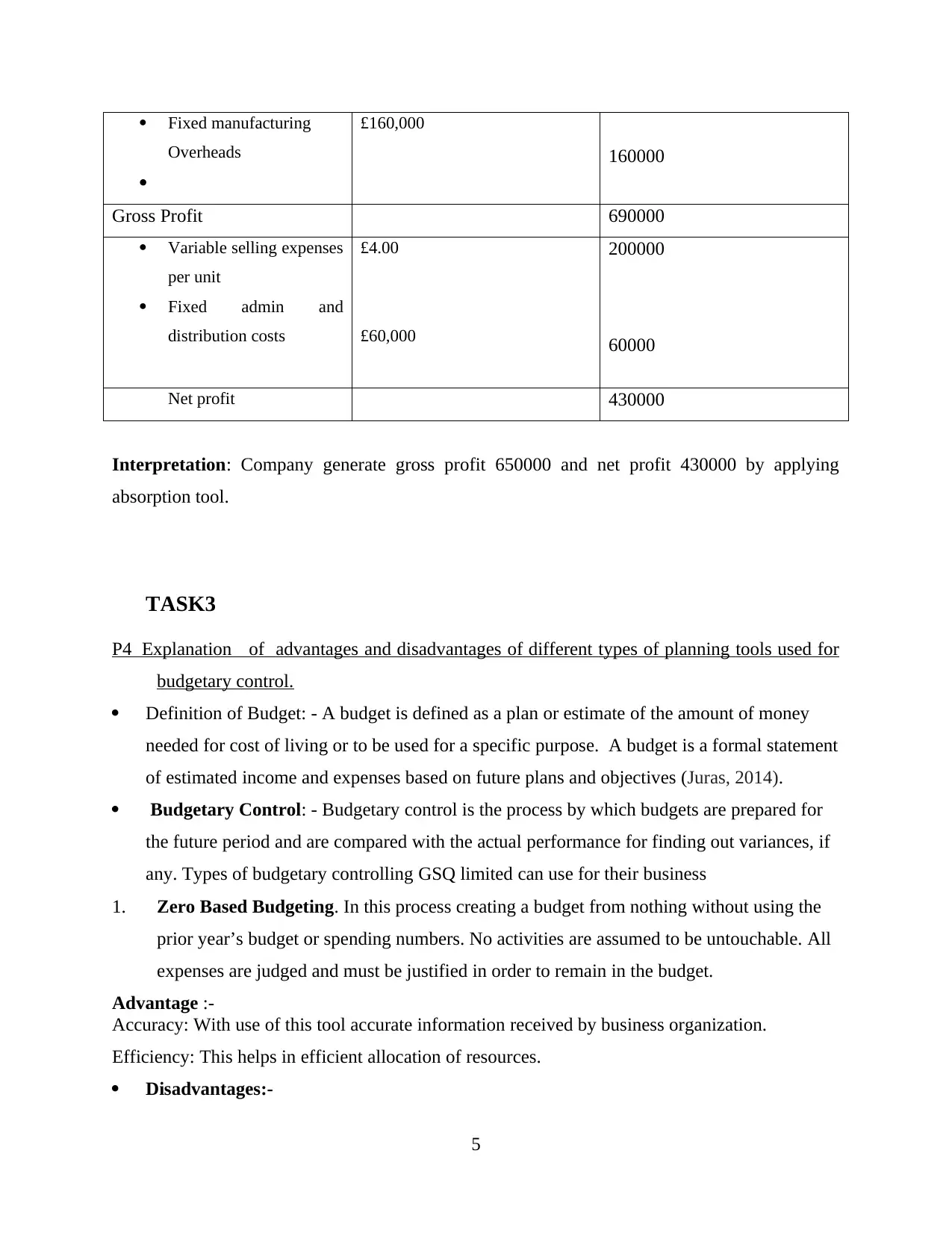

Fixed manufacturing

Overheads

£160,000

160000

Gross Profit 690000

Variable selling expenses

per unit

Fixed admin and

distribution costs

£4.00

£60,000

200000

60000

Net profit 430000

Interpretation: Company generate gross profit 650000 and net profit 430000 by applying

absorption tool.

TASK3

P4 Explanation of advantages and disadvantages of different types of planning tools used for

budgetary control.

