Management Accounting Report: Strategies for Jupiter PLC Success

VerifiedAdded on 2020/10/23

|17

|4549

|410

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their practical application, using Jupiter PLC, a medium-sized manufacturing company, as a case study. It begins with an introduction to management accounting, differentiating it from financial accounting, and outlining various management accounting systems, including cost accounting, inventory management, and job costing systems. The report then explores different reporting methods, such as budget reports, accounts receivable aging reports, and job cost reports, emphasizing their benefits for organizational performance. The core of the report focuses on preparing income statements using both absorption and marginal costing systems, providing detailed calculations and comparisons. Furthermore, it delves into the advantages and disadvantages of planning tools used in budgetary control, evaluating their role in resolving financial problems and contributing to sustainable success. The report concludes by summarizing the key findings and emphasizing the significance of management accounting in enhancing profitability and facilitating effective decision-making within organizations. The report also highlights the importance of integrating management accounting systems with organizational processes to improve overall performance.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Management accounting and different types of management accounting systems.....................1

Different methods used for management accounting reporting..................................................2

Benefits of management accounting systems..............................................................................3

TASK 2............................................................................................................................................4

Preparing income statement by undertaking both absorption and marginal costing system.......4

TASK 3............................................................................................................................................7

Explaining the advantages and disadvantages of different types of planning tools which are

used in budgetary control.............................................................................................................7

TASK 4..........................................................................................................................................10

Evaluating how planning tools help in resolving financial problems and thereby lead

sustainable success.....................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Management accounting and different types of management accounting systems.....................1

Different methods used for management accounting reporting..................................................2

Benefits of management accounting systems..............................................................................3

TASK 2............................................................................................................................................4

Preparing income statement by undertaking both absorption and marginal costing system.......4

TASK 3............................................................................................................................................7

Explaining the advantages and disadvantages of different types of planning tools which are

used in budgetary control.............................................................................................................7

TASK 4..........................................................................................................................................10

Evaluating how planning tools help in resolving financial problems and thereby lead

sustainable success.....................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting refers to presentation of accounting information in the form of

reports that will help the management in performing its day to day activities. Management

accounting helps the management in formulating policies. Jupiter PLC will be included in the

assignment to perform its various task. It is a medium sized manufacturing company. This study

will include management accounting and different types of management accounting information.

Furthermore, it will include different methods of management accounting reporting. Also, it will

provide benefits of management accounting systems and their application to Jupiter PLC.

Moreover, this study will include marginal costing and absorption costing. It will include the use

of planning tools in management accounting and use of management accounting to respond to

financial problems.

TASK 1

Management accounting and different types of management accounting systems

Management accounting is a branch of accounting in which accounting information is

provided to management in order to increase profitability of firm and reducing the losses. It

refers to accounting information to management to make proper decisions to improve various

operations of organisation.

Different types of management accounting systems: The following are the various management

accounting systems which assist in providing information to management. Cost accounting system: It is a system used by organisation to estimate the cost of its

products and services to determine the profitability and also assist in controlling the cost

of product to increase profitability. Cost accounting system include fixed cost and

variable cost which are used to identify the total cost of product. Fixed cost is a cost of

production that remains constant over the period and it does not change with the change

in volume whereas variable cost changes with the change in volume (Chenhall and

Moers, 2015). Cost accounting systems consist of Job order costing and process costing.

Job order costing is that technique in which the manufacturing cost is divided separately

for each job. Process costing refers to accumulating manufacturing cost separately for

each process. Cost accounting system is used by Jupiter PLC to determine the

profitability of the firm by estimating the cost of its products.

1

Management accounting refers to presentation of accounting information in the form of

reports that will help the management in performing its day to day activities. Management

accounting helps the management in formulating policies. Jupiter PLC will be included in the

assignment to perform its various task. It is a medium sized manufacturing company. This study

will include management accounting and different types of management accounting information.

Furthermore, it will include different methods of management accounting reporting. Also, it will

provide benefits of management accounting systems and their application to Jupiter PLC.

Moreover, this study will include marginal costing and absorption costing. It will include the use

of planning tools in management accounting and use of management accounting to respond to

financial problems.

TASK 1

Management accounting and different types of management accounting systems

Management accounting is a branch of accounting in which accounting information is

provided to management in order to increase profitability of firm and reducing the losses. It

refers to accounting information to management to make proper decisions to improve various

operations of organisation.

Different types of management accounting systems: The following are the various management

accounting systems which assist in providing information to management. Cost accounting system: It is a system used by organisation to estimate the cost of its

products and services to determine the profitability and also assist in controlling the cost

of product to increase profitability. Cost accounting system include fixed cost and

variable cost which are used to identify the total cost of product. Fixed cost is a cost of

production that remains constant over the period and it does not change with the change

in volume whereas variable cost changes with the change in volume (Chenhall and

Moers, 2015). Cost accounting systems consist of Job order costing and process costing.

Job order costing is that technique in which the manufacturing cost is divided separately

for each job. Process costing refers to accumulating manufacturing cost separately for

each process. Cost accounting system is used by Jupiter PLC to determine the

profitability of the firm by estimating the cost of its products.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system: It is system used of manage the level of inventory in the

organisation in order to utilise the resource in the proper way to reduce maintain stock

level according to the demand of customers. Inventory management system assist in

controlling the flow of inventory to reduce misappropriation of stock. Inventory

management perform functions such as creating purchase orders, sale orders, print

barcode labels etc. Inventory management system include FIFO and LIFO method for

valuation of inventory. According to FIFO method, the first inventory which is purchased

is the one to be sold first. LIFO method assume that the first inventory which is

purchased is the one to be sold at last. This system is used by Jupiter PLC to control the

stock level by utilising resources in the effective way.

Job costing system: It provides information relating to cost of specific job. It helps in

allocating the cost to particular job in the process of production of product. Job costing

system provide information relating to direct material, direct labour and overhead cost.

