Detailed Management Accounting Report: Imda Tech Corporation

VerifiedAdded on 2020/02/12

|18

|4262

|472

Report

AI Summary

This report delves into the realm of management accounting, emphasizing its pivotal role in organizational finance and decision-making. It commences with an introduction to management accounting, differentiating it from financial accounting, and underscores its significance as a tool for strategic decision-making within the context of Imda Tech, a UK-based manufacturing company. The report further explores various types of management accounting systems, including cost accounting, inventory management, price optimization, marginal costing, and ratio analysis, elucidating their applications across different functional departments. Task 1 provides a detailed explanation of management accounting and its distinctions from financial accounting. The report then highlights the importance of management accounting information as a decision-making tool for department managers within Imda Tech, focusing on its application in cost analysis, product and service production, marketing efforts, and financial forecasting. Task 2 includes calculations of absorption costing and marginal costing techniques. The report concludes by providing a comprehensive understanding of how Imda Tech can utilize accounting information to make business decisions.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION

In every business organisation, finance is very important part and in the absence of

sufficient quantity of finance no business firm can carried out its business activities and

functions. In order to manage the finance in an appropriate manner, firm requires to effective

management accounting system. With help of this system, business unit can able to prepare the

cost report and financial statement which aids in manage the financial record and analyse the

financial performance of the organisation. In a simple word it can be said that it is a process of

analysis, interpretation, examination of accounting information which can measured by

formulating of financial accounting, report and statements (Ax and Greve, 2016). These

accounting report and statements assist to business unit in taking the decision related to

allocation of fund, developing policies and practices, maintain the daily operational plans and

other purpose of the organisation. The following project report provides a depth knowledge and

understanding about the management of finance and accounting and how it is used in the taking

business decisions with respect of Imda Tech corporation. It is famous manufacturing

1

In every business organisation, finance is very important part and in the absence of

sufficient quantity of finance no business firm can carried out its business activities and

functions. In order to manage the finance in an appropriate manner, firm requires to effective

management accounting system. With help of this system, business unit can able to prepare the

cost report and financial statement which aids in manage the financial record and analyse the

financial performance of the organisation. In a simple word it can be said that it is a process of

analysis, interpretation, examination of accounting information which can measured by

formulating of financial accounting, report and statements (Ax and Greve, 2016). These

accounting report and statements assist to business unit in taking the decision related to

allocation of fund, developing policies and practices, maintain the daily operational plans and

other purpose of the organisation. The following project report provides a depth knowledge and

understanding about the management of finance and accounting and how it is used in the taking

business decisions with respect of Imda Tech corporation. It is famous manufacturing

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organisation in the UK which produce special charger for mobile telephones and other carry on

gadgets for retail outlet in the UK. The importance of management accounting information as a

decision making tool in the cited venture has been also discussed in this report. In addition to

this, various types of management accounting system and its implication has been also addressed

in this report.

TASK 1

a) (i) Explanation about the management accounting and to distinguish management accounting

from financial accounting

Management accounting is a systematic process of preparing management reports, accounts,

financial statements which assists in analysing, interpreting and examining of financial

information of the organisation. With assistance of these report and statements of account,

company can easily take the relevant decision about the allocation of fund, managing the risk,

daily operation related decision etc. In a simple word it can be said that management accounting

is the provisions of accounting information which used in the business for taking various

business related information. As per the view of (Brown and et.al., 2016) management

accounting is a profession that involves partnering in management decision making, devising

planning and performance management system, and providing expertise in financial reporting

and control to aid management in the formulation and implementation of the business strategy.

Financial accounting is quite different from the management accounting as financial

accounting considers on the financial statements which are allocated among stockholders,

lenders, financial analysts and other outsides of the organisation. On the other hand management

accounting considers on rendering information within the organisation so that its management

can operate the company more effectively and appropriately (Daskalakis, Devanur and

Weinberg, 2015). In a simple word it can be said that financial accounting is an accounting

system which considers on the formulation of financial statements of corporation in order to

render the financial information to the interested parties. On the other hand management

accounting provides relevant information to the manager to make policies, plans and strategies

for running the business effectively.

Following are some major differences between the management accounting and financial

accounting

2

gadgets for retail outlet in the UK. The importance of management accounting information as a

decision making tool in the cited venture has been also discussed in this report. In addition to

this, various types of management accounting system and its implication has been also addressed

in this report.

