Comprehensive Management Accounting Report: IMDA TECH Analysis

VerifiedAdded on 2020/10/23

|16

|4468

|118

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within the context of IMDA TECH, a company producing mobile chargers. The report begins with an introduction to management accounting, emphasizing its role in sustainable business objectives and the use of various tools for achieving higher productivity. It then delves into the different types of management accounting systems, including cost accounting, job costing, price optimization, and inventory management systems (LIFO, FIFO, and average costs). The report also covers diverse methods used for management accounting reporting, such as budget reports, account receivable aging reports, and performance reports. Furthermore, the report explores the application of marginal costing and absorption costing techniques to prepare an income statement, calculating costs and determining profitability. The report includes calculations for break-even analysis and margin of safety, providing a detailed financial analysis of IMDA TECH's operations and financial performance. The report concludes with a discussion of how management accounting systems can be integrated with management accounting reporting to achieve sustainable development efficiently.

Management

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

INTRODUCTION

Management Accounting is the most effective tool for making the business objectives in

a sustainable manner. Here are so many tools which can be used by the organization for gaining

higher productivity. By implementing management accounting tool, company could use an

efficient strategy that can be used by the organization for making the business sustainable and

reliable. Here are various kinds of business objectives that can be used by the organization for

making the business objectives. Here are various management accounting reports that can be

used by the organization for gaining sustainable development in an effective manner (Amoako,

2013). Various budgetary planning tools are used for measuring the expected results with the

actual one and gain the sustainability in an effective manner. This report is based on the IMDA

TECH company which main operations are to produce the business mobile chargers of various

segments. Here are so many tools that can be used by IMDA TECH for making the sustainable

development.

TASK 1

P1 Management Accounting and its different types of management accounting systems:

Management accounting system is a kind of process under which organisation for

identifying, summarizing, assessing and evaluating the non- financial information that can be

implemented by the organisation for making the business objectives in an efficient manner.

Management Accounting encompasses whole kinds of information which are related to the

business operations. Management Accountants implement information linked to the costs of

goods or services purchased by the organisation. Budgets are likewise implemented as a

quantitative expression of the organisation’s plan of operation (Management Accounting, 2017).

Individuals in managerial accounting implement performance reports to note deviations of actual

outcomes from budgets.

Here are various kinds of management accounting systems which are mentioned as

under:

Cost Accounting system: This is the system which is used by the organisation for

making the business development in an effective manner. Now, management of IMDA TECH

would require to make the product in a cost efficient manner that could reduce the cost of the

product. By using this tool, cited organisation would require to make an efficient strategy which

would be used by the organisation for gaining the strategy in an effective manner. By using this

3

Management Accounting is the most effective tool for making the business objectives in

a sustainable manner. Here are so many tools which can be used by the organization for gaining

higher productivity. By implementing management accounting tool, company could use an

efficient strategy that can be used by the organization for making the business sustainable and

reliable. Here are various kinds of business objectives that can be used by the organization for

making the business objectives. Here are various management accounting reports that can be

used by the organization for gaining sustainable development in an effective manner (Amoako,

2013). Various budgetary planning tools are used for measuring the expected results with the

actual one and gain the sustainability in an effective manner. This report is based on the IMDA

TECH company which main operations are to produce the business mobile chargers of various

segments. Here are so many tools that can be used by IMDA TECH for making the sustainable

development.

TASK 1

P1 Management Accounting and its different types of management accounting systems:

Management accounting system is a kind of process under which organisation for

identifying, summarizing, assessing and evaluating the non- financial information that can be

implemented by the organisation for making the business objectives in an efficient manner.

Management Accounting encompasses whole kinds of information which are related to the

business operations. Management Accountants implement information linked to the costs of

goods or services purchased by the organisation. Budgets are likewise implemented as a

quantitative expression of the organisation’s plan of operation (Management Accounting, 2017).

Individuals in managerial accounting implement performance reports to note deviations of actual

outcomes from budgets.

Here are various kinds of management accounting systems which are mentioned as

under:

Cost Accounting system: This is the system which is used by the organisation for

making the business development in an effective manner. Now, management of IMDA TECH

would require to make the product in a cost efficient manner that could reduce the cost of the

product. By using this tool, cited organisation would require to make an efficient strategy which

would be used by the organisation for gaining the strategy in an effective manner. By using this

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

technique, IMDA TECH would reduce per unit cost by removing wastage cost efficiently

(Vinayagamoorthi and et. al., 2012).

Job Costing System: This is elaborated as the tool of recording costs of manufacturing

job, instead of process. Along with the Job costing systems, a management accountant could

track of cost of each job, handling data that are usually highly concerned to operations of the

organisation. Job costing normally said that the particular accounting tool are used to track

expense of producing a product. This is the best tool that can be implemented by the organisation

for making the new product efficiently.

Price Optimization System: Under this system, consumer perspective would be assessed

regarding the company’s product price in an effective manner. This is the tool via which the

price of the product is identified in an effective manner which can be used for making the

business objectives in an effective manner. Via this tool, organisation is totally relied upon the

management accountant, who by using various tools, make the price of the product in an

effective manner. Now, this can be simply said that the management of IMDA TECH would

ultimately leads to gain the sustainability.

