Management Accounting Report: Imda Tech Analysis and Strategies

VerifiedAdded on 2020/01/07

|13

|3745

|66

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Imda Tech (UK) Limited, a company dealing in mobile chargers and gadgets. The introduction highlights the importance of effective management accounting systems for financial information, risk assessment, and performance evaluation. The report delves into the functions of management accounting, distinguishing it from financial accounting, and emphasizes its roles in planning, organizing, decision-making, and controlling. It explores various management accounting systems, including traditional and lean costing methods, cost accounting, inventory management, job costing, and price optimization. The report then presents an income statement analysis using both absorption and marginal costing methods to assess Imda Tech's profitability. Furthermore, it examines planning tools and pricing strategies, including budgeting, and concludes with a discussion on the balance scorecard approach. The report incorporates relevant financial data and calculations to illustrate key concepts and provides insights into how management accounting can be used to improve decision-making and overall business performance.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Functions and importance of management accounting ....................................................3

P2 Management accounting system and its use in Imda Tech...............................................5

TASK 2 ..........................................................................................................................................6

P3 Income statement of Imda Tech........................................................................................6

TASK 3............................................................................................................................................8

P4 Planning tools and pricing strategies related to Imda Tech..............................................8

TASK 4..........................................................................................................................................11

P5 Balance score card approach ..........................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Functions and importance of management accounting ....................................................3

P2 Management accounting system and its use in Imda Tech...............................................5

TASK 2 ..........................................................................................................................................6

P3 Income statement of Imda Tech........................................................................................6

TASK 3............................................................................................................................................8

P4 Planning tools and pricing strategies related to Imda Tech..............................................8

TASK 4..........................................................................................................................................11

P5 Balance score card approach ..........................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting consists of the financial information, risk factor and

performance of the company. It is Important for Imda Tech (UK) Limited to implement

effective system (Brandau and et. al., 2013). This company is dealing in mobile charger and

other gadgets. Company has faced the issue that was due to lack of financial information so it is

required for the company to adopt effective system that can help to over come such difficulties.

There are many methods of management accounting that can be used by company as Cost

accounting system, Inventory management system, job costing and price optimising system.

TASK 1

P1 Functions and importance of management accounting

Management accounting: It covers identification, analyzing and communication of

information. It helps to take effective decisions in the business to achieve goals and objectives. It

provides helpful information regarding the financial, risk associated with operation, strategic

management, performance of company in the market so that effective decisions can be taken.

Financial accounting: It is used to prepare financial statement. Company requires to appoint

such personal who are expert in their field to prepare financial statement. There is specific format

of financial statement that is required to follow (Otley and Emmanuel, 2013). The user of such

information are internal and external parties.

Following are the distinguish between management accounting and financial accounting

Management accounting Financial accounting

It covers various content as related to risk,

performance, strategic management.

It covers only financial information.

It is not mandatory for the company to prepare. It is mandatory to prepare.

Its main objective is to make the effective

planning and decisions.

The main objective is to provide financial

information to the outsider.

There is no timing to prepare. It can be

prepared at any time.

It is required to prepare at the end of financial

year.

The audit of management accounting is not It is required to make the regular auditing of

Management accounting consists of the financial information, risk factor and

performance of the company. It is Important for Imda Tech (UK) Limited to implement

effective system (Brandau and et. al., 2013). This company is dealing in mobile charger and

other gadgets. Company has faced the issue that was due to lack of financial information so it is

required for the company to adopt effective system that can help to over come such difficulties.

There are many methods of management accounting that can be used by company as Cost

accounting system, Inventory management system, job costing and price optimising system.

TASK 1

P1 Functions and importance of management accounting

Management accounting: It covers identification, analyzing and communication of

information. It helps to take effective decisions in the business to achieve goals and objectives. It

provides helpful information regarding the financial, risk associated with operation, strategic

management, performance of company in the market so that effective decisions can be taken.

Financial accounting: It is used to prepare financial statement. Company requires to appoint

such personal who are expert in their field to prepare financial statement. There is specific format

of financial statement that is required to follow (Otley and Emmanuel, 2013). The user of such

information are internal and external parties.

Following are the distinguish between management accounting and financial accounting

Management accounting Financial accounting

It covers various content as related to risk,

performance, strategic management.

It covers only financial information.

It is not mandatory for the company to prepare. It is mandatory to prepare.

Its main objective is to make the effective

planning and decisions.

The main objective is to provide financial

information to the outsider.

There is no timing to prepare. It can be

prepared at any time.

It is required to prepare at the end of financial

year.

The audit of management accounting is not It is required to make the regular auditing of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

compulsory. financial accounts.

Following are the functions of management accounting

1) Planning: It is crucial part of every organisation. It consists of the information of various

sector so it is easy to make the planning. It covers information as financial, strategic

management, performance, risk so it is easy to make the planning.

2) Organising: It is the process in which task is allotted to the employees of the company. It

is the important part because in this, it is required for the management to allot the task

according to the strength of the employee (Amidu, Effah and Abor, 2011).

3) Decision: Management accounting helps to make the decision because it provides various

information. It is very helpful agent to provide information to the management so that

they can make the decision.

4) Controlling: It is required for the organisation to make the control over the affairs. When

relevant information is provided then it is helpful to implement the effective control

mechanism.

Importance of management accounting

It is important tool that provides help to management to make the effective decisions. Importance

of management accounting are as follows:-

1. To find out goals and objective: It helps the organisation to make the effective decisions.

It provides various information to the management so it is better to decide about the goal

and objectives.