Definition of Budget: - A budget is defined as a plan or estimate of the amount of money

needed for cost of living or to be used for a specific purpose. A budget is a formal statement

of estimated income and expenses based on future plans and objectives (Juras, 2014).

Budgetary Control: - Budgetary control is the process by which budgets are prepared for

the future period and are compared with the actual performance for finding out variances, if

any. Types of budgetary controlling GSQ limited can use for their business

1. Zero Based Budgeting. In this process creating a budget from nothing without using the

prior year’s budget or spending numbers. No activities are assumed to be untouchable. All

expenses are judged and must be justified in order to remain in the budget.

Advantage :-

Accuracy: With use of this tool accurate information received by business organization.

Efficiency: This helps in efficient allocation of resources.

Disadvantages:-

5

Overheads

£160,000

160000

Gross Profit 690000

Variable selling expenses

per unit

Fixed admin and

distribution costs

£4.00

£60,000

200000

60000

Net profit 430000

Interpretation: Company generate gross profit 650000 and net profit 430000 by applying

absorption tool.

TASK3

P4 Explanation of advantages and disadvantages of different types of planning tools used for

budgetary control.

Definition of Budget: - A budget is defined as a plan or estimate of the amount of money

needed for cost of living or to be used for a specific purpose. A budget is a formal statement

of estimated income and expenses based on future plans and objectives (Juras, 2014).

Budgetary Control: - Budgetary control is the process by which budgets are prepared for

the future period and are compared with the actual performance for finding out variances, if

any. Types of budgetary controlling GSQ limited can use for their business

1. Zero Based Budgeting. In this process creating a budget from nothing without using the

prior year’s budget or spending numbers. No activities are assumed to be untouchable. All

expenses are judged and must be justified in order to remain in the budget.

Advantage :-

Accuracy: With use of this tool accurate information received by business organization.

Efficiency: This helps in efficient allocation of resources.

