University Name - Management Accounting for Cost & Control Assignment

VerifiedAdded on 2020/04/07

|15

|1670

|40

Homework Assignment

AI Summary

This document presents a detailed solution to a management accounting assignment, addressing key concepts such as process costing, variance analysis, and budgeting. The assignment explores the application of these concepts through various questions, including the analysis of cost variations, computation of equivalent units, and the evaluation of joint production costs. It also covers the importance of budgeting in relation to government policies and the impact of political factors. The document provides calculations, explanations, and answers to each question, along with references. The solution demonstrates the practical application of management accounting principles in different business scenarios. The document is a valuable resource for students seeking to understand and solve management accounting problems.

Running head: MANAGEMENT ACCOUNTING FOR COST & CONTROL

Management Accounting for Cost & Control

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting for Cost & Control

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Table of Contents

Answer to Question No 1................................................................................................................2

Requirement A:............................................................................................................................2

Requirement B:............................................................................................................................3

Answer to Question No 2................................................................................................................4

Answer to Question No 3................................................................................................................6

Requirement a:.............................................................................................................................6

Requirement b:.............................................................................................................................6

Answer to Question 4:.....................................................................................................................7

Requirement a:.............................................................................................................................7

Requirement b:.............................................................................................................................9

Answer to Question No 5..............................................................................................................11

Requirement A:..........................................................................................................................11

Requirement B:..........................................................................................................................12

Reference List................................................................................................................................14

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Table of Contents

Answer to Question No 1................................................................................................................2

Requirement A:............................................................................................................................2

Requirement B:............................................................................................................................3

Answer to Question No 2................................................................................................................4

Answer to Question No 3................................................................................................................6

Requirement a:.............................................................................................................................6

Requirement b:.............................................................................................................................6

Answer to Question 4:.....................................................................................................................7

Requirement a:.............................................................................................................................7

Requirement b:.............................................................................................................................9

Answer to Question No 5..............................................................................................................11

Requirement A:..........................................................................................................................11

Requirement B:..........................................................................................................................12

Reference List................................................................................................................................14

2

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Answer to Question No 1

Requirement A:

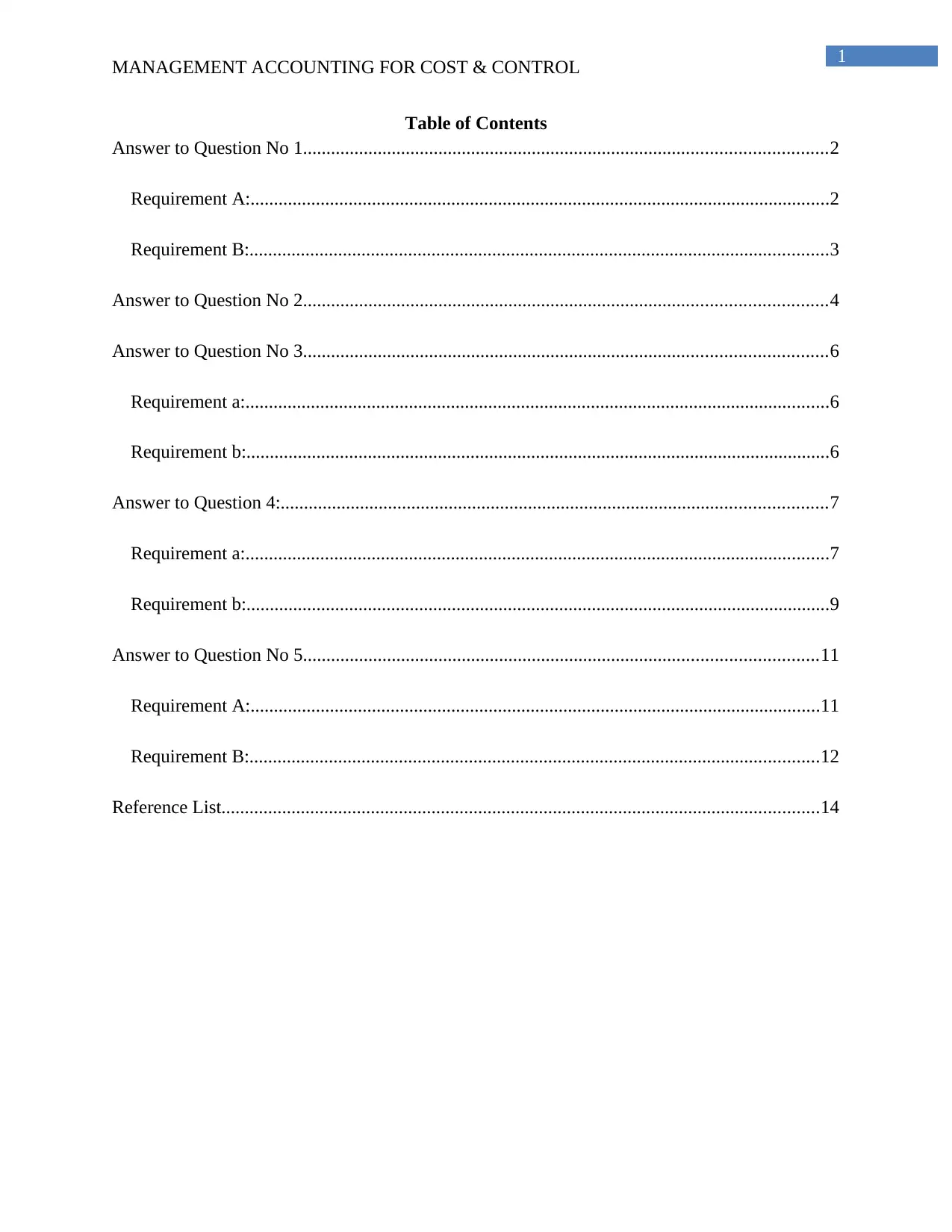

DR. CR.

Date Particulars Amount Date Particulars Amount

To, Balance b/d. 24855 31/8/14 By, Work-in-Process A/c. 6010

To, Accounts Payable A/c. 6155 By, Balance c/d 25000

31010 31010

DR. CR.

Date Particulars Amount Date Particulars Amount

1/8/X4 To, Balance b/d 8790 31/8/X4 By, Cost of Goods Sold A/c. 30000

31/8/X4 To, Work-in-Process A/c. 30110 By,Balance c/d 8900

38900 38900

DR. CR.

