Financial Analysis: Management Accounting Report for ABC Hotel

VerifiedAdded on 2019/12/28

|13

|2466

|195

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices applied to ABC Hotel. It begins with an introduction to management accounting and its importance in business decision-making. The report then delves into the need for budgeting, outlining its benefits like limiting expenditures and planning for future growth, along with the budgeting process. It includes a cash budget, budgeted income statement, and a budgeted statement of financial position for the hotel. Furthermore, the report explores investment appraisal techniques, specifically net present value (NPV), payback period, and discounted payback period, to assess the feasibility of potential investment projects. The analysis demonstrates how these techniques can be used to evaluate the profitability and financial health of ABC Hotel, ultimately aiding in informed decision-making regarding future investments and financial planning. The report concludes by emphasizing the significance of these financial tools in enhancing the business's strategic direction and profitability.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................4

(a) Cash budget............................................................................................................................4

(b) Budgeted income statement...................................................................................................6

(c) Budgeted statement of financial position...............................................................................6

TASK 3............................................................................................................................................7

CONCLUSION..............................................................................................................................10

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................4

(a) Cash budget............................................................................................................................4

(b) Budgeted income statement...................................................................................................6

(c) Budgeted statement of financial position...............................................................................6

TASK 3............................................................................................................................................7

CONCLUSION..............................................................................................................................10

2

INTRODUCTION

Management accounting is referred to as the process of preparing management reports as

well as accounts that offer accurate and timely information relating with finances and statistics

(Gill and Biger, 2013). This is required by the business to make day to day as well as short term

decisions. In the present study, management accounting has been discussed in context of ABC

hotel. The report involves the need for budgeting. Further, it includes preparation of documents.

In addition to this, the present study also involves techniques of investment appraisal so that

determination can be made regarding selection of the most suitable investment project.

TASK 1

Carrying out business operations requires the owners to plan and review their finances.

There is greater need for budgeting within the organization that has been enumerated below: Facts: This is related with representing detailed analysis of the ways in which business is

expected to spend money in future time span (Grier, 2007). Several organizations develop

budget annually so that expected needs of every department can be outlined within the

firm. Limit expenditures: A major advantage of using business budget relates with the ability to

limit the amount that needs to be spent on certain operations (Nikbakht and et.al, 2006).

The role of budget is effective in determining the expenses in order to ensure that capital

is not wasted on items that are not essential. Plan for future growth: The need for budgeting can be greatly viewed towards planning

for the future growth of business and expansion (Hansen and Otley, 2003). Budgeting

regarding future growth opportunities makes sure that firms possess capital on hand when

quick decisions are required to be made in relation to the expansion of business

operations.

Process of preparing budget

There is a certain process followed in preparation of budget. This includes the following: Obtaining estimates: It includes obtaining of the sales, production levels, expected costs

as well as availability of the resources for every sub division. The discussion regarding

3

Management accounting is referred to as the process of preparing management reports as

well as accounts that offer accurate and timely information relating with finances and statistics

(Gill and Biger, 2013). This is required by the business to make day to day as well as short term

decisions. In the present study, management accounting has been discussed in context of ABC

hotel. The report involves the need for budgeting. Further, it includes preparation of documents.

In addition to this, the present study also involves techniques of investment appraisal so that

determination can be made regarding selection of the most suitable investment project.

TASK 1

Carrying out business operations requires the owners to plan and review their finances.

There is greater need for budgeting within the organization that has been enumerated below: Facts: This is related with representing detailed analysis of the ways in which business is

expected to spend money in future time span (Grier, 2007). Several organizations develop

budget annually so that expected needs of every department can be outlined within the

firm. Limit expenditures: A major advantage of using business budget relates with the ability to

limit the amount that needs to be spent on certain operations (Nikbakht and et.al, 2006).

The role of budget is effective in determining the expenses in order to ensure that capital

is not wasted on items that are not essential. Plan for future growth: The need for budgeting can be greatly viewed towards planning

for the future growth of business and expansion (Hansen and Otley, 2003). Budgeting

regarding future growth opportunities makes sure that firms possess capital on hand when

quick decisions are required to be made in relation to the expansion of business

operations.

Process of preparing budget

There is a certain process followed in preparation of budget. This includes the following: Obtaining estimates: It includes obtaining of the sales, production levels, expected costs

as well as availability of the resources for every sub division. The discussion regarding

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this can be informal or written reports of plan that is submitted to the budget committee

for approval. Coordinating estimates: Another step relates with the evaluation of different plans

submitted by several organizational units in order to determine the potential plan in the

entire interest of the business. Communicating budget: Communication of the budget to the responsible managers and

concerned departments is another step (Harris and Mongiello, 2012). After that, budget

plan is being approved in the light of organizational goals and availability of resources. It

is being communicated to the departments and responsible managers. Implementing the budget plan: The final budget is being presented to the manager and is

adopted as a plan of operation for coming budget period. Reporting interim progress towards budgeted objectives: In accordance with the

feedback in budgeting process, performance reports are being prepared by firm so that

departmental managers can be informed regarding the performances achieved in relation

with budgeted figures (Milisn, 2009).

Limitations

Inaccuracy: The process of budgeting is based upon lots of assumptions that are related

with the estimation of expenses and revenues. They are on the basis of trends and

scenario of market that exist while making budget (Nobanee, Abdullatif and AlHajjar,

2011). Further, they are based upon predictions made for the coming year by taking into

account data available at the time of budgeting.