2. Formulation of plan: When management has required information then it is easy for them

to make the effective planning. Management accounting plays very important role in

formulation of plan (Brandau and et. al., 2013).

3. To provide services: Management accounting consists of the information regarding the

performance of the company so it is easy to check that are the customers happy with the

services so that better services can be provided.

4. Increase efficiency of business: management accounting plays an important role to

improve the efficiency. Because it helps to take decision so that when such are

implemented then it improves the efficiency.

Following are the functions of management accounting

1) Planning: It is crucial part of every organisation. It consists of the information of various

sector so it is easy to make the planning. It covers information as financial, strategic

management, performance, risk so it is easy to make the planning.

2) Organising: It is the process in which task is allotted to the employees of the company. It

is the important part because in this, it is required for the management to allot the task

according to the strength of the employee (Amidu, Effah and Abor, 2011).

3) Decision: Management accounting helps to make the decision because it provides various

information. It is very helpful agent to provide information to the management so that

they can make the decision.

4) Controlling: It is required for the organisation to make the control over the affairs. When

relevant information is provided then it is helpful to implement the effective control

mechanism.

Importance of management accounting

It is important tool that provides help to management to make the effective decisions. Importance

of management accounting are as follows:-

1. To find out goals and objective: It helps the organisation to make the effective decisions.

It provides various information to the management so it is better to decide about the goal

and objectives.

2. Formulation of plan: When management has required information then it is easy for them

to make the effective planning. Management accounting plays very important role in

formulation of plan (Brandau and et. al., 2013).

3. To provide services: Management accounting consists of the information regarding the

performance of the company so it is easy to check that are the customers happy with the

services so that better services can be provided.

4. Increase efficiency of business: management accounting plays an important role to

improve the efficiency. Because it helps to take decision so that when such are

implemented then it improves the efficiency.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

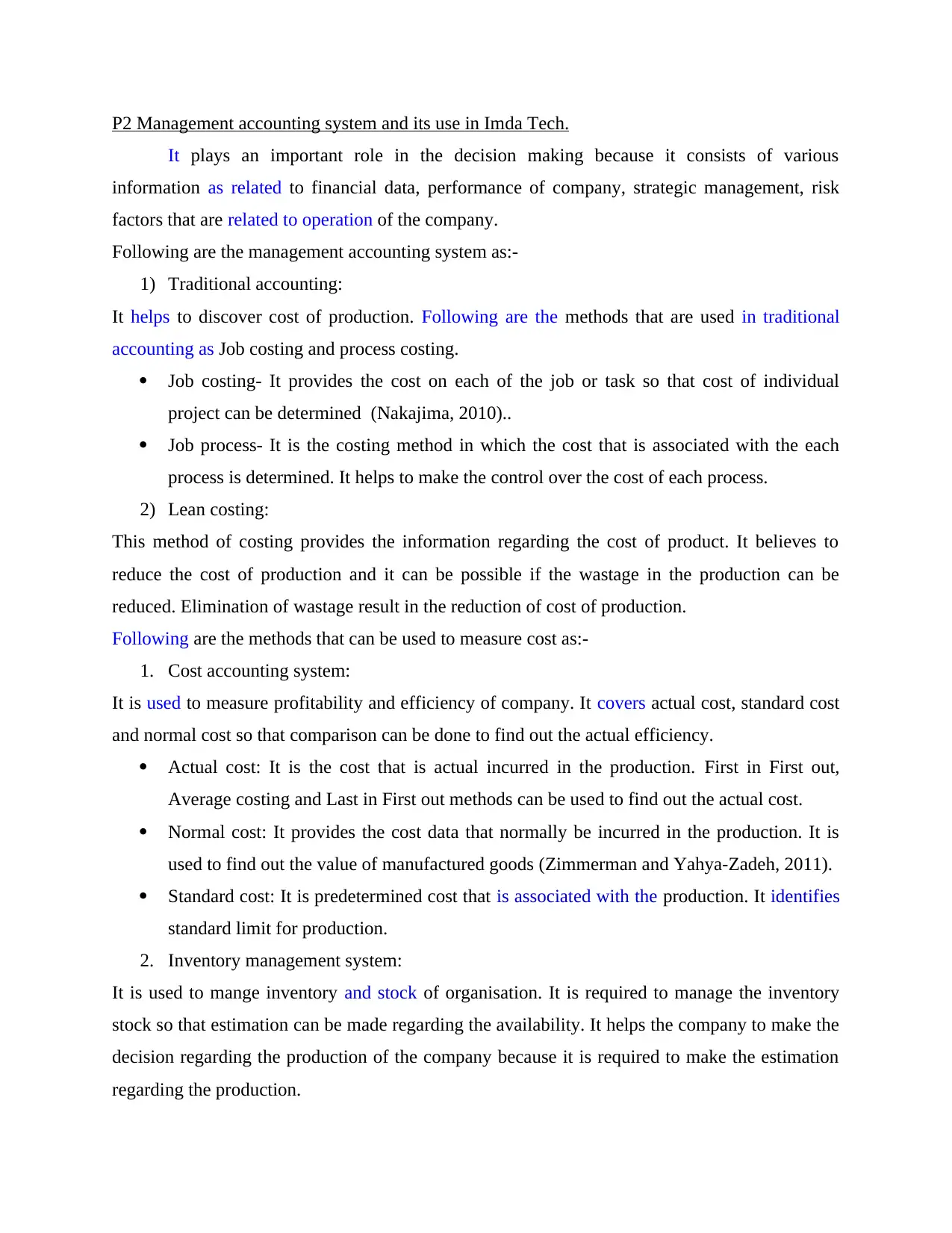

P2 Management accounting system and its use in Imda Tech.

