Management Accounting Report: Financial Analysis of IKEA Operations

VerifiedAdded on 2020/11/12

|20

|6153

|376

Report

AI Summary

This report delves into the management accounting practices of IKEA, a global furniture and home goods retailer. It begins by defining management accounting and outlining its requirements, exploring various systems like cost accounting, price optimization, job costing, and inventory management. The report then details management accounting reporting methods, including budget reports, accounts receivable reports, cost accounting reports, and job cost reports, highlighting their benefits and applications within IKEA. Furthermore, it examines the advantages and disadvantages of budgetary control tools, such as cash budgets and flexible cost budgets, and demonstrates how these tools can be used for preparing and forecasting budgets. The report also covers the preparation of an income statement using marginal and absorption costing and concludes by discussing how IKEA adapts its management accounting systems to address financial problems. The analysis provides a comprehensive understanding of how IKEA utilizes management accounting for decision-making, cost control, and financial planning.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

LO 1.................................................................................................................................................3

P1. Management accounting meaning and requirements of different management accounting 3

Systems.......................................................................................................................................3

P2. Presenting different methods for management accounting reporting...................................5

M1. Benefits of management accounting systems and their application....................................6

D1. Evaluating management accounting systems and management accounting reporting is ....7

integrated within organisational processes..................................................................................7

LO 2.................................................................................................................................................7

P3. Calculating costs & preparing an income statement using marginal and absorption costs.. 7

M2. Producing management accounting techniques and financial reporting documents...........7

D2. Interpreting data..................................................................................................................7

LO 3.................................................................................................................................................7

P4 Explaining the advantages and disadvantages of different types of planing tools used in

budgetary control........................................................................................................................7

M3. Different planning tools and their application for preparing and forecasting budgets........9

D3. Evaluating planning tools for solving financial problems.................................................11

LO 4...............................................................................................................................................13

P5. Adapting management accounting systems to respond to financial problems...................13

M4. Analysing how management accounting responds to financial problems.........................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

LO 1.................................................................................................................................................3

P1. Management accounting meaning and requirements of different management accounting 3

Systems.......................................................................................................................................3

P2. Presenting different methods for management accounting reporting...................................5

M1. Benefits of management accounting systems and their application....................................6

D1. Evaluating management accounting systems and management accounting reporting is ....7

integrated within organisational processes..................................................................................7

LO 2.................................................................................................................................................7

P3. Calculating costs & preparing an income statement using marginal and absorption costs.. 7

M2. Producing management accounting techniques and financial reporting documents...........7

D2. Interpreting data..................................................................................................................7

LO 3.................................................................................................................................................7

P4 Explaining the advantages and disadvantages of different types of planing tools used in

budgetary control........................................................................................................................7

M3. Different planning tools and their application for preparing and forecasting budgets........9

D3. Evaluating planning tools for solving financial problems.................................................11

LO 4...............................................................................................................................................13

P5. Adapting management accounting systems to respond to financial problems...................13

M4. Analysing how management accounting responds to financial problems.........................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

The term Management Accounting is defined as the process which is concern with

preparation of reports, statements and accounts related to the business operations & processes

which provides information about finance, statistical data to the managers which assists in

decision making process. The report is about IKEA, a Swedish multinational company engage in

business of designing, selling ready-to-assemble furniture, kitchen appliances, home accessories

etc. This report will show the requirements of different management accounting systems along

with the benefits and application within an organization. It will also define management

accounting reporting methods adopt by organization. Further, the report will preparation of

income statement for IKEA using marginal and absorption costs along with its interpretation.

Budgetary control and its planning tools with its advantages and disadvantages used for

preparing and forecasting budgets will be explain in the report. At last, the report will disclose

how IKEA will adapt management accounting systems to solve various financial problems.

MAIN BODY

LO 1

Management accounting meaning and requirements of different management accounting

Systems.

Management Accounting is a term which involves activity related to identifying,

analysing, interpreting and communicating the important financial as well as statistical

information to the management of the organisation for successful accomplishment of

organisational goals and objectives. With the help of management accounting, managers are

capable of making business related decision either short term or long term (Boučková, 2015).

The Management accounting technique like budgeting helps in increasing the operational

efficiency and productivity of the business as managers can formulate effective plans and

strategies, take decision on time with accurate information available to them. Thus, it helps in

making business related plans, controlling cost, assessing the profit level to be achieved in the

product lines with the help of various cost analysis methods etc.

The term Management Accounting is defined as the process which is concern with

preparation of reports, statements and accounts related to the business operations & processes

which provides information about finance, statistical data to the managers which assists in

decision making process. The report is about IKEA, a Swedish multinational company engage in

business of designing, selling ready-to-assemble furniture, kitchen appliances, home accessories

etc. This report will show the requirements of different management accounting systems along

with the benefits and application within an organization. It will also define management

accounting reporting methods adopt by organization. Further, the report will preparation of

income statement for IKEA using marginal and absorption costs along with its interpretation.

Budgetary control and its planning tools with its advantages and disadvantages used for

preparing and forecasting budgets will be explain in the report. At last, the report will disclose

how IKEA will adapt management accounting systems to solve various financial problems.

MAIN BODY

LO 1

Management accounting meaning and requirements of different management accounting

Systems.

