Detailed Analysis: Management Accounting Homework Solution

VerifiedAdded on 2020/03/23

|18

|2694

|257

Homework Assignment

AI Summary

This document presents a comprehensive solution to a management accounting assignment, covering various aspects of cost analysis and financial modeling. The assignment is divided into multiple parts, starting with the development of cost functions for different business components like part-time dentists, receptionists, supplies, rent, and administration. It then proceeds to analyze these costs, calculate average fees, and project future profits. Part B focuses on regression analysis, examining the relationship between revenues and visits with supplies cost, and interpreting the results, including R-squared values and p-values. Part C delves into overhead cost analysis, developing a cost function based on hours worked and calculating predicted versus actual overhead costs. Finally, Part D presents a basic probability problem involving meal choices. The solution provides detailed calculations, interpretations, and analyses to address each requirement of the assignment.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Answer to PART A:.........................................................................................................................3

Requirement A1:..........................................................................................................................3

Requirement A2:..........................................................................................................................5

Requirement A3:..........................................................................................................................5

Answer to Part B:.............................................................................................................................6

Requirement B1:..........................................................................................................................6

Requirement B.1a:.......................................................................................................................7

Requirement B.1b:.......................................................................................................................8

Requirement B.1c:.......................................................................................................................8

Requirement B.2:.........................................................................................................................8

Requirement B.2a:.......................................................................................................................9

Requirement B.2b:.....................................................................................................................10

Requirement B.2c:.....................................................................................................................10

Requirement B.2:.......................................................................................................................10

Answer to Part C:...........................................................................................................................12

Requirement C.1:.......................................................................................................................12

Requirement C.2:.......................................................................................................................13

Requirement C.3:.......................................................................................................................13

Requirement C.4:.......................................................................................................................13

Table of Contents

Answer to PART A:.........................................................................................................................3

Requirement A1:..........................................................................................................................3

Requirement A2:..........................................................................................................................5

Requirement A3:..........................................................................................................................5

Answer to Part B:.............................................................................................................................6

Requirement B1:..........................................................................................................................6

Requirement B.1a:.......................................................................................................................7

Requirement B.1b:.......................................................................................................................8

Requirement B.1c:.......................................................................................................................8

Requirement B.2:.........................................................................................................................8

Requirement B.2a:.......................................................................................................................9

Requirement B.2b:.....................................................................................................................10

Requirement B.2c:.....................................................................................................................10

Requirement B.2:.......................................................................................................................10

Answer to Part C:...........................................................................................................................12

Requirement C.1:.......................................................................................................................12

Requirement C.2:.......................................................................................................................13

Requirement C.3:.......................................................................................................................13

Requirement C.4:.......................................................................................................................13

2MANAGEMENT ACCOUNTING

Answer to Part D:..........................................................................................................................14

Bibliography:.................................................................................................................................17

Answer to Part D:..........................................................................................................................14

Bibliography:.................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

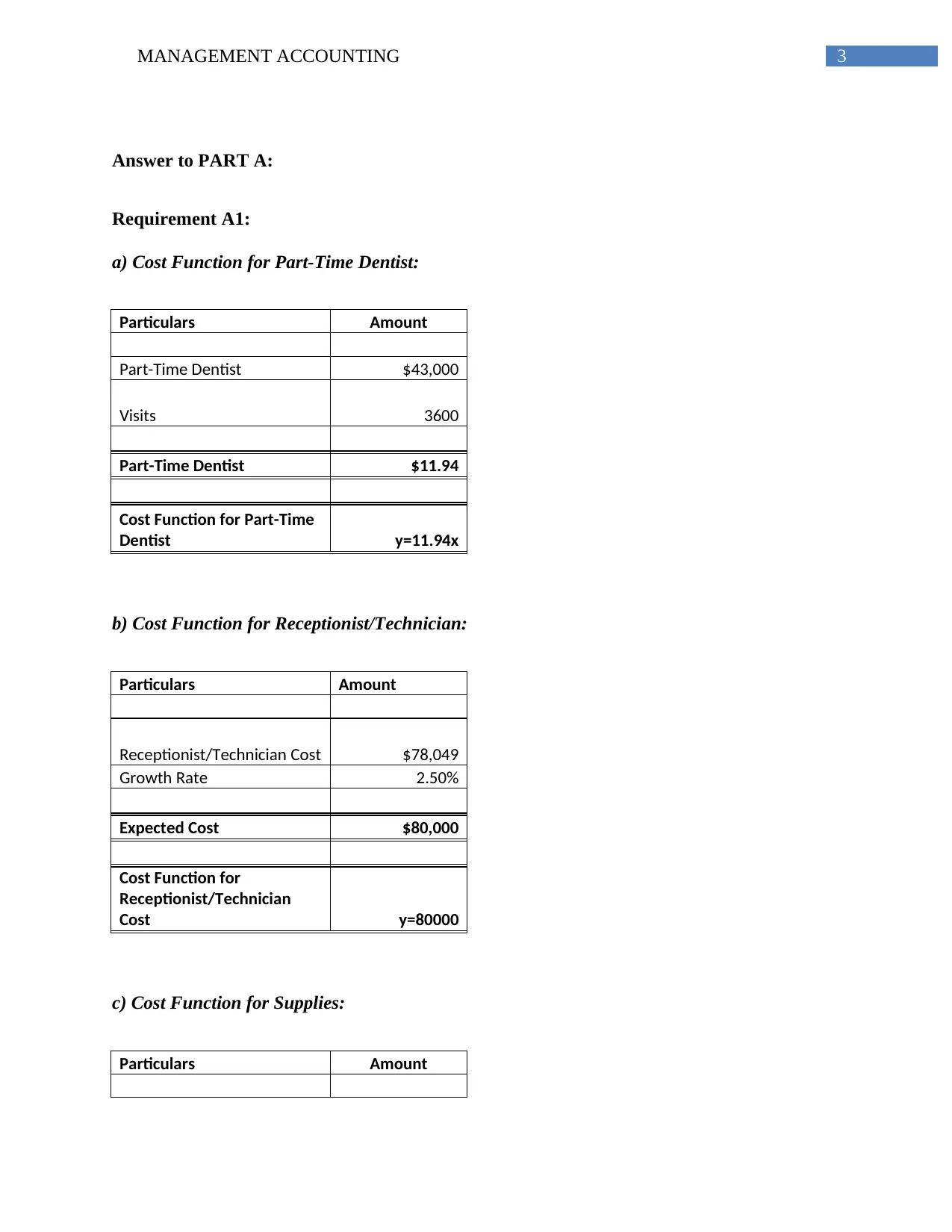

Answer to PART A:

