Comprehensive Management Accounting Report for KBC Ltd (Case Study)

VerifiedAdded on 2019/12/04

|26

|6654

|439

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to a case study of KBC Ltd. It begins with an introduction to management accounting and the significance of budgeting, outlining administrative procedures and the stages of the budgeting process. The report then delves into cost classification, including direct, indirect, fixed, variable, and semi-variable costs, alongside an explanation of the high-low method for calculating fixed and variable costs. Furthermore, the report examines the effects of absorption and marginal costing on stock valuation and profit determination, differentiating between job, batch, process, and service costing. The report includes profit and loss statements prepared under both absorption and marginal costing methods for different regions of KBC Ltd. It also offers recommendations related to product combinations with limited labor hours, and calculating profits under varying scenarios. The report concludes with an analysis of different budgeting methods, including cash budgets, and variance analysis, along with calculations of units sold, sales value, and profit determination at different sales levels. It also includes recommendations for improving performance of Bata Ltd.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

A Purpose of using budgeting......................................................................................................4

B Administrative budgeting procedure........................................................................................4

C Describing the stages of budgeting process.............................................................................5

TASK 2............................................................................................................................................5

A Classifying cost........................................................................................................................5

B Calculating the fixed and variable cost using high low method..............................................6

TASK 3............................................................................................................................................6

A Absorption and marginal costing effect on stock valuation and profit determination.............6

B Difference between job costing, batch costing, process costing and service costing..............7

C Preparing profit and loss statement for North and South area under absorption costing.........7

D Prepare profit and loss statement for South region on the basis of marginal costing..............9

TASK 4............................................................................................................................................9

A Advise the KBC.......................................................................................................................9

B Calculating following figures.................................................................................................10

(i) Contribution to sales ratio (PVR)..........................................................................................10

C Combination of products with limited labour hours..............................................................11

D Calculating of profits at 6000 further hours...........................................................................11

TASK 5..........................................................................................................................................11

A Different types of budgeting method.....................................................................................11

B Cash budget............................................................................................................................12

TASK 6..........................................................................................................................................13

Budget and calculation of variance............................................................................................13

TASK 7..........................................................................................................................................15

(A) Calculating units sold and sales value.................................................................................15

B Computing profit or loss at the sale of 26500 pair of shoes...................................................15

C Computation number of units to earn desired profit worth £240100....................................16

D Computing total number of units at increased selling price by 15% & advertisement cost of

£20000........................................................................................................................................16

E Recommending and justifying appropriate action for improving performance of Bata Ltd..16

2

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

A Purpose of using budgeting......................................................................................................4

B Administrative budgeting procedure........................................................................................4

C Describing the stages of budgeting process.............................................................................5

TASK 2............................................................................................................................................5

A Classifying cost........................................................................................................................5

B Calculating the fixed and variable cost using high low method..............................................6

TASK 3............................................................................................................................................6

A Absorption and marginal costing effect on stock valuation and profit determination.............6

B Difference between job costing, batch costing, process costing and service costing..............7

C Preparing profit and loss statement for North and South area under absorption costing.........7

D Prepare profit and loss statement for South region on the basis of marginal costing..............9

TASK 4............................................................................................................................................9

A Advise the KBC.......................................................................................................................9

B Calculating following figures.................................................................................................10

(i) Contribution to sales ratio (PVR)..........................................................................................10

C Combination of products with limited labour hours..............................................................11

D Calculating of profits at 6000 further hours...........................................................................11

TASK 5..........................................................................................................................................11

A Different types of budgeting method.....................................................................................11

B Cash budget............................................................................................................................12

TASK 6..........................................................................................................................................13

Budget and calculation of variance............................................................................................13

TASK 7..........................................................................................................................................15

(A) Calculating units sold and sales value.................................................................................15

B Computing profit or loss at the sale of 26500 pair of shoes...................................................15

C Computation number of units to earn desired profit worth £240100....................................16

D Computing total number of units at increased selling price by 15% & advertisement cost of

£20000........................................................................................................................................16

E Recommending and justifying appropriate action for improving performance of Bata Ltd..16