Date Particulars Amount Date Particulars Amount

31/8/X4 To, Finished Goods A/c. 30000 31/8/X4 By, Profit & Loss A/c. 32800

To, Manufacturing

Overhead A/c. 2800

32800 32800

Direct Material Account

Finished Goods

Cost of Goods Sold

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Answer to Question No 1

Requirement A:

DR. CR.

Date Particulars Amount Date Particulars Amount

To, Balance b/d. 24855 31/8/14 By, Work-in-Process A/c. 6010

To, Accounts Payable A/c. 6155 By, Balance c/d 25000

31010 31010

DR. CR.

Date Particulars Amount Date Particulars Amount

1/8/X4 To, Balance b/d 8790 31/8/X4 By, Cost of Goods Sold A/c. 30000

31/8/X4 To, Work-in-Process A/c. 30110 By,Balance c/d 8900

38900 38900

DR. CR.

Date Particulars Amount Date Particulars Amount

31/8/X4 To, Finished Goods A/c. 30000 31/8/X4 By, Profit & Loss A/c. 32800

To, Manufacturing

Overhead A/c. 2800

32800 32800

Direct Material Account

Finished Goods

Cost of Goods Sold

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING FOR COST & CONTROL

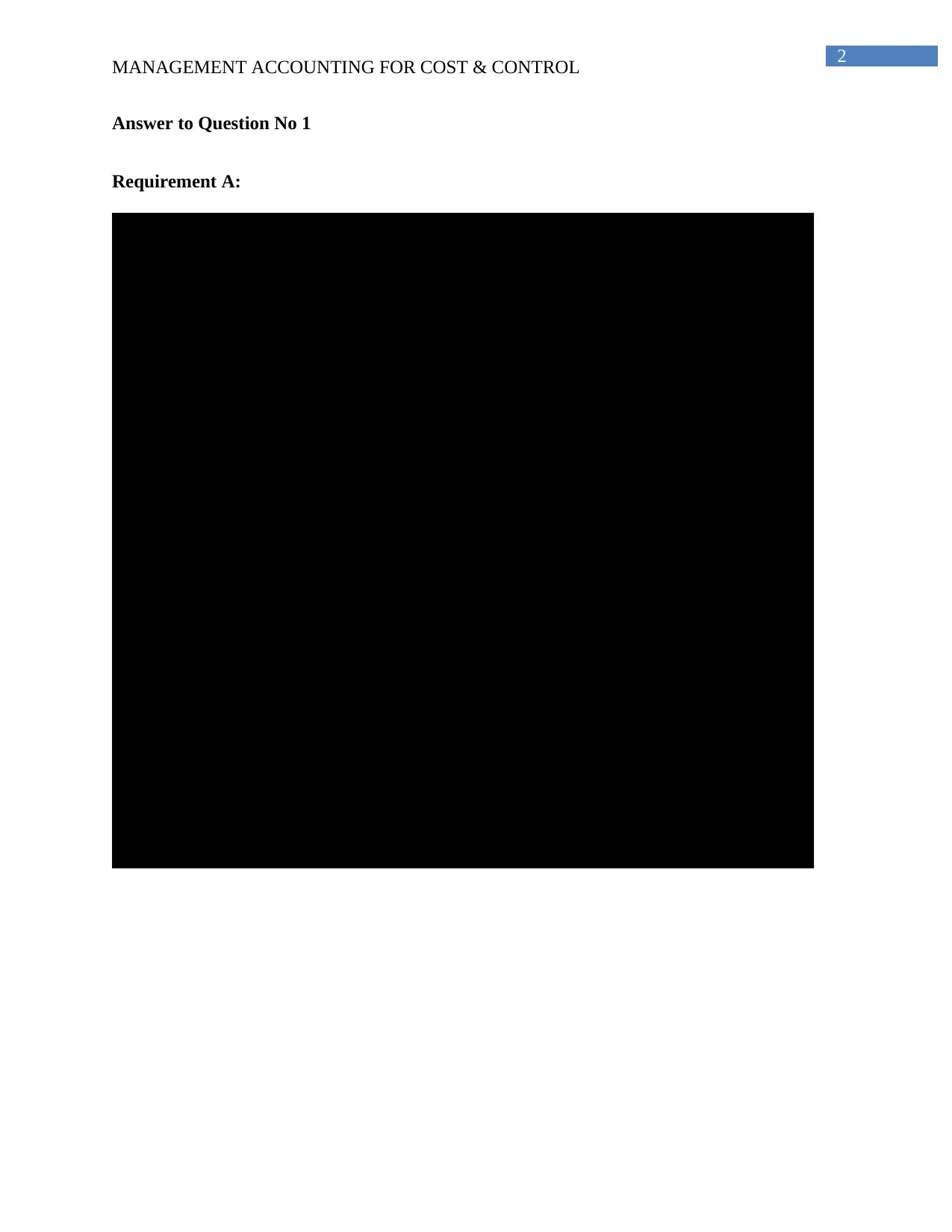

DR. CR.

Date Particulars Amount Date Particulars Amount

1/8/X4 To, Balance b/d 6700 31/8/X4 By, Finished Goods A/c. 30110

To, Direct Labor A/c. 14800 By, Balance c/d 9400

To, Manufacturing Overhead A/c. 12000

To, Direct Material A/c. 6010

39510 39510

DR. CR.

Date Particulars Amount Date Particulars Amount

31/8/X4 To, Bank A/c. 6700 1/8/X4 By, Balance b/d 2345

31/8/X4 To, Balance c/d 1800 By, Direct Material A/c. 6155

8500 8500

Work-in-Process

Accounts Payable

Requirement B:

There has been an existence of vast variation in the development of the great Pyramid of

Giza when it was constructed 4500 years ago. The development of the Giza pyramid required the

use of traditional methods that were inclusive of several stages like the execution, planning,

designing, initiation and closing. There were certain restraints with respect to the development of

the great pyramid that were inclusive of the resources, techniques and the costs (Alawattage et

al., 2017). The introduction of the innovative cost management accounting mechanism would

lead to a transformation in the difference among the mechanism utilised for the intention of

development along with the eradication of the restraints that have been explained earlier.

In this aspect, which is in association to the development of the great pyramid, the

incorporation of the process costing would be suitable. It would be supportive for the dissecting

of the cost that would aid in managing the construction cost. The cost per unit of the products has

been predicted to be the cost that is related to the cost discovered in the process costing (Otley,

MANAGEMENT ACCOUNTING FOR COST & CONTROL

DR. CR.

