Management Accounting Report: J Rotherham Financial Analysis

VerifiedAdded on 2021/02/20

|19

|3987

|347

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices, focusing on cost analysis, planning tools, and financial systems within an organization. The report begins with an introduction to management accounting and its significance, using J Rotherham, a manufacturing company, as a case study. It covers the differences between management and financial accounting, and explores various management accounting systems such as inventory management, cost accounting, and price optimization. The report further details different types of management accounting reports, including accounts receivable, inventory management, performance reports, and budget reports. Costing techniques, such as absorption and marginal costing, are explained, along with the reasons for analyzing profit variations. Planning tools, including budgeting, and their merits and demerits are discussed. The report also compares organizations that adopt accounting systems to solve financial problems. This report is valuable for students seeking to understand the practical application of management accounting in real-world business scenarios. This report is contributed by a student to be published on the website Desklib, which provides all the necessary AI based study tools for students.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

P1 Management accounting system and its demand in organisation..........................................1

P2 Different types of management accounting reports...............................................................3

Task 2...............................................................................................................................................4

P3 Calculation of cost with appropriate technique of cost analysis............................................4

b) Reason for analysing variations in profit ...............................................................................8

Task 3...............................................................................................................................................8

P4 Planning tools and its merits and demerits............................................................................8

Task 4.............................................................................................................................................10

P5 Comparison between organisation that adopts accounting system to solve financial

problems....................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCE.................................................................................................................................13

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

P1 Management accounting system and its demand in organisation..........................................1

P2 Different types of management accounting reports...............................................................3

Task 2...............................................................................................................................................4

P3 Calculation of cost with appropriate technique of cost analysis............................................4

b) Reason for analysing variations in profit ...............................................................................8

Task 3...............................................................................................................................................8

P4 Planning tools and its merits and demerits............................................................................8

Task 4.............................................................................................................................................10

P5 Comparison between organisation that adopts accounting system to solve financial

problems....................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCE.................................................................................................................................13

INTRODUCTION

Management accounting is study of accounts and transaction which is required to be

present by managers within organisation. It is the process of identifying, classifying, and

interpreting the accounts and information. The main aim of this report is to understand about

management accounting and its requirement within organisation (Arroyo, 2012). For

understanding this J Rotherham has been selected that is manufacturing organisation. It was

established in 1930 that manufacture stone and does architectural work on stone (Overview of J

Rotherham, 2019). This report will covered different topics such as management accounting and

its requirement, Methods which can be used for managing accounting reports and costing

technique that can help to decide the cost of organisation in order to maintain the profits.

Moreover, report discusses about planning tools which is used in budgetary control and different

type of accounting system to solve the financial problems within industry.

Task 1

P1 Management accounting system and its demand in organisation

Management accounting is defined as the process of monitoring, controlling and

evaluating the performance of the company for a specific period of time. It is very beneficial for

the internal stakeholders because it can help them to analyse actual status of the organisation. J

Rotherham Limited is a manufacturing company of hand carved stones currently working in

Yorkshire UK. It is used by all organisation to keep records of all transaction and increase the

profitability of organisation. Management refers planning, organising, staffing and controlling of

business information and activities. It help to maintain the accounts properly and increase the

working capacity of organisation. The main aim of management accounting to make easy

transaction and business decision.

Difference between management accounting and financial accounting

Basis Financial accounting Management accounting

Definition This is an accounting system which

focuses on preparation of financial

statement of a business entity. It is

used for internal or external

This system provides relevant

information that help to make

policies, strategies and plans for

running a business.

1

Management accounting is study of accounts and transaction which is required to be

present by managers within organisation. It is the process of identifying, classifying, and

interpreting the accounts and information. The main aim of this report is to understand about

management accounting and its requirement within organisation (Arroyo, 2012). For

understanding this J Rotherham has been selected that is manufacturing organisation. It was

established in 1930 that manufacture stone and does architectural work on stone (Overview of J

Rotherham, 2019). This report will covered different topics such as management accounting and

its requirement, Methods which can be used for managing accounting reports and costing

technique that can help to decide the cost of organisation in order to maintain the profits.

Moreover, report discusses about planning tools which is used in budgetary control and different

type of accounting system to solve the financial problems within industry.

Task 1

P1 Management accounting system and its demand in organisation

Management accounting is defined as the process of monitoring, controlling and

evaluating the performance of the company for a specific period of time. It is very beneficial for

the internal stakeholders because it can help them to analyse actual status of the organisation. J

Rotherham Limited is a manufacturing company of hand carved stones currently working in

Yorkshire UK. It is used by all organisation to keep records of all transaction and increase the

profitability of organisation. Management refers planning, organising, staffing and controlling of

business information and activities. It help to maintain the accounts properly and increase the

working capacity of organisation. The main aim of management accounting to make easy

transaction and business decision.

