Management Accounting Report: Exquisite Product Cost Analysis Report

VerifiedAdded on 2020/01/28

|19

|5677

|54

Report

AI Summary

This management accounting report analyzes the case of Jeffrey & Son's Ltd, a manufacturing firm producing the Exquisite product. It begins with an introduction to management accounting and its role in providing financial information for decision-making. Task 1 focuses on cost classification, job costing to calculate unit and total costs for a specific job, and absorption costing to determine the cost of the Exquisite product. It also analyzes the current allocation methods. Task 2 involves preparing and analyzing a cost report, commenting on variances, identifying areas for improvement using performance indicators, and exploring ways to reduce costs and enhance value. Task 3 delves into the budgeting process, including selecting appropriate budgeting methods and preparing different budget types, including a cash budget. Finally, Task 4 covers variance calculations, identifying causes, recommending corrective actions, preparing an operating statement, and reporting findings according to responsibility centers. The report concludes with a summary of findings and recommendations, supported by references.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Different types of cost classification......................................................................................3

1.2 Using job costing calculation of unit cost and total job cost for job 444...............................4

1.3 Calculating cost of Exquisite using absorption costing.........................................................5

1.4 Analyzing the cost of Exquisite focusing on technique used by Jeffrey & Son's Ltd...........7

TASK 2............................................................................................................................................7

2.1 Preparation and analysis of cost report and commenting on variance...................................7

2.2 Identification of areas of improvements using performance indicators.................................9

2.3 Ways to reduce costs, enhance value and quality................................................................10

TASK 3..........................................................................................................................................10

3.1 Purpose and nature of budgeting process.............................................................................10

3.2 Selection of appropriate budgeting methods for firm and its needs....................................10

3.3 Preparation of different types of budget..............................................................................10

3.4 Preparation of cash budget...................................................................................................11

TASK 4..........................................................................................................................................12

4.1 Calculation of variances, identification of causes and recommending corrective actions. .12

4.2 Preparation operating statement reconciling budgeted and actual results...........................13

4.3 Reporting findings to management according to responsibility centers identified..............13

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

2

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Different types of cost classification......................................................................................3

1.2 Using job costing calculation of unit cost and total job cost for job 444...............................4

1.3 Calculating cost of Exquisite using absorption costing.........................................................5

1.4 Analyzing the cost of Exquisite focusing on technique used by Jeffrey & Son's Ltd...........7

TASK 2............................................................................................................................................7

2.1 Preparation and analysis of cost report and commenting on variance...................................7

2.2 Identification of areas of improvements using performance indicators.................................9

2.3 Ways to reduce costs, enhance value and quality................................................................10

TASK 3..........................................................................................................................................10

3.1 Purpose and nature of budgeting process.............................................................................10

3.2 Selection of appropriate budgeting methods for firm and its needs....................................10

3.3 Preparation of different types of budget..............................................................................10

3.4 Preparation of cash budget...................................................................................................11

TASK 4..........................................................................................................................................12

4.1 Calculation of variances, identification of causes and recommending corrective actions. .12

4.2 Preparation operating statement reconciling budgeted and actual results...........................13

4.3 Reporting findings to management according to responsibility centers identified..............13

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

2

INTRODUCTION

Management accounting is regarded as an important business element that assists in

providing accounting information to the managers in the firm (Management accounting, 2014).

This is in order to offer them basis to develop informed business decision which would allow

them to be equipped in their management and keep a track on the functions (Burgstahler and

Eames, 2006). The reports relating with management accounting involve detailed accounts of the

company's available cash, generation of revenue and current organizations accounts payable and

receivables.

In the present report, management accounting has been discussed in context of case study

related with Jeffrey and Son's Ltd. The firm is manufacturing concern that produces popular and

brand product known as Exquisite. The present report entails to make analysis of cost

information in the firm. Further it involves methods to reduce costs and enhance value within

business. In addition to this it also includes preparation, forecasting and budgets for business. At

last it includes monitoring of performance against budget within firm.

TASK 1

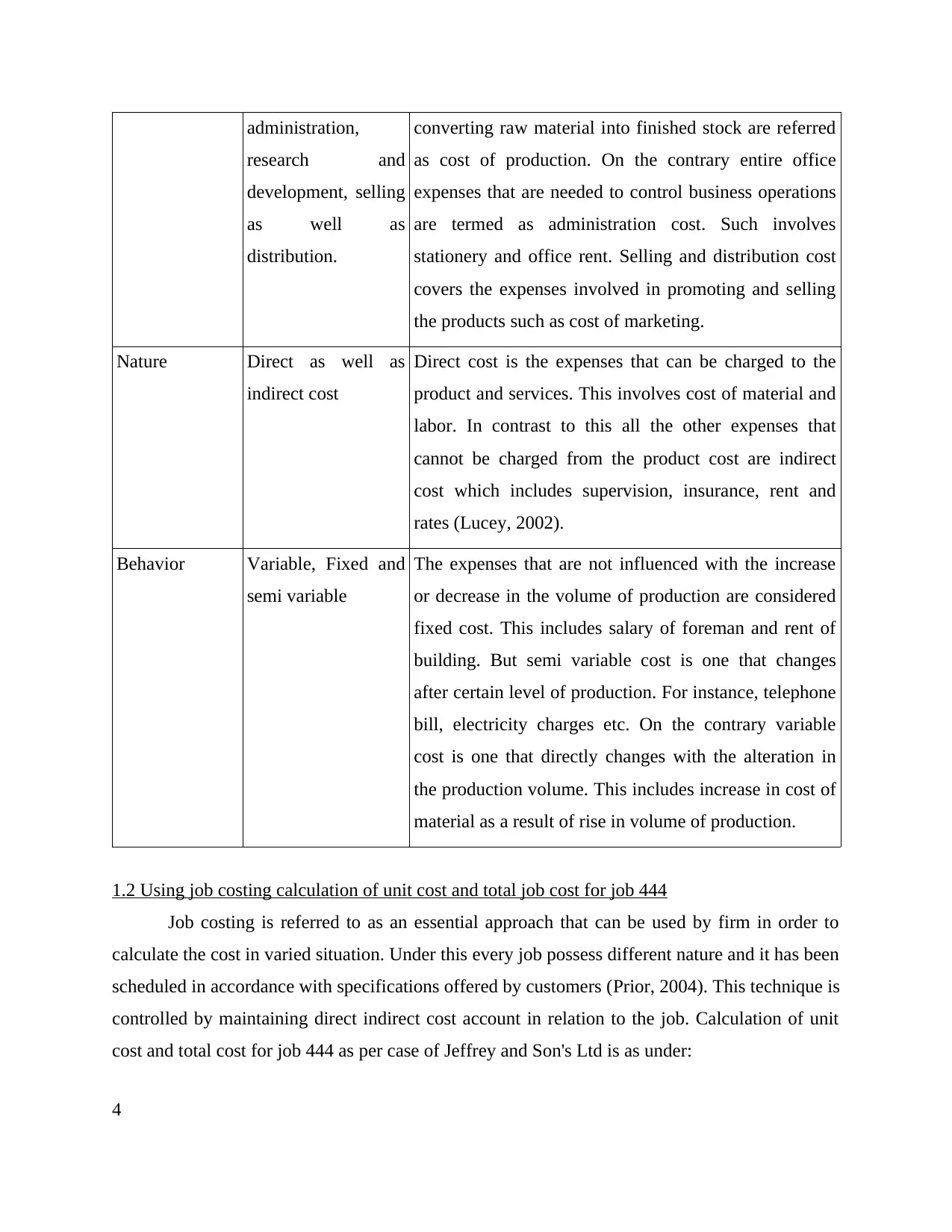

1.1 Different types of cost classification

Cost is referred to as expenditures incurred by the organization in accomplishment of its

activities. The cost of business is divided in the elements stated as under:

Basis of

classification

Type of cost Meaning

Elements Labor, Material and

overhead

Material is regarded as an essential element that

involves expenses to purchase raw material for

production of goods. In contrast to this labor are the one

who carries out production of goods (Exley and Smith,

2011). Further amount paid to them for their services is

referred as labor cost. Beside labor and material cost, all

the other expenses are considered as overhead. For

example, insurance, salary, factory rent etc.