TASK 2

(a) Cash budget

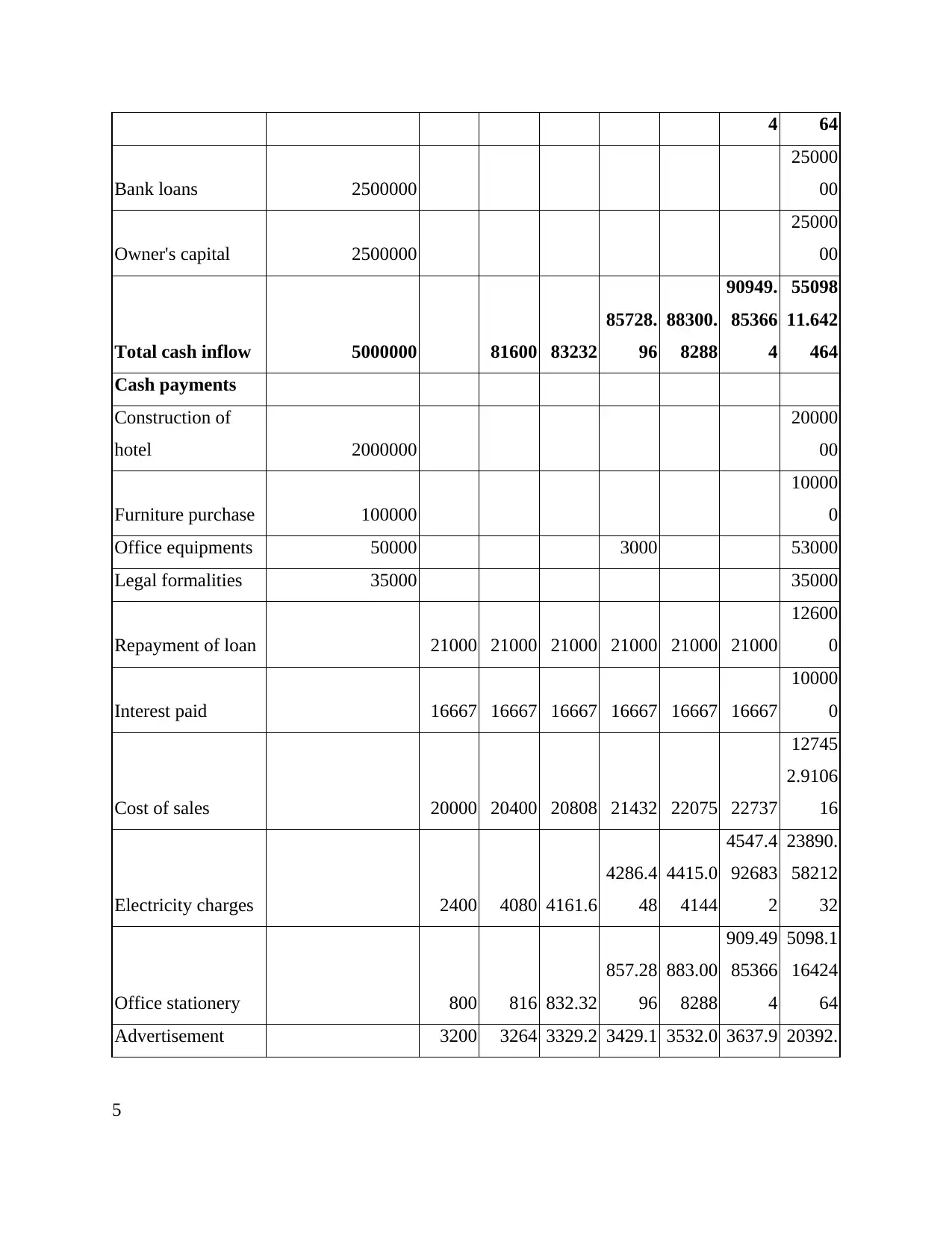

Cash Budget for the period of 6 months

Particulars

Pre-operating

year

Janua

ry

Febru

ary March April May June Total

Cash revenues

Cash sales 80000 81600 83232 85728.

96

88300.

8288

90949.

85366

50981

1.6424

4

for approval. Coordinating estimates: Another step relates with the evaluation of different plans

submitted by several organizational units in order to determine the potential plan in the

entire interest of the business. Communicating budget: Communication of the budget to the responsible managers and

concerned departments is another step (Harris and Mongiello, 2012). After that, budget

plan is being approved in the light of organizational goals and availability of resources. It

is being communicated to the departments and responsible managers. Implementing the budget plan: The final budget is being presented to the manager and is

adopted as a plan of operation for coming budget period. Reporting interim progress towards budgeted objectives: In accordance with the

feedback in budgeting process, performance reports are being prepared by firm so that

departmental managers can be informed regarding the performances achieved in relation

with budgeted figures (Milisn, 2009).

Limitations

Inaccuracy: The process of budgeting is based upon lots of assumptions that are related

with the estimation of expenses and revenues. They are on the basis of trends and

scenario of market that exist while making budget (Nobanee, Abdullatif and AlHajjar,

2011). Further, they are based upon predictions made for the coming year by taking into

account data available at the time of budgeting.

TASK 2

(a) Cash budget

Cash Budget for the period of 6 months

Particulars

Pre-operating

year

Janua

ry

Febru

ary March April May June Total

Cash revenues

Cash sales 80000 81600 83232 85728.

96

88300.

8288

90949.

85366

50981

1.6424

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4 64

Bank loans 2500000

25000

00

Owner's capital 2500000

25000

00

Total cash inflow 5000000 81600 83232

85728.

96

88300.

8288

90949.

85366

4

55098

11.642

464

Cash payments

Construction of

hotel 2000000

20000

00

Furniture purchase 100000

10000

0

Office equipments 50000 3000 53000

Legal formalities 35000 35000

Repayment of loan 21000 21000 21000 21000 21000 21000

12600

0

Interest paid 16667 16667 16667 16667 16667 16667

10000

0

Cost of sales 20000 20400 20808 21432 22075 22737

12745

2.9106

16

Electricity charges 2400 4080 4161.6

4286.4

48

4415.0

4144

4547.4

92683

2

23890.

58212

32

Office stationery 800 816 832.32

857.28

96

883.00

8288

909.49

85366

4

5098.1

16424

64

Advertisement 3200 3264 3329.2 3429.1 3532.0 3637.9 20392.

5

Bank loans 2500000

25000

00

Owner's capital 2500000

25000

00

Total cash inflow 5000000 81600 83232

85728.

96

88300.

8288

90949.

85366

4

55098

11.642

464

Cash payments

Construction of

hotel 2000000

20000

00

Furniture purchase 100000

10000

0

Office equipments 50000 3000 53000

Legal formalities 35000 35000

Repayment of loan 21000 21000 21000 21000 21000 21000

12600

0

Interest paid 16667 16667 16667 16667 16667 16667

10000

0

Cost of sales 20000 20400 20808 21432 22075 22737

12745

2.9106

16

Electricity charges 2400 4080 4161.6

4286.4

48

4415.0

4144

4547.4

92683

2

23890.

58212

32

Office stationery 800 816 832.32

857.28

96

883.00

8288

909.49

85366

4

5098.1

16424

64

Advertisement 3200 3264 3329.2 3429.1 3532.0 3637.9 20392.