2

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

3

REFERENCES..............................................................................................................................18

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INDEX OF TABLES

Table 1: Table 1: Profit for North Area...........................................................................................9

ILLUSTRATION INDEX

Illustration 1: P & L for south area................................................................................................10

Illustration 2: P & L for south Region...........................................................................................10

4

Table 1: Table 1: Profit for North Area...........................................................................................9

ILLUSTRATION INDEX

Illustration 1: P & L for south area................................................................................................10

Illustration 2: P & L for south Region...........................................................................................10

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting is the procedure of preparing management report and accounts

through which decision related to daily business activities are taken effectively. BY using

concepts of management accounting reports are generated on monthly or weekly basis in order to

show balance related to cash, sales turnover and outstanding debts. Present report is based on

case study of KBC Ltd which handle its work related to management accounting by utilizing

number of techniques. Furthermore, purpose of budgeting and control mechanism are also

explained effectively. In addition to this, effect of absorption and marginal costing has been

discussed along with proper demonstration.

TASK 1

A Purpose of using budgeting

Budgeting

Budgeting is defined as a tool used for estimating the revenue and expenditure, for the

pre-set time period. It is a quantitative plan used for deciding which activities and associated

expenditure. KBC Company designs budget to make optimum use of financial resource and to

find the way to overcome or control expenses. The main purpose is to have control over

expenses and avail financial resources on important activities of business.

Benefits of budgeting

Budgeting is very important for business as is provide certainty for future business

activities. It assists corporation in reducing cost of production and increasing overall rate of

return. The use of budget enable business to maintain effective balance between potential

expenditure and income in KBC ltd. Similarly, budgeting benefits management of KBC Ltd to

get information related to potential threats so that accordingly appropriate action can be taken for

smooth operation of business (Davies and Crawford, 2011). Another benefit of budget for KBC

Company is that resources allocation is also done with the help of budgeting process. It helps in

analyzing cost and expenses is done in the light of expected return or growth of company.

Budgeting facilitates KBC Ltd to access cost effective sources of finance in order to reduce cost

5

Management accounting is the procedure of preparing management report and accounts

through which decision related to daily business activities are taken effectively. BY using

concepts of management accounting reports are generated on monthly or weekly basis in order to

show balance related to cash, sales turnover and outstanding debts. Present report is based on

case study of KBC Ltd which handle its work related to management accounting by utilizing

number of techniques. Furthermore, purpose of budgeting and control mechanism are also

explained effectively. In addition to this, effect of absorption and marginal costing has been

discussed along with proper demonstration.

TASK 1

A Purpose of using budgeting

Budgeting

Budgeting is defined as a tool used for estimating the revenue and expenditure, for the

pre-set time period. It is a quantitative plan used for deciding which activities and associated

expenditure. KBC Company designs budget to make optimum use of financial resource and to

find the way to overcome or control expenses. The main purpose is to have control over

expenses and avail financial resources on important activities of business.

Benefits of budgeting

Budgeting is very important for business as is provide certainty for future business

activities. It assists corporation in reducing cost of production and increasing overall rate of

return. The use of budget enable business to maintain effective balance between potential

expenditure and income in KBC ltd. Similarly, budgeting benefits management of KBC Ltd to

get information related to potential threats so that accordingly appropriate action can be taken for

smooth operation of business (Davies and Crawford, 2011). Another benefit of budget for KBC

Company is that resources allocation is also done with the help of budgeting process. It helps in

analyzing cost and expenses is done in the light of expected return or growth of company.

Budgeting facilitates KBC Ltd to access cost effective sources of finance in order to reduce cost

5

of production and ensure expansion of business in the marketplace. As a benefit, effective

management of capital structure is ensured by using budgeting practices.

B Administrative budgeting procedure

The following points represents the administrative budgeting procedure:

Setting objectives of budgeting in a line with corporation budget: The administrative

budgeting process start with setting objectives of corporation for preparing budgets. In this

process m the KBC Ltd might set objectives related to enhancement of profitability and

increasing sales turnover and increased customer base (Gibbons and et.al. 2010).