Functions Production, The expenses related with production which assists in

3

Management accounting is regarded as an important business element that assists in

providing accounting information to the managers in the firm (Management accounting, 2014).

This is in order to offer them basis to develop informed business decision which would allow

them to be equipped in their management and keep a track on the functions (Burgstahler and

Eames, 2006). The reports relating with management accounting involve detailed accounts of the

company's available cash, generation of revenue and current organizations accounts payable and

receivables.

In the present report, management accounting has been discussed in context of case study

related with Jeffrey and Son's Ltd. The firm is manufacturing concern that produces popular and

brand product known as Exquisite. The present report entails to make analysis of cost

information in the firm. Further it involves methods to reduce costs and enhance value within

business. In addition to this it also includes preparation, forecasting and budgets for business. At

last it includes monitoring of performance against budget within firm.

TASK 1

1.1 Different types of cost classification

Cost is referred to as expenditures incurred by the organization in accomplishment of its

activities. The cost of business is divided in the elements stated as under:

Basis of

classification

Type of cost Meaning

Elements Labor, Material and

overhead

Material is regarded as an essential element that

involves expenses to purchase raw material for

production of goods. In contrast to this labor are the one

who carries out production of goods (Exley and Smith,

2011). Further amount paid to them for their services is

referred as labor cost. Beside labor and material cost, all

the other expenses are considered as overhead. For

example, insurance, salary, factory rent etc.

Functions Production, The expenses related with production which assists in

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

administration,

research and

development, selling

as well as

distribution.

converting raw material into finished stock are referred

as cost of production. On the contrary entire office

expenses that are needed to control business operations

are termed as administration cost. Such involves

stationery and office rent. Selling and distribution cost

covers the expenses involved in promoting and selling

the products such as cost of marketing.

Nature Direct as well as

indirect cost

Direct cost is the expenses that can be charged to the

product and services. This involves cost of material and

labor. In contrast to this all the other expenses that

cannot be charged from the product cost are indirect

cost which includes supervision, insurance, rent and

rates (Lucey, 2002).

Behavior Variable, Fixed and

semi variable

The expenses that are not influenced with the increase

or decrease in the volume of production are considered

fixed cost. This includes salary of foreman and rent of

building. But semi variable cost is one that changes

after certain level of production. For instance, telephone

bill, electricity charges etc. On the contrary variable

cost is one that directly changes with the alteration in

the production volume. This includes increase in cost of

material as a result of rise in volume of production.

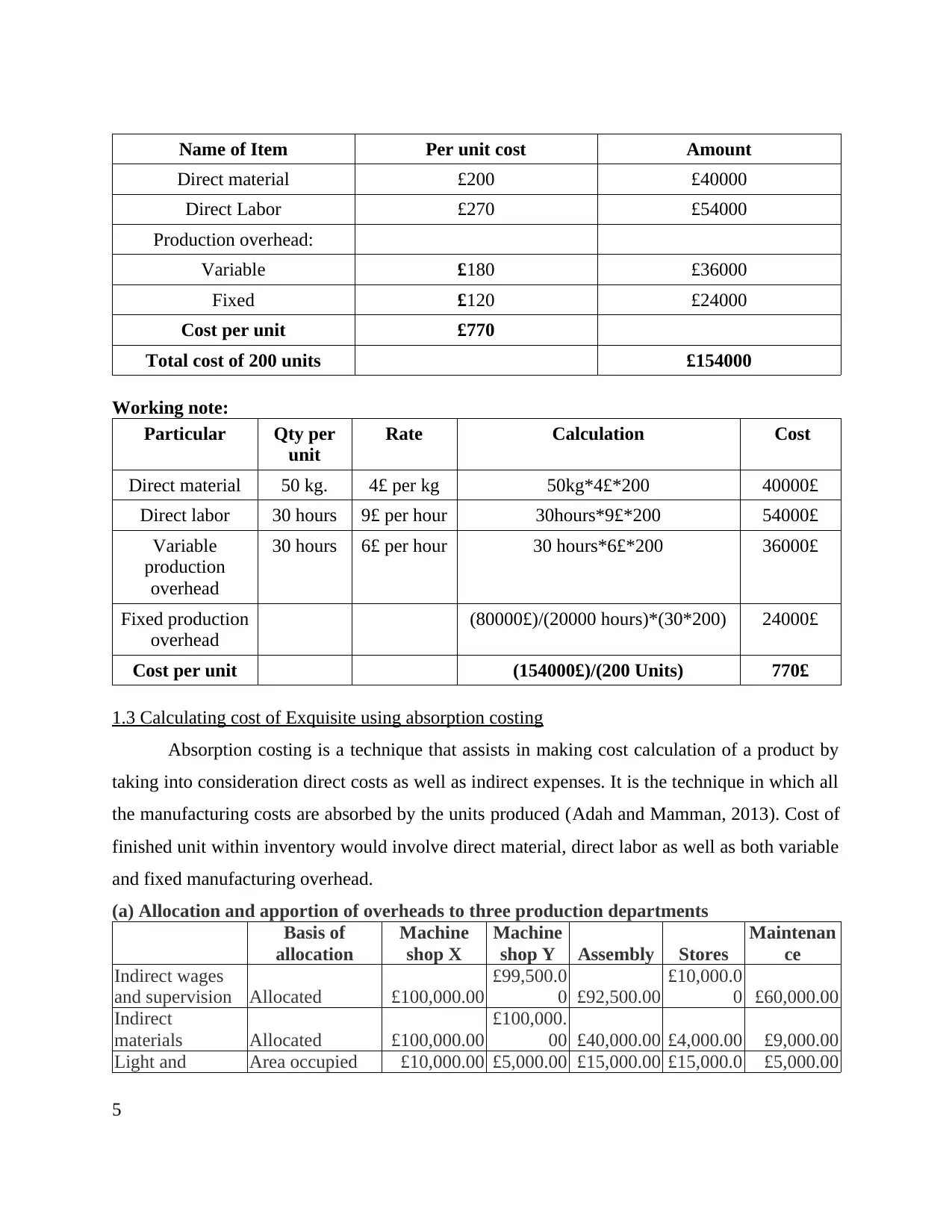

1.2 Using job costing calculation of unit cost and total job cost for job 444

Job costing is referred to as an essential approach that can be used by firm in order to

calculate the cost in varied situation. Under this every job possess different nature and it has been

scheduled in accordance with specifications offered by customers (Prior, 2004). This technique is

controlled by maintaining direct indirect cost account in relation to the job. Calculation of unit

cost and total cost for job 444 as per case of Jeffrey and Son's Ltd is as under:

4

research and

development, selling

as well as

distribution.

converting raw material into finished stock are referred

as cost of production. On the contrary entire office

expenses that are needed to control business operations

are termed as administration cost. Such involves

stationery and office rent. Selling and distribution cost

covers the expenses involved in promoting and selling

the products such as cost of marketing.

