Financial Analysis: Management Accounting Report for Imda Tech

VerifiedAdded on 2020/07/23

|18

|5292

|160

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application within Imda Tech (UK) Ltd, a manufacturing company. The report begins by differentiating between management and financial accounting, highlighting their distinct purposes and applications. It then delves into the practical application of costing methods, including the computation of income statements using both absorption costing and marginal costing. The report further explores various budgeting types, outlining their advantages and disadvantages, and the processes involved in budget preparation. Additionally, it examines pricing strategies relevant to Imda Tech. Finally, the report discusses the balanced scorecard approach and its implementation in delivering performance measures, offering a comprehensive overview of management accounting tools and techniques for financial decision-making and performance improvement. The report concludes by providing references for all the content included.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) (I) Definition of management accounting and difference between management accounting

and financial accounting.............................................................................................................1

a) (II) Significance of management accounting when used as decision making tool.................2

TASK 2............................................................................................................................................5

Computation of Absorption costing............................................................................................5

Computation of marginal costing................................................................................................6

TASK 3............................................................................................................................................6

(a) Types of budget and its advantages and disadvantages.........................................................6

(b) Process involved in preparation of budget............................................................................7

(c) Pricing strategies....................................................................................................................8

TASK 4............................................................................................................................................9

a) Balanced Scorecard approach and its implementation in delivering performance measures. 9

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) (I) Definition of management accounting and difference between management accounting

and financial accounting.............................................................................................................1

a) (II) Significance of management accounting when used as decision making tool.................2

TASK 2............................................................................................................................................5

Computation of Absorption costing............................................................................................5

Computation of marginal costing................................................................................................6

TASK 3............................................................................................................................................6

(a) Types of budget and its advantages and disadvantages.........................................................6

(b) Process involved in preparation of budget............................................................................7

(c) Pricing strategies....................................................................................................................8

TASK 4............................................................................................................................................9

a) Balanced Scorecard approach and its implementation in delivering performance measures. 9

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is an important tool, used by the companies in decision making

process. It advises on short term and long term financial decisions of the company based on its

financial and non financial data. Imda Tech (UK) Ltd is a manufacturing company involved in

producing special charges for mobile telephones and other carry on gadgets that can be sold on

retail outlets of UK. The report discusses difference between management accounting and

financial accounting (Tucker and Lowe, 2014). Further it focuses on calculation of income

statement based on two methods that is absorption costing and marginal costing for Imda Tech

Ltd. Moreover, various types of budgets and budget process is discussed in the report. Moreover,

pricing strategies are suggested to Imda Ltd that can be adopted to sell chargers and other

gadgets to the customers. In the end, the report ponders on the use of balanced scorecard and

discuss the effect of its implementation on improving the performance of the company.

TASK 1

a) (I) Definition of management accounting and difference between management accounting and

financial accounting

Management accounting is a combination of accounts, finance and management where

business skills are used to add value to the organisation. It is a framework to identify, analyse

measure, interpret and communicate information in order to achieve organisational goals.

Management accountants are competent enough to give advice not only on financial issues but

also takeupon the big business decisions, formulate strategies and monitor risk (Boyns and

Edwards, 2013). Managers use financial information to make short term decisions for day to day

operations. They generate weekly or monthly report which shows availability of cash, sales

revenues, debt outstanding, trend chart, variance analysis etc. These informations are used to

create a metrics and evaluate business performance.

There are various differences between financial accounting and management accounting.

Some differences are listed below:

Financial Accounting Management accounting

Preparation of report based on past trends in

order to fulfil reporting requirements.

Uses the information of revenue, cash flow,

assets and debts to generate the trend report

and produce statistics which is helpful in

1

Management accounting is an important tool, used by the companies in decision making

process. It advises on short term and long term financial decisions of the company based on its

financial and non financial data. Imda Tech (UK) Ltd is a manufacturing company involved in

producing special charges for mobile telephones and other carry on gadgets that can be sold on

retail outlets of UK. The report discusses difference between management accounting and

financial accounting (Tucker and Lowe, 2014). Further it focuses on calculation of income

statement based on two methods that is absorption costing and marginal costing for Imda Tech

Ltd. Moreover, various types of budgets and budget process is discussed in the report. Moreover,

pricing strategies are suggested to Imda Ltd that can be adopted to sell chargers and other

gadgets to the customers. In the end, the report ponders on the use of balanced scorecard and

discuss the effect of its implementation on improving the performance of the company.

TASK 1

a) (I) Definition of management accounting and difference between management accounting and

financial accounting

Management accounting is a combination of accounts, finance and management where

business skills are used to add value to the organisation. It is a framework to identify, analyse

measure, interpret and communicate information in order to achieve organisational goals.

Management accountants are competent enough to give advice not only on financial issues but

also takeupon the big business decisions, formulate strategies and monitor risk (Boyns and

Edwards, 2013). Managers use financial information to make short term decisions for day to day

operations. They generate weekly or monthly report which shows availability of cash, sales

revenues, debt outstanding, trend chart, variance analysis etc. These informations are used to

create a metrics and evaluate business performance.

There are various differences between financial accounting and management accounting.

Some differences are listed below:

Financial Accounting Management accounting

Preparation of report based on past trends in

order to fulfil reporting requirements.

Uses the information of revenue, cash flow,

assets and debts to generate the trend report

and produce statistics which is helpful in

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

taking business decisions.

Generate the financial information so that it

can be used by various other departments

functioning in the company.

