Detailed Analysis: Management Accounting Assignment Solution

VerifiedAdded on 2020/02/19

|15

|1606

|44

Homework Assignment

AI Summary

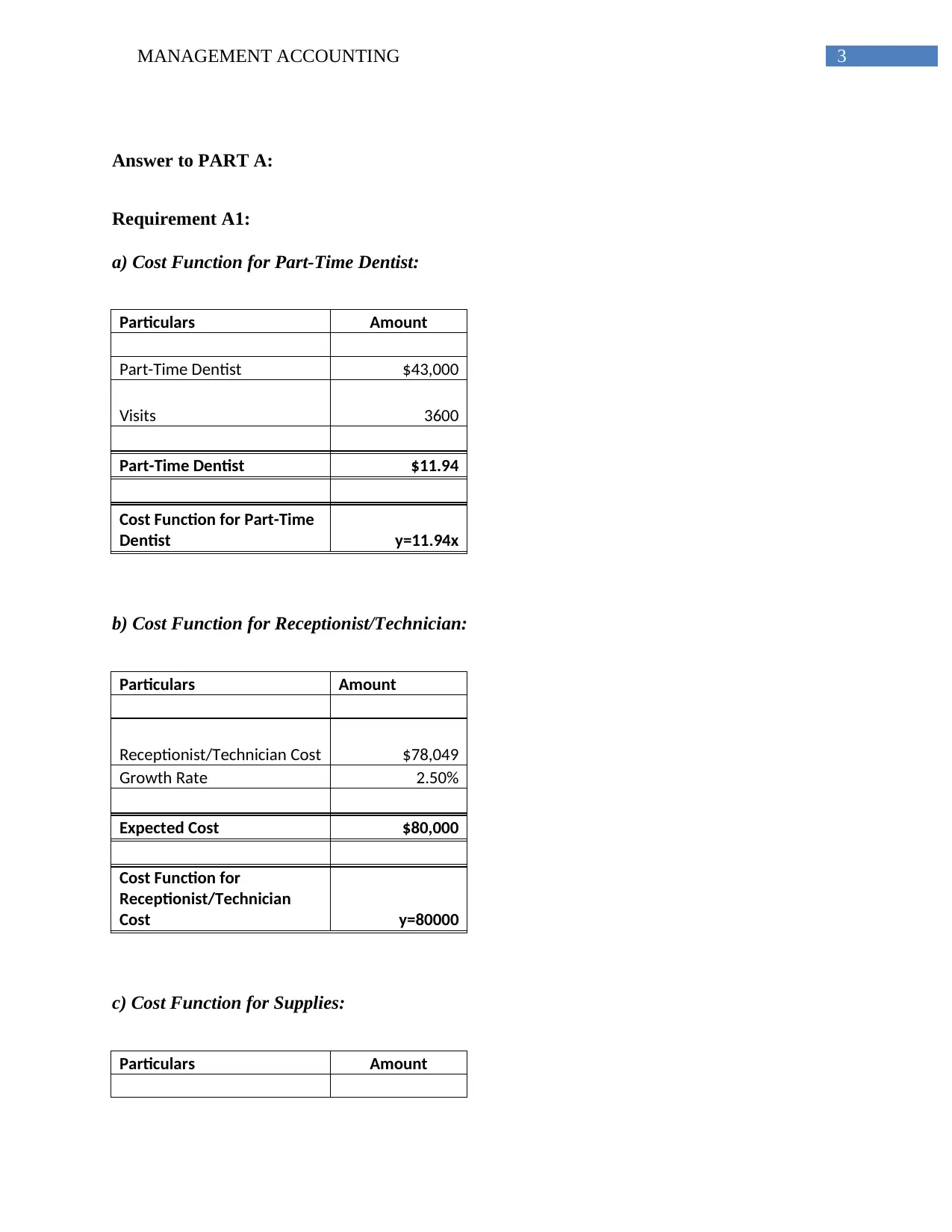