Date Particulars Amount Date Particulars Amount

1/8/X4 To, Balance b/d 6700 31/8/X4 By, Finished Goods A/c. 30110

To, Direct Labor A/c. 14800 By, Balance c/d 9400

To, Manufacturing Overhead A/c. 12000

To, Direct Material A/c. 6010

39510 39510

DR. CR.

Date Particulars Amount Date Particulars Amount

31/8/X4 To, Bank A/c. 6700 1/8/X4 By, Balance b/d 2345

31/8/X4 To, Balance c/d 1800 By, Direct Material A/c. 6155

8500 8500

Work-in-Process

Accounts Payable

Requirement B:

There has been an existence of vast variation in the development of the great Pyramid of

Giza when it was constructed 4500 years ago. The development of the Giza pyramid required the

use of traditional methods that were inclusive of several stages like the execution, planning,

designing, initiation and closing. There were certain restraints with respect to the development of

the great pyramid that were inclusive of the resources, techniques and the costs (Alawattage et

al., 2017). The introduction of the innovative cost management accounting mechanism would

lead to a transformation in the difference among the mechanism utilised for the intention of

development along with the eradication of the restraints that have been explained earlier.

In this aspect, which is in association to the development of the great pyramid, the

incorporation of the process costing would be suitable. It would be supportive for the dissecting

of the cost that would aid in managing the construction cost. The cost per unit of the products has

been predicted to be the cost that is related to the cost discovered in the process costing (Otley,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING FOR COST & CONTROL

2015). The processed costing depends on the standard cost, which becomes helpful when a vast

variety of products is produced. The development of the pyramid would become very tough

without describing the actual cost that is related. However, the incorporation of the process

costing would help in the assignment of the actual product cost.

Answer to Question No 2

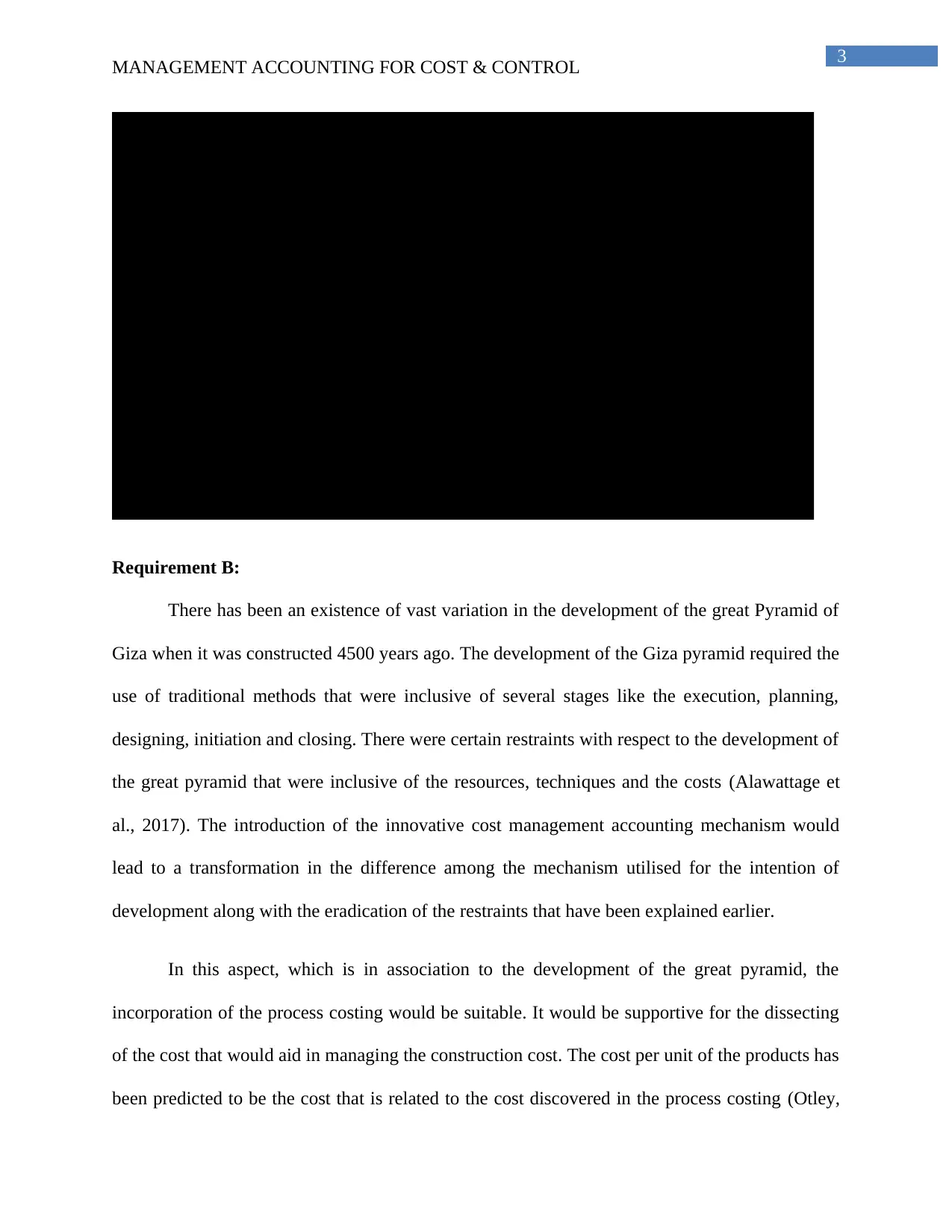

Computation of Equivalent Units:

Process 1 Physical Flow

Material Conversion

O/WIP 2000 0 1400

Started in May 6000

Total Production 8000

Completed in Process 7000 7000 7000

C/WIP 1000 1000 500

Total Equivalent Units 8000 7500

Process 2 Physical Flow

Material Conversion

O/WIP 1000 0 500

Started in May 7000

Total Production 8000

C/WIP 750 0 225

Completed I Process 7250 7250 7250

Total Equivalent Units 7250 7975

Equivalent Units

Equivalent Units

Cost per Equivalent Units:

MANAGEMENT ACCOUNTING FOR COST & CONTROL

2015). The processed costing depends on the standard cost, which becomes helpful when a vast

variety of products is produced. The development of the pyramid would become very tough

without describing the actual cost that is related. However, the incorporation of the process

costing would help in the assignment of the actual product cost.