UseConsiders the financial information to

display the complete picture of the business

which act as a success parameter while

comparing the businesses.

The financial produced are based on past

finance trends of the company.

It is based on current and future trends and

therefore, the results are not exact (Parker,

2012). Various factors such as economical and

legal factors are considered while forecasting

financial for the company.

Financial accounting is produced for the sake

of external stakeholders in order to convey

company's financial position.

Management accounting is produced for

internal use.

It is precise and follow the principle of

Generally Accepted Accounting Principles

(GAAPs)

It is more dependent on estimates and forecasts

rather than using exact numbers while taking

decisions.

a) (II) Significance of management accounting when used as decision making tool

Management accounting plays vital role in decision making process. This tool is used by

every department before reaching to any conclusion. It helps to take sound decisions for the

business. Imda should use this important tool of decision making because:

It takes care of inflow and outflow of cash and plan cash wise financing based on short

term and long term strategies of the company. For instance, analysing the current ratio

which is calculated by dividing current assets and current liabilities (Bodie, 2013). It

verifies that whether the business will be able to meets its short term debts with the

available current assets.

It helps to estimate income and expenses of the company at a certain point of time. It

ensures that the business is going on track and as per the plan of the managers. It helps to

determine that the company have sufficient revenues and is running into profits. If not,

the Imda Tech is required to take necessary steps to improve business conditions.

2

Generate the financial information so that it

can be used by various other departments

functioning in the company.

UseConsiders the financial information to

display the complete picture of the business

which act as a success parameter while

comparing the businesses.

The financial produced are based on past

finance trends of the company.

It is based on current and future trends and

therefore, the results are not exact (Parker,

2012). Various factors such as economical and

legal factors are considered while forecasting

financial for the company.

Financial accounting is produced for the sake

of external stakeholders in order to convey

company's financial position.

Management accounting is produced for

internal use.

It is precise and follow the principle of

Generally Accepted Accounting Principles

(GAAPs)

It is more dependent on estimates and forecasts

rather than using exact numbers while taking

decisions.

a) (II) Significance of management accounting when used as decision making tool

Management accounting plays vital role in decision making process. This tool is used by

every department before reaching to any conclusion. It helps to take sound decisions for the

business. Imda should use this important tool of decision making because:

It takes care of inflow and outflow of cash and plan cash wise financing based on short

term and long term strategies of the company. For instance, analysing the current ratio

which is calculated by dividing current assets and current liabilities (Bodie, 2013). It

verifies that whether the business will be able to meets its short term debts with the

available current assets.

It helps to estimate income and expenses of the company at a certain point of time. It

ensures that the business is going on track and as per the plan of the managers. It helps to

determine that the company have sufficient revenues and is running into profits. If not,

the Imda Tech is required to take necessary steps to improve business conditions.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It helps to read the generated reports and take decisions based on them. For instance, if

the budgeted sales on the company are way more than that of actual sales, the company

have to investigate the reason of variance in order to get the budgeted and actual sales

equal.

It helps to ascertain losses or risks beforehand, which further prevents the company from

bad financials.

It helps to take cost control measures which can further reduce the prices for ultimate

consumers (Renz, 2016). When the quality of the products are predetermined then it

becomes easy to produce quality goods and transfer it to ultimate consumers.

Management accounts are helpful in making important decisions forof the company

based on the financials present in front of the management accountants. It also measures

the performance of each department by comparing actual cost with that of standard cost.

The deviations found between the cost can be termed as good or bad conditions based on

the favourable and unfavourable values.

Management accounting helps to increase the efficiency of the business by evaluating the

risk beforehand and take important measures to achieve the organisational goals (Soin

and Collier, 2013).

b) There are different types of management accounting systems. Some of them are mentioned

below: Cost accounting system: It is a toolprocess to estimate the cost of a product in order to

analyse profits, evaluate inventory and control cost of the product. It is important to

estimate correct cost of the product in order to evaluateidentify if the product is profitable

or not. Further, the cost of the product helps the company to evaluate the closing

inventory value, work in progress, finished goods for the purpose of preparing financial

statements (Otley and Emmanuel, 2013). Cost can be of three types:

◦ Actual cost: The amount actually occurred in opposition to that of estimated amount.

Cost of actual direct labour cost, material cost or predetermined overheads on

manufacturing are the actual costs incurred by Imda.

◦ Normal costing: In case of normal costing the cost of direct material and labour are

actual. However, the cost of overheads are estimated.

3

the budgeted sales on the company are way more than that of actual sales, the company

have to investigate the reason of variance in order to get the budgeted and actual sales

equal.

It helps to ascertain losses or risks beforehand, which further prevents the company from

bad financials.

It helps to take cost control measures which can further reduce the prices for ultimate

consumers (Renz, 2016). When the quality of the products are predetermined then it

becomes easy to produce quality goods and transfer it to ultimate consumers.

Management accounts are helpful in making important decisions forof the company

based on the financials present in front of the management accountants. It also measures

the performance of each department by comparing actual cost with that of standard cost.

The deviations found between the cost can be termed as good or bad conditions based on

the favourable and unfavourable values.