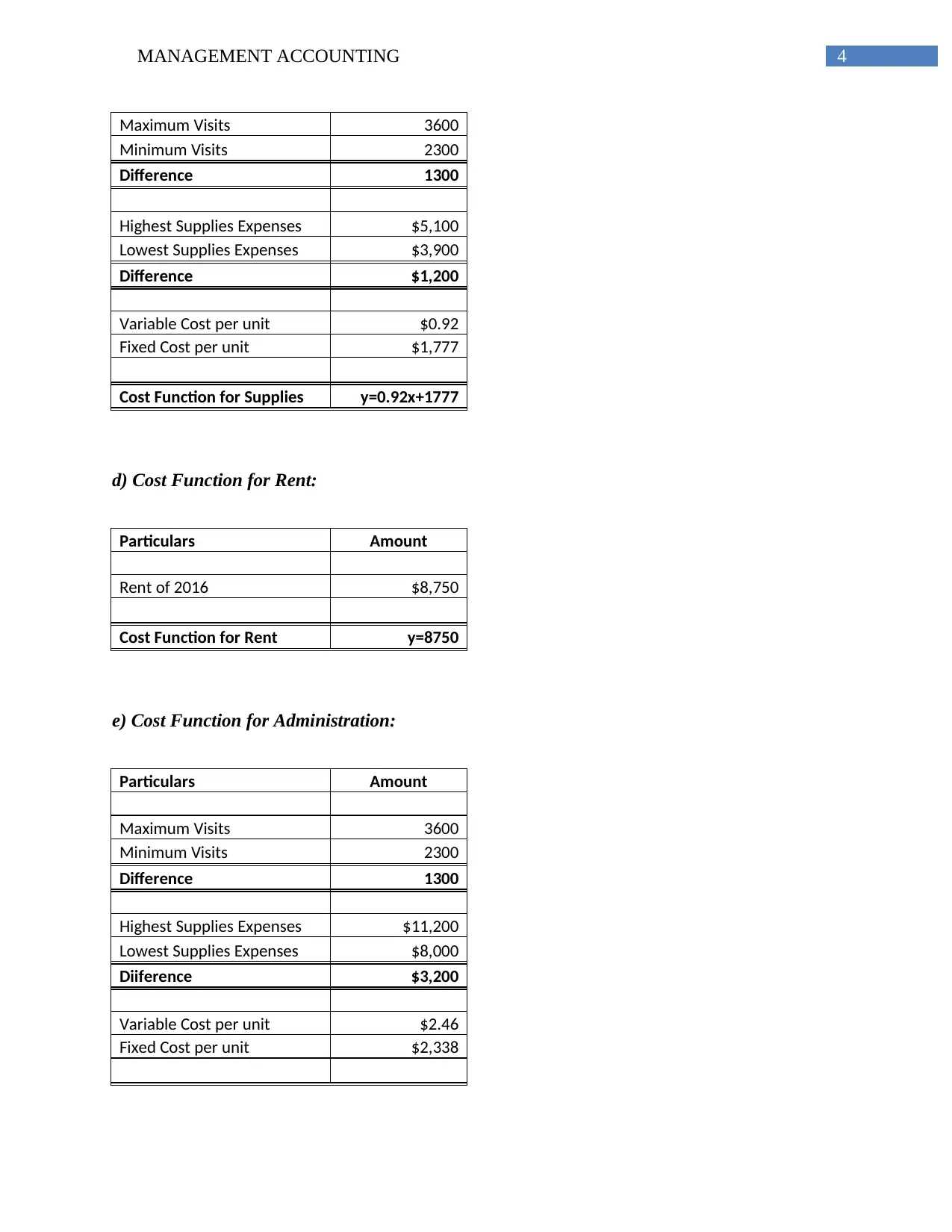

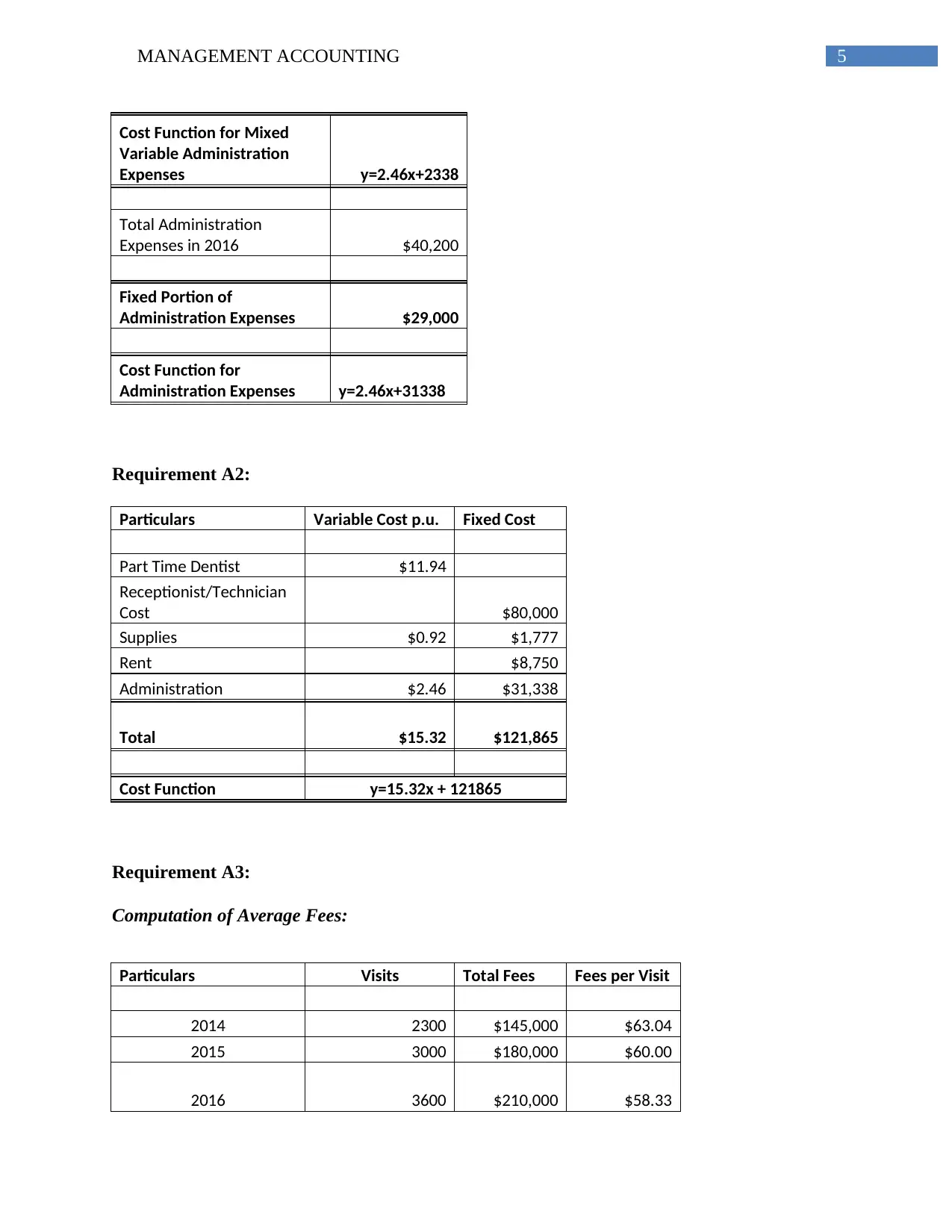

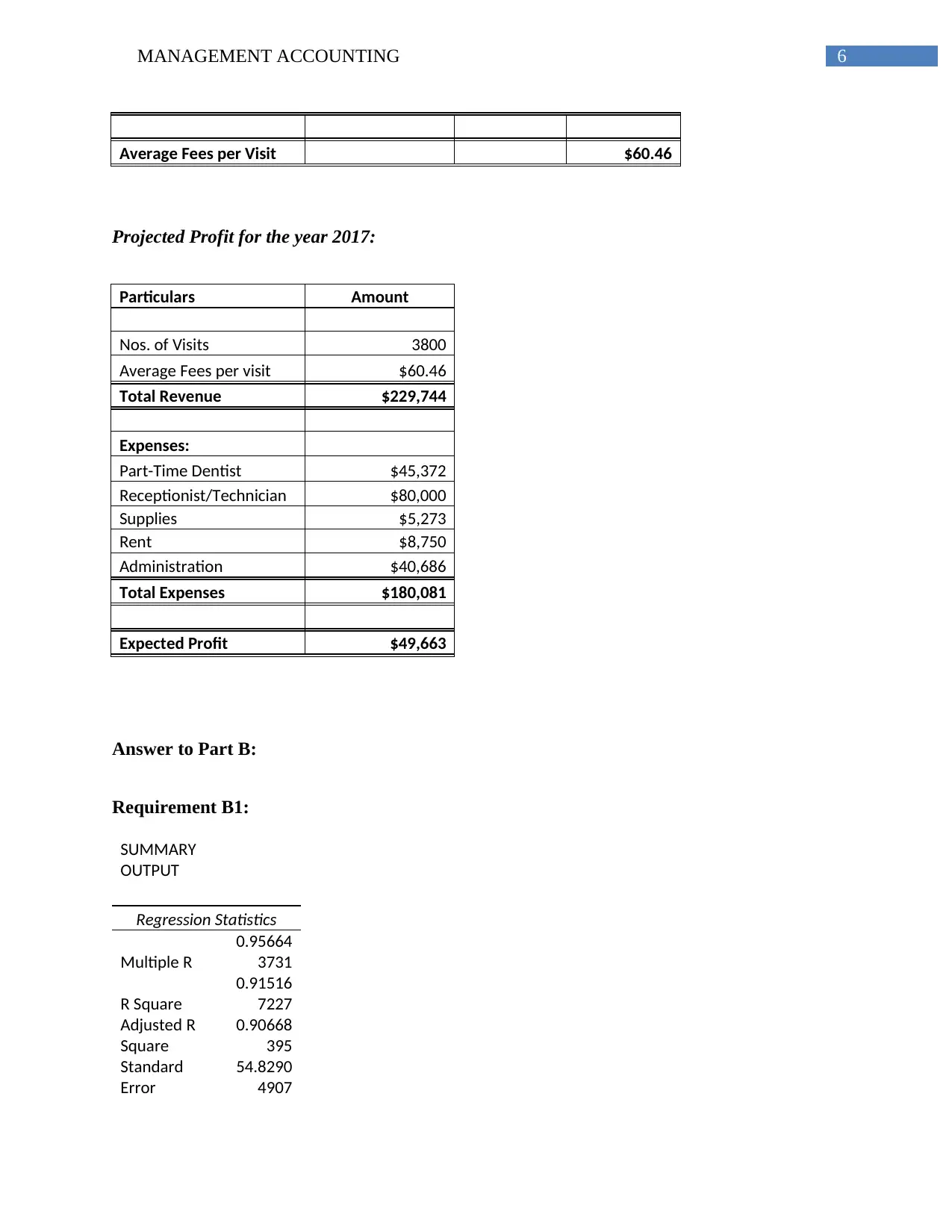

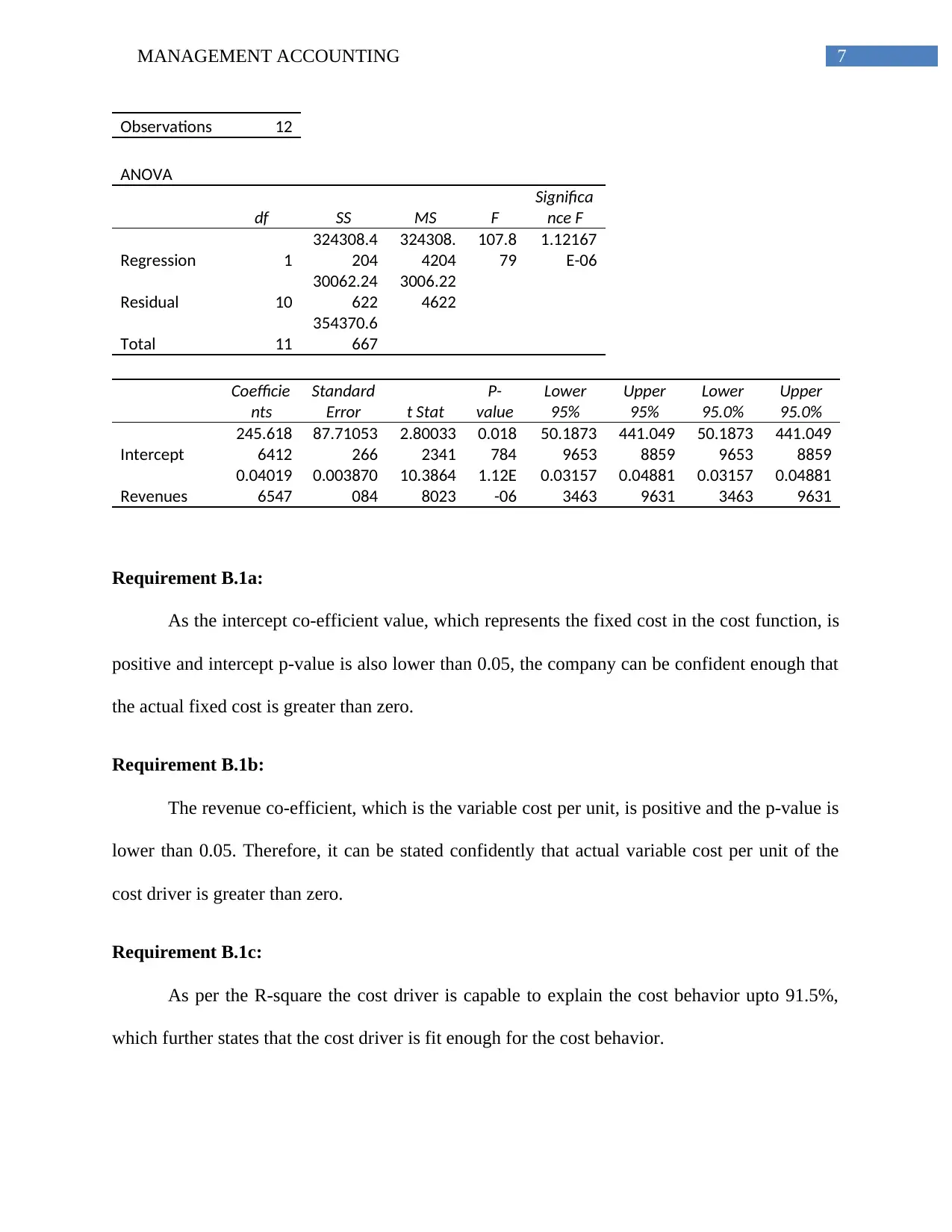

