ACC200 Management Accounting: Job Costing, Overheads, and ABC Analysis

VerifiedAdded on 2023/03/23

|13

|2694

|45

Report

AI Summary

This report provides a comprehensive analysis of job costing and activity-based costing (ABC) within the context of management accounting. It evaluates the applicability of job costing in various business scenarios and calculates the work-in-progress inventory and finished goods inventory values. The report also addresses the treatment of over-applied and under-applied overheads, comparing two alternative accounting methods. Furthermore, it highlights the advantages of ABC over traditional costing methods, emphasizing its ability to improve the accuracy and relevance of expense allocation by dividing production processes into different activities and using cost drivers. The analysis includes practical calculations and theoretical evaluations, concluding with the benefits of implementing ABC to enhance pricing strategies.

Management Accounting Problem

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The main objective of this report is to understand the concept of job costing and activity-

based costing from theoretical as well as a practical aspect. In the given case study

management has provided with some important formation in relation to the production

process of the organization and this report has calculated the cost and quantity of finished

goods at the end of 31st December. This report has also evaluated different aspects of ABC

costing and job costing. Job costing cannot be used by any business organizations and the

specific scenario in which job costing Method can be helpful is evaluated in this report. In

addition to the advantages of ABC costing method over the traditional costing method are

also discussed.

2

The main objective of this report is to understand the concept of job costing and activity-

based costing from theoretical as well as a practical aspect. In the given case study

management has provided with some important formation in relation to the production

process of the organization and this report has calculated the cost and quantity of finished

goods at the end of 31st December. This report has also evaluated different aspects of ABC

costing and job costing. Job costing cannot be used by any business organizations and the

specific scenario in which job costing Method can be helpful is evaluated in this report. In

addition to the advantages of ABC costing method over the traditional costing method are

also discussed.

2

Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Use of job costing method..........................................................................................................5

Balance in work in progress inventory account on 31st December...........................................7

Cost of the chairs in finished goods inventory at 31st December..............................................7

Over-applied or under-applied overheads................................................................................11

Two alternative accounting treatments for over-applied and under-applied overheads..........11

How activity-based costing overcome the deficiencies of the existing costing system...........12

Conclusion................................................................................................................................13

References................................................................................................................................14

3

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Use of job costing method..........................................................................................................5

Balance in work in progress inventory account on 31st December...........................................7

Cost of the chairs in finished goods inventory at 31st December..............................................7

Over-applied or under-applied overheads................................................................................11

Two alternative accounting treatments for over-applied and under-applied overheads..........11

How activity-based costing overcome the deficiencies of the existing costing system...........12

Conclusion................................................................................................................................13

References................................................................................................................................14

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Role of Management Accounting has increased in business organizations over the period of

time special in business organizations that are manufacturing product and services. For such

organizations, it is very important to make sure that two pricing attached to a particular

product or service is accurate and relevant. Wrong pricing will definitely have a significant

negative impact on business organization. For example, if prices charged from the customer

is higher than customers will move to alternative products whereas if pricing charged from

the customer is low then it will result in loss of profit for the company. Therefore it is very

important that an effective and efficient method of allocating cost is used by the business

organization in order to price their product and services. One of the most effective methods of

assigning prices to product and services is the job costing method and it should be used only

in certain circumstances. For example, a business organization is operating on the basis of

separate jobs i.e. production is done on the basis of specifications provided by customers. In

this method, the job, the costing method will be very effective as the cost of production will

be in accordance with services demanded by the customer. The main objective of this report

is to evaluate different aspects of job costing method along with the use of job costing

method to calculate the overall cost of production and finished goods.

