Comprehensive Report on Management Accounting Systems at Jupiter PLC

VerifiedAdded on 2020/10/23

|15

|5003

|83

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and their application within Jupiter PLC, a medium-sized food packaging company. The report explores the meaning of management accounting, detailing various systems such as inventory management, job costing, cost accounting, and price optimization. It examines different management accounting reporting methods, including inventory management reporting, job cost reporting, account receivable reporting, and performance reporting. The report also discusses the benefits of implementing management accounting systems and highlights the integration of these systems and reporting in organizational processes. Furthermore, the report analyzes costing techniques, including absorption and marginal costing, and their role in preparing income statements. It investigates the merits and demerits of planning tools used in budgetary control, as well as their application in preparing and forecasting budgets. The report also assesses how these tools help solve financial problems, comparing Jupiter PLC's approach with other organizations and evaluating the contribution of management accounting systems to sustainable success. The report concludes with an evaluation of how planning tools of budgetary control assist in solving financial problems.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Meaning of management accounting......................................................................................1

Different methods of management accounting reporting.......................................................3

Benefits of management accounting systems.........................................................................4

Integration of management accounting systems and management accounting reporting in

organizational processes.........................................................................................................4

TASK 2............................................................................................................................................5

Costing techniques and preparation of income statements.....................................................5

TASK 3............................................................................................................................................7

Merits and demerits of different types of planning tools used in budgetary control..............7

Use of planning tools in preparing and forecasting budgets..................................................9

Way in which planning tools help in solving financial problems..........................................9

TASK 4............................................................................................................................................9

Comparison of organizations adapting management accounting systems to resolve financial

issues.......................................................................................................................................9

Contribution of management accounting systems in achieving sustainable success...........10

Evaluation of how planning tools of budgetary control helps in solving financial problems10

CONLUSION ...............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Meaning of management accounting......................................................................................1

Different methods of management accounting reporting.......................................................3

Benefits of management accounting systems.........................................................................4

Integration of management accounting systems and management accounting reporting in

organizational processes.........................................................................................................4

TASK 2............................................................................................................................................5

Costing techniques and preparation of income statements.....................................................5

TASK 3............................................................................................................................................7

Merits and demerits of different types of planning tools used in budgetary control..............7

Use of planning tools in preparing and forecasting budgets..................................................9

Way in which planning tools help in solving financial problems..........................................9

TASK 4............................................................................................................................................9

Comparison of organizations adapting management accounting systems to resolve financial

issues.......................................................................................................................................9

Contribution of management accounting systems in achieving sustainable success...........10

Evaluation of how planning tools of budgetary control helps in solving financial problems10

CONLUSION ...............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is defined as process of collecting information, its interpretation

and then providing to management for decision making. In present time, every organisation

looking for valuable and reliable amounts so they can apply management accounting system for

recording necessary financial transactions. Management accounting is the proposition of

accounting information in order to develop the policies to be adoptive by the management and

help for day to day activities. In the context of this report, company chosen is Jupiter PLC. It is a

medium sized manufacturing company that is engaged in food packaging and delivering. In this

report aims to about various types of management accounting system as well as reporting method

useful for a company. Different types of costing methods those are taken into account for the

calculation of net profit (Busco and Scapens, 2011). Use of merit and demerit of planning tools

used in budgetary control process. Comparison with other organisation is done to examine, and

describing how management accounting system implemented for resolving financial problems.

TASK 1

Meaning of management accounting

Management accounting may be defined as a science and art to provide information to

the management so that they can perform their functions simultaneously and efficiently for

modify their operating efficiency. In the other words, it is the term used to describe the

accounting techniques, systems and methods which complied with special ability and knowledge

to assist management in its task of minimizing losses maximizing profits. Reports prepared under

management accounting systems are analysed and then decision making is done on this basis.

Management accounting aims at providing information to managers so that they can give this

information to senior management to run Jupiter PLC. Many aspects of accounting are covered

under this such as capital budgeting, net margin, gross margin, future trends, valuation

techniques etc. Information derived from management accounting is communicated to internal

stakeholders which are investors, board, and employees. Management accounting can be said as

lifeline for organizations (Sykianakis and Bellas, 2005). Because organizational structure is

complex and it is difficult to handle various departments. Different types of management

accounting systems mentioned below:

1

Management accounting is defined as process of collecting information, its interpretation

and then providing to management for decision making. In present time, every organisation

looking for valuable and reliable amounts so they can apply management accounting system for

recording necessary financial transactions. Management accounting is the proposition of

accounting information in order to develop the policies to be adoptive by the management and

help for day to day activities. In the context of this report, company chosen is Jupiter PLC. It is a

medium sized manufacturing company that is engaged in food packaging and delivering. In this

report aims to about various types of management accounting system as well as reporting method

useful for a company. Different types of costing methods those are taken into account for the

calculation of net profit (Busco and Scapens, 2011). Use of merit and demerit of planning tools

used in budgetary control process. Comparison with other organisation is done to examine, and

describing how management accounting system implemented for resolving financial problems.

TASK 1

Meaning of management accounting

Management accounting may be defined as a science and art to provide information to

the management so that they can perform their functions simultaneously and efficiently for

modify their operating efficiency. In the other words, it is the term used to describe the

accounting techniques, systems and methods which complied with special ability and knowledge

to assist management in its task of minimizing losses maximizing profits. Reports prepared under

management accounting systems are analysed and then decision making is done on this basis.