Disadvantages:-

5

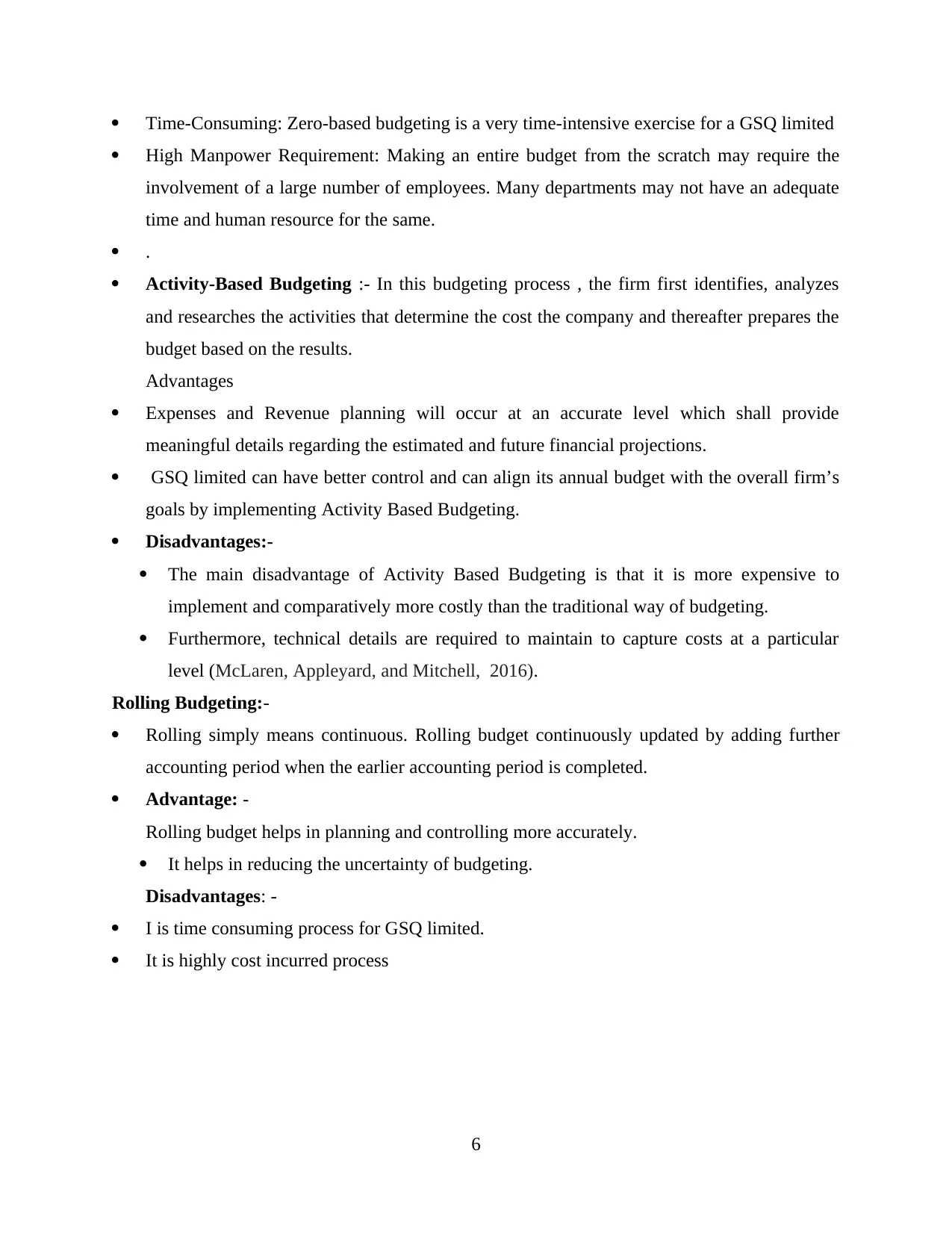

Time-Consuming: Zero-based budgeting is a very time-intensive exercise for a GSQ limited

High Manpower Requirement: Making an entire budget from the scratch may require the

involvement of a large number of employees. Many departments may not have an adequate

time and human resource for the same.

.

Activity-Based Budgeting :- In this budgeting process , the firm first identifies, analyzes

and researches the activities that determine the cost the company and thereafter prepares the

budget based on the results.

Advantages

Expenses and Revenue planning will occur at an accurate level which shall provide

meaningful details regarding the estimated and future financial projections.

GSQ limited can have better control and can align its annual budget with the overall firm’s

goals by implementing Activity Based Budgeting.

Disadvantages:-

The main disadvantage of Activity Based Budgeting is that it is more expensive to

implement and comparatively more costly than the traditional way of budgeting.

Furthermore, technical details are required to maintain to capture costs at a particular

level (McLaren, Appleyard, and Mitchell, 2016).

Rolling Budgeting:-

Rolling simply means continuous. Rolling budget continuously updated by adding further

accounting period when the earlier accounting period is completed.

Advantage: -

Rolling budget helps in planning and controlling more accurately.

It helps in reducing the uncertainty of budgeting.

Disadvantages: -

I is time consuming process for GSQ limited.

It is highly cost incurred process

6

High Manpower Requirement: Making an entire budget from the scratch may require the

involvement of a large number of employees. Many departments may not have an adequate

time and human resource for the same.

.

Activity-Based Budgeting :- In this budgeting process , the firm first identifies, analyzes

and researches the activities that determine the cost the company and thereafter prepares the

budget based on the results.

Advantages

Expenses and Revenue planning will occur at an accurate level which shall provide

meaningful details regarding the estimated and future financial projections.

GSQ limited can have better control and can align its annual budget with the overall firm’s

goals by implementing Activity Based Budgeting.

Disadvantages:-

The main disadvantage of Activity Based Budgeting is that it is more expensive to

implement and comparatively more costly than the traditional way of budgeting.

Furthermore, technical details are required to maintain to capture costs at a particular

level (McLaren, Appleyard, and Mitchell, 2016).

Rolling Budgeting:-

Rolling simply means continuous. Rolling budget continuously updated by adding further

accounting period when the earlier accounting period is completed.

Advantage: -

Rolling budget helps in planning and controlling more accurately.

It helps in reducing the uncertainty of budgeting.

Disadvantages: -

I is time consuming process for GSQ limited.

It is highly cost incurred process

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK4

P5 Uses of management accounting system to solve financial problem

Financial Problem: It is a situation in which organizations suffers from many issues due to

lack of money. Small and medium size enterprises faced financial problem during period of

industrial life cycle. GSQ is facing financial problem due to their lack of managerial decion

and increase rate of non payment of debtors. Their manger should be used management

accountings tools to solve their problem through following ways:

Key performance indicator: It is a tool which is used to analysis how effectively company

achieve their target at fixed time. Manger of GSQ uses this tool to identify effect of their

managerial policy, with the use of this tool they implement effective mange3rial policies.