5

8 584 33152

94146

56

46569

856

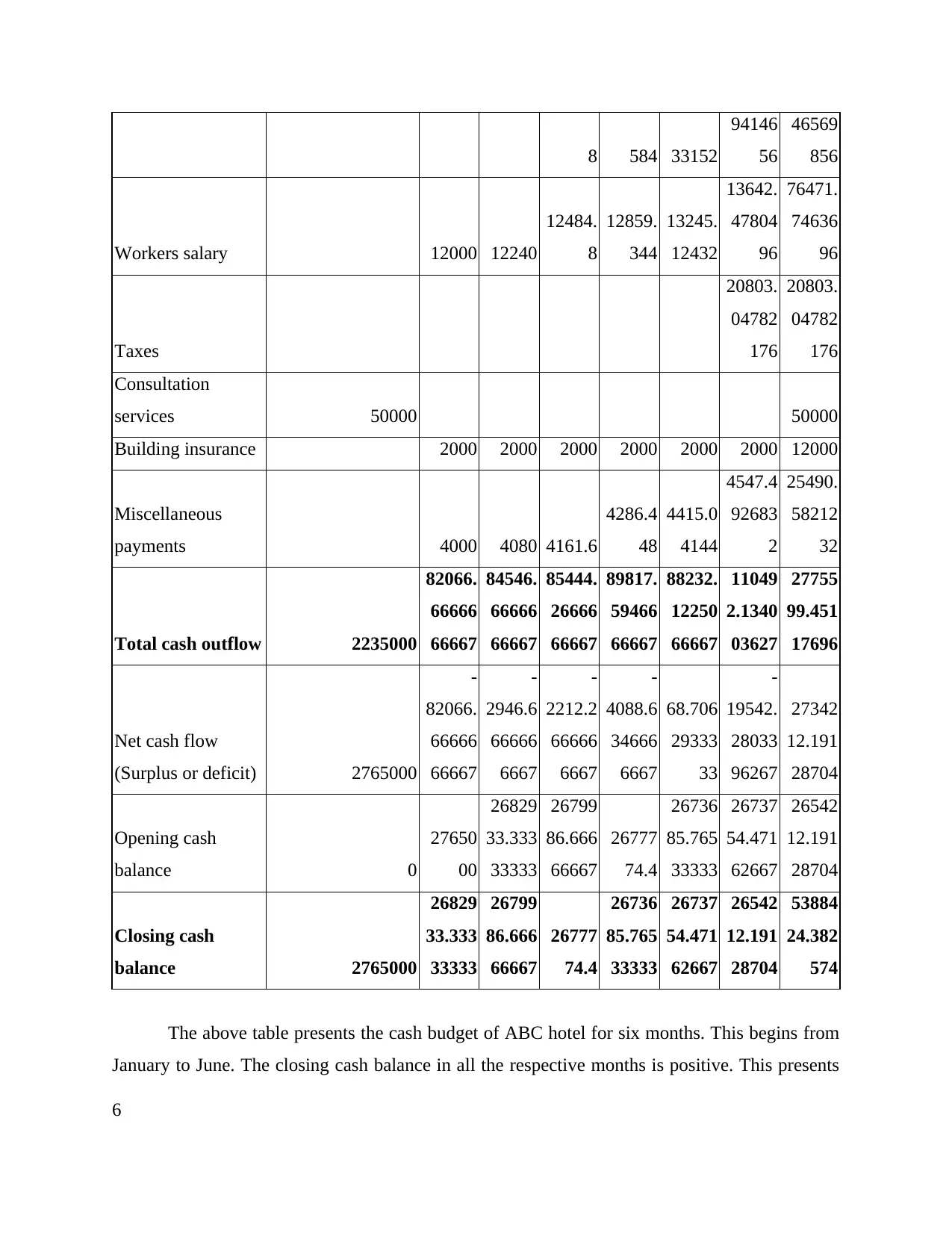

Workers salary 12000 12240

12484.

8

12859.

344

13245.

12432

13642.

47804

96

76471.

74636

96

Taxes

20803.

04782

176

20803.

04782

176

Consultation

services 50000 50000

Building insurance 2000 2000 2000 2000 2000 2000 12000

Miscellaneous

payments 4000 4080 4161.6

4286.4

48

4415.0

4144

4547.4

92683

2

25490.

58212

32

Total cash outflow 2235000

82066.

66666

66667

84546.

66666

66667

85444.

26666

66667

89817.

59466

66667

88232.

12250

66667

11049

2.1340

03627

27755

99.451

17696

Net cash flow

(Surplus or deficit) 2765000

-

82066.

66666

66667

-

2946.6

66666

6667

-

2212.2

66666

6667

-

4088.6

34666

6667

68.706

29333

33

-

19542.

28033

96267

27342

12.191

28704

Opening cash

balance 0

27650

00

26829

33.333

33333

26799

86.666

66667

26777

74.4

26736

85.765

33333

26737

54.471

62667

26542

12.191

28704

Closing cash

balance 2765000

26829

33.333

33333

26799

86.666

66667

26777

74.4

26736

85.765

33333

26737

54.471

62667

26542

12.191

28704

53884

24.382

574

The above table presents the cash budget of ABC hotel for six months. This begins from

January to June. The closing cash balance in all the respective months is positive. This presents

6

94146

56

46569

856

Workers salary 12000 12240

12484.

8

12859.

344

13245.

12432

13642.

47804

96

76471.

74636

96

Taxes

20803.

04782

176

20803.

04782

176

Consultation

services 50000 50000

Building insurance 2000 2000 2000 2000 2000 2000 12000

Miscellaneous

payments 4000 4080 4161.6

4286.4

48

4415.0

4144

4547.4

92683

2

25490.

58212

32

Total cash outflow 2235000

82066.

66666

66667

84546.

66666

66667

85444.

26666

66667

89817.

59466

66667

88232.

12250

66667

11049

2.1340

03627

27755

99.451

17696

Net cash flow

(Surplus or deficit) 2765000

-

82066.

66666

66667

-

2946.6

66666

6667

-

2212.2

66666

6667

-

4088.6

34666

6667

68.706

29333

33

-

19542.

28033

96267

27342

12.191

28704

Opening cash

balance 0

27650

00

26829

33.333

33333

26799

86.666

66667

26777

74.4

26736

85.765

33333

26737

54.471

62667

26542

12.191

28704

Closing cash

balance 2765000

26829

33.333

33333

26799

86.666

66667

26777

74.4

26736

85.765

33333

26737

54.471

62667

26542

12.191

28704

53884

24.382

574

The above table presents the cash budget of ABC hotel for six months. This begins from

January to June. The closing cash balance in all the respective months is positive. This presents

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that inflow of cash is greater that cash outflow. Thus, it can be determined that above budget can

be effective for the business. As such with this hotel can attain its pre-determined targets in an

effective manner.