Management Accounting is a term which involves activity related to identifying,

analysing, interpreting and communicating the important financial as well as statistical

information to the management of the organisation for successful accomplishment of

organisational goals and objectives. With the help of management accounting, managers are

capable of making business related decision either short term or long term (Boučková, 2015).

The Management accounting technique like budgeting helps in increasing the operational

efficiency and productivity of the business as managers can formulate effective plans and

strategies, take decision on time with accurate information available to them. Thus, it helps in

making business related plans, controlling cost, assessing the profit level to be achieved in the

product lines with the help of various cost analysis methods etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are different types of management accounting systems which can be used by IKEA:

Cost Accounting System – It is a method which is used by IKEA for estimating the cost

expenses incurred for producing goods or cost of their products so as to ascertain the profitability

situation and performance level of the company. It helps IKEA in making the correct valuation

of inventory and controls the cost expenses incurred in conducting the business processes. There

are two main cost accounting system:

Process Costing Method – It is a method of costing which helps in collecting separately all

the manufacturing costs incurred for each process.

Job order Costing Method – This method of cost accounting system accumulates the cost

related to manufacturing process separately for every job. This method is suitable when the

company is engaged in the production business of unique or distinct products.

Price Optimisation System – This system of management accounting is a method which

helps IKEA in understanding how customers will behave towards different prices assigned its

products and services with the help of different channels for distribution (Cooper, D. J., Ezzamel

and Qu, 2017). It helps in determining the best suitable prices which can be charged from the

customers for its products and services which in turn helps the company in achieving its goals

and objectives of maximum profit with minimum cost of production.

Job Costing System – It is a process which helps IKEA in determining the cost and other

related information of some specific product or activity or job process for customer knowledge.

It involves Direct material, labour and overhead costs. This helps customer in cost

reimbursement as per the terms and conditions defined in contract (George, 2016). With the help

of this costing system IKEA can evaluate cost incurred for any stage of job work completed.

Inventory Management System – This system helps IKEA in assessing and keeping a

check or track products through entire area and supply chain where business operation takes

place. It thus ensures continuity of workflow activity & improvements required if any, evaluates

amount of inventory available & reorder the required quantity before stock out situation arises.

This system has two sub types:

1. LIFO - LIFO stands for Last in, first out in which last inventory item purchased is sold first.

Cost Accounting System – It is a method which is used by IKEA for estimating the cost

expenses incurred for producing goods or cost of their products so as to ascertain the profitability

situation and performance level of the company. It helps IKEA in making the correct valuation

of inventory and controls the cost expenses incurred in conducting the business processes. There

are two main cost accounting system:

Process Costing Method – It is a method of costing which helps in collecting separately all

the manufacturing costs incurred for each process.

Job order Costing Method – This method of cost accounting system accumulates the cost

related to manufacturing process separately for every job. This method is suitable when the

company is engaged in the production business of unique or distinct products.

Price Optimisation System – This system of management accounting is a method which

helps IKEA in understanding how customers will behave towards different prices assigned its

products and services with the help of different channels for distribution (Cooper, D. J., Ezzamel

and Qu, 2017). It helps in determining the best suitable prices which can be charged from the

customers for its products and services which in turn helps the company in achieving its goals

and objectives of maximum profit with minimum cost of production.

Job Costing System – It is a process which helps IKEA in determining the cost and other

related information of some specific product or activity or job process for customer knowledge.

It involves Direct material, labour and overhead costs. This helps customer in cost

reimbursement as per the terms and conditions defined in contract (George, 2016). With the help

of this costing system IKEA can evaluate cost incurred for any stage of job work completed.

Inventory Management System – This system helps IKEA in assessing and keeping a

check or track products through entire area and supply chain where business operation takes

place. It thus ensures continuity of workflow activity & improvements required if any, evaluates

amount of inventory available & reorder the required quantity before stock out situation arises.

This system has two sub types:

1. LIFO - LIFO stands for Last in, first out in which last inventory item purchased is sold first.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. FIFO - FIFO stands for First in, first out in which goods purchased first are the goods sold

first.

Presenting different methods for management accounting reporting.

The management accounting reporting is related with the budgeting and guides the

direction of the managers in offering the best incentives to the employee, cutting the cost,

negotiating with vendors and suppliers. The reports are crucial for business as many of the

decision depends on its is and also it measures the performance of the business. There are

different past of the management accounting reports prepared by an organization:

Budget reports: are prepared in every business irrespective of their small or large. For

small business is produced as a whole and for large organization department wise reports are

generated. This reports are responsible to measure the performance of IKEA by stating the

estimate based on previous experiences (Rich, Roberts and Zhang, 2016). The budgets list out all

the income and expenditure of the business. With this budget reports the IKEA tries to achieve

the goals and objectives by being in the prescribed limits of the fund.

Account receivable reports: are more helpful for those businesses which relies heavily

extension of the credits to other. The reports directly breaks down the balance remaining form

the clients and arrange them within the specific time period (Mogues and Caceres, 2018). This

assist the managers in identification of the defaulters and also in finding out the problems

associated with the collection process of the business. With identification of the current lending

position of the business the manager of IKEA can step towards transformation and change the

credit policy of the company. Along with this the debt amount which is requires to be written off

in an accounting period is also identified by these reports.