Direct materials are those materials which are consumed in the produces of production

and can be identified with the product (Dekker, 2016). Direct materials are listed in the

bills of materials. Direct labour involves the manpower used in manufacturing that

product. Overhead cost are the operating expenses which are incurred by organisation in

manufacturing that product. This system is used by Jupiter PLC to allocate the cost of

product to each job it helps Jupiter PLC in controlling the cost at each stage.

Different methods used for management accounting reporting

There are different types of management accounting reports which are used by

organization to determine the profitability and to make decisions to improve the performance of

organization. Budget report: This report is prepared by management in order to identify various

deviation in performance by setting the standards of incomes and expenses and then

comparing the actual incomes and expenses with budgeted to take necessary action to

improve the performance to organization (Fullerton, Kennedy and Widener, 2013).

Budget report contains information about actual and estimated figures and on the basis of

this report, management can take decisions to improve the performance of organization. Accounts receivable aging report : This report is prepared to have understanding of

amount due from the customers to determine credibility of organization. This report assist

2

organisation in order to utilise the resource in the proper way to reduce maintain stock

level according to the demand of customers. Inventory management system assist in

controlling the flow of inventory to reduce misappropriation of stock. Inventory

management perform functions such as creating purchase orders, sale orders, print

barcode labels etc. Inventory management system include FIFO and LIFO method for

valuation of inventory. According to FIFO method, the first inventory which is purchased

is the one to be sold first. LIFO method assume that the first inventory which is

purchased is the one to be sold at last. This system is used by Jupiter PLC to control the

stock level by utilising resources in the effective way.

Job costing system: It provides information relating to cost of specific job. It helps in

allocating the cost to particular job in the process of production of product. Job costing

system provide information relating to direct material, direct labour and overhead cost.

Direct materials are those materials which are consumed in the produces of production

and can be identified with the product (Dekker, 2016). Direct materials are listed in the

bills of materials. Direct labour involves the manpower used in manufacturing that

product. Overhead cost are the operating expenses which are incurred by organisation in

manufacturing that product. This system is used by Jupiter PLC to allocate the cost of

product to each job it helps Jupiter PLC in controlling the cost at each stage.

Different methods used for management accounting reporting

There are different types of management accounting reports which are used by

organization to determine the profitability and to make decisions to improve the performance of

organization. Budget report: This report is prepared by management in order to identify various

deviation in performance by setting the standards of incomes and expenses and then

comparing the actual incomes and expenses with budgeted to take necessary action to

improve the performance to organization (Fullerton, Kennedy and Widener, 2013).

Budget report contains information about actual and estimated figures and on the basis of

this report, management can take decisions to improve the performance of organization. Accounts receivable aging report : This report is prepared to have understanding of

amount due from the customers to determine credibility of organization. This report assist

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in identifying about those customers which have not paid the amount due to organization.

It also assists management in identifying the bad debts. It also provides management

taking in various decisions about changes in credit policy of the firm.

Job cost reports : This reports are prepared by management which shows the cost of

each job in order to compare them with the estimates of revenue to determine the

profitability of firm (Messner, 2016). Job costing report helps in controlling the cost of

each job by identifying the expenses and make decisions to control the cost by reducing

the expenses due to which of cost of production increases.

These reports are used by Jupiter PLC to measure the profitability of the firm. Budget

report helps Jupiter PLC in measuring the performance by comparing the actual with the

standards. Account receivable report helps Jupiter PLC in identifying the customers that have no

paid the amount outstanding to their account. Also, job costing report is prepared by Jupiter

_PLC to accumulate cost of each job to control the cost of the each job.

Benefits of management accounting systems

Management accounting systems helps the organization in increasing its profitability by

identifying various information which provide assistance to firm in improving their performance

on the basis of these reports.

Benefits of cost accounting system

This system helps in measuring and improving efficiency of the organization which assist

in increasing profitability of firm.

It helps in utilizing the resources of organization effectively and efficiently to achieve the

goals of firm and also assist in controlling the cost by reducing expenses (Otley and

Emmanuel, 2013). It also helps in making effective decision for increasing the profitability of organization.

Limitations of cost accounting system

Cost is ascertained on the basis of full utilization of capacity and if cost is partly utilized

the cost determined may not be true.

Financial figures are not included for calculation cost due to which the cost determine is

not correct always. Cost accounting systems require high expenditure.

Benefits of inventory management system

3

It also assists management in identifying the bad debts. It also provides management

taking in various decisions about changes in credit policy of the firm.

Job cost reports : This reports are prepared by management which shows the cost of

each job in order to compare them with the estimates of revenue to determine the

profitability of firm (Messner, 2016). Job costing report helps in controlling the cost of

each job by identifying the expenses and make decisions to control the cost by reducing

the expenses due to which of cost of production increases.

These reports are used by Jupiter PLC to measure the profitability of the firm. Budget

report helps Jupiter PLC in measuring the performance by comparing the actual with the

standards. Account receivable report helps Jupiter PLC in identifying the customers that have no

paid the amount outstanding to their account. Also, job costing report is prepared by Jupiter

_PLC to accumulate cost of each job to control the cost of the each job.

Benefits of management accounting systems

Management accounting systems helps the organization in increasing its profitability by

identifying various information which provide assistance to firm in improving their performance

on the basis of these reports.

Benefits of cost accounting system

This system helps in measuring and improving efficiency of the organization which assist

in increasing profitability of firm.

It helps in utilizing the resources of organization effectively and efficiently to achieve the

goals of firm and also assist in controlling the cost by reducing expenses (Otley and

Emmanuel, 2013). It also helps in making effective decision for increasing the profitability of organization.

Limitations of cost accounting system

Cost is ascertained on the basis of full utilization of capacity and if cost is partly utilized

the cost determined may not be true.