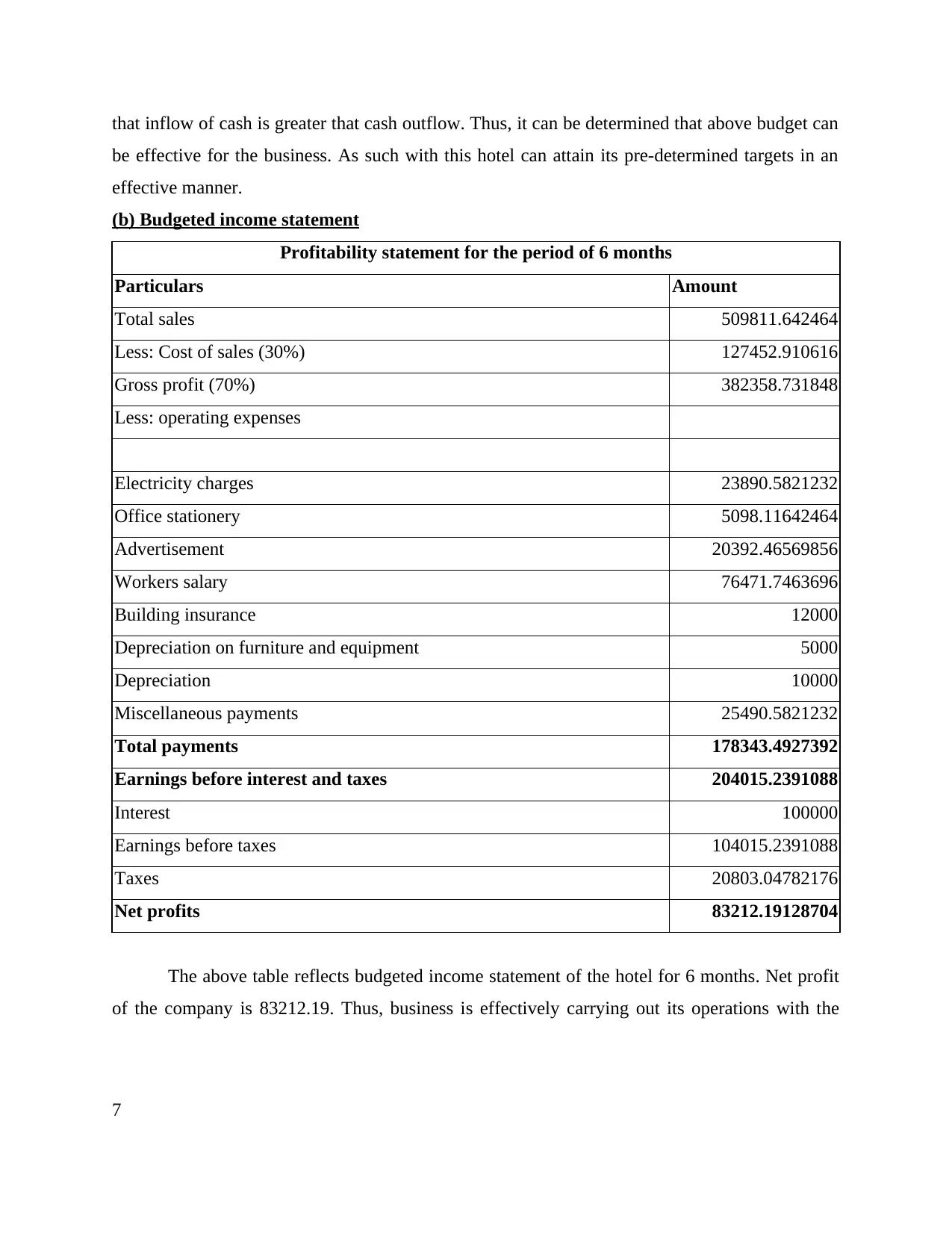

(b) Budgeted income statement

Profitability statement for the period of 6 months

Particulars Amount

Total sales 509811.642464

Less: Cost of sales (30%) 127452.910616

Gross profit (70%) 382358.731848

Less: operating expenses

Electricity charges 23890.5821232

Office stationery 5098.11642464

Advertisement 20392.46569856

Workers salary 76471.7463696

Building insurance 12000

Depreciation on furniture and equipment 5000

Depreciation 10000

Miscellaneous payments 25490.5821232

Total payments 178343.4927392

Earnings before interest and taxes 204015.2391088

Interest 100000

Earnings before taxes 104015.2391088

Taxes 20803.04782176

Net profits 83212.19128704

The above table reflects budgeted income statement of the hotel for 6 months. Net profit

of the company is 83212.19. Thus, business is effectively carrying out its operations with the

7

be effective for the business. As such with this hotel can attain its pre-determined targets in an

effective manner.

(b) Budgeted income statement

Profitability statement for the period of 6 months

Particulars Amount

Total sales 509811.642464

Less: Cost of sales (30%) 127452.910616

Gross profit (70%) 382358.731848

Less: operating expenses

Electricity charges 23890.5821232

Office stationery 5098.11642464

Advertisement 20392.46569856

Workers salary 76471.7463696

Building insurance 12000

Depreciation on furniture and equipment 5000

Depreciation 10000

Miscellaneous payments 25490.5821232

Total payments 178343.4927392

Earnings before interest and taxes 204015.2391088

Interest 100000

Earnings before taxes 104015.2391088

Taxes 20803.04782176

Net profits 83212.19128704

The above table reflects budgeted income statement of the hotel for 6 months. Net profit

of the company is 83212.19. Thus, business is effectively carrying out its operations with the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

available resources. The above budgeted income statement presents that it is the most suitable for

the organization as it reveals that company is making greater profitability.