It plays an important role in the decision making because it consists of various

information as related to financial data, performance of company, strategic management, risk

factors that are related to operation of the company.

Following are the management accounting system as:-

1) Traditional accounting:

It helps to discover cost of production. Following are the methods that are used in traditional

accounting as Job costing and process costing.

Job costing- It provides the cost on each of the job or task so that cost of individual

project can be determined (Nakajima, 2010)..

Job process- It is the costing method in which the cost that is associated with the each

process is determined. It helps to make the control over the cost of each process.

2) Lean costing:

This method of costing provides the information regarding the cost of product. It believes to

reduce the cost of production and it can be possible if the wastage in the production can be

reduced. Elimination of wastage result in the reduction of cost of production.

Following are the methods that can be used to measure cost as:-

1. Cost accounting system:

It is used to measure profitability and efficiency of company. It covers actual cost, standard cost

and normal cost so that comparison can be done to find out the actual efficiency.

Actual cost: It is the cost that is actual incurred in the production. First in First out,

Average costing and Last in First out methods can be used to find out the actual cost.

Normal cost: It provides the cost data that normally be incurred in the production. It is

used to find out the value of manufactured goods (Zimmerman and Yahya-Zadeh, 2011).

Standard cost: It is predetermined cost that is associated with the production. It identifies

standard limit for production.

2. Inventory management system:

It is used to mange inventory and stock of organisation. It is required to manage the inventory

stock so that estimation can be made regarding the availability. It helps the company to make the

decision regarding the production of the company because it is required to make the estimation

regarding the production.

It plays an important role in the decision making because it consists of various

information as related to financial data, performance of company, strategic management, risk

factors that are related to operation of the company.

Following are the management accounting system as:-

1) Traditional accounting:

It helps to discover cost of production. Following are the methods that are used in traditional

accounting as Job costing and process costing.

Job costing- It provides the cost on each of the job or task so that cost of individual

project can be determined (Nakajima, 2010)..

Job process- It is the costing method in which the cost that is associated with the each

process is determined. It helps to make the control over the cost of each process.

2) Lean costing:

This method of costing provides the information regarding the cost of product. It believes to

reduce the cost of production and it can be possible if the wastage in the production can be

reduced. Elimination of wastage result in the reduction of cost of production.

Following are the methods that can be used to measure cost as:-

1. Cost accounting system:

It is used to measure profitability and efficiency of company. It covers actual cost, standard cost

and normal cost so that comparison can be done to find out the actual efficiency.

Actual cost: It is the cost that is actual incurred in the production. First in First out,

Average costing and Last in First out methods can be used to find out the actual cost.

Normal cost: It provides the cost data that normally be incurred in the production. It is

used to find out the value of manufactured goods (Zimmerman and Yahya-Zadeh, 2011).

Standard cost: It is predetermined cost that is associated with the production. It identifies

standard limit for production.

2. Inventory management system:

It is used to mange inventory and stock of organisation. It is required to manage the inventory

stock so that estimation can be made regarding the availability. It helps the company to make the

decision regarding the production of the company because it is required to make the estimation

regarding the production.

3. Job costing:

It is the measure that can be used to measure the cost on each job or task. It is helpful to measure

the cost so that better decision making can be made. It is helpful to measure the cost of

individual project.

4. Price optimising system:

This system can be used to identify the price of product so that it can be measured such product

will be accepted by the customer or not. It makes the price at optimising level so that it can be

accepted by the customer (Sisaye and Birnberg, 2010).

Use by the organisation

It can be implemented by the organisation. It is beneficial for the company to implement

in product because it is helpful to optimise the cost of product and to measure requirements of

the production. It is useful to derive the information regarding the cost of various job and

process.

TASK 2

P3 Income statement of Imda Tech

Direct labour £5

Direct material £8

Variable production overhead £2

Fixed production overhead £5

Standard production cost £20

Budget £36,000/year

Actual overhead £15,000/each month

Selling, distribution and administration expenses are:

Fixed £10,000/month

Variable 15% of the sales value

Selling price £35/unit

It is the measure that can be used to measure the cost on each job or task. It is helpful to measure

the cost so that better decision making can be made. It is helpful to measure the cost of

individual project.

4. Price optimising system:

This system can be used to identify the price of product so that it can be measured such product

will be accepted by the customer or not. It makes the price at optimising level so that it can be

accepted by the customer (Sisaye and Birnberg, 2010).

Use by the organisation

It can be implemented by the organisation. It is beneficial for the company to implement

in product because it is helpful to optimise the cost of product and to measure requirements of

the production. It is useful to derive the information regarding the cost of various job and

process.

TASK 2

P3 Income statement of Imda Tech

Direct labour £5

Direct material £8

Variable production overhead £2

Fixed production overhead £5

Standard production cost £20

Budget £36,000/year

Actual overhead £15,000/each month

Selling, distribution and administration expenses are:

Fixed £10,000/month

Variable 15% of the sales value

Selling price £35/unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

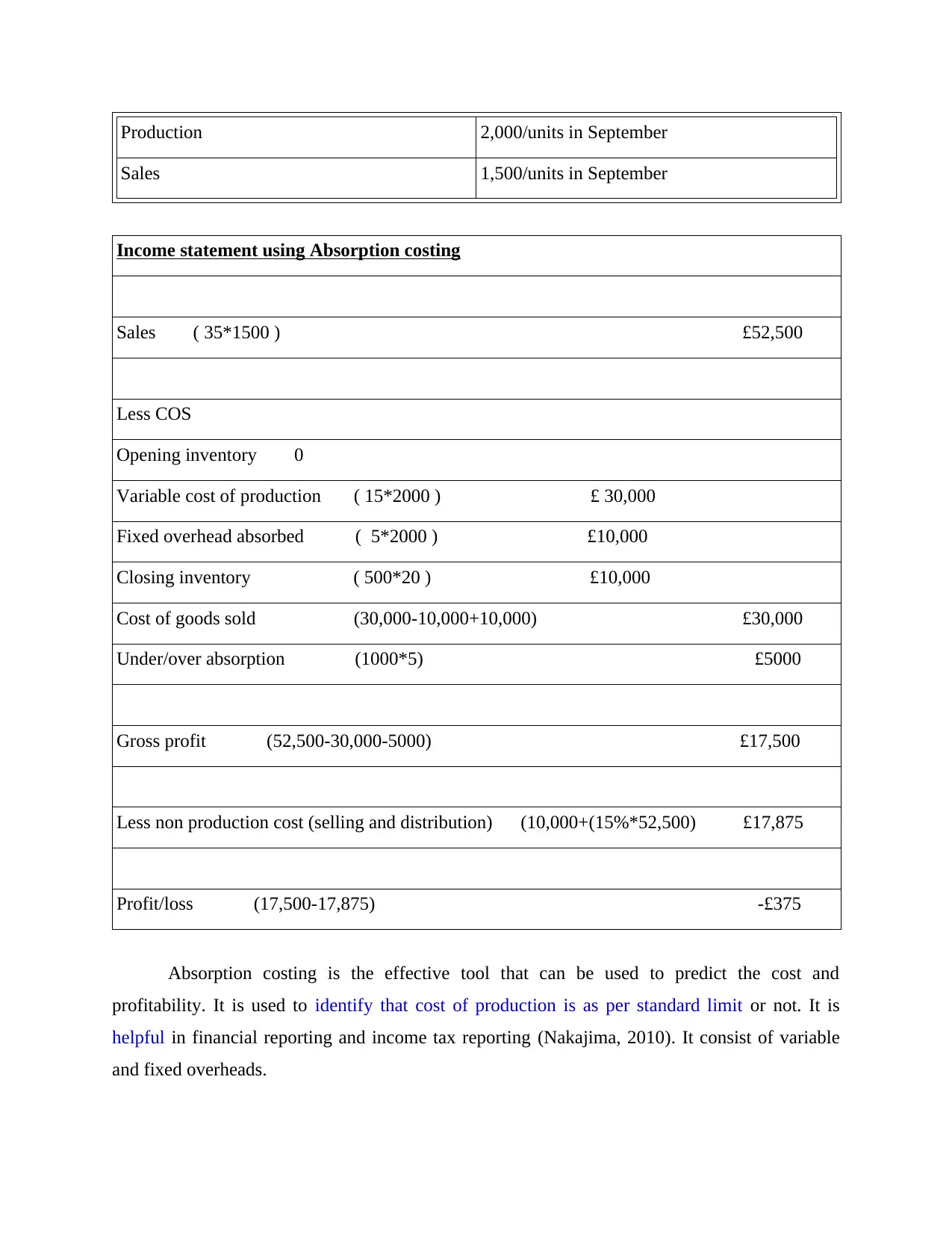

Production 2,000/units in September

Sales 1,500/units in September

Income statement using Absorption costing

Sales ( 35*1500 ) £52,500

Less COS

Opening inventory 0

Variable cost of production ( 15*2000 ) £ 30,000

Fixed overhead absorbed ( 5*2000 ) £10,000

Closing inventory ( 500*20 ) £10,000

Cost of goods sold (30,000-10,000+10,000) £30,000

Under/over absorption (1000*5) £5000

Gross profit (52,500-30,000-5000) £17,500

Less non production cost (selling and distribution) (10,000+(15%*52,500) £17,875

Profit/loss (17,500-17,875) -£375

Absorption costing is the effective tool that can be used to predict the cost and

profitability. It is used to identify that cost of production is as per standard limit or not. It is

helpful in financial reporting and income tax reporting (Nakajima, 2010). It consist of variable

and fixed overheads.

Sales 1,500/units in September

Income statement using Absorption costing

Sales ( 35*1500 ) £52,500

Less COS

Opening inventory 0

Variable cost of production ( 15*2000 ) £ 30,000

Fixed overhead absorbed ( 5*2000 ) £10,000

Closing inventory ( 500*20 ) £10,000

Cost of goods sold (30,000-10,000+10,000) £30,000

Under/over absorption (1000*5) £5000

Gross profit (52,500-30,000-5000) £17,500

Less non production cost (selling and distribution) (10,000+(15%*52,500) £17,875

Profit/loss (17,500-17,875) -£375

Absorption costing is the effective tool that can be used to predict the cost and

profitability. It is used to identify that cost of production is as per standard limit or not. It is

helpful in financial reporting and income tax reporting (Nakajima, 2010). It consist of variable

