University Management Accounting Assignment: Financial Analysis Report

VerifiedAdded on 2022/09/08

|11

|2339

|19

Homework Assignment

AI Summary

This document presents a comprehensive solution to a management accounting assignment, addressing various aspects of financial statement analysis. Part A includes detailed answers to essay questions, such as how financial statements are used by bankers, investors, and labor negotiators, as well as identifying violations of accounting principles. Part B provides solutions to exercises and questions, including the preparation of financial statements like income statements and balance sheets, along with the application of accounting principles. The assignment covers topics such as debt levels, dividends, auditor's reports, the accounting equation, and the use of subsidiary ledgers. The solution demonstrates an understanding of financial reporting, analysis, and interpretation, providing a valuable resource for students studying management accounting.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student

Name of the University

Author Note

Management Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Part A...............................................................................................................................................2

Answer to Question 1...................................................................................................................2

Answer to Question 2...................................................................................................................2

Answer to Question 3...................................................................................................................2

Answer to Question 4...................................................................................................................2

Answer to Question 5...................................................................................................................3

Answer to Question 6...................................................................................................................3

Answer to Question 7...................................................................................................................3

Part B...............................................................................................................................................4

Answer to Exercise 1...................................................................................................................4

Answer to Exercise 2...................................................................................................................4

Answer to Question 3...................................................................................................................5

Answer to Exercise 4...................................................................................................................5

Answer to Exercise 5...................................................................................................................6

Answer to Question 6...................................................................................................................7

Answer to Question 7...................................................................................................................7

Answer to Question 8...................................................................................................................9

References and Bibliography.....................................................................................................10

Table of Contents

Part A...............................................................................................................................................2

Answer to Question 1...................................................................................................................2

Answer to Question 2...................................................................................................................2

Answer to Question 3...................................................................................................................2

Answer to Question 4...................................................................................................................2

Answer to Question 5...................................................................................................................3

Answer to Question 6...................................................................................................................3

Answer to Question 7...................................................................................................................3

Part B...............................................................................................................................................4

Answer to Exercise 1...................................................................................................................4

Answer to Exercise 2...................................................................................................................4

Answer to Question 3...................................................................................................................5

Answer to Exercise 4...................................................................................................................5

Answer to Exercise 5...................................................................................................................6

Answer to Question 6...................................................................................................................7

Answer to Question 7...................................................................................................................7

Answer to Question 8...................................................................................................................9

References and Bibliography.....................................................................................................10

2MANAGEMENT ACCOUNTING

Part A

Answer to Question 1

A) The information provided in financial statements is useful in deciding whether a loan

should be granted to a business or not. The credit worthiness and the scope of bad debts

of the business can be determined by using the debt repayment details of the business.

B) The information that would be required from the financial statements of the entity are the

dividend yield of the company. The changes in the share prices of the entity over the

years are also essential to assess the company’s prospects (Gitman, Juchau and Flanagan

2015).

C) The financial statements can be used in negotiations with the management about

increasing the salaries of the employees. The profit levels and trends of the business can

be used as a basis for suggesting the rate of improvement in the salaries.

Answer to Question 2

The matching concept has been violated in this situation as the asset is not related to the

business.

The historical cost assumption principle has been violated in this situation.

The time period assumption is being violated in this case.

The going concern assumption is being violated in this particular situation.

Answer to Question 3

The financial statements would be used in reviewing the debt levels and ratio between the

assets and liabilities of the company. It will also be used in assessing the risk of default of the

loan and the revenues generated by the entity. The overall profitability will also be taken into

consideration.

Answer to Question 4

The main difference between dividends and other expenditures are the person to whom

they are paid to. Dividends are paid to the shareholders, who are the owners of the company.

They can only be paid to the shareholders after paying all the remaining expenditures. Other

expenditures are allowed as a deduction in calculating the income taxes. Dividends are paid after

the payment of the taxes to the authorities (Ofori‐Sasu, Abor and Osei 2017).

Part A

Answer to Question 1

A) The information provided in financial statements is useful in deciding whether a loan

should be granted to a business or not. The credit worthiness and the scope of bad debts

of the business can be determined by using the debt repayment details of the business.

B) The information that would be required from the financial statements of the entity are the

dividend yield of the company. The changes in the share prices of the entity over the

years are also essential to assess the company’s prospects (Gitman, Juchau and Flanagan

2015).

C) The financial statements can be used in negotiations with the management about

increasing the salaries of the employees. The profit levels and trends of the business can

be used as a basis for suggesting the rate of improvement in the salaries.

Answer to Question 2

The matching concept has been violated in this situation as the asset is not related to the

business.

The historical cost assumption principle has been violated in this situation.

