Management Accounting Report: Techniques, Benefits, and Planning Tools

VerifiedAdded on 2020/11/23

|17

|4294

|153

Report

AI Summary

This report on management accounting provides a comprehensive overview of the subject, covering key concepts, techniques, and their application within an organizational context. It begins with a definition of management accounting, its various types, and reporting methods, emphasizing its role in managerial decision-making, performance measurement, and financial planning. The report then delves into specific techniques such as marginal and absorption costing, illustrating their application through calculations and interpretations. It further explores budgetary control, examining the advantages and disadvantages of different planning tools like zero-based, top-down, and activity-based budgeting. The report concludes by discussing the adoption of management accounting systems to address financial problems and promote organizational growth, highlighting the integration of management accounting reports and systems within Jupiter Plc to achieve its objectives and gain competitive advantages. The report includes financial statements, cost analysis, and planning tools, providing a detailed understanding of how management accounting contributes to effective business operations and sustainable success.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Meaning of management accounting and different types of management accounting systems. 1

different methods of management accounting reporting........................................................3

Benefits of management accounting system with organisational context..............................4

Integration of management accounting system and management accounting report in

organisational process............................................................................................................5

TASK 2............................................................................................................................................6

a.) marginal costing................................................................................................................6

b.) absorption costing.............................................................................................................6

TASK 3............................................................................................................................................9

Advantages and disadvantage of different types of planning tools used in budgetary control9

Use of different planning tools for preparing budget ..........................................................10

TASK 4..........................................................................................................................................11

Adoption of management account systems to responds to financial problems of the

organisation..........................................................................................................................11

Factors which leads to develop organisational growth by use of management accounting 12

Response of planning tool for solving financial problems in achieving sustainable success13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Meaning of management accounting and different types of management accounting systems. 1

different methods of management accounting reporting........................................................3

Benefits of management accounting system with organisational context..............................4

Integration of management accounting system and management accounting report in

organisational process............................................................................................................5

TASK 2............................................................................................................................................6

a.) marginal costing................................................................................................................6

b.) absorption costing.............................................................................................................6

TASK 3............................................................................................................................................9

Advantages and disadvantage of different types of planning tools used in budgetary control9

Use of different planning tools for preparing budget ..........................................................10

TASK 4..........................................................................................................................................11

Adoption of management account systems to responds to financial problems of the

organisation..........................................................................................................................11

Factors which leads to develop organisational growth by use of management accounting 12

Response of planning tool for solving financial problems in achieving sustainable success13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is the term which is used in decision making to managers with

the provision of financial and non-financial accounting. This present report will cover definition

of management accounting with its essentials requirements, its different methods and its benefits.

Further, in this report calculations is to be provided of management accounting techniques.

Different types of planning tools in budgetary controls and also for preparing forecasting budgets

explanations are to be provided in this report. Further, in this report adoption of management

accounting to solve financial problems is to be discussed.

TASK 1

Meaning of management accounting and different types of management accounting systems

Management accounting is the process of recording accounting information which is used

by managers before they take any decision for organisation operations. Management accounting

used to measure performance and functions of day to day activities of business organisation

(Woodruff, 2018). Therefore, it helps management to perform activities like planning,

organising, staffing, directing and controlling.

`different types of management accounting systems

To measure financial information and regular activities of the company, management accounting

is created. Different types are as follows-

scope

To measure typical financial data of the organisation management accounting used in all the

departments of the organisation. Departments may be finance, IT, marketing, human resources,

operations and also sales.

Product costing

Management accounting also used to identify actual costs, profits and also cash flow of goods

and services of the organisation. Main motive to create management accounting is for product

costing. For allocating overhead expenses to drive true cost of products this accounting is

developed by managers.

Cost analysis

1

Management accounting is the term which is used in decision making to managers with

the provision of financial and non-financial accounting. This present report will cover definition

of management accounting with its essentials requirements, its different methods and its benefits.

Further, in this report calculations is to be provided of management accounting techniques.

Different types of planning tools in budgetary controls and also for preparing forecasting budgets

explanations are to be provided in this report. Further, in this report adoption of management

accounting to solve financial problems is to be discussed.

TASK 1

Meaning of management accounting and different types of management accounting systems

Management accounting is the process of recording accounting information which is used

by managers before they take any decision for organisation operations. Management accounting

used to measure performance and functions of day to day activities of business organisation

(Woodruff, 2018). Therefore, it helps management to perform activities like planning,

organising, staffing, directing and controlling.

`different types of management accounting systems

To measure financial information and regular activities of the company, management accounting

is created. Different types are as follows-

scope

To measure typical financial data of the organisation management accounting used in all the

departments of the organisation. Departments may be finance, IT, marketing, human resources,

operations and also sales.