Inventory management system: This is the system which is implemented for making

the inventory efficiently. Via Inventory management system, firm would track products through

whole supply chain of it an organisation operates in. Which comprises each from manufacturing

to retail, warehousing to shipping, and whole movements of stock and parts between. Inventory

is managed via LIFO, FIFO and AVCO method (Macinati and Anessi-Pessina, 2014).

LIFO method: This stands for “Last in, First Out”. Which is implemented to place an

accounting value on the inventory. LIFO method operates as per the assumption that the last item

of inventory purchased is firstly sold out. On the other hand, this is rightly said that the new

inventory assets are entered firstly and then it is sold firstly.

FIFO method: This is the inventory valuation method, under which firstly goods are

purchased, are sold out firstly. Various organisation uses this method to optimise the value of the

inventory in an effective manner. On the other hand, the last inventory asset is recorded as sold

firstly.

Average Costs: Average cost method would emerge total costs of goods which are

available for sales and divide it by the total sum of the product from starting inventory and

purchases.

4

(Vinayagamoorthi and et. al., 2012).

Job Costing System: This is elaborated as the tool of recording costs of manufacturing

job, instead of process. Along with the Job costing systems, a management accountant could

track of cost of each job, handling data that are usually highly concerned to operations of the

organisation. Job costing normally said that the particular accounting tool are used to track

expense of producing a product. This is the best tool that can be implemented by the organisation

for making the new product efficiently.

Price Optimization System: Under this system, consumer perspective would be assessed

regarding the company’s product price in an effective manner. This is the tool via which the

price of the product is identified in an effective manner which can be used for making the

business objectives in an effective manner. Via this tool, organisation is totally relied upon the

management accountant, who by using various tools, make the price of the product in an

effective manner. Now, this can be simply said that the management of IMDA TECH would

ultimately leads to gain the sustainability.

Inventory management system: This is the system which is implemented for making

the inventory efficiently. Via Inventory management system, firm would track products through

whole supply chain of it an organisation operates in. Which comprises each from manufacturing

to retail, warehousing to shipping, and whole movements of stock and parts between. Inventory

is managed via LIFO, FIFO and AVCO method (Macinati and Anessi-Pessina, 2014).

LIFO method: This stands for “Last in, First Out”. Which is implemented to place an

accounting value on the inventory. LIFO method operates as per the assumption that the last item

of inventory purchased is firstly sold out. On the other hand, this is rightly said that the new

inventory assets are entered firstly and then it is sold firstly.

FIFO method: This is the inventory valuation method, under which firstly goods are

purchased, are sold out firstly. Various organisation uses this method to optimise the value of the

inventory in an effective manner. On the other hand, the last inventory asset is recorded as sold

firstly.

Average Costs: Average cost method would emerge total costs of goods which are

available for sales and divide it by the total sum of the product from starting inventory and

purchases.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Diverse methods used for management accounting reporting:

Reporting is the best tool which can be used by the organisation for doing the business

objectives in an effective manner. Managerial accounting likewise related to the inner

information that can be used for planning, regulating, decision making and calculating

performance. These kinds of the reports are consistently produced via accounting and book-

keeping period, as per the needs. As, various managers assess these reports to highlight specific

patterns and convert them into an effective information for the organisation. Here are some of the

reports are mentioned hereunder:

Budget Reports: This reports are mostly complicated in assessing organisation

performance and are produced as a whole for small organisations and, department wise, for

broader companies. Although, each organisation forms an entire budget to know grand scheme

of their firm. Although, each organisation forms an entire budget to know about the business.

Budget forecast is formed which is relied upon the earlier experiences, via huge budget always

supplies for the unexpected situations which could emerge. An organisation’s budget lists whole

of the sources of income and expenditures. An organisation tries to attain its targets and mission

at the time of staying throughout the budgeted amount.

Account Receivable Ageing reports: If the organisation totally based upon extending

credit, then account receivable aging reports are crucial to it. By breaking down, remaining

balances of the client into the particular period which enables the managers to determine

defaulters and identify the issues in the company collection process (Lim, 2011). In this, there is

always few bad debts which are required to be written off. Although, organisation must need to

know who owes from the organisation and who owes you what.

Performance Reports: This is formed to review the performance of the organisation as a

whole and every employee at the end of the team. Divisional performance reports are likewise

produced in the big firms. Managers implement these kind of performance reports in order to

form key strategic decisions about the future of the firm. Individuals are usually awarded for

their commitment to the firm and under performers are dealt with as needed. This reports

likewise offers depth investigation into the working of the organisation.