Review the plan with different departments: The plan of budget is to be discussed with

different department so as to assess the funding needs for each department. This is the process in

which business has to define functions of finance. The budget is to be set in accordance with

objectives of each department which are set in order to ensure growth and success of KBC Ltd.

Make a budget: The last stage is of preparing budget for the business by monitoring

strategies so as to reduce gap between actual and expected outcome. The continuous monitoring

tend is to be ensured for growth and success of company for long run (Kaplan and Atkinson,

2015).

C Describing the stages of budgeting process

The budgeting process of KBC Ltd has been stated as follows- Draft- The primary stage of budgeting is to draft the budget. In this stage, objectives of

budgets are to be designed in accordance with the requirements of business. Budgeting is

done by managers by drafting the budgets such as sales budget, cash budget and

production budget (Chua, Lowe and Puxty, 2015).

Approve- The prepared budget is to be approved by the management of company for this,

it has to set standard related to expenses. The expected amount of profitability can be

debated by the managers. Execute- After their approval, the process starts with implementation of budget and start

expending. The activities discussed with budgets and monetary aspects of budget will be

applied.

6

management of capital structure is ensured by using budgeting practices.

B Administrative budgeting procedure

The following points represents the administrative budgeting procedure:

Setting objectives of budgeting in a line with corporation budget: The administrative

budgeting process start with setting objectives of corporation for preparing budgets. In this

process m the KBC Ltd might set objectives related to enhancement of profitability and

increasing sales turnover and increased customer base (Gibbons and et.al. 2010).

Review the plan with different departments: The plan of budget is to be discussed with

different department so as to assess the funding needs for each department. This is the process in

which business has to define functions of finance. The budget is to be set in accordance with

objectives of each department which are set in order to ensure growth and success of KBC Ltd.

Make a budget: The last stage is of preparing budget for the business by monitoring

strategies so as to reduce gap between actual and expected outcome. The continuous monitoring

tend is to be ensured for growth and success of company for long run (Kaplan and Atkinson,

2015).

C Describing the stages of budgeting process

The budgeting process of KBC Ltd has been stated as follows- Draft- The primary stage of budgeting is to draft the budget. In this stage, objectives of

budgets are to be designed in accordance with the requirements of business. Budgeting is

done by managers by drafting the budgets such as sales budget, cash budget and

production budget (Chua, Lowe and Puxty, 2015).

Approve- The prepared budget is to be approved by the management of company for this,

it has to set standard related to expenses. The expected amount of profitability can be

debated by the managers. Execute- After their approval, the process starts with implementation of budget and start

expending. The activities discussed with budgets and monetary aspects of budget will be

applied.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Review- After setting or creating budget monitoring or reviewing process is started so

that expected outcome is achieved. This is the last step under which modification are

done in accordance with variation of expected and actual outcome.

TASK 2

A Classifying cost

The cost classification has been done as follows- Nature-It classifies cost into two parts such as direct and indirect. Here, direct cost is

incurred on production activities which consists of wages, material and other related cost.

On the other part, stationary, depreciation and salaries of administrative department will

also be included (Zimmerman and Yahya-Zadeh, 2011). Behavior-According to behavior there are different types of cost such as fixed, variable

and semi-variable as well as stepped fixed cost. The first one remain constant throughout

production process whereas variable cost varies in accordance with volume of production

(Mistry and et. al., 2014). Furthermore, semi-variable cost includes electricity and

telephone bill whee some portion remain constant and after that expenses are based on

consumption. In addition to this, stepped fixed cost is like fixed cost of production which

does not decrease or increase with production. However, due to shifting of production

activities cause high cost of production.

Function-Under this, different activities such as production, marketing and

administration. Here, production cost includes expenses of rent, unproductive wages and

depreciation as well as lighting (Caliskan, 2014). On the other hand, marketing cost

consists of expenses such as advertisement, free sample. These cost are indirectly related

to production. Apart from this, administrative cost consists stationary, postage and office

rent etc.

7

that expected outcome is achieved. This is the last step under which modification are

done in accordance with variation of expected and actual outcome.