The time period assumption is being violated in this case.

The going concern assumption is being violated in this particular situation.

Answer to Question 3

The financial statements would be used in reviewing the debt levels and ratio between the

assets and liabilities of the company. It will also be used in assessing the risk of default of the

loan and the revenues generated by the entity. The overall profitability will also be taken into

consideration.

Answer to Question 4

The main difference between dividends and other expenditures are the person to whom

they are paid to. Dividends are paid to the shareholders, who are the owners of the company.

They can only be paid to the shareholders after paying all the remaining expenditures. Other

expenditures are allowed as a deduction in calculating the income taxes. Dividends are paid after

the payment of the taxes to the authorities (Ofori‐Sasu, Abor and Osei 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

Answer to Question 5

a. The main purpose of the auditor’s report is to provide a reasonable assurance that the

books of accounts are free from any major errors. They apply all the required procedures

to make a judgement on the validity of the financial statements.

b. A going concern is a business which plans to continue its operations in the near future

and not liquidate itself at the end of the financial year. The business is looking to grow

and expand into the future while also trying to maintain the accepted levels of

profitability (Fischer, Marsh and Brown 2016).

c. No, it cannot be said that aspects like losses, restructuring and the disposal of segments

are the precursors to the demise of a company. They can also be considered to be steps

towards making the company more efficient and profitable for the period following the

period for which the above mentioned activities have taken place.

d. The auditors are suggesting that the losses incurred by the company have resulted in the

overall deficit of the company going up to $49.7 million. The lack of sufficient cash and

working capital with the company add to the doubts that the company may not be able to

continue its operations in the foreseeable future. The plans of the management do not

contain any details about the adjustments that have occurred as a result of the

uncertainties.

Answer to Question 6

Merck & Co. mean that the results of the lawsuits faced by them are likely to result in

their favour. The losses that will be incurred by them due to these lawsuits are not likely to cause

any material changes in the financial statements of the entity. Here, material means the changes

are unlikely to cause major losses to the company. Remote means the chances of losses

occurring due to the lawsuits are extremely low or unlikely. The legal authorities are in the best

position to determine the outcome of a lawsuit (Hærem, Pentland and Miller 2015).

Answer to Question 7

On the basis of the information provided, it can be said that Unique Factory is a business

entity. This is because the financial statements suggest that the entity is involved in the sales of

goods and is incurring administrative and other expenses. It is also recording net income in its

books of accounts after the payment of taxes. It is also recording depreciation on the assets and

Answer to Question 5

a. The main purpose of the auditor’s report is to provide a reasonable assurance that the

books of accounts are free from any major errors. They apply all the required procedures

to make a judgement on the validity of the financial statements.

b. A going concern is a business which plans to continue its operations in the near future

and not liquidate itself at the end of the financial year. The business is looking to grow

and expand into the future while also trying to maintain the accepted levels of

profitability (Fischer, Marsh and Brown 2016).

c. No, it cannot be said that aspects like losses, restructuring and the disposal of segments

are the precursors to the demise of a company. They can also be considered to be steps

towards making the company more efficient and profitable for the period following the

period for which the above mentioned activities have taken place.

d. The auditors are suggesting that the losses incurred by the company have resulted in the

overall deficit of the company going up to $49.7 million. The lack of sufficient cash and

working capital with the company add to the doubts that the company may not be able to

continue its operations in the foreseeable future. The plans of the management do not

contain any details about the adjustments that have occurred as a result of the

uncertainties.

Answer to Question 6

Merck & Co. mean that the results of the lawsuits faced by them are likely to result in

their favour. The losses that will be incurred by them due to these lawsuits are not likely to cause

any material changes in the financial statements of the entity. Here, material means the changes

are unlikely to cause major losses to the company. Remote means the chances of losses

occurring due to the lawsuits are extremely low or unlikely. The legal authorities are in the best

position to determine the outcome of a lawsuit (Hærem, Pentland and Miller 2015).

Answer to Question 7

On the basis of the information provided, it can be said that Unique Factory is a business

entity. This is because the financial statements suggest that the entity is involved in the sales of

goods and is incurring administrative and other expenses. It is also recording net income in its

books of accounts after the payment of taxes. It is also recording depreciation on the assets and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

the liabilities of the entity, net of accumulated depreciation. Hence, these suggest that the

business is being carried on to make profits through the normal course of business.

Part B

Answer to Exercise 1

Particulars Amount

Long-term debt 41000

Accounts

Payable

24000

Total Liabilities 65000

Answer to Exercise 2

Particulars Amount

Sales 560000

Less: Cost of Goods Sold 400000

Gross Profit 160000

Less: Salary Expense 40000

PBIT 120000

Less: Interest expense 30000

PBT 90000

Less: Income tax expense 25000

Net Income for the company 65000

the liabilities of the entity, net of accumulated depreciation. Hence, these suggest that the

business is being carried on to make profits through the normal course of business.