Product costing

Management accounting also used to identify actual costs, profits and also cash flow of goods

and services of the organisation. Main motive to create management accounting is for product

costing. For allocating overhead expenses to drive true cost of products this accounting is

developed by managers.

Cost analysis

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To identify actual cost from results of the operations, executives use this performance report

(Nishimura, 2018). This is also known as variance analysis accounting which used to measure

non-performing areas of the organisation.

Constraints analysis

Another importance for developing management accounting is to analyse workflow of the

production process and sales process of the organisation. Therefore, to prevent obstacles or

constraints this management accounting is prepared.

Trend analysis and forecasting

Management accounting is created by organisation to overlook the future of the organisation. For

forecasting future managers will use trend lines in their accounting process which includes

budgets, administrative expenses etc.

different methods of management accounting reporting

2

(Nishimura, 2018). This is also known as variance analysis accounting which used to measure

non-performing areas of the organisation.

Constraints analysis

Another importance for developing management accounting is to analyse workflow of the

production process and sales process of the organisation. Therefore, to prevent obstacles or

constraints this management accounting is prepared.

Trend analysis and forecasting

Management accounting is created by organisation to overlook the future of the organisation. For

forecasting future managers will use trend lines in their accounting process which includes

budgets, administrative expenses etc.

different methods of management accounting reporting

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

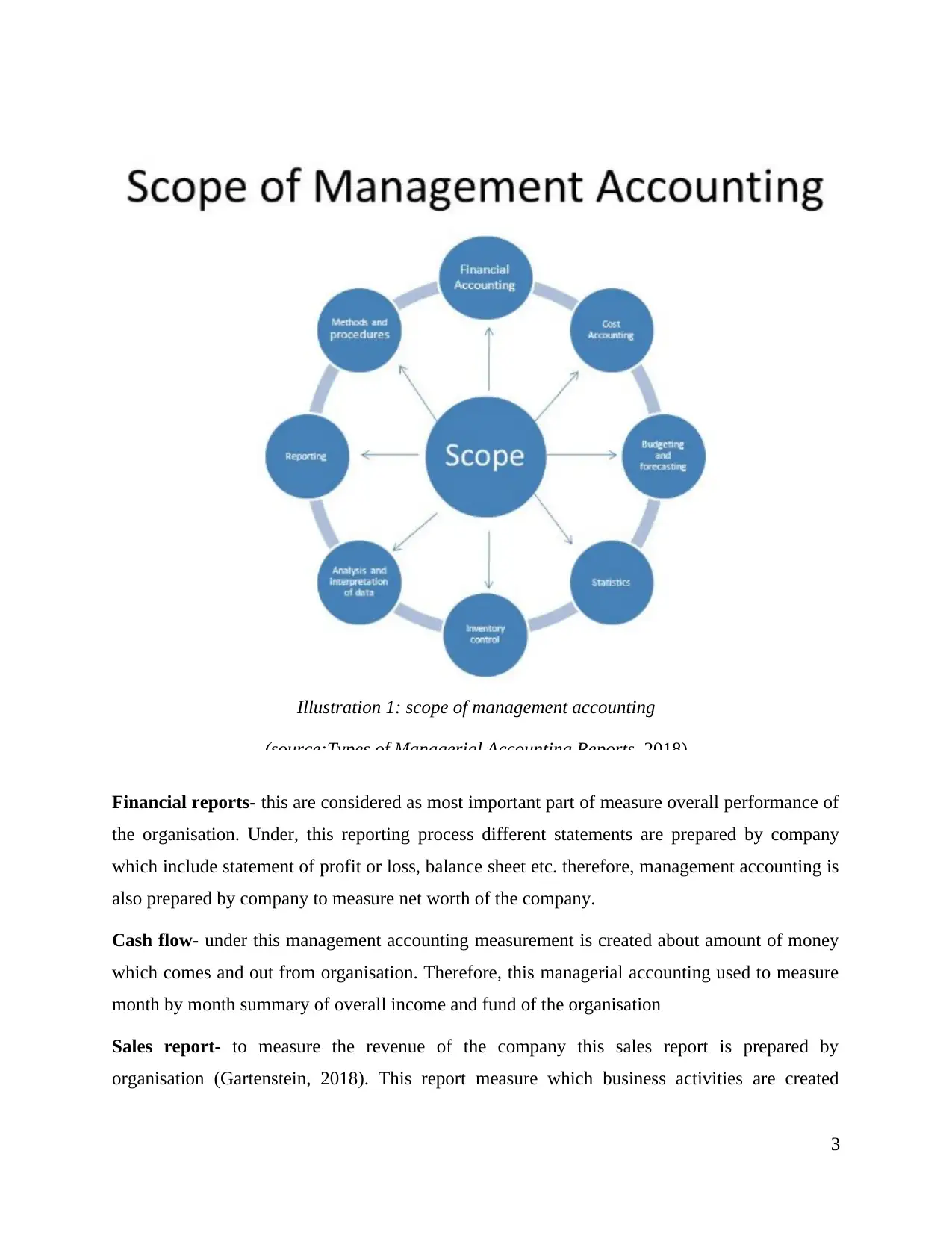

Financial reports- this are considered as most important part of measure overall performance of

the organisation. Under, this reporting process different statements are prepared by company

which include statement of profit or loss, balance sheet etc. therefore, management accounting is

also prepared by company to measure net worth of the company.