Management accounting aims at providing information to managers so that they can give this

information to senior management to run Jupiter PLC. Many aspects of accounting are covered

under this such as capital budgeting, net margin, gross margin, future trends, valuation

techniques etc. Information derived from management accounting is communicated to internal

stakeholders which are investors, board, and employees. Management accounting can be said as

lifeline for organizations (Sykianakis and Bellas, 2005). Because organizational structure is

complex and it is difficult to handle various departments. Different types of management

accounting systems mentioned below:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system: It tracks complete supply chain of business operations

or a part of it. Also it covers every aspect from manufacturing, warehousing to supplying of

goods to retailers and wholesalers for sale. This system can be said as a combination of different

technologies(software, hardware) and processes which helps in monitoring inventory. Inventory

includes raw materials, finished goods, work in progress (Hussain and Gunasekaran, 2002). This

system allows to take better decisions regarding investments and maintenance of inventory in

Jupiter PLC. There are different types of inventory management systems prevailing in companies

like manufacturing inventory system, warehouse inventory management, retail inventory

management. Software used for this system includes many items like bar coding, reporting tools,

inventory alerts and forecasting.

Job costing system: Job costing system refers to the procedure of collecting information

related to costs associated with a job or project. Information or data collected through this system

are also used in determining quality of computation system of Jupiter PLC. As these information

are later assists in quoting prices of products taking into consideration profit part. Form of

information provided by this system are direct material, direct labour and overhead. Overhead

costs are depreciation, rent, electricity etc. In practical manner, job costing system should fulfil

requirements of customer. With this, one can identify profitability of each job or project in

Jupiter PLC.

Cost accounting system: This system is also known as product costing. Cost accounting

system is a kind of framework used for cost estimation, analysing degree of profitability, stock

valuation and cost controlling. For the purpose of valuable operations, there should be an

accurate estimation of product cost. When it is done, one can easily identify between more

profitable goods and less profitable goods (Grabski, Leech and Sangster, 2009). Thereafter,

ascertainment of closing stock, work-in-progress, and finished stock will be done to prepare

financial reports as well as financial statements. Balance sheet and trading account necessarily

needed value of inventory to depict correct financial position of Jupiter PLC.

Price optimization system: Price optimization system refers to a process of identifying

that level of price which is optimum. In other words, it defines setting reasonable level of value

that a customer is able and willing to pay for goods as well as for services. Factors that affect

price optimization are market demand, degree of competition, manufacturing costs etc. Jupiter

PLC should not set prices of goods at too much higher level and neither at too much low level.

2

or a part of it. Also it covers every aspect from manufacturing, warehousing to supplying of

goods to retailers and wholesalers for sale. This system can be said as a combination of different

technologies(software, hardware) and processes which helps in monitoring inventory. Inventory

includes raw materials, finished goods, work in progress (Hussain and Gunasekaran, 2002). This

system allows to take better decisions regarding investments and maintenance of inventory in

Jupiter PLC. There are different types of inventory management systems prevailing in companies

like manufacturing inventory system, warehouse inventory management, retail inventory

management. Software used for this system includes many items like bar coding, reporting tools,

inventory alerts and forecasting.

Job costing system: Job costing system refers to the procedure of collecting information

related to costs associated with a job or project. Information or data collected through this system

are also used in determining quality of computation system of Jupiter PLC. As these information

are later assists in quoting prices of products taking into consideration profit part. Form of

information provided by this system are direct material, direct labour and overhead. Overhead

costs are depreciation, rent, electricity etc. In practical manner, job costing system should fulfil

requirements of customer. With this, one can identify profitability of each job or project in

Jupiter PLC.

Cost accounting system: This system is also known as product costing. Cost accounting

system is a kind of framework used for cost estimation, analysing degree of profitability, stock

valuation and cost controlling. For the purpose of valuable operations, there should be an

accurate estimation of product cost. When it is done, one can easily identify between more

profitable goods and less profitable goods (Grabski, Leech and Sangster, 2009). Thereafter,

ascertainment of closing stock, work-in-progress, and finished stock will be done to prepare

financial reports as well as financial statements. Balance sheet and trading account necessarily

needed value of inventory to depict correct financial position of Jupiter PLC.

Price optimization system: Price optimization system refers to a process of identifying

that level of price which is optimum. In other words, it defines setting reasonable level of value

that a customer is able and willing to pay for goods as well as for services. Factors that affect

price optimization are market demand, degree of competition, manufacturing costs etc. Jupiter

PLC should not set prices of goods at too much higher level and neither at too much low level.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Because, if prices will be high then no one will purchase and if prices will be low then profit

margin would be low. For this, price optimization model has been developed which calculates

variation of demand in accordance with change in price levels.

Different methods of management accounting reporting

In order to formulate management accounting system, reports are necessarily need to be

prepared. These accounting reports are used for planning, regulating, performance measurement

and decision making (Baxter and Chua, 2006). Report preparation is not a one time process, but

is a continuous in nature according to need. This is because, there are so many critical decisions

are dependent on credibility of these reports. That is why, these are carefully drafted by

managers. Management accounting reporting is mainly done to know about overall level of

performance of Jupiter PLC. There is no requirement of drafting management accounting reports

in a specific standardized format. Also these reports are necessarily to be prepared by every

organization. This depends on the need of company. But those companies which prepares these

reports are benefited a lot in efficient operations. Formatting of financial reports are done

keeping in mind GAAP (Generally Accepted Accounting Principles) but management

accounting reports can be made in any format which makes sense. Different methods of

management accounting reporting are:

Inventory management reporting: These reports are valuable for those companies

which are engaged in manufacturing activities. Thus, for these kind of operations, these helps in

centralizing information about cost of inventory, labour costs, overheads incurred in production

process. Manufacturing processes becomes as much efficient to cop up with changing conditions

in Jupiter PLC. Items consists in these reports are inventory waste, per hour labour costs, and per

unit cost of overheads. Also, comparison can be done among them in accordance with assembly

lines. So, in this way, organization can identify performing areas which are best and reward

system can be made according to departments which performs best.

