HND Business: Management Accounting Systems Analysis at Agment

VerifiedAdded on 2023/03/30

|20

|4783

|334

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems relevant to Agment LLC, a manufacturing company specializing in metal platers, oil supplies, and other items. It explores various management accounting tools, including costing, budgeting, and variance analysis, and their application in measuring performance and facilitating decision-making. The report details essential requirements of different management accounting systems such as financial accounting, cost accounting, inventory management, and performance management. Furthermore, it discusses the preparation and maintenance of key reports like budget reports, inventory management reports, price optimization reports, ratio analysis reports, job cost reports, and accounts receivable aging reports. The report also includes calculations using absorption and marginal costing methods, highlighting their impact on profitability. Finally, it examines the advantages and disadvantages of different budgetary planning tools and recommends management accounting systems to mitigate economic challenges faced by Agment LLC.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................4

TASK 1............................................................................................................................................4

P1) Management accounting and essential requirements of different types of systems.............4

P2) Management accounting reports...........................................................................................6

TASK 2............................................................................................................................................9

P3) Calculation of absorption and marginal costing statement...................................................9

TASK 3..........................................................................................................................................12

P4) advantage and disadvantage of different types of budgetary planning tools......................12

P5) Management accounting systems to reduce economic problems of Agment.....................15

CONCLUSION..............................................................................................................................17

REFERENCE.................................................................................................................................18

INTRODUCTION ..........................................................................................................................4

TASK 1............................................................................................................................................4

P1) Management accounting and essential requirements of different types of systems.............4

P2) Management accounting reports...........................................................................................6

TASK 2............................................................................................................................................9

P3) Calculation of absorption and marginal costing statement...................................................9

TASK 3..........................................................................................................................................12

P4) advantage and disadvantage of different types of budgetary planning tools......................12

P5) Management accounting systems to reduce economic problems of Agment.....................15

CONCLUSION..............................................................................................................................17

REFERENCE.................................................................................................................................18

INDEX OF TABLES

Table 1 Calculation of cost per unit under marginal & absorption costing method......................10

Table 2 Calculation of net profitability under absorption costing.................................................10

Table 3 Calculation of net profitability under marginal costing....................................................11

Table 4 Profit Reconciliation statement.........................................................................................12

Table 1 Calculation of cost per unit under marginal & absorption costing method......................10

Table 2 Calculation of net profitability under absorption costing.................................................10

Table 3 Calculation of net profitability under marginal costing....................................................11

Table 4 Profit Reconciliation statement.........................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a procedure in which statistical and financial information

obtained through financial and cost accounting is analysed, examined and interpreted. It

assists managers in sound decision-making process, creation of policies, strategic planning

& day to day operational management plans. Performance measurement & analysis, risk

assessment, resource allocation and others are several key focus areas of management

accounting. It assist all the business establishments regardless their sizes whether small,

medium or large sized in successful execution of their regular activities. The present

research paper investigates the contribution of managerial accounting tools for Agment

LLC. It operates in manufacturing industry and produces metal platers, fat & oil supplies,

surface finishers, hi-temperature alloy and many others items. The report targeted at

examining different types of management accounting systems which policymakers can

utilize for measuring & interpreting their actual results and make good decisions for

running operations in a better way. Besides this, marginal & absorption cost methods and

other techniques like key performance indicators and benchmarking will be discussed to

combat financial difficulties.

TASK 1

P1) Management accounting and essential requirements of different types of systems

Management accounting: - It is a multidisciplinary approach of accounting system

that is useful to mange entire operations of business organisation. However, actual

performance of entity is analysed by using management accounting systems on the basis of

which further decisions are made to provide better product services effectively. It

influences productivity and profitability of company which is linked with its business and

competitive strategies for producing goods and services in future time (RURY, 2013). In

addition to this, several tools are used of management accounting system like; costing,

budgeting, variance analysis and so on. By this way, actual position of Agment LLC is

presented for manufacturing chemicals of different forms. Besides this, various substances

are presented to show its scope, nature and overall potential to improve its financial

position regarding future business operations. It involves financial, cost, inventory and

performance management systems of organisation that proceed to make further to

implement its strategies. In this process, financial data are obtained as well managed in a

4 | P a g e

Management accounting is a procedure in which statistical and financial information

obtained through financial and cost accounting is analysed, examined and interpreted. It

assists managers in sound decision-making process, creation of policies, strategic planning

& day to day operational management plans. Performance measurement & analysis, risk

assessment, resource allocation and others are several key focus areas of management

accounting. It assist all the business establishments regardless their sizes whether small,

medium or large sized in successful execution of their regular activities. The present

research paper investigates the contribution of managerial accounting tools for Agment

LLC. It operates in manufacturing industry and produces metal platers, fat & oil supplies,

surface finishers, hi-temperature alloy and many others items. The report targeted at

examining different types of management accounting systems which policymakers can

utilize for measuring & interpreting their actual results and make good decisions for

running operations in a better way. Besides this, marginal & absorption cost methods and

other techniques like key performance indicators and benchmarking will be discussed to

combat financial difficulties.