Part B

Answer to Exercise 1

Particulars Amount

Long-term debt 41000

Accounts

Payable

24000

Total Liabilities 65000

Answer to Exercise 2

Particulars Amount

Sales 560000

Less: Cost of Goods Sold 400000

Gross Profit 160000

Less: Salary Expense 40000

PBIT 120000

Less: Interest expense 30000

PBT 90000

Less: Income tax expense 25000

Net Income for the company 65000

5MANAGEMENT ACCOUNTING

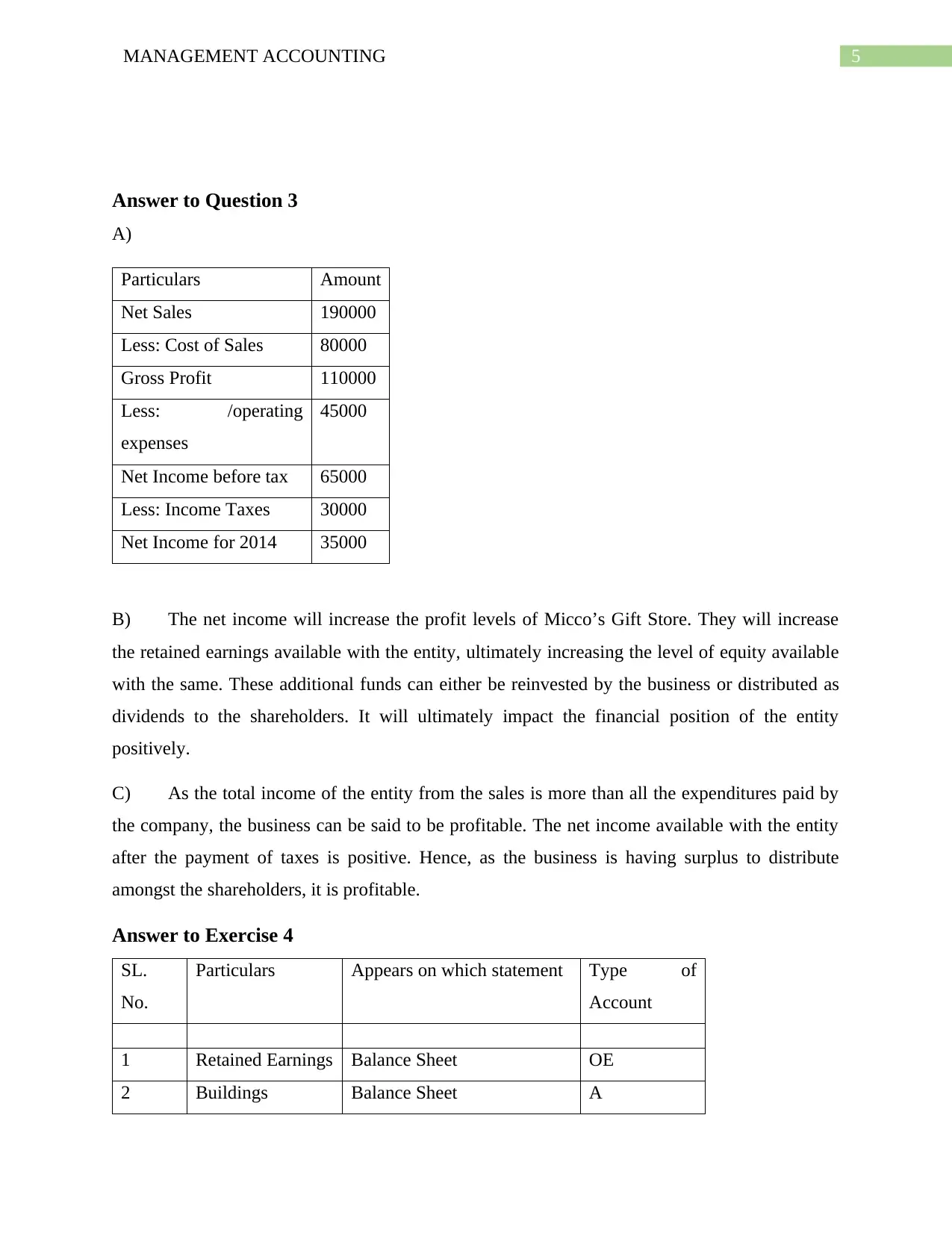

Answer to Question 3

A)

Particulars Amount

Net Sales 190000

Less: Cost of Sales 80000

Gross Profit 110000

Less: /operating

expenses

45000

Net Income before tax 65000

Less: Income Taxes 30000

Net Income for 2014 35000

B) The net income will increase the profit levels of Micco’s Gift Store. They will increase

the retained earnings available with the entity, ultimately increasing the level of equity available

with the same. These additional funds can either be reinvested by the business or distributed as

dividends to the shareholders. It will ultimately impact the financial position of the entity

positively.