and fixed overheads.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

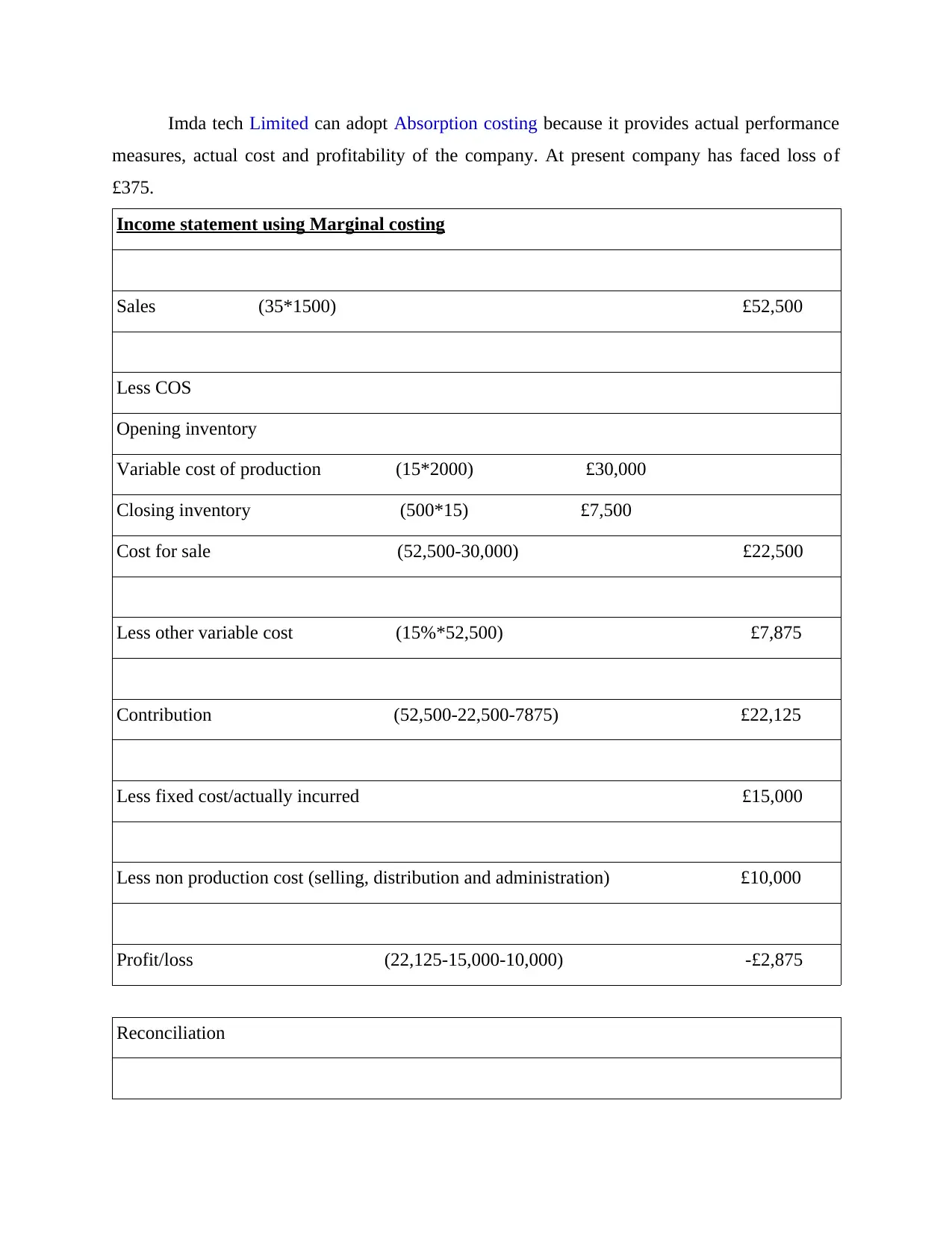

Imda tech Limited can adopt Absorption costing because it provides actual performance

measures, actual cost and profitability of the company. At present company has faced loss of

£375.

Income statement using Marginal costing

Sales (35*1500) £52,500

Less COS

Opening inventory

Variable cost of production (15*2000) £30,000

Closing inventory (500*15) £7,500

Cost for sale (52,500-30,000) £22,500

Less other variable cost (15%*52,500) £7,875

Contribution (52,500-22,500-7875) £22,125

Less fixed cost/actually incurred £15,000

Less non production cost (selling, distribution and administration) £10,000

Profit/loss (22,125-15,000-10,000) -£2,875

Reconciliation

measures, actual cost and profitability of the company. At present company has faced loss of

£375.