4

Role of Management Accounting has increased in business organizations over the period of

time special in business organizations that are manufacturing product and services. For such

organizations, it is very important to make sure that two pricing attached to a particular

product or service is accurate and relevant. Wrong pricing will definitely have a significant

negative impact on business organization. For example, if prices charged from the customer

is higher than customers will move to alternative products whereas if pricing charged from

the customer is low then it will result in loss of profit for the company. Therefore it is very

important that an effective and efficient method of allocating cost is used by the business

organization in order to price their product and services. One of the most effective methods of

assigning prices to product and services is the job costing method and it should be used only

in certain circumstances. For example, a business organization is operating on the basis of

separate jobs i.e. production is done on the basis of specifications provided by customers. In

this method, the job, the costing method will be very effective as the cost of production will

be in accordance with services demanded by the customer. The main objective of this report

is to evaluate different aspects of job costing method along with the use of job costing

method to calculate the overall cost of production and finished goods.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Use of job costing method

Job costing method helps in calculation of cost associated with material labour and indirect

expenses in a particular job executed by the organization. There is various type of business

organization that is providing goods and services to customers on the basis of their demand

from the organization (Fisher and Krumwiede, 2015). For example, customizable software

provided by an IT organization is based on the specific needs and requirements of the

company rather than providing similar services to each and every customer. In such a

scenario, the traditional costing method would not be very appropriate because in the

traditional method of all the costs are calculated together and distributed among products

manufactured by the organization equally. This type of Costing method would not be

appropriate in this scenario because product and services are customizable and customers are

taking different services from the organization (Mu, Jiang and Leng, 2017). There is a

probability that management of the company might to charge lower selling price as compared

to value from one customer and charge more from another customer due to the application of

the traditional method.

On the basis of this analysis, it can be said that job costing Method can be used in business

organizations that are dividing their production process on the basis of different jobs. This

will definitely help in increasing the accuracy of pricing strategies developed by the

company. In the given scenario, Connectta has divided its product and services into two

different jobs. For example management of the company has categorized its production

process into different jobs as the production of chair, computer caddy, desk, and printer stand

(Maskell, Baggaley and Grasso, 2016). Use of job costing method in this and I will be very

appropriate as the cost associated with each of the product mentioned above will be different

from each other.

The cost associated with the material, purchased parts and labour can be categorized easily on

the basis of material and Labour used for the production of a particular job. The main

difficulty in this scenario arises for the allocation of manufacturing overhead. Manufacturing

overhead is incurred by the organization on the production of all the product and services

manufactured by the organization rather than on specific product (Bull, 2014). Therefore it is

important that the appropriate method of allocation is used by management for allocation of

manufacturing overhead in order to make sure that pricing strategy is effective. Here

management can identify whether the production process is machine intensive or labour

5

Job costing method helps in calculation of cost associated with material labour and indirect

expenses in a particular job executed by the organization. There is various type of business

organization that is providing goods and services to customers on the basis of their demand

from the organization (Fisher and Krumwiede, 2015). For example, customizable software

provided by an IT organization is based on the specific needs and requirements of the

company rather than providing similar services to each and every customer. In such a

scenario, the traditional costing method would not be very appropriate because in the

traditional method of all the costs are calculated together and distributed among products

manufactured by the organization equally. This type of Costing method would not be

appropriate in this scenario because product and services are customizable and customers are

taking different services from the organization (Mu, Jiang and Leng, 2017). There is a

probability that management of the company might to charge lower selling price as compared

to value from one customer and charge more from another customer due to the application of

the traditional method.

On the basis of this analysis, it can be said that job costing Method can be used in business

organizations that are dividing their production process on the basis of different jobs. This

will definitely help in increasing the accuracy of pricing strategies developed by the

company. In the given scenario, Connectta has divided its product and services into two

different jobs. For example management of the company has categorized its production

process into different jobs as the production of chair, computer caddy, desk, and printer stand

(Maskell, Baggaley and Grasso, 2016). Use of job costing method in this and I will be very

appropriate as the cost associated with each of the product mentioned above will be different

from each other.

The cost associated with the material, purchased parts and labour can be categorized easily on

the basis of material and Labour used for the production of a particular job. The main

difficulty in this scenario arises for the allocation of manufacturing overhead. Manufacturing

overhead is incurred by the organization on the production of all the product and services

manufactured by the organization rather than on specific product (Bull, 2014). Therefore it is

important that the appropriate method of allocation is used by management for allocation of

manufacturing overhead in order to make sure that pricing strategy is effective. Here

management can identify whether the production process is machine intensive or labour

5

intensive. If the production process is machine intensive then the manufacturing overhead

should be divided on the basis of machine power used by each and every job. On the other

hand, if production processes labour intensive than labour hours used by every job should be

considered. In the given scenario machine hours are used for allocation of manufacturing

overhead (Oseifuah, 2014).