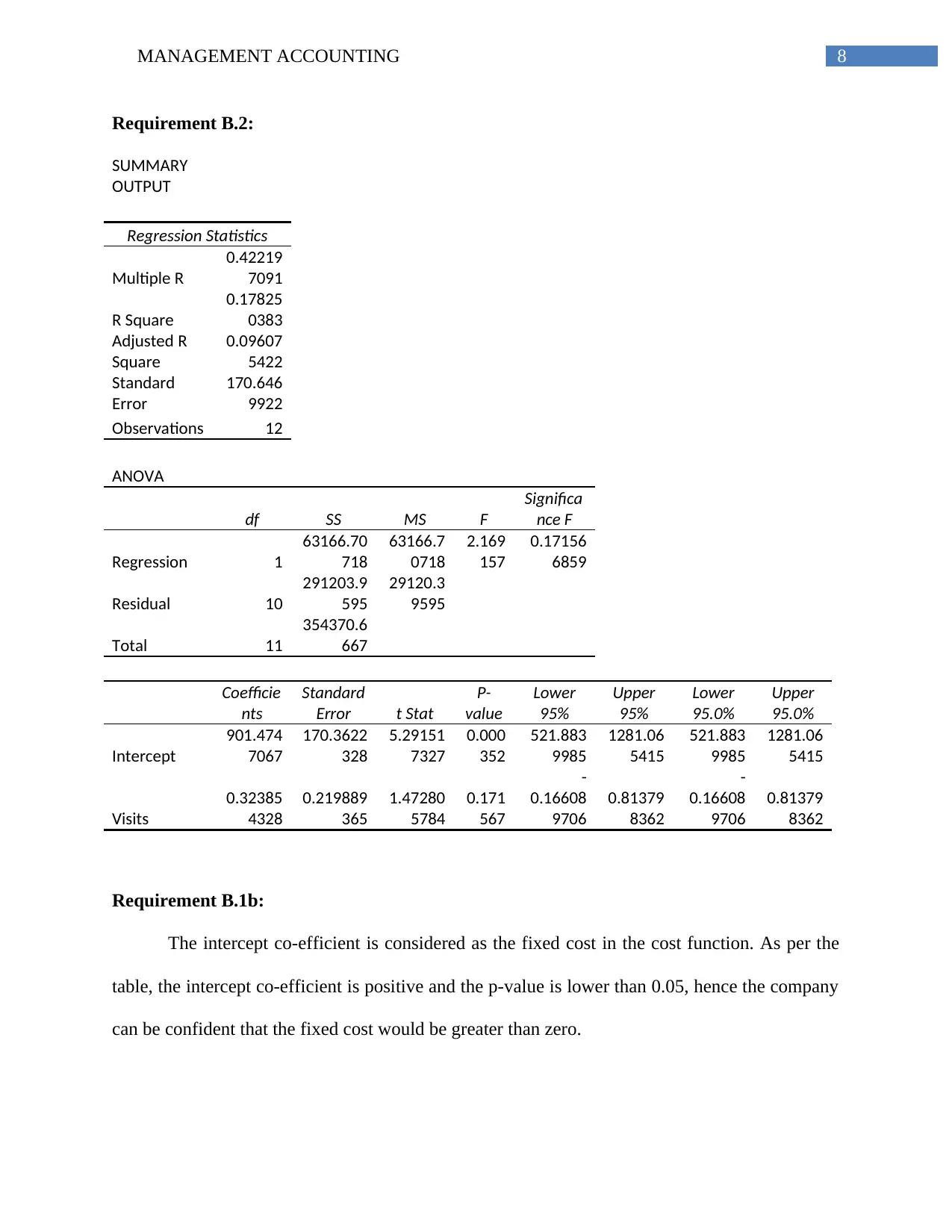

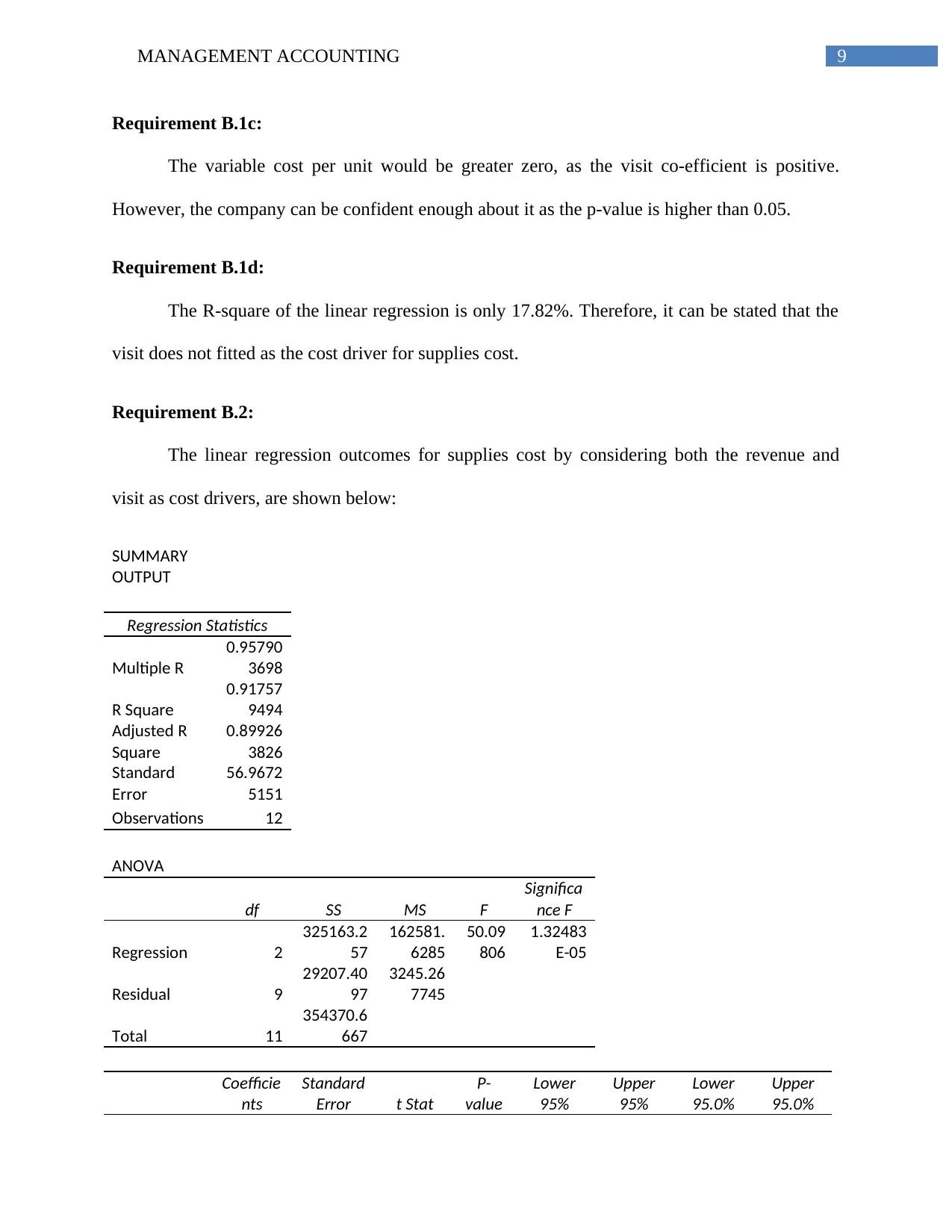

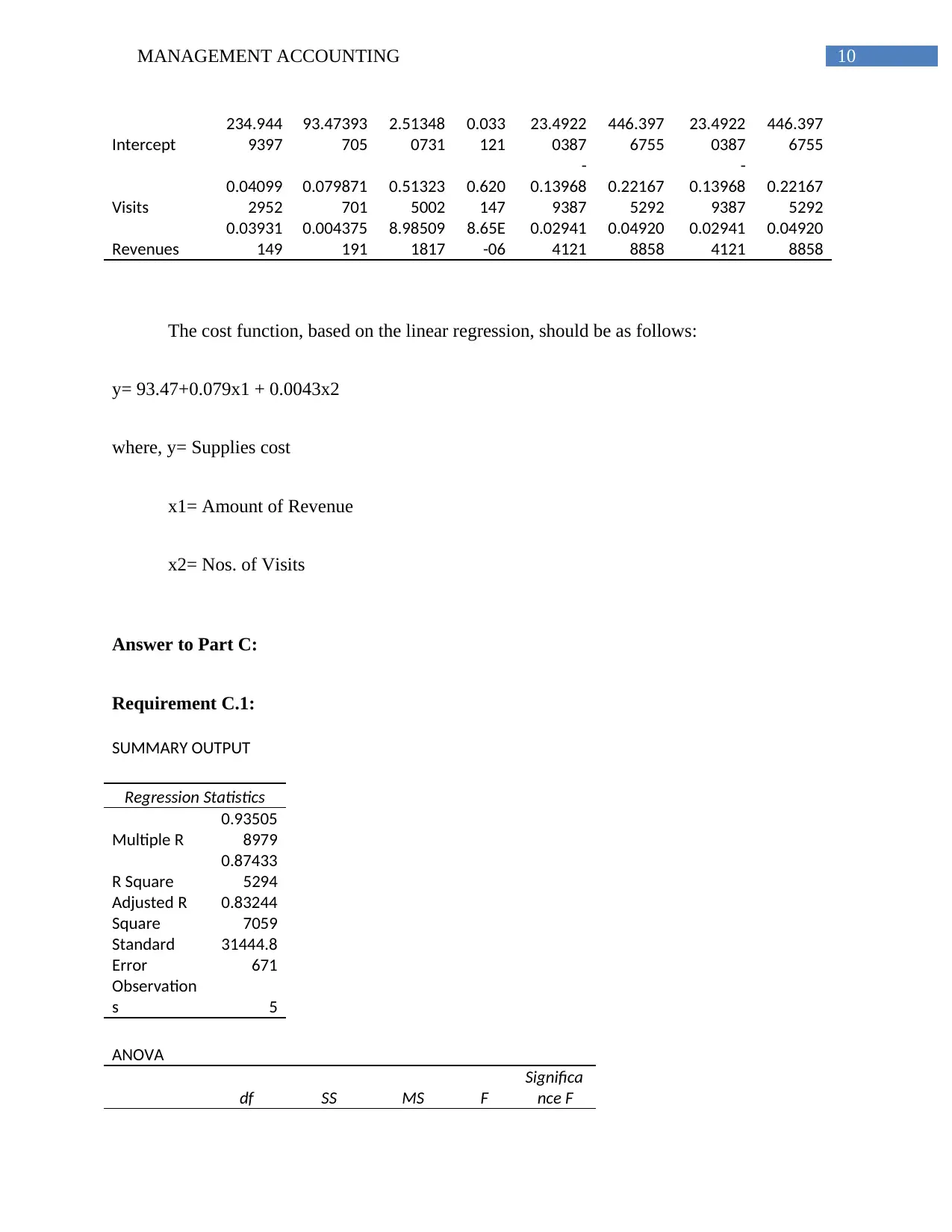

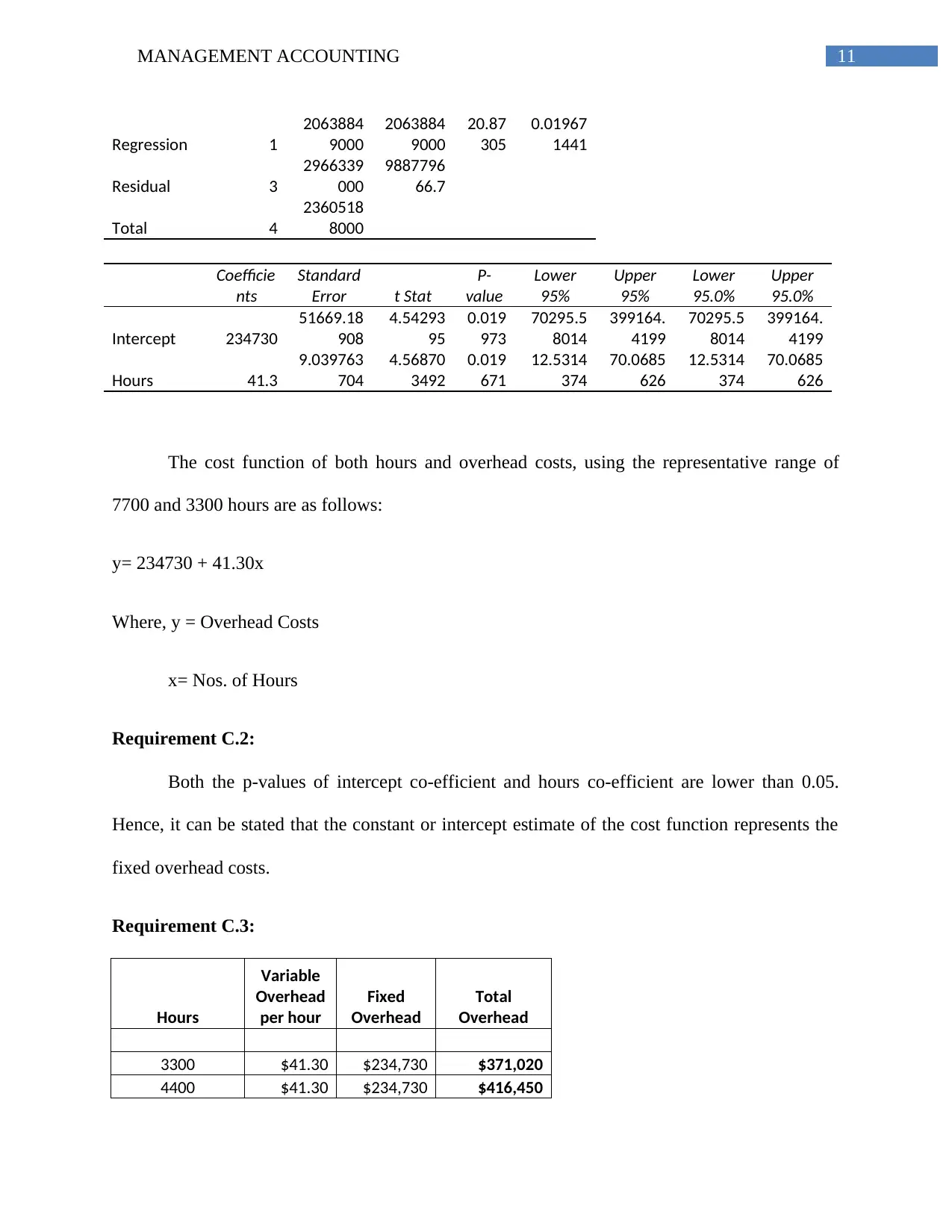

This document presents a comprehensive solution to a management accounting assignment, covering various aspects of financial analysis. The solution begins with Part A, which focuses on cost function analysis for different cost components like part-time dentists, receptionists/technicians, supplies, rent, and administration. Part B delves into regression analysis, examining the relationship between revenue and cost drivers, and assessing the goodness of fit using R-squared values. Part C addresses overhead cost analysis, developing a cost function based on hours and calculating predicted overhead costs. Finally, Part D introduces probability concepts using tree diagrams and the counting principle to determine meal preferences. The assignment utilizes various statistical techniques and financial modeling to provide a detailed understanding of accounting principles and their applications.

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.