Requirement A1:

a) Cost Function for Part-Time Dentist:

Particulars Amount

Part-Time Dentist $43,000

Visits 3600

Part-Time Dentist $11.94

Cost Function for Part-Time

Dentist y=11.94x

b) Cost Function for Receptionist/Technician:

Particulars Amount

Receptionist/Technician Cost $78,049

Growth Rate 2.50%

Expected Cost $80,000

Cost Function for

Receptionist/Technician

Cost y=80000

c) Cost Function for Supplies:

Particulars Amount

Answer to PART A:

Requirement A1:

a) Cost Function for Part-Time Dentist:

Particulars Amount

Part-Time Dentist $43,000

Visits 3600

Part-Time Dentist $11.94

Cost Function for Part-Time

Dentist y=11.94x

b) Cost Function for Receptionist/Technician:

Particulars Amount

Receptionist/Technician Cost $78,049

Growth Rate 2.50%

Expected Cost $80,000

Cost Function for

Receptionist/Technician

Cost y=80000

c) Cost Function for Supplies:

Particulars Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

Maximum Visits 3600

Minimum Visits 2300

Difference 1300

Highest Supplies Expenses $5,100

Lowest Supplies Expenses $3,900

Difference $1,200

Variable Cost per unit $0.92

Fixed Cost per unit $1,777

Cost Function for Supplies y=0.92x+1777

d) Cost Function for Rent:

Particulars Amount

Rent of 2016 $8,750

Cost Function for Rent y=8750

e) Cost Function for Administration:

Particulars Amount

Maximum Visits 3600

Minimum Visits 2300

Difference 1300

Highest Supplies Expenses $11,200

Lowest Supplies Expenses $8,000

Diiference $3,200

Variable Cost per unit $2.46

Fixed Cost per unit $2,338

Maximum Visits 3600

Minimum Visits 2300

Difference 1300

Highest Supplies Expenses $5,100

Lowest Supplies Expenses $3,900

Difference $1,200

Variable Cost per unit $0.92

Fixed Cost per unit $1,777

Cost Function for Supplies y=0.92x+1777

d) Cost Function for Rent:

Particulars Amount

Rent of 2016 $8,750

Cost Function for Rent y=8750

e) Cost Function for Administration:

Particulars Amount

Maximum Visits 3600

Minimum Visits 2300

Difference 1300

Highest Supplies Expenses $11,200

Lowest Supplies Expenses $8,000

Diiference $3,200

Variable Cost per unit $2.46

Fixed Cost per unit $2,338

5MANAGEMENT ACCOUNTING

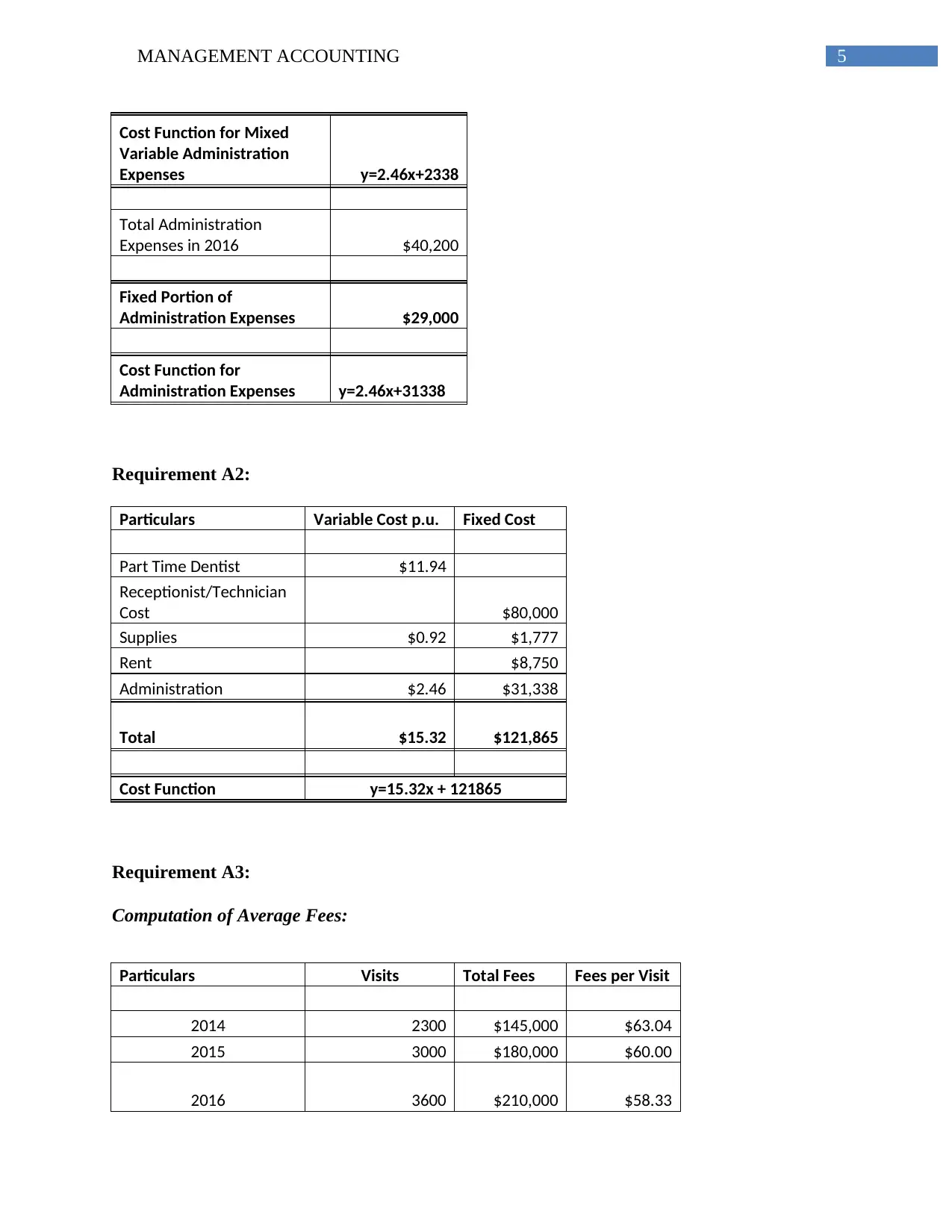

Cost Function for Mixed

Variable Administration

Expenses y=2.46x+2338

Total Administration

Expenses in 2016 $40,200

Fixed Portion of

Administration Expenses $29,000

Cost Function for

Administration Expenses y=2.46x+31338

Requirement A2:

Particulars Variable Cost p.u. Fixed Cost

Part Time Dentist $11.94

Receptionist/Technician

Cost $80,000

Supplies $0.92 $1,777

Rent $8,750

Administration $2.46 $31,338

Total $15.32 $121,865

Cost Function y=15.32x + 121865

Requirement A3:

Computation of Average Fees:

Particulars Visits Total Fees Fees per Visit

2014 2300 $145,000 $63.04

2015 3000 $180,000 $60.00

2016 3600 $210,000 $58.33

Cost Function for Mixed

Variable Administration

Expenses y=2.46x+2338

Total Administration

Expenses in 2016 $40,200

Fixed Portion of

Administration Expenses $29,000

Cost Function for

Administration Expenses y=2.46x+31338

Requirement A2:

Particulars Variable Cost p.u. Fixed Cost

Part Time Dentist $11.94

Receptionist/Technician

Cost $80,000

Supplies $0.92 $1,777

Rent $8,750

Administration $2.46 $31,338

Total $15.32 $121,865

Cost Function y=15.32x + 121865

Requirement A3:

Computation of Average Fees:

Particulars Visits Total Fees Fees per Visit

2014 2300 $145,000 $63.04

2015 3000 $180,000 $60.00

2016 3600 $210,000 $58.33

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

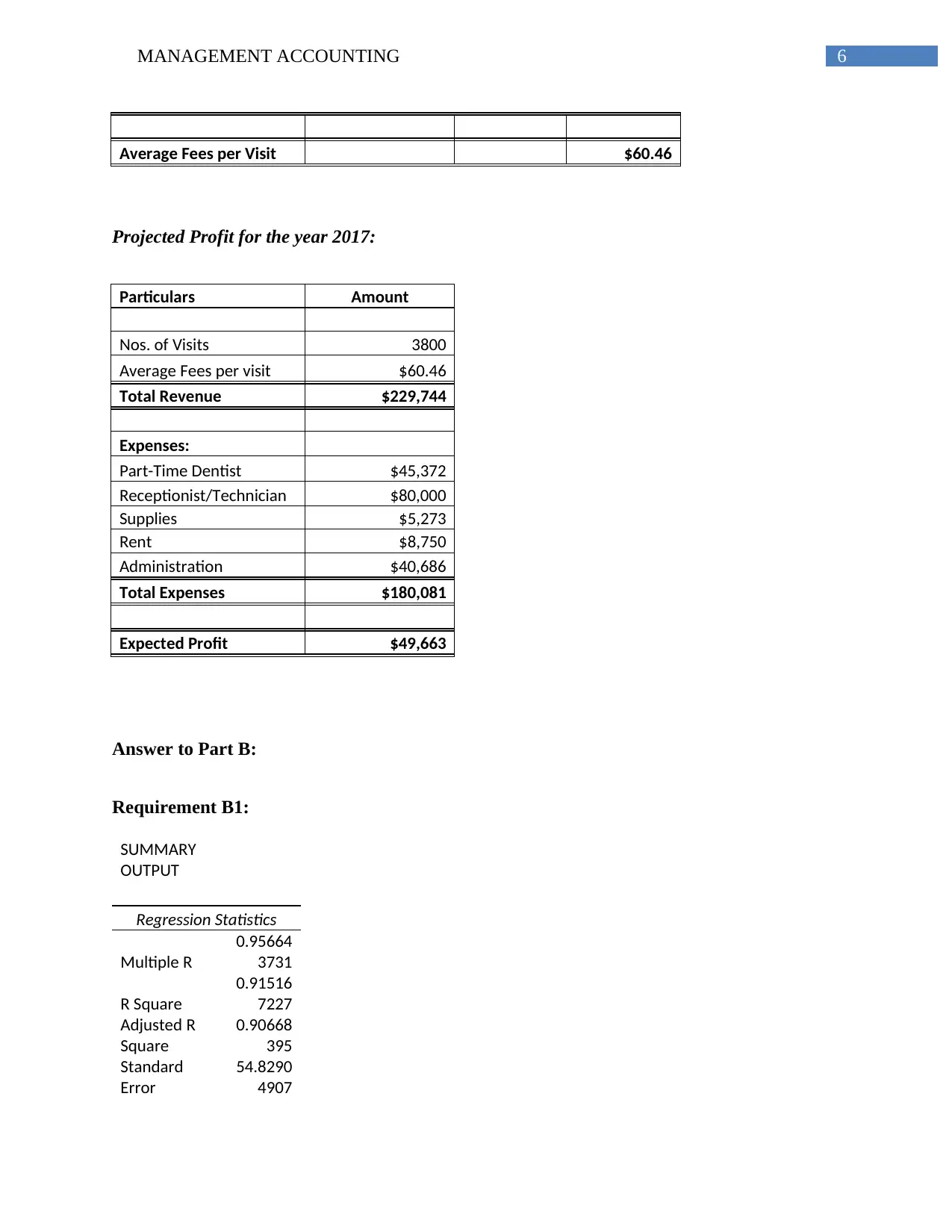

Average Fees per Visit $60.46

Projected Profit for the year 2017:

Particulars Amount

Nos. of Visits 3800

Average Fees per visit $60.46

Total Revenue $229,744

Expenses:

Part-Time Dentist $45,372

Receptionist/Technician $80,000

Supplies $5,273

Rent $8,750

Administration $40,686

Total Expenses $180,081

Expected Profit $49,663

Answer to Part B:

Requirement B1:

SUMMARY

OUTPUT

Regression Statistics

Multiple R

0.95664

3731

R Square

0.91516

7227

Adjusted R

Square

0.90668

395

Standard

Error

54.8290

4907

Average Fees per Visit $60.46

Projected Profit for the year 2017:

Particulars Amount

Nos. of Visits 3800

Average Fees per visit $60.46

Total Revenue $229,744

Expenses:

Part-Time Dentist $45,372

Receptionist/Technician $80,000

Supplies $5,273

Rent $8,750

Administration $40,686

Total Expenses $180,081

Expected Profit $49,663

Answer to Part B:

Requirement B1:

SUMMARY

OUTPUT

Regression Statistics

Multiple R

0.95664

3731

R Square

0.91516

7227

Adjusted R

Square

0.90668

395

Standard

Error

54.8290

4907

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

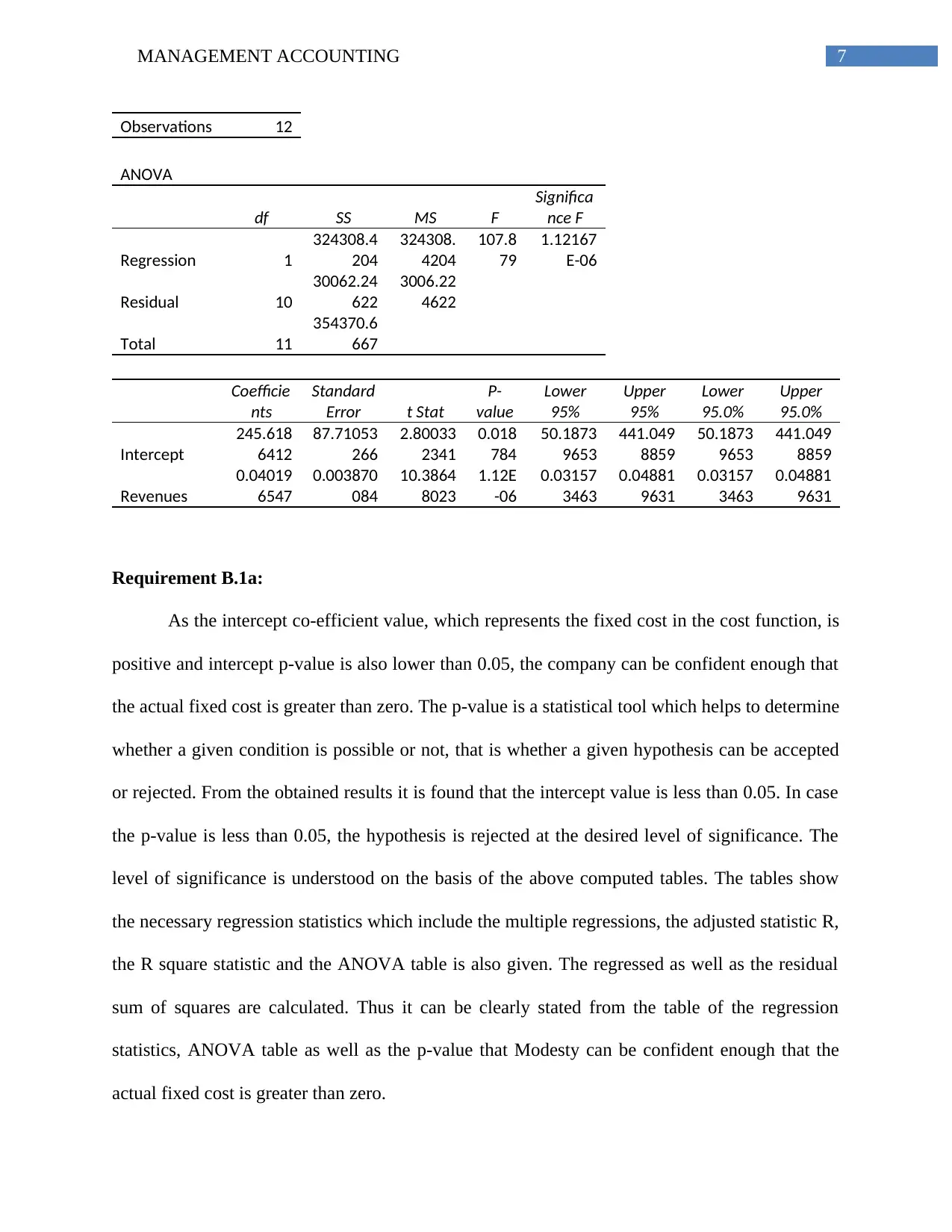

Observations 12

ANOVA

df SS MS F

Significa

nce F

Regression 1

324308.4

204

324308.