Answer to Question No 2

Computation of Equivalent Units:

Process 1 Physical Flow

Material Conversion

O/WIP 2000 0 1400

Started in May 6000

Total Production 8000

Completed in Process 7000 7000 7000

C/WIP 1000 1000 500

Total Equivalent Units 8000 7500

Process 2 Physical Flow

Material Conversion

O/WIP 1000 0 500

Started in May 7000

Total Production 8000

C/WIP 750 0 225

Completed I Process 7250 7250 7250

Total Equivalent Units 7250 7975

Equivalent Units

Equivalent Units

Cost per Equivalent Units:

5

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Particulars Material Coversion Transferred-in Total

Process 1:

O/WIP Cost $3,000 $2,000 $5,000

Current Cost $30,000 $60,000 $90,000

Total Production Cost of Process 1 $33,000 $62,000 $95,000

Total Equivalent Units 8000 7500

Cost per Equivalent Units of Process 1 $4.13 $8.27 $12.39

Process 2:

O/WIP Cost $3,000 $4,000 $8,000 $15,000

Current Cost $35,000 $45,000 $86,742 $166,742

Total Production Cost of Process 2 $38,000 $49,000 $94,742 $181,742

Total Equivalent Units 7250 7975 7000

Cost per Equivalent Units of Process 2 $5.24 $6.14 $13.53 $25

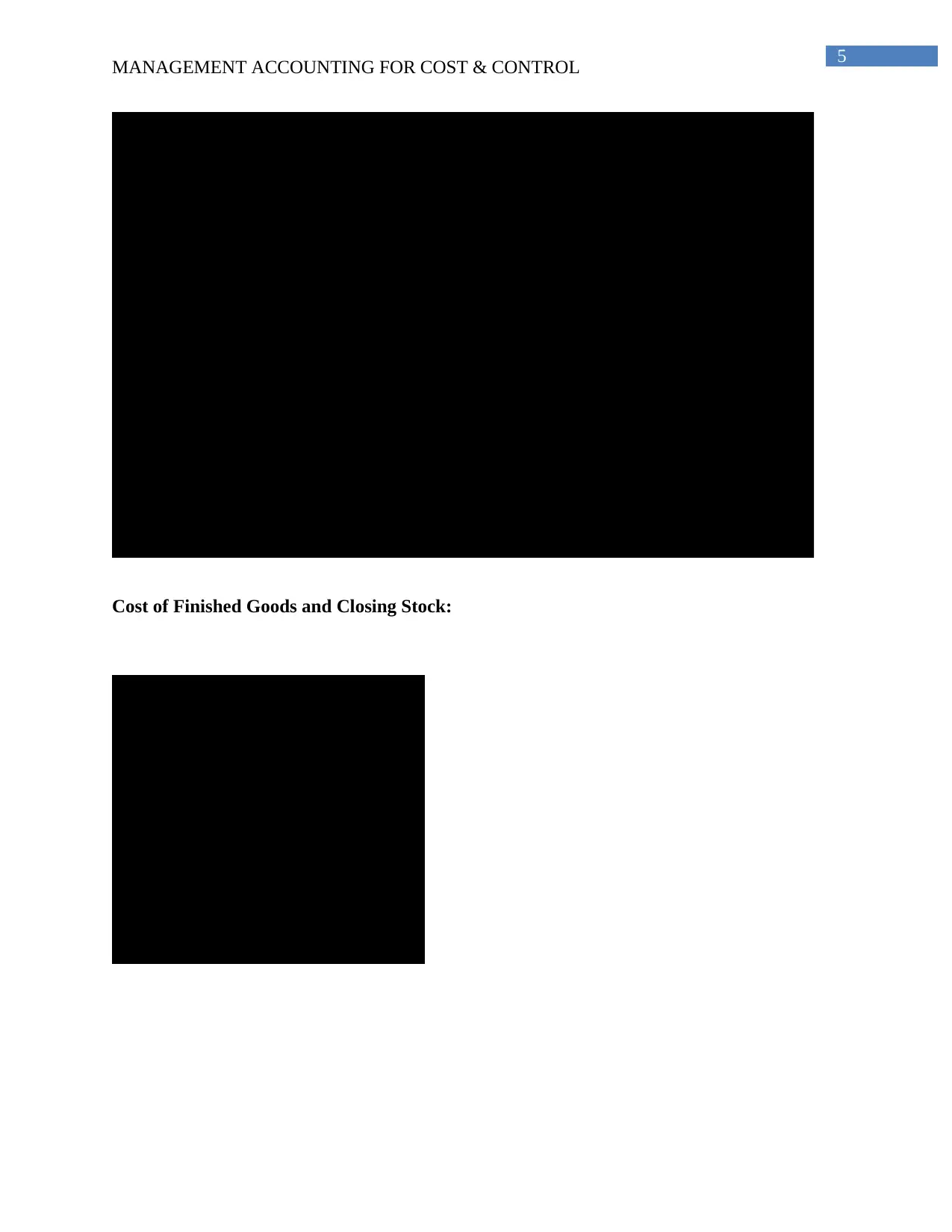

Cost of Finished Goods and Closing Stock:

Particulars Amount

Finished Goods Completed during May 7250

Cost per Equivalent Units $25

Cost of Finished Goods Completed $180,671

Closing Stock in Process 1 1000

Cost per Equivalent Units for Process 1 $12.39

Cost of Closing Stock in Process 1 $12,391.67

Closing Stock in Process 2 750

Cost per Equivalent Units for Process 1 $24.92

Cost of Closing Stock in Process 2 $18,690.08

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Particulars Material Coversion Transferred-in Total

Process 1:

O/WIP Cost $3,000 $2,000 $5,000

Current Cost $30,000 $60,000 $90,000

Total Production Cost of Process 1 $33,000 $62,000 $95,000

Total Equivalent Units 8000 7500

Cost per Equivalent Units of Process 1 $4.13 $8.27 $12.39

Process 2:

O/WIP Cost $3,000 $4,000 $8,000 $15,000

Current Cost $35,000 $45,000 $86,742 $166,742

Total Production Cost of Process 2 $38,000 $49,000 $94,742 $181,742

Total Equivalent Units 7250 7975 7000

Cost per Equivalent Units of Process 2 $5.24 $6.14 $13.53 $25

Cost of Finished Goods and Closing Stock:

Particulars Amount

Finished Goods Completed during May 7250

Cost per Equivalent Units $25

Cost of Finished Goods Completed $180,671

Closing Stock in Process 1 1000

Cost per Equivalent Units for Process 1 $12.39

Cost of Closing Stock in Process 1 $12,391.67

Closing Stock in Process 2 750

Cost per Equivalent Units for Process 1 $24.92

Cost of Closing Stock in Process 2 $18,690.08

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Answer to Question No 3

Requirement a:

Particulars Amount

Total Joint Production Cost A $250,000

Less: Joint Cost allocated to

A B $187,500

Joint Cost allocated to B C=A-B $62,500

Sales Volume of C (in kg.) D 60000

Selling Price per kg. of C E $4.50

Net Realisable Value of C F=DxE $270,000

Net Realisable Value of D

G=Fx(C/

B) $90,000

Sales Volume of D (in kg.) H 40000

Selling Price per kg. of D I=G/H $2.25

Requirement b:

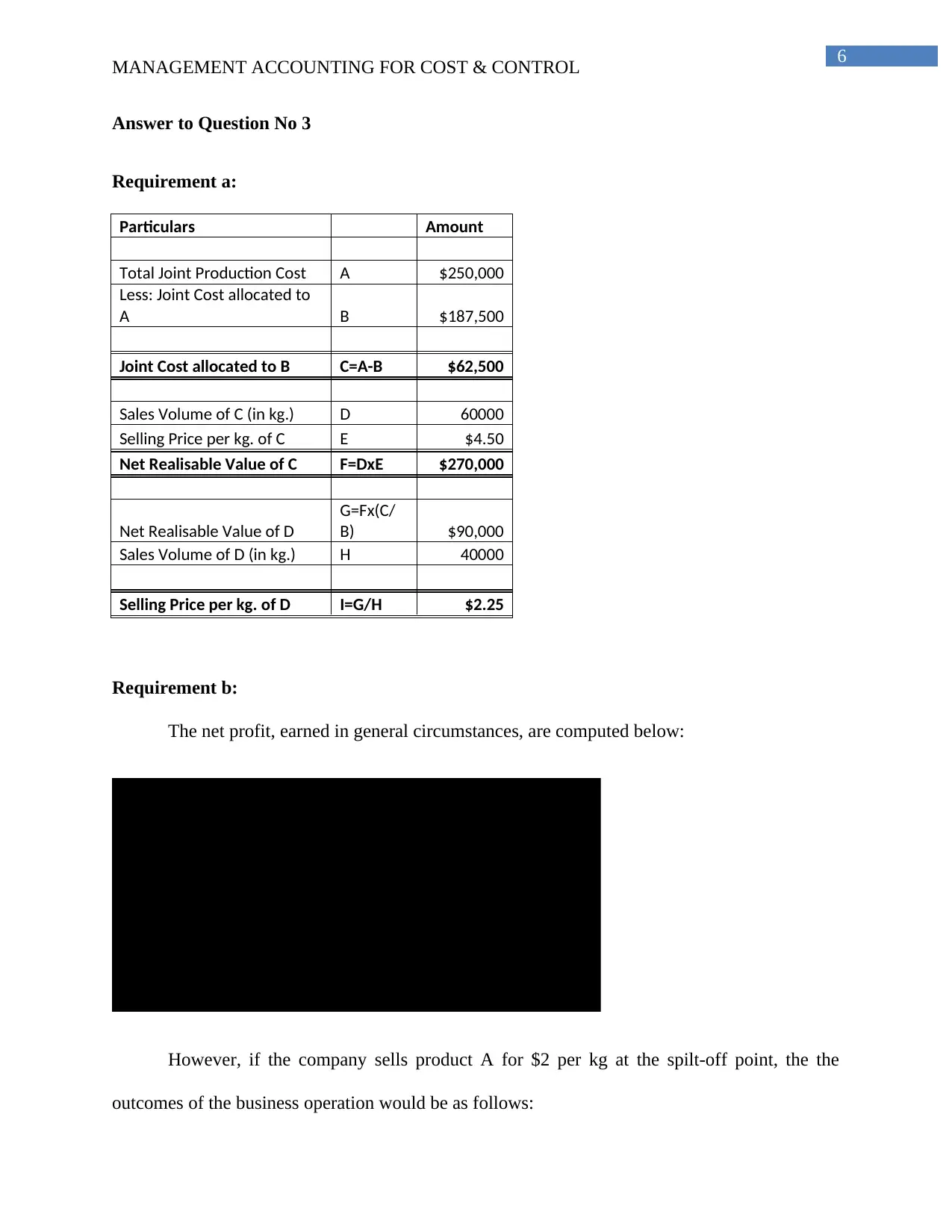

The net profit, earned in general circumstances, are computed below:

Particulars A B Total

Selling Price per unit $4.50 $2.25

Sales Volume 60000 40000 100000

Total Sale Revenue $270,000 $90,000 $360,000

Joint Cost Allocation ($187,500) ($62,500) ($250,000)

Further Processing Cost ($45,000) ($25,000) ($70,000)

Net Profit $37,500 $2,500 $40,000

However, if the company sells product A for $2 per kg at the spilt-off point, the the

outcomes of the business operation would be as follows:

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Answer to Question No 3

Requirement a:

Particulars Amount

Total Joint Production Cost A $250,000

Less: Joint Cost allocated to

A B $187,500

Joint Cost allocated to B C=A-B $62,500

Sales Volume of C (in kg.) D 60000

Selling Price per kg. of C E $4.50

Net Realisable Value of C F=DxE $270,000

Net Realisable Value of D

G=Fx(C/

B) $90,000

Sales Volume of D (in kg.) H 40000

Selling Price per kg. of D I=G/H $2.25

Requirement b:

The net profit, earned in general circumstances, are computed below:

Particulars A B Total

Selling Price per unit $4.50 $2.25

Sales Volume 60000 40000 100000

Total Sale Revenue $270,000 $90,000 $360,000

Joint Cost Allocation ($187,500) ($62,500) ($250,000)

Further Processing Cost ($45,000) ($25,000) ($70,000)

Net Profit $37,500 $2,500 $40,000

However, if the company sells product A for $2 per kg at the spilt-off point, the the

outcomes of the business operation would be as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING FOR COST & CONTROL