Financial figures are not included for calculation cost due to which the cost determine is

not correct always. Cost accounting systems require high expenditure.

Benefits of inventory management system

3

It helps in controlling over utilization of resources and maintaining the stock level

according to the requirements. This will assist Jupiter PLC in maintaining the stock level

according the demands of customers.

This system helps in increasing profitability of Jupiter PLC By reducing the expenses of

maintaining stock (Ramanathan, 2014). This system also helps in tracking the inventory level and assist in reducing

misappropriation of stock.

Limitations of inventory management system

Organization have to incur high expenditure for implementing this system in the firm.

This system in difficult to understand due to which organization may face problem in

using this system.

Inventory management system will require more information regarding future demand to

maintain the stock level.

Management accounting system and reporting integration with organisational process

Management accounting system and reporting are integrated with the organization

process as helps in determining the information of the various activities of the Jupiter PLC which

will assist in increasing the profitability of firm.

Integrated management accounting system and reporting helps in maintaining the stock

level according to demands of customers. It also helps in improving the various activities of the

Jupiter PLC.

Management accounting reporting helps in identifying the customer's information that

have their amount unpaid for the products and services provided by firm . This helps the Jupiter

Plc in modifying its credit policies.

TASK 2

Preparing income statement by undertaking both absorption and marginal costing system

Absorption costing: In the modern era, such method of costing is highly significant which

provides assistance in calculating the cost of product by taking into account both direct as well as

indirect expenses. On the basis of such costing method all the manufacturing costs are absorbed

by the units produced. As per this method, fixed and variable costs are apportioned to cost

centres where absorption rates are considered for the purpose of evaluation.

4

according to the requirements. This will assist Jupiter PLC in maintaining the stock level

according the demands of customers.

This system helps in increasing profitability of Jupiter PLC By reducing the expenses of

maintaining stock (Ramanathan, 2014). This system also helps in tracking the inventory level and assist in reducing

misappropriation of stock.

Limitations of inventory management system

Organization have to incur high expenditure for implementing this system in the firm.

This system in difficult to understand due to which organization may face problem in

using this system.

Inventory management system will require more information regarding future demand to

maintain the stock level.

Management accounting system and reporting integration with organisational process

Management accounting system and reporting are integrated with the organization

process as helps in determining the information of the various activities of the Jupiter PLC which

will assist in increasing the profitability of firm.

Integrated management accounting system and reporting helps in maintaining the stock

level according to demands of customers. It also helps in improving the various activities of the

Jupiter PLC.

Management accounting reporting helps in identifying the customer's information that

have their amount unpaid for the products and services provided by firm . This helps the Jupiter

Plc in modifying its credit policies.

TASK 2

Preparing income statement by undertaking both absorption and marginal costing system

Absorption costing: In the modern era, such method of costing is highly significant which

provides assistance in calculating the cost of product by taking into account both direct as well as

indirect expenses. On the basis of such costing method all the manufacturing costs are absorbed

by the units produced. As per this method, fixed and variable costs are apportioned to cost

centres where absorption rates are considered for the purpose of evaluation.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