4204

107.8

79

1.12167

E-06

Residual 10

30062.24

622

3006.22

4622

Total 11

354370.6

667

Coefficie

nts

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

245.618

6412

87.71053

266

2.80033

2341

0.018

784

50.1873

9653

441.049

8859

50.1873

9653

441.049

8859

Revenues

0.04019

6547

0.003870

084

10.3864

8023

1.12E

-06

0.03157

3463

0.04881

9631

0.03157

3463

0.04881

9631

Requirement B.1a:

As the intercept co-efficient value, which represents the fixed cost in the cost function, is

positive and intercept p-value is also lower than 0.05, the company can be confident enough that

the actual fixed cost is greater than zero. The p-value is a statistical tool which helps to determine

whether a given condition is possible or not, that is whether a given hypothesis can be accepted

or rejected. From the obtained results it is found that the intercept value is less than 0.05. In case

the p-value is less than 0.05, the hypothesis is rejected at the desired level of significance. The

level of significance is understood on the basis of the above computed tables. The tables show

the necessary regression statistics which include the multiple regressions, the adjusted statistic R,

the R square statistic and the ANOVA table is also given. The regressed as well as the residual

sum of squares are calculated. Thus it can be clearly stated from the table of the regression

statistics, ANOVA table as well as the p-value that Modesty can be confident enough that the

actual fixed cost is greater than zero.

Observations 12

ANOVA

df SS MS F

Significa

nce F

Regression 1

324308.4

204

324308.

4204

107.8

79

1.12167

E-06

Residual 10

30062.24

622

3006.22

4622

Total 11

354370.6

667

Coefficie

nts

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

245.618

6412

87.71053

266

2.80033

2341

0.018

784

50.1873

9653

441.049

8859

50.1873

9653

441.049

8859

Revenues

0.04019

6547

0.003870

084

10.3864

8023

1.12E

-06

0.03157

3463

0.04881

9631

0.03157

3463

0.04881

9631

Requirement B.1a:

As the intercept co-efficient value, which represents the fixed cost in the cost function, is

positive and intercept p-value is also lower than 0.05, the company can be confident enough that

the actual fixed cost is greater than zero. The p-value is a statistical tool which helps to determine

whether a given condition is possible or not, that is whether a given hypothesis can be accepted

or rejected. From the obtained results it is found that the intercept value is less than 0.05. In case

the p-value is less than 0.05, the hypothesis is rejected at the desired level of significance. The

level of significance is understood on the basis of the above computed tables. The tables show

the necessary regression statistics which include the multiple regressions, the adjusted statistic R,

the R square statistic and the ANOVA table is also given. The regressed as well as the residual

sum of squares are calculated. Thus it can be clearly stated from the table of the regression

statistics, ANOVA table as well as the p-value that Modesty can be confident enough that the

actual fixed cost is greater than zero.

8MANAGEMENT ACCOUNTING

Requirement B.1b:

The revenue co-efficient, which is the variable cost per unit, is positive and the p-value is

lower than 0.05. Therefore, it can be stated confidently that actual variable cost per unit of the

cost driver is greater than zero. In this case as well the values calculated help modesty reach a

conclusion that the actual cost of the variable is greater than zero. The p-value being lower than

0.05 helps come to the conclusion that the hypothetical assumption is to be neglected and also

the actual variable cost is significantly greater than zero.

Requirement B.1c:

As per the R-square the cost driver is capable to explain the cost behavior up to 91.5%,

which further states that the cost driver is fit enough for the cost behavior. From the table of the

regression values, the adjusted R, the R square as well as the information on the total number of

observations, the implications can be clearly understood. The value of the adjusted R square and

the multiple R square values it is found that the cost driver significantly explains cost behavior.

This is because the R- square is a statistical measure of how close the given data are close to the

best fitted regression line. The more the percentage, that is more the obtained value after

multiplication of the value of R square by 100, the more the capability of the data to explain the

nature of the variability or the connection of the data to the obtained results. In this case, the

obtained value is 91.5%, so this is said that the cost driver explains the variation to a huge extent.

Requirement B.2:

SUMMARY

OUTPUT

Regression Statistics

Multiple R

0.42219

7091

R Square 0.17825

Requirement B.1b:

The revenue co-efficient, which is the variable cost per unit, is positive and the p-value is

lower than 0.05. Therefore, it can be stated confidently that actual variable cost per unit of the

cost driver is greater than zero. In this case as well the values calculated help modesty reach a

conclusion that the actual cost of the variable is greater than zero. The p-value being lower than

0.05 helps come to the conclusion that the hypothetical assumption is to be neglected and also

the actual variable cost is significantly greater than zero.

Requirement B.1c:

As per the R-square the cost driver is capable to explain the cost behavior up to 91.5%,

which further states that the cost driver is fit enough for the cost behavior. From the table of the

regression values, the adjusted R, the R square as well as the information on the total number of

observations, the implications can be clearly understood. The value of the adjusted R square and

the multiple R square values it is found that the cost driver significantly explains cost behavior.

This is because the R- square is a statistical measure of how close the given data are close to the

best fitted regression line. The more the percentage, that is more the obtained value after

multiplication of the value of R square by 100, the more the capability of the data to explain the

nature of the variability or the connection of the data to the obtained results. In this case, the

obtained value is 91.5%, so this is said that the cost driver explains the variation to a huge extent.