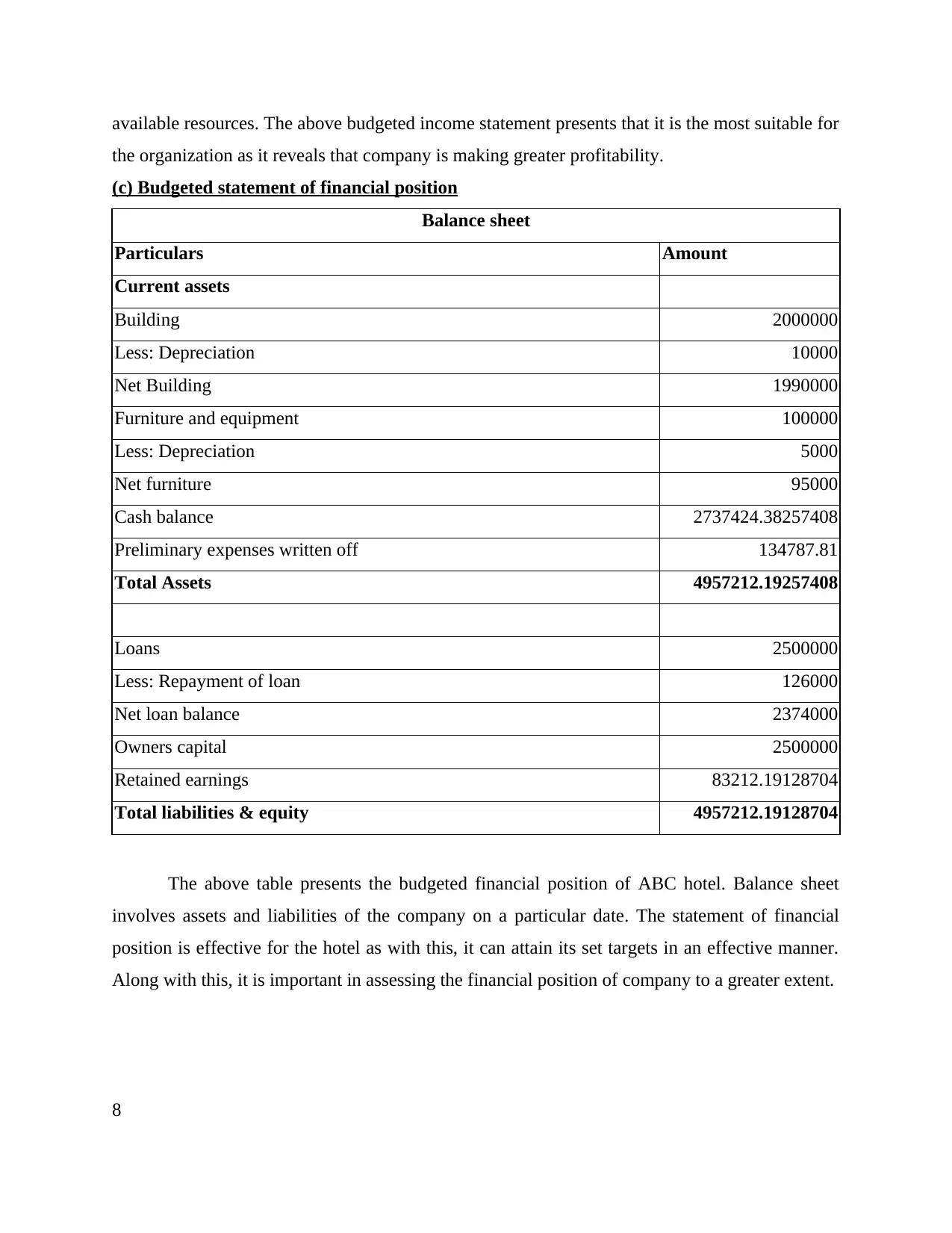

(c) Budgeted statement of financial position

Balance sheet

Particulars Amount

Current assets

Building 2000000

Less: Depreciation 10000

Net Building 1990000

Furniture and equipment 100000

Less: Depreciation 5000

Net furniture 95000

Cash balance 2737424.38257408

Preliminary expenses written off 134787.81

Total Assets 4957212.19257408

Loans 2500000

Less: Repayment of loan 126000

Net loan balance 2374000

Owners capital 2500000

Retained earnings 83212.19128704

Total liabilities & equity 4957212.19128704

The above table presents the budgeted financial position of ABC hotel. Balance sheet

involves assets and liabilities of the company on a particular date. The statement of financial

position is effective for the hotel as with this, it can attain its set targets in an effective manner.

Along with this, it is important in assessing the financial position of company to a greater extent.

8

the organization as it reveals that company is making greater profitability.

(c) Budgeted statement of financial position

Balance sheet

Particulars Amount

Current assets

Building 2000000

Less: Depreciation 10000

Net Building 1990000

Furniture and equipment 100000

Less: Depreciation 5000

Net furniture 95000

Cash balance 2737424.38257408

Preliminary expenses written off 134787.81

Total Assets 4957212.19257408

Loans 2500000

Less: Repayment of loan 126000

Net loan balance 2374000

Owners capital 2500000

Retained earnings 83212.19128704

Total liabilities & equity 4957212.19128704

The above table presents the budgeted financial position of ABC hotel. Balance sheet

involves assets and liabilities of the company on a particular date. The statement of financial

position is effective for the hotel as with this, it can attain its set targets in an effective manner.

Along with this, it is important in assessing the financial position of company to a greater extent.

8

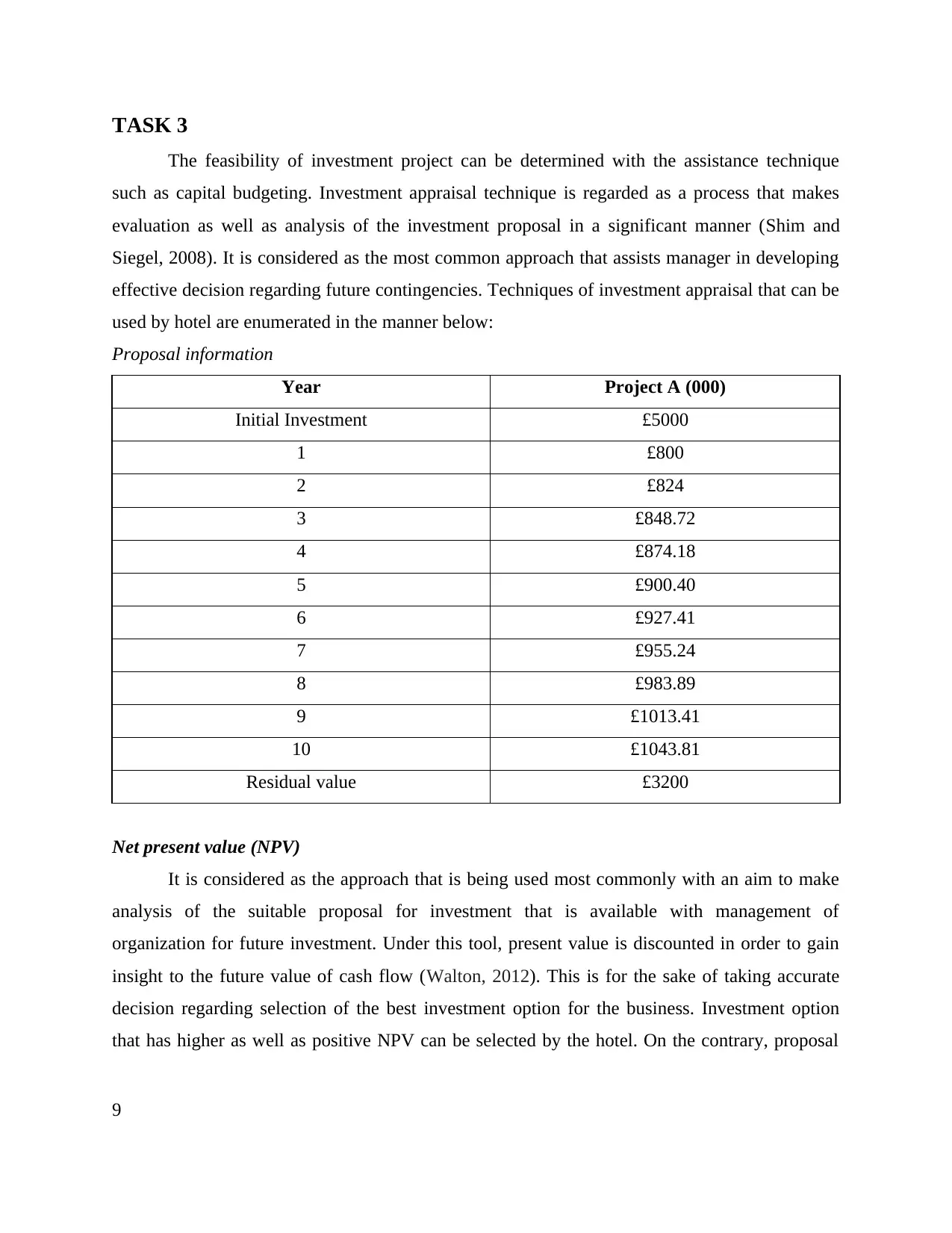

TASK 3

The feasibility of investment project can be determined with the assistance technique

such as capital budgeting. Investment appraisal technique is regarded as a process that makes

evaluation as well as analysis of the investment proposal in a significant manner (Shim and

Siegel, 2008). It is considered as the most common approach that assists manager in developing

effective decision regarding future contingencies. Techniques of investment appraisal that can be

used by hotel are enumerated in the manner below:

Proposal information

Year Project A (000)