TASK 1

P1) Management accounting and essential requirements of different types of systems

Management accounting: - It is a multidisciplinary approach of accounting system

that is useful to mange entire operations of business organisation. However, actual

performance of entity is analysed by using management accounting systems on the basis of

which further decisions are made to provide better product services effectively. It

influences productivity and profitability of company which is linked with its business and

competitive strategies for producing goods and services in future time (RURY, 2013). In

addition to this, several tools are used of management accounting system like; costing,

budgeting, variance analysis and so on. By this way, actual position of Agment LLC is

presented for manufacturing chemicals of different forms. Besides this, various substances

are presented to show its scope, nature and overall potential to improve its financial

position regarding future business operations. It involves financial, cost, inventory and

performance management systems of organisation that proceed to make further to

implement its strategies. In this process, financial data are obtained as well managed in a

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

specific manner for improvement in activities systematically. Thus, management

accountant of Agment identifies all operations for manufacturing chemical by which

adequate decisions are made for setting price on expenditure for labour and purchasing

materials. Including this, cost incurred on additional overhead is also evaluated that affects

production and distribution of metal platers, oil etc. Hence, management accounting is

essential for decision making to produce better product services and creating optimum

utilization of resources and fund (Ahmed, Neel and Wang, 2013).

Essential requirements of different management accounting systems:-

Management accounting systems comprised of several tools for decision making to

provide better product services. It includes financial accounting, cost accounting, inventory

management and performance evaluation systems that remains appropriate for adequate

decision-making and implementing services in a systematic manner (Demski, 2013).

Accordingly, some of the management accounting systems and their necessities can

describe as below:- Financial accounting system: - Financial accounting is an approach involves

recognising different components like; financial statements, notes which shows

monetary position of Agment. In this process, management accountant identifies

profit and loss account, balance sheet, income statement. Therefore, potential of

entity to create innovation in business operations is gained that proceed to make

decisions for its implementation. In addition to this, balances between incurred

expenditure and gained revenue is obtained that proceed to decision-making

process adequately (Hennes, Leone and Miller, 2013). Hence, financial accounting

system is benefited for proper management of entire business operations

economically. Cost accounting system: - Through this process system, incurred expenses and

gained revenue on production of metal platers and oil is recognized. Further,

decisions are made regarding setting cost for product services and their production

efficiently. It is appropriate for cost effectiveness and creating proper balance

between production and supplement of goods (Ball, 2013). Thus, cost accounting

5 | P a g e

accountant of Agment identifies all operations for manufacturing chemical by which

adequate decisions are made for setting price on expenditure for labour and purchasing

materials. Including this, cost incurred on additional overhead is also evaluated that affects

production and distribution of metal platers, oil etc. Hence, management accounting is

essential for decision making to produce better product services and creating optimum

utilization of resources and fund (Ahmed, Neel and Wang, 2013).

Essential requirements of different management accounting systems:-

Management accounting systems comprised of several tools for decision making to

provide better product services. It includes financial accounting, cost accounting, inventory

management and performance evaluation systems that remains appropriate for adequate

decision-making and implementing services in a systematic manner (Demski, 2013).

Accordingly, some of the management accounting systems and their necessities can

describe as below:- Financial accounting system: - Financial accounting is an approach involves

recognising different components like; financial statements, notes which shows

monetary position of Agment. In this process, management accountant identifies

profit and loss account, balance sheet, income statement. Therefore, potential of

entity to create innovation in business operations is gained that proceed to make

decisions for its implementation. In addition to this, balances between incurred

expenditure and gained revenue is obtained that proceed to decision-making

process adequately (Hennes, Leone and Miller, 2013). Hence, financial accounting

system is benefited for proper management of entire business operations

economically. Cost accounting system: - Through this process system, incurred expenses and

gained revenue on production of metal platers and oil is recognized. Further,

decisions are made regarding setting cost for product services and their production

efficiently. It is appropriate for cost effectiveness and creating proper balance

between production and supplement of goods (Ball, 2013). Thus, cost accounting

5 | P a g e

system is vital for proper costing and making decisions regarding various

implementations and adequate production of manufacturing company's products Inventory management system: - Under this management accounting

system,liquidity position of Agment is identified for which different ideas are

created to improve it. However, all inventories get managed through this system as

well proper strategy is prepared to implement its quality goods efficiently. It is

helpful for utilization of resources and fund that impacts on its productivity and

profitability for producing metal platers, surface finishers, hi-temperature alloy and

so on. Including this, various innovations are created for providing better quality of

company's items . Thus, inventory management system of management accounting

is essential for proper management of goods and different implementations

effectively (Warren, Reeve and Duchac, 2013).

Performance management system: - As management accounting is a

multidisciplinary approach, it evaluates performance of entity and its workers.

Under this system, performance of Agment involves its business and competitive

strategies to face competition and make place in competitive market. In this regard,

various tools are applied for improving performance and product services provided

by entity. It is interlinked with further decision making process and useful for

enhancing its efficiency at high level (Adibah and et.al., 2013). Therefore, business

performance get improved systematically that affects productivity and profitability

of organisation in further years.