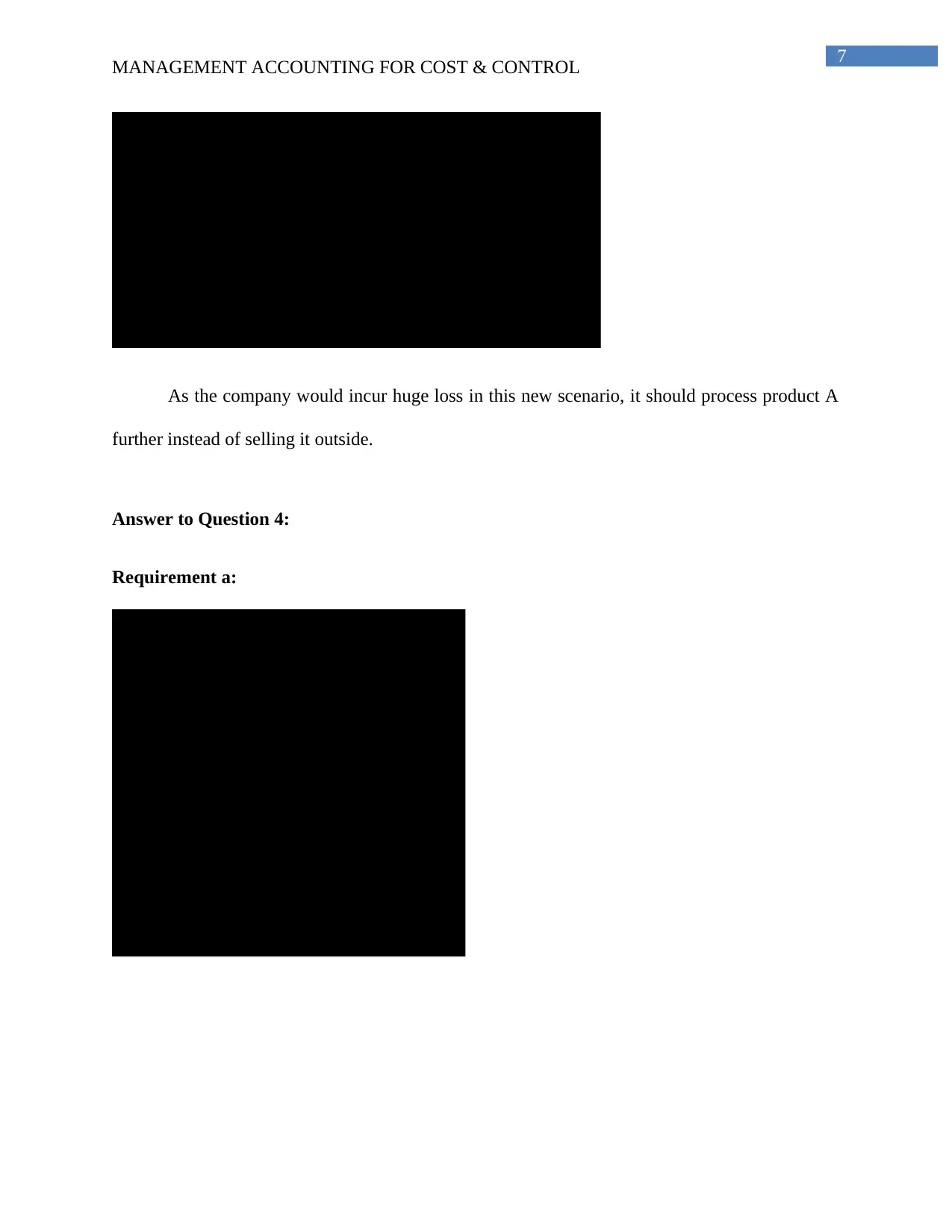

Particulars A B Total

Selling Price per unit $2.00 $2.25

Sales Volume 60000 40000 100000

Total Sale Revenue $120,000 $90,000 $210,000

Joint Cost Allocation ($142,857) ($107,143) ($250,000)

Further Processing Cost ($25,000) ($25,000)

Net Profit ($22,857) ($42,143) ($65,000)

As the company would incur huge loss in this new scenario, it should process product A

further instead of selling it outside.

Answer to Question 4:

Requirement a:

Particulars Amount

Material Purchased (in units) 220000

Standard Price per kg $6

Standard Cost for Actual Material

Purchased $1,320,000

Actual Cost of Actual Material

Purchased $1,364,000

Material Price Variance ($44,000)

Remarks Unfavorable

Material Price Variance:

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Particulars A B Total

Selling Price per unit $2.00 $2.25

Sales Volume 60000 40000 100000

Total Sale Revenue $120,000 $90,000 $210,000

Joint Cost Allocation ($142,857) ($107,143) ($250,000)

Further Processing Cost ($25,000) ($25,000)

Net Profit ($22,857) ($42,143) ($65,000)

As the company would incur huge loss in this new scenario, it should process product A

further instead of selling it outside.

Answer to Question 4:

Requirement a:

Particulars Amount

Material Purchased (in units) 220000

Standard Price per kg $6

Standard Cost for Actual Material

Purchased $1,320,000

Actual Cost of Actual Material

Purchased $1,364,000

Material Price Variance ($44,000)

Remarks Unfavorable

Material Price Variance:

8

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Particulars Amount

Units Produced 19500

Standard Usage per unit of

production 11

Standard Usage for Actual

Production 214500

Actual Material Usage 197000

Standard price per kg. $6

Material Usage Variance $105,000

Remarks Favorable

Material Usage Variance:

Particulars Amount

Actual Production 19500

Standard Labor hour per unit 2

Standard Labor Hour for Actual

Production 39000

Actual Labor Hours 40000

Standard Labor Rate per hour $20

Direct Labor Efficiency Variance ($20,000)

Total Direct Labor Variance ($1,650)

Direct Labor Rate Variace $18,350

Standard Labor Cost for Actual

Labor Hours $800,000

Actual Labor Cost $781,650

Actual Direct Labor Rate per hour $19.54

Actual Direct Labor Rate per hour:

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Particulars Amount

Units Produced 19500

Standard Usage per unit of

production 11

Standard Usage for Actual

Production 214500

Actual Material Usage 197000

Standard price per kg. $6

Material Usage Variance $105,000

Remarks Favorable

Material Usage Variance:

Particulars Amount

Actual Production 19500

Standard Labor hour per unit 2

Standard Labor Hour for Actual

Production 39000

Actual Labor Hours 40000

Standard Labor Rate per hour $20

Direct Labor Efficiency Variance ($20,000)

Total Direct Labor Variance ($1,650)

Direct Labor Rate Variace $18,350

Standard Labor Cost for Actual

Labor Hours $800,000

Actual Labor Cost $781,650

Actual Direct Labor Rate per hour $19.54

Actual Direct Labor Rate per hour:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING FOR COST & CONTROL