Initial Investment £5000

1 £800

2 £824

3 £848.72

4 £874.18

5 £900.40

6 £927.41

7 £955.24

8 £983.89

9 £1013.41

10 £1043.81

Residual value £3200

Net present value (NPV)

It is considered as the approach that is being used most commonly with an aim to make

analysis of the suitable proposal for investment that is available with management of

organization for future investment. Under this tool, present value is discounted in order to gain

insight to the future value of cash flow (Walton, 2012). This is for the sake of taking accurate

decision regarding selection of the best investment option for the business. Investment option

that has higher as well as positive NPV can be selected by the hotel. On the contrary, proposal

9

The feasibility of investment project can be determined with the assistance technique

such as capital budgeting. Investment appraisal technique is regarded as a process that makes

evaluation as well as analysis of the investment proposal in a significant manner (Shim and

Siegel, 2008). It is considered as the most common approach that assists manager in developing

effective decision regarding future contingencies. Techniques of investment appraisal that can be

used by hotel are enumerated in the manner below:

Proposal information

Year Project A (000)

Initial Investment £5000

1 £800

2 £824

3 £848.72

4 £874.18

5 £900.40

6 £927.41

7 £955.24

8 £983.89

9 £1013.41

10 £1043.81

Residual value £3200

Net present value (NPV)

It is considered as the approach that is being used most commonly with an aim to make

analysis of the suitable proposal for investment that is available with management of

organization for future investment. Under this tool, present value is discounted in order to gain

insight to the future value of cash flow (Walton, 2012). This is for the sake of taking accurate

decision regarding selection of the best investment option for the business. Investment option

that has higher as well as positive NPV can be selected by the hotel. On the contrary, proposal

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

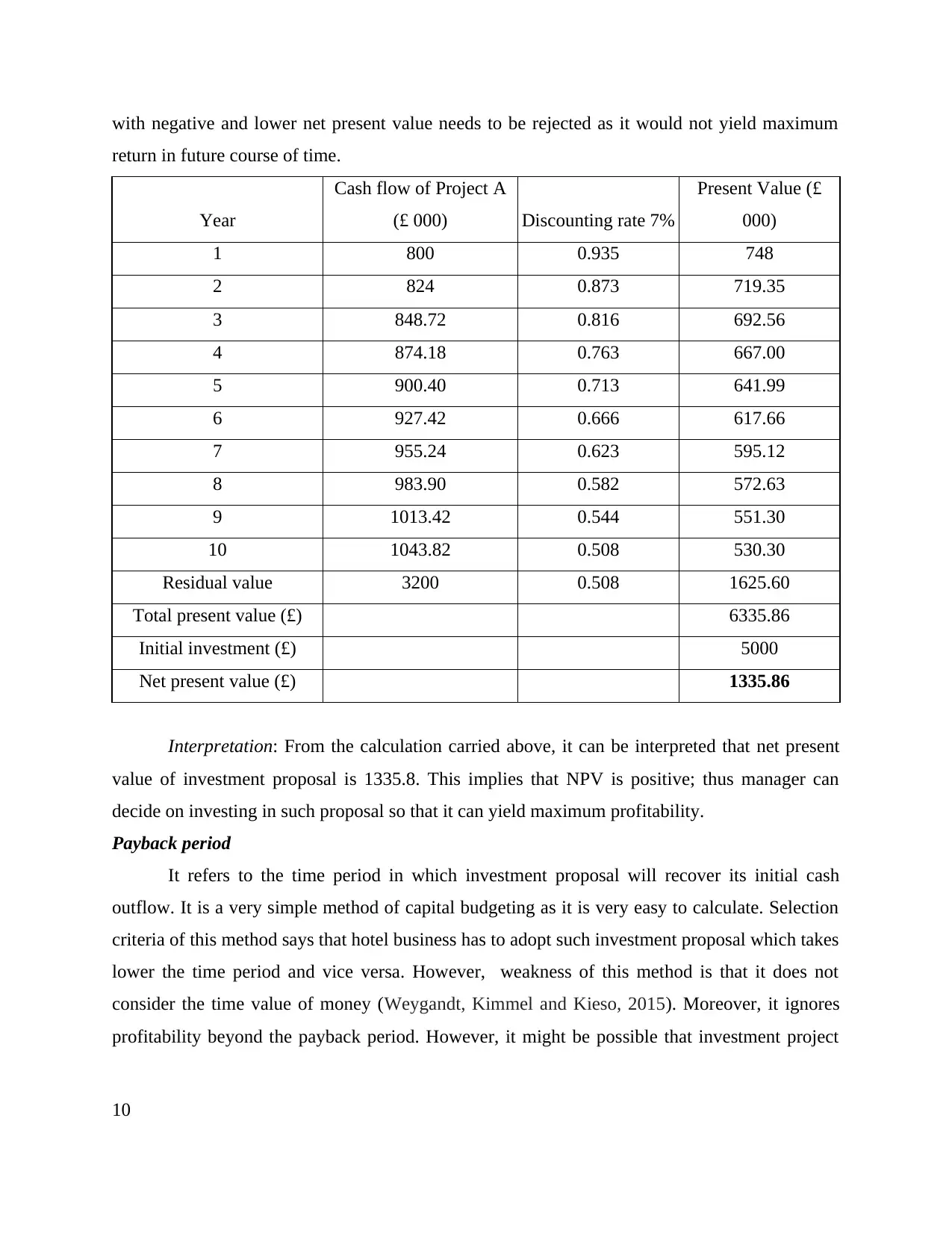

with negative and lower net present value needs to be rejected as it would not yield maximum

return in future course of time.

Year

Cash flow of Project A

(£ 000) Discounting rate 7%

Present Value (£

000)

1 800 0.935 748

2 824 0.873 719.35

3 848.72 0.816 692.56

4 874.18 0.763 667.00

5 900.40 0.713 641.99

6 927.42 0.666 617.66

7 955.24 0.623 595.12

8 983.90 0.582 572.63

9 1013.42 0.544 551.30

10 1043.82 0.508 530.30

Residual value 3200 0.508 1625.60

Total present value (£) 6335.86

Initial investment (£) 5000

Net present value (£) 1335.86

Interpretation: From the calculation carried above, it can be interpreted that net present

value of investment proposal is 1335.8. This implies that NPV is positive; thus manager can

decide on investing in such proposal so that it can yield maximum profitability.