C) As the total income of the entity from the sales is more than all the expenditures paid by

the company, the business can be said to be profitable. The net income available with the entity

after the payment of taxes is positive. Hence, as the business is having surplus to distribute

amongst the shareholders, it is profitable.

Answer to Exercise 4

SL.

No.

Particulars Appears on which statement Type of

Account

1 Retained Earnings Balance Sheet OE

2 Buildings Balance Sheet A

Answer to Question 3

A)

Particulars Amount

Net Sales 190000

Less: Cost of Sales 80000

Gross Profit 110000

Less: /operating

expenses

45000

Net Income before tax 65000

Less: Income Taxes 30000

Net Income for 2014 35000

B) The net income will increase the profit levels of Micco’s Gift Store. They will increase

the retained earnings available with the entity, ultimately increasing the level of equity available

with the same. These additional funds can either be reinvested by the business or distributed as

dividends to the shareholders. It will ultimately impact the financial position of the entity

positively.

C) As the total income of the entity from the sales is more than all the expenditures paid by

the company, the business can be said to be profitable. The net income available with the entity

after the payment of taxes is positive. Hence, as the business is having surplus to distribute

amongst the shareholders, it is profitable.

Answer to Exercise 4

SL.

No.

Particulars Appears on which statement Type of

Account

1 Retained Earnings Balance Sheet OE

2 Buildings Balance Sheet A

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

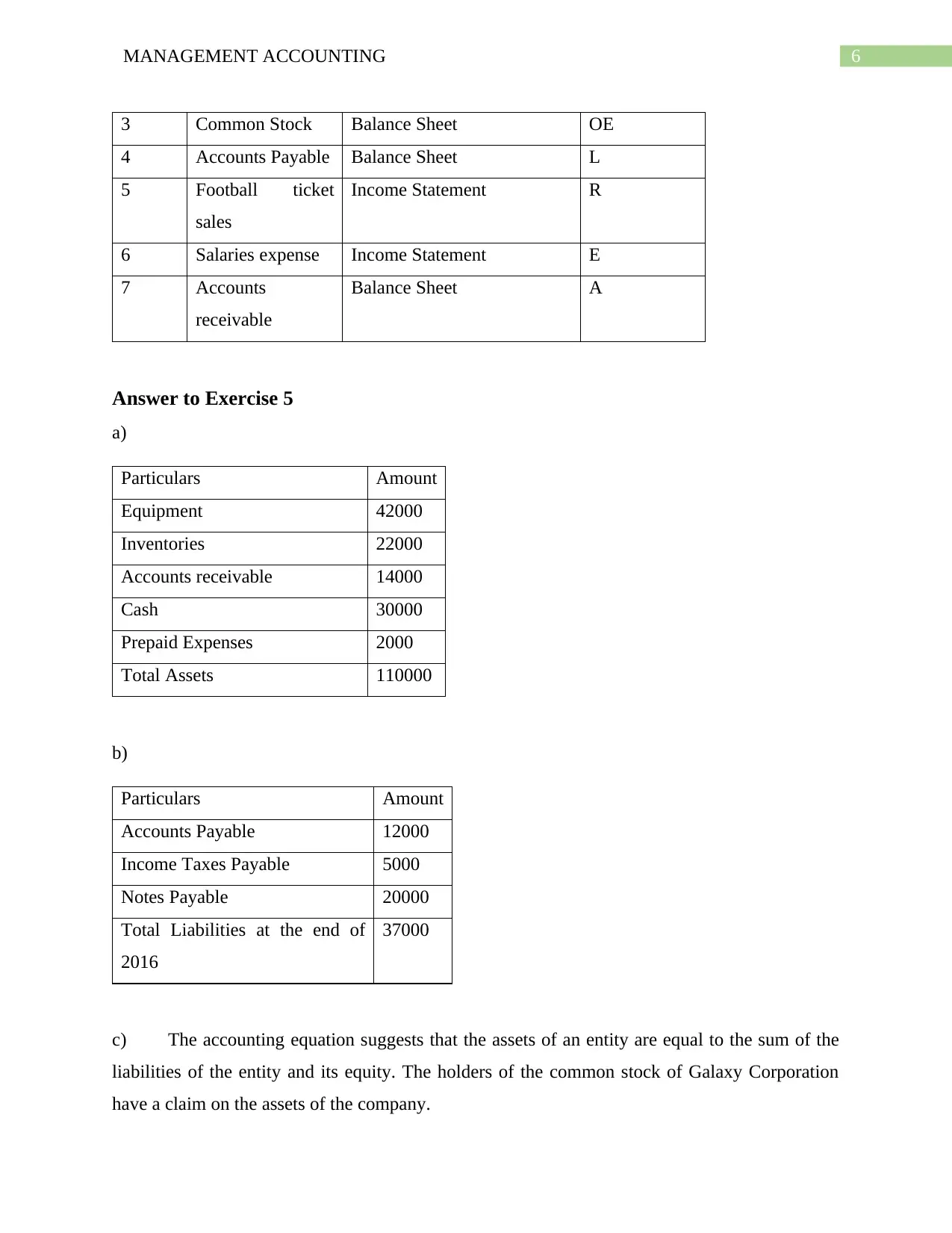

3 Common Stock Balance Sheet OE

4 Accounts Payable Balance Sheet L

5 Football ticket

sales

Income Statement R

6 Salaries expense Income Statement E

7 Accounts

receivable

Balance Sheet A

Answer to Exercise 5

a)

Particulars Amount

Equipment 42000

Inventories 22000

Accounts receivable 14000

Cash 30000

Prepaid Expenses 2000

Total Assets 110000

b)

Particulars Amount

Accounts Payable 12000

Income Taxes Payable 5000

Notes Payable 20000

Total Liabilities at the end of

2016

37000

c) The accounting equation suggests that the assets of an entity are equal to the sum of the

liabilities of the entity and its equity. The holders of the common stock of Galaxy Corporation

have a claim on the assets of the company.

3 Common Stock Balance Sheet OE

4 Accounts Payable Balance Sheet L

5 Football ticket

sales

Income Statement R

6 Salaries expense Income Statement E

7 Accounts

receivable

Balance Sheet A

Answer to Exercise 5

a)

Particulars Amount

Equipment 42000

Inventories 22000

Accounts receivable 14000

Cash 30000

Prepaid Expenses 2000

Total Assets 110000

b)

Particulars Amount

Accounts Payable 12000

Income Taxes Payable 5000

Notes Payable 20000

Total Liabilities at the end of

2016

37000

c) The accounting equation suggests that the assets of an entity are equal to the sum of the

liabilities of the entity and its equity. The holders of the common stock of Galaxy Corporation

have a claim on the assets of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