Difference between management accounting and financial accounting

Basis Financial accounting Management accounting

Definition This is an accounting system which

focuses on preparation of financial

statement of a business entity. It is

used for internal or external

This system provides relevant

information that help to make

policies, strategies and plans for

running a business.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

purpose.

Information It involves monetary information

only.

This contains monetary and non

monetary information.

Main objective Its main objective is to give

financial information to outsiders

like creditors, shareholders and

investors.

Its main objective is to make plans

and effective business decision

within organisation.

Management accounting system are used by managers to know the performance and

expand the business activities in a company (Wickramasinghe and Alawattage, 2012).

Management accounting system means a system which is used to get the information about

accounts and transaction within organisation. It help to maintain the proper records of

information and maintain the profitability (Fadzil and Rababah, 2012). The description of some

management accounting system are given as:

Inventory management system: This is important system that can help business

organisation to keep records of inventory and should place next order accordingly. This is mostly

used in inventory management and use it systematically. In J Rotherham, managers use this

system to track and manage the inventory or stock within organisation. In this company, it is

important for managers to track the raw material and manages it to increase the profitability. It is

manages by a software that help to analyse the data and generate reports. The manager of J

Rotherham uses different method that is described as:

FIFO: This means first in first out that states organisation should sell the product which

came firstly.

LIFO: Last in first out method means sell the products which came at last.

AVOC: In this method organisation sell goods and services which help to calculate

average cost for production.

Cost accounting system: This is an effective system which is used by manufactures and

other business concern to record production activities by using a perceptual inventory system. It

is require in all organisation to manage the cost as well as accounts in order to make profits.

Basically, this system works by tracking raw material as managers of J Rotherham go through

manufacturing stage and turn slowly in to finished goods in real time. It help to managers to

2

Information It involves monetary information

only.

This contains monetary and non

monetary information.

Main objective Its main objective is to give

financial information to outsiders

like creditors, shareholders and

investors.

Its main objective is to make plans

and effective business decision

within organisation.

Management accounting system are used by managers to know the performance and

expand the business activities in a company (Wickramasinghe and Alawattage, 2012).

Management accounting system means a system which is used to get the information about

accounts and transaction within organisation. It help to maintain the proper records of

information and maintain the profitability (Fadzil and Rababah, 2012). The description of some

management accounting system are given as:

Inventory management system: This is important system that can help business

organisation to keep records of inventory and should place next order accordingly. This is mostly

used in inventory management and use it systematically. In J Rotherham, managers use this

system to track and manage the inventory or stock within organisation. In this company, it is

important for managers to track the raw material and manages it to increase the profitability. It is

manages by a software that help to analyse the data and generate reports. The manager of J

Rotherham uses different method that is described as:

FIFO: This means first in first out that states organisation should sell the product which

came firstly.

LIFO: Last in first out method means sell the products which came at last.

AVOC: In this method organisation sell goods and services which help to calculate

average cost for production.

Cost accounting system: This is an effective system which is used by manufactures and

other business concern to record production activities by using a perceptual inventory system. It

is require in all organisation to manage the cost as well as accounts in order to make profits.

Basically, this system works by tracking raw material as managers of J Rotherham go through

manufacturing stage and turn slowly in to finished goods in real time. It help to managers to

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

focus on cost and improve the production process that help to increase the profitability. It is

required to give accurate cost by using software that help to maintain the profit margin.

Price optimisation system: This is the system that conclude mathematical analysis by an

industry to define how customers responds for different prices for products and services. It is

used by managers to set the prices of products and influence the customer. J Rotherham is

manufacturing company that works on stone as designing or Architectural work which influence

customers. It uses the software to fix the price of products and maintain the profitability within

organisation. Such as manager of J Rotherham bear all cost and expenses while manufacturing

the products and set the reasonable price. This process help organisation to meet with objectives

like maximisation of profit in a company (Grabner and Moers, 2013).

Presenting financial information

Financial information means information which is related to cash or monetary terms that

help to make business decision. It should be relevant to user, reliable, accurate and up to date

because it help to expand the further business activities. If information will be relevant or

accurate then manager of J Rotherham can make correct business decision. Moreover, it should

be up to date because without up to date managers can not think about future activities and

profitability. J Rotherham is uses job costing system that help to divide and track the cost and

revenues in order to perform organisation functions.

This information should be presented in proper and accurate way that can be understand

easily and managers can make business decision efficiently. If information should be

understandable them organisation can maximize the profits because there is no need to spent

extra money to get understand.

P2 Different types of management accounting reports

Management accounting reporting

Management accounting reporting is regulating on yearly basis by J Rotherham so that

strategies decision can be formulated by managers for the betterment of the organisation. Four

different types of reporting are followed by management of J Rotherham company.

Account receivable reports:

This is the collection tool that assuring the customers pay their invoices. Good

receivables management helps impede overdue payment or non-payment. It is a quick and

effective way to strengthen the company's financial or liquidity position. The report is also used

3

required to give accurate cost by using software that help to maintain the profit margin.