Cost accounting reports: are directly linked to the cost incurred on the manufactures of

good and products by IKEA. In this report overall cost breakdown is shown which is spent on

each category of the cost. The cost related to each product manufactured in the company is

bifurcated in material, labour and others overheads. The cost accounting report is related with

defines each element of the cost spent to produce a single unit of product. This includes the cost

incurred form he time of procurement of raw material till the time is sent our from the factory of

IKEA for selling it.

first.

Presenting different methods for management accounting reporting.

The management accounting reporting is related with the budgeting and guides the

direction of the managers in offering the best incentives to the employee, cutting the cost,

negotiating with vendors and suppliers. The reports are crucial for business as many of the

decision depends on its is and also it measures the performance of the business. There are

different past of the management accounting reports prepared by an organization:

Budget reports: are prepared in every business irrespective of their small or large. For

small business is produced as a whole and for large organization department wise reports are

generated. This reports are responsible to measure the performance of IKEA by stating the

estimate based on previous experiences (Rich, Roberts and Zhang, 2016). The budgets list out all

the income and expenditure of the business. With this budget reports the IKEA tries to achieve

the goals and objectives by being in the prescribed limits of the fund.

Account receivable reports: are more helpful for those businesses which relies heavily

extension of the credits to other. The reports directly breaks down the balance remaining form

the clients and arrange them within the specific time period (Mogues and Caceres, 2018). This

assist the managers in identification of the defaulters and also in finding out the problems

associated with the collection process of the business. With identification of the current lending

position of the business the manager of IKEA can step towards transformation and change the

credit policy of the company. Along with this the debt amount which is requires to be written off

in an accounting period is also identified by these reports.

Cost accounting reports: are directly linked to the cost incurred on the manufactures of

good and products by IKEA. In this report overall cost breakdown is shown which is spent on

each category of the cost. The cost related to each product manufactured in the company is

bifurcated in material, labour and others overheads. The cost accounting report is related with

defines each element of the cost spent to produce a single unit of product. This includes the cost

incurred form he time of procurement of raw material till the time is sent our from the factory of

IKEA for selling it.

Job cost reports: shows the expenses done on a specific project which is funded by

IKEA. The actual amount is then compared with the estimated revenues in order to evaluate the

performance of that job and its profitability (Smith, 2017). The job cost reports aids in

identification of the area with high earnings within the business and can divert it focuses on those

activities with putting in additional efforts which are more profitable. In this way the IKEA can

save time and resources from being wasted on jobs with low profits margins. This report

analyses the expenses incurred on a job while it is in the progress so the company can identify

the correct area of waste before cost spiral out of control.

Benefits of management accounting systems and their application.

Management accounting system is an internal system which helps in making evaluation

and assessment of business processes thereby preparing managerial reports and accounts which

aids managers in decision-making process.

Benefits of management accounting systems in IKEA are as follows:

Cost Accounting System – With the help of this system, IKEA can determine the cost

incurred in carrying on business operations, manufacturing processes and also helps in

ascertaining the cost of goods sold.

Price Optimisation System – It helps IKEA in analysing and understanding the pattern

of customer’s preferences for buying a product with different pricing which in turn help

the company in making decision related to pricing factor (Tucker and Schaltegger, 2016).

Job Costing System – It helps IKEA in monitoring and tracking the business

performance in relation with the operational efficiency, productivity, controlling cost

expenses.

Inventory Management System – This system of Inventory management helps in

tracking the level of inventory or stock available with IKEA for meeting customer

demand, orders, by making sales and delivery on time.

Evaluating management accounting systems and management accounting reporting is

integrated within organisational processes.

Budget Report – With the help of budget report IKEA can control its cost and expenses

related to business operations by preparing estimated budgets. By making budget

IKEA. The actual amount is then compared with the estimated revenues in order to evaluate the

performance of that job and its profitability (Smith, 2017). The job cost reports aids in

identification of the area with high earnings within the business and can divert it focuses on those

activities with putting in additional efforts which are more profitable. In this way the IKEA can

save time and resources from being wasted on jobs with low profits margins. This report

analyses the expenses incurred on a job while it is in the progress so the company can identify

the correct area of waste before cost spiral out of control.

Benefits of management accounting systems and their application.

Management accounting system is an internal system which helps in making evaluation

and assessment of business processes thereby preparing managerial reports and accounts which

aids managers in decision-making process.

Benefits of management accounting systems in IKEA are as follows:

Cost Accounting System – With the help of this system, IKEA can determine the cost

incurred in carrying on business operations, manufacturing processes and also helps in

ascertaining the cost of goods sold.

Price Optimisation System – It helps IKEA in analysing and understanding the pattern

of customer’s preferences for buying a product with different pricing which in turn help

the company in making decision related to pricing factor (Tucker and Schaltegger, 2016).

Job Costing System – It helps IKEA in monitoring and tracking the business

performance in relation with the operational efficiency, productivity, controlling cost

expenses.

Inventory Management System – This system of Inventory management helps in

tracking the level of inventory or stock available with IKEA for meeting customer

demand, orders, by making sales and delivery on time.

Evaluating management accounting systems and management accounting reporting is

integrated within organisational processes.