M1

Management accounting systems are the best tools for gaining the productivity in the

IMDA TECH company. By implementing various management accounting systems, company

5

Reporting is the best tool which can be used by the organisation for doing the business

objectives in an effective manner. Managerial accounting likewise related to the inner

information that can be used for planning, regulating, decision making and calculating

performance. These kinds of the reports are consistently produced via accounting and book-

keeping period, as per the needs. As, various managers assess these reports to highlight specific

patterns and convert them into an effective information for the organisation. Here are some of the

reports are mentioned hereunder:

Budget Reports: This reports are mostly complicated in assessing organisation

performance and are produced as a whole for small organisations and, department wise, for

broader companies. Although, each organisation forms an entire budget to know grand scheme

of their firm. Although, each organisation forms an entire budget to know about the business.

Budget forecast is formed which is relied upon the earlier experiences, via huge budget always

supplies for the unexpected situations which could emerge. An organisation’s budget lists whole

of the sources of income and expenditures. An organisation tries to attain its targets and mission

at the time of staying throughout the budgeted amount.

Account Receivable Ageing reports: If the organisation totally based upon extending

credit, then account receivable aging reports are crucial to it. By breaking down, remaining

balances of the client into the particular period which enables the managers to determine

defaulters and identify the issues in the company collection process (Lim, 2011). In this, there is

always few bad debts which are required to be written off. Although, organisation must need to

know who owes from the organisation and who owes you what.

Performance Reports: This is formed to review the performance of the organisation as a

whole and every employee at the end of the team. Divisional performance reports are likewise

produced in the big firms. Managers implement these kind of performance reports in order to

form key strategic decisions about the future of the firm. Individuals are usually awarded for

their commitment to the firm and under performers are dealt with as needed. This reports

likewise offers depth investigation into the working of the organisation.

M1

Management accounting systems are the best tools for gaining the productivity in the

IMDA TECH company. By implementing various management accounting systems, company

5

produce its products in lowering the product costs by removing the wastage costs from the

product. The product cost is minimised by way of using various accounting systems that can be

helpful for making the business sustainable and reliable (van Helden and Uddin, 2016). Now,

this is the most crucial tool that can be used for gaining the sustainability in an effective manner.

D1

Management accounting systems are useful which further able to make the diverse kinds

of accounting reports. IMDA TECH would ultimately help to integrate the management

accounting systems with the management accounting reporting which would assist to gain the

sustainable development efficiently.

TASK 2

P3 Calculate costs using appropriate techniques tools of cost analysis to prepare an income

statement using marginal and absorption costing:

Marginal costing method – This is the tool which consider all the variable costs while

calculating contribution. This is the most effective tool that could be used for selling or

production expenses against contribution. Marginal costing covers measuring of marginal cost

that is sum of whole direct costs like direct material cost, direct labour costs, variable

manufacturing and selling costs, any changes in the variable costs or units which are directly

influence income of the organisation. Marginal costing is the decision making tool that are

implemented to form an efficient decision about the diverse expenses which occurred by the

organisation.

The calculation of ascertaining net profit using marginal costing is:

Sales revenue + Marginal Cost of goods sold (opening stock + production – closing stock) =

Contribution - Fixed cost = Net profit

Absorption costing method – This is likewise recognised as an entire costing as it

includes whole production related expenses either variable or fixed. On the other hand, all the

manufacturing costs which comprises variable and fixed costs, are considered while calculating

net profits as per absorption costing.

Manufacturing expenses or cost of goods sold involves all direct expenses such as direct

material, direct labour, variable or fixed manufacturing expenses, these expenses are charged to

6

product. The product cost is minimised by way of using various accounting systems that can be

helpful for making the business sustainable and reliable (van Helden and Uddin, 2016). Now,

this is the most crucial tool that can be used for gaining the sustainability in an effective manner.

D1

Management accounting systems are useful which further able to make the diverse kinds

of accounting reports. IMDA TECH would ultimately help to integrate the management

accounting systems with the management accounting reporting which would assist to gain the

sustainable development efficiently.

TASK 2

P3 Calculate costs using appropriate techniques tools of cost analysis to prepare an income

statement using marginal and absorption costing:

Marginal costing method – This is the tool which consider all the variable costs while

calculating contribution. This is the most effective tool that could be used for selling or

production expenses against contribution. Marginal costing covers measuring of marginal cost

that is sum of whole direct costs like direct material cost, direct labour costs, variable

manufacturing and selling costs, any changes in the variable costs or units which are directly

influence income of the organisation. Marginal costing is the decision making tool that are

implemented to form an efficient decision about the diverse expenses which occurred by the

organisation.

The calculation of ascertaining net profit using marginal costing is:

Sales revenue + Marginal Cost of goods sold (opening stock + production – closing stock) =

Contribution - Fixed cost = Net profit

Absorption costing method – This is likewise recognised as an entire costing as it

includes whole production related expenses either variable or fixed. On the other hand, all the

manufacturing costs which comprises variable and fixed costs, are considered while calculating

net profits as per absorption costing.