TASK 2

A Classifying cost

The cost classification has been done as follows- Nature-It classifies cost into two parts such as direct and indirect. Here, direct cost is

incurred on production activities which consists of wages, material and other related cost.

On the other part, stationary, depreciation and salaries of administrative department will

also be included (Zimmerman and Yahya-Zadeh, 2011). Behavior-According to behavior there are different types of cost such as fixed, variable

and semi-variable as well as stepped fixed cost. The first one remain constant throughout

production process whereas variable cost varies in accordance with volume of production

(Mistry and et. al., 2014). Furthermore, semi-variable cost includes electricity and

telephone bill whee some portion remain constant and after that expenses are based on

consumption. In addition to this, stepped fixed cost is like fixed cost of production which

does not decrease or increase with production. However, due to shifting of production

activities cause high cost of production.

Function-Under this, different activities such as production, marketing and

administration. Here, production cost includes expenses of rent, unproductive wages and

depreciation as well as lighting (Caliskan, 2014). On the other hand, marketing cost

consists of expenses such as advertisement, free sample. These cost are indirectly related

to production. Apart from this, administrative cost consists stationary, postage and office

rent etc.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

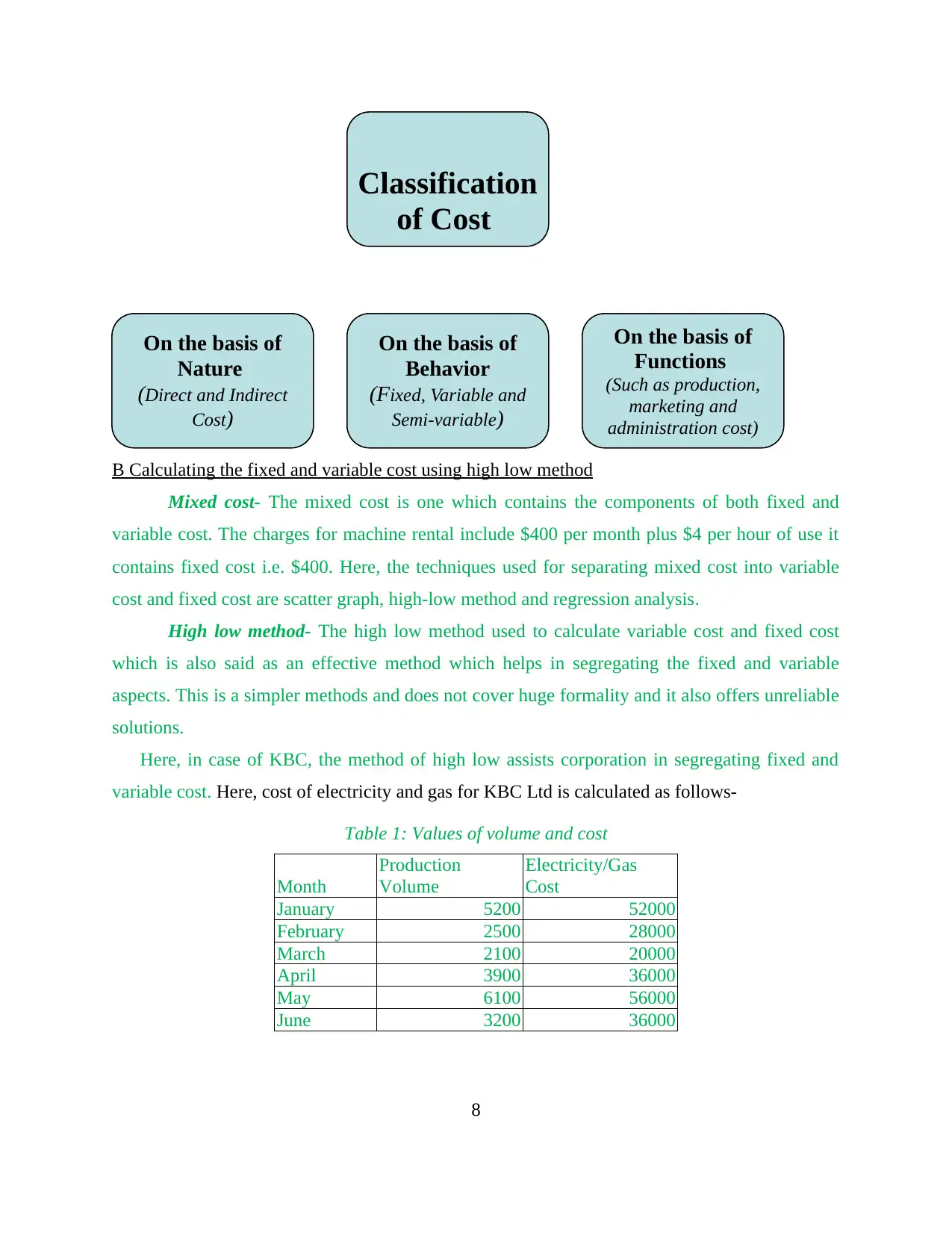

B Calculating the fixed and variable cost using high low method

Mixed cost- The mixed cost is one which contains the components of both fixed and

variable cost. The charges for machine rental include $400 per month plus $4 per hour of use it

contains fixed cost i.e. $400. Here, the techniques used for separating mixed cost into variable

cost and fixed cost are scatter graph, high-low method and regression analysis.

High low method- The high low method used to calculate variable cost and fixed cost