Budget Report – With the help of budget report IKEA can control its cost and expenses

related to business operations by preparing estimated budgets. By making budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company can compare actual outcomes with estimated budget for achieving goals &

objectives with maximum profitability with minimum cost of production and limited

budget amount.

Performance Report – It can help IKEA in monitoring, reviewing and evaluating the

performance level of the business operations & makes relevant decision. It helps

company in formulating suitable business strategies & plans for attainment of goals.

Cost Managerial Accounting Report – It helps IKEA in evaluating the costs of

producing a specific unit or group of units by considering direct raw material costs, direct

labour cost and overhead cost, and other costs (Boučková, 2015). It helps in making

realization of the cost and selling prices of the product and comparing for determining the

profit margins.

LO 2

Calculating costs & preparing an income statement using marginal and absorption costs.

Producing management accounting techniques and financial reporting documents

Interpreting data.

LO 3

Explaining the advantages and disadvantages of different types of planing tools used in

budgetary control

Budgetary control is defined as establishment of budgets relating to the responsibilities of

the executives to the acquirements of policy of IKEA. In this control system there is continuous

comparison of the actual and budgeted results in order to secure the individual actions of the

policy and activity and to provide a revisionary basis. The budgetary control is done through

various planning tools such a Zero bases budgets, cash budgets, fixed cost and flexible cost

budgets.

Cash budgeting:

The pros of the cash budgets are that it determines the cash requirement with IKEA in the

current as well future time, in order to meet the obligation of the company and to have funds to

objectives with maximum profitability with minimum cost of production and limited

budget amount.

Performance Report – It can help IKEA in monitoring, reviewing and evaluating the

performance level of the business operations & makes relevant decision. It helps

company in formulating suitable business strategies & plans for attainment of goals.

Cost Managerial Accounting Report – It helps IKEA in evaluating the costs of

producing a specific unit or group of units by considering direct raw material costs, direct

labour cost and overhead cost, and other costs (Boučková, 2015). It helps in making

realization of the cost and selling prices of the product and comparing for determining the

profit margins.

LO 2

Calculating costs & preparing an income statement using marginal and absorption costs.

Producing management accounting techniques and financial reporting documents

Interpreting data.

LO 3

Explaining the advantages and disadvantages of different types of planing tools used in

budgetary control

Budgetary control is defined as establishment of budgets relating to the responsibilities of

the executives to the acquirements of policy of IKEA. In this control system there is continuous

comparison of the actual and budgeted results in order to secure the individual actions of the

policy and activity and to provide a revisionary basis. The budgetary control is done through

various planning tools such a Zero bases budgets, cash budgets, fixed cost and flexible cost

budgets.

Cash budgeting:

The pros of the cash budgets are that it determines the cash requirement with IKEA in the

current as well future time, in order to meet the obligation of the company and to have funds to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

conduct the operations of the business (Maas, Schaltegger and Crutzen, 2016). This budgets

assist in avoiding the debt liability of the business as it allowed company to have cash to meet

the immediate debt obligations. This assist the organisation in making it more resourceful by

eliminating the wastage and unnecessary use of the money. The cons of cash budgeting are that it

create a danger of theft and limits the spending power of the IKEA. The budgeted spending

when compared with actual expenses a huge difference can be seen sometimes and that create a

panic situation in the business.

Flexible cost budgeting:

The benefits of flexible budgets can be defined as it possess the quality of adaptability

with the real and constant changes. A flexible budget is one that is allowed to adjust based on a

change in the assumptions used to create the budget during management's planning process of

IKEA. All the expenses which are seasonal are considered by this budget. This allows the

avoidance of limits of missing opportunities of saving money. The drawbacks of this budgeting

are that it is quite confusing as it requires regular planning in order to track the expenses and

adjust the difference accordingly (Boiral, 2016). In preparation of flexible budgets more rules are

there, to be followed which increase the chance of them being bent or broken. This budgets are

less disciplined over the static budget as there is no strict requirement and rigid program to

adhere to the policies. This system is unlikely to foster the same discipline for a long term in the

IKEA.

Zero-based-budgeting:

The advantage of zero based budgeting can be summarised as it makes sure that

managers are accountable for what they spent in every financial year. In this the budgets are

prepared from the Zero base this directly mitigate the chances of misallocation of the resources

in various departments of the company (Maas, Schaltegger and Crutzen, 2016). The

disadvantage of this planning tool for budgetary control can be outlines as it give influence to the

short term thinking and golds and shift the direction of the long term objectives of the IKEA.

This can effect the objective achievement capacity of the company. This budgeting is resources

intensive which means it takes more time and efforts in reviewing and justifying the budgets.

This budget do not justify the time cost of the business.

assist in avoiding the debt liability of the business as it allowed company to have cash to meet

the immediate debt obligations. This assist the organisation in making it more resourceful by

eliminating the wastage and unnecessary use of the money. The cons of cash budgeting are that it

create a danger of theft and limits the spending power of the IKEA. The budgeted spending

when compared with actual expenses a huge difference can be seen sometimes and that create a

panic situation in the business.