Management accounting helps to increase the efficiency of the business by evaluating the

risk beforehand and take important measures to achieve the organisational goals (Soin

and Collier, 2013).

b) There are different types of management accounting systems. Some of them are mentioned

below: Cost accounting system: It is a toolprocess to estimate the cost of a product in order to

analyse profits, evaluate inventory and control cost of the product. It is important to

estimate correct cost of the product in order to evaluateidentify if the product is profitable

or not. Further, the cost of the product helps the company to evaluate the closing

inventory value, work in progress, finished goods for the purpose of preparing financial

statements (Otley and Emmanuel, 2013). Cost can be of three types:

◦ Actual cost: The amount actually occurred in opposition to that of estimated amount.

Cost of actual direct labour cost, material cost or predetermined overheads on

manufacturing are the actual costs incurred by Imda.

◦ Normal costing: In case of normal costing the cost of direct material and labour are

actual. However, the cost of overheads are estimated.

3

◦ Standard costing: It is a tool to plan budgets, manage and control costs and evaluate

the performance of the management. It estimates the cost of production.

Inventory management systems: Use of desktops, barcode scanners and printers and

mobile devices is conducted to design and provide the management of inventory. It tracks

two main functions of warehouse that is receiving and shipping (Caglio and Ditillo,

2012). The main motive is to control the current inventory level and reduce the situation

of under stock and overstock. It improves the stock accuracy of the company and further

helps in smooth workflow. Imda can use this system to track its inventory level and take

smarter inventory decisions. Some functions of inventory management system are:

◦ Creating orders of purchase

◦ Receiving, allocating, adjusting and disposing the inventory

◦ Creating sales orders

◦ Picking, packing and shipping the product

◦ Counting the physical inventory available in the warehouse and evaluating cycle

counts.

◦ Printing barcode labels

Job costing systems: It is a process to collect information with respect to the cost

associated with the production of a specific product or service. Job costing system is used

when cost information is required to be submitted to the customer under the contract

when customer himself is going to bear the cost (Chenhall and Moers, 2015). It is

required to collect the following information, such as:

◦ Direct material

◦ Direct labour

◦ Overhead cost

This job costing system can be tailor-made according to the requirement of the customer

as some customer allow charging the cost from them, when buying a product.

Price optimising system: It is tool used by the company to assess the reaction of the

customers to different prices of the products and services using various channels. Based

on the evaluation it is assessed that which price of the product will serve the objectives of

the company to the maximum. For instance Imda can evaluate its pricing strategy of

chargers by adopting various methodologies (Lavia López and Hiebl, 2014). The price

4

the performance of the management. It estimates the cost of production.

Inventory management systems: Use of desktops, barcode scanners and printers and

mobile devices is conducted to design and provide the management of inventory. It tracks

two main functions of warehouse that is receiving and shipping (Caglio and Ditillo,

2012). The main motive is to control the current inventory level and reduce the situation

of under stock and overstock. It improves the stock accuracy of the company and further

helps in smooth workflow. Imda can use this system to track its inventory level and take

smarter inventory decisions. Some functions of inventory management system are:

◦ Creating orders of purchase

◦ Receiving, allocating, adjusting and disposing the inventory

◦ Creating sales orders

◦ Picking, packing and shipping the product

◦ Counting the physical inventory available in the warehouse and evaluating cycle

counts.

◦ Printing barcode labels

Job costing systems: It is a process to collect information with respect to the cost

associated with the production of a specific product or service. Job costing system is used

when cost information is required to be submitted to the customer under the contract

when customer himself is going to bear the cost (Chenhall and Moers, 2015). It is

required to collect the following information, such as:

◦ Direct material

◦ Direct labour

◦ Overhead cost

This job costing system can be tailor-made according to the requirement of the customer

as some customer allow charging the cost from them, when buying a product.

Price optimising system: It is tool used by the company to assess the reaction of the

customers to different prices of the products and services using various channels. Based

on the evaluation it is assessed that which price of the product will serve the objectives of

the company to the maximum. For instance Imda can evaluate its pricing strategy of

chargers by adopting various methodologies (Lavia López and Hiebl, 2014). The price

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

chosen should meet atleast basic demands of the product. It starts from segmentation of

the product that is to whom the product will be offered by the company. Imda can further

evaluate that how demand can vary at different level of pricing strategies. The company

can choose the point where it can fulfil the demand and also earn profits. Price optimising

technique helps to determine initial pricing, promotional pricing and discount pricing of a

product or service.