Requirement B.2:

SUMMARY

OUTPUT

Regression Statistics

Multiple R

0.42219

7091

R Square 0.17825

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

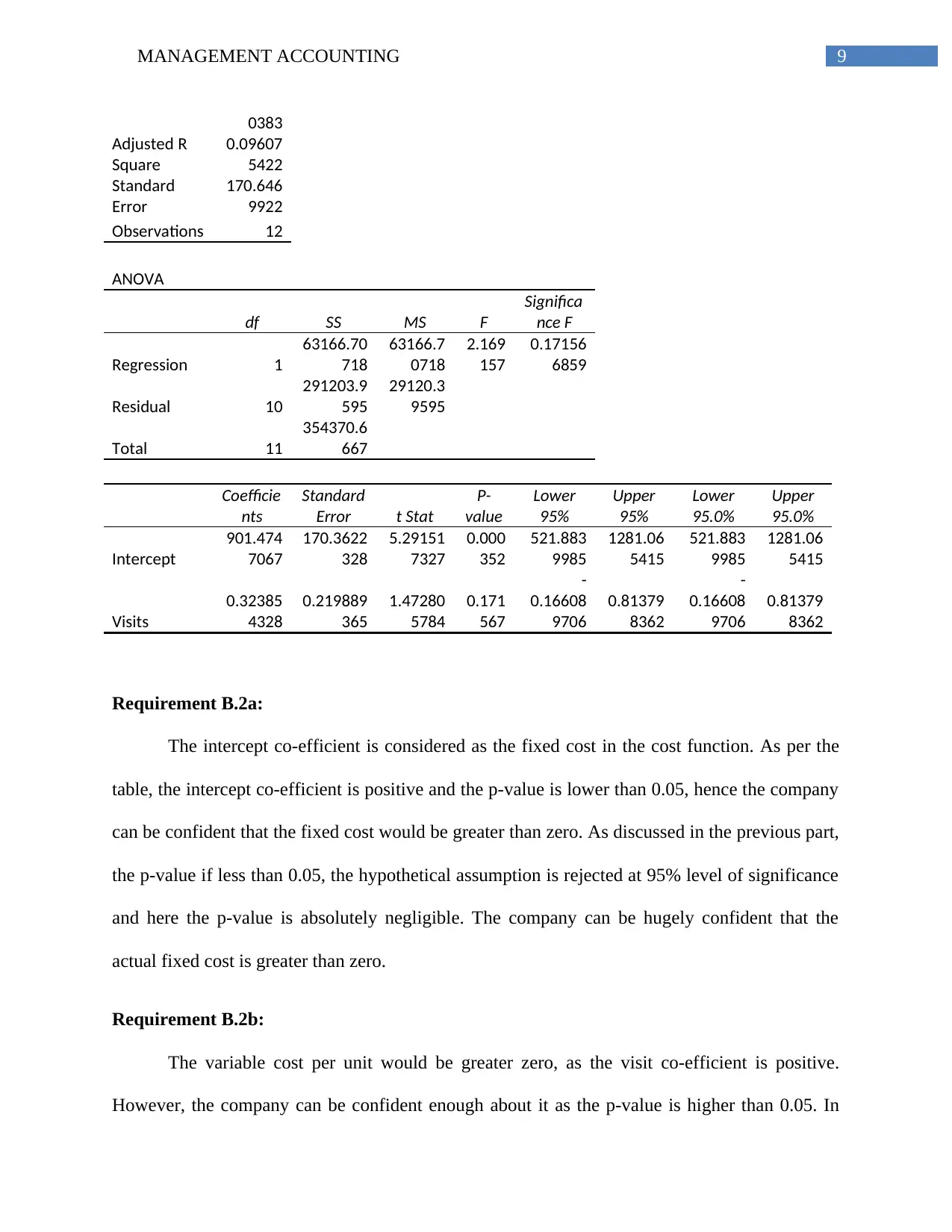

0383

Adjusted R

Square

0.09607

5422

Standard

Error

170.646

9922

Observations 12

ANOVA

df SS MS F

Significa

nce F

Regression 1

63166.70

718

63166.7

0718

2.169

157

0.17156

6859

Residual 10

291203.9

595

29120.3

9595

Total 11

354370.6

667

Coefficie

nts

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

901.474

7067

170.3622

328

5.29151

7327

0.000

352

521.883

9985

1281.06

5415

521.883

9985

1281.06

5415

Visits

0.32385

4328

0.219889

365

1.47280

5784

0.171

567

-

0.16608

9706

0.81379

8362

-

0.16608

9706

0.81379

8362

Requirement B.2a:

The intercept co-efficient is considered as the fixed cost in the cost function. As per the

table, the intercept co-efficient is positive and the p-value is lower than 0.05, hence the company

can be confident that the fixed cost would be greater than zero. As discussed in the previous part,

the p-value if less than 0.05, the hypothetical assumption is rejected at 95% level of significance

and here the p-value is absolutely negligible. The company can be hugely confident that the

actual fixed cost is greater than zero.

Requirement B.2b:

The variable cost per unit would be greater zero, as the visit co-efficient is positive.

However, the company can be confident enough about it as the p-value is higher than 0.05. In

0383

Adjusted R

Square

0.09607

5422

Standard

Error

170.646

9922

Observations 12

ANOVA

df SS MS F

Significa

nce F

Regression 1

63166.70

718

63166.7

0718

2.169

157

0.17156

6859

Residual 10

291203.9

595

29120.3

9595

Total 11

354370.6

667

Coefficie

nts

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

901.474

7067

170.3622

328

5.29151

7327

0.000

352

521.883

9985

1281.06

5415

521.883

9985

1281.06

5415

Visits

0.32385

4328

0.219889

365

1.47280

5784

0.171

567

-

0.16608

9706

0.81379

8362

-

0.16608

9706

0.81379

8362

Requirement B.2a:

The intercept co-efficient is considered as the fixed cost in the cost function. As per the

table, the intercept co-efficient is positive and the p-value is lower than 0.05, hence the company

can be confident that the fixed cost would be greater than zero. As discussed in the previous part,

the p-value if less than 0.05, the hypothetical assumption is rejected at 95% level of significance

and here the p-value is absolutely negligible. The company can be hugely confident that the

actual fixed cost is greater than zero.

Requirement B.2b:

The variable cost per unit would be greater zero, as the visit co-efficient is positive.

However, the company can be confident enough about it as the p-value is higher than 0.05. In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

this case also due to the negligible p value the conclusion is arrived at that the actual variable

cost is greater than zero. The data is also significant and helpful in concluding that the actual

variable cost is greater than zero. The p-value is basically an important statistical measure to

determine whether the assumed statistical fact is genuine or not. This measure is useful in major

company decisions related to the cost drivers as well as the several factors contributing to the

company.