Flexible cost budgeting:

The benefits of flexible budgets can be defined as it possess the quality of adaptability

with the real and constant changes. A flexible budget is one that is allowed to adjust based on a

change in the assumptions used to create the budget during management's planning process of

IKEA. All the expenses which are seasonal are considered by this budget. This allows the

avoidance of limits of missing opportunities of saving money. The drawbacks of this budgeting

are that it is quite confusing as it requires regular planning in order to track the expenses and

adjust the difference accordingly (Boiral, 2016). In preparation of flexible budgets more rules are

there, to be followed which increase the chance of them being bent or broken. This budgets are

less disciplined over the static budget as there is no strict requirement and rigid program to

adhere to the policies. This system is unlikely to foster the same discipline for a long term in the

IKEA.

Zero-based-budgeting:

The advantage of zero based budgeting can be summarised as it makes sure that

managers are accountable for what they spent in every financial year. In this the budgets are

prepared from the Zero base this directly mitigate the chances of misallocation of the resources

in various departments of the company (Maas, Schaltegger and Crutzen, 2016). The

disadvantage of this planning tool for budgetary control can be outlines as it give influence to the

short term thinking and golds and shift the direction of the long term objectives of the IKEA.

This can effect the objective achievement capacity of the company. This budgeting is resources

intensive which means it takes more time and efforts in reviewing and justifying the budgets.

This budget do not justify the time cost of the business.

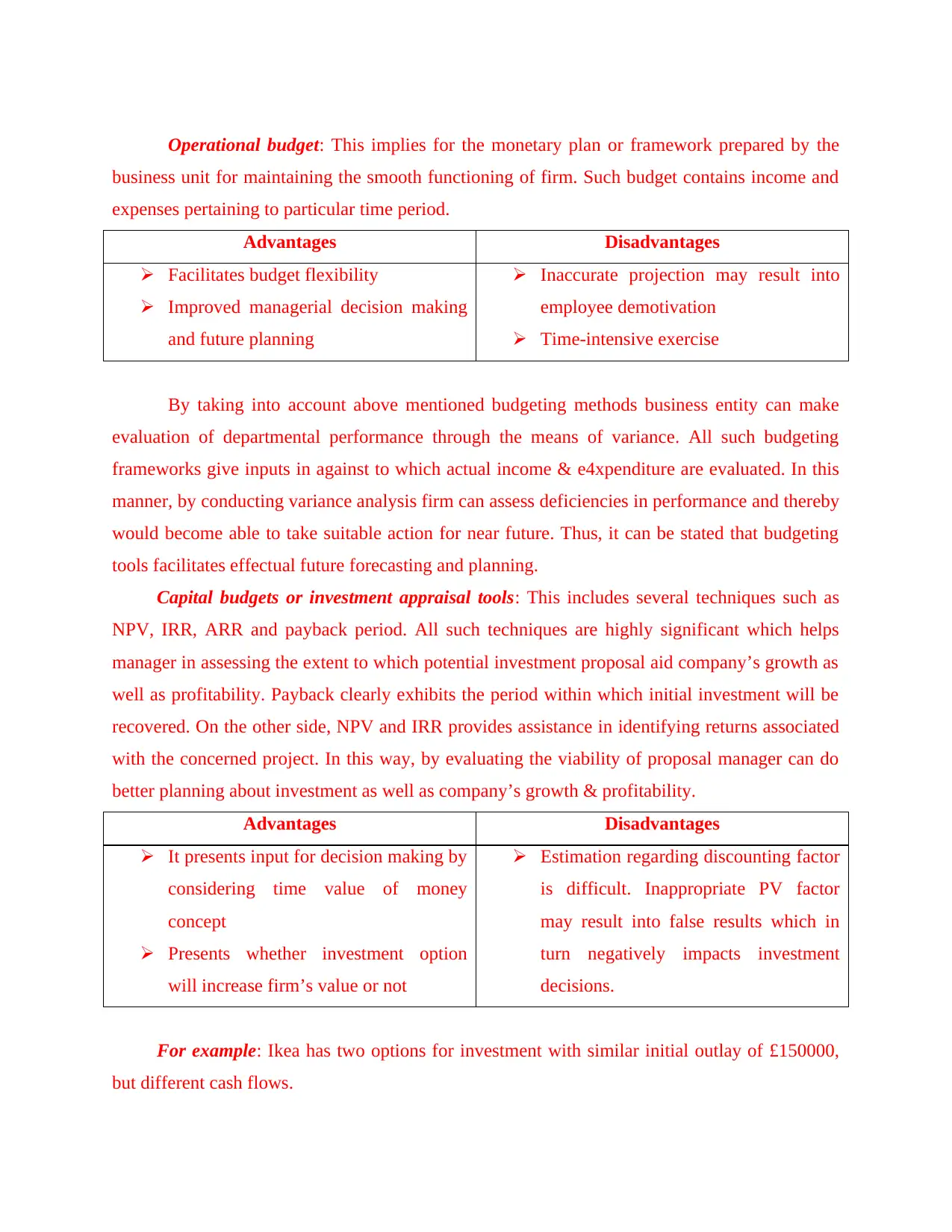

Operational budget: This implies for the monetary plan or framework prepared by the

business unit for maintaining the smooth functioning of firm. Such budget contains income and

expenses pertaining to particular time period.