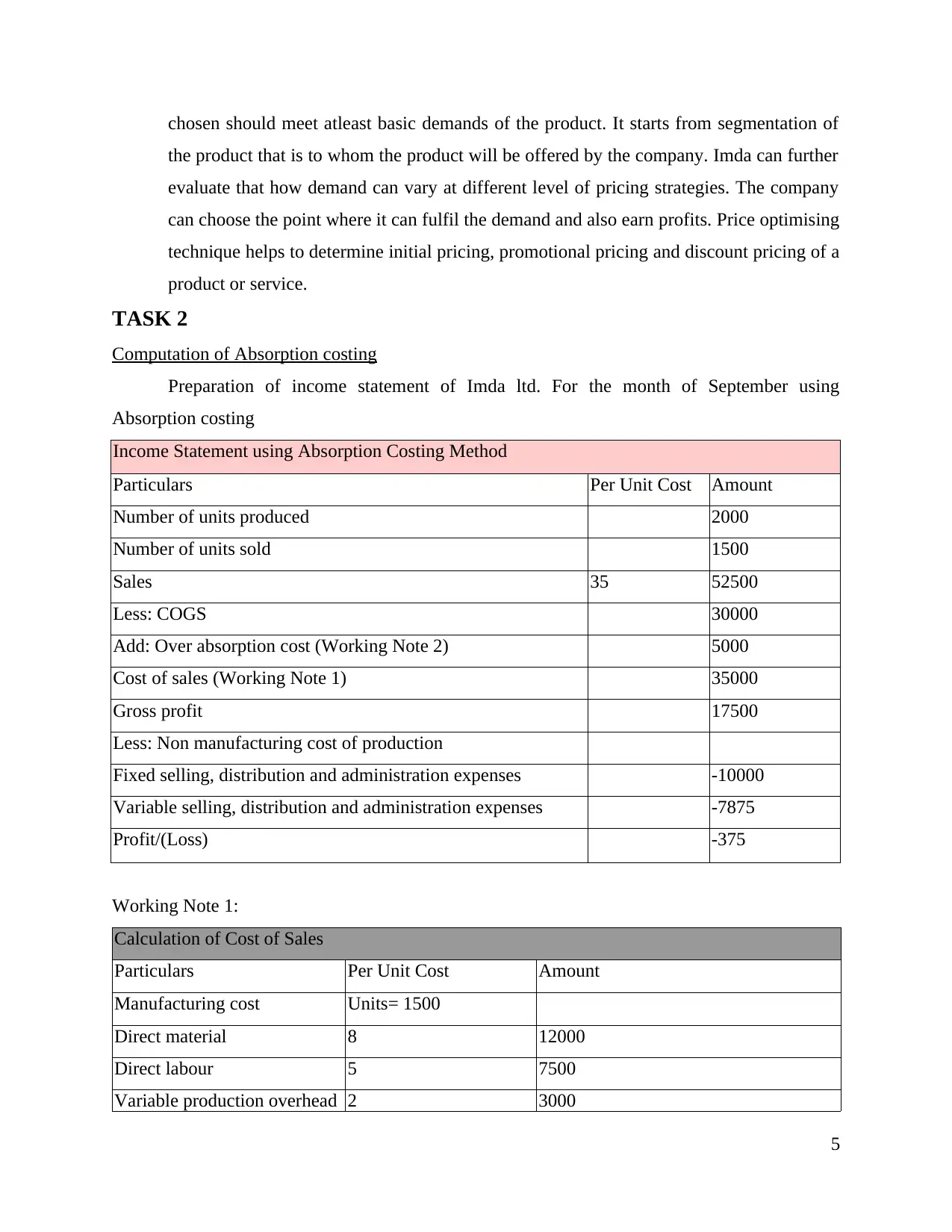

TASK 2

Computation of Absorption costing

Preparation of income statement of Imda ltd. For the month of September using

Absorption costing

Income Statement using Absorption Costing Method

Particulars Per Unit Cost Amount

Number of units produced 2000

Number of units sold 1500

Sales 35 52500

Less: COGS 30000

Add: Over absorption cost (Working Note 2) 5000

Cost of sales (Working Note 1) 35000

Gross profit 17500

Less: Non manufacturing cost of production

Fixed selling, distribution and administration expenses -10000

Variable selling, distribution and administration expenses -7875

Profit/(Loss) -375

Working Note 1:

Calculation of Cost of Sales

Particulars Per Unit Cost Amount

Manufacturing cost Units= 1500

Direct material 8 12000

Direct labour 5 7500

Variable production overhead 2 3000

5

the product that is to whom the product will be offered by the company. Imda can further

evaluate that how demand can vary at different level of pricing strategies. The company

can choose the point where it can fulfil the demand and also earn profits. Price optimising

technique helps to determine initial pricing, promotional pricing and discount pricing of a

product or service.

TASK 2

Computation of Absorption costing

Preparation of income statement of Imda ltd. For the month of September using

Absorption costing

Income Statement using Absorption Costing Method

Particulars Per Unit Cost Amount

Number of units produced 2000

Number of units sold 1500

Sales 35 52500

Less: COGS 30000

Add: Over absorption cost (Working Note 2) 5000

Cost of sales (Working Note 1) 35000

Gross profit 17500

Less: Non manufacturing cost of production

Fixed selling, distribution and administration expenses -10000

Variable selling, distribution and administration expenses -7875

Profit/(Loss) -375

Working Note 1:

Calculation of Cost of Sales

Particulars Per Unit Cost Amount

Manufacturing cost Units= 1500

Direct material 8 12000

Direct labour 5 7500

Variable production overhead 2 3000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