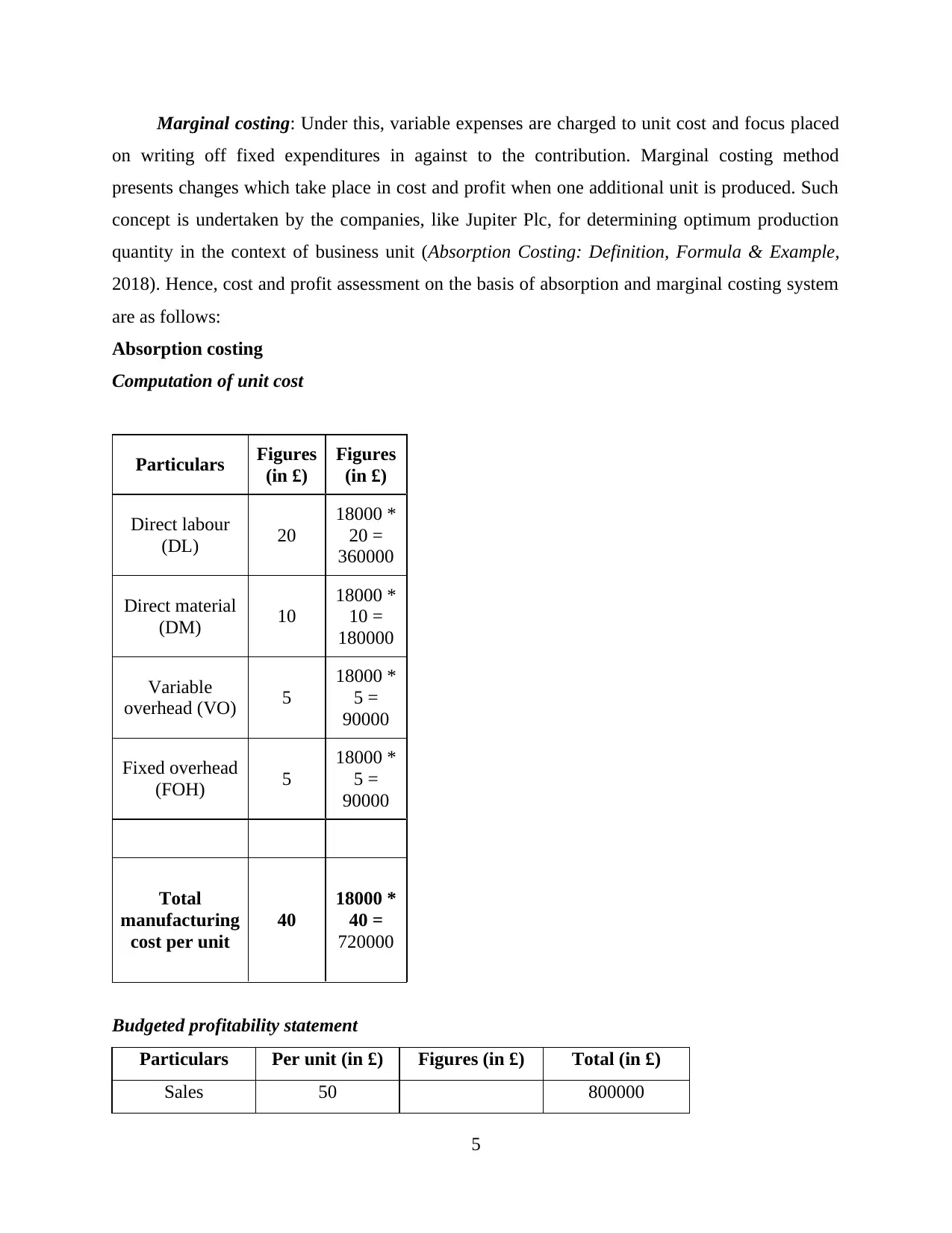

Marginal costing: Under this, variable expenses are charged to unit cost and focus placed

on writing off fixed expenditures in against to the contribution. Marginal costing method

presents changes which take place in cost and profit when one additional unit is produced. Such

concept is undertaken by the companies, like Jupiter Plc, for determining optimum production

quantity in the context of business unit (Absorption Costing: Definition, Formula & Example,

2018). Hence, cost and profit assessment on the basis of absorption and marginal costing system

are as follows:

Absorption costing

Computation of unit cost

Particulars Figures

(in £)

Figures

(in £)

Direct labour

(DL) 20

18000 *

20 =

360000

Direct material

(DM) 10

18000 *

10 =

180000

Variable

overhead (VO) 5

18000 *

5 =

90000

Fixed overhead

(FOH) 5

18000 *

5 =

90000

Total

manufacturing

cost per unit

40

18000 *

40 =

720000

Budgeted profitability statement

Particulars Per unit (in £) Figures (in £) Total (in £)

Sales 50 800000

5

on writing off fixed expenditures in against to the contribution. Marginal costing method

presents changes which take place in cost and profit when one additional unit is produced. Such

concept is undertaken by the companies, like Jupiter Plc, for determining optimum production

quantity in the context of business unit (Absorption Costing: Definition, Formula & Example,

2018). Hence, cost and profit assessment on the basis of absorption and marginal costing system

are as follows:

Absorption costing

Computation of unit cost

Particulars Figures

(in £)

Figures

(in £)

Direct labour

(DL) 20

18000 *

20 =

360000

Direct material

(DM) 10

18000 *

10 =

180000

Variable

overhead (VO) 5

18000 *

5 =

90000

Fixed overhead

(FOH) 5

18000 *

5 =

90000

Total

manufacturing

cost per unit

40

18000 *

40 =

720000

Budgeted profitability statement

Particulars Per unit (in £) Figures (in £) Total (in £)

Sales 50 800000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of

production

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

720000

Beginning

inventory

0

Less: Ending

stock

80000

Less: Cost of

goods

sold(COGS)

640000

Gross Budgeted

profit

160000

Less: Under

absorption

10000

Net standard

profit

150000

Actual P&L

Particulars Per unit (in £) Figures (in £) Total (in £)

Revenue 50 800000

Production cost

Material 10 190000

Labour expenses 20 380000

Variable

overhead

5 95000

6

production

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

720000

Beginning

inventory

0

Less: Ending

stock

80000

Less: Cost of

goods

sold(COGS)

640000

Gross Budgeted

profit

160000

Less: Under

absorption

10000

Net standard

profit

150000

Actual P&L

Particulars Per unit (in £) Figures (in £) Total (in £)