Nature Direct as well as

indirect cost

Direct cost is the expenses that can be charged to the

product and services. This involves cost of material and

labor. In contrast to this all the other expenses that

cannot be charged from the product cost are indirect

cost which includes supervision, insurance, rent and

rates (Lucey, 2002).

Behavior Variable, Fixed and

semi variable

The expenses that are not influenced with the increase

or decrease in the volume of production are considered

fixed cost. This includes salary of foreman and rent of

building. But semi variable cost is one that changes

after certain level of production. For instance, telephone

bill, electricity charges etc. On the contrary variable

cost is one that directly changes with the alteration in

the production volume. This includes increase in cost of

material as a result of rise in volume of production.

1.2 Using job costing calculation of unit cost and total job cost for job 444

Job costing is referred to as an essential approach that can be used by firm in order to

calculate the cost in varied situation. Under this every job possess different nature and it has been

scheduled in accordance with specifications offered by customers (Prior, 2004). This technique is

controlled by maintaining direct indirect cost account in relation to the job. Calculation of unit

cost and total cost for job 444 as per case of Jeffrey and Son's Ltd is as under:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Name of Item Per unit cost Amount

Direct material £200 £40000

Direct Labor £270 £54000

Production overhead:

Variable £180 £36000

Fixed £120 £24000

Cost per unit £770

Total cost of 200 units £154000

Working note:

Particular Qty per

unit

Rate Calculation Cost

Direct material 50 kg. 4£ per kg 50kg*4£*200 40000£

Direct labor 30 hours 9£ per hour 30hours*9£*200 54000£

Variable

production

overhead

30 hours 6£ per hour 30 hours*6£*200 36000£

Fixed production

overhead

(80000£)/(20000 hours)*(30*200) 24000£

Cost per unit (154000£)/(200 Units) 770£

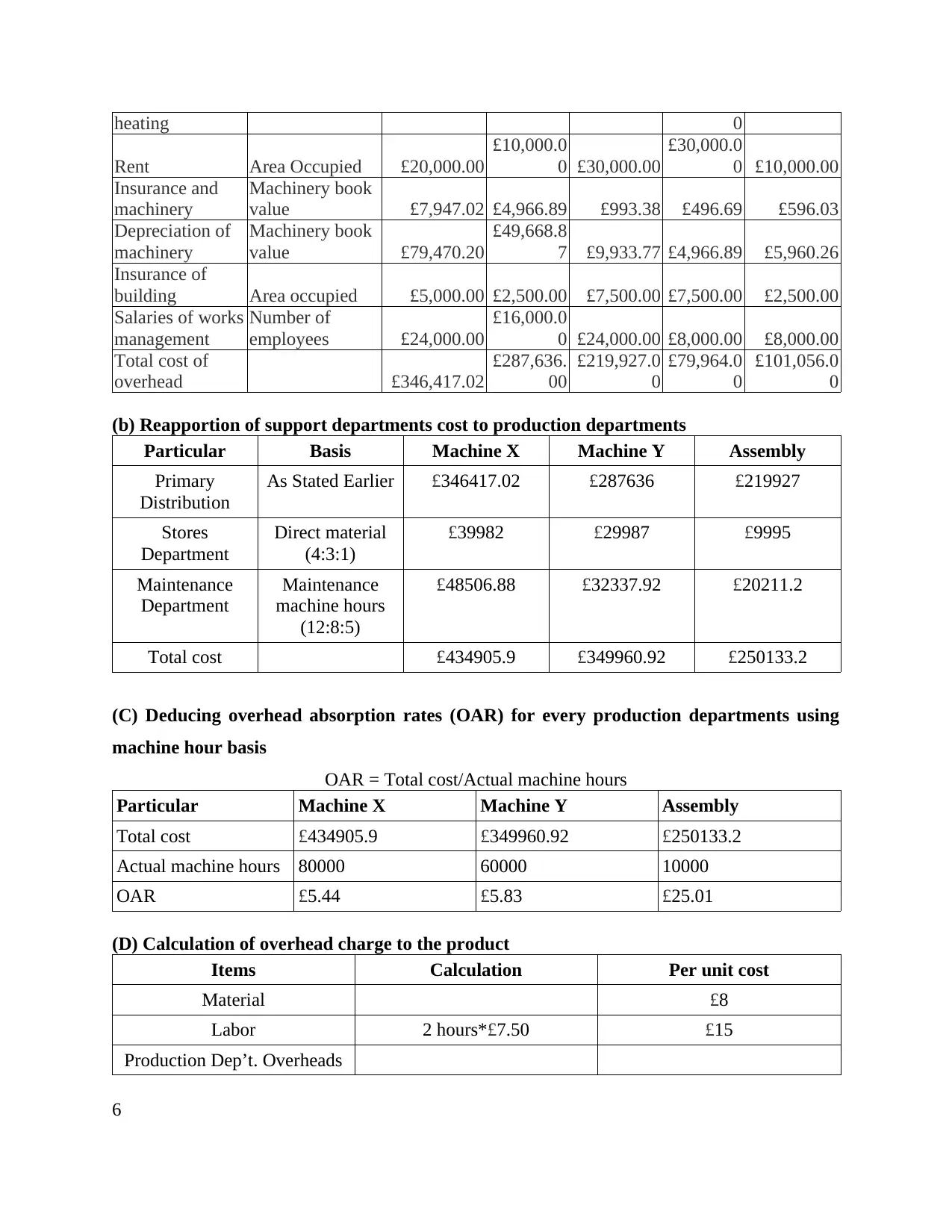

1.3 Calculating cost of Exquisite using absorption costing

Absorption costing is a technique that assists in making cost calculation of a product by

taking into consideration direct costs as well as indirect expenses. It is the technique in which all

the manufacturing costs are absorbed by the units produced (Adah and Mamman, 2013). Cost of

finished unit within inventory would involve direct material, direct labor as well as both variable

and fixed manufacturing overhead.

(a) Allocation and apportion of overheads to three production departments

Basis of

allocation

Machine

shop X

Machine

shop Y Assembly Stores

Maintenan

ce

Indirect wages

and supervision Allocated £100,000.00

£99,500.0

0 £92,500.00

£10,000.0

0 £60,000.00

Indirect

materials Allocated £100,000.00

£100,000.