Income statement using Marginal costing

Sales (35*1500) £52,500

Less COS

Opening inventory

Variable cost of production (15*2000) £30,000

Closing inventory (500*15) £7,500

Cost for sale (52,500-30,000) £22,500

Less other variable cost (15%*52,500) £7,875

Contribution (52,500-22,500-7875) £22,125

Less fixed cost/actually incurred £15,000

Less non production cost (selling, distribution and administration) £10,000

Profit/loss (22,125-15,000-10,000) -£2,875

Reconciliation

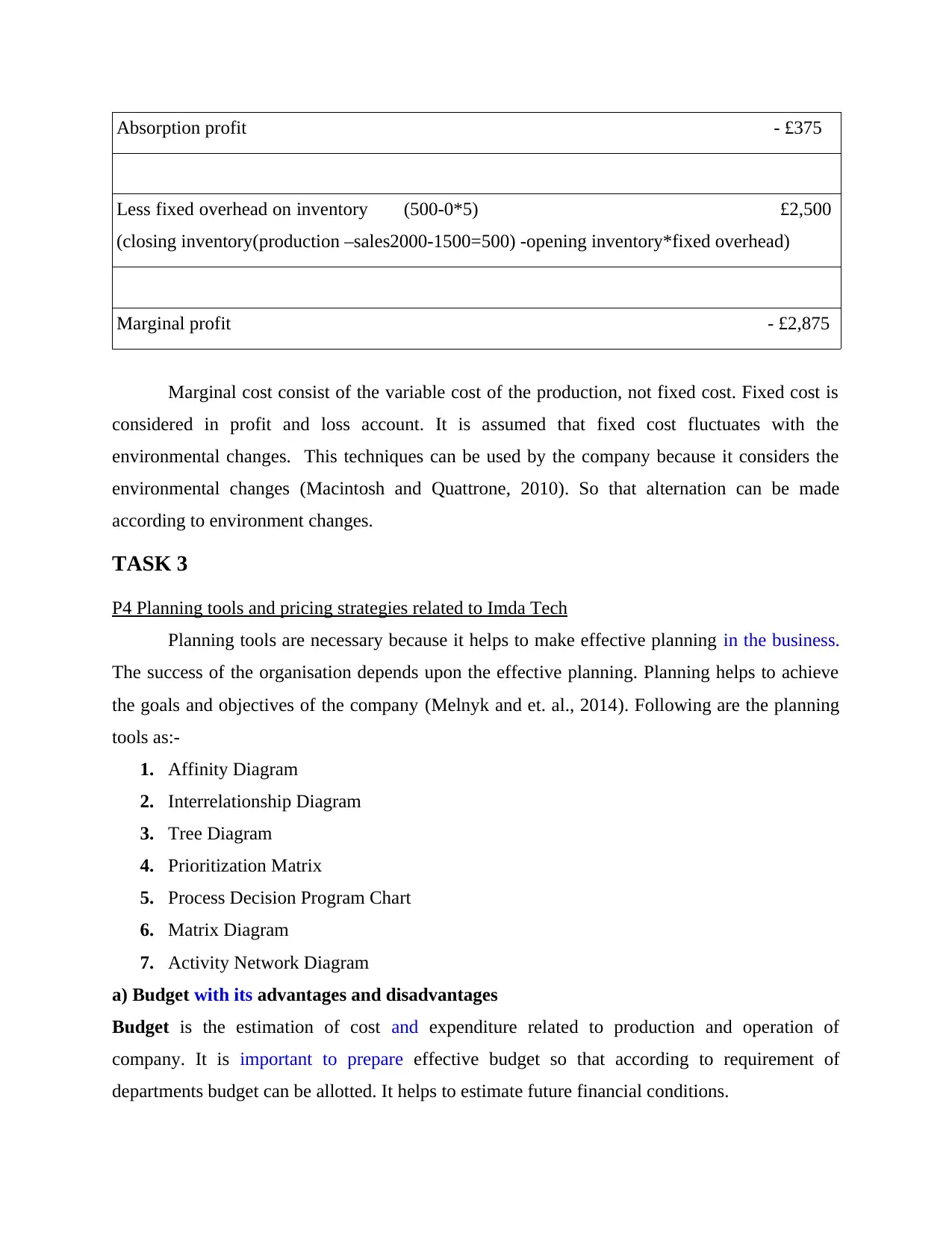

Absorption profit - £375

Less fixed overhead on inventory (500-0*5) £2,500

(closing inventory(production –sales2000-1500=500) -opening inventory*fixed overhead)

Marginal profit - £2,875

Marginal cost consist of the variable cost of the production, not fixed cost. Fixed cost is

considered in profit and loss account. It is assumed that fixed cost fluctuates with the

environmental changes. This techniques can be used by the company because it considers the

environmental changes (Macintosh and Quattrone, 2010). So that alternation can be made

according to environment changes.

TASK 3

P4 Planning tools and pricing strategies related to Imda Tech

Planning tools are necessary because it helps to make effective planning in the business.

The success of the organisation depends upon the effective planning. Planning helps to achieve

the goals and objectives of the company (Melnyk and et. al., 2014). Following are the planning

tools as:-

1. Affinity Diagram

2. Interrelationship Diagram

3. Tree Diagram

4. Prioritization Matrix

5. Process Decision Program Chart

6. Matrix Diagram

7. Activity Network Diagram

a) Budget with its advantages and disadvantages

Budget is the estimation of cost and expenditure related to production and operation of

company. It is important to prepare effective budget so that according to requirement of

departments budget can be allotted. It helps to estimate future financial conditions.

Less fixed overhead on inventory (500-0*5) £2,500

(closing inventory(production –sales2000-1500=500) -opening inventory*fixed overhead)

Marginal profit - £2,875

Marginal cost consist of the variable cost of the production, not fixed cost. Fixed cost is

considered in profit and loss account. It is assumed that fixed cost fluctuates with the

environmental changes. This techniques can be used by the company because it considers the

environmental changes (Macintosh and Quattrone, 2010). So that alternation can be made

according to environment changes.

TASK 3

P4 Planning tools and pricing strategies related to Imda Tech

Planning tools are necessary because it helps to make effective planning in the business.

The success of the organisation depends upon the effective planning. Planning helps to achieve

the goals and objectives of the company (Melnyk and et. al., 2014). Following are the planning

tools as:-

1. Affinity Diagram

2. Interrelationship Diagram

3. Tree Diagram

4. Prioritization Matrix

5. Process Decision Program Chart

6. Matrix Diagram

7. Activity Network Diagram

a) Budget with its advantages and disadvantages

Budget is the estimation of cost and expenditure related to production and operation of

company. It is important to prepare effective budget so that according to requirement of

departments budget can be allotted. It helps to estimate future financial conditions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