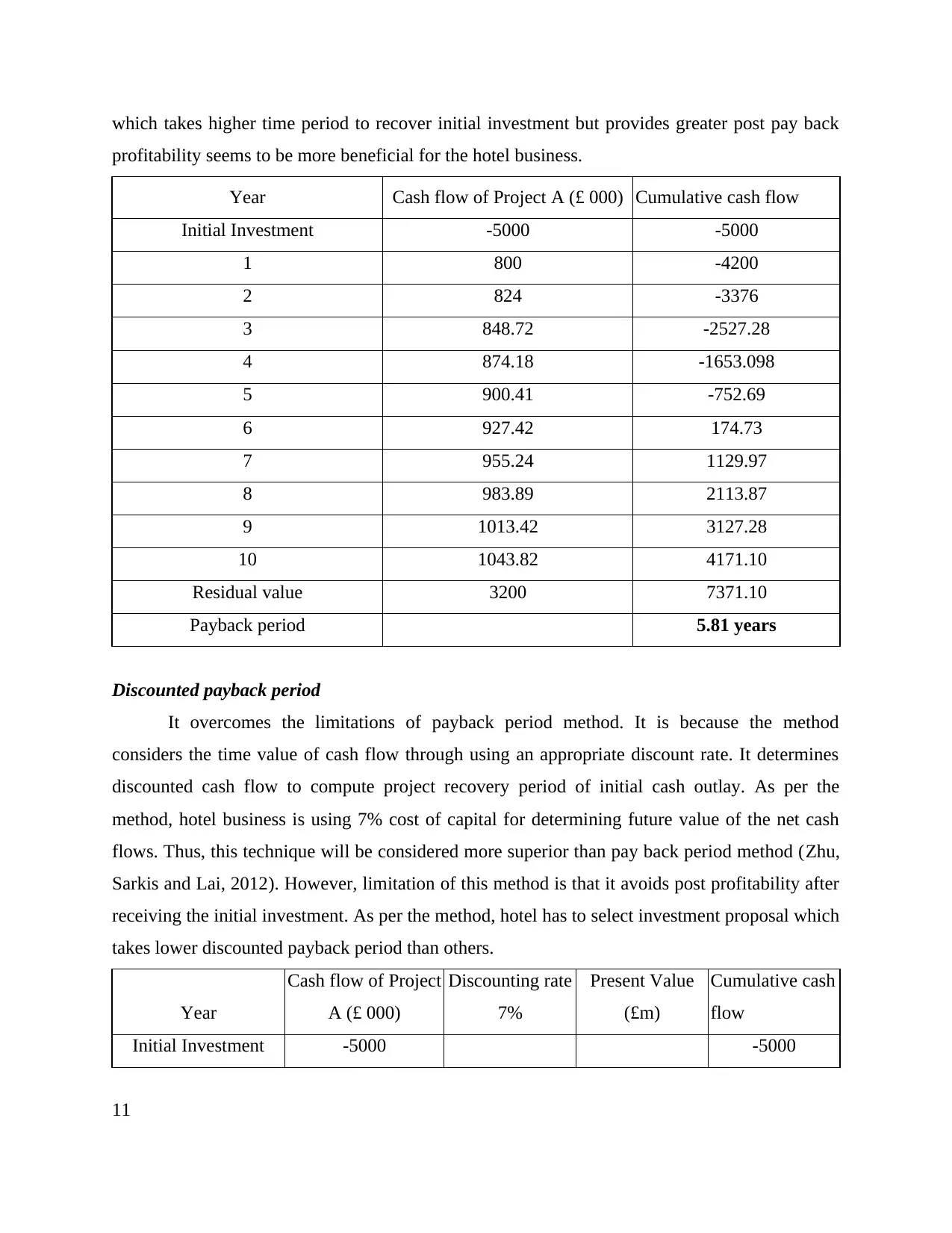

Payback period

It refers to the time period in which investment proposal will recover its initial cash

outflow. It is a very simple method of capital budgeting as it is very easy to calculate. Selection

criteria of this method says that hotel business has to adopt such investment proposal which takes

lower the time period and vice versa. However, weakness of this method is that it does not

consider the time value of money (Weygandt, Kimmel and Kieso, 2015). Moreover, it ignores

profitability beyond the payback period. However, it might be possible that investment project

10

return in future course of time.

Year

Cash flow of Project A

(£ 000) Discounting rate 7%

Present Value (£

000)

1 800 0.935 748

2 824 0.873 719.35

3 848.72 0.816 692.56

4 874.18 0.763 667.00

5 900.40 0.713 641.99

6 927.42 0.666 617.66

7 955.24 0.623 595.12

8 983.90 0.582 572.63

9 1013.42 0.544 551.30

10 1043.82 0.508 530.30

Residual value 3200 0.508 1625.60

Total present value (£) 6335.86

Initial investment (£) 5000

Net present value (£) 1335.86

Interpretation: From the calculation carried above, it can be interpreted that net present

value of investment proposal is 1335.8. This implies that NPV is positive; thus manager can

decide on investing in such proposal so that it can yield maximum profitability.

Payback period

It refers to the time period in which investment proposal will recover its initial cash

outflow. It is a very simple method of capital budgeting as it is very easy to calculate. Selection

criteria of this method says that hotel business has to adopt such investment proposal which takes

lower the time period and vice versa. However, weakness of this method is that it does not

consider the time value of money (Weygandt, Kimmel and Kieso, 2015). Moreover, it ignores

profitability beyond the payback period. However, it might be possible that investment project

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which takes higher time period to recover initial investment but provides greater post pay back

profitability seems to be more beneficial for the hotel business.

Year Cash flow of Project A (£ 000) Cumulative cash flow

Initial Investment -5000 -5000

1 800 -4200

2 824 -3376

3 848.72 -2527.28

4 874.18 -1653.098

5 900.41 -752.69

6 927.42 174.73

7 955.24 1129.97

8 983.89 2113.87

9 1013.42 3127.28

10 1043.82 4171.10

Residual value 3200 7371.10

Payback period 5.81 years

Discounted payback period

It overcomes the limitations of payback period method. It is because the method

considers the time value of cash flow through using an appropriate discount rate. It determines

discounted cash flow to compute project recovery period of initial cash outlay. As per the

method, hotel business is using 7% cost of capital for determining future value of the net cash

flows. Thus, this technique will be considered more superior than pay back period method (Zhu,

Sarkis and Lai, 2012). However, limitation of this method is that it avoids post profitability after

receiving the initial investment. As per the method, hotel has to select investment proposal which

takes lower discounted payback period than others.

Year

Cash flow of Project

A (£ 000)

Discounting rate

7%

Present Value

(£m)

Cumulative cash

flow

Initial Investment -5000 -5000

11

profitability seems to be more beneficial for the hotel business.

Year Cash flow of Project A (£ 000) Cumulative cash flow

Initial Investment -5000 -5000

1 800 -4200

2 824 -3376

3 848.72 -2527.28

4 874.18 -1653.098

5 900.41 -752.69

6 927.42 174.73

7 955.24 1129.97

8 983.89 2113.87

9 1013.42 3127.28

10 1043.82 4171.10

Residual value 3200 7371.10

Payback period 5.81 years

Discounted payback period

It overcomes the limitations of payback period method. It is because the method

considers the time value of cash flow through using an appropriate discount rate. It determines

discounted cash flow to compute project recovery period of initial cash outlay. As per the

method, hotel business is using 7% cost of capital for determining future value of the net cash

flows. Thus, this technique will be considered more superior than pay back period method (Zhu,

Sarkis and Lai, 2012). However, limitation of this method is that it avoids post profitability after

receiving the initial investment. As per the method, hotel has to select investment proposal which

takes lower discounted payback period than others.