Cash flow- under this management accounting measurement is created about amount of money

which comes and out from organisation. Therefore, this managerial accounting used to measure

month by month summary of overall income and fund of the organisation

Sales report- to measure the revenue of the company this sales report is prepared by

organisation (Gartenstein, 2018). This report measure which business activities are created

3

Illustration 1: scope of management accounting

(source:Types of Managerial Accounting Reports, 2018)

the organisation. Under, this reporting process different statements are prepared by company

which include statement of profit or loss, balance sheet etc. therefore, management accounting is

also prepared by company to measure net worth of the company.

Cash flow- under this management accounting measurement is created about amount of money

which comes and out from organisation. Therefore, this managerial accounting used to measure

month by month summary of overall income and fund of the organisation

Sales report- to measure the revenue of the company this sales report is prepared by

organisation (Gartenstein, 2018). This report measure which business activities are created

3

Illustration 1: scope of management accounting

(source:Types of Managerial Accounting Reports, 2018)

higher earning in organisation. Basis of this report is to generate activities which are performing

higher and the activities which are not performing less in organisation.

Cost reports- this is the another reporting method to analysis the areas in which business is most

profitable. It also shows the amount which has spent during conducting business operations in

each categories of business. Items covered under this report is labour, material and also other

expenses of the organisation and their contribution for different types of earnings. This report

will also provide net profit as per category of the item of organisation.

These are the methods of management accounting reports which prepared by organisation

to measure overall performance and profitability of the organisation.

Benefits of management accounting system with organisational context

Management accounting has various benefits as it helps to measure overall performance

of the organisation (Christ and Burritt, 2017). Therefore, different benefits with Jupitor Plc

organisational context are as follows-

It helps in increasing efficiency of the company

Management accounting adopted by organisations because it increases overall efficiency of the

business operations. Management accounting is the process to develop better performance of the

company by comparing and evaluating business operations. Therefore, it also helps to motivate

employees morale by which needs gets fulfilled.

It increases the lines of profitability

Capital budgeting and budgetary controls are the parts of management accounting. These

methods used to eliminate extra expenditure of business operations so that cost get saved.

Therefore, this process helps to increase lines of profits in organisation which helps to reduce

price of products.

It simplifies decision making process

Management accounting helps to develop effective decision by analysing financial statements of

the company. It also creates interpretation of the regular business transactions of the company.

This accounting simplified financial statements by which appropriate decision developed by

managers of the company.

4

higher and the activities which are not performing less in organisation.

Cost reports- this is the another reporting method to analysis the areas in which business is most

profitable. It also shows the amount which has spent during conducting business operations in

each categories of business. Items covered under this report is labour, material and also other

expenses of the organisation and their contribution for different types of earnings. This report

will also provide net profit as per category of the item of organisation.

These are the methods of management accounting reports which prepared by organisation

to measure overall performance and profitability of the organisation.

Benefits of management accounting system with organisational context

Management accounting has various benefits as it helps to measure overall performance

of the organisation (Christ and Burritt, 2017). Therefore, different benefits with Jupitor Plc

organisational context are as follows-

It helps in increasing efficiency of the company

Management accounting adopted by organisations because it increases overall efficiency of the

business operations. Management accounting is the process to develop better performance of the

company by comparing and evaluating business operations. Therefore, it also helps to motivate

employees morale by which needs gets fulfilled.

It increases the lines of profitability

Capital budgeting and budgetary controls are the parts of management accounting. These

methods used to eliminate extra expenditure of business operations so that cost get saved.

Therefore, this process helps to increase lines of profits in organisation which helps to reduce

price of products.

It simplifies decision making process

Management accounting helps to develop effective decision by analysing financial statements of

the company. It also creates interpretation of the regular business transactions of the company.

This accounting simplified financial statements by which appropriate decision developed by

managers of the company.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost transparency

Management accounting works closely with IT department of the company because majority of

cost come from that department only (Otley, 2016). Therefore, to develop effective budget in

organisation this accounting provides cost transparency to company.

Flexibility and freedom

Nature of management accounting is flexible as this not require to made with particular period of

time. Therefore, this reports made with enough time which gives accurate performance of the

company.