P2) Management accounting reports

Management accountant of Agment prepares and maintains different reports to

show its financial and non-economic position. It evolves reports like; price optimization,

ratio analysis, variance analysis, budgeting and budgetary control system etc (Huber and

Scheytt, 2013). In this process, performance of entity is recognised that generates several

ideas for further implementation and for providing better quality services systematically.

Thus, some of the main reports can be understood as:- Budget report: - It is beneficial for adequate decision-making process and use of

resources and fund that influences further profitability and sustainability However,

6 | P a g e

implementations and adequate production of manufacturing company's products Inventory management system: - Under this management accounting

system,liquidity position of Agment is identified for which different ideas are

created to improve it. However, all inventories get managed through this system as

well proper strategy is prepared to implement its quality goods efficiently. It is

helpful for utilization of resources and fund that impacts on its productivity and

profitability for producing metal platers, surface finishers, hi-temperature alloy and

so on. Including this, various innovations are created for providing better quality of

company's items . Thus, inventory management system of management accounting

is essential for proper management of goods and different implementations

effectively (Warren, Reeve and Duchac, 2013).

Performance management system: - As management accounting is a

multidisciplinary approach, it evaluates performance of entity and its workers.

Under this system, performance of Agment involves its business and competitive

strategies to face competition and make place in competitive market. In this regard,

various tools are applied for improving performance and product services provided

by entity. It is interlinked with further decision making process and useful for

enhancing its efficiency at high level (Adibah and et.al., 2013). Therefore, business

performance get improved systematically that affects productivity and profitability

of organisation in further years.

P2) Management accounting reports

Management accountant of Agment prepares and maintains different reports to

show its financial and non-economic position. It evolves reports like; price optimization,

ratio analysis, variance analysis, budgeting and budgetary control system etc (Huber and

Scheytt, 2013). In this process, performance of entity is recognised that generates several

ideas for further implementation and for providing better quality services systematically.

Thus, some of the main reports can be understood as:- Budget report: - It is beneficial for adequate decision-making process and use of

resources and fund that influences further profitability and sustainability However,

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

budget report is a kind of preparing agenda and steps to be followed on

systematically (Kim and et.al., 2013). For preparing budget, management

accountant of Agment analyses all business operations and further makes decision

related to improvement in its quality services. Therefore, management of entire

business is possible by using this process as well increasing organisation's

efficiency. Hence, budget report is beneficial for providing better services and

managing all operations of the entity effectively. In this process, cost incurred on

production and supplement of goods is also determined that is helpful for cost

effectiveness. Along with this, proper balance between production and distribution

of goods can be achieved to achieve effective business operations. Thus, preparing

budget report is essential for formulating strategies requires to be followed on as

well creating innovations in overall business entity's operations. Inventory management report:- For preparing and maintaining report is related to

improving liquidity position of organisation, all inventories are analysed as well

managed systematically. In accordance to this, management of all goods and

services provided by Agment is determined involving cost effectiveness,

effectiveness of organisation, improving efficiency and so on. Therefore,

appropriate management of all inventories is possible by identifying mentioned

data presented in last year's inventory report. Moreover, it is related with business

operations and financial position of Agment also remains suitable for their proper

management (Methot and Wetzel, 2013). Thus, inventory management report is one

of the vital recording data part that affects effectiveness of entity same as creates

various innovative ideas for utilization of resources for manufacturing of oil, metal

platers, surface finishers etc. It is beneficial for keeping goods safe and helpful to

improve quality services of organisation. Hence, management accountant of the

company evaluates all inventories and their implementation for better services and

effectiveness at high level. Price optimization report: - It is related with cost effectiveness approach that is

essential to be reported price of goods. In accordance to this, several aspects are

used for reporting and setting price of producing items of Agment in future time

period. However, varieties are ideas are created for price optimization and

7 | P a g e

systematically (Kim and et.al., 2013). For preparing budget, management

accountant of Agment analyses all business operations and further makes decision

related to improvement in its quality services. Therefore, management of entire

business is possible by using this process as well increasing organisation's

efficiency. Hence, budget report is beneficial for providing better services and

managing all operations of the entity effectively. In this process, cost incurred on

production and supplement of goods is also determined that is helpful for cost

effectiveness. Along with this, proper balance between production and distribution

of goods can be achieved to achieve effective business operations. Thus, preparing

budget report is essential for formulating strategies requires to be followed on as

well creating innovations in overall business entity's operations. Inventory management report:- For preparing and maintaining report is related to

improving liquidity position of organisation, all inventories are analysed as well

managed systematically. In accordance to this, management of all goods and

services provided by Agment is determined involving cost effectiveness,

effectiveness of organisation, improving efficiency and so on. Therefore,

appropriate management of all inventories is possible by identifying mentioned

data presented in last year's inventory report. Moreover, it is related with business

operations and financial position of Agment also remains suitable for their proper

management (Methot and Wetzel, 2013). Thus, inventory management report is one

of the vital recording data part that affects effectiveness of entity same as creates