00 £40,000.00 £4,000.00 £9,000.00

Light and Area occupied £10,000.00 £5,000.00 £15,000.00 £15,000.0 £5,000.00

5

Direct material £200 £40000

Direct Labor £270 £54000

Production overhead:

Variable £180 £36000

Fixed £120 £24000

Cost per unit £770

Total cost of 200 units £154000

Working note:

Particular Qty per

unit

Rate Calculation Cost

Direct material 50 kg. 4£ per kg 50kg*4£*200 40000£

Direct labor 30 hours 9£ per hour 30hours*9£*200 54000£

Variable

production

overhead

30 hours 6£ per hour 30 hours*6£*200 36000£

Fixed production

overhead

(80000£)/(20000 hours)*(30*200) 24000£

Cost per unit (154000£)/(200 Units) 770£

1.3 Calculating cost of Exquisite using absorption costing

Absorption costing is a technique that assists in making cost calculation of a product by

taking into consideration direct costs as well as indirect expenses. It is the technique in which all

the manufacturing costs are absorbed by the units produced (Adah and Mamman, 2013). Cost of

finished unit within inventory would involve direct material, direct labor as well as both variable

and fixed manufacturing overhead.

(a) Allocation and apportion of overheads to three production departments

Basis of

allocation

Machine

shop X

Machine

shop Y Assembly Stores

Maintenan

ce

Indirect wages

and supervision Allocated £100,000.00

£99,500.0

0 £92,500.00

£10,000.0

0 £60,000.00

Indirect

materials Allocated £100,000.00

£100,000.

00 £40,000.00 £4,000.00 £9,000.00

Light and Area occupied £10,000.00 £5,000.00 £15,000.00 £15,000.0 £5,000.00

5

heating 0

Rent Area Occupied £20,000.00

£10,000.0

0 £30,000.00

£30,000.0

0 £10,000.00

Insurance and

machinery

Machinery book

value £7,947.02 £4,966.89 £993.38 £496.69 £596.03

Depreciation of

machinery

Machinery book

value £79,470.20

£49,668.8

7 £9,933.77 £4,966.89 £5,960.26

Insurance of

building Area occupied £5,000.00 £2,500.00 £7,500.00 £7,500.00 £2,500.00

Salaries of works

management

Number of

employees £24,000.00

£16,000.0

0 £24,000.00 £8,000.00 £8,000.00

Total cost of

overhead £346,417.02

£287,636.

00

£219,927.0

0

£79,964.0

0

£101,056.0

0

(b) Reapportion of support departments cost to production departments

Particular Basis Machine X Machine Y Assembly

Primary

Distribution

As Stated Earlier £346417.02 £287636 £219927

Stores

Department

Direct material

(4:3:1)

£39982 £29987 £9995

Maintenance

Department

Maintenance

machine hours

(12:8:5)

£48506.88 £32337.92 £20211.2

Total cost £434905.9 £349960.92 £250133.2

(C) Deducing overhead absorption rates (OAR) for every production departments using

machine hour basis

OAR = Total cost/Actual machine hours

Particular Machine X Machine Y Assembly

Total cost £434905.9 £349960.92 £250133.2

Actual machine hours 80000 60000 10000

OAR £5.44 £5.83 £25.01

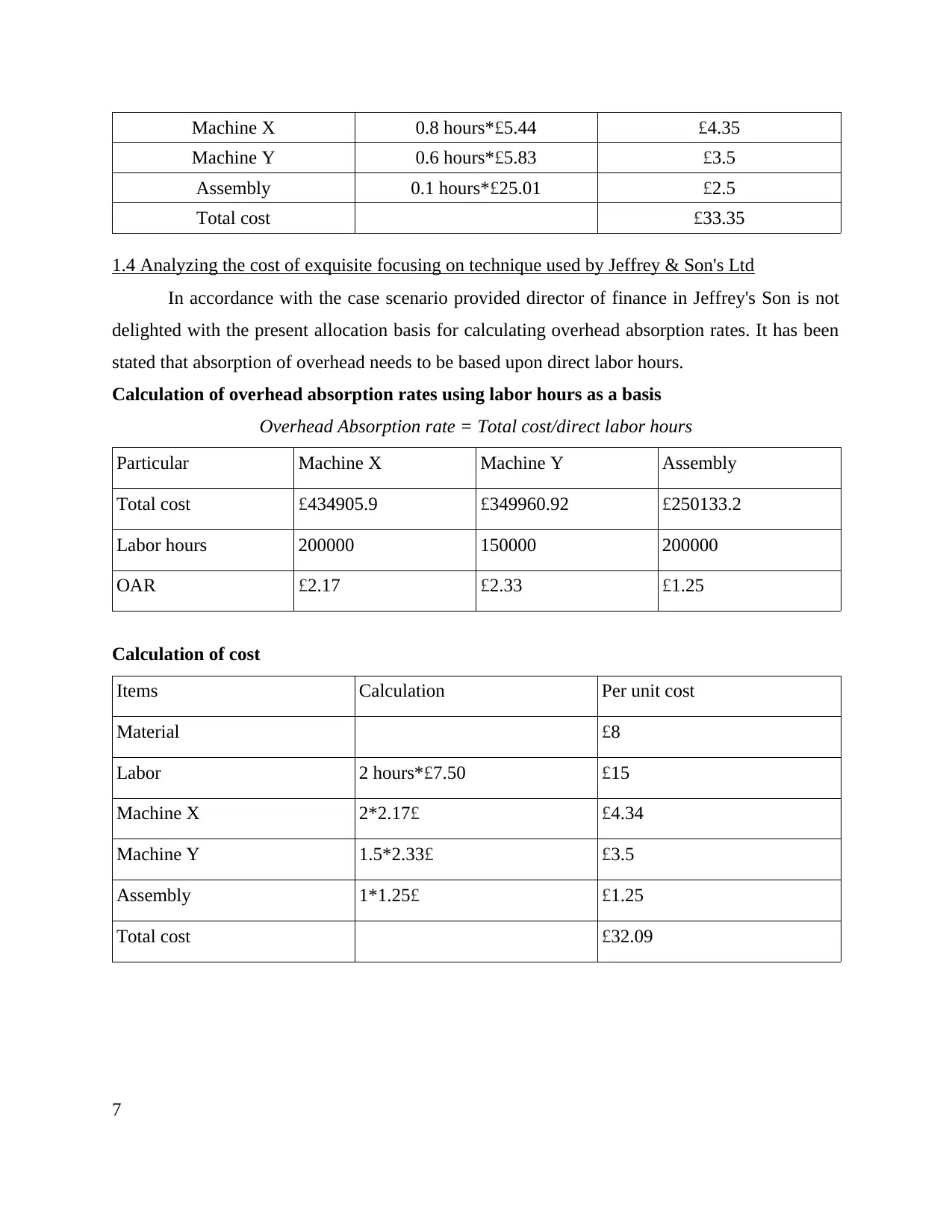

(D) Calculation of overhead charge to the product

Items Calculation Per unit cost

Material £8

Labor 2 hours*£7.50 £15

Production Dep’t. Overheads

6

Rent Area Occupied £20,000.00

£10,000.0

0 £30,000.00

£30,000.0

0 £10,000.00

Insurance and

machinery

Machinery book

value £7,947.02 £4,966.89 £993.38 £496.69 £596.03

Depreciation of

machinery

Machinery book

value £79,470.20

£49,668.8

7 £9,933.77 £4,966.89 £5,960.26

Insurance of

building Area occupied £5,000.00 £2,500.00 £7,500.00 £7,500.00 £2,500.00

Salaries of works

management

Number of

employees £24,000.00

£16,000.0

0 £24,000.00 £8,000.00 £8,000.00

Total cost of

overhead £346,417.02

£287,636.