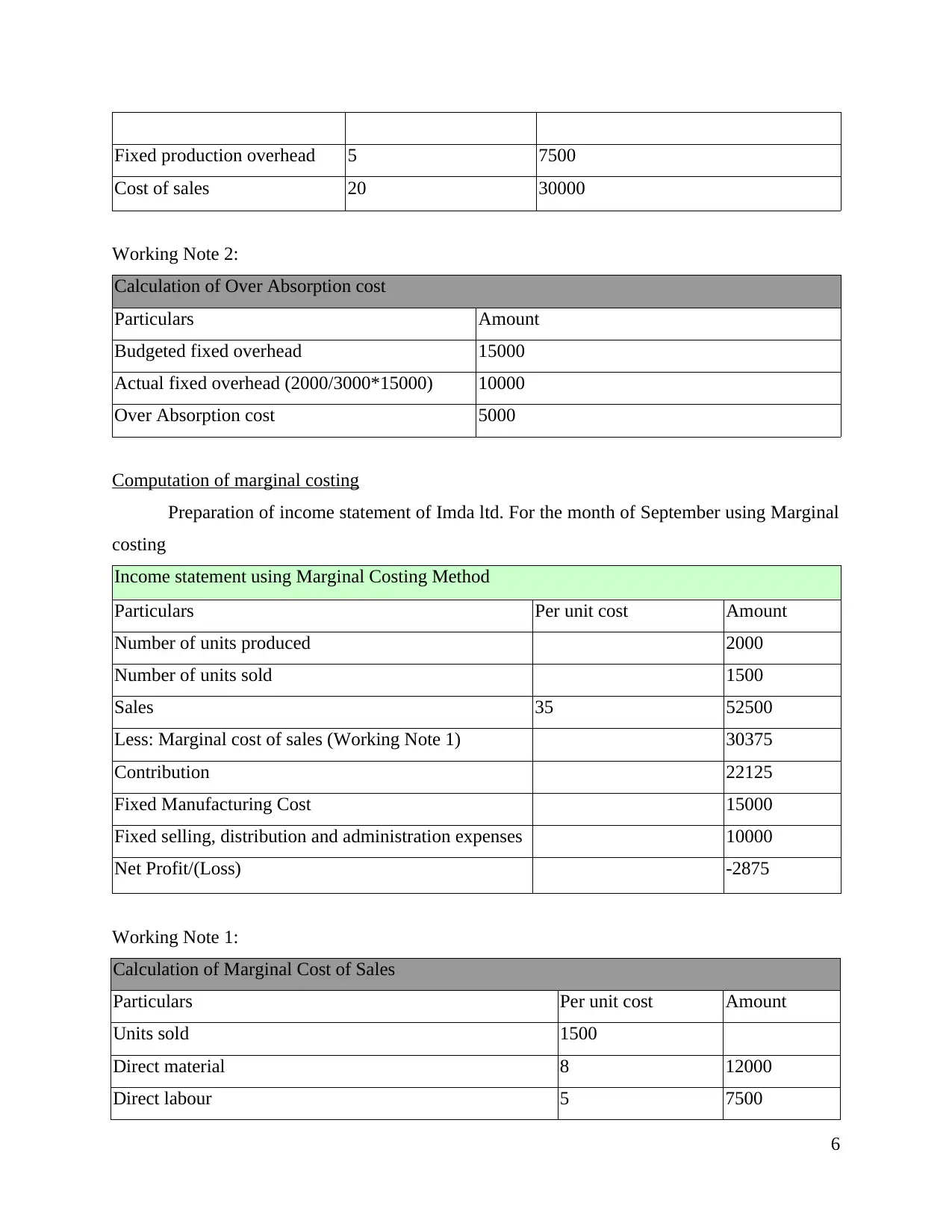

Fixed production overhead 5 7500

Cost of sales 20 30000

Working Note 2:

Calculation of Over Absorption cost

Particulars Amount

Budgeted fixed overhead 15000

Actual fixed overhead (2000/3000*15000) 10000

Over Absorption cost 5000

Computation of marginal costing

Preparation of income statement of Imda ltd. For the month of September using Marginal

costing

Income statement using Marginal Costing Method

Particulars Per unit cost Amount

Number of units produced 2000

Number of units sold 1500

Sales 35 52500

Less: Marginal cost of sales (Working Note 1) 30375

Contribution 22125

Fixed Manufacturing Cost 15000

Fixed selling, distribution and administration expenses 10000

Net Profit/(Loss) -2875

Working Note 1:

Calculation of Marginal Cost of Sales

Particulars Per unit cost Amount

Units sold 1500

Direct material 8 12000

Direct labour 5 7500

6

Cost of sales 20 30000

Working Note 2:

Calculation of Over Absorption cost

Particulars Amount

Budgeted fixed overhead 15000

Actual fixed overhead (2000/3000*15000) 10000

Over Absorption cost 5000

Computation of marginal costing

Preparation of income statement of Imda ltd. For the month of September using Marginal

costing

Income statement using Marginal Costing Method

Particulars Per unit cost Amount

Number of units produced 2000

Number of units sold 1500

Sales 35 52500

Less: Marginal cost of sales (Working Note 1) 30375

Contribution 22125

Fixed Manufacturing Cost 15000

Fixed selling, distribution and administration expenses 10000

Net Profit/(Loss) -2875

Working Note 1:

Calculation of Marginal Cost of Sales

Particulars Per unit cost Amount

Units sold 1500

Direct material 8 12000

Direct labour 5 7500

6

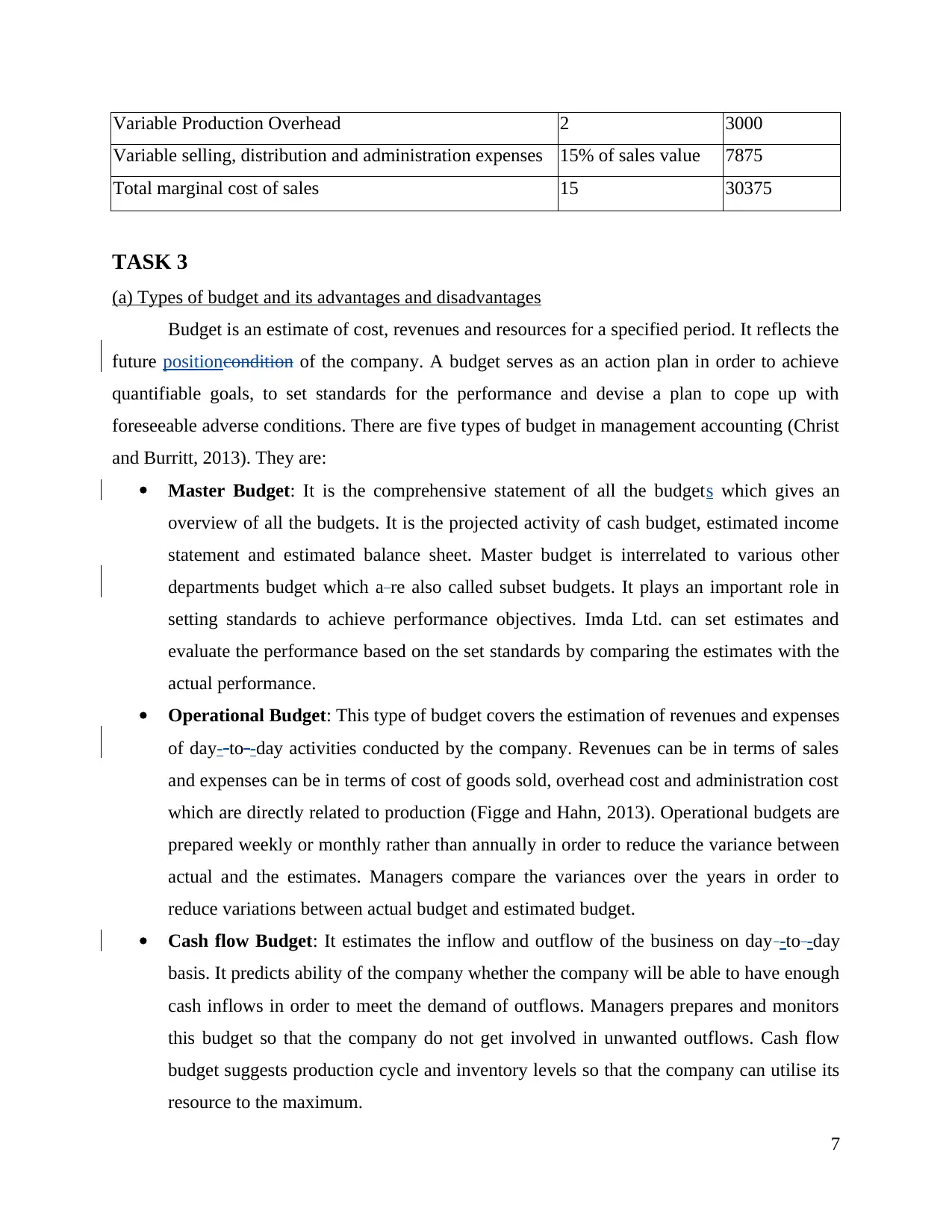

Variable Production Overhead 2 3000

Variable selling, distribution and administration expenses 15% of sales value 7875

Total marginal cost of sales 15 30375

TASK 3

(a) Types of budget and its advantages and disadvantages

Budget is an estimate of cost, revenues and resources for a specified period. It reflects the

future positioncondition of the company. A budget serves as an action plan in order to achieve

quantifiable goals, to set standards for the performance and devise a plan to cope up with

foreseeable adverse conditions. There are five types of budget in management accounting (Christ

and Burritt, 2013). They are:

Master Budget: It is the comprehensive statement of all the budgets which gives an

overview of all the budgets. It is the projected activity of cash budget, estimated income

statement and estimated balance sheet. Master budget is interrelated to various other

departments budget which a re also called subset budgets. It plays an important role in

setting standards to achieve performance objectives. Imda Ltd. can set estimates and

evaluate the performance based on the set standards by comparing the estimates with the

actual performance.

Operational Budget: This type of budget covers the estimation of revenues and expenses

of day- to -day activities conducted by the company. Revenues can be in terms of sales

and expenses can be in terms of cost of goods sold, overhead cost and administration cost

which are directly related to production (Figge and Hahn, 2013). Operational budgets are

prepared weekly or monthly rather than annually in order to reduce the variance between

actual and the estimates. Managers compare the variances over the years in order to

reduce variations between actual budget and estimated budget.

Cash flow Budget: It estimates the inflow and outflow of the business on day -to -day

basis. It predicts ability of the company whether the company will be able to have enough

cash inflows in order to meet the demand of outflows. Managers prepares and monitors

this budget so that the company do not get involved in unwanted outflows. Cash flow

budget suggests production cycle and inventory levels so that the company can utilise its

resource to the maximum.

7

Variable selling, distribution and administration expenses 15% of sales value 7875

Total marginal cost of sales 15 30375

TASK 3

(a) Types of budget and its advantages and disadvantages

Budget is an estimate of cost, revenues and resources for a specified period. It reflects the

future positioncondition of the company. A budget serves as an action plan in order to achieve

quantifiable goals, to set standards for the performance and devise a plan to cope up with

foreseeable adverse conditions. There are five types of budget in management accounting (Christ

and Burritt, 2013). They are:

Master Budget: It is the comprehensive statement of all the budgets which gives an

overview of all the budgets. It is the projected activity of cash budget, estimated income

statement and estimated balance sheet. Master budget is interrelated to various other

departments budget which a re also called subset budgets. It plays an important role in

setting standards to achieve performance objectives. Imda Ltd. can set estimates and

evaluate the performance based on the set standards by comparing the estimates with the

actual performance.