Revenue 50 800000

Production cost

Material 10 190000

Labour expenses 20 380000

Variable

overhead

5 95000

6

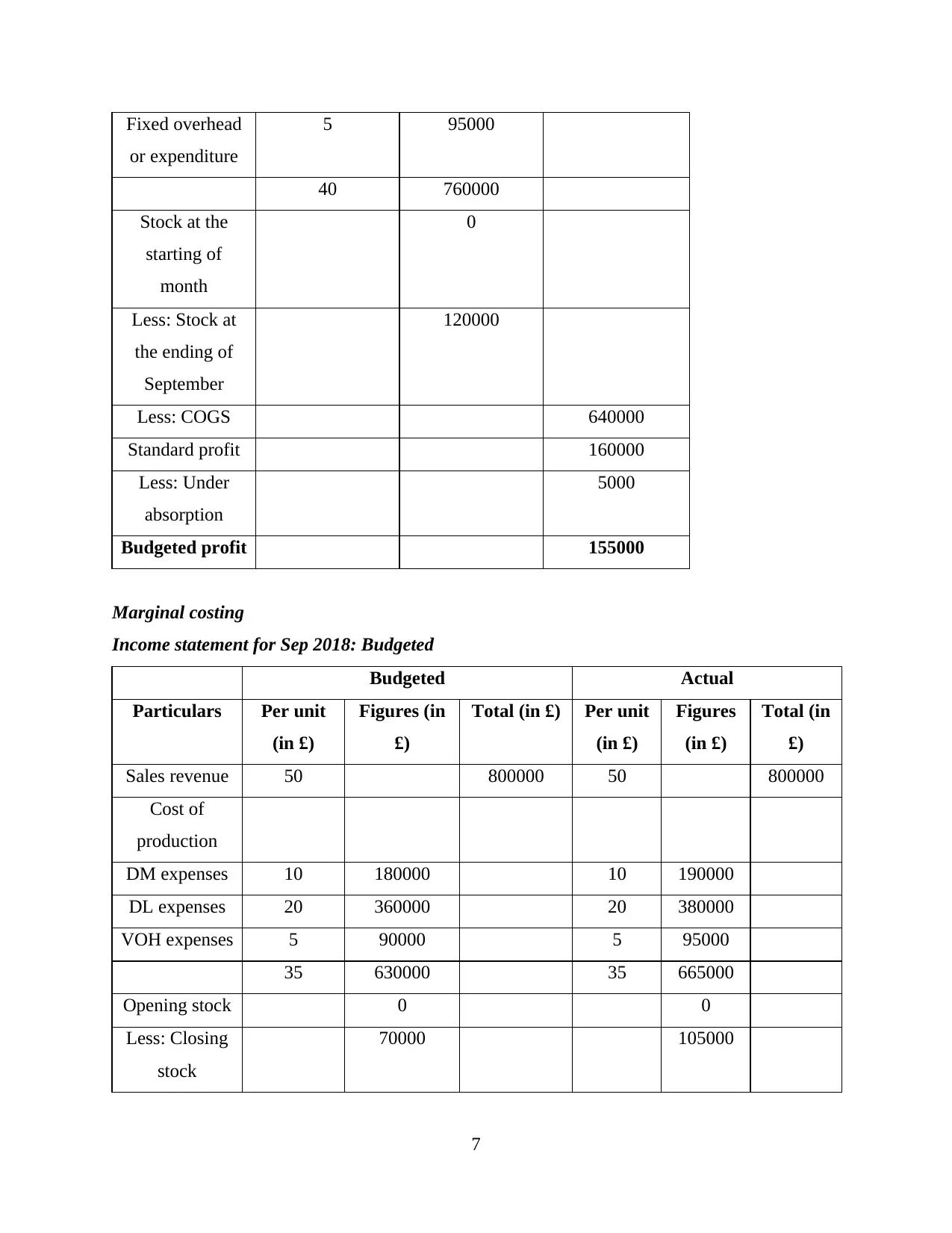

Fixed overhead

or expenditure

5 95000

40 760000

Stock at the

starting of

month

0

Less: Stock at

the ending of

September

120000

Less: COGS 640000

Standard profit 160000

Less: Under

absorption

5000

Budgeted profit 155000

Marginal costing

Income statement for Sep 2018: Budgeted

Budgeted Actual

Particulars Per unit

(in £)

Figures (in

£)

Total (in £) Per unit

(in £)

Figures

(in £)

Total (in

£)

Sales revenue 50 800000 50 800000

Cost of

production

DM expenses 10 180000 10 190000

DL expenses 20 360000 20 380000

VOH expenses 5 90000 5 95000

35 630000 35 665000

Opening stock 0 0

Less: Closing

stock

70000 105000

7

or expenditure

5 95000

40 760000

Stock at the

starting of

month

0

Less: Stock at

the ending of

September

120000

Less: COGS 640000

Standard profit 160000

Less: Under

absorption

5000

Budgeted profit 155000

Marginal costing

Income statement for Sep 2018: Budgeted

Budgeted Actual

Particulars Per unit

(in £)

Figures (in

£)

Total (in £) Per unit

(in £)

Figures

(in £)

Total (in

£)