TASK 1

a) (i) Explanation about the management accounting and to distinguish management accounting

from financial accounting

Management accounting is a systematic process of preparing management reports, accounts,

financial statements which assists in analysing, interpreting and examining of financial

information of the organisation. With assistance of these report and statements of account,

company can easily take the relevant decision about the allocation of fund, managing the risk,

daily operation related decision etc. In a simple word it can be said that management accounting

is the provisions of accounting information which used in the business for taking various

business related information. As per the view of (Brown and et.al., 2016) management

accounting is a profession that involves partnering in management decision making, devising

planning and performance management system, and providing expertise in financial reporting

and control to aid management in the formulation and implementation of the business strategy.

Financial accounting is quite different from the management accounting as financial

accounting considers on the financial statements which are allocated among stockholders,

lenders, financial analysts and other outsides of the organisation. On the other hand management

accounting considers on rendering information within the organisation so that its management

can operate the company more effectively and appropriately (Daskalakis, Devanur and

Weinberg, 2015). In a simple word it can be said that financial accounting is an accounting

system which considers on the formulation of financial statements of corporation in order to

render the financial information to the interested parties. On the other hand management

accounting provides relevant information to the manager to make policies, plans and strategies

for running the business effectively.

Following are some major differences between the management accounting and financial

accounting

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial accounting includes monetary information whereas management accounting

involves monetary and non monetary information.

The major objective of the financial accounting is to provide financial information to

outsiders. On the other hand management accounting main aim to aids in planning and

decision making process by rendering detailed information on various business related

matters (Giri and Sharma, 2014).

Financial accounting statements are generally formulated at the end of the accounting

period which is usually one year. On the other hand management accounting reports are

prepared as per the requirement of the corporation.

In the financial accounting publishing and auditing are required by statutory auditors. On

the other hand in the management accounting neither published nor audited by statutory

auditors (Guinea, 2016).

Financial accounting are publicly published in order to report the financial success to the

external audiences hence confidentiality is not maintained. On the other hand in the

context of management accounting, report are prepared by the manger and it keeps full

confidential.

With assistance of management accounting, company can maintain its financial record

and rep[port and use them according to the financial activities and functions.

ii) Importance and significance of management accounting information as a decision making

tools for department manager

Imda Tech company is famous manufacturing corporation in the UK which deals with

mobile chargers and gadgets for retail outlet. It is very important for the organisation to take

strategic decision making for business success and growth in the competitive market. In order to

take the strategic decision related to allocation of fund, long term and short term decision related

to sales performance, corporation required to consider management accounting information.

Following are some importance and use of management accounting information in taking the

decision related to business in the Imda Tech company-

In the Imda Tech company, manager can find out the way of attaining the business

objective by use of reports, financial accounts and other set of data.

3

involves monetary and non monetary information.

The major objective of the financial accounting is to provide financial information to

outsiders. On the other hand management accounting main aim to aids in planning and

decision making process by rendering detailed information on various business related

matters (Giri and Sharma, 2014).

Financial accounting statements are generally formulated at the end of the accounting

period which is usually one year. On the other hand management accounting reports are

prepared as per the requirement of the corporation.

In the financial accounting publishing and auditing are required by statutory auditors. On

the other hand in the management accounting neither published nor audited by statutory

auditors (Guinea, 2016).

Financial accounting are publicly published in order to report the financial success to the

external audiences hence confidentiality is not maintained. On the other hand in the

context of management accounting, report are prepared by the manger and it keeps full

confidential.

With assistance of management accounting, company can maintain its financial record

and rep[port and use them according to the financial activities and functions.

ii) Importance and significance of management accounting information as a decision making

tools for department manager

Imda Tech company is famous manufacturing corporation in the UK which deals with

mobile chargers and gadgets for retail outlet. It is very important for the organisation to take

strategic decision making for business success and growth in the competitive market. In order to

take the strategic decision related to allocation of fund, long term and short term decision related

to sales performance, corporation required to consider management accounting information.

Following are some importance and use of management accounting information in taking the

decision related to business in the Imda Tech company-

In the Imda Tech company, manager can find out the way of attaining the business

objective by use of reports, financial accounts and other set of data.

3

With assistance of management accounting, manager of the cited venture can analyse and

interpret the past performance in order to develop effective planning that is cost cutting,

pricing decision and other relevant decisions of the business (Järvinen, 2016).

Information which are served by the management accounting information system aids in

performing relevant cost analysis. With assistance of management accounting, company

can able to take the decision related to the specific kind of product and services

production and manufacturing activities. It assists in taking the decision related to

marketing efforts and plan.