Operational Budget: This type of budget covers the estimation of revenues and expenses

of day- to -day activities conducted by the company. Revenues can be in terms of sales

and expenses can be in terms of cost of goods sold, overhead cost and administration cost

which are directly related to production (Figge and Hahn, 2013). Operational budgets are

prepared weekly or monthly rather than annually in order to reduce the variance between

actual and the estimates. Managers compare the variances over the years in order to

reduce variations between actual budget and estimated budget.

Cash flow Budget: It estimates the inflow and outflow of the business on day -to -day

basis. It predicts ability of the company whether the company will be able to have enough

cash inflows in order to meet the demand of outflows. Managers prepares and monitors

this budget so that the company do not get involved in unwanted outflows. Cash flow

budget suggests production cycle and inventory levels so that the company can utilise its

resource to the maximum.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Budget: This type of budget estimates receipts and payments where revenues

are from core business activities and cost incurred is from capital expenditures. Managing

core assets of the company in order to evaluate financial health of the company. It helps

to preparein preparing strategic plan for future. Imda can use this budget in order to

evaluate financial performance of the business.

Static Budget: According to this type of budget, expenditure remains the same in

accordance with variations in level of sales (Fullerton, Kennedy and Widener, 2013).

Overhead cost budget is a type of static budget. It is fixed for entire period, however, it

can change over a period due to external forcing factors.

(b) Process involved in preparation of budget

Process of preparation of budget involves the following listed steps:

Getting estimates: Managers get the estimates of sales, production level, resource

availability based on the actual outcomes of previous year. Managers are also required to

consider current market forces that can change budgeted amount which has a great

impact on the functioning of the company. Plan is prepared according to detailed

discussions with the managers of different departments involved in the company.

Coordinating estimates: Managers evaluated the plan submitted by various departments

and determine whether the plan has enough potential to fulfil the overall objectives of the

company. Managers also evaluate the availability of resources which can be allocated to

different departments that are present in Imda Ltd.

Communicating Budget: The budget is then communicated to respective departments

and responsible managers. After evaluating the availability of resources and allocating

the budget to different departments, the budget is communicated for applying it into

actions. If any changes or modifications are performed in the final budget then it is also

communicated to the responsible managers (Fullerton, Kennedy and Widener, 2014). It is

required that the budget is effectively communicated to the managers for its successful

implementation.

Implementing the budget: After preparation of final budget, it is finally implemented

for operation in the next budget period. Departments are provided with necessary

material, labour and other resources for successful incorporation of the budget.

8

are from core business activities and cost incurred is from capital expenditures. Managing

core assets of the company in order to evaluate financial health of the company. It helps

to preparein preparing strategic plan for future. Imda can use this budget in order to

evaluate financial performance of the business.

Static Budget: According to this type of budget, expenditure remains the same in

accordance with variations in level of sales (Fullerton, Kennedy and Widener, 2013).

Overhead cost budget is a type of static budget. It is fixed for entire period, however, it

can change over a period due to external forcing factors.

(b) Process involved in preparation of budget

Process of preparation of budget involves the following listed steps:

Getting estimates: Managers get the estimates of sales, production level, resource

availability based on the actual outcomes of previous year. Managers are also required to

consider current market forces that can change budgeted amount which has a great

impact on the functioning of the company. Plan is prepared according to detailed

discussions with the managers of different departments involved in the company.

Coordinating estimates: Managers evaluated the plan submitted by various departments

and determine whether the plan has enough potential to fulfil the overall objectives of the

company. Managers also evaluate the availability of resources which can be allocated to

different departments that are present in Imda Ltd.

Communicating Budget: The budget is then communicated to respective departments

and responsible managers. After evaluating the availability of resources and allocating

the budget to different departments, the budget is communicated for applying it into

actions. If any changes or modifications are performed in the final budget then it is also

communicated to the responsible managers (Fullerton, Kennedy and Widener, 2014). It is

required that the budget is effectively communicated to the managers for its successful

implementation.

Implementing the budget: After preparation of final budget, it is finally implemented

for operation in the next budget period. Departments are provided with necessary

material, labour and other resources for successful incorporation of the budget.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reporting progress towards the objectives: The performances achieved by different

departments are required to be communicated to top level management so hat they can

assess whether the budget is able to fulfil its objectives or not. These investigations can

further help in making modifications in the stated budget for high performance.

(c) Pricing strategies

Pricing plays an important role in the success of any produce or services. It is required to

prepare the pricing strategy in such a way that it can fulfil Organisational goals. Imda Ltd can

use various pricing strategies in order to promote its special chargers. Some strategies are listed

below:

Premium Pricing: According to this pricing strategy, Imda can keep the price of its

chargers a bit higher than that of its competitors. This strategy is used when the company

is offering something unique i.e. market penetration or when the product is launched by

the any company for the first time in the market (Herbert and Seal, 2012). It is an

optimistic approach of pricing with a hope to earn higher revenues in the early stage of

product cycle.

Penetration Pricing: In this strategy, the company enters the market with relatively low

price in order to attract the customers towards that product. The idea behind this pricing

strategy is to initially create loss with the hope to earn profits in the late stage of product

cycle. Imda Tech can use this policy which will increase its word of mouth in the market

and also will create brand awareness about the special chargers.

Economy Pricing: The company charges bare minimum price from the customers in

order to create a customer base. The products offered are not fancy but basic products

that are easily available in the market. This strategy attracts the customers of specific

segment which is very price sensitive due to common product offered by various

companies.