Sales revenue 50 800000 50 800000

Cost of

production

DM expenses 10 180000 10 190000

DL expenses 20 360000 20 380000

VOH expenses 5 90000 5 95000

35 630000 35 665000

Opening stock 0 0

Less: Closing

stock

70000 105000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

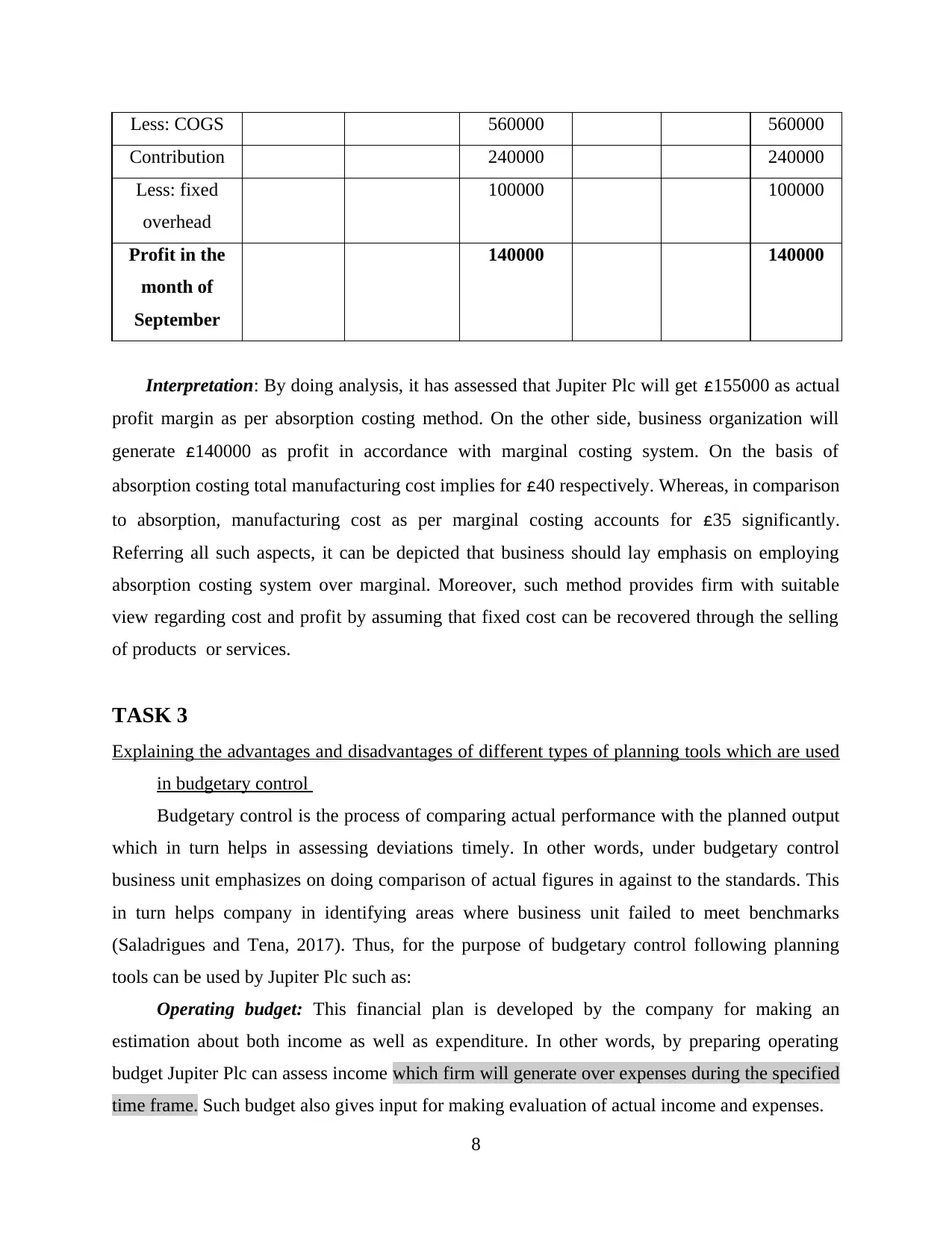

Less: COGS 560000 560000

Contribution 240000 240000

Less: fixed

overhead

100000 100000

Profit in the

month of

September

140000 140000

Interpretation: By doing analysis, it has assessed that Jupiter Plc will get £155000 as actual

profit margin as per absorption costing method. On the other side, business organization will

generate £140000 as profit in accordance with marginal costing system. On the basis of

absorption costing total manufacturing cost implies for £40 respectively. Whereas, in comparison

to absorption, manufacturing cost as per marginal costing accounts for £35 significantly.

Referring all such aspects, it can be depicted that business should lay emphasis on employing

absorption costing system over marginal. Moreover, such method provides firm with suitable

view regarding cost and profit by assuming that fixed cost can be recovered through the selling

of products or services.

TASK 3

Explaining the advantages and disadvantages of different types of planning tools which are used

in budgetary control

Budgetary control is the process of comparing actual performance with the planned output

which in turn helps in assessing deviations timely. In other words, under budgetary control

business unit emphasizes on doing comparison of actual figures in against to the standards. This

in turn helps company in identifying areas where business unit failed to meet benchmarks

(Saladrigues and Tena, 2017). Thus, for the purpose of budgetary control following planning

tools can be used by Jupiter Plc such as:

Operating budget: This financial plan is developed by the company for making an

estimation about both income as well as expenditure. In other words, by preparing operating

budget Jupiter Plc can assess income which firm will generate over expenses during the specified

time frame. Such budget also gives input for making evaluation of actual income and expenses.

8

Contribution 240000 240000

Less: fixed

overhead

100000 100000

Profit in the

month of

September

140000 140000

Interpretation: By doing analysis, it has assessed that Jupiter Plc will get £155000 as actual

profit margin as per absorption costing method. On the other side, business organization will

generate £140000 as profit in accordance with marginal costing system. On the basis of

absorption costing total manufacturing cost implies for £40 respectively. Whereas, in comparison

to absorption, manufacturing cost as per marginal costing accounts for £35 significantly.

Referring all such aspects, it can be depicted that business should lay emphasis on employing

absorption costing system over marginal. Moreover, such method provides firm with suitable

view regarding cost and profit by assuming that fixed cost can be recovered through the selling

of products or services.

TASK 3

Explaining the advantages and disadvantages of different types of planning tools which are used

in budgetary control

Budgetary control is the process of comparing actual performance with the planned output

which in turn helps in assessing deviations timely. In other words, under budgetary control

business unit emphasizes on doing comparison of actual figures in against to the standards. This

in turn helps company in identifying areas where business unit failed to meet benchmarks

(Saladrigues and Tena, 2017). Thus, for the purpose of budgetary control following planning

tools can be used by Jupiter Plc such as:

Operating budget: This financial plan is developed by the company for making an

estimation about both income as well as expenditure. In other words, by preparing operating

budget Jupiter Plc can assess income which firm will generate over expenses during the specified

time frame. Such budget also gives input for making evaluation of actual income and expenses.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