Job cost reporting: Job cost reporting method refers to cost ascertainment of a particular

job or project. Thereafter, comparison is done between cost incurred and expected revenue

earned that specific job or project (Yalcin, 2012). For the purpose of evaluation of profitability in

Jupiter PLC, these reports are made. In job cost reporting there are few aspects that should be

kept in mind such as smart estimates, need of information, progress reports. These reports are

utilized in a way that, these reports provides considerable amount of time to management for cost

3

margin would be low. For this, price optimization model has been developed which calculates

variation of demand in accordance with change in price levels.

Different methods of management accounting reporting

In order to formulate management accounting system, reports are necessarily need to be

prepared. These accounting reports are used for planning, regulating, performance measurement

and decision making (Baxter and Chua, 2006). Report preparation is not a one time process, but

is a continuous in nature according to need. This is because, there are so many critical decisions

are dependent on credibility of these reports. That is why, these are carefully drafted by

managers. Management accounting reporting is mainly done to know about overall level of

performance of Jupiter PLC. There is no requirement of drafting management accounting reports

in a specific standardized format. Also these reports are necessarily to be prepared by every

organization. This depends on the need of company. But those companies which prepares these

reports are benefited a lot in efficient operations. Formatting of financial reports are done

keeping in mind GAAP (Generally Accepted Accounting Principles) but management

accounting reports can be made in any format which makes sense. Different methods of

management accounting reporting are:

Inventory management reporting: These reports are valuable for those companies

which are engaged in manufacturing activities. Thus, for these kind of operations, these helps in

centralizing information about cost of inventory, labour costs, overheads incurred in production

process. Manufacturing processes becomes as much efficient to cop up with changing conditions

in Jupiter PLC. Items consists in these reports are inventory waste, per hour labour costs, and per

unit cost of overheads. Also, comparison can be done among them in accordance with assembly

lines. So, in this way, organization can identify performing areas which are best and reward

system can be made according to departments which performs best.

Job cost reporting: Job cost reporting method refers to cost ascertainment of a particular

job or project. Thereafter, comparison is done between cost incurred and expected revenue

earned that specific job or project (Yalcin, 2012). For the purpose of evaluation of profitability in

Jupiter PLC, these reports are made. In job cost reporting there are few aspects that should be

kept in mind such as smart estimates, need of information, progress reports. These reports are

utilized in a way that, these reports provides considerable amount of time to management for cost

3

controlling in remaining project. Along with this, decision can be made that whether a particular

job will be continued in future or not.

Account receivable reporting: These reports are mainly prepared by companies which

are highly involved in extending goods and services on credit basis. Debtors increases and this

leads to decrease in profitability. Records of customers are maintained according to their

outstanding balances. This is done to reduce bad debts and strengthening credit policies as well

as terms (Cadez and Guilding, 2008). Customers are extended credit on the basis of number of

days such as 30 days, 60 days, 90 days. Credit repayment abilities are examined so that next

time Jupiter PLC would be aware about customers who made late payment. These reports are

also known as accounts receivable aging reports. These mainly includes customer invoices and

credit memos.

Performance reporting: It is defined as process of collecting information, and then

communicating it to relevant parties such as senior management, executives. Information is in

form of status reports, progress measurement, and forecasting. Performance is measured in

Jupiter PLC on the basis of some established criteria. It is being prepared separately for various

departments and for organization as a whole. Recommendations and suggestions are given to

those people as well departments who underperformed.

Benefits of management accounting systems

There are several benefits derived by companies which adopts management accounting

systems. Different systems of management accounting that mentioned above are inventory

management, price optimization, cost accounting, and job costing. These are vital part of Jupiter

PLC as these systems increases efficiency, enhances level of profitability with the help of capital

budgeting, and simplify complex decision-making process. Along with this, inventory

management reports helps in maintaining optimum level of inventory. Price optimization system

ultimately leads to customer satisfaction and increase in market share (Harris and Durden, 2012).

Cost accounting contributes to proper appropriation and allocation of production costs. Lastly,

Job costing assists in driving effective performance.

Integration of management accounting systems and management accounting reporting in

organizational processes

Management accounting reporting and management accounting systems have a lot of

similarities, so these are integrated in Jupiter PLC to increase level of it among all present as well

4

job will be continued in future or not.

Account receivable reporting: These reports are mainly prepared by companies which

are highly involved in extending goods and services on credit basis. Debtors increases and this

leads to decrease in profitability. Records of customers are maintained according to their

outstanding balances. This is done to reduce bad debts and strengthening credit policies as well

as terms (Cadez and Guilding, 2008). Customers are extended credit on the basis of number of

days such as 30 days, 60 days, 90 days. Credit repayment abilities are examined so that next

time Jupiter PLC would be aware about customers who made late payment. These reports are

also known as accounts receivable aging reports. These mainly includes customer invoices and

credit memos.