Manufacturing expenses or cost of goods sold involves all direct expenses such as direct

material, direct labour, variable or fixed manufacturing expenses, these expenses are charged to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

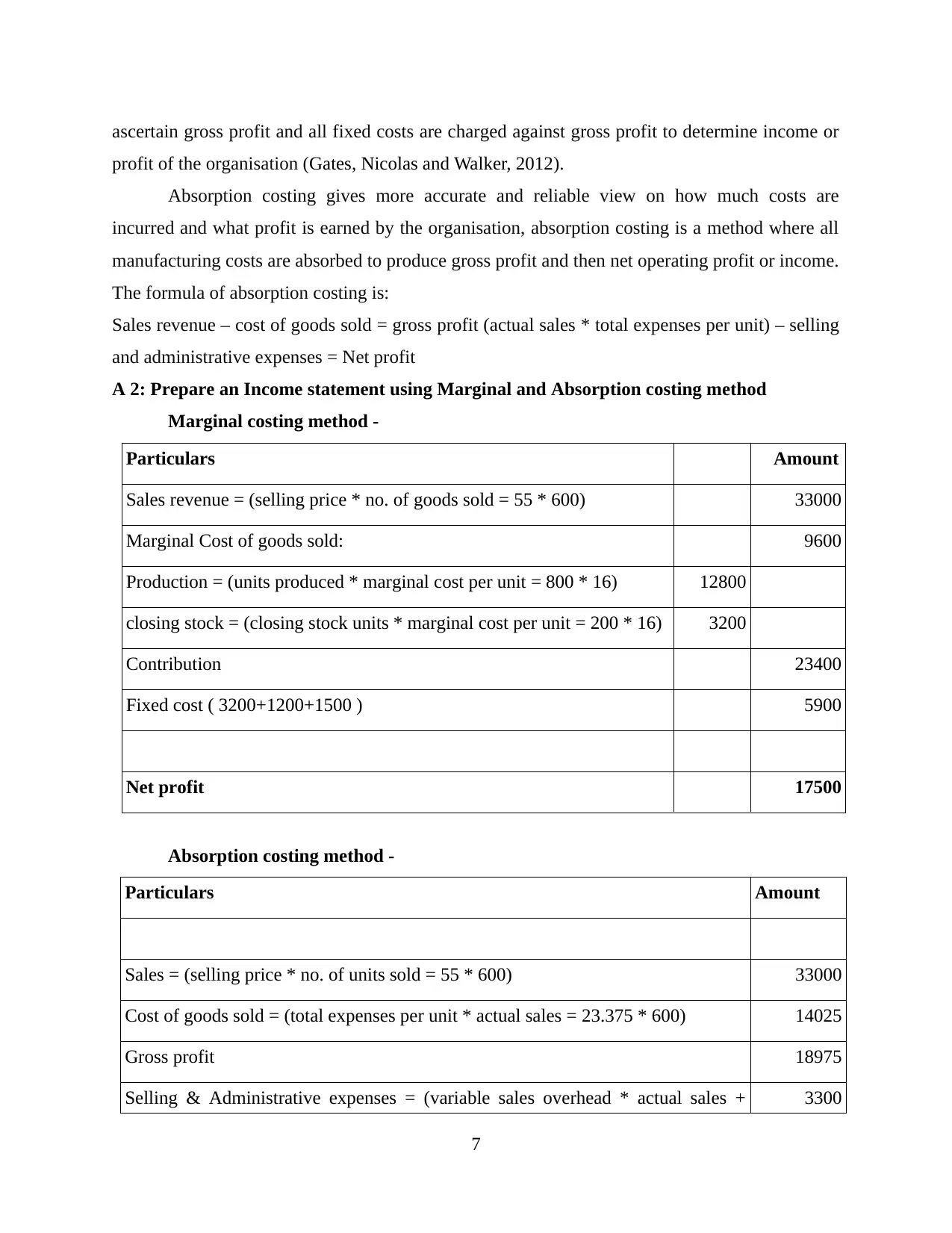

ascertain gross profit and all fixed costs are charged against gross profit to determine income or

profit of the organisation (Gates, Nicolas and Walker, 2012).

Absorption costing gives more accurate and reliable view on how much costs are

incurred and what profit is earned by the organisation, absorption costing is a method where all

manufacturing costs are absorbed to produce gross profit and then net operating profit or income.

The formula of absorption costing is:

Sales revenue – cost of goods sold = gross profit (actual sales * total expenses per unit) – selling

and administrative expenses = Net profit

A 2: Prepare an Income statement using Marginal and Absorption costing method

Marginal costing method -

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 * 16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Absorption costing method -

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales + 3300

7

profit of the organisation (Gates, Nicolas and Walker, 2012).

Absorption costing gives more accurate and reliable view on how much costs are

incurred and what profit is earned by the organisation, absorption costing is a method where all

manufacturing costs are absorbed to produce gross profit and then net operating profit or income.