various innovative ideas for utilization of resources for manufacturing of oil, metal

platers, surface finishers etc. It is beneficial for keeping goods safe and helpful to

improve quality services of organisation. Hence, management accountant of the

company evaluates all inventories and their implementation for better services and

effectiveness at high level. Price optimization report: - It is related with cost effectiveness approach that is

essential to be reported price of goods. In accordance to this, several aspects are

used for reporting and setting price of producing items of Agment in future time

period. However, varieties are ideas are created for price optimization and

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

determining affordability of customer to pay on produced goods. In this process,

cost for production and distribution of goods provided by entity is set that affects

further profitability of entity. However, price optimization report is helpful for cost

effectiveness and adequate costing of goods. Thus, preparing this report remains

suitable for management of business operations effectively and satisfying its

customers by setting affordable cost. For setting price of product, all costs incurred

on material, labour and additional overhead are determined that proceed to

production of products. Hence, price optimization report is beneficial for adequate

costing and proper decision making for appropriate business operations

(Management Accounting, 2016). Ratio analysis report:- It is financial component that is suitable to analyse

economic position of Agment to operate activities in future time period. For this

purpose, several ratios are analysed including profitability, liquidity, efficiency, debt

equity ratio and so on. In this regard, monetary and non-economic position of entity

is analysed by which different innovative ideas are created for providing better

services. In addition to this, comparison of last years' performance is obtained for ,

bridge the gap and improving services various tools are obtained. Along with this,

ratio analysis also creates comparison of organisation's position to its other

competitive entity. In accordance to this, various innovative methods are applied for

creating market position and increasing its competitive strategies. Thus, preparing

report of ratio analysis is helpful to recognise performance and position of metal

platers' provider entity effectively (RURY, 2013). On the basis of which, different

ideas are generated for adequate production and distribution of goods and services

provided by entity. Job cost report: - Preparing and maintaining job cost report is useful to analyse

expenses incurred on business operations. It is suitable to recognise earning areas to

operate business activities. For manufacturing company Agment, job cost report is

essential to identify cost incurred on manufacturing, production and supplement of

items. It influences productivity and profitability of entity also affects its

competitive strategy to face competition and sustaining its position in market.

However, various ideas are created for costing and producing goods. Therefore,

8 | P a g e

cost for production and distribution of goods provided by entity is set that affects

further profitability of entity. However, price optimization report is helpful for cost

effectiveness and adequate costing of goods. Thus, preparing this report remains

suitable for management of business operations effectively and satisfying its

customers by setting affordable cost. For setting price of product, all costs incurred

on material, labour and additional overhead are determined that proceed to

production of products. Hence, price optimization report is beneficial for adequate

costing and proper decision making for appropriate business operations

(Management Accounting, 2016). Ratio analysis report:- It is financial component that is suitable to analyse

economic position of Agment to operate activities in future time period. For this

purpose, several ratios are analysed including profitability, liquidity, efficiency, debt

equity ratio and so on. In this regard, monetary and non-economic position of entity

is analysed by which different innovative ideas are created for providing better

services. In addition to this, comparison of last years' performance is obtained for ,

bridge the gap and improving services various tools are obtained. Along with this,

ratio analysis also creates comparison of organisation's position to its other

competitive entity. In accordance to this, various innovative methods are applied for

creating market position and increasing its competitive strategies. Thus, preparing

report of ratio analysis is helpful to recognise performance and position of metal

platers' provider entity effectively (RURY, 2013). On the basis of which, different

ideas are generated for adequate production and distribution of goods and services

provided by entity. Job cost report: - Preparing and maintaining job cost report is useful to analyse

expenses incurred on business operations. It is suitable to recognise earning areas to

operate business activities. For manufacturing company Agment, job cost report is

essential to identify cost incurred on manufacturing, production and supplement of

items. It influences productivity and profitability of entity also affects its

competitive strategy to face competition and sustaining its position in market.

However, various ideas are created for costing and producing goods. Therefore,

8 | P a g e

records of setting costs for production and distribution is presented that affects

further implementations. In this report, various tools are applied for manufacturing

of metal platers, oil and surface finishers systematically (Ahmed, Neel and Wang,

2013). Thus, on the basis of analysing this report, further decisions are made for

adequate costing and producing items of the organisation.

Accounts Receivable Aging: - By preparing this report, company's cash collection

process is determined. It includes analysis of credit to its customers through

presented invoices in aging reports. Therefore, problems with collection of money

form customers is obtained by which further credit policies are crated to tighten the

operations and cost of products. Thus, manager of the organisation identifies

account receivable aging by which credit for producing and supplementing money

can manage effectively (Demski, 2013).