Performance reporting: It is defined as process of collecting information, and then

communicating it to relevant parties such as senior management, executives. Information is in

form of status reports, progress measurement, and forecasting. Performance is measured in

Jupiter PLC on the basis of some established criteria. It is being prepared separately for various

departments and for organization as a whole. Recommendations and suggestions are given to

those people as well departments who underperformed.

Benefits of management accounting systems

There are several benefits derived by companies which adopts management accounting

systems. Different systems of management accounting that mentioned above are inventory

management, price optimization, cost accounting, and job costing. These are vital part of Jupiter

PLC as these systems increases efficiency, enhances level of profitability with the help of capital

budgeting, and simplify complex decision-making process. Along with this, inventory

management reports helps in maintaining optimum level of inventory. Price optimization system

ultimately leads to customer satisfaction and increase in market share (Harris and Durden, 2012).

Cost accounting contributes to proper appropriation and allocation of production costs. Lastly,

Job costing assists in driving effective performance.

Integration of management accounting systems and management accounting reporting in

organizational processes

Management accounting reporting and management accounting systems have a lot of

similarities, so these are integrated in Jupiter PLC to increase level of it among all present as well

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as potential competitors. Monetary funds of company can be resisted from major fluctuations as

these are used in controlled manner. Different management reports are prepared for each

department and these assists in better functioning. Functions includes planning, organizing,

monitoring as well as measuring performance. In an organization, where there are lot of different

departments, projects as well as processes, management accounting reporting covers every small

detail of them. Management accounting systems monitor all financial aspects of Jupiter PLC like

cost controlling, its estimation and cost incurred by each department as well as process.

TASK 2

Costing techniques and preparation of income statements

Absorption and marginal costing are techniques of ascertaining costs. Cost refers to value

which is paid by a person for purchase or production. Manager has to accumulate all the relevant

information about production costs (Baines and Langfield-Smith, 2003). Because these are very

crucial to know about profitability aspects. There are different types of costs in Jupiter PLC, and

are mainly classified in broad categories of fixed and variable costs. If talk about costing

techniques, they are defined as ways of controlling and appropriation of costs. Also these can be

said as methods for ascertainment of costs, decision-making, and assessment of performance.

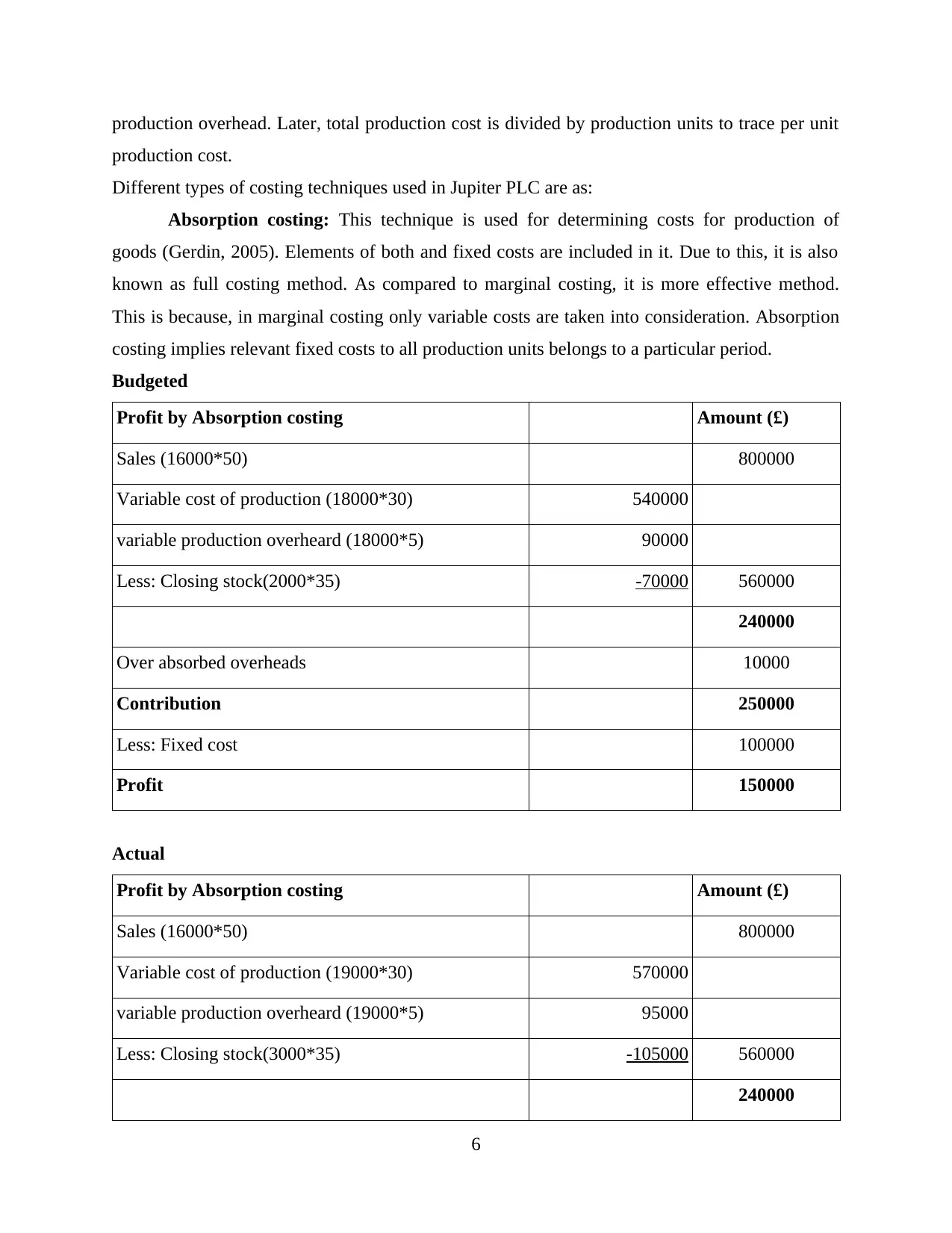

Production cost: Production cost includes direct labour, direct material and overhead