The formula of absorption costing is:

Sales revenue – cost of goods sold = gross profit (actual sales * total expenses per unit) – selling

and administrative expenses = Net profit

A 2: Prepare an Income statement using Marginal and Absorption costing method

Marginal costing method -

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 * 16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Absorption costing method -

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales + 3300

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

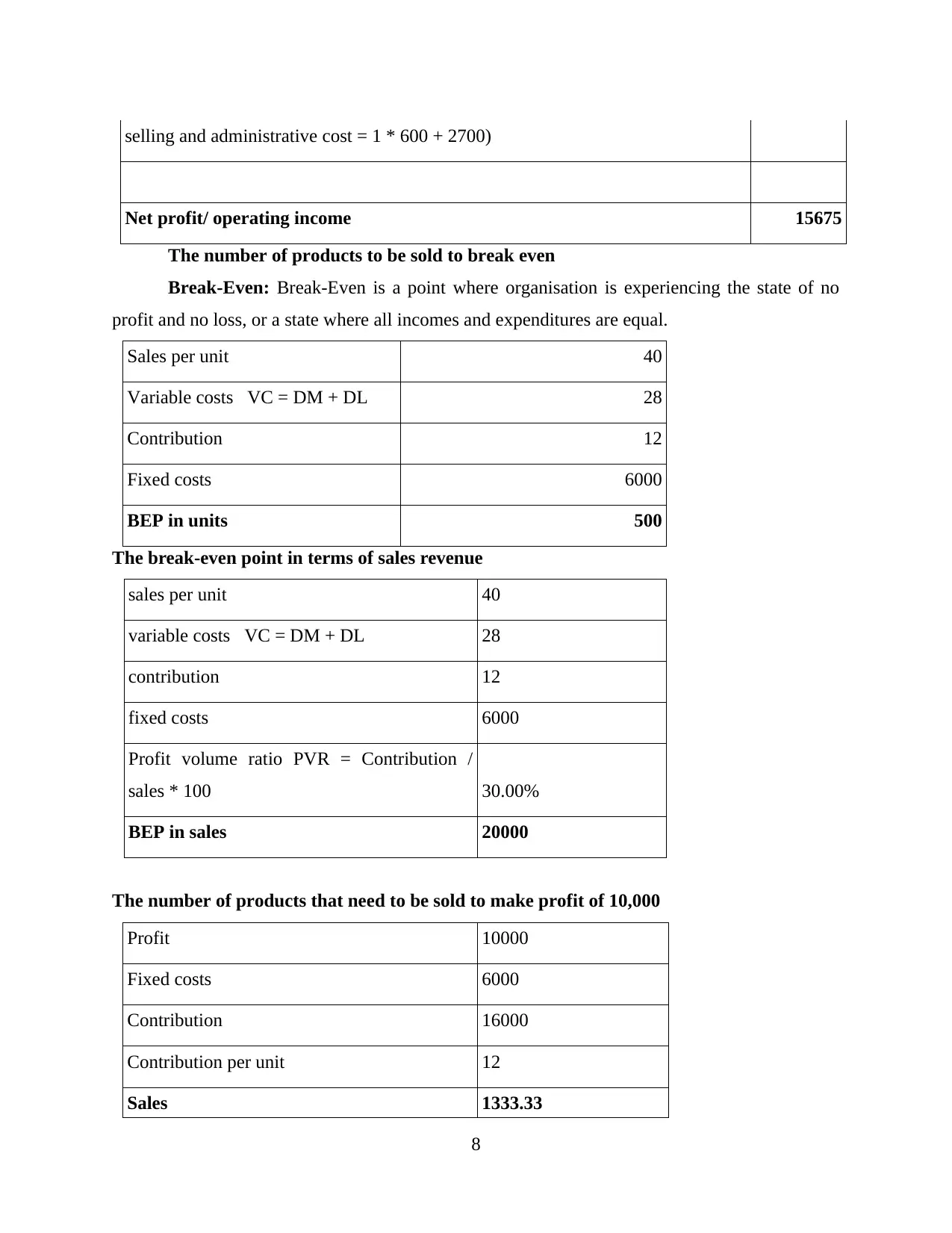

selling and administrative cost = 1 * 600 + 2700)

Net profit/ operating income 15675

The number of products to be sold to break even

Break-Even: Break-Even is a point where organisation is experiencing the state of no

profit and no loss, or a state where all incomes and expenditures are equal.

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

The break-even point in terms of sales revenue

sales per unit 40

variable costs VC = DM + DL 28

contribution 12

fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

The number of products that need to be sold to make profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

8

Net profit/ operating income 15675

The number of products to be sold to break even

Break-Even: Break-Even is a point where organisation is experiencing the state of no

profit and no loss, or a state where all incomes and expenditures are equal.

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

The break-even point in terms of sales revenue

sales per unit 40

variable costs VC = DM + DL 28

contribution 12

fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

The number of products that need to be sold to make profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