6

should be divided on the basis of machine power used by each and every job. On the other

hand, if production processes labour intensive than labour hours used by every job should be

considered. In the given scenario machine hours are used for allocation of manufacturing

overhead (Oseifuah, 2014).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

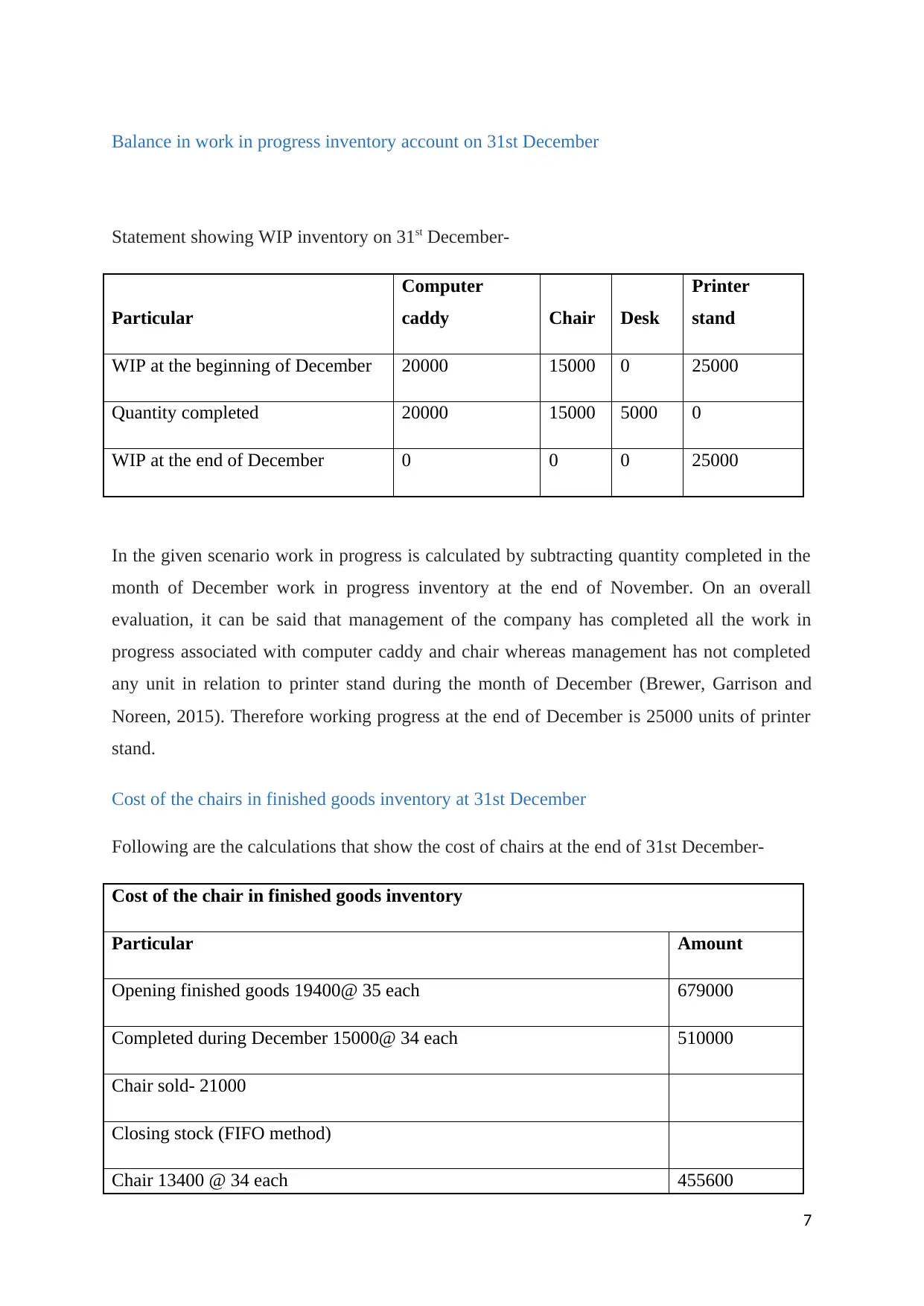

Balance in work in progress inventory account on 31st December

Statement showing WIP inventory on 31st December-

Particular

Computer

caddy Chair Desk

Printer

stand

WIP at the beginning of December 20000 15000 0 25000

Quantity completed 20000 15000 5000 0

WIP at the end of December 0 0 0 25000

In the given scenario work in progress is calculated by subtracting quantity completed in the