Management accounting information renders a systematic analysis of data by use of

various tools such as budgeting, financial statement projection and balance scorecards.

With aid if this management accounting system company can take the decision related to

business activities and function in the existing as we;ll as future business (Schroeder,

Clark and Cathey, 2016).

Management accounting system also assists in predict cash flow and the impact of cash

flow on the business. It assist in identifying that from where will its revenue come from

and will the revenue increase and decrease in the future.

In the Imda Tech company manager can identify the future required resources and scope

of investment with help of management accounting system. They can forecast the future

revenue and take the decision related to future investment, allocation of fund within

business activities by help of existing accounting information.

B) Description of various types of management accounting systems and its use in various

functional department of the cited venture

Management accounting is a computerised application which collects the data from wider set of

operations like sales, cost of material, labour, inventory and other process in order to formulate

the report of business. With assistance of this management accounting system, company can able

to analyse its financial condition and forecast the future revenue. It aids in identity the various

information about the profitability and loss of business and according to management accounting

information company can be to take the decision related to business activities and function.

Cost accounting system- The cost accounting system have major objective is to provide the

relevant information and data about the cost and price of the product and services. In the Imda

4

interpret the past performance in order to develop effective planning that is cost cutting,

pricing decision and other relevant decisions of the business (Järvinen, 2016).

Information which are served by the management accounting information system aids in

performing relevant cost analysis. With assistance of management accounting, company

can able to take the decision related to the specific kind of product and services

production and manufacturing activities. It assists in taking the decision related to

marketing efforts and plan.

Management accounting information renders a systematic analysis of data by use of

various tools such as budgeting, financial statement projection and balance scorecards.

With aid if this management accounting system company can take the decision related to

business activities and function in the existing as we;ll as future business (Schroeder,

Clark and Cathey, 2016).

Management accounting system also assists in predict cash flow and the impact of cash

flow on the business. It assist in identifying that from where will its revenue come from

and will the revenue increase and decrease in the future.

In the Imda Tech company manager can identify the future required resources and scope

of investment with help of management accounting system. They can forecast the future

revenue and take the decision related to future investment, allocation of fund within

business activities by help of existing accounting information.

B) Description of various types of management accounting systems and its use in various

functional department of the cited venture

Management accounting is a computerised application which collects the data from wider set of

operations like sales, cost of material, labour, inventory and other process in order to formulate

the report of business. With assistance of this management accounting system, company can able

to analyse its financial condition and forecast the future revenue. It aids in identity the various

information about the profitability and loss of business and according to management accounting

information company can be to take the decision related to business activities and function.

Cost accounting system- The cost accounting system have major objective is to provide the

relevant information and data about the cost and price of the product and services. In the Imda

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tech company, cost accounting system provide a framework to manager in anticipating the sum

of total payment and cost of the product and services (Taleizadeh and et.al., 2017). Cost

accounting system generally used in the production process under which production department

manager can figure out the sum total of direct and indirect expenditures incurred in the

production process so as manager can estimate the total cost and expenses of the production in

the company.

Inventory management system- Inventory management system is related to the inventory of the

organisation. It is based on the computerised software which is beneficial for inventory tracking

because by use of this system, company can gather the information elated to distribution of

product and services, delivery, sales order. With help of this system, company can adjust the

item accordingly. In the context of Imda Tech Ltd company, this inventory management system

assist in creating order, conduct billing process and other documentation for the production

function (Taylor and Scapens, 2016). It can be said that with help of inventory management

system, company can easily mange the inventory and stock. With help of this tool, delivery and

distribution of product and services can mange within the market.

Price optimisation system- Price optimisation system can use in the selling department of

the Imda Tech Ltd company. Price optimisation system assist in determining various prices of

the product and services through different channels. It will assist in determining the relevant

pricing strategy for company's product and services. Price optimisation is the mathematical

analysis by the corporation to determine how customer will respond to different price for its

product and services through various channels. Sales and marketing department of the cited

venture can use this price optimisation system in order to set the prices of the product and

services. It will help in making analytical based prices that is reasonable for both the corporation

and customers.

Marginal costing- Marginal costing is very essential part of the management accounting system

which assist in taking the suitable pricing decision. It enables firm to derive the number of units

which it required to produce and sell for attaining the desired level of profit margin. The major

use of the marginal costing is that it assist in determine the level of margin of safety (Thai,

Varghese and Barker, 2015). It aids in making appropriate decision related to the cost and price

of the product and services within the organisation.