Advantages Disadvantages

Facilitates budget flexibility

Improved managerial decision making

and future planning

Inaccurate projection may result into

employee demotivation

Time-intensive exercise

By taking into account above mentioned budgeting methods business entity can make

evaluation of departmental performance through the means of variance. All such budgeting

frameworks give inputs in against to which actual income & e4xpenditure are evaluated. In this

manner, by conducting variance analysis firm can assess deficiencies in performance and thereby

would become able to take suitable action for near future. Thus, it can be stated that budgeting

tools facilitates effectual future forecasting and planning.

Capital budgets or investment appraisal tools: This includes several techniques such as

NPV, IRR, ARR and payback period. All such techniques are highly significant which helps

manager in assessing the extent to which potential investment proposal aid company’s growth as

well as profitability. Payback clearly exhibits the period within which initial investment will be

recovered. On the other side, NPV and IRR provides assistance in identifying returns associated

with the concerned project. In this way, by evaluating the viability of proposal manager can do

better planning about investment as well as company’s growth & profitability.

Advantages Disadvantages

It presents input for decision making by

considering time value of money

concept

Presents whether investment option

will increase firm’s value or not

Estimation regarding discounting factor

is difficult. Inappropriate PV factor

may result into false results which in

turn negatively impacts investment

decisions.

For example: Ikea has two options for investment with similar initial outlay of £150000,

but different cash flows.

business unit for maintaining the smooth functioning of firm. Such budget contains income and

expenses pertaining to particular time period.

Advantages Disadvantages

Facilitates budget flexibility

Improved managerial decision making

and future planning

Inaccurate projection may result into

employee demotivation

Time-intensive exercise

By taking into account above mentioned budgeting methods business entity can make

evaluation of departmental performance through the means of variance. All such budgeting

frameworks give inputs in against to which actual income & e4xpenditure are evaluated. In this

manner, by conducting variance analysis firm can assess deficiencies in performance and thereby

would become able to take suitable action for near future. Thus, it can be stated that budgeting

tools facilitates effectual future forecasting and planning.

Capital budgets or investment appraisal tools: This includes several techniques such as

NPV, IRR, ARR and payback period. All such techniques are highly significant which helps

manager in assessing the extent to which potential investment proposal aid company’s growth as

well as profitability. Payback clearly exhibits the period within which initial investment will be

recovered. On the other side, NPV and IRR provides assistance in identifying returns associated

with the concerned project. In this way, by evaluating the viability of proposal manager can do

better planning about investment as well as company’s growth & profitability.

Advantages Disadvantages

It presents input for decision making by

considering time value of money

concept

Presents whether investment option

will increase firm’s value or not

Estimation regarding discounting factor

is difficult. Inappropriate PV factor

may result into false results which in

turn negatively impacts investment

decisions.

For example: Ikea has two options for investment with similar initial outlay of £150000,