TASK 2

P3) Calculation of absorption and marginal costing statement

According to the stated case scenario, Agmet Company produces a single item and

incur various costs to produce the item such as material, labour and other fixed and variable

overheads. Cost management is an important area of management accounting in which

managers create plans, policies and decisions for controlling overrunning expenditures and

maintain such expense in line with the target (Cooper, Ezzamel and Qu, 2017). There are

two most fundamental techniques applied by numerous business entities for cost

computation i.e. marginal and absorption costing methods, detailed here as follows:

Marginal costing: It is an accounting system which gives value to variable costs

only thus, it determines production costs through accumulating all those expenditures

which changes proportionately with the change in output (Ax and Greve, 2017). It is a

principle costing method that helps in successful & sound business decisions. It find out

contribution and net profitability through using following formula:

Contribution: Total sales turnover – total variable cost

Net profitability: Contribution – Total fixed cost OR Total sales turnover – Total cost

Here, Total cost = Total fixed cost + Total variable cost

9 | P a g e

further implementations. In this report, various tools are applied for manufacturing

of metal platers, oil and surface finishers systematically (Ahmed, Neel and Wang,

2013). Thus, on the basis of analysing this report, further decisions are made for

adequate costing and producing items of the organisation.

Accounts Receivable Aging: - By preparing this report, company's cash collection

process is determined. It includes analysis of credit to its customers through

presented invoices in aging reports. Therefore, problems with collection of money

form customers is obtained by which further credit policies are crated to tighten the

operations and cost of products. Thus, manager of the organisation identifies

account receivable aging by which credit for producing and supplementing money

can manage effectively (Demski, 2013).

TASK 2

P3) Calculation of absorption and marginal costing statement

According to the stated case scenario, Agmet Company produces a single item and

incur various costs to produce the item such as material, labour and other fixed and variable

overheads. Cost management is an important area of management accounting in which

managers create plans, policies and decisions for controlling overrunning expenditures and

maintain such expense in line with the target (Cooper, Ezzamel and Qu, 2017). There are

two most fundamental techniques applied by numerous business entities for cost

computation i.e. marginal and absorption costing methods, detailed here as follows:

Marginal costing: It is an accounting system which gives value to variable costs

only thus, it determines production costs through accumulating all those expenditures

which changes proportionately with the change in output (Ax and Greve, 2017). It is a

principle costing method that helps in successful & sound business decisions. It find out

contribution and net profitability through using following formula:

Contribution: Total sales turnover – total variable cost

Net profitability: Contribution – Total fixed cost OR Total sales turnover – Total cost