5

of total payment and cost of the product and services (Taleizadeh and et.al., 2017). Cost

accounting system generally used in the production process under which production department

manager can figure out the sum total of direct and indirect expenditures incurred in the

production process so as manager can estimate the total cost and expenses of the production in

the company.

Inventory management system- Inventory management system is related to the inventory of the

organisation. It is based on the computerised software which is beneficial for inventory tracking

because by use of this system, company can gather the information elated to distribution of

product and services, delivery, sales order. With help of this system, company can adjust the

item accordingly. In the context of Imda Tech Ltd company, this inventory management system

assist in creating order, conduct billing process and other documentation for the production

function (Taylor and Scapens, 2016). It can be said that with help of inventory management

system, company can easily mange the inventory and stock. With help of this tool, delivery and

distribution of product and services can mange within the market.

Price optimisation system- Price optimisation system can use in the selling department of

the Imda Tech Ltd company. Price optimisation system assist in determining various prices of

the product and services through different channels. It will assist in determining the relevant

pricing strategy for company's product and services. Price optimisation is the mathematical

analysis by the corporation to determine how customer will respond to different price for its

product and services through various channels. Sales and marketing department of the cited

venture can use this price optimisation system in order to set the prices of the product and

services. It will help in making analytical based prices that is reasonable for both the corporation

and customers.

Marginal costing- Marginal costing is very essential part of the management accounting system

which assist in taking the suitable pricing decision. It enables firm to derive the number of units

which it required to produce and sell for attaining the desired level of profit margin. The major

use of the marginal costing is that it assist in determine the level of margin of safety (Thai,

Varghese and Barker, 2015). It aids in making appropriate decision related to the cost and price

of the product and services within the organisation.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ratio analysis- Ratio analysis is another major part of the management accounting which used in

forecasting, making plan, communicating and coordination business activities and function. In

the context of stakeholder like employees, customer, supplier can get the information about the

profit and revenue generated in the business enterprise (Casini, Marone and Scozzafava, 2014)

In addition to this ration analysis aids management in getting the data about the extent to which

resources used by the employees.