00

£219,927.0

0

£79,964.0

0

£101,056.0

0

(b) Reapportion of support departments cost to production departments

Particular Basis Machine X Machine Y Assembly

Primary

Distribution

As Stated Earlier £346417.02 £287636 £219927

Stores

Department

Direct material

(4:3:1)

£39982 £29987 £9995

Maintenance

Department

Maintenance

machine hours

(12:8:5)

£48506.88 £32337.92 £20211.2

Total cost £434905.9 £349960.92 £250133.2

(C) Deducing overhead absorption rates (OAR) for every production departments using

machine hour basis

OAR = Total cost/Actual machine hours

Particular Machine X Machine Y Assembly

Total cost £434905.9 £349960.92 £250133.2

Actual machine hours 80000 60000 10000

OAR £5.44 £5.83 £25.01

(D) Calculation of overhead charge to the product

Items Calculation Per unit cost

Material £8

Labor 2 hours*£7.50 £15

Production Dep’t. Overheads

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Machine X 0.8 hours*£5.44 £4.35

Machine Y 0.6 hours*£5.83 £3.5

Assembly 0.1 hours*£25.01 £2.5

Total cost £33.35

1.4 Analyzing the cost of exquisite focusing on technique used by Jeffrey & Son's Ltd

In accordance with the case scenario provided director of finance in Jeffrey's Son is not

delighted with the present allocation basis for calculating overhead absorption rates. It has been

stated that absorption of overhead needs to be based upon direct labor hours.

Calculation of overhead absorption rates using labor hours as a basis

Overhead Absorption rate = Total cost/direct labor hours

Particular Machine X Machine Y Assembly

Total cost £434905.9 £349960.92 £250133.2

Labor hours 200000 150000 200000

OAR £2.17 £2.33 £1.25

Calculation of cost

Items Calculation Per unit cost

Material £8

Labor 2 hours*£7.50 £15

Machine X 2*2.17£ £4.34

Machine Y 1.5*2.33£ £3.5

Assembly 1*1.25£ £1.25

Total cost £32.09

7

Machine Y 0.6 hours*£5.83 £3.5

Assembly 0.1 hours*£25.01 £2.5

Total cost £33.35

1.4 Analyzing the cost of exquisite focusing on technique used by Jeffrey & Son's Ltd

In accordance with the case scenario provided director of finance in Jeffrey's Son is not

delighted with the present allocation basis for calculating overhead absorption rates. It has been

stated that absorption of overhead needs to be based upon direct labor hours.

Calculation of overhead absorption rates using labor hours as a basis

Overhead Absorption rate = Total cost/direct labor hours

Particular Machine X Machine Y Assembly

Total cost £434905.9 £349960.92 £250133.2

Labor hours 200000 150000 200000

OAR £2.17 £2.33 £1.25

Calculation of cost

Items Calculation Per unit cost

Material £8

Labor 2 hours*£7.50 £15

Machine X 2*2.17£ £4.34

Machine Y 1.5*2.33£ £3.5

Assembly 1*1.25£ £1.25

Total cost £32.09

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Therefore it can be determined that labor hour basis is quite good allocation basis. This is

due to reason that under this basis, there is decrease in cost per unit to £32.09. With this firm can

reduce the cost of product.

TASK 2

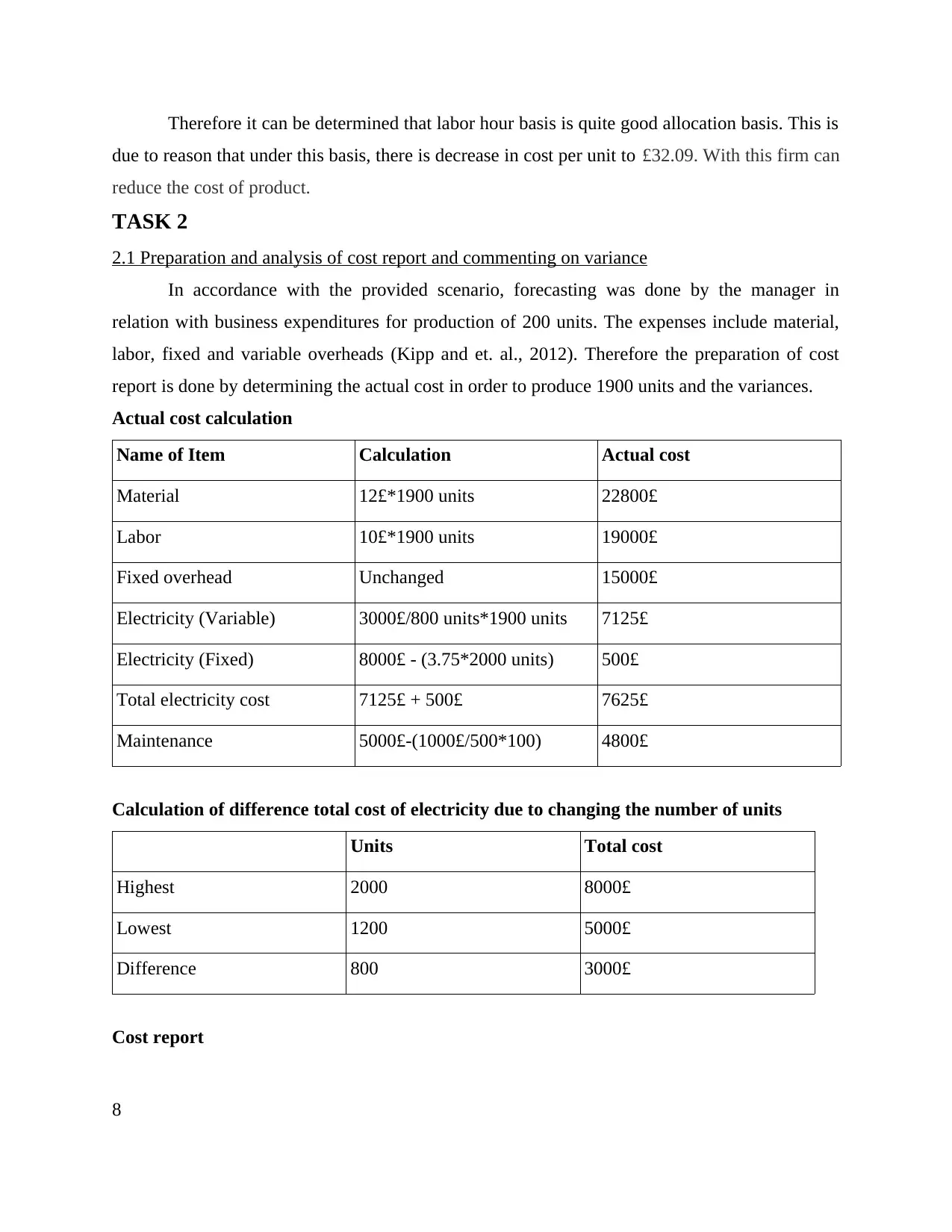

2.1 Preparation and analysis of cost report and commenting on variance

In accordance with the provided scenario, forecasting was done by the manager in

relation with business expenditures for production of 200 units. The expenses include material,

labor, fixed and variable overheads (Kipp and et. al., 2012). Therefore the preparation of cost

report is done by determining the actual cost in order to produce 1900 units and the variances.