which is also said as an effective method which helps in segregating the fixed and variable

aspects. This is a simpler methods and does not cover huge formality and it also offers unreliable

solutions.

Here, in case of KBC, the method of high low assists corporation in segregating fixed and

variable cost. Here, cost of electricity and gas for KBC Ltd is calculated as follows-

Table 1: Values of volume and cost

Month

Production

Volume

Electricity/Gas

Cost

January 5200 52000

February 2500 28000

March 2100 20000

April 3900 36000

May 6100 56000

June 3200 36000

8

Classification

of Cost

On the basis of

Nature

(Direct and Indirect

Cost)

On the basis of

Behavior

(Fixed, Variable and

Semi-variable)

On the basis of

Functions

(Such as production,

marketing and

administration cost)

Mixed cost- The mixed cost is one which contains the components of both fixed and

variable cost. The charges for machine rental include $400 per month plus $4 per hour of use it

contains fixed cost i.e. $400. Here, the techniques used for separating mixed cost into variable

cost and fixed cost are scatter graph, high-low method and regression analysis.

High low method- The high low method used to calculate variable cost and fixed cost

which is also said as an effective method which helps in segregating the fixed and variable

aspects. This is a simpler methods and does not cover huge formality and it also offers unreliable

solutions.

Here, in case of KBC, the method of high low assists corporation in segregating fixed and

variable cost. Here, cost of electricity and gas for KBC Ltd is calculated as follows-

Table 1: Values of volume and cost

Month

Production

Volume

Electricity/Gas

Cost

January 5200 52000

February 2500 28000

March 2100 20000

April 3900 36000

May 6100 56000

June 3200 36000

8

Classification

of Cost

On the basis of

Nature

(Direct and Indirect

Cost)

On the basis of

Behavior

(Fixed, Variable and

Semi-variable)

On the basis of

Functions

(Such as production,

marketing and

administration cost)

