Management Accounting Report: HSBC Holdings PLC Case Study

VerifiedAdded on 2021/02/19

|20

|4052

|29

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within HSBC Holdings PLC. It begins with an introduction to management accounting, differentiating it from financial accounting and highlighting its essential requirements. The report then delves into various management accounting systems, including price optimization, cost accounting, inventory management, and job costing, detailing their benefits and applications within an organizational context. It further explores different methods used in management accounting, such as performance reports, budget reports, and cost managerial accounting reports. The report also examines planning tools used in management accounting and how these tools can be applied for preparing and forecasting budgets. Finally, it addresses how management accounting systems can respond to financial problems, providing an evaluation of planning tools for solving financial issues. The analysis incorporates relevant examples and case studies to illustrate the practical implementation of these concepts within HSBC.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of different types of management

accounting systems.................................................................................................................1

M1 Benefits of management accounting systems and its application within an organisational

context....................................................................................................................................3

D1 Management accounting systems and management accounting reporting is integrated

within organisation.................................................................................................................4

P2 Methods that are used for management accounting period...............................................4

TASK 2............................................................................................................................................6

P3 Appropriate techniques of cost analysis to prepare income statement for HSBC...........6

M2 Several range of management accounting techniques and appropriate financial reporting

documents.............................................................................................................................11

D2 Financial reports that accurately apply and interpret data for a range of business activities

..............................................................................................................................................11

TASK 3..........................................................................................................................................12

P4 Planning tools used in management accounting.............................................................12

M3 Planning tools and their application for preparing and forecasting budgets..................14

TASK 4 .........................................................................................................................................14

P5 Management accounting systems to respond to financial problems...............................14

M4 Responding to financial problems with context of management accounting...............16

D3 Evaluation of planning tools for accounting appropriately to solving financial problems16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of different types of management

accounting systems.................................................................................................................1

M1 Benefits of management accounting systems and its application within an organisational

context....................................................................................................................................3

D1 Management accounting systems and management accounting reporting is integrated

within organisation.................................................................................................................4

P2 Methods that are used for management accounting period...............................................4

TASK 2............................................................................................................................................6

P3 Appropriate techniques of cost analysis to prepare income statement for HSBC...........6

M2 Several range of management accounting techniques and appropriate financial reporting

documents.............................................................................................................................11

D2 Financial reports that accurately apply and interpret data for a range of business activities

..............................................................................................................................................11

TASK 3..........................................................................................................................................12

P4 Planning tools used in management accounting.............................................................12

M3 Planning tools and their application for preparing and forecasting budgets..................14

TASK 4 .........................................................................................................................................14

P5 Management accounting systems to respond to financial problems...............................14

M4 Responding to financial problems with context of management accounting...............16

D3 Evaluation of planning tools for accounting appropriately to solving financial problems16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting is a systematic approach which is used by the organisation to

track the financial and statistical information. The information collected with the help of

managerial accounting system helps the business managers in their decision making process.

Every business uses accounting techniques to support strategy formation, business execution and

risk taking. In this report, the chosen association is HSBC holding plc. It is the 7th largest

multinational banking and financial services holding company. The company provides services

like Retail banking, corporate banking, investment banking, mortgage loans, private banking,

wealth management, credit cards and insurance (Zayed and Liu, 2014).

. In this respective report the areas which the company focuses are different management

techniques and reporting methods , planning tools used in management accounting. At last it

describe about how management accounting is used by business to solve their financial

problems.

TASK 1

P1 Management accounting and essential requirements of different types of management

accounting systems.

Management accounting involves providing informations regarding the scarce financial

resources and their allocations. These are the reports prepared as per the needs and requirements

of the organisation's. The company like HSBC is required to establish managerial accounting in

their business in order to predict about the future events, companies costs and revenues and this

would also help them in comparing overheads, hourly labour costs, productivity figures between

departments. These reports are based on management's informational needs and include

budgeting, break even charts, products cost analysis, trend charts and forecasting. For

maintaining this the company is required to cover all the types of management accounting which

are mentioned below :-

Difference between Management accounting and Financial accounting :

Management accounting Financial accounting

Management accounting is the one which is

prepared for the internal use of managers and

Financial accounting are the one prepared for

the used of stakeholders, creditors, banks and

1

Management accounting is a systematic approach which is used by the organisation to

track the financial and statistical information. The information collected with the help of

managerial accounting system helps the business managers in their decision making process.

Every business uses accounting techniques to support strategy formation, business execution and

risk taking. In this report, the chosen association is HSBC holding plc. It is the 7th largest

multinational banking and financial services holding company. The company provides services

like Retail banking, corporate banking, investment banking, mortgage loans, private banking,

wealth management, credit cards and insurance (Zayed and Liu, 2014).