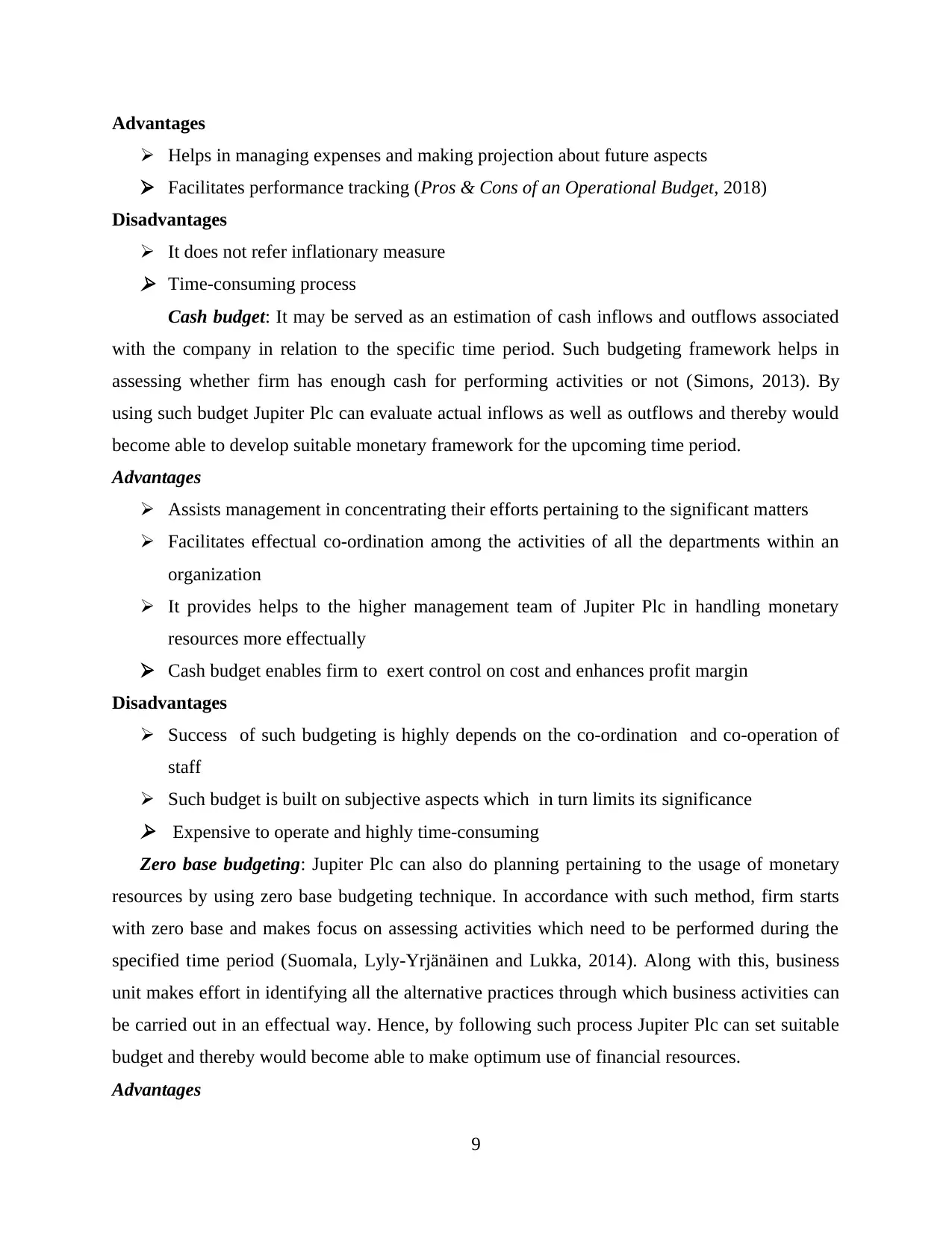

Advantages

Helps in managing expenses and making projection about future aspects

Facilitates performance tracking (Pros & Cons of an Operational Budget, 2018)

Disadvantages

It does not refer inflationary measure Time-consuming process

Cash budget: It may be served as an estimation of cash inflows and outflows associated

with the company in relation to the specific time period. Such budgeting framework helps in

assessing whether firm has enough cash for performing activities or not (Simons, 2013). By

using such budget Jupiter Plc can evaluate actual inflows as well as outflows and thereby would

become able to develop suitable monetary framework for the upcoming time period.

Advantages

Assists management in concentrating their efforts pertaining to the significant matters

Facilitates effectual co-ordination among the activities of all the departments within an

organization

It provides helps to the higher management team of Jupiter Plc in handling monetary

resources more effectually

Cash budget enables firm to exert control on cost and enhances profit margin

Disadvantages

Success of such budgeting is highly depends on the co-ordination and co-operation of

staff

Such budget is built on subjective aspects which in turn limits its significance Expensive to operate and highly time-consuming

Zero base budgeting: Jupiter Plc can also do planning pertaining to the usage of monetary

resources by using zero base budgeting technique. In accordance with such method, firm starts

with zero base and makes focus on assessing activities which need to be performed during the

specified time period (Suomala, Lyly-Yrjänäinen and Lukka, 2014). Along with this, business

unit makes effort in identifying all the alternative practices through which business activities can

be carried out in an effectual way. Hence, by following such process Jupiter Plc can set suitable

budget and thereby would become able to make optimum use of financial resources.

Advantages

9

Helps in managing expenses and making projection about future aspects

Facilitates performance tracking (Pros & Cons of an Operational Budget, 2018)

Disadvantages

It does not refer inflationary measure Time-consuming process

Cash budget: It may be served as an estimation of cash inflows and outflows associated

with the company in relation to the specific time period. Such budgeting framework helps in

assessing whether firm has enough cash for performing activities or not (Simons, 2013). By

using such budget Jupiter Plc can evaluate actual inflows as well as outflows and thereby would

become able to develop suitable monetary framework for the upcoming time period.

Advantages

Assists management in concentrating their efforts pertaining to the significant matters

Facilitates effectual co-ordination among the activities of all the departments within an

organization

It provides helps to the higher management team of Jupiter Plc in handling monetary

resources more effectually

Cash budget enables firm to exert control on cost and enhances profit margin

Disadvantages

Success of such budgeting is highly depends on the co-ordination and co-operation of

staff

Such budget is built on subjective aspects which in turn limits its significance Expensive to operate and highly time-consuming

Zero base budgeting: Jupiter Plc can also do planning pertaining to the usage of monetary

resources by using zero base budgeting technique. In accordance with such method, firm starts

with zero base and makes focus on assessing activities which need to be performed during the

specified time period (Suomala, Lyly-Yrjänäinen and Lukka, 2014). Along with this, business

unit makes effort in identifying all the alternative practices through which business activities can

be carried out in an effectual way. Hence, by following such process Jupiter Plc can set suitable

budget and thereby would become able to make optimum use of financial resources.