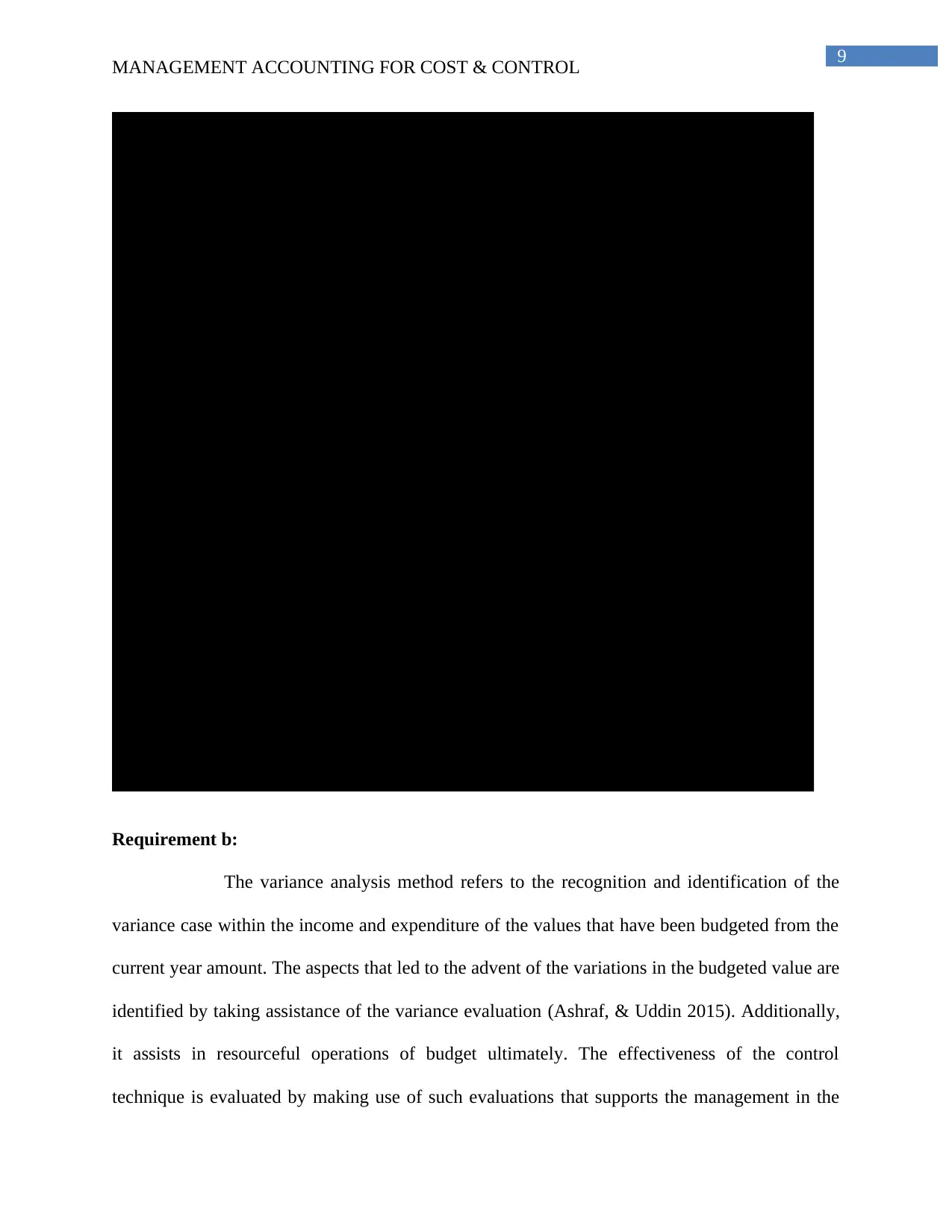

Dr. Cr.

Date Amount Amount

Direct Material A/c. Dr. $1,364,000

To, Accounts Payable A/c. $1,364,000

Work-in-Progress A/c. Dr. 1287000

To, Direct Material A/c. 1287000

Material Price Variance A/c. Dr. $44,000

To, Direct Material A/c. $44,000

Direct Material A/c. Dr. $105,000

To, Material Usage Variance A/c. $105,000

Direct Labor Cost A/c. Dr. $781,650

To, Accrued Payroll A/c. $781,650

Work-in-Progress A/c. Dr. 780000

To, Direct Labor Cost A/c. 780000

Direct Labor Cost A/c. Dr. $18,350

To, Direct Labor Rate Variance A/c. $18,350

Direct Labor Efficiency Variance A/c. Dr. $20,000

To, Direct Labor Cost A/c. $20,000

Material Usage Variance A/c. Dr. $105,000

Direct Labor Rate Variance A/c. Dr. $18,350

To, Cost of Goods Sold A/c. $59,350

To, Direct Labor Efficiency Variance A/c. $20,000

To, Material Price Variance A/c. $44,000

Particulars

Requirement b:

The variance analysis method refers to the recognition and identification of the

variance case within the income and expenditure of the values that have been budgeted from the

current year amount. The aspects that led to the advent of the variations in the budgeted value are

identified by taking assistance of the variance evaluation (Ashraf, & Uddin 2015). Additionally,

it assists in resourceful operations of budget ultimately. The effectiveness of the control

technique is evaluated by making use of such evaluations that supports the management in the

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Dr. Cr.

Date Amount Amount

Direct Material A/c. Dr. $1,364,000

To, Accounts Payable A/c. $1,364,000

Work-in-Progress A/c. Dr. 1287000

To, Direct Material A/c. 1287000

Material Price Variance A/c. Dr. $44,000

To, Direct Material A/c. $44,000

Direct Material A/c. Dr. $105,000

To, Material Usage Variance A/c. $105,000

Direct Labor Cost A/c. Dr. $781,650

To, Accrued Payroll A/c. $781,650

Work-in-Progress A/c. Dr. 780000

To, Direct Labor Cost A/c. 780000

Direct Labor Cost A/c. Dr. $18,350

To, Direct Labor Rate Variance A/c. $18,350

Direct Labor Efficiency Variance A/c. Dr. $20,000

To, Direct Labor Cost A/c. $20,000

Material Usage Variance A/c. Dr. $105,000

Direct Labor Rate Variance A/c. Dr. $18,350

To, Cost of Goods Sold A/c. $59,350

To, Direct Labor Efficiency Variance A/c. $20,000

To, Material Price Variance A/c. $44,000

Particulars

Requirement b:

The variance analysis method refers to the recognition and identification of the

variance case within the income and expenditure of the values that have been budgeted from the

current year amount. The aspects that led to the advent of the variations in the budgeted value are

identified by taking assistance of the variance evaluation (Ashraf, & Uddin 2015). Additionally,

it assists in resourceful operations of budget ultimately. The effectiveness of the control

technique is evaluated by making use of such evaluations that supports the management in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING FOR COST & CONTROL

development of certain proposals that would be helpful in restraining these discrepancies. It even

assists during the allotment of the accountabilities, which occupies the department with the help

of the controlling mechanisms.