Bench marking: In this technique manger compare their achieved goal with standard goal.

GSQ limited use it to identify number of default debtor and then make policies through

which defaulters pay their money within sure time period (Nelson, and Miller, 2014).

Financial governance: This tool is used to make sure that business organizations should

follow ethical rules and regulation, they monitor each activity of business organizations.

CONCLUSION

From the above analysis it has been concluded that managerial accounting process play

essential part in running successful business organization. It will help manager to uses

accounting information in a way which will help in reducing cost and taken effective

investment decision through with they utilized their resource effectively. Business

organizations use Management accounting techniques and tools in order to achieve their

predetermine goal at fixed time.

7

P5 Uses of management accounting system to solve financial problem

Financial Problem: It is a situation in which organizations suffers from many issues due to

lack of money. Small and medium size enterprises faced financial problem during period of

industrial life cycle. GSQ is facing financial problem due to their lack of managerial decion

and increase rate of non payment of debtors. Their manger should be used management

accountings tools to solve their problem through following ways:

Key performance indicator: It is a tool which is used to analysis how effectively company

achieve their target at fixed time. Manger of GSQ uses this tool to identify effect of their

managerial policy, with the use of this tool they implement effective mange3rial policies.

Bench marking: In this technique manger compare their achieved goal with standard goal.

GSQ limited use it to identify number of default debtor and then make policies through

which defaulters pay their money within sure time period (Nelson, and Miller, 2014).

Financial governance: This tool is used to make sure that business organizations should

follow ethical rules and regulation, they monitor each activity of business organizations.

CONCLUSION

From the above analysis it has been concluded that managerial accounting process play

essential part in running successful business organization. It will help manager to uses

accounting information in a way which will help in reducing cost and taken effective

investment decision through with they utilized their resource effectively. Business

organizations use Management accounting techniques and tools in order to achieve their

predetermine goal at fixed time.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFRENCES

From books and journal

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research, 45(1). pp.27-54.

Wouters, M. and Kirchberger, M. A., 2015. Customer value propositions as interorganizational

management accounting to support customer collaboration. Industrial Marketing

Management, 46, pp.54-67.

Chiwamit, P., Modell, S. and Yang, C. L., 2014. The societal relevance of management

accounting innovations: economic value added and institutional work in the fields of

Chinese and Thai state-owned enterprises. Accounting and Business Research, 44(2).

pp.144-180.

Hiebl, M. R., Duller, C., Feldbauer-Durstmüller, B. and Ulrich, P., 2015. Family influence and

management accounting usage—Findings from Germany and Austria. Schmalenbach

Business Review, 67(3). pp.368-404.

Juras, A., 2014. Strategic Management Accounting-What Is the Current State of the

Concept?. Economy Transdisciplinarity Cognition, 17(2). p.76.

McLaren, J., Appleyard, T. and Mitchell, F., 2016. The rise and fall of management accounting

systems: A case study investigation of EVA™. The British Accounting Review, 48(3).

pp.341-358.

Nelson, A. T. and Miller, P. B., 2014. Modern management accounting. Australasian.

Accounting, Business and Finance Journal, 8 .p.2.

8

From books and journal

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research, 45(1). pp.27-54.

Wouters, M. and Kirchberger, M. A., 2015. Customer value propositions as interorganizational

management accounting to support customer collaboration. Industrial Marketing

Management, 46, pp.54-67.

Chiwamit, P., Modell, S. and Yang, C. L., 2014. The societal relevance of management

accounting innovations: economic value added and institutional work in the fields of

Chinese and Thai state-owned enterprises. Accounting and Business Research, 44(2).

pp.144-180.

Hiebl, M. R., Duller, C., Feldbauer-Durstmüller, B. and Ulrich, P., 2015. Family influence and

management accounting usage—Findings from Germany and Austria. Schmalenbach

Business Review, 67(3). pp.368-404.

Juras, A., 2014. Strategic Management Accounting-What Is the Current State of the

Concept?. Economy Transdisciplinarity Cognition, 17(2). p.76.

McLaren, J., Appleyard, T. and Mitchell, F., 2016. The rise and fall of management accounting

systems: A case study investigation of EVA™. The British Accounting Review, 48(3).

pp.341-358.

Nelson, A. T. and Miller, P. B., 2014. Modern management accounting. Australasian.

Accounting, Business and Finance Journal, 8 .p.2.

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.