. In this respective report the areas which the company focuses are different management

techniques and reporting methods , planning tools used in management accounting. At last it

describe about how management accounting is used by business to solve their financial

problems.

TASK 1

P1 Management accounting and essential requirements of different types of management

accounting systems.

Management accounting involves providing informations regarding the scarce financial

resources and their allocations. These are the reports prepared as per the needs and requirements

of the organisation's. The company like HSBC is required to establish managerial accounting in

their business in order to predict about the future events, companies costs and revenues and this

would also help them in comparing overheads, hourly labour costs, productivity figures between

departments. These reports are based on management's informational needs and include

budgeting, break even charts, products cost analysis, trend charts and forecasting. For

maintaining this the company is required to cover all the types of management accounting which

are mentioned below :-

Difference between Management accounting and Financial accounting :

Management accounting Financial accounting

Management accounting is the one which is

prepared for the internal use of managers and

Financial accounting are the one prepared for

the used of stakeholders, creditors, banks and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

employees. government.

It does not involve any legal requirement. These are necessary to be prepared by the

limited companies.

Management accounting is prepared

considering specific areas of the business.

This provides us with the information on the

entire organisation.

Management accounting is prepared to

measure financial and operational

performance.

Financial accounting measures only financial

data.

Price optimisation system: It is a crucial component of price management which is used

by business to determine the customer's reactions on different prices of products and services. If

the company HSBC adopts the strategy of price optimisation they can easily identify the initial

pricing , promotional pricing and markdown pricing (Yang and Liu, 2017).

Initial pricing – This price optimisation tool works well when the organisation has a stable base

and long lasting life of their services.

Promotional pricing – This would helps the business to set temporary prices of their services to

build the customer base.

Discount pricing – This would help the business to sell short term services like insurance ,

credit facilities.

This strategy will also helps HSBC holding plc in saving time, providing with market

transparency and full control.

Cost accounting system: This strategy of management accounting helps in computing

the overall cost of operations and activities by evaluating prices of each units separately. It has

been designed by the managers to identify the flow of inventory (van Helden and Uddin, 2016).

Cost accounting system would help HSBC in immediate saving and would also ensure that the

banks remains competitive in the longer term, and would also help them in fixation of price ,

controlling costs and facilitating short term decisions, especially during the period of depression.

Inventory management system: It is an ongoing process in the business which is used

for balancing inventory and it also helps in de terming that how much inventory is exactly

needed. Inventory management system helps the organisation's in keeping records of every items

2

It does not involve any legal requirement. These are necessary to be prepared by the

limited companies.

Management accounting is prepared

considering specific areas of the business.

This provides us with the information on the

entire organisation.

Management accounting is prepared to

measure financial and operational

performance.

Financial accounting measures only financial

data.

Price optimisation system: It is a crucial component of price management which is used

by business to determine the customer's reactions on different prices of products and services. If

the company HSBC adopts the strategy of price optimisation they can easily identify the initial

pricing , promotional pricing and markdown pricing (Yang and Liu, 2017).

Initial pricing – This price optimisation tool works well when the organisation has a stable base

and long lasting life of their services.

Promotional pricing – This would helps the business to set temporary prices of their services to

build the customer base.

Discount pricing – This would help the business to sell short term services like insurance ,

credit facilities.

This strategy will also helps HSBC holding plc in saving time, providing with market

transparency and full control.

Cost accounting system: This strategy of management accounting helps in computing

the overall cost of operations and activities by evaluating prices of each units separately. It has

been designed by the managers to identify the flow of inventory (van Helden and Uddin, 2016).

Cost accounting system would help HSBC in immediate saving and would also ensure that the

banks remains competitive in the longer term, and would also help them in fixation of price ,

controlling costs and facilitating short term decisions, especially during the period of depression.

Inventory management system: It is an ongoing process in the business which is used

for balancing inventory and it also helps in de terming that how much inventory is exactly

needed. Inventory management system helps the organisation's in keeping records of every items

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and assets. HSBC is required to install proper inventory management system in their banks to

ensure improved cash flow, better reporting and forecasting facilities, proper planning, enhanced

transparency and better organisation. In banking sector this would also help in advance user

security, active directory, assets depreciation etc.

Job costing system: It is beneficial in the computing the cost of each job which is assigned to

different activities. If HSBC adopts this strategy it can easily identify the following points :-

It acts as a gauge determining the profitability of the job and helps for the future

customers or institution to decide whether to take up the job or not. It also gives us an

idea about the feasibility of the job (Tappura and et. al., 2015).

Budgetary control comes into action when taken consideration of the various overhead

charges which are predetermined for each department.

Job costing provides an easy computation of cost overheads for specific needs,and in a

precise manner. Job costing enables the supervisors to keep track of various factor such

as money, materials and the performance of the employees.