Price optimisation system: This is the system that conclude mathematical analysis by an

industry to define how customers responds for different prices for products and services. It is

used by managers to set the prices of products and influence the customer. J Rotherham is

manufacturing company that works on stone as designing or Architectural work which influence

customers. It uses the software to fix the price of products and maintain the profitability within

organisation. Such as manager of J Rotherham bear all cost and expenses while manufacturing

the products and set the reasonable price. This process help organisation to meet with objectives

like maximisation of profit in a company (Grabner and Moers, 2013).

Presenting financial information

Financial information means information which is related to cash or monetary terms that

help to make business decision. It should be relevant to user, reliable, accurate and up to date

because it help to expand the further business activities. If information will be relevant or

accurate then manager of J Rotherham can make correct business decision. Moreover, it should

be up to date because without up to date managers can not think about future activities and

profitability. J Rotherham is uses job costing system that help to divide and track the cost and

revenues in order to perform organisation functions.

This information should be presented in proper and accurate way that can be understand

easily and managers can make business decision efficiently. If information should be

understandable them organisation can maximize the profits because there is no need to spent

extra money to get understand.

P2 Different types of management accounting reports

Management accounting reporting

Management accounting reporting is regulating on yearly basis by J Rotherham so that

strategies decision can be formulated by managers for the betterment of the organisation. Four

different types of reporting are followed by management of J Rotherham company.

Account receivable reports:

This is the collection tool that assuring the customers pay their invoices. Good

receivables management helps impede overdue payment or non-payment. It is a quick and

effective way to strengthen the company's financial or liquidity position. The report is also used

3

by management of J Rotherham Limited to determine the effectiveness of the credit and

collection functions of the company. It is beneficial for the company as it may help to strengthen

the credit policy .

Inventory management reports:

This is a report that shows real time perception of the stock turnover in a accounting

period. This report is generated by manufacturing companies in order to keep track record of

inventory. In J Rotherham it is prepared by the managers to keep detailed information regarding

inventory that are used by the company to perform its operations activities. It help to manage

the report that can assist for inventory handling and real time stock management (Hilton and

Platt, 2013).

Performance Report:

Performance Report measured that result of an activity which is performed by an

individual. This report compare the actual final result with standard input of a specific activities

and variances are being figured out. For example ,Annual performance report analysis for each

employee that what they have contributed for an organisation in the term of performance. J

Rotherham measure the various aspect regarding the current performance of the employee with

their actual efficiency that can help to increase the efficiency and productivity.

Budget report

It is interim management accounting concepts that derives the variances from estimated

prediction with actual performance gained by organization. J Rotherham's managers are

generated the budget report to make sure that all the operational activities are performed in the

estimated budget or not. With the help of this budget report company can evaluate the accurate

output and managers can make appropriate financial decision.

Task 2

P3 Calculation of cost with appropriate technique of cost analysis

Cost volume profit is an analysing method that can be used to define how changes in cost

and volume affect organisation's operating income and net income. It involves flexible budget

and cost variance.

4

collection functions of the company. It is beneficial for the company as it may help to strengthen

the credit policy .

Inventory management reports:

This is a report that shows real time perception of the stock turnover in a accounting

period. This report is generated by manufacturing companies in order to keep track record of

inventory. In J Rotherham it is prepared by the managers to keep detailed information regarding

inventory that are used by the company to perform its operations activities. It help to manage

the report that can assist for inventory handling and real time stock management (Hilton and

Platt, 2013).

Performance Report:

Performance Report measured that result of an activity which is performed by an

individual. This report compare the actual final result with standard input of a specific activities

and variances are being figured out. For example ,Annual performance report analysis for each

employee that what they have contributed for an organisation in the term of performance. J

Rotherham measure the various aspect regarding the current performance of the employee with

their actual efficiency that can help to increase the efficiency and productivity.

Budget report

It is interim management accounting concepts that derives the variances from estimated

prediction with actual performance gained by organization. J Rotherham's managers are

generated the budget report to make sure that all the operational activities are performed in the

estimated budget or not. With the help of this budget report company can evaluate the accurate

output and managers can make appropriate financial decision.

Task 2

P3 Calculation of cost with appropriate technique of cost analysis

Cost volume profit is an analysing method that can be used to define how changes in cost

and volume affect organisation's operating income and net income. It involves flexible budget

and cost variance.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost: This means amount of money which is created business concern in order to

manufacture products and services. It is required in all organisation as it help to define the cost of

manufacturing activities. Different types of cost are defined as:

Direct and indirect cost: Direct cost means cost which is arises in directly

manner and it provides single cost that help to classify the cost in indirect and

direct. Where as indirect cost are arises in more than one business activity in order

to complete business objects.