8

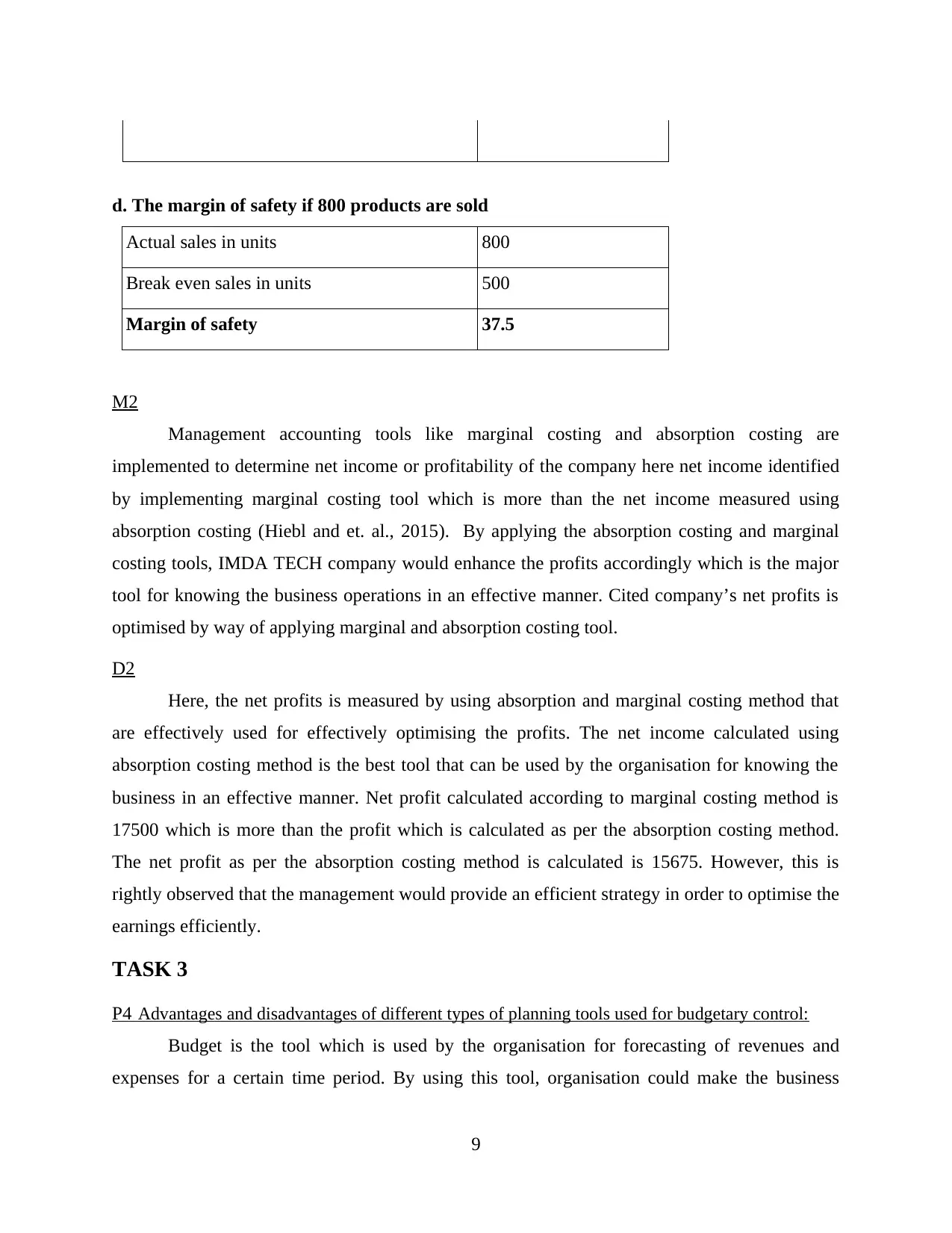

d. The margin of safety if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2

Management accounting tools like marginal costing and absorption costing are

implemented to determine net income or profitability of the company here net income identified

by implementing marginal costing tool which is more than the net income measured using

absorption costing (Hiebl and et. al., 2015). By applying the absorption costing and marginal

costing tools, IMDA TECH company would enhance the profits accordingly which is the major

tool for knowing the business operations in an effective manner. Cited company’s net profits is

optimised by way of applying marginal and absorption costing tool.

D2

Here, the net profits is measured by using absorption and marginal costing method that

are effectively used for effectively optimising the profits. The net income calculated using

absorption costing method is the best tool that can be used by the organisation for knowing the

business in an effective manner. Net profit calculated according to marginal costing method is

17500 which is more than the profit which is calculated as per the absorption costing method.

The net profit as per the absorption costing method is calculated is 15675. However, this is

rightly observed that the management would provide an efficient strategy in order to optimise the

earnings efficiently.

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control:

Budget is the tool which is used by the organisation for forecasting of revenues and

expenses for a certain time period. By using this tool, organisation could make the business

9

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2

Management accounting tools like marginal costing and absorption costing are

implemented to determine net income or profitability of the company here net income identified

by implementing marginal costing tool which is more than the net income measured using

absorption costing (Hiebl and et. al., 2015). By applying the absorption costing and marginal

costing tools, IMDA TECH company would enhance the profits accordingly which is the major

tool for knowing the business operations in an effective manner. Cited company’s net profits is

optimised by way of applying marginal and absorption costing tool.

D2

Here, the net profits is measured by using absorption and marginal costing method that

are effectively used for effectively optimising the profits. The net income calculated using

absorption costing method is the best tool that can be used by the organisation for knowing the

business in an effective manner. Net profit calculated according to marginal costing method is

17500 which is more than the profit which is calculated as per the absorption costing method.