TASK 2

Calculation of absorption costing and marginal costing technique

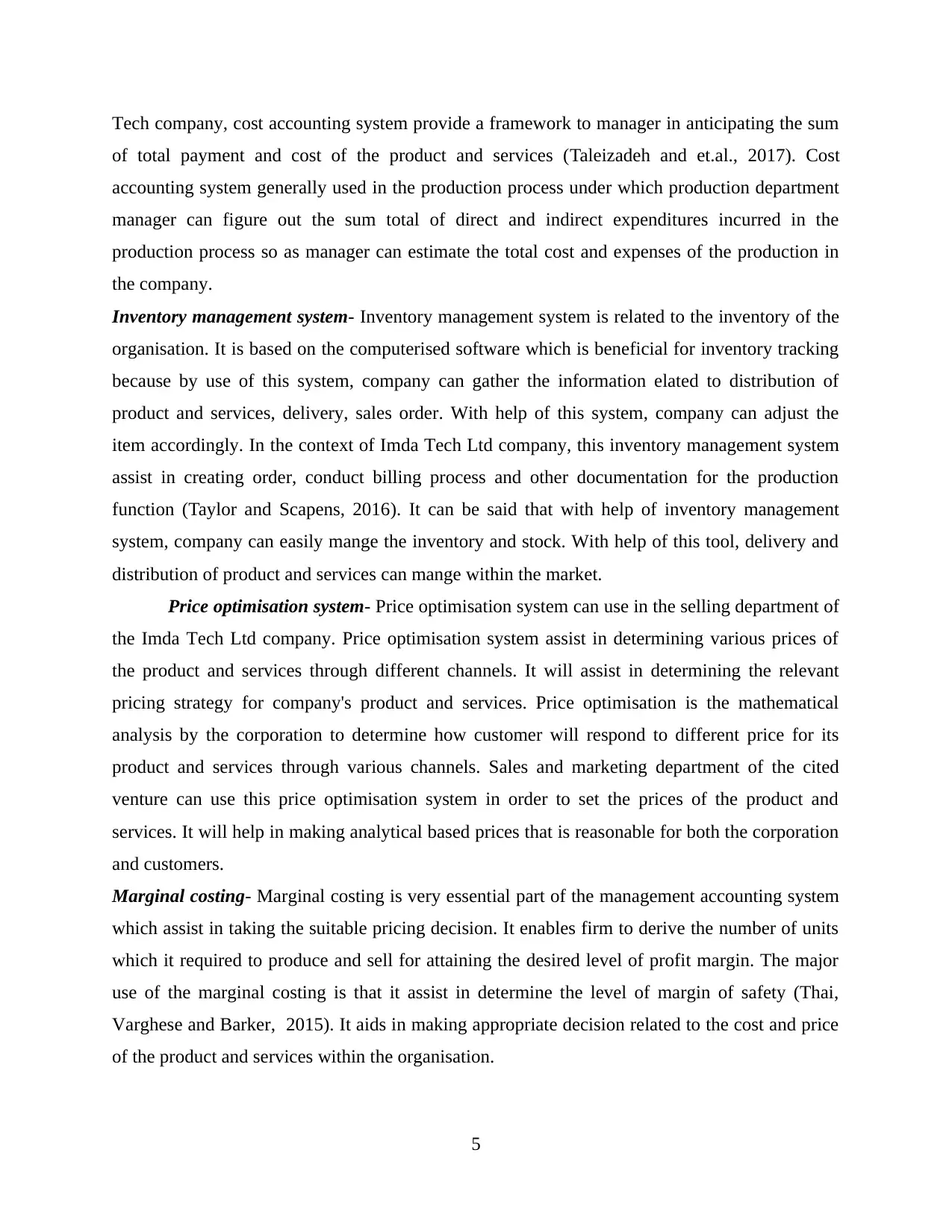

Marginal costing- Marginal costing is very essential part of the management accounting system

which assist in taking the suitable pricing decision. Major marginal costing used by organisation

in formulating the financial statements in every financial year. The major use of the marginal

costing is that it assist in determine the level of margin of safety (Christopher, 2016). It aids in

making appropriate decision related to the cost and price of the product and services within the

organisation. In this marginal costing, calculation of management account can take only

material, direct labour and variable production and fixed expenses. In a simple term it can be said

that marginal costing is an ascertainment, by differentiating between fixed cost and variable cost

of marginal cost. The increase and decrease in the total cost of production run for making one

additional unit of an item is known as marginal cisting.

6

forecasting, making plan, communicating and coordination business activities and function. In

the context of stakeholder like employees, customer, supplier can get the information about the

profit and revenue generated in the business enterprise (Casini, Marone and Scozzafava, 2014)

In addition to this ration analysis aids management in getting the data about the extent to which

resources used by the employees.

TASK 2

Calculation of absorption costing and marginal costing technique

Marginal costing- Marginal costing is very essential part of the management accounting system

which assist in taking the suitable pricing decision. Major marginal costing used by organisation

in formulating the financial statements in every financial year. The major use of the marginal

costing is that it assist in determine the level of margin of safety (Christopher, 2016). It aids in

making appropriate decision related to the cost and price of the product and services within the

organisation. In this marginal costing, calculation of management account can take only

material, direct labour and variable production and fixed expenses. In a simple term it can be said

that marginal costing is an ascertainment, by differentiating between fixed cost and variable cost

of marginal cost. The increase and decrease in the total cost of production run for making one

additional unit of an item is known as marginal cisting.