Helps to achieved goals of organisation

Management accounting provides a detailed information of company's performance which helps

company in developing effective decisions by which organisational objectives get achieved with

the long term success.

Integration of management accounting system and management accounting report in

organisational process

Jupiter Plc has integrated management accounting report and system to achieved business

performance effectively. By doing integration company will able to develop effective decision

which helps them to achieve overall business objectives. Firstly, this management accounting

system helps organisation in increasing overall efficiency of the company. These increase in

efficiency helps them to perform their performance by which they will able to gain competitive

advantages in business market. Management accounting is best known for flexibility accounting

therefore these helps them to prepare accounts with enough process of time.

Jupiter Plc organisation process also gets improved after integrating management

accounting system and management accounting report when by comparing their statements

company's lines of profitability increases (Hieu and Dung, 2018). This comparison is done by

making capital budgeting and also with budgetary control of the organisation. These methods

help Jupiter in reducing their extra expenditures of the company.

This integration also provides cost transparency in products of the company by which

they will able to decide the price of the goods and services of the company. By calibrating with

5

Management accounting works closely with IT department of the company because majority of

cost come from that department only (Otley, 2016). Therefore, to develop effective budget in

organisation this accounting provides cost transparency to company.

Flexibility and freedom

Nature of management accounting is flexible as this not require to made with particular period of

time. Therefore, this reports made with enough time which gives accurate performance of the

company.

Helps to achieved goals of organisation

Management accounting provides a detailed information of company's performance which helps

company in developing effective decisions by which organisational objectives get achieved with

the long term success.

Integration of management accounting system and management accounting report in

organisational process

Jupiter Plc has integrated management accounting report and system to achieved business

performance effectively. By doing integration company will able to develop effective decision

which helps them to achieve overall business objectives. Firstly, this management accounting

system helps organisation in increasing overall efficiency of the company. These increase in

efficiency helps them to perform their performance by which they will able to gain competitive

advantages in business market. Management accounting is best known for flexibility accounting

therefore these helps them to prepare accounts with enough process of time.

Jupiter Plc organisation process also gets improved after integrating management

accounting system and management accounting report when by comparing their statements

company's lines of profitability increases (Hieu and Dung, 2018). This comparison is done by

making capital budgeting and also with budgetary control of the organisation. These methods

help Jupiter in reducing their extra expenditures of the company.

This integration also provides cost transparency in products of the company by which

they will able to decide the price of the goods and services of the company. By calibrating with

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IT department company will able in developing effective budget for business operations. Further,

this also helps organisation in simplified decision making process by interpreting financial

statements of the company. Overall impact of this integration between management accounting

system and management accounting report is that Jupiter Plc is able to achieve its organisational

objectives and also will able to develop effective strategies by which future needs and goals of

the organisation achieved from business market.