Job costing acts as a form of analysis detailing all the type of costs that are present

throughout the manufacturing process. This includes the direct costs, the labour costs,

and the overhead charges.

Characteristic of good information system

Reliable- It is essential for HSBC to implement the data that is relevant and reliable for

the organisation. Moreover this data need to be maintain as trustworthy for the

organisation that is accurate, consistent and related with facts that need to implement in

project.

Accuracy- Data which is collected by the organisation needs to be accurate. So at time of

implement them in the project management of HSBC derive positive results in the

organisation.

Up to date- In context of this data whereas organisation implement information that is

desirable and updated because there is constant changes are changed in information that

is present in the market.

3

ensure improved cash flow, better reporting and forecasting facilities, proper planning, enhanced

transparency and better organisation. In banking sector this would also help in advance user

security, active directory, assets depreciation etc.

Job costing system: It is beneficial in the computing the cost of each job which is assigned to

different activities. If HSBC adopts this strategy it can easily identify the following points :-

It acts as a gauge determining the profitability of the job and helps for the future

customers or institution to decide whether to take up the job or not. It also gives us an

idea about the feasibility of the job (Tappura and et. al., 2015).

Budgetary control comes into action when taken consideration of the various overhead

charges which are predetermined for each department.

Job costing provides an easy computation of cost overheads for specific needs,and in a

precise manner. Job costing enables the supervisors to keep track of various factor such

as money, materials and the performance of the employees.

Job costing acts as a form of analysis detailing all the type of costs that are present

throughout the manufacturing process. This includes the direct costs, the labour costs,

and the overhead charges.

Characteristic of good information system

Reliable- It is essential for HSBC to implement the data that is relevant and reliable for

the organisation. Moreover this data need to be maintain as trustworthy for the

organisation that is accurate, consistent and related with facts that need to implement in

project.

Accuracy- Data which is collected by the organisation needs to be accurate. So at time of

implement them in the project management of HSBC derive positive results in the

organisation.

Up to date- In context of this data whereas organisation implement information that is

desirable and updated because there is constant changes are changed in information that

is present in the market.

3

M1 Benefits of management accounting systems and its application within an organisational

context

Management accounting does not works on the principle of national accounting

standards. In this system the business owners design the management system by themselves in

order to carry out their business operations. Management accounting has certain benefits, these

benefits are usually concerned with the ability for companies to enhance their profitability and

performances. proper allocation of cost can also develop and creates competitive advantages for

the owner of the business (Scherbina, Afanasyeva and Lapina, 2013). These benefits would also

help HSBC in certain ways which are as follows :-

Reduce expenses: This helps the business in reducing their operational expense . It would

also helps the manager of HSBC to reduce the cost of operation by allowing them to evaluate

and identify that how much it cost to run the business.

Improve cash flow : Management accounting has a great impact on improving the

process of cash flow as it keeps complete records of all the floes of goods and services . This also

helps the company Like HSBC by allowing its manager to roadmap the financial budget which

will further reduce their unnecessary cash expenditure.

Business decisions : This will also help the manager of HSBC banks to improve their

business decision making process. The managers here will use quantitative analysis to assure that

the manager have the clear understanding regarding the business decision-making.

D1 Management accounting systems and management accounting reporting is integrated within

organisation

Management accounting system is interconnected with management reporting system

that helps them to make effective decisions in the organisation. It results for the improvement of

organisation (Parker, 2012). Example through which it is easy to understand cost accounting

system. HSBC analysis the total cost of their operations in order prepare the budget on the basis

of current financial position of an organisation which enhance productivity of their operations

and employees. Example- Cost accounting reporting helps an organisation to find actual cost of

their activities. But this are manage along with cost accounting system that creates issue for the

organisation as it is time consuming. While the results which are prepared by them helps HSBC

to find out profits margin which is earned by them through analysing their production cost.

4

context

Management accounting does not works on the principle of national accounting

standards. In this system the business owners design the management system by themselves in

order to carry out their business operations. Management accounting has certain benefits, these

benefits are usually concerned with the ability for companies to enhance their profitability and

performances. proper allocation of cost can also develop and creates competitive advantages for

the owner of the business (Scherbina, Afanasyeva and Lapina, 2013). These benefits would also

help HSBC in certain ways which are as follows :-

Reduce expenses: This helps the business in reducing their operational expense . It would

also helps the manager of HSBC to reduce the cost of operation by allowing them to evaluate

and identify that how much it cost to run the business.

Improve cash flow : Management accounting has a great impact on improving the

process of cash flow as it keeps complete records of all the floes of goods and services . This also

helps the company Like HSBC by allowing its manager to roadmap the financial budget which

will further reduce their unnecessary cash expenditure.

Business decisions : This will also help the manager of HSBC banks to improve their

business decision making process. The managers here will use quantitative analysis to assure that

the manager have the clear understanding regarding the business decision-making.