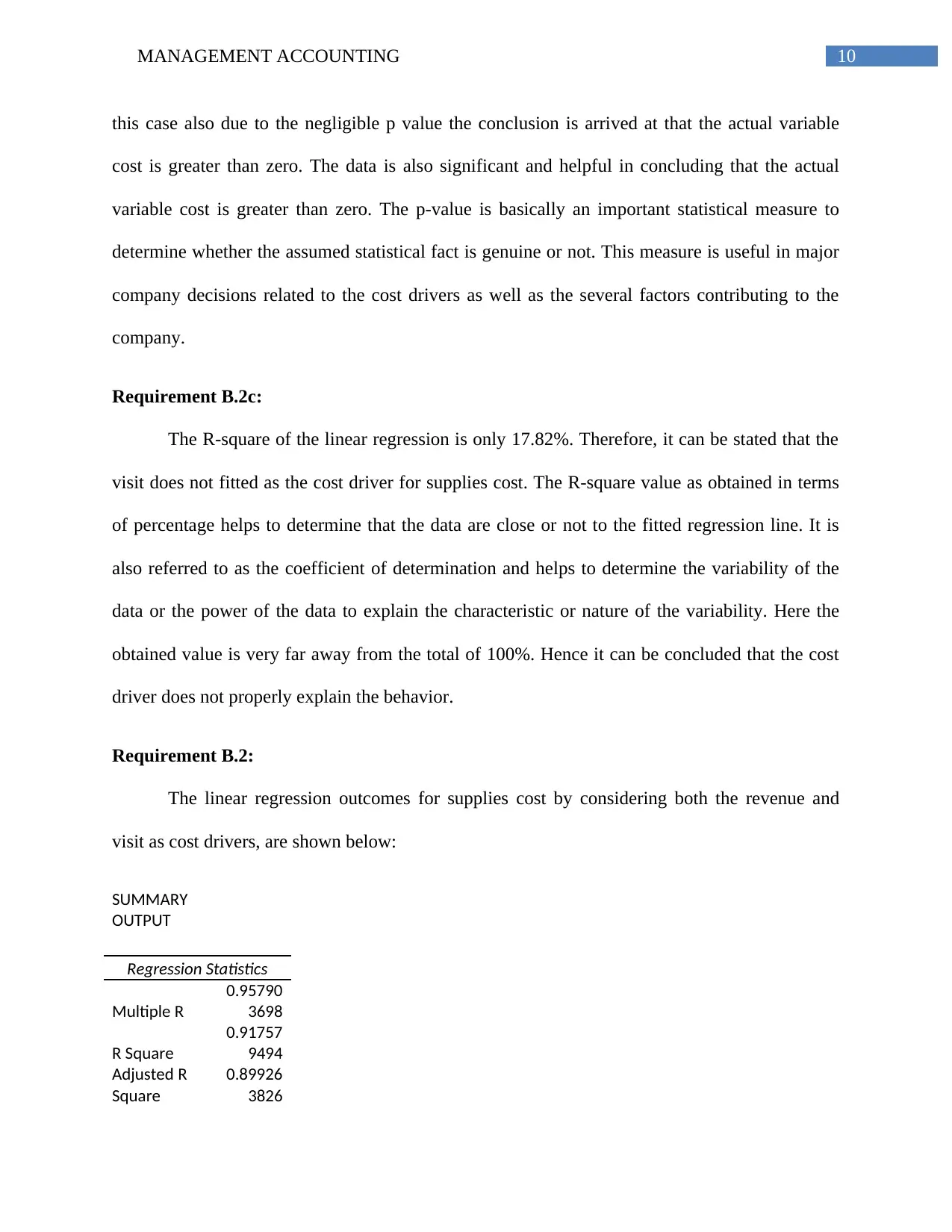

Requirement B.2c:

The R-square of the linear regression is only 17.82%. Therefore, it can be stated that the

visit does not fitted as the cost driver for supplies cost. The R-square value as obtained in terms

of percentage helps to determine that the data are close or not to the fitted regression line. It is

also referred to as the coefficient of determination and helps to determine the variability of the

data or the power of the data to explain the characteristic or nature of the variability. Here the

obtained value is very far away from the total of 100%. Hence it can be concluded that the cost

driver does not properly explain the behavior.

Requirement B.2:

The linear regression outcomes for supplies cost by considering both the revenue and

visit as cost drivers, are shown below:

SUMMARY

OUTPUT

Regression Statistics

Multiple R

0.95790

3698

R Square

0.91757

9494

Adjusted R

Square

0.89926

3826

this case also due to the negligible p value the conclusion is arrived at that the actual variable

cost is greater than zero. The data is also significant and helpful in concluding that the actual

variable cost is greater than zero. The p-value is basically an important statistical measure to

determine whether the assumed statistical fact is genuine or not. This measure is useful in major

company decisions related to the cost drivers as well as the several factors contributing to the

company.

Requirement B.2c:

The R-square of the linear regression is only 17.82%. Therefore, it can be stated that the

visit does not fitted as the cost driver for supplies cost. The R-square value as obtained in terms

of percentage helps to determine that the data are close or not to the fitted regression line. It is

also referred to as the coefficient of determination and helps to determine the variability of the

data or the power of the data to explain the characteristic or nature of the variability. Here the

obtained value is very far away from the total of 100%. Hence it can be concluded that the cost

driver does not properly explain the behavior.