Fixed and variable cost: Fixed cost are defined as a cost which can not change in

business activities or remain fixed. Where as variable cost can be change as per

requirement. It get changes by changing in the level of activity of material cost.

For instance, direct material and direct labour.

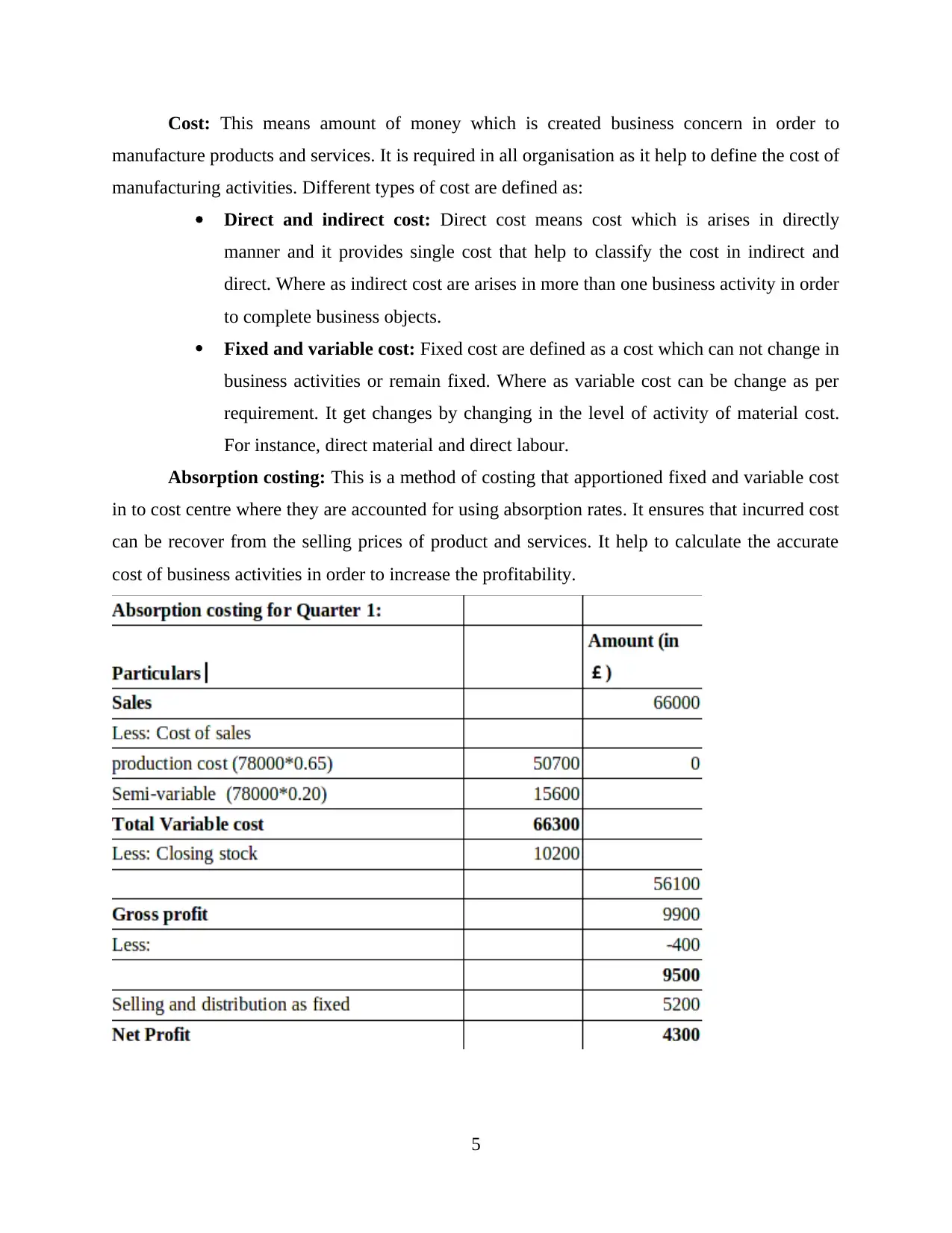

Absorption costing: This is a method of costing that apportioned fixed and variable cost

in to cost centre where they are accounted for using absorption rates. It ensures that incurred cost

can be recover from the selling prices of product and services. It help to calculate the accurate

cost of business activities in order to increase the profitability.

5

manufacture products and services. It is required in all organisation as it help to define the cost of

manufacturing activities. Different types of cost are defined as:

Direct and indirect cost: Direct cost means cost which is arises in directly

manner and it provides single cost that help to classify the cost in indirect and

direct. Where as indirect cost are arises in more than one business activity in order

to complete business objects.

Fixed and variable cost: Fixed cost are defined as a cost which can not change in

business activities or remain fixed. Where as variable cost can be change as per

requirement. It get changes by changing in the level of activity of material cost.

For instance, direct material and direct labour.