Advantages

9

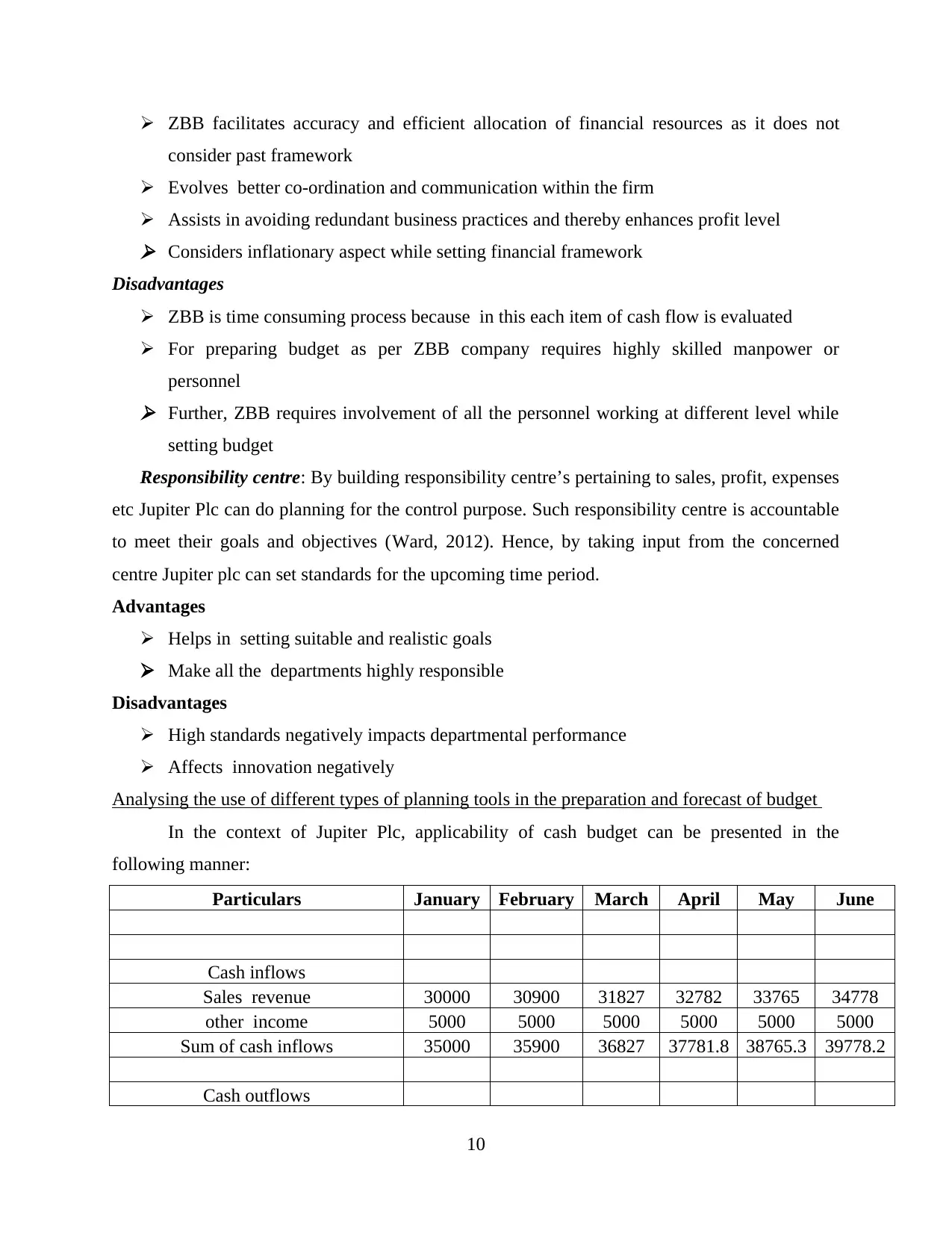

ZBB facilitates accuracy and efficient allocation of financial resources as it does not

consider past framework

Evolves better co-ordination and communication within the firm

Assists in avoiding redundant business practices and thereby enhances profit level Considers inflationary aspect while setting financial framework

Disadvantages

ZBB is time consuming process because in this each item of cash flow is evaluated

For preparing budget as per ZBB company requires highly skilled manpower or

personnel Further, ZBB requires involvement of all the personnel working at different level while

setting budget

Responsibility centre: By building responsibility centre’s pertaining to sales, profit, expenses

etc Jupiter Plc can do planning for the control purpose. Such responsibility centre is accountable

to meet their goals and objectives (Ward, 2012). Hence, by taking input from the concerned

centre Jupiter plc can set standards for the upcoming time period.

Advantages

Helps in setting suitable and realistic goals

Make all the departments highly responsible

Disadvantages

High standards negatively impacts departmental performance

Affects innovation negatively

Analysing the use of different types of planning tools in the preparation and forecast of budget

In the context of Jupiter Plc, applicability of cash budget can be presented in the

following manner:

Particulars January February March April May June

Cash inflows

Sales revenue 30000 30900 31827 32782 33765 34778

other income 5000 5000 5000 5000 5000 5000

Sum of cash inflows 35000 35900 36827 37781.8 38765.3 39778.2

Cash outflows

10

consider past framework

Evolves better co-ordination and communication within the firm

Assists in avoiding redundant business practices and thereby enhances profit level Considers inflationary aspect while setting financial framework

Disadvantages

ZBB is time consuming process because in this each item of cash flow is evaluated

For preparing budget as per ZBB company requires highly skilled manpower or

personnel Further, ZBB requires involvement of all the personnel working at different level while

setting budget

Responsibility centre: By building responsibility centre’s pertaining to sales, profit, expenses

etc Jupiter Plc can do planning for the control purpose. Such responsibility centre is accountable

to meet their goals and objectives (Ward, 2012). Hence, by taking input from the concerned

centre Jupiter plc can set standards for the upcoming time period.

Advantages

Helps in setting suitable and realistic goals

Make all the departments highly responsible

Disadvantages

High standards negatively impacts departmental performance

Affects innovation negatively

Analysing the use of different types of planning tools in the preparation and forecast of budget

In the context of Jupiter Plc, applicability of cash budget can be presented in the

following manner:

Particulars January February March April May June

Cash inflows

Sales revenue 30000 30900 31827 32782 33765 34778

other income 5000 5000 5000 5000 5000 5000

Sum of cash inflows 35000 35900 36827 37781.8 38765.3 39778.2

Cash outflows

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.