Actual cost calculation

Name of Item Calculation Actual cost

Material 12£*1900 units 22800£

Labor 10£*1900 units 19000£

Fixed overhead Unchanged 15000£

Electricity (Variable) 3000£/800 units*1900 units 7125£

Electricity (Fixed) 8000£ - (3.75*2000 units) 500£

Total electricity cost 7125£ + 500£ 7625£

Maintenance 5000£-(1000£/500*100) 4800£

Calculation of difference total cost of electricity due to changing the number of units

Units Total cost

Highest 2000 8000£

Lowest 1200 5000£

Difference 800 3000£

Cost report

8

due to reason that under this basis, there is decrease in cost per unit to £32.09. With this firm can

reduce the cost of product.

TASK 2

2.1 Preparation and analysis of cost report and commenting on variance

In accordance with the provided scenario, forecasting was done by the manager in

relation with business expenditures for production of 200 units. The expenses include material,

labor, fixed and variable overheads (Kipp and et. al., 2012). Therefore the preparation of cost

report is done by determining the actual cost in order to produce 1900 units and the variances.

Actual cost calculation

Name of Item Calculation Actual cost

Material 12£*1900 units 22800£

Labor 10£*1900 units 19000£

Fixed overhead Unchanged 15000£

Electricity (Variable) 3000£/800 units*1900 units 7125£

Electricity (Fixed) 8000£ - (3.75*2000 units) 500£

Total electricity cost 7125£ + 500£ 7625£

Maintenance 5000£-(1000£/500*100) 4800£

Calculation of difference total cost of electricity due to changing the number of units

Units Total cost

Highest 2000 8000£

Lowest 1200 5000£

Difference 800 3000£

Cost report

8

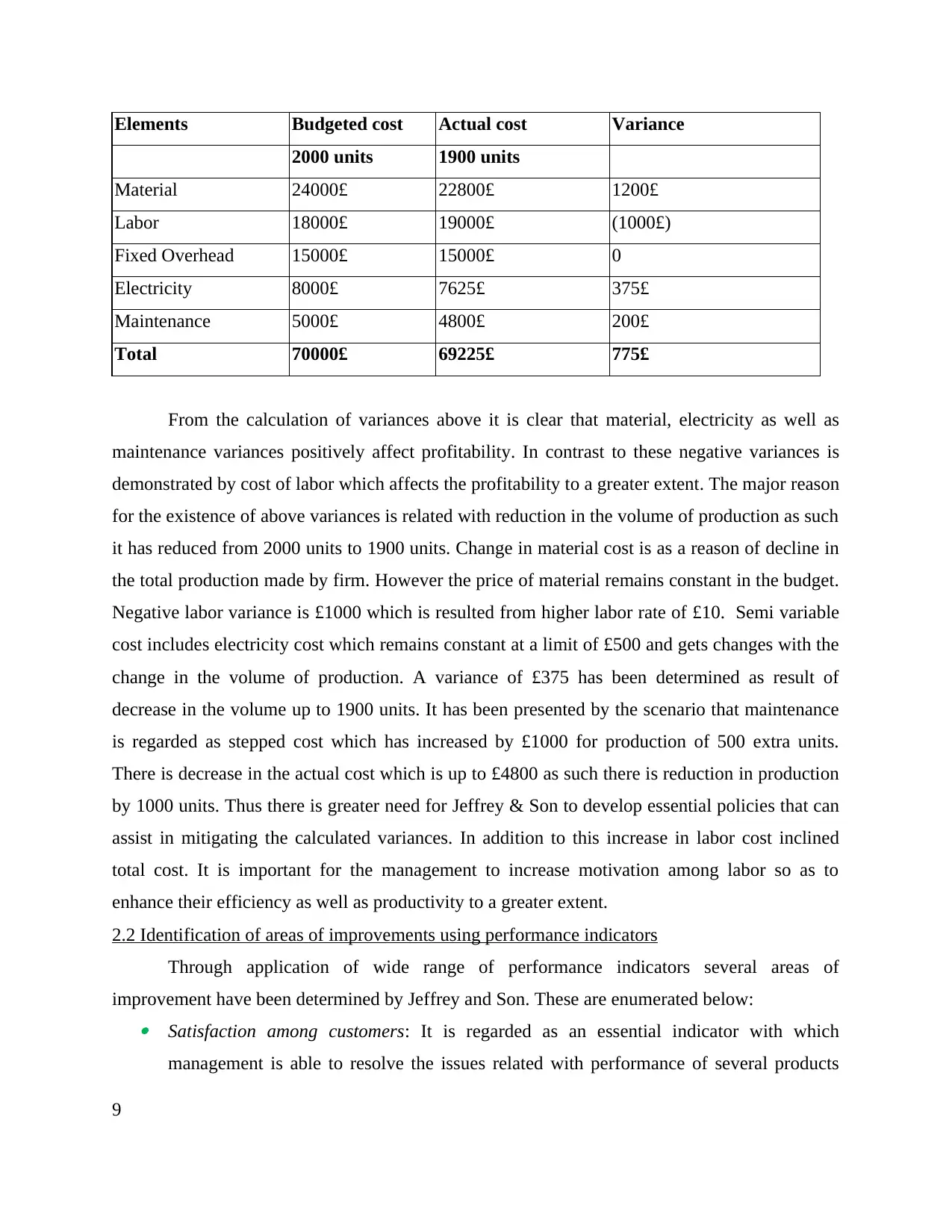

Elements Budgeted cost Actual cost Variance

2000 units 1900 units

Material 24000£ 22800£ 1200£

Labor 18000£ 19000£ (1000£)

Fixed Overhead 15000£ 15000£ 0

Electricity 8000£ 7625£ 375£

Maintenance 5000£ 4800£ 200£

Total 70000£ 69225£ 775£

From the calculation of variances above it is clear that material, electricity as well as

maintenance variances positively affect profitability. In contrast to these negative variances is

demonstrated by cost of labor which affects the profitability to a greater extent. The major reason

for the existence of above variances is related with reduction in the volume of production as such

it has reduced from 2000 units to 1900 units. Change in material cost is as a reason of decline in

the total production made by firm. However the price of material remains constant in the budget.

Negative labor variance is £1000 which is resulted from higher labor rate of £10. Semi variable

cost includes electricity cost which remains constant at a limit of £500 and gets changes with the

change in the volume of production. A variance of £375 has been determined as result of

decrease in the volume up to 1900 units. It has been presented by the scenario that maintenance

is regarded as stepped cost which has increased by £1000 for production of 500 extra units.

There is decrease in the actual cost which is up to £4800 as such there is reduction in production

by 1000 units. Thus there is greater need for Jeffrey & Son to develop essential policies that can

assist in mitigating the calculated variances. In addition to this increase in labor cost inclined

total cost. It is important for the management to increase motivation among labor so as to

enhance their efficiency as well as productivity to a greater extent.

2.2 Identification of areas of improvements using performance indicators

Through application of wide range of performance indicators several areas of

improvement have been determined by Jeffrey and Son. These are enumerated below: Satisfaction among customers: It is regarded as an essential indicator with which

management is able to resolve the issues related with performance of several products

9

2000 units 1900 units

Material 24000£ 22800£ 1200£

Labor 18000£ 19000£ (1000£)

Fixed Overhead 15000£ 15000£ 0

Electricity 8000£ 7625£ 375£

Maintenance 5000£ 4800£ 200£

Total 70000£ 69225£ 775£

From the calculation of variances above it is clear that material, electricity as well as

maintenance variances positively affect profitability. In contrast to these negative variances is

demonstrated by cost of labor which affects the profitability to a greater extent. The major reason

for the existence of above variances is related with reduction in the volume of production as such

it has reduced from 2000 units to 1900 units. Change in material cost is as a reason of decline in

the total production made by firm. However the price of material remains constant in the budget.