Absorption costing: This is a method of costing that apportioned fixed and variable cost

in to cost centre where they are accounted for using absorption rates. It ensures that incurred cost

can be recover from the selling prices of product and services. It help to calculate the accurate

cost of business activities in order to increase the profitability.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

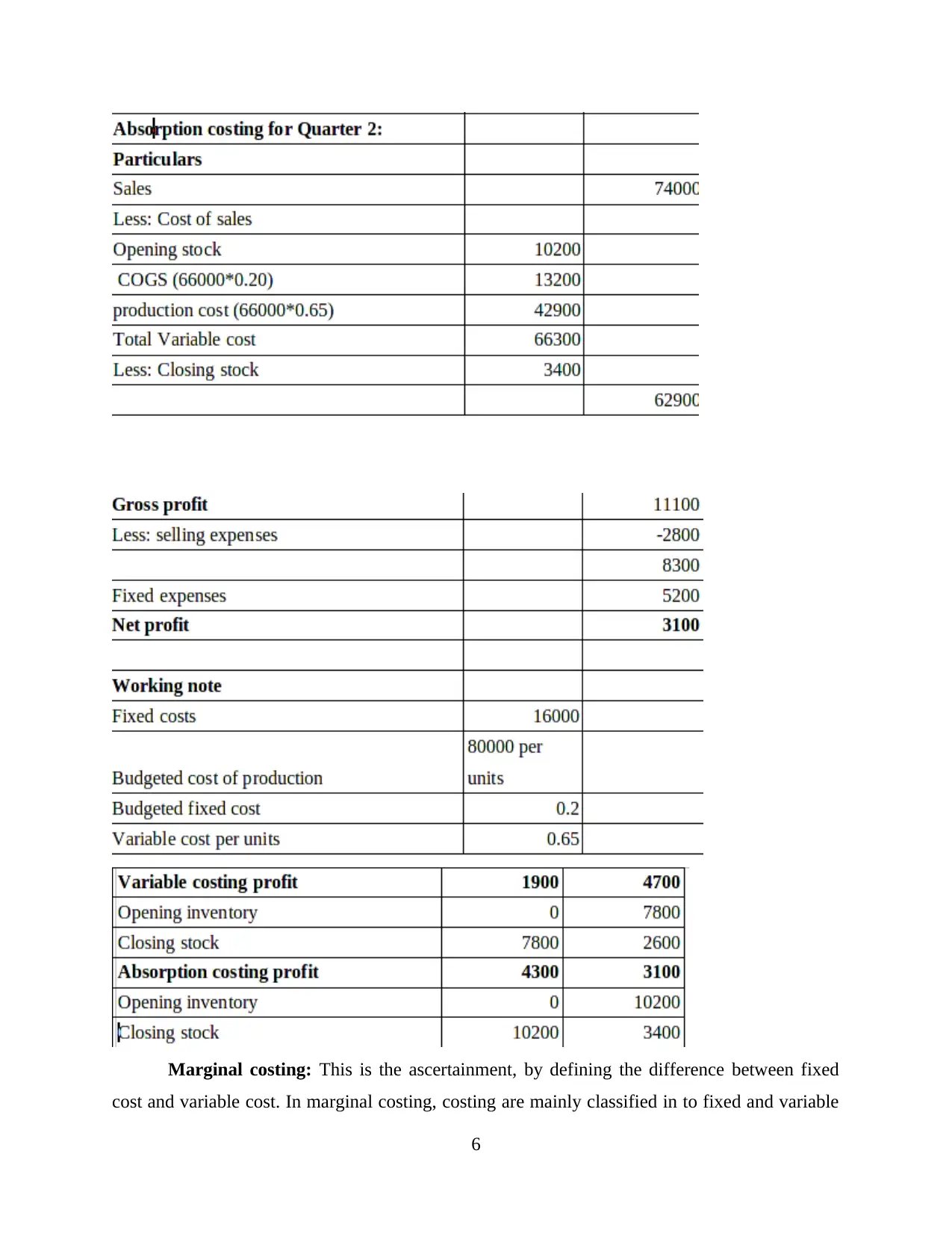

Marginal costing: This is the ascertainment, by defining the difference between fixed

cost and variable cost. In marginal costing, costing are mainly classified in to fixed and variable

6

cost and variable cost. In marginal costing, costing are mainly classified in to fixed and variable