Year

Cash flow of Project

A (£ 000)

Discounting rate

7%

Present Value

(£m)

Cumulative cash

flow

Initial Investment -5000 -5000

11

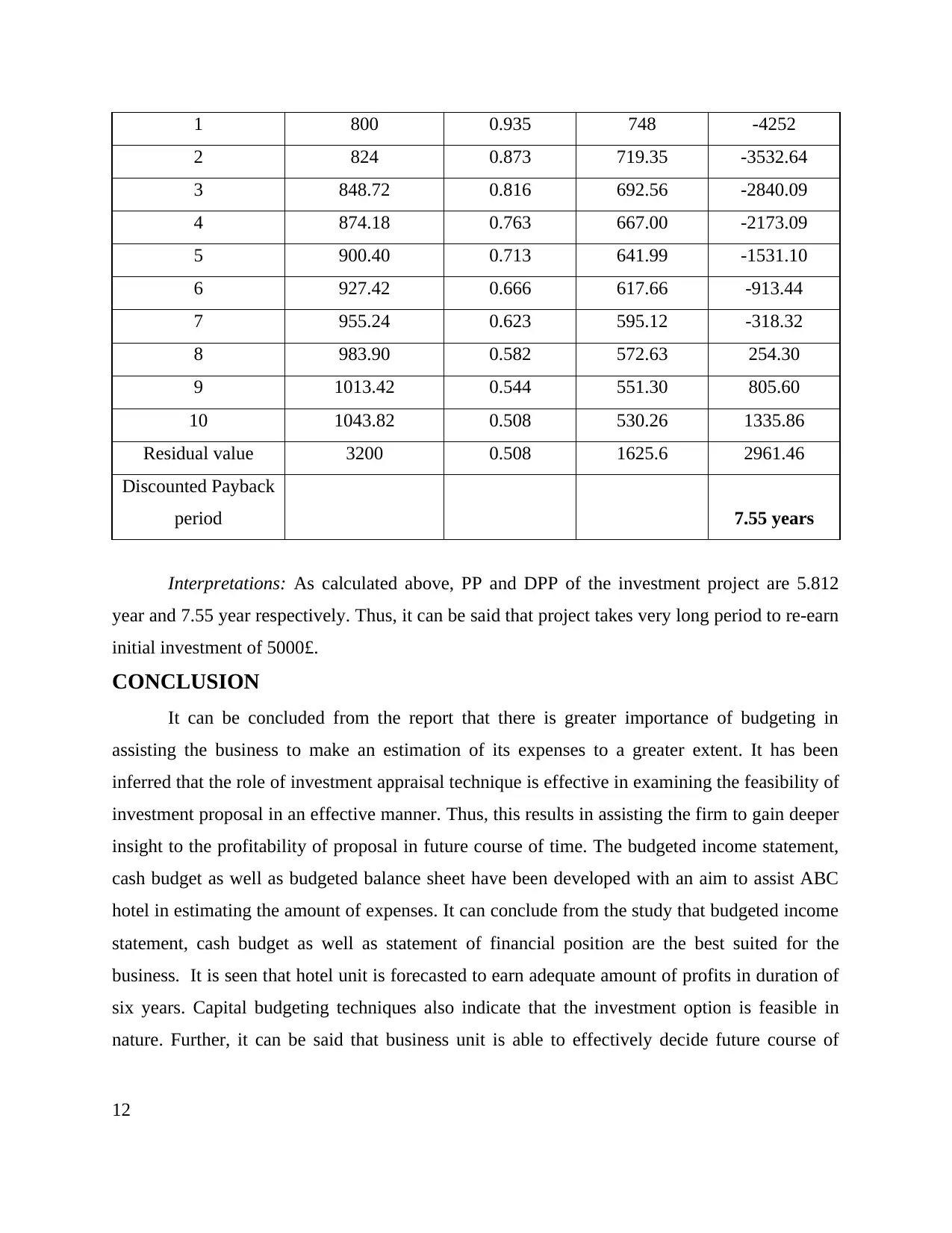

1 800 0.935 748 -4252

2 824 0.873 719.35 -3532.64

3 848.72 0.816 692.56 -2840.09

4 874.18 0.763 667.00 -2173.09

5 900.40 0.713 641.99 -1531.10

6 927.42 0.666 617.66 -913.44

7 955.24 0.623 595.12 -318.32

8 983.90 0.582 572.63 254.30

9 1013.42 0.544 551.30 805.60

10 1043.82 0.508 530.26 1335.86

Residual value 3200 0.508 1625.6 2961.46

Discounted Payback

period 7.55 years

Interpretations: As calculated above, PP and DPP of the investment project are 5.812

year and 7.55 year respectively. Thus, it can be said that project takes very long period to re-earn

initial investment of 5000£.

CONCLUSION

It can be concluded from the report that there is greater importance of budgeting in

assisting the business to make an estimation of its expenses to a greater extent. It has been

inferred that the role of investment appraisal technique is effective in examining the feasibility of

investment proposal in an effective manner. Thus, this results in assisting the firm to gain deeper

insight to the profitability of proposal in future course of time. The budgeted income statement,

cash budget as well as budgeted balance sheet have been developed with an aim to assist ABC

hotel in estimating the amount of expenses. It can conclude from the study that budgeted income

statement, cash budget as well as statement of financial position are the best suited for the

business. It is seen that hotel unit is forecasted to earn adequate amount of profits in duration of

six years. Capital budgeting techniques also indicate that the investment option is feasible in

nature. Further, it can be said that business unit is able to effectively decide future course of

12

2 824 0.873 719.35 -3532.64

3 848.72 0.816 692.56 -2840.09

4 874.18 0.763 667.00 -2173.09

5 900.40 0.713 641.99 -1531.10

6 927.42 0.666 617.66 -913.44

7 955.24 0.623 595.12 -318.32

8 983.90 0.582 572.63 254.30

9 1013.42 0.544 551.30 805.60

10 1043.82 0.508 530.26 1335.86

Residual value 3200 0.508 1625.6 2961.46

Discounted Payback

period 7.55 years

Interpretations: As calculated above, PP and DPP of the investment project are 5.812

year and 7.55 year respectively. Thus, it can be said that project takes very long period to re-earn

initial investment of 5000£.

CONCLUSION

It can be concluded from the report that there is greater importance of budgeting in

assisting the business to make an estimation of its expenses to a greater extent. It has been

inferred that the role of investment appraisal technique is effective in examining the feasibility of

investment proposal in an effective manner. Thus, this results in assisting the firm to gain deeper

insight to the profitability of proposal in future course of time. The budgeted income statement,

cash budget as well as budgeted balance sheet have been developed with an aim to assist ABC

hotel in estimating the amount of expenses. It can conclude from the study that budgeted income

statement, cash budget as well as statement of financial position are the best suited for the

business. It is seen that hotel unit is forecasted to earn adequate amount of profits in duration of

six years. Capital budgeting techniques also indicate that the investment option is feasible in

nature. Further, it can be said that business unit is able to effectively decide future course of

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.