month of December work in progress inventory at the end of November. On an overall

evaluation, it can be said that management of the company has completed all the work in

progress associated with computer caddy and chair whereas management has not completed

any unit in relation to printer stand during the month of December (Brewer, Garrison and

Noreen, 2015). Therefore working progress at the end of December is 25000 units of printer

stand.

Cost of the chairs in finished goods inventory at 31st December

Following are the calculations that show the cost of chairs at the end of 31st December-

Cost of the chair in finished goods inventory

Particular Amount

Opening finished goods 19400@ 35 each 679000

Completed during December 15000@ 34 each 510000

Chair sold- 21000

Closing stock (FIFO method)

Chair 13400 @ 34 each 455600

7

Statement showing WIP inventory on 31st December-

Particular

Computer

caddy Chair Desk

Printer

stand

WIP at the beginning of December 20000 15000 0 25000

Quantity completed 20000 15000 5000 0

WIP at the end of December 0 0 0 25000

In the given scenario work in progress is calculated by subtracting quantity completed in the

month of December work in progress inventory at the end of November. On an overall

evaluation, it can be said that management of the company has completed all the work in

progress associated with computer caddy and chair whereas management has not completed

any unit in relation to printer stand during the month of December (Brewer, Garrison and

Noreen, 2015). Therefore working progress at the end of December is 25000 units of printer

stand.

Cost of the chairs in finished goods inventory at 31st December

Following are the calculations that show the cost of chairs at the end of 31st December-

Cost of the chair in finished goods inventory

Particular Amount

Opening finished goods 19400@ 35 each 679000

Completed during December 15000@ 34 each 510000

Chair sold- 21000

Closing stock (FIFO method)