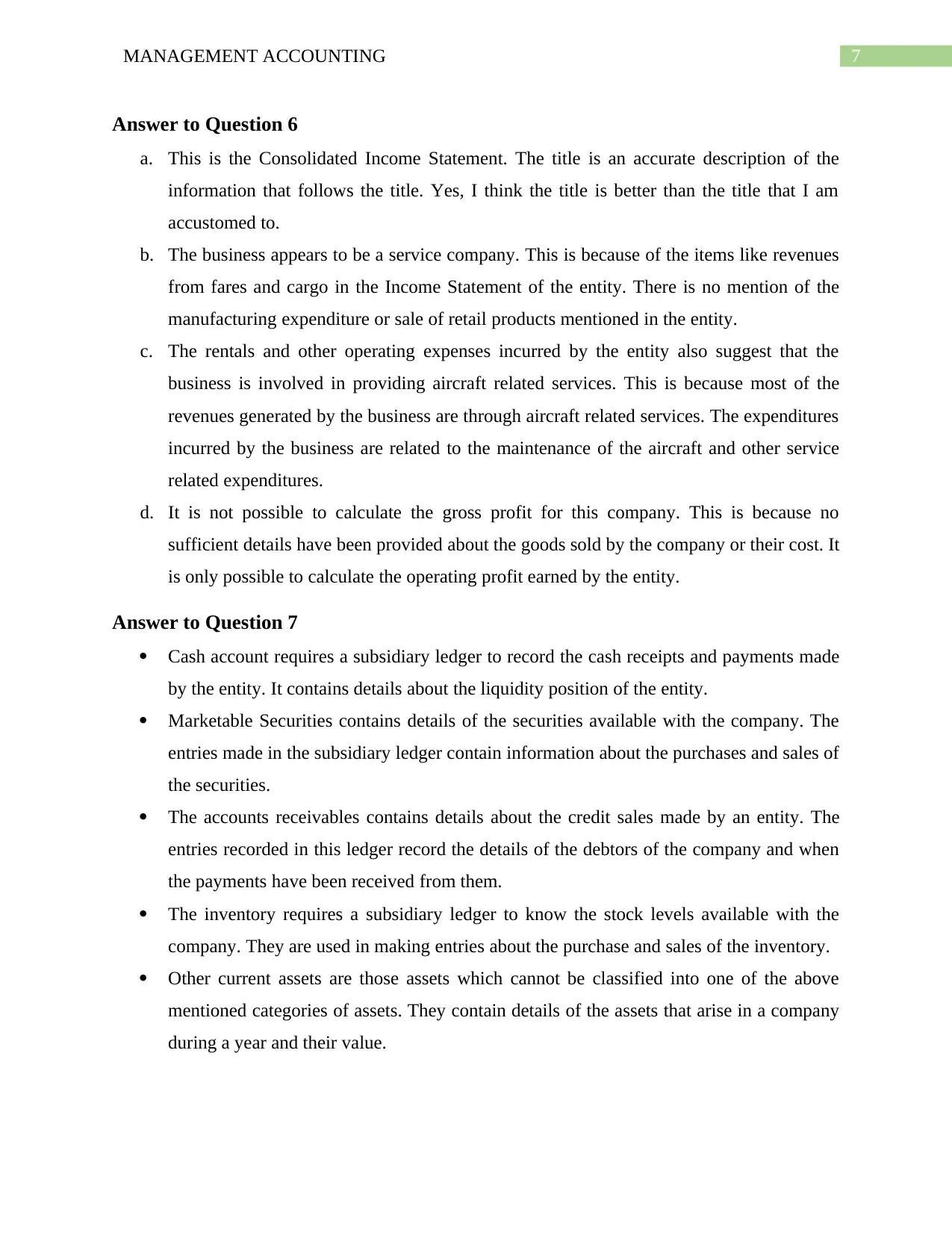

Answer to Question 6

a. This is the Consolidated Income Statement. The title is an accurate description of the

information that follows the title. Yes, I think the title is better than the title that I am

accustomed to.

b. The business appears to be a service company. This is because of the items like revenues

from fares and cargo in the Income Statement of the entity. There is no mention of the

manufacturing expenditure or sale of retail products mentioned in the entity.

c. The rentals and other operating expenses incurred by the entity also suggest that the

business is involved in providing aircraft related services. This is because most of the

revenues generated by the business are through aircraft related services. The expenditures

incurred by the business are related to the maintenance of the aircraft and other service

related expenditures.

d. It is not possible to calculate the gross profit for this company. This is because no

sufficient details have been provided about the goods sold by the company or their cost. It

is only possible to calculate the operating profit earned by the entity.

Answer to Question 7

Cash account requires a subsidiary ledger to record the cash receipts and payments made

by the entity. It contains details about the liquidity position of the entity.

Marketable Securities contains details of the securities available with the company. The

entries made in the subsidiary ledger contain information about the purchases and sales of

the securities.

The accounts receivables contains details about the credit sales made by an entity. The

entries recorded in this ledger record the details of the debtors of the company and when

the payments have been received from them.

The inventory requires a subsidiary ledger to know the stock levels available with the

company. They are used in making entries about the purchase and sales of the inventory.

Other current assets are those assets which cannot be classified into one of the above

mentioned categories of assets. They contain details of the assets that arise in a company