costs. Also indirect costs are counted that are associated with product manufacturing.

Calculation of production cost

Production cost (18000 units)

Direct material 10 180000

Direct labour 20 360000

Total variable cost 540000

Fixed production overhead 100000

Total production cost 640000

Production cost per unit 35.56

Interpretation: As data shown in table, production cost per unit is derived from

calculation of total variable cost and total production cost. Variable cost is sum of direct labour

and direct material. While production cost is ascertained by adding total variable cost and fixed

5

these are used in controlled manner. Different management reports are prepared for each

department and these assists in better functioning. Functions includes planning, organizing,

monitoring as well as measuring performance. In an organization, where there are lot of different

departments, projects as well as processes, management accounting reporting covers every small

detail of them. Management accounting systems monitor all financial aspects of Jupiter PLC like

cost controlling, its estimation and cost incurred by each department as well as process.

TASK 2

Costing techniques and preparation of income statements

Absorption and marginal costing are techniques of ascertaining costs. Cost refers to value

which is paid by a person for purchase or production. Manager has to accumulate all the relevant

information about production costs (Baines and Langfield-Smith, 2003). Because these are very

crucial to know about profitability aspects. There are different types of costs in Jupiter PLC, and

are mainly classified in broad categories of fixed and variable costs. If talk about costing

techniques, they are defined as ways of controlling and appropriation of costs. Also these can be

said as methods for ascertainment of costs, decision-making, and assessment of performance.

Production cost: Production cost includes direct labour, direct material and overhead

costs. Also indirect costs are counted that are associated with product manufacturing.

Calculation of production cost

Production cost (18000 units)

Direct material 10 180000

Direct labour 20 360000

Total variable cost 540000

Fixed production overhead 100000

Total production cost 640000

Production cost per unit 35.56

Interpretation: As data shown in table, production cost per unit is derived from

calculation of total variable cost and total production cost. Variable cost is sum of direct labour

and direct material. While production cost is ascertained by adding total variable cost and fixed

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

production overhead. Later, total production cost is divided by production units to trace per unit

production cost.

Different types of costing techniques used in Jupiter PLC are as:

Absorption costing: This technique is used for determining costs for production of

goods (Gerdin, 2005). Elements of both and fixed costs are included in it. Due to this, it is also

known as full costing method. As compared to marginal costing, it is more effective method.

This is because, in marginal costing only variable costs are taken into consideration. Absorption

costing implies relevant fixed costs to all production units belongs to a particular period.

Budgeted

Profit by Absorption costing Amount (£)

Sales (16000*50) 800000

Variable cost of production (18000*30) 540000

variable production overheard (18000*5) 90000

Less: Closing stock(2000*35) -70000 560000

240000

Over absorbed overheads 10000

Contribution 250000

Less: Fixed cost 100000

Profit 150000

Actual

Profit by Absorption costing Amount (£)

Sales (16000*50) 800000

Variable cost of production (19000*30) 570000

variable production overheard (19000*5) 95000

Less: Closing stock(3000*35) -105000 560000

240000

6

production cost.

Different types of costing techniques used in Jupiter PLC are as:

Absorption costing: This technique is used for determining costs for production of

goods (Gerdin, 2005). Elements of both and fixed costs are included in it. Due to this, it is also

known as full costing method. As compared to marginal costing, it is more effective method.

This is because, in marginal costing only variable costs are taken into consideration. Absorption

costing implies relevant fixed costs to all production units belongs to a particular period.

Budgeted

Profit by Absorption costing Amount (£)

Sales (16000*50) 800000

Variable cost of production (18000*30) 540000

variable production overheard (18000*5) 90000

Less: Closing stock(2000*35) -70000 560000

240000

Over absorbed overheads 10000

Contribution 250000

Less: Fixed cost 100000

Profit 150000

Actual

Profit by Absorption costing Amount (£)