Chair 13400 @ 34 each 455600

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

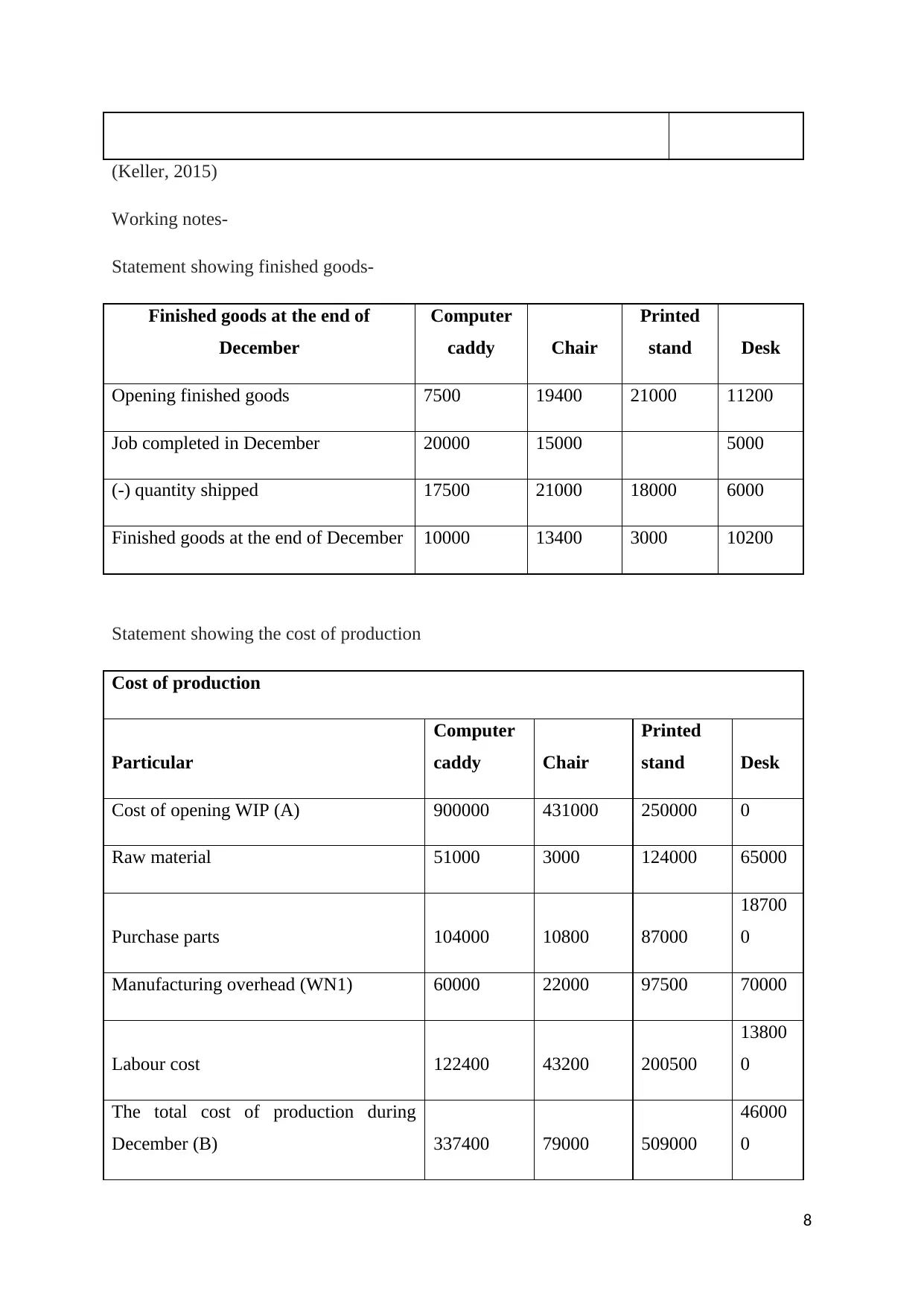

(Keller, 2015)

Working notes-

Statement showing finished goods-

Finished goods at the end of

December

Computer

caddy Chair

Printed

stand Desk

Opening finished goods 7500 19400 21000 11200

Job completed in December 20000 15000 5000

(-) quantity shipped 17500 21000 18000 6000

Finished goods at the end of December 10000 13400 3000 10200

Statement showing the cost of production

Cost of production

Particular

Computer

caddy Chair

Printed

stand Desk

Cost of opening WIP (A) 900000 431000 250000 0

Raw material 51000 3000 124000 65000

Purchase parts 104000 10800 87000

18700

0

Manufacturing overhead (WN1) 60000 22000 97500 70000

Labour cost 122400 43200 200500

13800

0

The total cost of production during

December (B) 337400 79000 509000

46000

0

8

Working notes-

Statement showing finished goods-

Finished goods at the end of

December

Computer

caddy Chair

Printed

stand Desk

Opening finished goods 7500 19400 21000 11200

Job completed in December 20000 15000 5000

(-) quantity shipped 17500 21000 18000 6000

Finished goods at the end of December 10000 13400 3000 10200

Statement showing the cost of production

Cost of production

Particular

Computer

caddy Chair

Printed

stand Desk

Cost of opening WIP (A) 900000 431000 250000 0

Raw material 51000 3000 124000 65000

Purchase parts 104000 10800 87000

18700

0

Manufacturing overhead (WN1) 60000 22000 97500 70000

Labour cost 122400 43200 200500

13800

0

The total cost of production during

December (B) 337400 79000 509000

46000

0

8

The total cost of goods completed in

December (B) 1237400 510000 759000

46000

0

Items completed during the year (Units) 20000 15000 5000 0

WIP at the end of December (Units) 0 0 0 5000

Cost of finished unit 61.87 34 151.8 0

Cost of WIP (Chair) 92

Calculation of manufacturing overhead

Particular Amount

Budgeted manufacturing overhead 4500000

Budgeted machine hours 900000

Overhear recovery rate 5

(Triyuwono, Chandra and Asri, 2018)