TASK 2

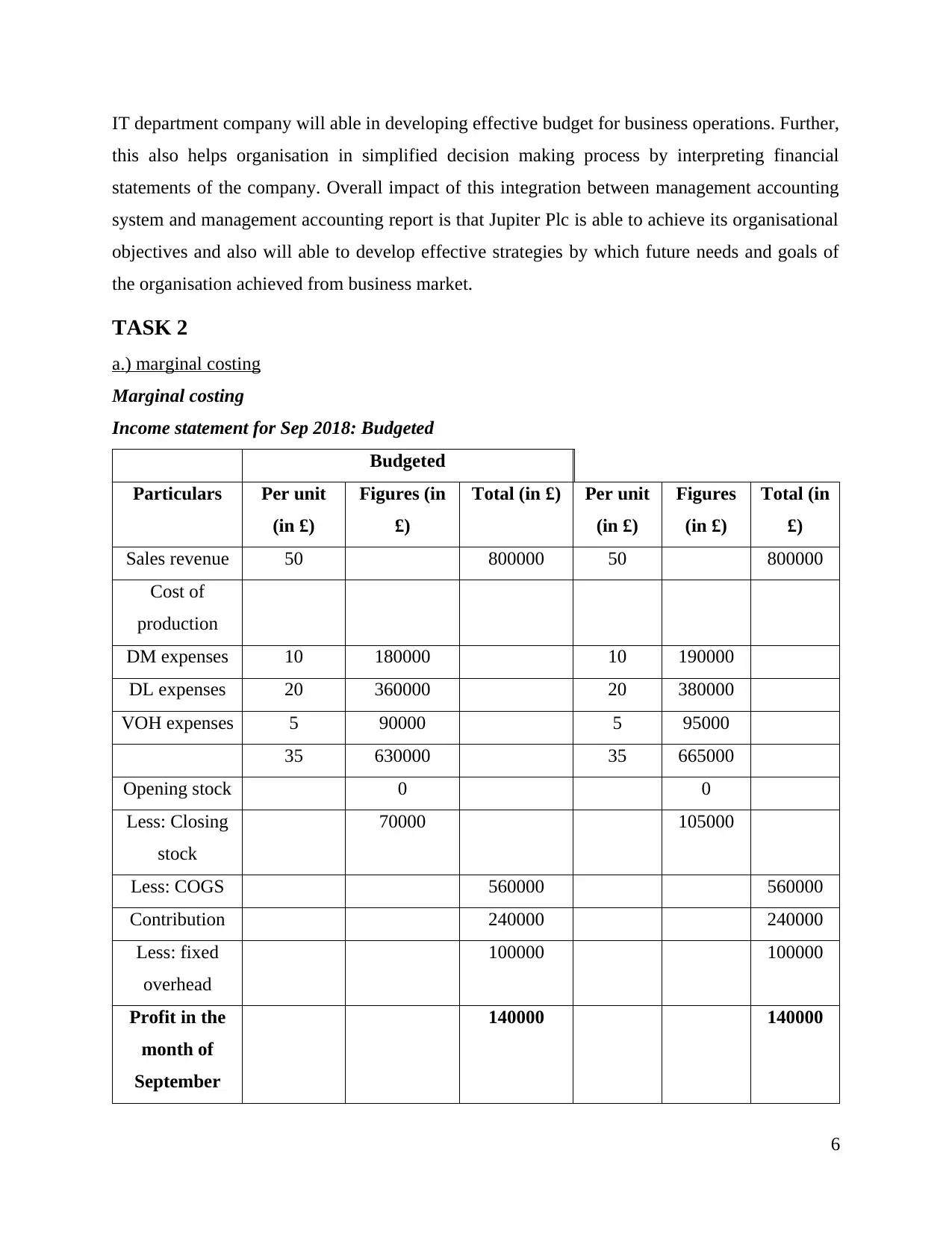

a.) marginal costing

Marginal costing

Income statement for Sep 2018: Budgeted

Budgeted

Particulars Per unit

(in £)

Figures (in

£)

Total (in £) Per unit

(in £)

Figures

(in £)

Total (in

£)

Sales revenue 50 800000 50 800000

Cost of

production

DM expenses 10 180000 10 190000

DL expenses 20 360000 20 380000

VOH expenses 5 90000 5 95000

35 630000 35 665000

Opening stock 0 0

Less: Closing

stock

70000 105000

Less: COGS 560000 560000

Contribution 240000 240000

Less: fixed

overhead

100000 100000

Profit in the

month of

September

140000 140000

6

this also helps organisation in simplified decision making process by interpreting financial

statements of the company. Overall impact of this integration between management accounting

system and management accounting report is that Jupiter Plc is able to achieve its organisational

objectives and also will able to develop effective strategies by which future needs and goals of

the organisation achieved from business market.

TASK 2

a.) marginal costing

Marginal costing

Income statement for Sep 2018: Budgeted

Budgeted

Particulars Per unit

(in £)

Figures (in

£)

Total (in £) Per unit

(in £)

Figures

(in £)

Total (in

£)