but different cash flows.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

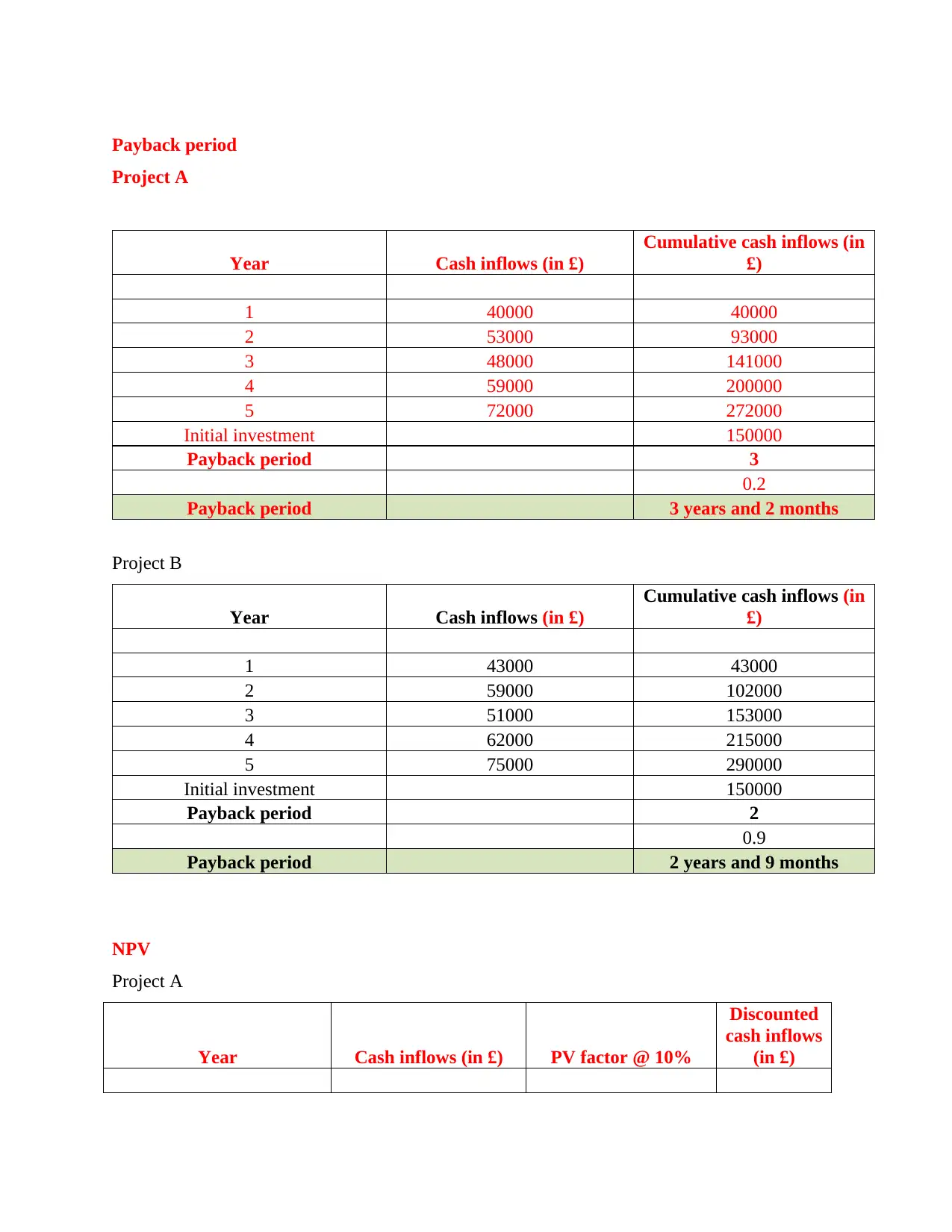

Payback period

Project A

Year Cash inflows (in £)

Cumulative cash inflows (in

£)

1 40000 40000

2 53000 93000

3 48000 141000

4 59000 200000

5 72000 272000

Initial investment 150000

Payback period 3

0.2

Payback period 3 years and 2 months

Project B

Year Cash inflows (in £)

Cumulative cash inflows (in

£)

1 43000 43000

2 59000 102000

3 51000 153000

4 62000 215000

5 75000 290000

Initial investment 150000

Payback period 2

0.9

Payback period 2 years and 9 months

NPV

Project A

Year Cash inflows (in £) PV factor @ 10%

Discounted

cash inflows

(in £)

Project A

Year Cash inflows (in £)

Cumulative cash inflows (in

£)

1 40000 40000

2 53000 93000

3 48000 141000

4 59000 200000

5 72000 272000

Initial investment 150000

Payback period 3

0.2

Payback period 3 years and 2 months

Project B

Year Cash inflows (in £)

Cumulative cash inflows (in

£)

1 43000 43000

2 59000 102000

3 51000 153000

4 62000 215000

5 75000 290000

Initial investment 150000

Payback period 2

0.9

Payback period 2 years and 9 months

NPV

Project A

Year Cash inflows (in £) PV factor @ 10%

Discounted

cash inflows

(in £)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 40000 0.909 36363.63

2 53000 0.826 43802

3 48000 0.751 36063

4 59000 0.683 40298

5 72000 0.621 44706

Total discounted cash

inflow 201233

Initial investment 150000

NPV (Total discounted

cash inflows - initial

investment) 51233

Project B

Year Cash inflows (in £) PV factor @ 10%

Discounted

cash inflows

(in £)

1 43000 0.909 39090.90

2 59000 0.826 48760

3 51000 0.751 38317

4 62000 0.683 42347

5 75000 0.621 46569

Total discounted cash

inflow 215084

Initial investment 150000

NPV (Total discounted

cash inflows - initial

investment) 65084

IRR

Project A

Year Cash inflows (in £)

0 -150000

1 40000

2 53000

3 48000

4 59000

5 72000

2 53000 0.826 43802

3 48000 0.751 36063

4 59000 0.683 40298

5 72000 0.621 44706

Total discounted cash

inflow 201233

Initial investment 150000

NPV (Total discounted

cash inflows - initial

investment) 51233

Project B

Year Cash inflows (in £) PV factor @ 10%

Discounted

cash inflows

(in £)

1 43000 0.909 39090.90

2 59000 0.826 48760

3 51000 0.751 38317

4 62000 0.683 42347

5 75000 0.621 46569

Total discounted cash

inflow 215084

Initial investment 150000

NPV (Total discounted

cash inflows - initial

investment) 65084

IRR

Project A

Year Cash inflows (in £)