D1 Management accounting systems and management accounting reporting is integrated within

organisation

Management accounting system is interconnected with management reporting system

that helps them to make effective decisions in the organisation. It results for the improvement of

organisation (Parker, 2012). Example through which it is easy to understand cost accounting

system. HSBC analysis the total cost of their operations in order prepare the budget on the basis

of current financial position of an organisation which enhance productivity of their operations

and employees. Example- Cost accounting reporting helps an organisation to find actual cost of

their activities. But this are manage along with cost accounting system that creates issue for the

organisation as it is time consuming. While the results which are prepared by them helps HSBC

to find out profits margin which is earned by them through analysing their production cost.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P2 Methods that are used for management accounting period

Management accounting is considered different methods that are used by HSBC in order

to keep records for every business transaction that take place in the organisation on daily basis.

This helps management to take relevant decision as on basis of information that is contain by

society in order to generate more profits in the organisation (Nielsen, Mitchell and Nørreklit,

2015). This reporting system are discussed as below briefly:

Types of reports :

Performance report : This reports are based on the performance of different factors like

operation, functions etc. that are performed by the organisation in order to achieve their desired

goals. This helps organisation to generate report of employees and functions that are done HSBC

as their routine work. Along with this it is also a part of management plans through which

management communicate with their employees. HSBC formulate performance management

card on daily basis in order to communicate with employees that help to overcome from different

issues by explaining weak points to employees.

Budget report : Budgets are prepared to compare the actual cost with the estimated cost

specifically in management accounting system. The main intention of budget is to control the

cost and expenses that are unnecessary bear by organisation. In context of HSBC it is essential

for them to control their expenditure in order to increase their profits. Finance department of

organisation develop budget in order to allocate their resources effectively. Along with this it

also helps them to reduce cost of operations and increase the availability of funds in the

organisation.

Account receivable ageing reports : This is an essential tool for the organisation that

helps to manage business with systematic approach. By maintaining this approach it is easy for

organisation to find out the number of debtors that are present in the organisation. It includes the

amount which is paid by customer and to measure time which is obscure by customers

(Kacharava, 2016). For HSBC it is essential for them in order to check the availability of funds.

Cost managerial accounting report : This report is prepared to know the cost of

amount spent on manufacturing the article . It provides full detail about the money invested in

carrying out business operations. Cambridge manufacturing Ltd. needs to prepared this to control

the cost which unnecessarily affects the profitability of the business and to understand the exact

expenditure of the organisations so that the optimization of resources can be done properly.

5

Management accounting is considered different methods that are used by HSBC in order

to keep records for every business transaction that take place in the organisation on daily basis.

This helps management to take relevant decision as on basis of information that is contain by

society in order to generate more profits in the organisation (Nielsen, Mitchell and Nørreklit,

2015). This reporting system are discussed as below briefly:

Types of reports :

Performance report : This reports are based on the performance of different factors like

operation, functions etc. that are performed by the organisation in order to achieve their desired

goals. This helps organisation to generate report of employees and functions that are done HSBC

as their routine work. Along with this it is also a part of management plans through which

management communicate with their employees. HSBC formulate performance management

card on daily basis in order to communicate with employees that help to overcome from different

issues by explaining weak points to employees.

Budget report : Budgets are prepared to compare the actual cost with the estimated cost

specifically in management accounting system. The main intention of budget is to control the

cost and expenses that are unnecessary bear by organisation. In context of HSBC it is essential

for them to control their expenditure in order to increase their profits. Finance department of

organisation develop budget in order to allocate their resources effectively. Along with this it

also helps them to reduce cost of operations and increase the availability of funds in the

organisation.

Account receivable ageing reports : This is an essential tool for the organisation that

helps to manage business with systematic approach. By maintaining this approach it is easy for

organisation to find out the number of debtors that are present in the organisation. It includes the

amount which is paid by customer and to measure time which is obscure by customers

(Kacharava, 2016). For HSBC it is essential for them in order to check the availability of funds.

Cost managerial accounting report : This report is prepared to know the cost of

amount spent on manufacturing the article . It provides full detail about the money invested in

carrying out business operations. Cambridge manufacturing Ltd. needs to prepared this to control

the cost which unnecessarily affects the profitability of the business and to understand the exact

expenditure of the organisations so that the optimization of resources can be done properly.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost report : Cost accounting is essential for the organisation because it helps them to

calculate the amount that is expense by them for conducting particular project. They provides

whole detail that is invested by them in order to complete their operations. It is important for

HSBC to measure and control the cost that is unnecessarily increases the expenses of

organisation.

Inventory Managerial Report- This is the report which is managed by supervisors in

an organisation which considers about the availability of raw materials that is present in the

organisation. It is beneficial for HSBC because it helps them to deliver quick services in the

market. Along with this it helps them to manage raw material which are required to produce

goods.