Negative labor variance is £1000 which is resulted from higher labor rate of £10. Semi variable

cost includes electricity cost which remains constant at a limit of £500 and gets changes with the

change in the volume of production. A variance of £375 has been determined as result of

decrease in the volume up to 1900 units. It has been presented by the scenario that maintenance

is regarded as stepped cost which has increased by £1000 for production of 500 extra units.

There is decrease in the actual cost which is up to £4800 as such there is reduction in production

by 1000 units. Thus there is greater need for Jeffrey & Son to develop essential policies that can

assist in mitigating the calculated variances. In addition to this increase in labor cost inclined

total cost. It is important for the management to increase motivation among labor so as to

enhance their efficiency as well as productivity to a greater extent.

2.2 Identification of areas of improvements using performance indicators

Through application of wide range of performance indicators several areas of

improvement have been determined by Jeffrey and Son. These are enumerated below: Satisfaction among customers: It is regarded as an essential indicator with which

management is able to resolve the issues related with performance of several products

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and services. Under this procedure improvement can be made by management in the

quality of product with respect to customer reviews (Pilleboue and et. al., 2015). By

taking into account feedback and complaints Jeffrey & Son's management can develop

suitable strategies for the purpose of making advancement in the process of production

with which customer satisfaction can be improved.

Accounting statement: Through detail evaluation of several accounting statements like

income statements, balance sheet and cash flow etc. Jeffrey & Son's management can

make assessment of change in financial position. If firm determines reduction in sales

along with the profitability in the expenditure of business then it is important for

management to bring changes in the operational strategies so as to enhance performance

of the organization. Such statements present effectiveness in offering description

regarding the changes that has occurred in the financial values in a particular financial

year.

2.3 Ways to reduce costs, enhance value and quality

There is existence of different techniques that can assist Jeffrey & Son in accomplishing

its target with respect to reduction in cost, enhancement of value and quality. These are

enumerated below: Total quality management: It is an effective tool that assists in bringing qualitative

improvements in the various operational activities of firm. Thus total quality approach is

related with improvement in entire process of production through evaluation and

resolution of several variances in the process of manufacturing (Jorgensen, Patrick and

Soderstrom, 2012). With this Jeffrey & Son can bring improvement in its efficiency to a

greater extent.

Kaizen: Likewise, TQM approach, the technique of Kaizen pays huge attention towards

continuous betterment in the entire functioning of the organization. The tool has proved

to be beneficial in terms of motivating the personnel towards attainment of operational

activities in an effective way. It assists management in minimizing wastage of resources

by taking into account the factors such as high time of waiting, ineffective human

resource allocation and increment in faulty units of production. Further it also involves

10

quality of product with respect to customer reviews (Pilleboue and et. al., 2015). By

taking into account feedback and complaints Jeffrey & Son's management can develop

suitable strategies for the purpose of making advancement in the process of production

with which customer satisfaction can be improved.

Accounting statement: Through detail evaluation of several accounting statements like

income statements, balance sheet and cash flow etc. Jeffrey & Son's management can

make assessment of change in financial position. If firm determines reduction in sales

along with the profitability in the expenditure of business then it is important for

management to bring changes in the operational strategies so as to enhance performance

of the organization. Such statements present effectiveness in offering description

regarding the changes that has occurred in the financial values in a particular financial

year.

2.3 Ways to reduce costs, enhance value and quality

There is existence of different techniques that can assist Jeffrey & Son in accomplishing

its target with respect to reduction in cost, enhancement of value and quality. These are

enumerated below: Total quality management: It is an effective tool that assists in bringing qualitative

improvements in the various operational activities of firm. Thus total quality approach is

related with improvement in entire process of production through evaluation and

resolution of several variances in the process of manufacturing (Jorgensen, Patrick and

Soderstrom, 2012). With this Jeffrey & Son can bring improvement in its efficiency to a

greater extent.

Kaizen: Likewise, TQM approach, the technique of Kaizen pays huge attention towards

continuous betterment in the entire functioning of the organization. The tool has proved

to be beneficial in terms of motivating the personnel towards attainment of operational

activities in an effective way. It assists management in minimizing wastage of resources

by taking into account the factors such as high time of waiting, ineffective human

resource allocation and increment in faulty units of production. Further it also involves

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inappropriate management of inventory as well as inadequacy in the quantity of

production.

TASK 3

3.1 Purpose and nature of budgeting process

Budget is the monetary plan that is prepared by the company for each and every department,

organization and projects that estimate the presumptive income generate and expenses made by

the company during a specific time period. Here are some of the following purpose of preparing

the budgets by Jeffrey & Son’s management is as follows:-

1. Budgets are prepared by the company is order to estimate the future income, profitability

and expenditure that can be incurred by the company after the completion of the specific

time period.

2. These are also prepared by the managers in order to compare the actual output with that

of budgeted output.

3. Another purpose of preparing this budget is to create a framework for the managers in

order to prepare various strategies (Kaplan and Atkinson, 2015). Strategies are prepared

by the organization in order to achieve the desired target and to beat its competitors.

Nature of budgeting process that is adopted by the Jeffrey & Son's management in order to

prepare various types of budgets is as follows:-

1. Company should use the last budget prepared by them in order to estimate the upcoming

financial environment.

2. After that company should determine the estimated amount of fund that can be rendered

by them from the sales of the product or other activities.

3. After that company should specify the approx amount of expenditure that can be faced by

them in terms of raw material, advertisements, production overheads and labour (Parker

and Kyj, 2006).

4. Then after that Jeffrey & Son's management should subtract the estimated income from

that of estimated expenses in order to analyse the budget is showing the condition of

deficit or surplus (Mohapatra, 2015).

5. After considering and reviewing all the above steps the final budget is need to be

submitted (Budgeting and budgetary control, 2016).

11

production.

TASK 3

3.1 Purpose and nature of budgeting process

Budget is the monetary plan that is prepared by the company for each and every department,

organization and projects that estimate the presumptive income generate and expenses made by

the company during a specific time period. Here are some of the following purpose of preparing

the budgets by Jeffrey & Son’s management is as follows:-

1. Budgets are prepared by the company is order to estimate the future income, profitability

and expenditure that can be incurred by the company after the completion of the specific

time period.

2. These are also prepared by the managers in order to compare the actual output with that

of budgeted output.

3. Another purpose of preparing this budget is to create a framework for the managers in

order to prepare various strategies (Kaplan and Atkinson, 2015). Strategies are prepared

by the organization in order to achieve the desired target and to beat its competitors.

Nature of budgeting process that is adopted by the Jeffrey & Son's management in order to

prepare various types of budgets is as follows:-

1. Company should use the last budget prepared by them in order to estimate the upcoming

financial environment.

2. After that company should determine the estimated amount of fund that can be rendered

by them from the sales of the product or other activities.

3. After that company should specify the approx amount of expenditure that can be faced by

them in terms of raw material, advertisements, production overheads and labour (Parker

and Kyj, 2006).