Requirement B.2:

The linear regression outcomes for supplies cost by considering both the revenue and

visit as cost drivers, are shown below:

SUMMARY

OUTPUT

Regression Statistics

Multiple R

0.95790

3698

R Square

0.91757

9494

Adjusted R

Square

0.89926

3826

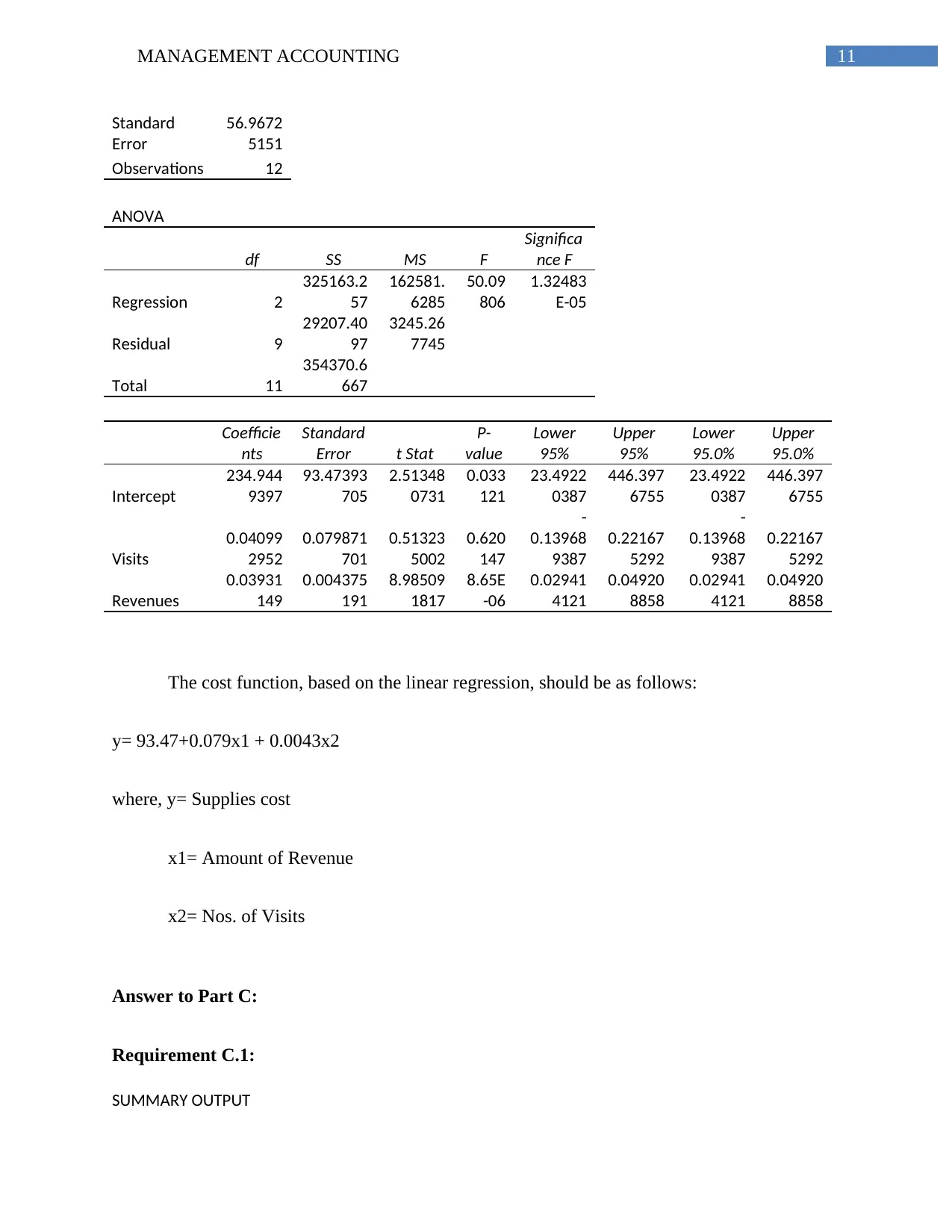

11MANAGEMENT ACCOUNTING

Standard

Error

56.9672

5151

Observations 12

ANOVA

df SS MS F

Significa

nce F

Regression 2

325163.2

57

162581.

6285

50.09

806

1.32483

E-05

Residual 9

29207.40

97

3245.26

7745

Total 11

354370.6

667

Coefficie

nts

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

234.944

9397

93.47393

705

2.51348

0731

0.033

121

23.4922

0387

446.397

6755

23.4922

0387

446.397

6755

Visits

0.04099

2952

0.079871

701

0.51323

5002

0.620

147

-

0.13968

9387

0.22167

5292

-

0.13968

9387

0.22167

5292

Revenues

0.03931

149

0.004375

191

8.98509

1817

8.65E

-06

0.02941

4121

0.04920

8858

0.02941

4121

0.04920

8858

The cost function, based on the linear regression, should be as follows:

y= 93.47+0.079x1 + 0.0043x2

where, y= Supplies cost

x1= Amount of Revenue

x2= Nos. of Visits

Answer to Part C:

Requirement C.1:

SUMMARY OUTPUT

Standard

Error

56.9672

5151

Observations 12

ANOVA

df SS MS F

Significa

nce F

Regression 2

325163.2

57

162581.

6285

50.09

806

1.32483

E-05

Residual 9

29207.40

97

3245.26

7745

Total 11

354370.6

667

Coefficie

nts

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

234.944

9397

93.47393

705

2.51348

0731

0.033

121

23.4922

0387

446.397

6755

23.4922

0387

446.397

6755

Visits

0.04099

2952

0.079871

701

0.51323

5002

0.620

147

-

0.13968

9387

0.22167

5292

-

0.13968

9387

0.22167

5292

Revenues

0.03931

149

0.004375

191

8.98509

1817

8.65E

-06

0.02941

4121

0.04920

8858

0.02941

4121

0.04920

8858

The cost function, based on the linear regression, should be as follows:

y= 93.47+0.079x1 + 0.0043x2

where, y= Supplies cost

x1= Amount of Revenue

x2= Nos. of Visits

Answer to Part C:

Requirement C.1:

SUMMARY OUTPUT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.