TASK 2

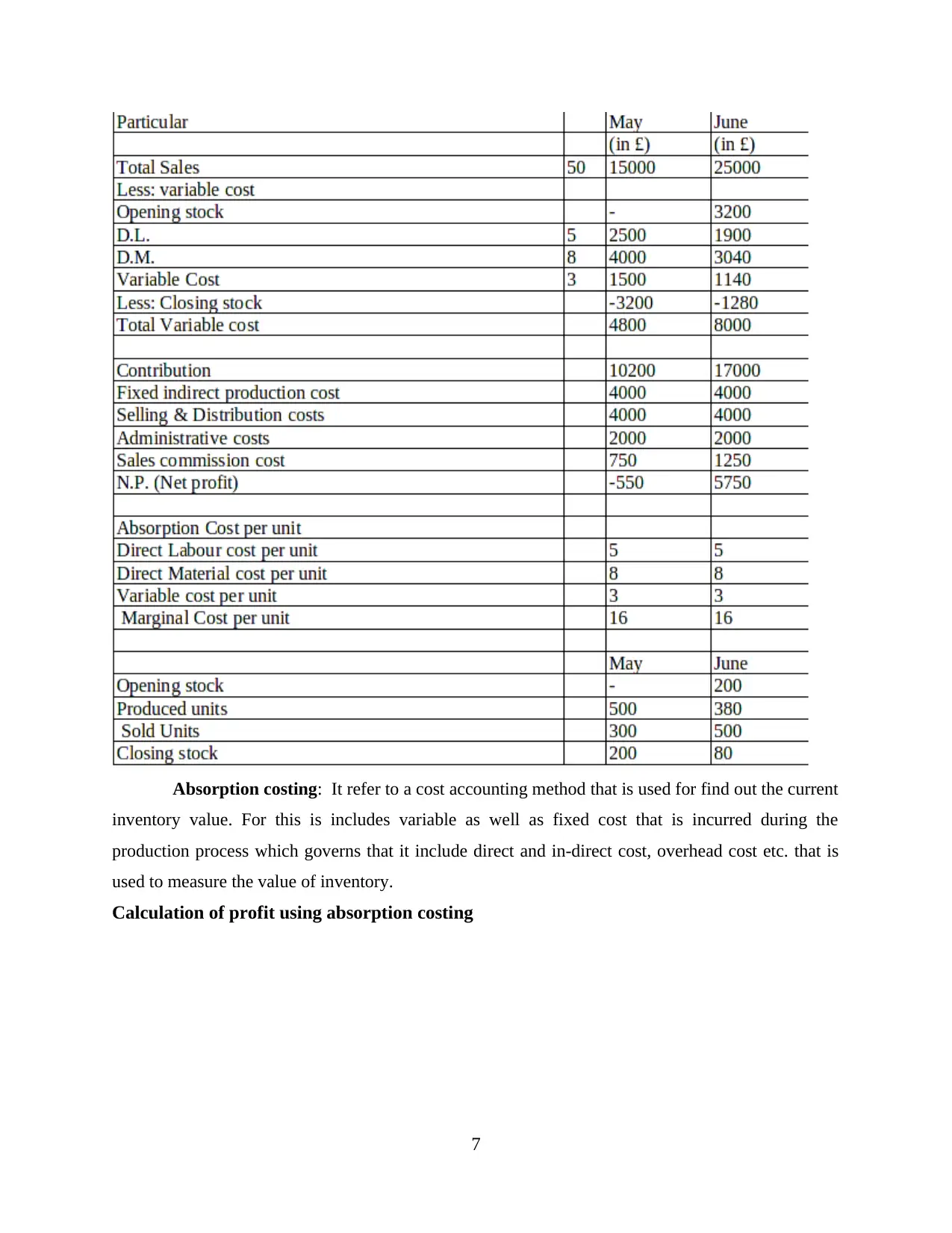

P3 Appropriate techniques of cost analysis to prepare income statement for HSBC

COST: The term cost includes all factors that are measured on monetary basis. This refers to

the amount that are essential to paid for purchasing any item inside the organisation. Usually cost is

the evaluation of efforts, machine, materials, resources etc. that are essential for organisation to

manufacture a product or service (Gond and et. al., 2012). Moreover cost is the amount that is

required to complete a business or job. Marginal and absorption are two type of cost that helps an

organisation to prepare income statement.