Allocated manufacturing overhead

Particular Computer caddy Chair Printed stand Desk

Machine hours used 12000 4400 19500 14000

Overhead recovery rate 5 5 5 5

Allocated overhead 60000 22000 97500 70000

9

December (B) 1237400 510000 759000

46000

0

Items completed during the year (Units) 20000 15000 5000 0

WIP at the end of December (Units) 0 0 0 5000

Cost of finished unit 61.87 34 151.8 0

Cost of WIP (Chair) 92

Calculation of manufacturing overhead

Particular Amount

Budgeted manufacturing overhead 4500000

Budgeted machine hours 900000

Overhear recovery rate 5

(Triyuwono, Chandra and Asri, 2018)

Allocated manufacturing overhead

Particular Computer caddy Chair Printed stand Desk

Machine hours used 12000 4400 19500 14000

Overhead recovery rate 5 5 5 5

Allocated overhead 60000 22000 97500 70000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Over-applied or under-applied overheads

As it is provided in the case scenario that actual overhead incurred by the organization during

the production process of December was $252000. On the other hand, the total budgeted

overhead allocated to all the products under consideration was $249500 during the month of

December. On the basis of this evaluation, it can be said that actual overheads are exceeding

by $2500 in the month of December which should be charge from profit and loss account in

the organization.

On the basis of this calculation, it can be said that management of the company has under

applied the overhead expenses by $2,500 in the month of December.

Two alternative accounting treatments for over-applied and under-applied overheads

Following are the two alternative accounting treatments for over-applied and under-applied

overheads-

Method 1- Allocating under-applied or over-applied overhead in work in progress, finished

goods and cost of goods sold. Under this method, the total cost associated with under-applied

or over-applied overhead is distributed among work in progress finished goods and cost of

goods sold. In this method, the ratio is calculated in which overhead is allocated to finished

goods cost of goods sold and work in progress and then over-applied and under-applied

overhead is distributed accordingly (Weygandt et.al, 2018).

Method 2- One of the other most common method charging the under-applied or over-applied

overhead in profit and loss account of the company. In this method under applied or over-

applied overhead is included in the cost of goods sold recorded by the organization in profit

and loss account. In the case of the under-applied overhead overall cost of goods sold is

increased whereas it is decreased in the case of over-applied overhead (Kaplan and Atkinson,

2015). This is one of the most commonly used two methods of recording over-applied and

under-applied overheads during any accounting period as it is very simple to calculate and it

is also not very complex.

10

As it is provided in the case scenario that actual overhead incurred by the organization during

the production process of December was $252000. On the other hand, the total budgeted

overhead allocated to all the products under consideration was $249500 during the month of

December. On the basis of this evaluation, it can be said that actual overheads are exceeding

by $2500 in the month of December which should be charge from profit and loss account in

the organization.

On the basis of this calculation, it can be said that management of the company has under

applied the overhead expenses by $2,500 in the month of December.

Two alternative accounting treatments for over-applied and under-applied overheads

Following are the two alternative accounting treatments for over-applied and under-applied

overheads-

Method 1- Allocating under-applied or over-applied overhead in work in progress, finished

goods and cost of goods sold. Under this method, the total cost associated with under-applied

or over-applied overhead is distributed among work in progress finished goods and cost of

goods sold. In this method, the ratio is calculated in which overhead is allocated to finished

goods cost of goods sold and work in progress and then over-applied and under-applied

overhead is distributed accordingly (Weygandt et.al, 2018).

Method 2- One of the other most common method charging the under-applied or over-applied

overhead in profit and loss account of the company. In this method under applied or over-

applied overhead is included in the cost of goods sold recorded by the organization in profit

and loss account. In the case of the under-applied overhead overall cost of goods sold is

increased whereas it is decreased in the case of over-applied overhead (Kaplan and Atkinson,

2015). This is one of the most commonly used two methods of recording over-applied and

under-applied overheads during any accounting period as it is very simple to calculate and it

is also not very complex.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

How activity-based costing overcome the deficiencies of the existing costing system

Activity-based costing can be very helpful in evaluating the actual cost of production in this

scenario. Following are some of the advantages of activity-based costing that will help in

improving the accuracy and relevancy of allocation of expense-

One of the primary advantages of using activity-based costing is that all the production

process are divided into different activities in this type of Costing. Allocation of expenses on

product and services manufactured by the organization are on the basis of the cost associated

with activities performed in the production of a particular product (Warren Jr, Moffitt and

Byrnes, 2015). This will definitely improve the accuracy level of allocating expense.