during a year and their value.

Answer to Question 6

a. This is the Consolidated Income Statement. The title is an accurate description of the

information that follows the title. Yes, I think the title is better than the title that I am

accustomed to.

b. The business appears to be a service company. This is because of the items like revenues

from fares and cargo in the Income Statement of the entity. There is no mention of the

manufacturing expenditure or sale of retail products mentioned in the entity.

c. The rentals and other operating expenses incurred by the entity also suggest that the

business is involved in providing aircraft related services. This is because most of the

revenues generated by the business are through aircraft related services. The expenditures

incurred by the business are related to the maintenance of the aircraft and other service

related expenditures.

d. It is not possible to calculate the gross profit for this company. This is because no

sufficient details have been provided about the goods sold by the company or their cost. It

is only possible to calculate the operating profit earned by the entity.

Answer to Question 7

Cash account requires a subsidiary ledger to record the cash receipts and payments made

by the entity. It contains details about the liquidity position of the entity.

Marketable Securities contains details of the securities available with the company. The

entries made in the subsidiary ledger contain information about the purchases and sales of

the securities.

The accounts receivables contains details about the credit sales made by an entity. The

entries recorded in this ledger record the details of the debtors of the company and when

the payments have been received from them.

The inventory requires a subsidiary ledger to know the stock levels available with the

company. They are used in making entries about the purchase and sales of the inventory.

Other current assets are those assets which cannot be classified into one of the above

mentioned categories of assets. They contain details of the assets that arise in a company

during a year and their value.