The net profit as per the absorption costing method is calculated is 15675. However, this is

rightly observed that the management would provide an efficient strategy in order to optimise the

earnings efficiently.

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control:

Budget is the tool which is used by the organisation for forecasting of revenues and

expenses for a certain time period. By using this tool, organisation could make the business

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

objectives in an effective manner so that they could make an efficient business decision in an

effective manner. Budget is the tool that can be used by the firm for making the business

objectives effectively. Although, this is rightly said that the management would effectively

implement an efficient strategy that can be helpful for the organisation for making the business

objectives in an effective manner. With the help of various budgets, organisation would require

to form certain objectives in an effective manner. Here are so many budgets which is used by the

organisation for making the business organisation.

Cash budgets: This is the budget under which all the cash related expenses and incomes are

calculated for a particular period of time (Jalaludin, Sulaiman and Nazli Nik Ahmad, 2011).

Now, management of the cited firm would consider all the cash related items. Cash budgets is

the most efficient tool which is used for knowing the future requirement and availability of the

cash for a certain period of time.

Advantages:

Cash budget is the most effective tool which helps to identify the cash related revenues

and expenditures for a certain period of time. This assist the management to focus their

attention on the crucial matters which is not proceeding as per the plan. This also assist to

improve communication, sound understanding and effective link among employees.

This budget assist to co-ordinate activities of whole division in a firm.

This assist the management to think ahead and devise an efficient manner of maintaining

resources.

This assist in lowering the costs of the product and optimise the profits in an effective

manner.

Disadvantages:

The feasibility of this budget is totally relied upon the operation of staff.

This is made on subjective forecasting.

This is too costly to operate a budget.

This might emerge a more time to attain.

This could limit the morale and productivity if the pre-set objectives are not genuine.

Master Budget: This is the budget which acts like the summary that form its component

functional budgets and that are totally approved considered and employed. This comprises

budget which becomes the master budget (Zang, 2011). Although, summary budget is considered

10

effective manner. Budget is the tool that can be used by the firm for making the business

objectives effectively. Although, this is rightly said that the management would effectively

implement an efficient strategy that can be helpful for the organisation for making the business

objectives in an effective manner. With the help of various budgets, organisation would require

to form certain objectives in an effective manner. Here are so many budgets which is used by the

organisation for making the business organisation.

Cash budgets: This is the budget under which all the cash related expenses and incomes are

calculated for a particular period of time (Jalaludin, Sulaiman and Nazli Nik Ahmad, 2011).

Now, management of the cited firm would consider all the cash related items. Cash budgets is

the most efficient tool which is used for knowing the future requirement and availability of the

cash for a certain period of time.

Advantages:

Cash budget is the most effective tool which helps to identify the cash related revenues

and expenditures for a certain period of time. This assist the management to focus their

attention on the crucial matters which is not proceeding as per the plan. This also assist to

improve communication, sound understanding and effective link among employees.

This budget assist to co-ordinate activities of whole division in a firm.

This assist the management to think ahead and devise an efficient manner of maintaining

resources.

This assist in lowering the costs of the product and optimise the profits in an effective

manner.

Disadvantages:

The feasibility of this budget is totally relied upon the operation of staff.

This is made on subjective forecasting.

This is too costly to operate a budget.

This might emerge a more time to attain.

This could limit the morale and productivity if the pre-set objectives are not genuine.

Master Budget: This is the budget which acts like the summary that form its component

functional budgets and that are totally approved considered and employed. This comprises

budget which becomes the master budget (Zang, 2011). Although, summary budget is considered

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and approved, this becomes the master budget. Master budget is made by the budget committee

and renders instructions for each operation of a company.

Advantages:

Under this functional budgets are produced in a capsule form.

Whole functional budgets are available in the one report.

Whole functional budgets could be checked along with cross verification of information

rendered in the master budget.

This renders forecasted profit of the company.

This renders information which are linked to the firm.

This renders information that are connected to estimate balance sheet.

Master budget is more useful to the top level managers of the organisation. Henceforth, useful

information is presented in the capsule form.

Disadvantages:

Rigidity: Divisional staff is forced for the attainment of the pre-set target instead of

having practical difficulties in attaining the same. This is because of the pressure from the

top management. This leads to have low revenue forecasting and more expense

forecasting. Managers might not adopt advance opportunities for development of the

company.

Difficult to update: Master budget does not easy to modify. To add, modify or delete small

alterations needs more steps in the whole budget (Vakalfotis, Ballantine and Wall, 2013). This

covers lengthy descriptions and charts. Although, a master budget can’t be known to the layman.

Planning tools for budgetary control

Budgets can be prepared or analysed using various tools, that is forecasting and

contingency which helps an organisation to forecast the future events so that they can be

prepared for future circumstances, some of the applications and benefits of these tools are:

Contingency tool – Contingency planning is a tool of developing prevention measures in

advance for the events which can result in extreme loss, a good contingency plan should involve

good events too. From the help of contingency planning, an organisation can minimise the losses

incurred from events like natural disasters such as flood, fires etc. and organisational crises such

as strike, lock outs etc.