4. Then after that Jeffrey & Son's management should subtract the estimated income from

that of estimated expenses in order to analyse the budget is showing the condition of

deficit or surplus (Mohapatra, 2015).

5. After considering and reviewing all the above steps the final budget is need to be

submitted (Budgeting and budgetary control, 2016).

11

Therefore, at last when budgeting period is completed after the specific time period than in that

case actual budget need to be compared with the estimate budget in order to analyse the actual

result.

3.2 Selection of appropriate budgeting methods for firm and its needs

Incremental budgeting method is used by Jeffery & Son's in order to prepare various

budgets that prove beneficial for the organization. At the time of preparation of incremental

budget manger of Jeffery & Son's undertake the previous budgets made by them in order to

prepare the new budget for the upcoming time period. This budget prepared by the Jeffery &

Son's has very little importance in the ever-changing business environment. Therefore, in order

to set up more realistic budget Jeffery & Son's should move on towards the preparation of Zero

based budgeting. Zero based budgeting is the method of budgeting the all the expenses that

warrant for each new period of time. Zero based budgeting starts from a zero base. In other

words it could say that zero based budgeting is the method of budgeting, budget holder and

manager of an organization considering the zero as the base for the calculation of income and

expenditure.

This method is used by the manager to make all necessary attempts in order to identify

the various alternatives for the income and expenditure. In addition to this manager also make

real assessment of the income and expenditure which they can obtain over a specific period of

time. In order to form appropriate budget Zero based budgets undertake all the realistic aspects

and views (Fisher and Krumwiede, 2015). Therefore, at last it could be concluded that zero based

budget helps the Jeffery & Son' to achieve the various desired targets and results by reducing the

variance.

3.3 Preparation of different types of budget

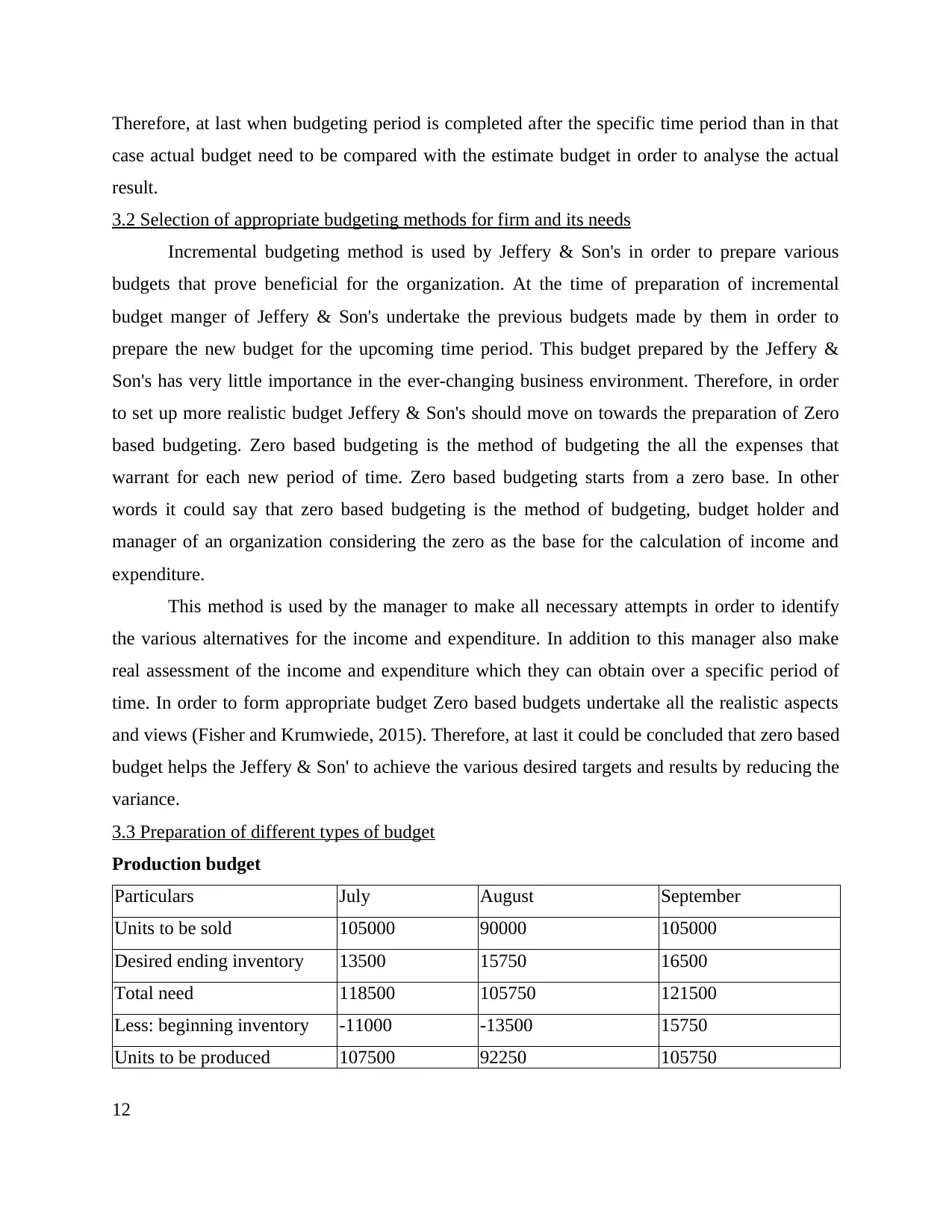

Production budget

Particulars July August September

Units to be sold 105000 90000 105000

Desired ending inventory 13500 15750 16500

Total need 118500 105750 121500

Less: beginning inventory -11000 -13500 15750

Units to be produced 107500 92250 105750

12

case actual budget need to be compared with the estimate budget in order to analyse the actual

result.

3.2 Selection of appropriate budgeting methods for firm and its needs

Incremental budgeting method is used by Jeffery & Son's in order to prepare various

budgets that prove beneficial for the organization. At the time of preparation of incremental

budget manger of Jeffery & Son's undertake the previous budgets made by them in order to

prepare the new budget for the upcoming time period. This budget prepared by the Jeffery &

Son's has very little importance in the ever-changing business environment. Therefore, in order

to set up more realistic budget Jeffery & Son's should move on towards the preparation of Zero

based budgeting. Zero based budgeting is the method of budgeting the all the expenses that

warrant for each new period of time. Zero based budgeting starts from a zero base. In other

words it could say that zero based budgeting is the method of budgeting, budget holder and

manager of an organization considering the zero as the base for the calculation of income and

expenditure.

This method is used by the manager to make all necessary attempts in order to identify

the various alternatives for the income and expenditure. In addition to this manager also make

real assessment of the income and expenditure which they can obtain over a specific period of

time. In order to form appropriate budget Zero based budgets undertake all the realistic aspects

and views (Fisher and Krumwiede, 2015). Therefore, at last it could be concluded that zero based

budget helps the Jeffery & Son' to achieve the various desired targets and results by reducing the

variance.

3.3 Preparation of different types of budget

Production budget

Particulars July August September

Units to be sold 105000 90000 105000

Desired ending inventory 13500 15750 16500

Total need 118500 105750 121500

Less: beginning inventory -11000 -13500 15750

Units to be produced 107500 92250 105750

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.