8MANAGEMENT ACCOUNTING

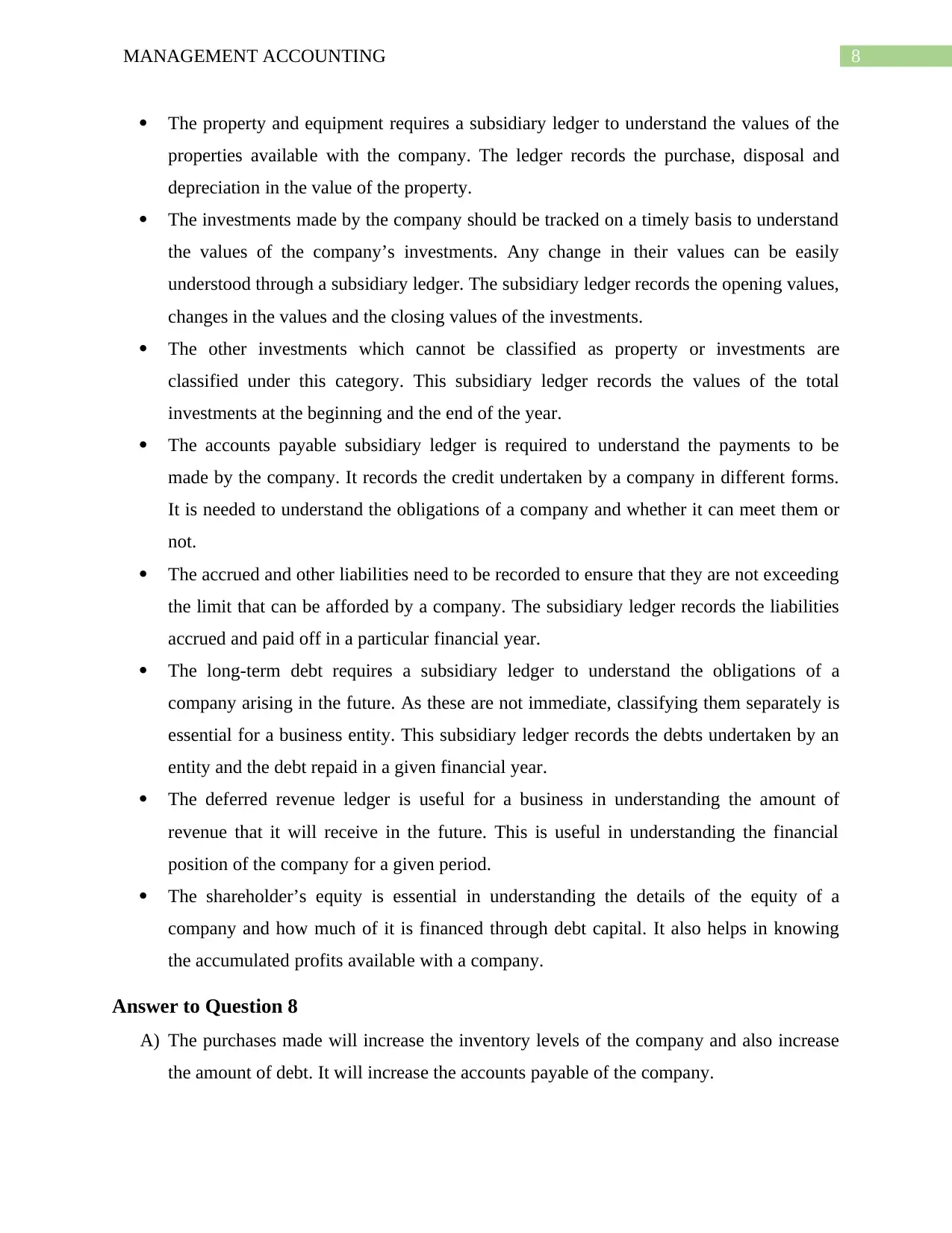

The property and equipment requires a subsidiary ledger to understand the values of the

properties available with the company. The ledger records the purchase, disposal and

depreciation in the value of the property.

The investments made by the company should be tracked on a timely basis to understand

the values of the company’s investments. Any change in their values can be easily

understood through a subsidiary ledger. The subsidiary ledger records the opening values,

changes in the values and the closing values of the investments.

The other investments which cannot be classified as property or investments are

classified under this category. This subsidiary ledger records the values of the total

investments at the beginning and the end of the year.

The accounts payable subsidiary ledger is required to understand the payments to be

made by the company. It records the credit undertaken by a company in different forms.

It is needed to understand the obligations of a company and whether it can meet them or

not.