Forecasting tool– Forecasting planning is a process of prediction of future events, this

11

and renders instructions for each operation of a company.

Advantages:

Under this functional budgets are produced in a capsule form.

Whole functional budgets are available in the one report.

Whole functional budgets could be checked along with cross verification of information

rendered in the master budget.

This renders forecasted profit of the company.

This renders information which are linked to the firm.

This renders information that are connected to estimate balance sheet.

Master budget is more useful to the top level managers of the organisation. Henceforth, useful

information is presented in the capsule form.

Disadvantages:

Rigidity: Divisional staff is forced for the attainment of the pre-set target instead of

having practical difficulties in attaining the same. This is because of the pressure from the

top management. This leads to have low revenue forecasting and more expense

forecasting. Managers might not adopt advance opportunities for development of the

company.

Difficult to update: Master budget does not easy to modify. To add, modify or delete small

alterations needs more steps in the whole budget (Vakalfotis, Ballantine and Wall, 2013). This

covers lengthy descriptions and charts. Although, a master budget can’t be known to the layman.

Planning tools for budgetary control

Budgets can be prepared or analysed using various tools, that is forecasting and

contingency which helps an organisation to forecast the future events so that they can be

prepared for future circumstances, some of the applications and benefits of these tools are:

Contingency tool – Contingency planning is a tool of developing prevention measures in

advance for the events which can result in extreme loss, a good contingency plan should involve

good events too. From the help of contingency planning, an organisation can minimise the losses

incurred from events like natural disasters such as flood, fires etc. and organisational crises such

as strike, lock outs etc.

Forecasting tool– Forecasting planning is a process of prediction of future events, this

11

tool helps an organisation to pre determine future demand so that production can accordingly be

altered. Forecasting is a tool which anticipate future in order to expand business.

M3

There are various planning tools which are used for making and forecasting of the

budgets. Some of them are mentioned above. But, this is rightly said that the management

accounting systems are effectively used for making the business objectives in an effective

manner. Various budgets are implemented in the organisation for knowing and making the

variance analysis so that they would get to know about the in an effective manner. however, this

is simply said that the management of the cited organisation would requires to make an efficient

strategy that could help out to gain the sustainability in an effective manner. Apart from that,

organisation would implement an effective strategy which will make the business objectives

sustainable

D3

Accounting is an important concept that helps management in carrying t different operations of

business in an effective manner. It assists in maintaining proper records and transparency in the

working of an enterprise (Bodie, 2013). There are range of tools that are implemented in

business like cash flow statement, balance sheet etc. Which has their own significance. Through

same the current position of business can be identified at any point of time which is useful in

taking the future decisions for business. When the judgments are taken on the basis of previous

records and performances there are higher chances that the expected result are achieved. Apart

from this from the different planning tools like fund and cash flow statement gives a clear detail

of area in which the resources of firm are invested and shows how much returns were earned

from them. This way it is identified that what all went wrong and which areas were not

profitable. Budgetary tools are the major mode that are part of the planning. In this limits are set

for distinct department and therefore overall cost of the firm is controlled. Furthermore, it also

helps in providing guideline to the working staff which they have to keep in mind while

operating which is important to minimize the deviations in business. Cost accounting is widely

used in the refereed business which helps management in getting the record of cost as per the

product, department process and branch (Lukka and Vinnari, 2014). This way the management

12

altered. Forecasting is a tool which anticipate future in order to expand business.

M3

There are various planning tools which are used for making and forecasting of the

budgets. Some of them are mentioned above. But, this is rightly said that the management

accounting systems are effectively used for making the business objectives in an effective

manner. Various budgets are implemented in the organisation for knowing and making the

variance analysis so that they would get to know about the in an effective manner. however, this

is simply said that the management of the cited organisation would requires to make an efficient

strategy that could help out to gain the sustainability in an effective manner. Apart from that,

organisation would implement an effective strategy which will make the business objectives

sustainable

D3

Accounting is an important concept that helps management in carrying t different operations of

business in an effective manner. It assists in maintaining proper records and transparency in the

working of an enterprise (Bodie, 2013). There are range of tools that are implemented in

business like cash flow statement, balance sheet etc. Which has their own significance. Through

same the current position of business can be identified at any point of time which is useful in

taking the future decisions for business. When the judgments are taken on the basis of previous

records and performances there are higher chances that the expected result are achieved. Apart

from this from the different planning tools like fund and cash flow statement gives a clear detail

of area in which the resources of firm are invested and shows how much returns were earned

from them. This way it is identified that what all went wrong and which areas were not

profitable. Budgetary tools are the major mode that are part of the planning. In this limits are set

for distinct department and therefore overall cost of the firm is controlled. Furthermore, it also

helps in providing guideline to the working staff which they have to keep in mind while

operating which is important to minimize the deviations in business. Cost accounting is widely

used in the refereed business which helps management in getting the record of cost as per the

product, department process and branch (Lukka and Vinnari, 2014). This way the management

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.