Sales (16000*50) 800000

Variable cost of production (19000*30) 570000

variable production overheard (19000*5) 95000

Less: Closing stock(3000*35) -105000 560000

240000

6

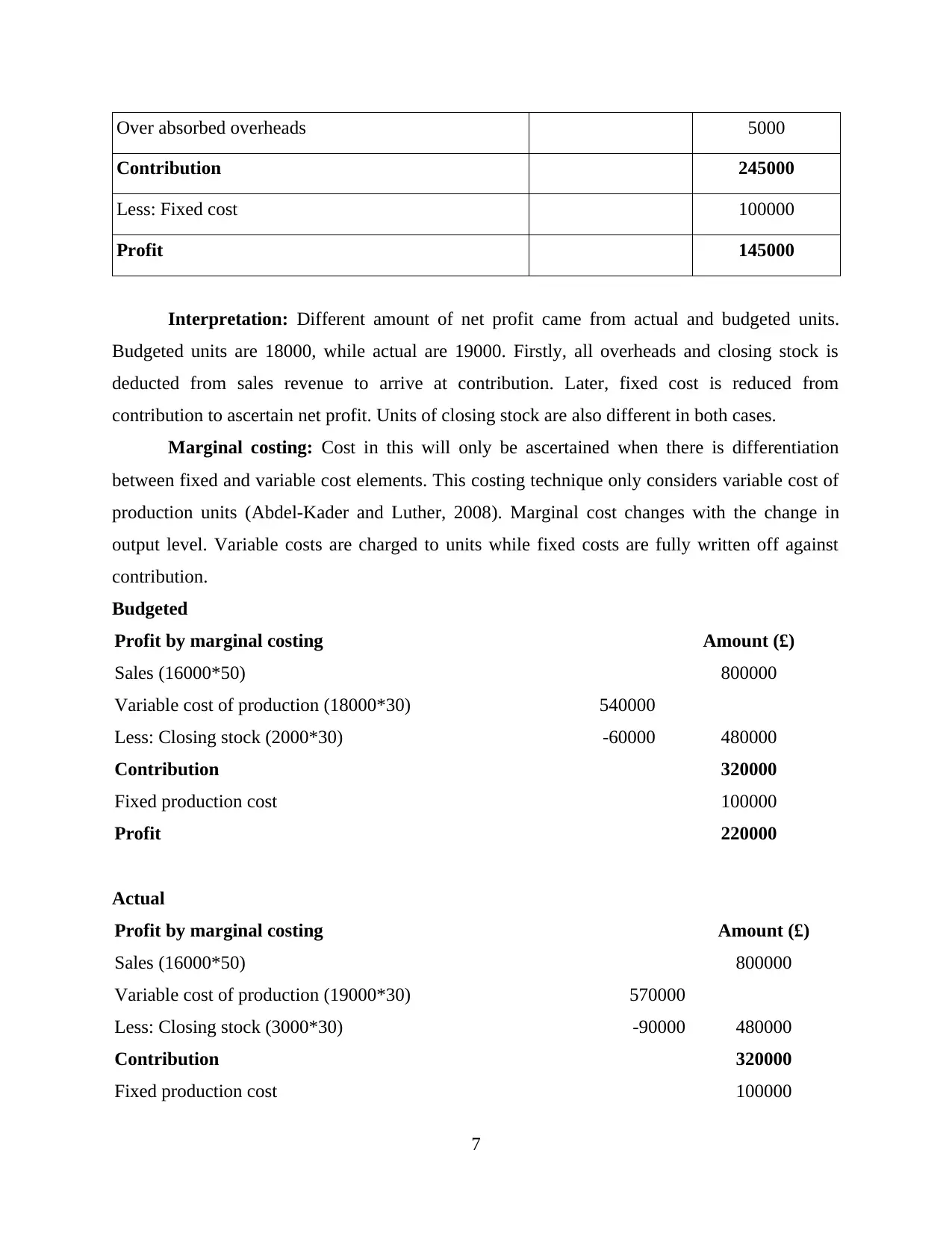

Over absorbed overheads 5000

Contribution 245000

Less: Fixed cost 100000

Profit 145000

Interpretation: Different amount of net profit came from actual and budgeted units.

Budgeted units are 18000, while actual are 19000. Firstly, all overheads and closing stock is

deducted from sales revenue to arrive at contribution. Later, fixed cost is reduced from

contribution to ascertain net profit. Units of closing stock are also different in both cases.

Marginal costing: Cost in this will only be ascertained when there is differentiation

between fixed and variable cost elements. This costing technique only considers variable cost of

production units (Abdel-Kader and Luther, 2008). Marginal cost changes with the change in

output level. Variable costs are charged to units while fixed costs are fully written off against

contribution.

Budgeted

Profit by marginal costing Amount (£)

Sales (16000*50) 800000

Variable cost of production (18000*30) 540000

Less: Closing stock (2000*30) -60000 480000

Contribution 320000

Fixed production cost 100000

Profit 220000

Actual

Profit by marginal costing Amount (£)

Sales (16000*50) 800000

Variable cost of production (19000*30) 570000

Less: Closing stock (3000*30) -90000 480000

Contribution 320000

Fixed production cost 100000

7

Contribution 245000

Less: Fixed cost 100000

Profit 145000

Interpretation: Different amount of net profit came from actual and budgeted units.

Budgeted units are 18000, while actual are 19000. Firstly, all overheads and closing stock is

deducted from sales revenue to arrive at contribution. Later, fixed cost is reduced from

contribution to ascertain net profit. Units of closing stock are also different in both cases.

Marginal costing: Cost in this will only be ascertained when there is differentiation

between fixed and variable cost elements. This costing technique only considers variable cost of

production units (Abdel-Kader and Luther, 2008). Marginal cost changes with the change in

output level. Variable costs are charged to units while fixed costs are fully written off against

contribution.

Budgeted

Profit by marginal costing Amount (£)

Sales (16000*50) 800000

Variable cost of production (18000*30) 540000

Less: Closing stock (2000*30) -60000 480000

Contribution 320000

Fixed production cost 100000

Profit 220000

Actual

Profit by marginal costing Amount (£)

Sales (16000*50) 800000

Variable cost of production (19000*30) 570000

Less: Closing stock (3000*30) -90000 480000

Contribution 320000

Fixed production cost 100000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit 220000

Interpretation: As per given tables, income statement is prepared by marginal costing

method. In this also, separate calculations of net profit are done for actual and budgeted units.