The accrued and other liabilities need to be recorded to ensure that they are not exceeding

the limit that can be afforded by a company. The subsidiary ledger records the liabilities

accrued and paid off in a particular financial year.

The long-term debt requires a subsidiary ledger to understand the obligations of a

company arising in the future. As these are not immediate, classifying them separately is

essential for a business entity. This subsidiary ledger records the debts undertaken by an

entity and the debt repaid in a given financial year.

The deferred revenue ledger is useful for a business in understanding the amount of

revenue that it will receive in the future. This is useful in understanding the financial

position of the company for a given period.

The shareholder’s equity is essential in understanding the details of the equity of a

company and how much of it is financed through debt capital. It also helps in knowing

the accumulated profits available with a company.

Answer to Question 8

A) The purchases made will increase the inventory levels of the company and also increase

the amount of debt. It will increase the accounts payable of the company.

The property and equipment requires a subsidiary ledger to understand the values of the

properties available with the company. The ledger records the purchase, disposal and

depreciation in the value of the property.

The investments made by the company should be tracked on a timely basis to understand

the values of the company’s investments. Any change in their values can be easily

understood through a subsidiary ledger. The subsidiary ledger records the opening values,

changes in the values and the closing values of the investments.

The other investments which cannot be classified as property or investments are

classified under this category. This subsidiary ledger records the values of the total

investments at the beginning and the end of the year.

The accounts payable subsidiary ledger is required to understand the payments to be

made by the company. It records the credit undertaken by a company in different forms.

It is needed to understand the obligations of a company and whether it can meet them or

not.

The accrued and other liabilities need to be recorded to ensure that they are not exceeding

the limit that can be afforded by a company. The subsidiary ledger records the liabilities

accrued and paid off in a particular financial year.

The long-term debt requires a subsidiary ledger to understand the obligations of a

company arising in the future. As these are not immediate, classifying them separately is

essential for a business entity. This subsidiary ledger records the debts undertaken by an

entity and the debt repaid in a given financial year.

The deferred revenue ledger is useful for a business in understanding the amount of

revenue that it will receive in the future. This is useful in understanding the financial

position of the company for a given period.

The shareholder’s equity is essential in understanding the details of the equity of a

company and how much of it is financed through debt capital. It also helps in knowing

the accumulated profits available with a company.

Answer to Question 8

A) The purchases made will increase the inventory levels of the company and also increase

the amount of debt. It will increase the accounts payable of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

B) This will cause a reduction in the accounts payable and also a reduction in the inventory

levels.

C) The payments will result in the reduction in the cash levels and the accounts payable of

the company.

D) Both transactions would reduce the inventory levels. Cash sales would increase the sales

made while credit sales would improve the accounts receivable.

E) Returns would lead to an increase in the inventory levels while reducing the profits

earned by the entity.

F) This will improve the cash balances and the profits earned by the company.

B) This will cause a reduction in the accounts payable and also a reduction in the inventory

levels.

C) The payments will result in the reduction in the cash levels and the accounts payable of

the company.

D) Both transactions would reduce the inventory levels. Cash sales would increase the sales

made while credit sales would improve the accounts receivable.

E) Returns would lead to an increase in the inventory levels while reducing the profits

earned by the entity.

F) This will improve the cash balances and the profits earned by the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

References and Bibliography

Fischer, M., Marsh, T. and Brown, P.D., 2016. Going concern: Decision usefulness or harbinger

of doom?. Journal of Business and Accounting, 9(1), p.136.

Gibson, A.M., 2016. Internal Control: It's More Than a Locked Safe.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Hærem, T., Pentland, B.T. and Miller, K.D., 2015. Task complexity: Extending a core

concept. Academy of Management Review, 40(3), pp.446-460.

Ofori‐Sasu, D., Abor, J.Y. and Osei, A.K., 2017. Dividend policy and shareholders’ value:

evidence from listed companies in Ghana. African Development Review, 29(2), pp.293-304.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2019. Financial accounting. Wiley.

References and Bibliography

Fischer, M., Marsh, T. and Brown, P.D., 2016. Going concern: Decision usefulness or harbinger

of doom?. Journal of Business and Accounting, 9(1), p.136.

Gibson, A.M., 2016. Internal Control: It's More Than a Locked Safe.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Hærem, T., Pentland, B.T. and Miller, K.D., 2015. Task complexity: Extending a core

concept. Academy of Management Review, 40(3), pp.446-460.

Ofori‐Sasu, D., Abor, J.Y. and Osei, A.K., 2017. Dividend policy and shareholders’ value:

evidence from listed companies in Ghana. African Development Review, 29(2), pp.293-304.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2019. Financial accounting. Wiley.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.