Here, Total cost = Total fixed cost + Total variable cost

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

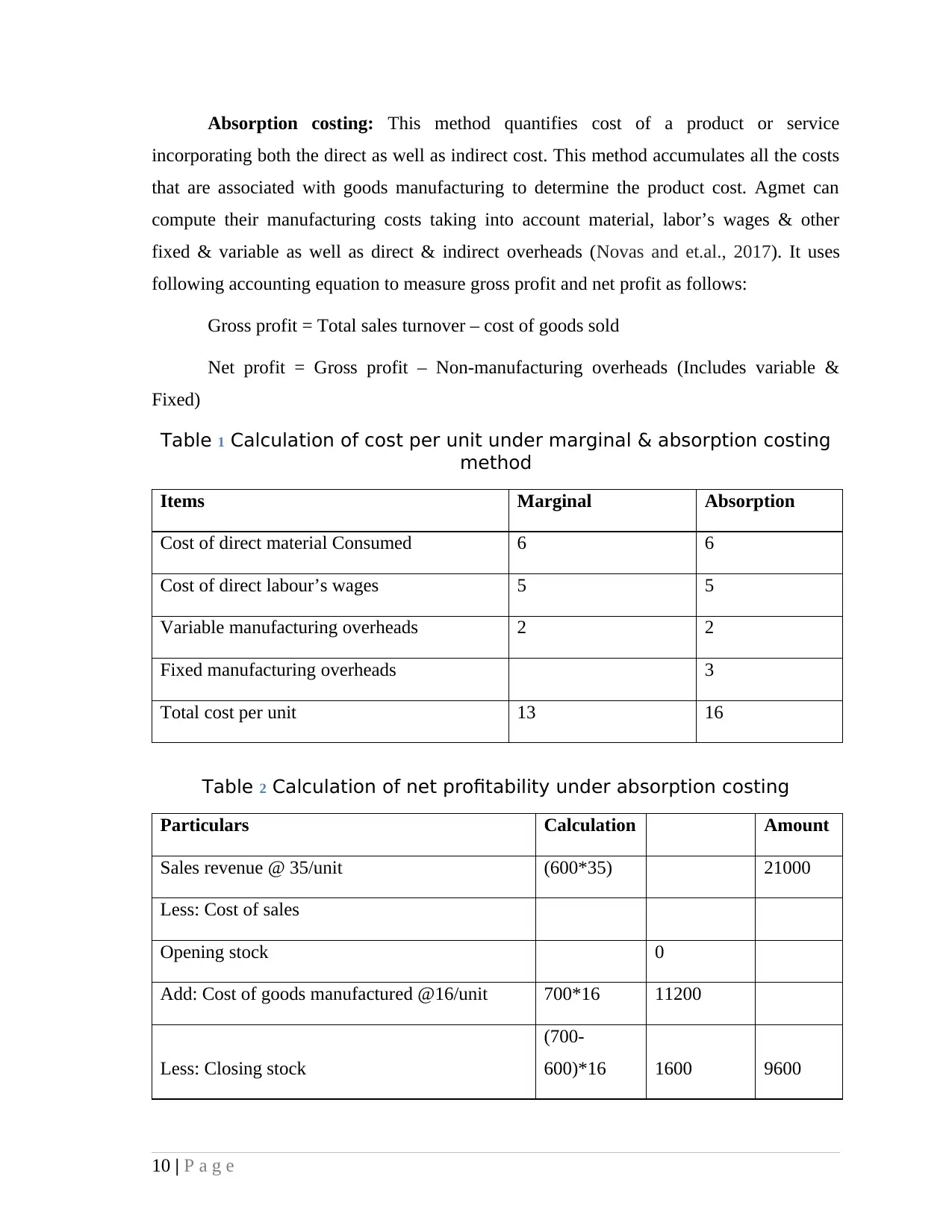

Absorption costing: This method quantifies cost of a product or service

incorporating both the direct as well as indirect cost. This method accumulates all the costs

that are associated with goods manufacturing to determine the product cost. Agmet can

compute their manufacturing costs taking into account material, labor’s wages & other

fixed & variable as well as direct & indirect overheads (Novas and et.al., 2017). It uses

following accounting equation to measure gross profit and net profit as follows:

Gross profit = Total sales turnover – cost of goods sold

Net profit = Gross profit – Non-manufacturing overheads (Includes variable &

Fixed)

Table 1 Calculation of cost per unit under marginal & absorption costing

method

Items Marginal Absorption

Cost of direct material Consumed 6 6

Cost of direct labour’s wages 5 5

Variable manufacturing overheads 2 2

Fixed manufacturing overheads 3

Total cost per unit 13 16

Table 2 Calculation of net profitability under absorption costing

Particulars Calculation Amount

Sales revenue @ 35/unit (600*35) 21000

Less: Cost of sales

Opening stock 0

Add: Cost of goods manufactured @16/unit 700*16 11200

Less: Closing stock

(700-

600)*16 1600 9600

10 | P a g e

incorporating both the direct as well as indirect cost. This method accumulates all the costs

that are associated with goods manufacturing to determine the product cost. Agmet can

compute their manufacturing costs taking into account material, labor’s wages & other

fixed & variable as well as direct & indirect overheads (Novas and et.al., 2017). It uses

following accounting equation to measure gross profit and net profit as follows:

Gross profit = Total sales turnover – cost of goods sold

Net profit = Gross profit – Non-manufacturing overheads (Includes variable &

Fixed)