Sales revenue 50 800000 50 800000

Cost of

production

DM expenses 10 180000 10 190000

DL expenses 20 360000 20 380000

VOH expenses 5 90000 5 95000

35 630000 35 665000

Opening stock 0 0

Less: Closing

stock

70000 105000

Less: COGS 560000 560000

Contribution 240000 240000

Less: fixed

overhead

100000 100000

Profit in the

month of

September

140000 140000

6

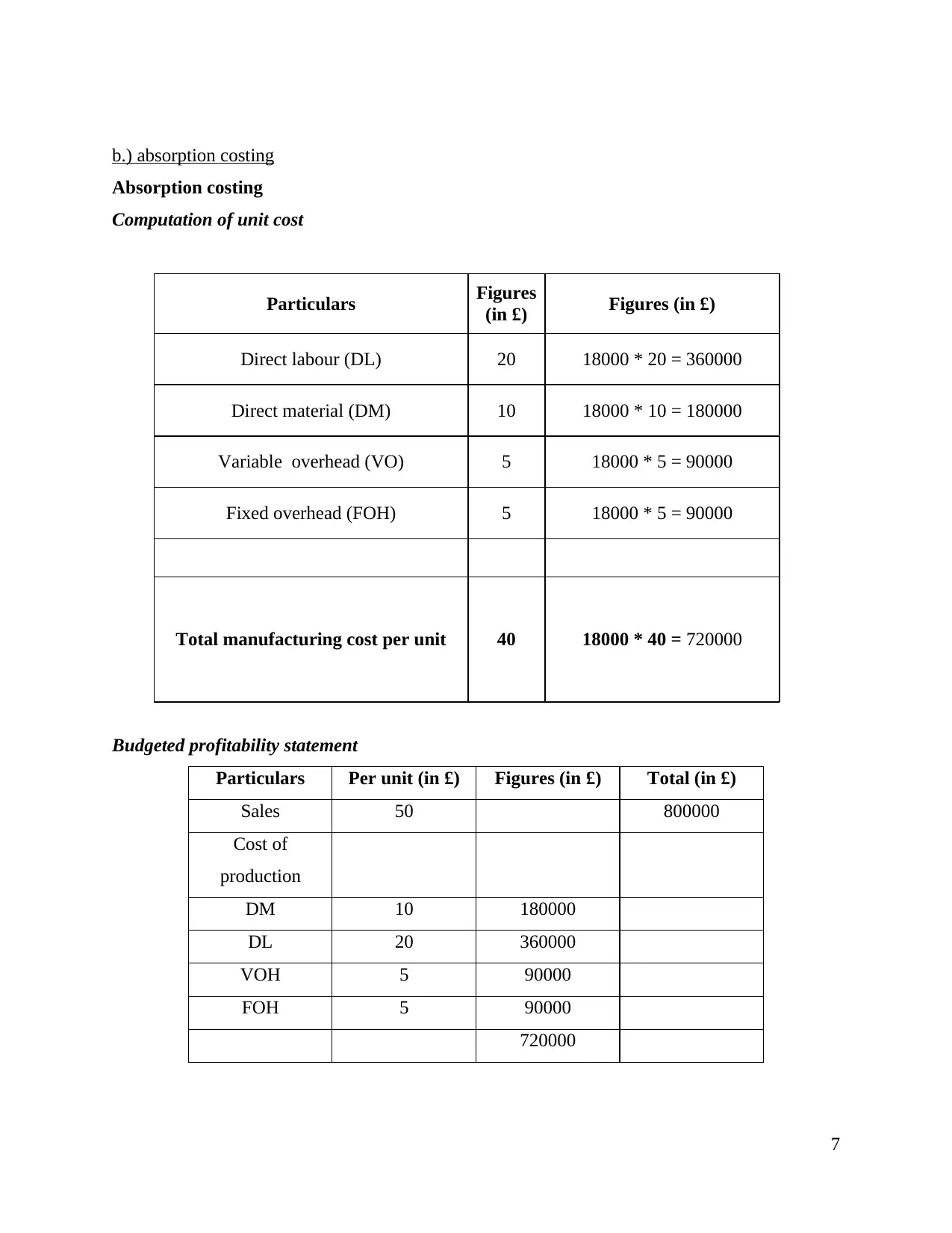

b.) absorption costing

Absorption costing

Computation of unit cost

Particulars Figures

(in £) Figures (in £)

Direct labour (DL) 20 18000 * 20 = 360000

Direct material (DM) 10 18000 * 10 = 180000

Variable overhead (VO) 5 18000 * 5 = 90000

Fixed overhead (FOH) 5 18000 * 5 = 90000

Total manufacturing cost per unit 40 18000 * 40 = 720000

Budgeted profitability statement

Particulars Per unit (in £) Figures (in £) Total (in £)

Sales 50 800000

Cost of

production

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

720000

7

Absorption costing

Computation of unit cost

Particulars Figures

(in £) Figures (in £)

Direct labour (DL) 20 18000 * 20 = 360000

Direct material (DM) 10 18000 * 10 = 180000

Variable overhead (VO) 5 18000 * 5 = 90000

Fixed overhead (FOH) 5 18000 * 5 = 90000

Total manufacturing cost per unit 40 18000 * 40 = 720000

Budgeted profitability statement

Particulars Per unit (in £) Figures (in £) Total (in £)