Sales revenue is calculated as per given information. Then, variable cost of production and

closing sock which is differ for actual and budgeted. After that, net profit is derived by deducting

fixed cost from total contribution.

TASK 3

Merits and demerits of different types of planning tools used in budgetary control

Planning tools utilized for budgetary control smooths way to prepare budgets. Budgetary

control is a tool of management according to which actual outcomes, incomes, expenses are

compared with established budgeted figures (Williams and Seaman, 2001). After following

plans, if there are any differences between actual and estimated results, then these are called

variances. Variances have to be reduced by taking appropriate action or measures. Budgetary

control is a very long process because it involves budget preparation, coordination between

different departments, assigning them their roles and responsibilities. Budgetary control starts

with preparation of budgets. Thus, budget is a plan for future in which incomes, expenses are

calculated in advance to achieve definite goals (Gerdin and Greve, 2004). Also, it can be said as

comparison tool for determining which activities and functions an organization can carry out in

future. Although, there are many essential elements of budgetary control successful like budget

period, budget manual, budget centres etc. Main benefits of budgetary control are profit

maximization, coordination among departments, expenditure planning, performance

measurement, and identifying deviations. Objectives of budgetary control are future planning,

reducing wastes and assigning responsibilities to workforce. Planning tools that are used in

budgetary control are mentioned beneath:

Contingency: Contingency planning is done to prepare for unfortunate events or

emergency that can arrive in future. Unfortunate events can be loss of information of clients,

suppliers, customers and other important parties of organisation. It is often done when Jupiter

PLC is somehow aware about future hazard or threat. Steps involved in contingency planning are

preparing, analysing, developing, implementing and review.

8

Interpretation: As per given tables, income statement is prepared by marginal costing

method. In this also, separate calculations of net profit are done for actual and budgeted units.

Sales revenue is calculated as per given information. Then, variable cost of production and

closing sock which is differ for actual and budgeted. After that, net profit is derived by deducting

fixed cost from total contribution.

TASK 3

Merits and demerits of different types of planning tools used in budgetary control

Planning tools utilized for budgetary control smooths way to prepare budgets. Budgetary

control is a tool of management according to which actual outcomes, incomes, expenses are

compared with established budgeted figures (Williams and Seaman, 2001). After following

plans, if there are any differences between actual and estimated results, then these are called

variances. Variances have to be reduced by taking appropriate action or measures. Budgetary

control is a very long process because it involves budget preparation, coordination between

different departments, assigning them their roles and responsibilities. Budgetary control starts

with preparation of budgets. Thus, budget is a plan for future in which incomes, expenses are

calculated in advance to achieve definite goals (Gerdin and Greve, 2004). Also, it can be said as

comparison tool for determining which activities and functions an organization can carry out in

future. Although, there are many essential elements of budgetary control successful like budget

period, budget manual, budget centres etc. Main benefits of budgetary control are profit

maximization, coordination among departments, expenditure planning, performance

measurement, and identifying deviations. Objectives of budgetary control are future planning,

reducing wastes and assigning responsibilities to workforce. Planning tools that are used in

budgetary control are mentioned beneath:

Contingency: Contingency planning is done to prepare for unfortunate events or

emergency that can arrive in future. Unfortunate events can be loss of information of clients,

suppliers, customers and other important parties of organisation. It is often done when Jupiter

PLC is somehow aware about future hazard or threat. Steps involved in contingency planning are

preparing, analysing, developing, implementing and review.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages – Contingency planning helps in risk assessment and management. B-plans

are always prepared so that organization would be prepared for future uncertainties.

Disadvantages – This is very tough task to motivate employees to prepare back up plans

for emergency. Also, probability of happening and non-happening of unfortunate event is

uncertain. Thus, employees do not take this planning seriously.

Forecasting: According to this planning tool, data of past performance is used for future

estimation. Firms that require long-term prospects, forecasting provides them standards

(Naranjo-Gil and Hartmann, 2007). Jupiter PLC uses forecasting technique to determine amount

of expenses to be allocated for budget for a given period of time.

Advantages – It helps in taking informed decisions about business operations. Along with

it, it estimates requirement of resources, prepare schedules for production process.

Disadvantages – Sometimes, it is difficult to forecast future in an accurate manner. No

one can be sure on predictions. Often, forecasting tool uses same data but delivers diverse

outcomes.

Scenario: Scenario planning tool provides way to organization for thinking and strategic

planning about upcoming time. Assumptions are made so that changing business environment

can not affect strategies of Jupiter PLC. Few sets of future uncertainties are designed and then

testing is done on these scenarios. Process of scenario planning consists of different stages that

are identifying dynamic forces and critical uncertainties, after that developing possible scenarios,

and then evaluation of implications.

Advantages – An organization is provided with clearer vision and best predictions

through providing better choices. Critical thinking is involved that develops confidence among

employees of Jupiter PLC.

Disadvantages – It is not an easy task to develop different set of scenario because it

consumes a lot of time and resources. Also this does not give assurance.

Use of planning tools in preparing and forecasting budgets

Planning tools and techniques of budgetary control are vital components of management

accounting. Budgetary control is directly related to budgets. Planning tools used for budgetary

control will also be related to budgets (Järvenpää, 2007). Contingency, forecasting, and scenario

tools are majorly involved in process of developing plans for preparation of budgets. As in

9

are always prepared so that organization would be prepared for future uncertainties.