Table 1 Calculation of cost per unit under marginal & absorption costing

method

Items Marginal Absorption

Cost of direct material Consumed 6 6

Cost of direct labour’s wages 5 5

Variable manufacturing overheads 2 2

Fixed manufacturing overheads 3

Total cost per unit 13 16

Table 2 Calculation of net profitability under absorption costing

Particulars Calculation Amount

Sales revenue @ 35/unit (600*35) 21000

Less: Cost of sales

Opening stock 0

Add: Cost of goods manufactured @16/unit 700*16 11200

Less: Closing stock

(700-

600)*16 1600 9600

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

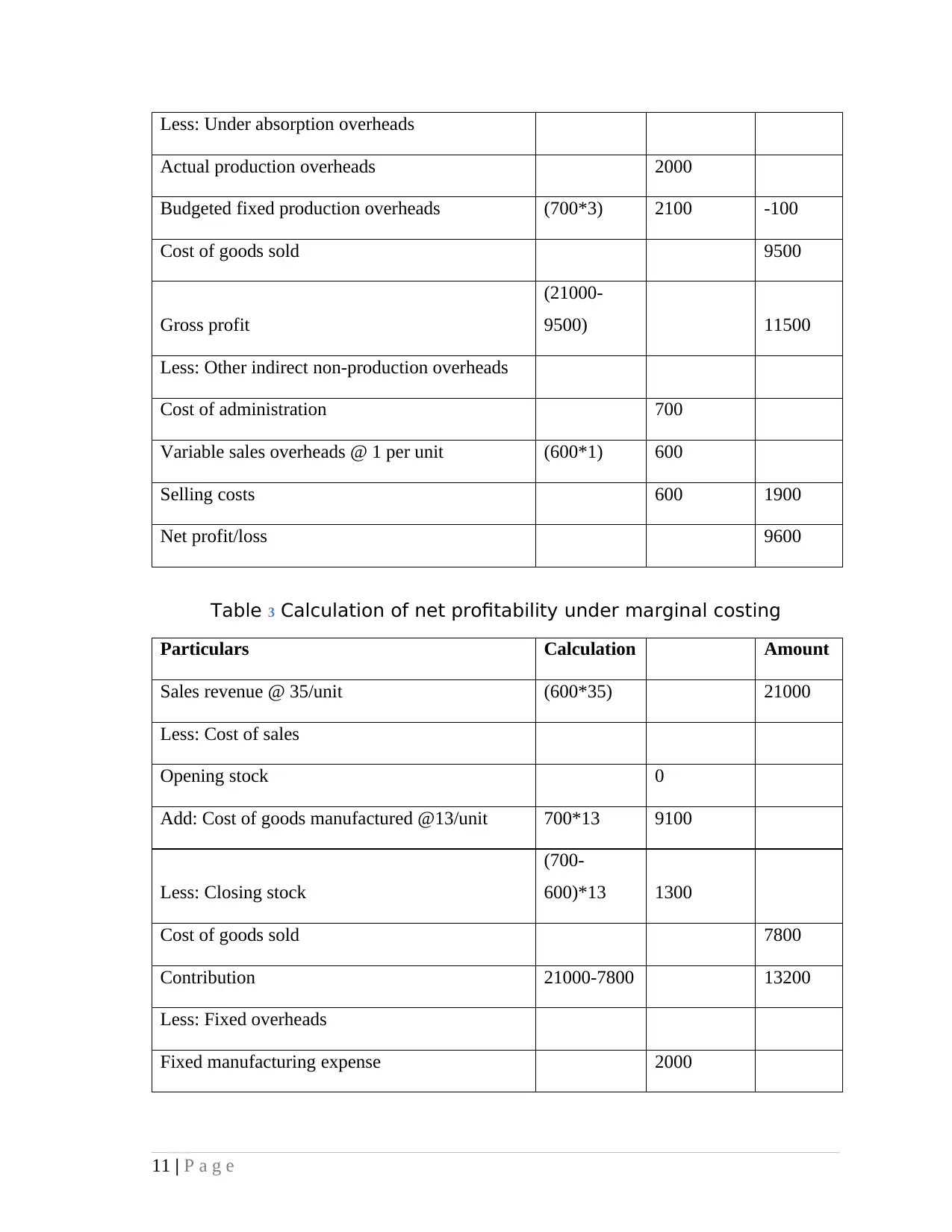

Less: Under absorption overheads

Actual production overheads 2000

Budgeted fixed production overheads (700*3) 2100 -100

Cost of goods sold 9500

Gross profit

(21000-

9500) 11500

Less: Other indirect non-production overheads

Cost of administration 700

Variable sales overheads @ 1 per unit (600*1) 600

Selling costs 600 1900

Net profit/loss 9600

Table 3 Calculation of net profitability under marginal costing

Particulars Calculation Amount

Sales revenue @ 35/unit (600*35) 21000

Less: Cost of sales

Opening stock 0

Add: Cost of goods manufactured @13/unit 700*13 9100

Less: Closing stock

(700-

600)*13 1300

Cost of goods sold 7800

Contribution 21000-7800 13200

Less: Fixed overheads

Fixed manufacturing expense 2000

11 | P a g e

Actual production overheads 2000

Budgeted fixed production overheads (700*3) 2100 -100

Cost of goods sold 9500

Gross profit

(21000-

9500) 11500

Less: Other indirect non-production overheads

Cost of administration 700

Variable sales overheads @ 1 per unit (600*1) 600

Selling costs 600 1900

Net profit/loss 9600

Table 3 Calculation of net profitability under marginal costing

Particulars Calculation Amount

Sales revenue @ 35/unit (600*35) 21000

Less: Cost of sales

Opening stock 0

Add: Cost of goods manufactured @13/unit 700*13 9100

Less: Closing stock

(700-

600)*13 1300

Cost of goods sold 7800

Contribution 21000-7800 13200

Less: Fixed overheads

Fixed manufacturing expense 2000

11 | P a g e

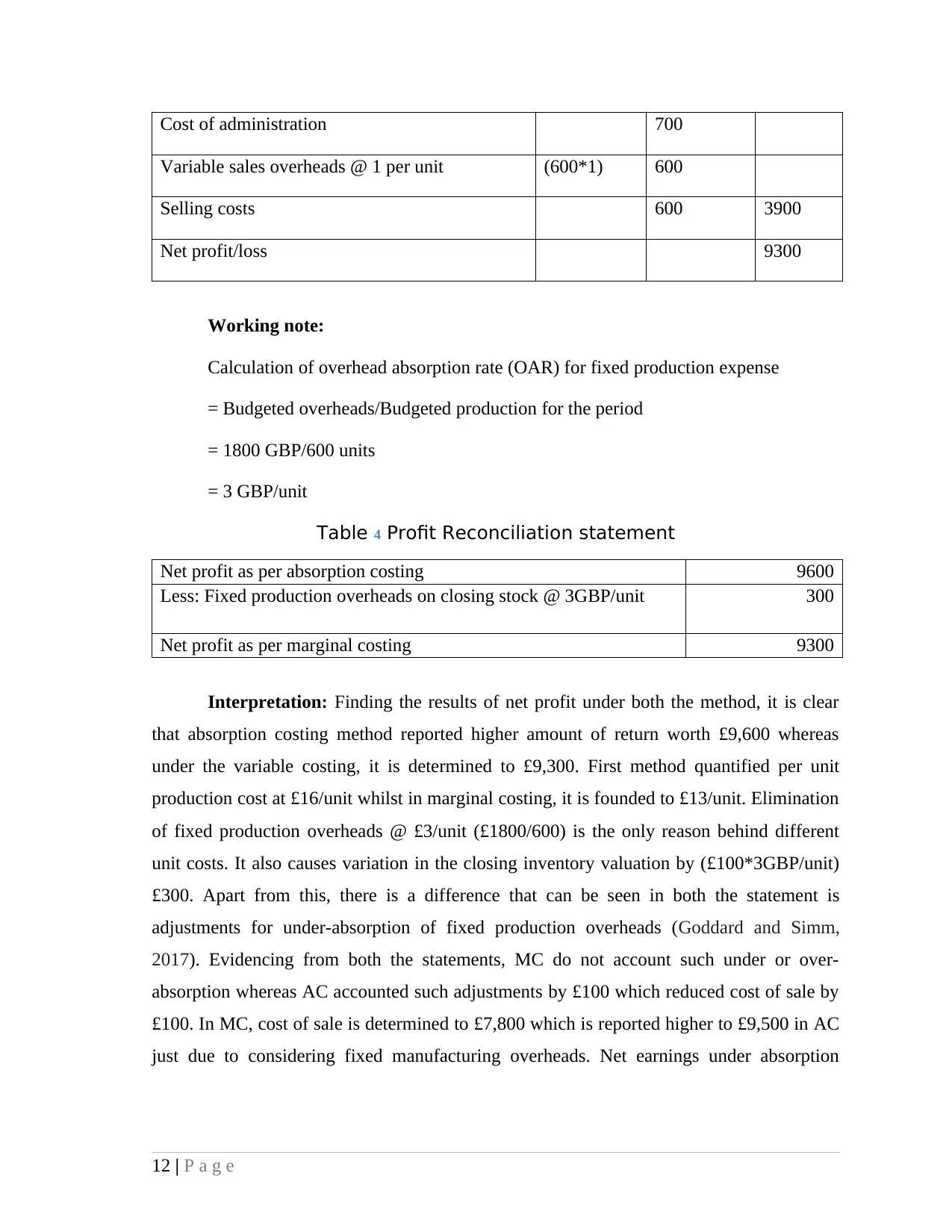

Cost of administration 700

Variable sales overheads @ 1 per unit (600*1) 600

Selling costs 600 3900

Net profit/loss 9300

Working note:

Calculation of overhead absorption rate (OAR) for fixed production expense

= Budgeted overheads/Budgeted production for the period

= 1800 GBP/600 units

= 3 GBP/unit

Table 4 Profit Reconciliation statement

Net profit as per absorption costing 9600

Less: Fixed production overheads on closing stock @ 3GBP/unit 300

Net profit as per marginal costing 9300