Sales 50 800000

Cost of

production

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

720000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

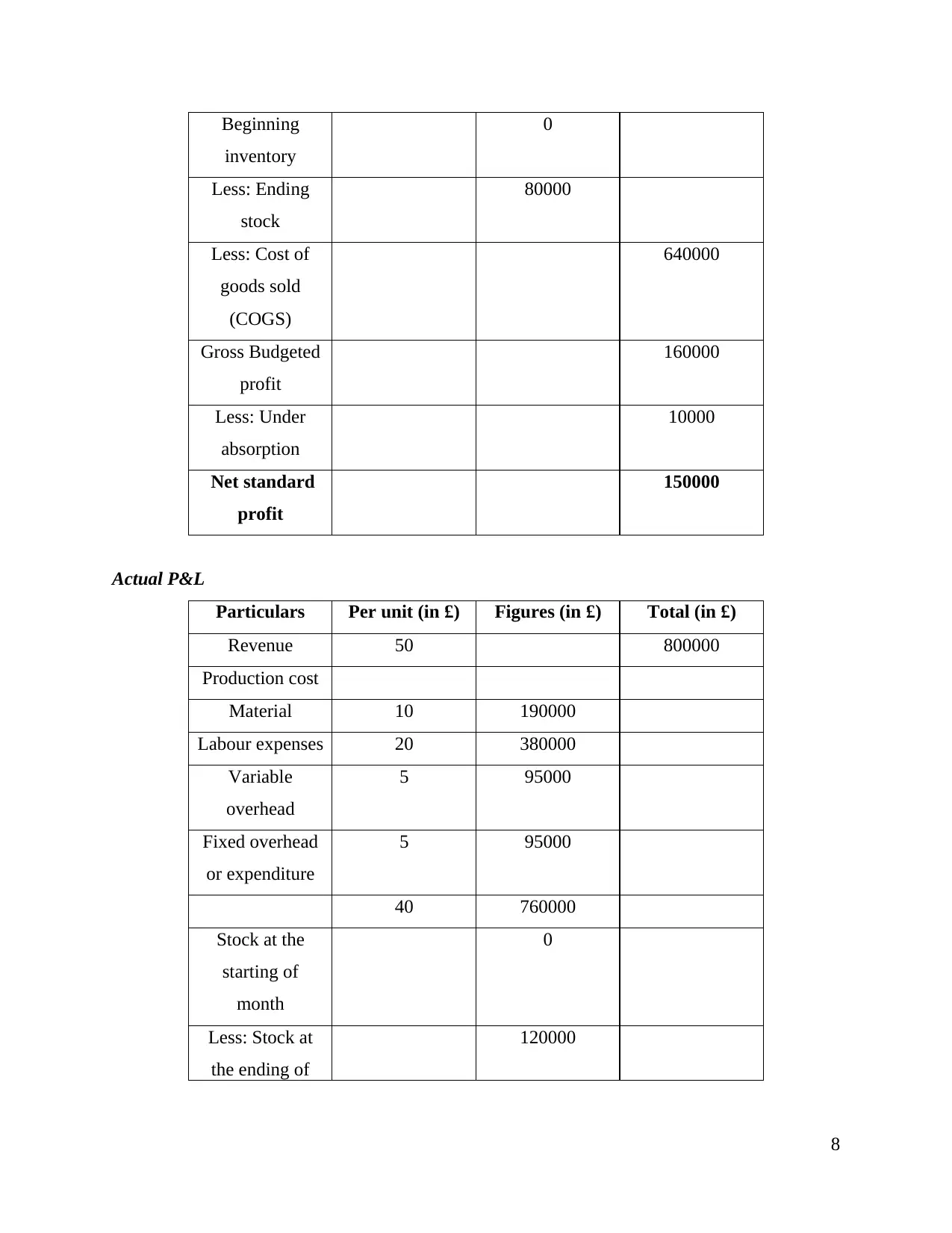

Beginning

inventory

0

Less: Ending

stock

80000

Less: Cost of

goods sold

(COGS)

640000

Gross Budgeted

profit

160000

Less: Under

absorption

10000

Net standard

profit

150000

Actual P&L

Particulars Per unit (in £) Figures (in £) Total (in £)

Revenue 50 800000

Production cost

Material 10 190000

Labour expenses 20 380000

Variable

overhead

5 95000

Fixed overhead

or expenditure

5 95000

40 760000

Stock at the

starting of

month

0

Less: Stock at

the ending of

120000

8

inventory

0

Less: Ending

stock

80000

Less: Cost of

goods sold

(COGS)

640000

Gross Budgeted

profit

160000

Less: Under

absorption

10000

Net standard

profit

150000

Actual P&L

Particulars Per unit (in £) Figures (in £) Total (in £)

Revenue 50 800000

Production cost

Material 10 190000

Labour expenses 20 380000

Variable

overhead

5 95000

Fixed overhead

or expenditure

5 95000

40 760000

Stock at the

starting of

month

0

Less: Stock at

the ending of

120000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

September

Less: COGS 640000

Standard profit 160000

Less: Under

absorption

5000

Budgeted profit 155000

Interpretation: from the above table, it is interpreted that as per marginal costing profit for the

month of September is 1,40,000 and as per absorption costing profit net standard profit is

1,50,000 and budgeted profit is 155000. For Jupiter plc company it is profitable for them in

adopting absorption costing method in calculating profits of the firm.

TASK 3

Advantages and disadvantage of different types of planning tools used in budgetary control

Planning tools used by organisation to manage organisational plans, goals and also to

forecast company's overall budgets. This planning tools overall helps in achieving organisational

objectives. Different budgetary tools are zero-based budgeting, top-down budgeting and activity

based budgeting.