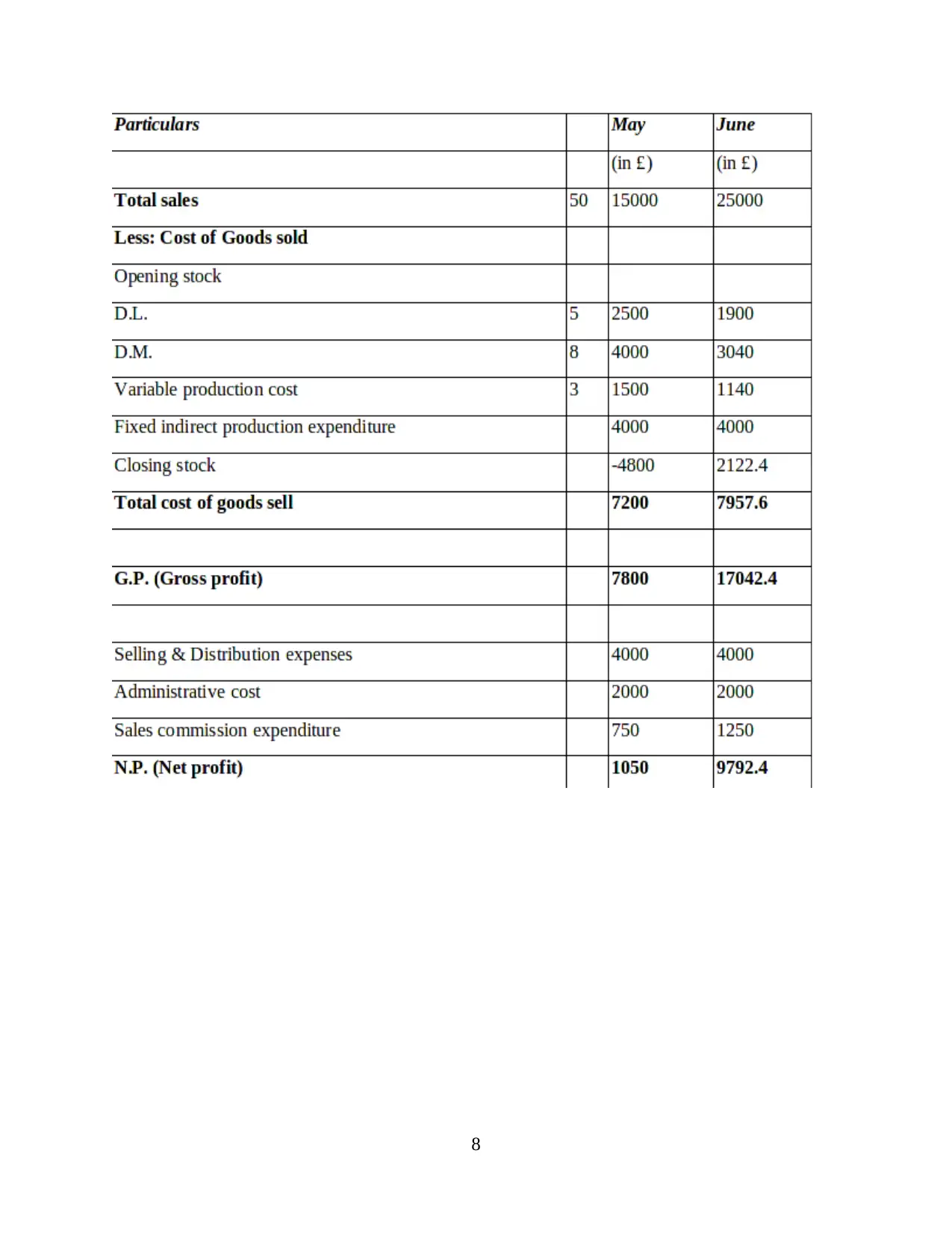

Marginal costing : It refers to increase and decrease in the price of product through which

there is changes in the cost of organisation production process. This refers to the cost that is used for

producing specific units in the organisation. Sometimes there is change in variable cost of

organisation but fixed cost is always stable for all business (Gibassier and Schaltegger, 2015).

Calculation of profit using marginal costing:

Income statement under Marginal costing method for month of May & June

6

calculate the amount that is expense by them for conducting particular project. They provides

whole detail that is invested by them in order to complete their operations. It is important for

HSBC to measure and control the cost that is unnecessarily increases the expenses of

organisation.

Inventory Managerial Report- This is the report which is managed by supervisors in

an organisation which considers about the availability of raw materials that is present in the

organisation. It is beneficial for HSBC because it helps them to deliver quick services in the

market. Along with this it helps them to manage raw material which are required to produce

goods.

TASK 2

P3 Appropriate techniques of cost analysis to prepare income statement for HSBC

COST: The term cost includes all factors that are measured on monetary basis. This refers to

the amount that are essential to paid for purchasing any item inside the organisation. Usually cost is

the evaluation of efforts, machine, materials, resources etc. that are essential for organisation to

manufacture a product or service (Gond and et. al., 2012). Moreover cost is the amount that is

required to complete a business or job. Marginal and absorption are two type of cost that helps an

organisation to prepare income statement.