6

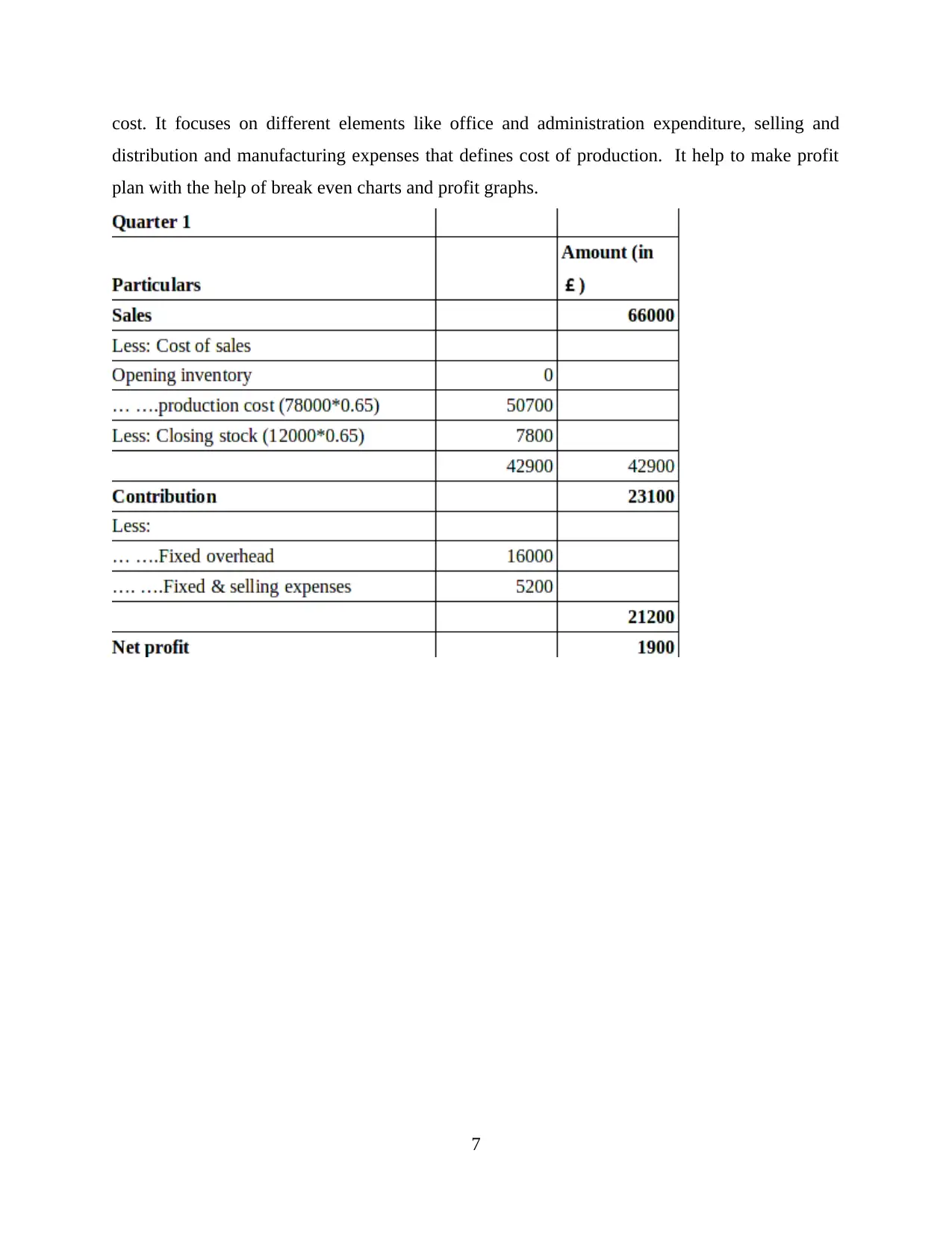

cost. It focuses on different elements like office and administration expenditure, selling and

distribution and manufacturing expenses that defines cost of production. It help to make profit

plan with the help of break even charts and profit graphs.

7

distribution and manufacturing expenses that defines cost of production. It help to make profit

plan with the help of break even charts and profit graphs.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