6

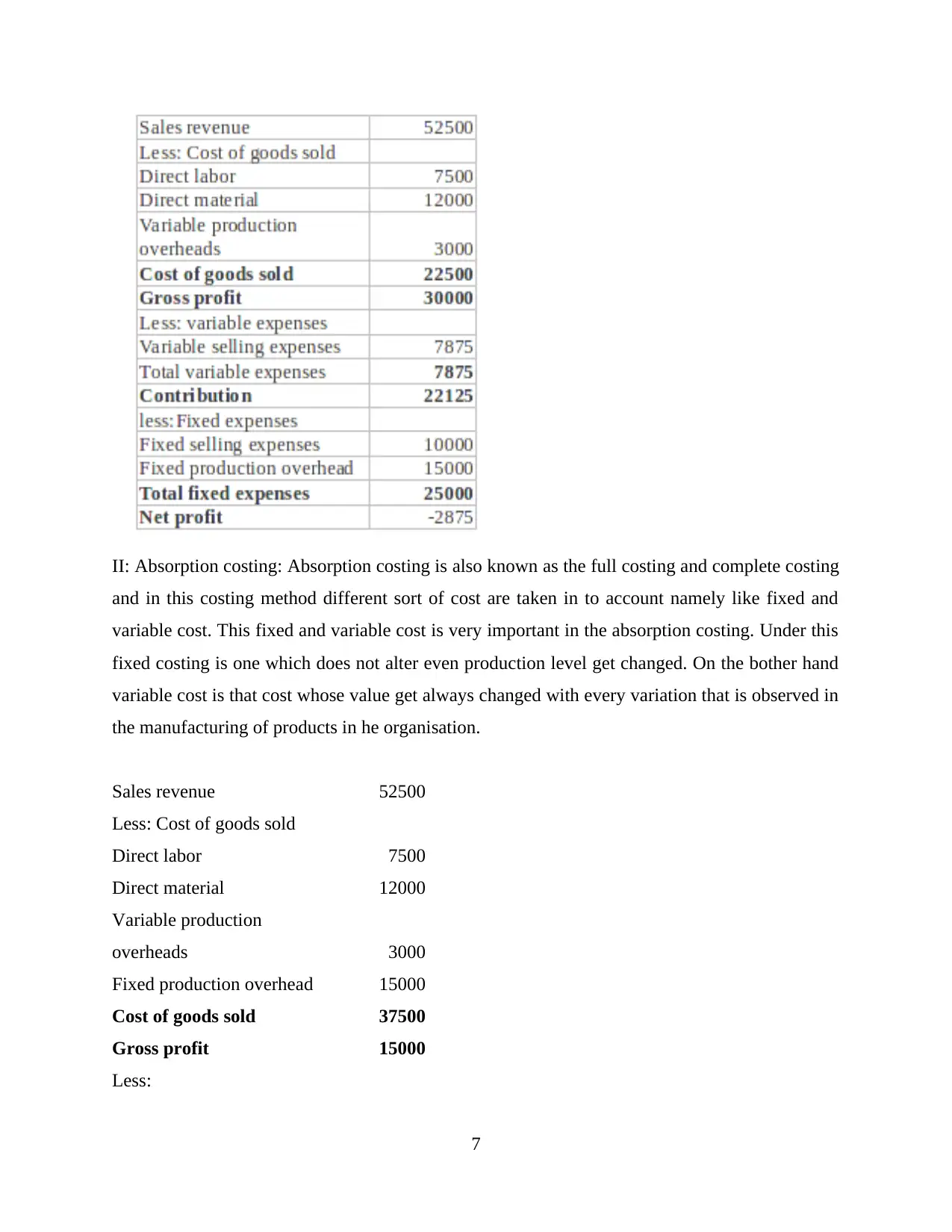

II: Absorption costing: Absorption costing is also known as the full costing and complete costing

and in this costing method different sort of cost are taken in to account namely like fixed and

variable cost. This fixed and variable cost is very important in the absorption costing. Under this

fixed costing is one which does not alter even production level get changed. On the bother hand

variable cost is that cost whose value get always changed with every variation that is observed in

the manufacturing of products in he organisation.

Sales revenue 52500

Less: Cost of goods sold

Direct labor 7500

Direct material 12000

Variable production

overheads 3000

Fixed production overhead 15000

Cost of goods sold 37500

Gross profit 15000

Less:

7

and in this costing method different sort of cost are taken in to account namely like fixed and

variable cost. This fixed and variable cost is very important in the absorption costing. Under this

fixed costing is one which does not alter even production level get changed. On the bother hand

variable cost is that cost whose value get always changed with every variation that is observed in

the manufacturing of products in he organisation.

Sales revenue 52500

Less: Cost of goods sold

Direct labor 7500

Direct material 12000

Variable production

overheads 3000

Fixed production overhead 15000

Cost of goods sold 37500

Gross profit 15000

Less:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable selling expenses 7875

Fixed selling expenses 10000

Total expenses 17875

Net profit -2875

TASK 3

A) Explanation about the various kinds of budget and their advantage and disadvantages

In the concept of management accounting, budget is another major important part through which

form can forecast the future business cost and expenses. It assists in taking the decision related to

allocation of fund and invest the amount of capital in the various business activities and function.

In a simple word it can be said that budget is an estimation of the revenue and expenses over a

specified future period. It is a process under which cost, revenue and resources over a specified

period can estimated by the organisation. Following are various kinds of budget prepared in the

organisation- Fixed budget and its advantage and disadvantage- In this budget of management

accounting, company can analyse current business performance and further prepare fixed

planning strategies to be implemented in the further month. Fixed budget refers to an

estimate of pre determined income and expenditure which once prepared, does not

change with the variation in the activity level attained. Fixed budget can not be modified

as per the actual volume and it is based on the assumption. It aids the management to set

the revenue and expenses for the period but it does not always provide accurate because it

is not always determine future needs and requirement of business (Christopher, 2016).