Marginal costing : It refers to increase and decrease in the price of product through which

there is changes in the cost of organisation production process. This refers to the cost that is used for

producing specific units in the organisation. Sometimes there is change in variable cost of

organisation but fixed cost is always stable for all business (Gibassier and Schaltegger, 2015).

Calculation of profit using marginal costing:

Income statement under Marginal costing method for month of May & June

6

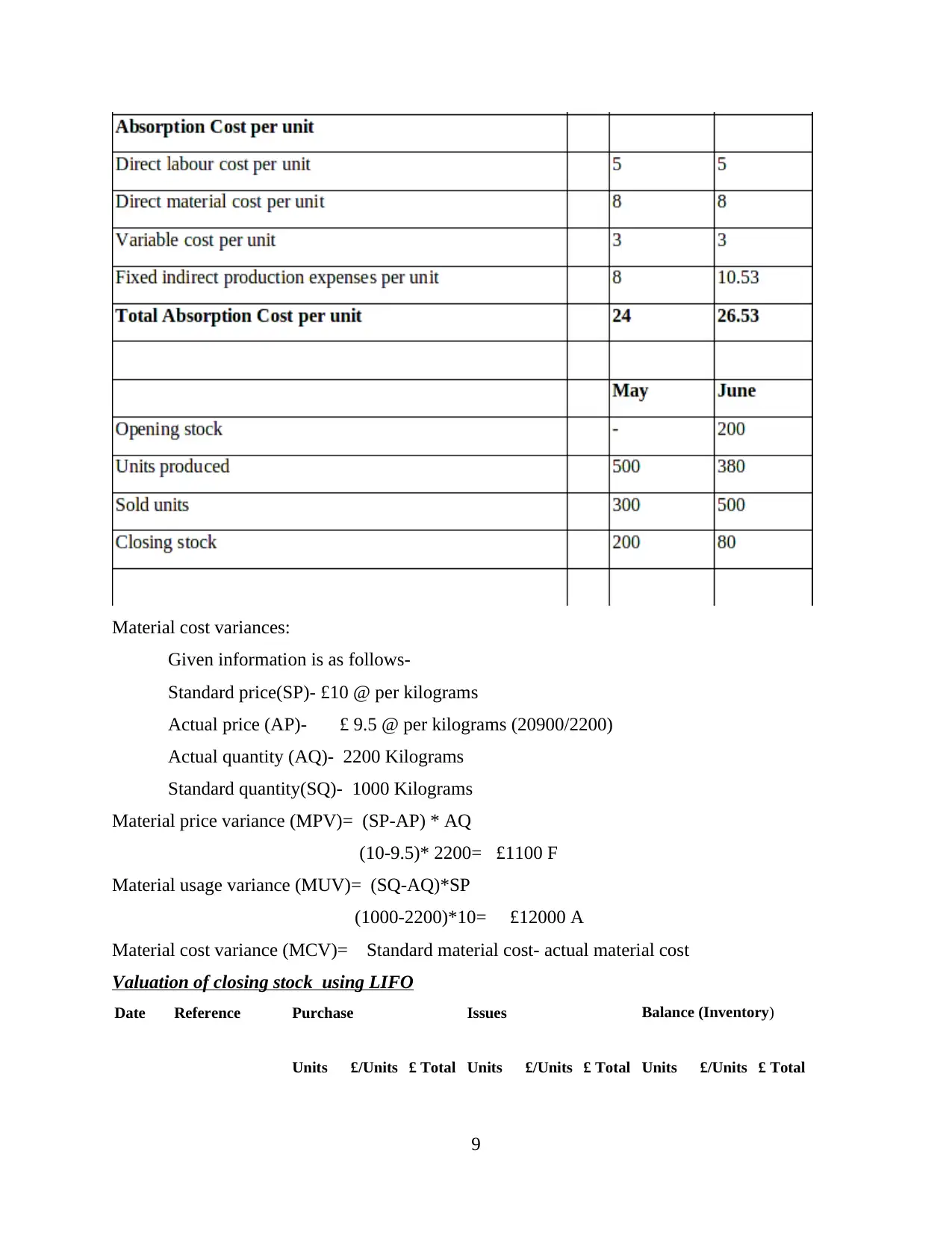

Absorption costing: It refer to a cost accounting method that is used for find out the current

inventory value. For this is includes variable as well as fixed cost that is incurred during the

production process which governs that it include direct and in-direct cost, overhead cost etc. that is

used to measure the value of inventory.

Calculation of profit using absorption costing

7

inventory value. For this is includes variable as well as fixed cost that is incurred during the

production process which governs that it include direct and in-direct cost, overhead cost etc. that is

used to measure the value of inventory.