Advantages and disadvantage of zero-based budgeting

Profit centre- which means that it helps in properly allocating resources of the

organisation by which overall profitability increased in the organisation. This results in

generating high amount of revenues by which funding will appropriately generate in

organisation (Chenhall and Moers, 2015).

Detailed information- it provides information which is in detail therefore business gets

save from reducing errors of the organisation. Therefore, these method helps to look

closely business process and operations in achieving goals.

It does not focus on cost centres- this method does not generate immediate profits and

also does not encourage for the funding. This effect long term profitability of the

company which is not good for company's health.

9

Less: COGS 640000

Standard profit 160000

Less: Under

absorption

5000

Budgeted profit 155000

Interpretation: from the above table, it is interpreted that as per marginal costing profit for the

month of September is 1,40,000 and as per absorption costing profit net standard profit is

1,50,000 and budgeted profit is 155000. For Jupiter plc company it is profitable for them in

adopting absorption costing method in calculating profits of the firm.

TASK 3

Advantages and disadvantage of different types of planning tools used in budgetary control

Planning tools used by organisation to manage organisational plans, goals and also to

forecast company's overall budgets. This planning tools overall helps in achieving organisational

objectives. Different budgetary tools are zero-based budgeting, top-down budgeting and activity

based budgeting.

Advantages and disadvantage of zero-based budgeting

Profit centre- which means that it helps in properly allocating resources of the

organisation by which overall profitability increased in the organisation. This results in

generating high amount of revenues by which funding will appropriately generate in

organisation (Chenhall and Moers, 2015).

Detailed information- it provides information which is in detail therefore business gets

save from reducing errors of the organisation. Therefore, these method helps to look

closely business process and operations in achieving goals.

It does not focus on cost centres- this method does not generate immediate profits and

also does not encourage for the funding. This effect long term profitability of the

company which is not good for company's health.

9

Too complex- it need detail information for the analysis which make complex for

managers in developing budget for organisation.

Advantages and disadvantage of top down budgeting

Financial control- it helps managers in providing detailed information of financial needs

of the company. It provides decision regarding factors which provide positive impact of

finance in company. Therefore, it is used by managers in maintaining financial budget of

the organisation.

Accountability of staff- to develop greater financial accountability and for comparing

more product this method is the best suited to achieve this factors. In this method of

budget certain budget is provided to workers in performing their job role.

Inaccurate forecasting- this sometimes create an over funding because understanding of

financial needs will only be better when it runs under a flow of management. Employee morale- it decreases employee morale when resentful input is not valued in

budgeting process. Therefore, this method is not suitable for financial issues.

Advantages and disadvantage of activity based costing

Accurate product cost- this method provides an accuracy and reliability of company's

products. In determining overall cost determination this method is beneficial for

organisations.

Track activities for cost object- this method helpful in recognising activities which is

within and beyond control of organisation (Novas, Alves, and Sousa, 2017). Therefore,

this method provides an information related to cost activities of the company.

High implementation cost- to implement activity based costing this method will not

prove to be best because wastage of overheads occur most in this method. Also it

required huge time to develop this method in organisation.

Use of different planning tools for preparing budget

Planning tools as discussed above are activity-based budgeting, zero-based budgeting and

top down budgeting. Jupiter Plc apply this method to develop effective budget for organisation

activities. Their use are as follows-

10

managers in developing budget for organisation.

Advantages and disadvantage of top down budgeting

Financial control- it helps managers in providing detailed information of financial needs

of the company. It provides decision regarding factors which provide positive impact of

finance in company. Therefore, it is used by managers in maintaining financial budget of

the organisation.

Accountability of staff- to develop greater financial accountability and for comparing

more product this method is the best suited to achieve this factors. In this method of

budget certain budget is provided to workers in performing their job role.

Inaccurate forecasting- this sometimes create an over funding because understanding of

financial needs will only be better when it runs under a flow of management. Employee morale- it decreases employee morale when resentful input is not valued in

budgeting process. Therefore, this method is not suitable for financial issues.

Advantages and disadvantage of activity based costing

Accurate product cost- this method provides an accuracy and reliability of company's

products. In determining overall cost determination this method is beneficial for

organisations.

Track activities for cost object- this method helpful in recognising activities which is

within and beyond control of organisation (Novas, Alves, and Sousa, 2017). Therefore,

this method provides an information related to cost activities of the company.

High implementation cost- to implement activity based costing this method will not

prove to be best because wastage of overheads occur most in this method. Also it

required huge time to develop this method in organisation.

Use of different planning tools for preparing budget

Planning tools as discussed above are activity-based budgeting, zero-based budgeting and

top down budgeting. Jupiter Plc apply this method to develop effective budget for organisation

activities. Their use are as follows-

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.