Interpretation: Finding the results of net profit under both the method, it is clear

that absorption costing method reported higher amount of return worth £9,600 whereas

under the variable costing, it is determined to £9,300. First method quantified per unit

production cost at £16/unit whilst in marginal costing, it is founded to £13/unit. Elimination

of fixed production overheads @ £3/unit (£1800/600) is the only reason behind different

unit costs. It also causes variation in the closing inventory valuation by (£100*3GBP/unit)

£300. Apart from this, there is a difference that can be seen in both the statement is

adjustments for under-absorption of fixed production overheads (Goddard and Simm,

2017). Evidencing from both the statements, MC do not account such under or over-

absorption whereas AC accounted such adjustments by £100 which reduced cost of sale by

£100. In MC, cost of sale is determined to £7,800 which is reported higher to £9,500 in AC

just due to considering fixed manufacturing overheads. Net earnings under absorption

12 | P a g e

Variable sales overheads @ 1 per unit (600*1) 600

Selling costs 600 3900

Net profit/loss 9300

Working note:

Calculation of overhead absorption rate (OAR) for fixed production expense

= Budgeted overheads/Budgeted production for the period

= 1800 GBP/600 units

= 3 GBP/unit

Table 4 Profit Reconciliation statement

Net profit as per absorption costing 9600

Less: Fixed production overheads on closing stock @ 3GBP/unit 300

Net profit as per marginal costing 9300

Interpretation: Finding the results of net profit under both the method, it is clear

that absorption costing method reported higher amount of return worth £9,600 whereas

under the variable costing, it is determined to £9,300. First method quantified per unit

production cost at £16/unit whilst in marginal costing, it is founded to £13/unit. Elimination

of fixed production overheads @ £3/unit (£1800/600) is the only reason behind different

unit costs. It also causes variation in the closing inventory valuation by (£100*3GBP/unit)

£300. Apart from this, there is a difference that can be seen in both the statement is

adjustments for under-absorption of fixed production overheads (Goddard and Simm,

2017). Evidencing from both the statements, MC do not account such under or over-

absorption whereas AC accounted such adjustments by £100 which reduced cost of sale by

£100. In MC, cost of sale is determined to £7,800 which is reported higher to £9,500 in AC

just due to considering fixed manufacturing overheads. Net earnings under absorption

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.