Disadvantages – This is very tough task to motivate employees to prepare back up plans

for emergency. Also, probability of happening and non-happening of unfortunate event is

uncertain. Thus, employees do not take this planning seriously.

Forecasting: According to this planning tool, data of past performance is used for future

estimation. Firms that require long-term prospects, forecasting provides them standards

(Naranjo-Gil and Hartmann, 2007). Jupiter PLC uses forecasting technique to determine amount

of expenses to be allocated for budget for a given period of time.

Advantages – It helps in taking informed decisions about business operations. Along with

it, it estimates requirement of resources, prepare schedules for production process.

Disadvantages – Sometimes, it is difficult to forecast future in an accurate manner. No

one can be sure on predictions. Often, forecasting tool uses same data but delivers diverse

outcomes.

Scenario: Scenario planning tool provides way to organization for thinking and strategic

planning about upcoming time. Assumptions are made so that changing business environment

can not affect strategies of Jupiter PLC. Few sets of future uncertainties are designed and then

testing is done on these scenarios. Process of scenario planning consists of different stages that

are identifying dynamic forces and critical uncertainties, after that developing possible scenarios,

and then evaluation of implications.

Advantages – An organization is provided with clearer vision and best predictions

through providing better choices. Critical thinking is involved that develops confidence among

employees of Jupiter PLC.

Disadvantages – It is not an easy task to develop different set of scenario because it

consumes a lot of time and resources. Also this does not give assurance.

Use of planning tools in preparing and forecasting budgets

Planning tools and techniques of budgetary control are vital components of management

accounting. Budgetary control is directly related to budgets. Planning tools used for budgetary

control will also be related to budgets (Järvenpää, 2007). Contingency, forecasting, and scenario

tools are majorly involved in process of developing plans for preparation of budgets. As in

9

budget, expenses are allocated and income is estimated. Thus, contingency removes all the

hindrances that can create issue in budget planning and forecasting.

Way in which planning tools help in solving financial problems

It is better understood that financial issues occurs with every business. But the way in

which resolved through planning tools is important. Financial problems from that planning tools

have to deal are uncertain cash inflow and outflow, insufficient funding or financing for capital

needs, excessive debts, reducing profitability. Scenario tool conceptualize all financial aspects in

advance, so that in future, Jupiter PLC will not face any kind of financial issue. Contingency

plan are also developed for quantitative elements as in future they will cop up with problems

related with them.

TASK 4

Comparison of organizations adapting management accounting systems to resolve financial

issues

Financial issues associated with organizations are defined as monetary issues that can

create stress. Management is always careful about these financial problems (Business financing

problems, 2018). These are improper taxation strategies, insufficient collateral, inadequacy in

working capital etc. So, when Jupiter PLC adopts management accounting systems then it finds

ways to solve these above mentioned issues. Two management accounting systems are as:

KPI: Key Performance Indicators are those performance areas which are crucial for

business to achieve success. Senior management focuses on those functions and processes whose

contribution to profitability are maximum. These are of two types, financial and non-financial

indicators. This tool aids in resolving financial issues such as inefficiency in identifying less and

more profitable areas in a way that it finds key points to organizational success. This can be done

through KPI as it contributes in meeting performance objectives.

Benchmarking: To identify best practices in industry and to achieve them,

benchmarking is adopted. Performance, strategies are compared to other companies in order to

attain standards or benchmarks. Different types of benchmarking are strategic, competitive,

process, functional benchmarking (What is Benchmarking, 2018). Data or information is

gathered in this tool which is also related to financial performance. Financial problems in respect

10

hindrances that can create issue in budget planning and forecasting.

Way in which planning tools help in solving financial problems

It is better understood that financial issues occurs with every business. But the way in

which resolved through planning tools is important. Financial problems from that planning tools

have to deal are uncertain cash inflow and outflow, insufficient funding or financing for capital

needs, excessive debts, reducing profitability. Scenario tool conceptualize all financial aspects in

advance, so that in future, Jupiter PLC will not face any kind of financial issue. Contingency

plan are also developed for quantitative elements as in future they will cop up with problems

related with them.

TASK 4

Comparison of organizations adapting management accounting systems to resolve financial

issues

Financial issues associated with organizations are defined as monetary issues that can

create stress. Management is always careful about these financial problems (Business financing

problems, 2018). These are improper taxation strategies, insufficient collateral, inadequacy in

working capital etc. So, when Jupiter PLC adopts management accounting systems then it finds

ways to solve these above mentioned issues. Two management accounting systems are as:

KPI: Key Performance Indicators are those performance areas which are crucial for

business to achieve success. Senior management focuses on those functions and processes whose

contribution to profitability are maximum. These are of two types, financial and non-financial

indicators. This tool aids in resolving financial issues such as inefficiency in identifying less and

more profitable areas in a way that it finds key points to organizational success. This can be done

through KPI as it contributes in meeting performance objectives.

Benchmarking: To identify best practices in industry and to achieve them,

benchmarking is adopted. Performance, strategies are compared to other companies in order to

attain standards or benchmarks. Different types of benchmarking are strategic, competitive,

process, functional benchmarking (What is Benchmarking, 2018). Data or information is

gathered in this tool which is also related to financial performance. Financial problems in respect

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.