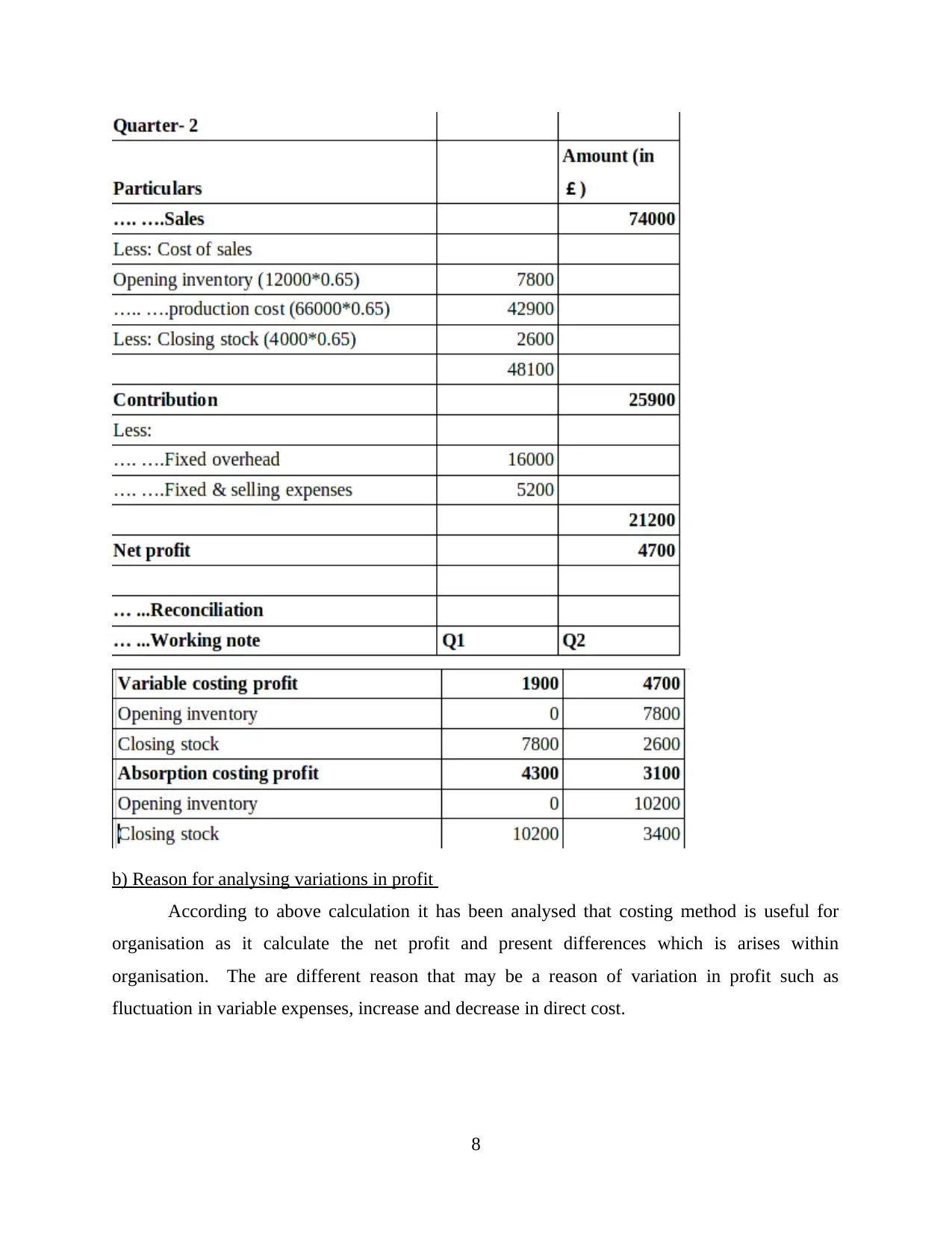

b) Reason for analysing variations in profit

According to above calculation it has been analysed that costing method is useful for

organisation as it calculate the net profit and present differences which is arises within

organisation. The are different reason that may be a reason of variation in profit such as

fluctuation in variable expenses, increase and decrease in direct cost.

8

According to above calculation it has been analysed that costing method is useful for

organisation as it calculate the net profit and present differences which is arises within

organisation. The are different reason that may be a reason of variation in profit such as

fluctuation in variable expenses, increase and decrease in direct cost.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 3

P4 Planning tools and its merits and demerits

Preparing a budget: Budget is the estimation of income and expenses which is arises

within organisation due to running a business activities. Every organisation should prepares these

budget that help to get information about income and expenses. This is the predetermination

which starts before beginning a project. Such as the manager of Nero Ltd prepares a budget by

recording the transaction such as sale , purchase and availability of resources. This budget help

to give idea about future uncertainties and can be improve if is needed (Kaplan and Atkinson,

2015).

Planning tools are the techniques which is used by managers to control over budget and

use it properly. It also help to increase the productivity and profitability in organisation. The

manager of Nero Ltd uses different types of planning tools or budgets in order to improve the

business performance. The different types of budget are defined as:

Operating budget: This is a financial plan which is designed to meet with organisation's

debt obligations and sustainable growth over time period. It help to operate business functions

effectively. It is important to manage current expenses or fixed expenses. In Nero Ltd manager

prepares operating budget for maintaining the operating activities within organisation. This type

of budget are prepares on the basis of quarterly, half yearly and annually.

Advantages: Operating budget helps to make plan for day to day operations of

business so not need to run in to financial ditch. It help Nero Ltd to tracking the

actual expenses, projecting future expenses and also help to build investment in

order to perform operating functions effectively. Moreover, it helps to manage the

current expenses and future expenses.

Disadvantages: It has drawback also such as it is time consuming process that

consume more time. It does not give correct results such as revenues and expenses

can be increases that affect operational activity (Nielsen, Mitchell and Nørrekli,

2015).

Master budget: This is the total of all small budgets which is prepares by managers

within organisation. It involves estimated financial statement, cash forecast, and financing plans.