The analysis of the variance is considered as a key tool in the management of business

and is significant in the process of management accounting. This helps in the scrutinising of the

factors for the digression between the actual and the predicted values that helps in developing the

efficiency and in that way helps in maintaining the authority over the expenses of the venture by

effectual monitoring of the actual and the premeditated expenses (Mohd-Jamal, & Tayles 2014).

The several problems, trends and opportunities in regards to the long-term and the short-term

achievements for any kind of projects of the firm that are disclosed by taking assistance of the

assessment of the variance. It assists in explaining the variances of the revenue and the cost.

The quantitative inspection has been a key factor in numerous other areas, which includes

the examination of the organizational behaviour, performance of the company and the human

resource department. This assists in providing a free communication with respect to the

anticipations of the feedback and the performance of the several other departments. The financial

result of the firm is directly connected with the human resource performance and the evaluation

of the variance assists in establishing a relationship among the transformations in various

departments. The incorporation of the variance assessment helps in examining the answers of the

employees with respect to numerous components that would that will be helpful in gaining the

feedback (Abdelmoneim Mohamed, & Jones 2014). The managers are certain levels performing

in numerous departments exploit the variance assessment that assists then in implementing the

effective equipments and tools for taking care of the costs. They try to achieve the utmost degree

of advantages from the variance of using of the materials.

MANAGEMENT ACCOUNTING FOR COST & CONTROL

development of certain proposals that would be helpful in restraining these discrepancies. It even

assists during the allotment of the accountabilities, which occupies the department with the help

of the controlling mechanisms.

The analysis of the variance is considered as a key tool in the management of business

and is significant in the process of management accounting. This helps in the scrutinising of the

factors for the digression between the actual and the predicted values that helps in developing the

efficiency and in that way helps in maintaining the authority over the expenses of the venture by

effectual monitoring of the actual and the premeditated expenses (Mohd-Jamal, & Tayles 2014).

The several problems, trends and opportunities in regards to the long-term and the short-term

achievements for any kind of projects of the firm that are disclosed by taking assistance of the

assessment of the variance. It assists in explaining the variances of the revenue and the cost.

The quantitative inspection has been a key factor in numerous other areas, which includes

the examination of the organizational behaviour, performance of the company and the human

resource department. This assists in providing a free communication with respect to the

anticipations of the feedback and the performance of the several other departments. The financial

result of the firm is directly connected with the human resource performance and the evaluation

of the variance assists in establishing a relationship among the transformations in various

departments. The incorporation of the variance assessment helps in examining the answers of the

employees with respect to numerous components that would that will be helpful in gaining the

feedback (Abdelmoneim Mohamed, & Jones 2014). The managers are certain levels performing

in numerous departments exploit the variance assessment that assists then in implementing the

effective equipments and tools for taking care of the costs. They try to achieve the utmost degree

of advantages from the variance of using of the materials.

11

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Answer to Question No 5

Requirement A:

Particulars 20X2 20X3 20X4 20X5 20X6

Sales Volume 32400 34992 37791 40000 40000

Selling Price per unit $6.63 $6.97 $7.38 $8.13 $8.78

Total Sales Revenue $214,812 $243,824 $279,051 $325,080 $351,000

Cost of Goods Sold ($164,520) ($186,192) ($212,841) ($238,760) ($257,120)

Gross Profit $50,292 $57,632 $66,210 $86,320 $93,880

General & Administrative

Expenses ($30,074) ($34,135) ($39,067) ($45,511) ($49,140)

Net Profit before Tax $20,218 $23,496 $27,143 $40,809 $44,740

Less: Income Tax @40% ($8,087) ($9,399) ($10,857) ($16,324) ($17,896)

Net Profit after Tax $12,131 $14,098 $16,286 $24,485 $26,844

Particulars 20X2 20X3 20X4 20X5 20X6

Opening Balance of Retained

Earnings $3,500 $3,780 $4,082 $4,409 $4,762

Net Profit for the period $12,131 $14,098 $16,286 $24,485 $26,844

$15,631 $17,878 $20,368 $28,894 $31,606

Less: Dividends Payable ($7,885) ($9,164) ($10,586) ($15,915) ($17,449)

Closing Balance of Retained

Earnings $3,780 $8,714 $9,782 $12,979 $14,157

Budgeted Income Statement:

Budgeted Statement of Retained Earnings:

Workings:

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Answer to Question No 5

Requirement A:

Particulars 20X2 20X3 20X4 20X5 20X6

Sales Volume 32400 34992 37791 40000 40000

Selling Price per unit $6.63 $6.97 $7.38 $8.13 $8.78

Total Sales Revenue $214,812 $243,824 $279,051 $325,080 $351,000

Cost of Goods Sold ($164,520) ($186,192) ($212,841) ($238,760) ($257,120)

Gross Profit $50,292 $57,632 $66,210 $86,320 $93,880

General & Administrative

Expenses ($30,074) ($34,135) ($39,067) ($45,511) ($49,140)

Net Profit before Tax $20,218 $23,496 $27,143 $40,809 $44,740

Less: Income Tax @40% ($8,087) ($9,399) ($10,857) ($16,324) ($17,896)

Net Profit after Tax $12,131 $14,098 $16,286 $24,485 $26,844

Particulars 20X2 20X3 20X4 20X5 20X6

Opening Balance of Retained

Earnings $3,500 $3,780 $4,082 $4,409 $4,762

Net Profit for the period $12,131 $14,098 $16,286 $24,485 $26,844

$15,631 $17,878 $20,368 $28,894 $31,606

Less: Dividends Payable ($7,885) ($9,164) ($10,586) ($15,915) ($17,449)

Closing Balance of Retained

Earnings $3,780 $8,714 $9,782 $12,979 $14,157

Budgeted Income Statement:

Budgeted Statement of Retained Earnings:

Workings:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.