Price Skimming: The company offers the product at maximum price and gain revenues

in the initial stage of product cycle (Lambert and Sponem, 2012). The idea is to earn

maximum profit in the beginning before any other competitor enter the market with same

product at low price. Imda Ltd can use this strategy and earn high revenues at initial

stage.

9

departments are required to be communicated to top level management so hat they can

assess whether the budget is able to fulfil its objectives or not. These investigations can

further help in making modifications in the stated budget for high performance.

(c) Pricing strategies

Pricing plays an important role in the success of any produce or services. It is required to

prepare the pricing strategy in such a way that it can fulfil Organisational goals. Imda Ltd can

use various pricing strategies in order to promote its special chargers. Some strategies are listed

below:

Premium Pricing: According to this pricing strategy, Imda can keep the price of its

chargers a bit higher than that of its competitors. This strategy is used when the company

is offering something unique i.e. market penetration or when the product is launched by

the any company for the first time in the market (Herbert and Seal, 2012). It is an

optimistic approach of pricing with a hope to earn higher revenues in the early stage of

product cycle.

Penetration Pricing: In this strategy, the company enters the market with relatively low

price in order to attract the customers towards that product. The idea behind this pricing

strategy is to initially create loss with the hope to earn profits in the late stage of product

cycle. Imda Tech can use this policy which will increase its word of mouth in the market

and also will create brand awareness about the special chargers.

Economy Pricing: The company charges bare minimum price from the customers in

order to create a customer base. The products offered are not fancy but basic products

that are easily available in the market. This strategy attracts the customers of specific

segment which is very price sensitive due to common product offered by various

companies.

Price Skimming: The company offers the product at maximum price and gain revenues

in the initial stage of product cycle (Lambert and Sponem, 2012). The idea is to earn

maximum profit in the beginning before any other competitor enter the market with same

product at low price. Imda Ltd can use this strategy and earn high revenues at initial

stage.

9

Psychological Pricing: This is strategy is based on the theory that certain prices have

great impact on the minds of people. For instance pricing a product for 99 rather than

100. However, the difference is just for 1 but it created high psychological impact. People

tend to purchase a product priced in odd numbers more rather than when it is common

even numbers. Imda Ltd can use this strategy and which will definitely impact sales and

generate higher revenues for the company.

TASK 4

a) Balanced Scorecard approach and its implementation in delivering performance measures.

Balanced Scorecard approach is the strategic performance management tool to identify

and improve the variousdifferent internal functions of the business and their consequent

outcomes. It's is used to measure organisational performance and furnishing feedback to

organisation (Cooper, Ezzamel and Qu, 2017). To make better decisions for the company the

proper and relevant data are to be collected, as they are used by executives in decision-making

process.

Measuring financial performance is not adequate to measure Imda's current position. This

approach views four major perspectives of the organisation, Financial, Customers, Internal

Business Process and Learning & Growth.

Financial: Steps that are to be undertaken to improve sustainable economic value. Data

such as turnover, expenses, financial gain are used to determine the financial performance

of Imda Tech. These financial metrics includes dollar amounts, financial ratios, budget

variances or income targets. Focusing upon this perspective, coves the profit targets and

revenue targets of Imda. Additionally, Budget and cost-saving targets are looked upon.

The good financial performance is the outcome of increased performance in other three

perspectives.

Customers: Their needs and desires from the company and ways to achieve those

requirements by customers. Growth and service targets with the branding objectives are

focused in this perspective. Satisfaction of customers with product and services offered to

them, regarding prices, availability and quality. They provide feedback on their needs

being fulfilled with current product or service.

Internal Business Process: Identifying Levels of productivity, efficiency and quality to

satisfy the stakeholders. Management of product range is the another measure for this

10

great impact on the minds of people. For instance pricing a product for 99 rather than

100. However, the difference is just for 1 but it created high psychological impact. People

tend to purchase a product priced in odd numbers more rather than when it is common

even numbers. Imda Ltd can use this strategy and which will definitely impact sales and

generate higher revenues for the company.

TASK 4

a) Balanced Scorecard approach and its implementation in delivering performance measures.

Balanced Scorecard approach is the strategic performance management tool to identify

and improve the variousdifferent internal functions of the business and their consequent

outcomes. It's is used to measure organisational performance and furnishing feedback to

organisation (Cooper, Ezzamel and Qu, 2017). To make better decisions for the company the

proper and relevant data are to be collected, as they are used by executives in decision-making

process.

Measuring financial performance is not adequate to measure Imda's current position. This

approach views four major perspectives of the organisation, Financial, Customers, Internal

Business Process and Learning & Growth.

Financial: Steps that are to be undertaken to improve sustainable economic value. Data

such as turnover, expenses, financial gain are used to determine the financial performance

of Imda Tech. These financial metrics includes dollar amounts, financial ratios, budget

variances or income targets. Focusing upon this perspective, coves the profit targets and

revenue targets of Imda. Additionally, Budget and cost-saving targets are looked upon.

The good financial performance is the outcome of increased performance in other three

perspectives.

Customers: Their needs and desires from the company and ways to achieve those

requirements by customers. Growth and service targets with the branding objectives are

focused in this perspective. Satisfaction of customers with product and services offered to

them, regarding prices, availability and quality. They provide feedback on their needs

being fulfilled with current product or service.

Internal Business Process: Identifying Levels of productivity, efficiency and quality to

satisfy the stakeholders. Management of product range is the another measure for this

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.