0 -150000

1 40000

2 53000

3 48000

4 59000

5 72000

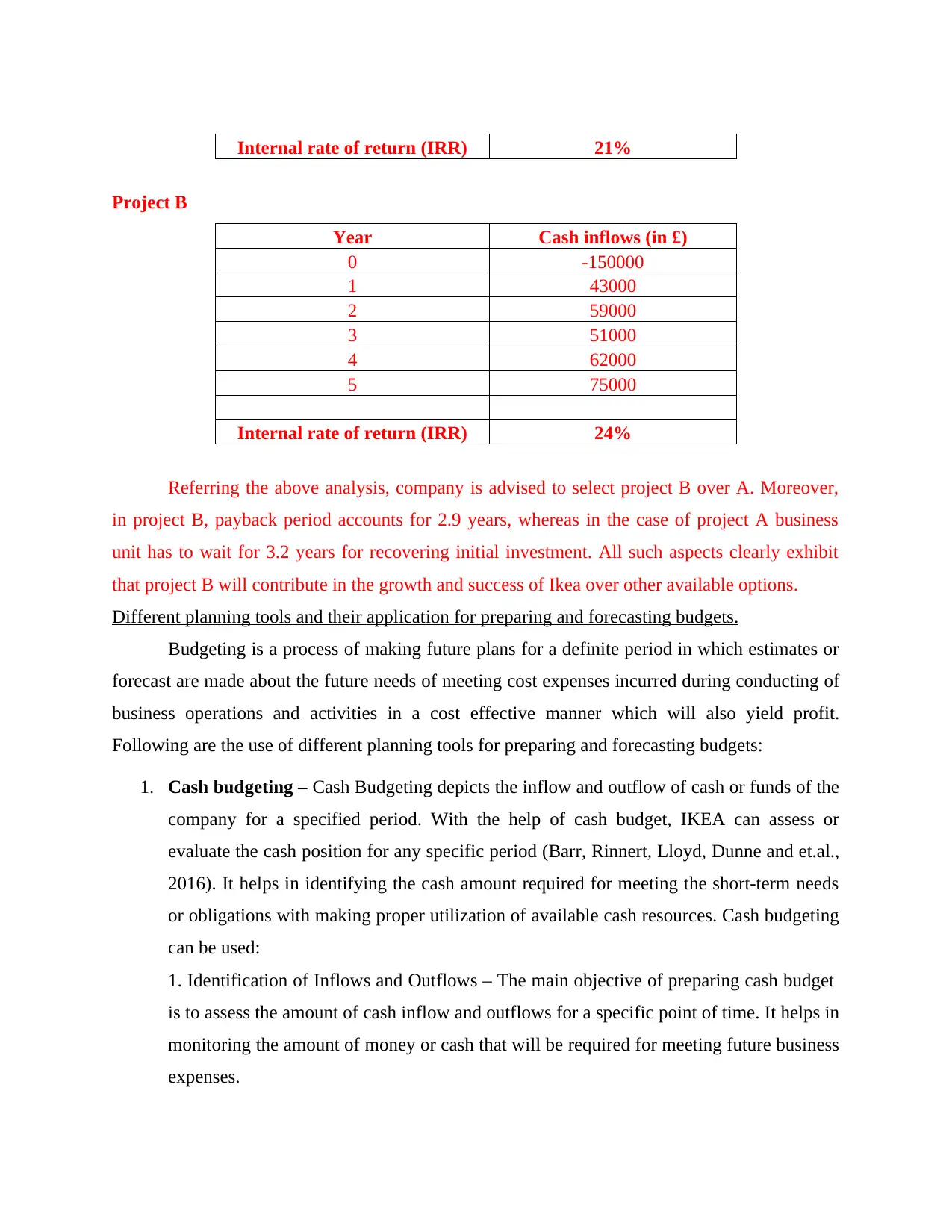

Internal rate of return (IRR) 21%

Project B

Year Cash inflows (in £)

0 -150000

1 43000

2 59000

3 51000

4 62000

5 75000

Internal rate of return (IRR) 24%

Referring the above analysis, company is advised to select project B over A. Moreover,

in project B, payback period accounts for 2.9 years, whereas in the case of project A business

unit has to wait for 3.2 years for recovering initial investment. All such aspects clearly exhibit

that project B will contribute in the growth and success of Ikea over other available options.

Different planning tools and their application for preparing and forecasting budgets.

Budgeting is a process of making future plans for a definite period in which estimates or

forecast are made about the future needs of meeting cost expenses incurred during conducting of

business operations and activities in a cost effective manner which will also yield profit.

Following are the use of different planning tools for preparing and forecasting budgets:

1. Cash budgeting – Cash Budgeting depicts the inflow and outflow of cash or funds of the

company for a specified period. With the help of cash budget, IKEA can assess or

evaluate the cash position for any specific period (Barr, Rinnert, Lloyd, Dunne and et.al.,

2016). It helps in identifying the cash amount required for meeting the short-term needs

or obligations with making proper utilization of available cash resources. Cash budgeting

can be used:

1. Identification of Inflows and Outflows – The main objective of preparing cash budget

is to assess the amount of cash inflow and outflows for a specific point of time. It helps in

monitoring the amount of money or cash that will be required for meeting future business

expenses.

Project B

Year Cash inflows (in £)

0 -150000

1 43000

2 59000

3 51000

4 62000

5 75000

Internal rate of return (IRR) 24%

Referring the above analysis, company is advised to select project B over A. Moreover,

in project B, payback period accounts for 2.9 years, whereas in the case of project A business

unit has to wait for 3.2 years for recovering initial investment. All such aspects clearly exhibit

that project B will contribute in the growth and success of Ikea over other available options.

Different planning tools and their application for preparing and forecasting budgets.

Budgeting is a process of making future plans for a definite period in which estimates or

forecast are made about the future needs of meeting cost expenses incurred during conducting of

business operations and activities in a cost effective manner which will also yield profit.

Following are the use of different planning tools for preparing and forecasting budgets:

1. Cash budgeting – Cash Budgeting depicts the inflow and outflow of cash or funds of the

company for a specified period. With the help of cash budget, IKEA can assess or

evaluate the cash position for any specific period (Barr, Rinnert, Lloyd, Dunne and et.al.,

2016). It helps in identifying the cash amount required for meeting the short-term needs

or obligations with making proper utilization of available cash resources. Cash budgeting

can be used:

1. Identification of Inflows and Outflows – The main objective of preparing cash budget

is to assess the amount of cash inflow and outflows for a specific point of time. It helps in

monitoring the amount of money or cash that will be required for meeting future business

expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.