It help to make budget with the support of all low budgets in order to increase the productivity

9

P4 Planning tools and its merits and demerits

Preparing a budget: Budget is the estimation of income and expenses which is arises

within organisation due to running a business activities. Every organisation should prepares these

budget that help to get information about income and expenses. This is the predetermination

which starts before beginning a project. Such as the manager of Nero Ltd prepares a budget by

recording the transaction such as sale , purchase and availability of resources. This budget help

to give idea about future uncertainties and can be improve if is needed (Kaplan and Atkinson,

2015).

Planning tools are the techniques which is used by managers to control over budget and

use it properly. It also help to increase the productivity and profitability in organisation. The

manager of Nero Ltd uses different types of planning tools or budgets in order to improve the

business performance. The different types of budget are defined as:

Operating budget: This is a financial plan which is designed to meet with organisation's

debt obligations and sustainable growth over time period. It help to operate business functions

effectively. It is important to manage current expenses or fixed expenses. In Nero Ltd manager

prepares operating budget for maintaining the operating activities within organisation. This type

of budget are prepares on the basis of quarterly, half yearly and annually.

Advantages: Operating budget helps to make plan for day to day operations of

business so not need to run in to financial ditch. It help Nero Ltd to tracking the

actual expenses, projecting future expenses and also help to build investment in

order to perform operating functions effectively. Moreover, it helps to manage the

current expenses and future expenses.

Disadvantages: It has drawback also such as it is time consuming process that

consume more time. It does not give correct results such as revenues and expenses

can be increases that affect operational activity (Nielsen, Mitchell and Nørrekli,

2015).

Master budget: This is the total of all small budgets which is prepares by managers

within organisation. It involves estimated financial statement, cash forecast, and financing plans.

It help to make budget with the support of all low budgets in order to increase the productivity

9

and profitability. In Nero Ltd, manager prepares master budget that help to make financial plan

for gaining profits.

Advantages: Master budget is the superior of all budget that includes all accounts

in order to make profits. It help Nero Ltd's managers to achieve goals and

objectives after making budgets. Moreover, it help to provide continuous

improvement in order to increase the production.

Disadvantages: It is rigid that is difficult to update within organisation. The

manager of Nero Ltd can face problem while preparing master budget as low

revenues and high expenses. Managers may not involve new opportunities for the

further growth of organisation.

Cash budget: This is the estimation of cash inflow and outflow of a business over a

certain period of time. This is used to assess the organisation have sufficient balance or not to

operate the business. It involves only cash transaction that should be in monetary terms. Such as

manager of Nero Ltd prepares cash budget by including cash income and expenses that help to

maintain profits.

Advantages: It help to avoid the debt that increase the productivity and

profitability. Is is beneficial to minimize the cost and maximize the profits by

using cash budget. In Nero Ltd, manager help to maintain the cash transaction

within organisation.

Disadvantages: It has drawback also such as it is difficult to analysis the

financial information through specific budget. It does not involve non cash items

that creates confusion. As result organisation can not get correct profits within

business entity.

Pricing strategies: This means policies, rules and regulation which is set by managers of

business organisation. Pricing strategy attracts the people in order to purchase the products and

services. Such as manager of Nero Ltd set the pricing policy of products and services in order to

influence the customers. Pricing strategy is used by responsible person who have knowledge

about setting the pricing policy by including all cost which is incurred by organisation. The

different types of pricing policy is defines as:

10

for gaining profits.

Advantages: Master budget is the superior of all budget that includes all accounts

in order to make profits. It help Nero Ltd's managers to achieve goals and

objectives after making budgets. Moreover, it help to provide continuous

improvement in order to increase the production.

Disadvantages: It is rigid that is difficult to update within organisation. The

manager of Nero Ltd can face problem while preparing master budget as low

revenues and high expenses. Managers may not involve new opportunities for the

further growth of organisation.

Cash budget: This is the estimation of cash inflow and outflow of a business over a

certain period of time. This is used to assess the organisation have sufficient balance or not to

operate the business. It involves only cash transaction that should be in monetary terms. Such as

manager of Nero Ltd prepares cash budget by including cash income and expenses that help to

maintain profits.

Advantages: It help to avoid the debt that increase the productivity and

profitability. Is is beneficial to minimize the cost and maximize the profits by

using cash budget. In Nero Ltd, manager help to maintain the cash transaction

within organisation.

Disadvantages: It has drawback also such as it is difficult to analysis the

financial information through specific budget. It does not involve non cash items

that creates confusion. As result organisation can not get correct profits within

business entity.

Pricing strategies: This means policies, rules and regulation which is set by managers of

business organisation. Pricing strategy attracts the people in order to purchase the products and

services. Such as manager of Nero Ltd set the pricing policy of products and services in order to

influence the customers. Pricing strategy is used by responsible person who have knowledge

about setting the pricing policy by including all cost which is incurred by organisation. The

different types of pricing policy is defines as:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.