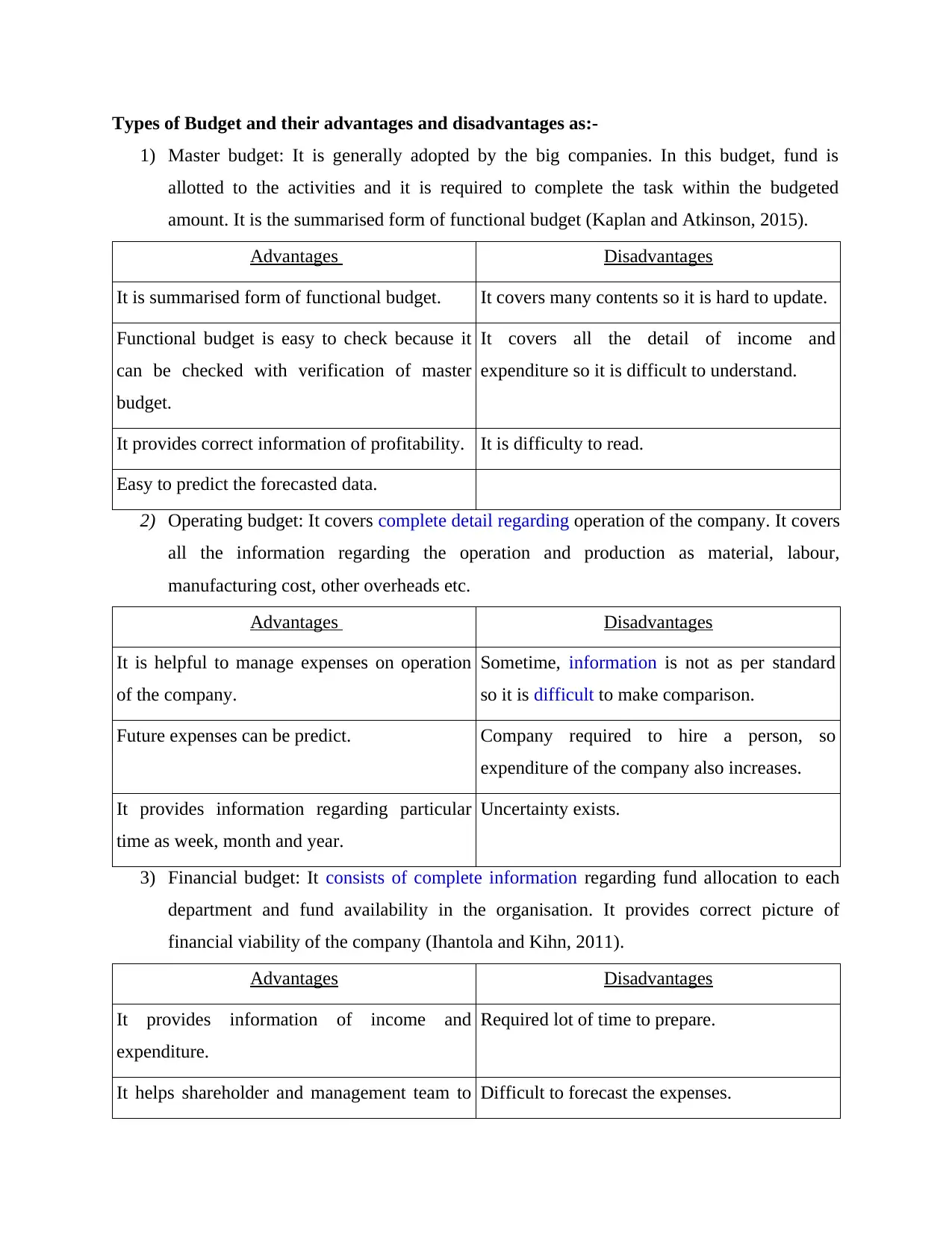

Types of Budget and their advantages and disadvantages as:-

1) Master budget: It is generally adopted by the big companies. In this budget, fund is

allotted to the activities and it is required to complete the task within the budgeted

amount. It is the summarised form of functional budget (Kaplan and Atkinson, 2015).

Advantages Disadvantages

It is summarised form of functional budget. It covers many contents so it is hard to update.

Functional budget is easy to check because it

can be checked with verification of master

budget.

It covers all the detail of income and

expenditure so it is difficult to understand.

It provides correct information of profitability. It is difficulty to read.

Easy to predict the forecasted data.

2) Operating budget: It covers complete detail regarding operation of the company. It covers

all the information regarding the operation and production as material, labour,

manufacturing cost, other overheads etc.

Advantages Disadvantages

It is helpful to manage expenses on operation

of the company.

Sometime, information is not as per standard

so it is difficult to make comparison.

Future expenses can be predict. Company required to hire a person, so

expenditure of the company also increases.

It provides information regarding particular

time as week, month and year.

Uncertainty exists.

3) Financial budget: It consists of complete information regarding fund allocation to each

department and fund availability in the organisation. It provides correct picture of

financial viability of the company (Ihantola and Kihn, 2011).

Advantages Disadvantages

It provides information of income and

expenditure.

Required lot of time to prepare.

It helps shareholder and management team to Difficult to forecast the expenses.

1) Master budget: It is generally adopted by the big companies. In this budget, fund is

allotted to the activities and it is required to complete the task within the budgeted

amount. It is the summarised form of functional budget (Kaplan and Atkinson, 2015).

Advantages Disadvantages

It is summarised form of functional budget. It covers many contents so it is hard to update.

Functional budget is easy to check because it

can be checked with verification of master

budget.

It covers all the detail of income and

expenditure so it is difficult to understand.

It provides correct information of profitability. It is difficulty to read.

Easy to predict the forecasted data.

2) Operating budget: It covers complete detail regarding operation of the company. It covers

all the information regarding the operation and production as material, labour,

manufacturing cost, other overheads etc.

Advantages Disadvantages

It is helpful to manage expenses on operation

of the company.

Sometime, information is not as per standard

so it is difficult to make comparison.

Future expenses can be predict. Company required to hire a person, so

expenditure of the company also increases.

It provides information regarding particular

time as week, month and year.