In the current method, management is using machinery for the allocation of overhead

expenses. This type of allocation can be inaccurate as the use of machines in the production

of one product can differ as compared to other product. This type of allocation does not

represent an accurate allocation of overhead expenses (Walther and Skousen, 2017).

Cost drivers are prepared by the organization for allocation of particular expenses into

different product and services which will definitely improve the accuracy of allocating cost.

In traditional costing method, the cost is distributed on the basis of a number of units

produced or on the basis of percentage of labour hour or machine hour used for the

production of a particular product. On the other hand, activity-based costing uses different

cost drivers for the allocation of expenses (Saguinsin, 2019). Therefore it can be said that a

more accurate method of allocation is used in the case of activity-based costing.

Total cost pools decided in case of traditional costing method is limited to one or two

whereas in case of activity-based costing cost pools are representative of different activities

undertaken by business organization for the production process (Pleis, 2016).

It is true that the complexity in the allocation of expenses through activity-based costing can

be very high but effective and efficient activity-based costing will definitely improve the

pricing strategies of the company.

11

Activity-based costing can be very helpful in evaluating the actual cost of production in this

scenario. Following are some of the advantages of activity-based costing that will help in

improving the accuracy and relevancy of allocation of expense-

One of the primary advantages of using activity-based costing is that all the production

process are divided into different activities in this type of Costing. Allocation of expenses on

product and services manufactured by the organization are on the basis of the cost associated

with activities performed in the production of a particular product (Warren Jr, Moffitt and

Byrnes, 2015). This will definitely improve the accuracy level of allocating expense.

In the current method, management is using machinery for the allocation of overhead

expenses. This type of allocation can be inaccurate as the use of machines in the production

of one product can differ as compared to other product. This type of allocation does not

represent an accurate allocation of overhead expenses (Walther and Skousen, 2017).

Cost drivers are prepared by the organization for allocation of particular expenses into

different product and services which will definitely improve the accuracy of allocating cost.

In traditional costing method, the cost is distributed on the basis of a number of units

produced or on the basis of percentage of labour hour or machine hour used for the

production of a particular product. On the other hand, activity-based costing uses different

cost drivers for the allocation of expenses (Saguinsin, 2019). Therefore it can be said that a

more accurate method of allocation is used in the case of activity-based costing.

Total cost pools decided in case of traditional costing method is limited to one or two

whereas in case of activity-based costing cost pools are representative of different activities

undertaken by business organization for the production process (Pleis, 2016).

It is true that the complexity in the allocation of expenses through activity-based costing can

be very high but effective and efficient activity-based costing will definitely improve the

pricing strategies of the company.

11

Conclusion

An overall conclusion it can be said that the importance of selecting an appropriate method

for costing purpose is very important for any business organization. An effective and efficient

method of allocating expenses will help the business organization to maintain accuracy and

pricing strategy which is important to sustain in the market. On the basis of this report, it can

be said that effective methodology has been used for the purpose of allocation by the

company. There is a requirement of improving the level of accuracy in estimating budgeted

overhead expenses as total budgeted overhead expenses for lower as compared to actual

expenses. This report has also evaluated that management of the organization should allocate

under-applied overhead expenses to work in progress, cost of goods sold and finished

inventory. Another option available with the organization is to charge the under-applied

overhead expenses to cost of goods sold.

12

An overall conclusion it can be said that the importance of selecting an appropriate method

for costing purpose is very important for any business organization. An effective and efficient

method of allocating expenses will help the business organization to maintain accuracy and

pricing strategy which is important to sustain in the market. On the basis of this report, it can

be said that effective methodology has been used for the purpose of allocation by the

company. There is a requirement of improving the level of accuracy in estimating budgeted

overhead expenses as total budgeted overhead expenses for lower as compared to actual

expenses. This report has also evaluated that management of the organization should allocate

under-applied overhead expenses to work in progress, cost of goods sold and finished

inventory. Another option available with the organization is to charge the under-applied

overhead expenses to cost of goods sold.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.