The major advantage of the fixed budget is that it allows organisation to compare

company's actual sales figures stack up against expected sales figures. In addition to this

it also allow company to prepare for expenses in advance. A fixed budget will not change

or fluctuate the amount from month to month and year to year. This makes company's

budget much more solid and the careful planning will make it easier to deal with

emergencies and stressful situation. On the other hand the greatest disadvantage of this

budget is that it have lack of flexibility and if company establishes a budget on a certain

8

Fixed selling expenses 10000

Total expenses 17875

Net profit -2875

TASK 3

A) Explanation about the various kinds of budget and their advantage and disadvantages

In the concept of management accounting, budget is another major important part through which

form can forecast the future business cost and expenses. It assists in taking the decision related to

allocation of fund and invest the amount of capital in the various business activities and function.

In a simple word it can be said that budget is an estimation of the revenue and expenses over a

specified future period. It is a process under which cost, revenue and resources over a specified

period can estimated by the organisation. Following are various kinds of budget prepared in the

organisation- Fixed budget and its advantage and disadvantage- In this budget of management

accounting, company can analyse current business performance and further prepare fixed

planning strategies to be implemented in the further month. Fixed budget refers to an

estimate of pre determined income and expenditure which once prepared, does not

change with the variation in the activity level attained. Fixed budget can not be modified

as per the actual volume and it is based on the assumption. It aids the management to set

the revenue and expenses for the period but it does not always provide accurate because it

is not always determine future needs and requirement of business (Christopher, 2016).

The major advantage of the fixed budget is that it allows organisation to compare

company's actual sales figures stack up against expected sales figures. In addition to this

it also allow company to prepare for expenses in advance. A fixed budget will not change

or fluctuate the amount from month to month and year to year. This makes company's

budget much more solid and the careful planning will make it easier to deal with

emergencies and stressful situation. On the other hand the greatest disadvantage of this

budget is that it have lack of flexibility and if company establishes a budget on a certain

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

level of sales volume and that volume enhances. If a company identifies

underperforming area of the business, it can not allocate the additional responses to help.

Flexible budget and its advantage and disadvantage- In the context of flexibility budget,

flexibility refers to the fluctuation in the financial activities of the entity. Flexible budget

is a financial plan which created for various activity level. In a simple word it can be said

that budget designed to change in the activity level is known as the flexible budget.

Flexible budget can easily fluctuate and modified in accordance with the activity level

attained. Flexible budget is suited for the corporation where there is great and high level

of variability in sales and production. The major advantage of flexible budget is that it

gives effective control during the budget period and it enables company to control the

cost because it shows where the actual performance deviated from the planning

performance (Dagiliene, 2015). On the other hand disadvantage of the flexible costing is

that it requires relevant information and business owner may find it difficult to get

accurate information even if they access to database and electronic process. Another

major disadvantage of this flexible budget is that sales result are the major component for

adjusting a flexible budget and it can adjust for other factor like skill of employees,

interest rates, degree of competition, prices of raw material etc.

B) Process of preparing budget

In the Imda Tech limited company, management accounting plays a very crucial role in

allocation of fund, managing business activities and taking the decisions related to the business

activities and functions. In order to manage the financial activities, corporation requires

formulating an effective budget. In order to prepare a systematic budget, company required to

consider on the following systematic process- Update budget assumptions: In this stage of budget process, Imda Tech company creates

the ideas for further business operation. In this stage company analyse assumption as well

recognizes current business performance. At this state manager of account department

analyse and assess the actual business performance and identified data are updated and

further assumption are acquired by manager in this stage (Fullerton, Kennedy and

Widener, 2014). Review bottlenecks: After analysing and recognise the current performance of the

organisation, in the next stage effectiveness of the organisation is reviewed by obtained

9

underperforming area of the business, it can not allocate the additional responses to help.

Flexible budget and its advantage and disadvantage- In the context of flexibility budget,

flexibility refers to the fluctuation in the financial activities of the entity. Flexible budget

is a financial plan which created for various activity level. In a simple word it can be said

that budget designed to change in the activity level is known as the flexible budget.

Flexible budget can easily fluctuate and modified in accordance with the activity level

attained. Flexible budget is suited for the corporation where there is great and high level

of variability in sales and production. The major advantage of flexible budget is that it

gives effective control during the budget period and it enables company to control the

cost because it shows where the actual performance deviated from the planning

performance (Dagiliene, 2015). On the other hand disadvantage of the flexible costing is

that it requires relevant information and business owner may find it difficult to get

accurate information even if they access to database and electronic process. Another

major disadvantage of this flexible budget is that sales result are the major component for

adjusting a flexible budget and it can adjust for other factor like skill of employees,

interest rates, degree of competition, prices of raw material etc.