Uncertainty exists.

3) Financial budget: It consists of complete information regarding fund allocation to each

department and fund availability in the organisation. It provides correct picture of

financial viability of the company (Ihantola and Kihn, 2011).

Advantages Disadvantages

It provides information of income and

expenditure.

Required lot of time to prepare.

It helps shareholder and management team to Difficult to forecast the expenses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

take decision.

4) Static Budget: It covers the information that is prior to budget period. It is of

unchangeable in nature. It changes only with the change in sales and revenue.

Advantages Disadvantages

No regular changes are required to be made. It is not flexible.

Overestimating and underestimating can be

assessed.

Difficult to implement the changes.

Easy to implement.

b) Process of budget preparation

It is required for the company to make their best effort to prepare the budget. Following are the

steps to prepare the budget:-

1) To check the past budget: It is required to check the past budget and then made the

necessary changes (Gates, Nicolas and Walker, 2012).

2) Availability of fund: Fund availability at present is evaluated so that budget can be

prepared.

3) Estimation of expenses: It is required to make the estimation of expenditure so that funds

can be allotted.

4) Revenue forecast: Revenue and income are forecasted so that funds for expenditure can

be allotted accordingly.

5) Create budget package and issue it: Recent amendments are considered and then it is

issued to the recipients.

6) Answer to question: It is required to consider the points of recipients so that effective

budget can be prepared.

7) Prepare the budget: When all the above points are considered then final budget is

prepared and issued (France, 2010).

c) Pricing strategies

It is required for organisation to make the effective pricing strategy so that effective price

can be made to the product. It is essential to cover account segment, market condition, action of

competitor, input cost.

Pricing strategies are as follows:-

4) Static Budget: It covers the information that is prior to budget period. It is of

unchangeable in nature. It changes only with the change in sales and revenue.

Advantages Disadvantages

No regular changes are required to be made. It is not flexible.

Overestimating and underestimating can be

assessed.

Difficult to implement the changes.

Easy to implement.

b) Process of budget preparation

It is required for the company to make their best effort to prepare the budget. Following are the

steps to prepare the budget:-

1) To check the past budget: It is required to check the past budget and then made the

necessary changes (Gates, Nicolas and Walker, 2012).

2) Availability of fund: Fund availability at present is evaluated so that budget can be

prepared.

3) Estimation of expenses: It is required to make the estimation of expenditure so that funds

can be allotted.

4) Revenue forecast: Revenue and income are forecasted so that funds for expenditure can

be allotted accordingly.

5) Create budget package and issue it: Recent amendments are considered and then it is

issued to the recipients.

6) Answer to question: It is required to consider the points of recipients so that effective

budget can be prepared.

7) Prepare the budget: When all the above points are considered then final budget is

prepared and issued (France, 2010).

c) Pricing strategies

It is required for organisation to make the effective pricing strategy so that effective price

can be made to the product. It is essential to cover account segment, market condition, action of

competitor, input cost.

Pricing strategies are as follows:-

1) Penetration Pricing- The price of product is low as comparison to product price of

competitor. It is used to enter into the market and take stand in the market. In starting,

organisation faces loss.

2) Premium Pricing-

The price of the product is higher because the product has some additional features that is not in

competitor's product. It is accepted because of the advantages with the product.

3) Economy pricing-

It is used to attract the customers so the price of the product is very low ( Chiwamit, Modell and

Yang, 2014).

4) Skimming pricing-

At initial level, the price of product is high and after certain time price of the product is dropped.

The aim is to earn more profit before the competitor enters into the market.

TASK 4

P5 Balance score card approach

It is used to identify the performance of company in market. It helps to identify the

improvements that are required. It is helpful to take decisions regarding the performance of the

company. It is accepted by every industry whether it is of industrial, government organisation

and non-government. The present performance of company is compared with past performance

so that better decisions can be made to improve such conditions (Chiarini, 2012).

Imda Tech Limited has loss of £1.5 million. It shows that it is arise due to lack of

financial governance. It aids the company to improve their financial and non-financial

conditions.

It is used to identify the goals and objectives, growth and performance of the company

and to give prioritization to the product and services. Key performance indicator (KPIs) can be

used by company to identify its performance so that effective measures can be implemented by

the company to make the improve. KPI dashboard helps to provide quick review of performance

of project.

Use to address the financial problems

competitor. It is used to enter into the market and take stand in the market. In starting,

organisation faces loss.

2) Premium Pricing-

The price of the product is higher because the product has some additional features that is not in

competitor's product. It is accepted because of the advantages with the product.

3) Economy pricing-

It is used to attract the customers so the price of the product is very low ( Chiwamit, Modell and

Yang, 2014).

4) Skimming pricing-

At initial level, the price of product is high and after certain time price of the product is dropped.

The aim is to earn more profit before the competitor enters into the market.

TASK 4

P5 Balance score card approach

It is used to identify the performance of company in market. It helps to identify the

improvements that are required. It is helpful to take decisions regarding the performance of the

company. It is accepted by every industry whether it is of industrial, government organisation

and non-government. The present performance of company is compared with past performance

so that better decisions can be made to improve such conditions (Chiarini, 2012).

Imda Tech Limited has loss of £1.5 million. It shows that it is arise due to lack of

financial governance. It aids the company to improve their financial and non-financial

conditions.

It is used to identify the goals and objectives, growth and performance of the company

and to give prioritization to the product and services. Key performance indicator (KPIs) can be

used by company to identify its performance so that effective measures can be implemented by

the company to make the improve. KPI dashboard helps to provide quick review of performance

of project.

Use to address the financial problems

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.