Calculation of profit using absorption costing

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

(10-9.5)* 2200= £1100 F

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

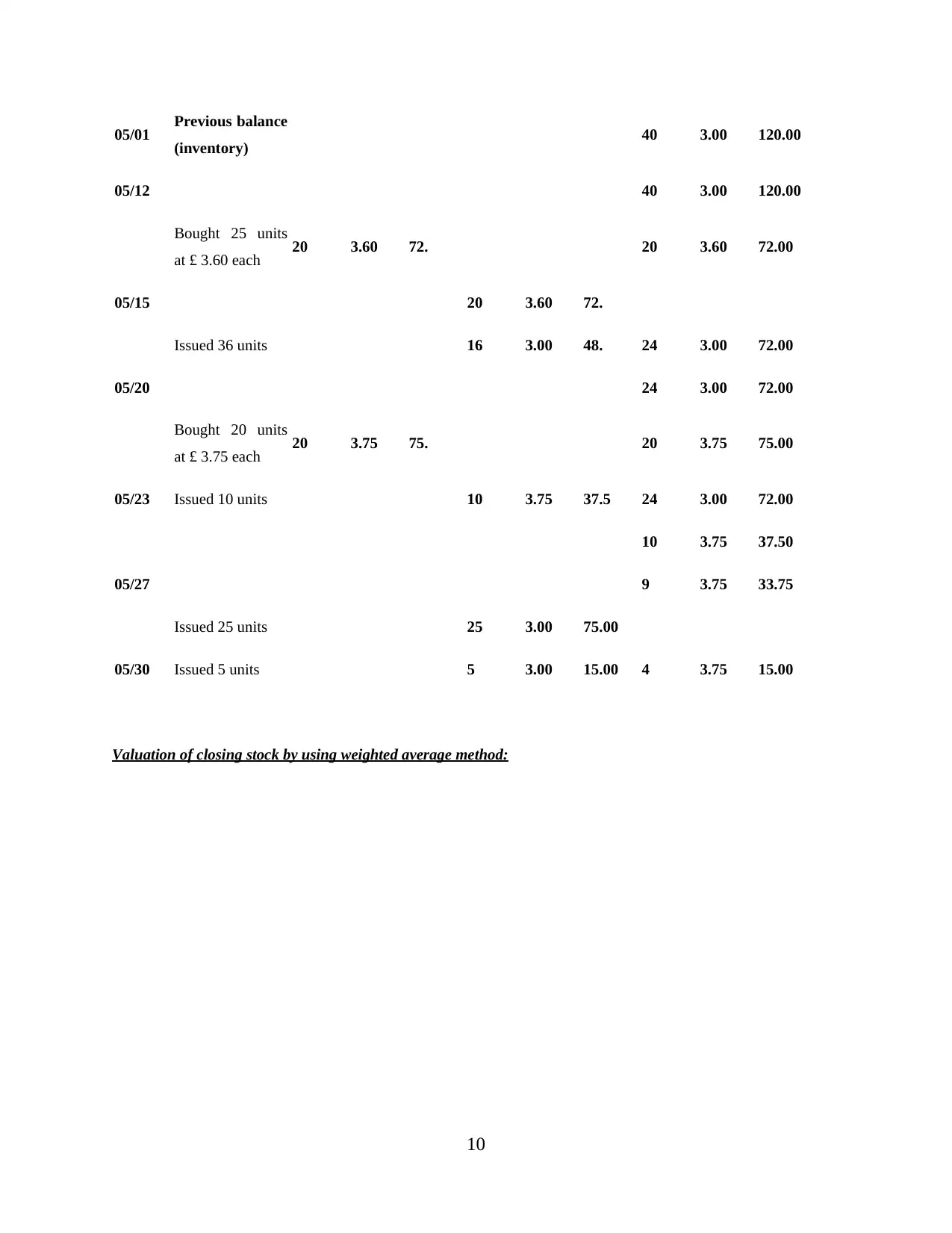

Valuation of closing stock using LIFO

Date Reference Purchase Issues Balance (Inventory)

Units £/Units £ Total Units £/Units £ Total Units £/Units £ Total

9

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

(10-9.5)* 2200= £1100 F

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

Valuation of closing stock using LIFO

Date Reference Purchase Issues Balance (Inventory)

Units £/Units £ Total Units £/Units £ Total Units £/Units £ Total

9

05/01 Previous balance

(inventory) 40 3.00 120.00

05/12 40 3.00 120.00

Bought 25 units

at £ 3.60 each 20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units

at £ 3.75 each 20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

Valuation of closing stock by using weighted average method:

10

(inventory) 40 3.00 120.00

05/12 40 3.00 120.00

Bought 25 units

at £ 3.60 each 20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units

at £ 3.75 each 20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

Valuation of closing stock by using weighted average method:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.