B) Process of preparing budget

In the Imda Tech limited company, management accounting plays a very crucial role in

allocation of fund, managing business activities and taking the decisions related to the business

activities and functions. In order to manage the financial activities, corporation requires

formulating an effective budget. In order to prepare a systematic budget, company required to

consider on the following systematic process- Update budget assumptions: In this stage of budget process, Imda Tech company creates

the ideas for further business operation. In this stage company analyse assumption as well

recognizes current business performance. At this state manager of account department

analyse and assess the actual business performance and identified data are updated and

further assumption are acquired by manager in this stage (Fullerton, Kennedy and

Widener, 2014). Review bottlenecks: After analysing and recognise the current performance of the

organisation, in the next stage effectiveness of the organisation is reviewed by obtained

9

capability of organisation for investment and implementing action plan related to increase

company's revenue. Available funding:- In this stage, management of company observe available net funding

along with acquired profitability and expenses. In this stage manager analyse and assess

the actual available fund within the organisation for operate business activities and

functions. Creating budget package:- In this stage, overall expenses and revenue is obtained for

adequate production and distribution of service provided by the cited organisation. In this

stage proper budget is prepared for effectiveness of the company and increase its

efficiency at high level.

Obtain revenue forecast and department budget- After creating budget package. In the

next stage, manager of the cited organisation take the decision for further

implementation. Estimated income and department performance is forecasted for further

implementation.

c) Pricing strategies

Price is major factor in the business enterprise which define the product and services

value in the market. In order to gain effective success and competency, every firm required to set

it's some pricing strategy. Pricing strategy can be set for maximise profitability for each unit sold

or from the market overall. There are various kinds of pricing strategy such as market

penetration, cost leadership, price skimming etc. Pricing strategy is interrelated with preparing

planning for the cost (Jarzabkowski and Kaplan, 2015). By adopting effective pricing strategy

company can develop its own brand image in the market and acquire the large number of

customers. Company have to set the pricing strategy according to the market condition and

demand of the customer toward the product and services. In order to attract the large number of

customer and develop effective brand image on the market, company used effective pricing

strategy. Thus, pricing strategies are of various kinds to fit costs of product and devising

decisions for show of customers towards product choice. It determinant market position and

competitive strategies to set cost according to consumer's affordability. Cited venture have to

adopt effective pricing strategy in order to develop effective brand image in the market and

attract the large number of customer (Ax and Greve, 2016). Pricing strategy is only one which

distinguish company from the other rival and develop its own goodwill in the market.

10

company's revenue. Available funding:- In this stage, management of company observe available net funding

along with acquired profitability and expenses. In this stage manager analyse and assess

the actual available fund within the organisation for operate business activities and

functions. Creating budget package:- In this stage, overall expenses and revenue is obtained for

adequate production and distribution of service provided by the cited organisation. In this

stage proper budget is prepared for effectiveness of the company and increase its

efficiency at high level.

Obtain revenue forecast and department budget- After creating budget package. In the

next stage, manager of the cited organisation take the decision for further

implementation. Estimated income and department performance is forecasted for further

implementation.

c) Pricing strategies

Price is major factor in the business enterprise which define the product and services

value in the market. In order to gain effective success and competency, every firm required to set

it's some pricing strategy. Pricing strategy can be set for maximise profitability for each unit sold

or from the market overall. There are various kinds of pricing strategy such as market

penetration, cost leadership, price skimming etc. Pricing strategy is interrelated with preparing

planning for the cost (Jarzabkowski and Kaplan, 2015). By adopting effective pricing strategy

company can develop its own brand image in the market and acquire the large number of

customers. Company have to set the pricing strategy according to the market condition and

demand of the customer toward the product and services. In order to attract the large number of

customer and develop effective brand image on the market, company used effective pricing

strategy. Thus, pricing strategies are of various kinds to fit costs of product and devising

decisions for show of customers towards product choice. It determinant market position and

competitive strategies to set cost according to consumer's affordability. Cited venture have to

adopt effective pricing strategy in order to develop effective brand image in the market and

attract the large number of customer (Ax and Greve, 2016). Pricing strategy is only one which

distinguish company from the other rival and develop its own goodwill in the market.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.