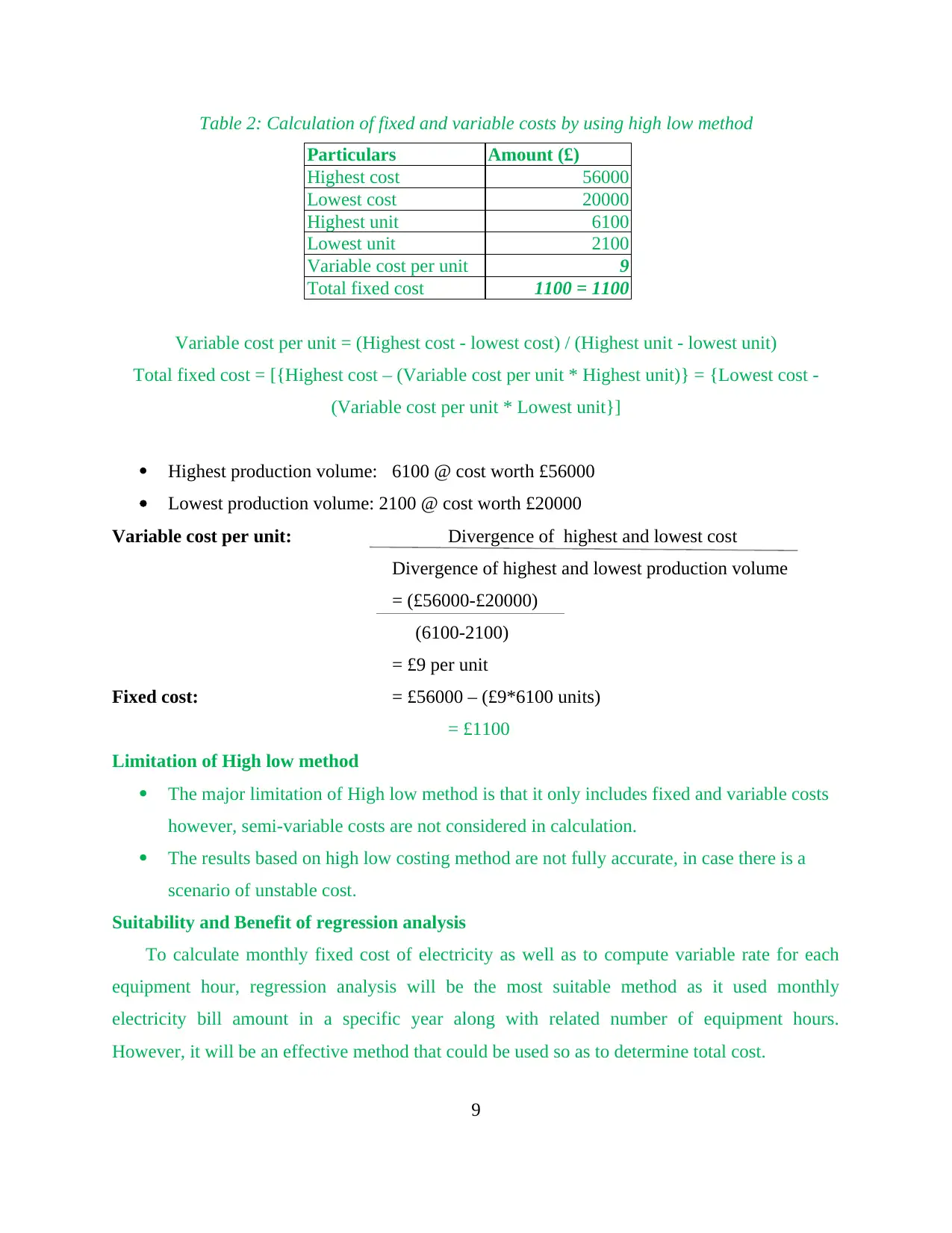

Table 2: Calculation of fixed and variable costs by using high low method

Particulars Amount (£)

Highest cost 56000

Lowest cost 20000

Highest unit 6100

Lowest unit 2100

Variable cost per unit 9

Total fixed cost 1100 = 1100

Variable cost per unit = (Highest cost - lowest cost) / (Highest unit - lowest unit)

Total fixed cost = [{Highest cost – (Variable cost per unit * Highest unit)} = {Lowest cost -

(Variable cost per unit * Lowest unit}]

Highest production volume: 6100 @ cost worth £56000

Lowest production volume: 2100 @ cost worth £20000

Variable cost per unit: Divergence of highest and lowest cost

Divergence of highest and lowest production volume

= (£56000-£20000)

(6100-2100)

= £9 per unit

Fixed cost: = £56000 – (£9*6100 units)

= £1100

Limitation of High low method

The major limitation of High low method is that it only includes fixed and variable costs

however, semi-variable costs are not considered in calculation.

The results based on high low costing method are not fully accurate, in case there is a

scenario of unstable cost.

Suitability and Benefit of regression analysis

To calculate monthly fixed cost of electricity as well as to compute variable rate for each

equipment hour, regression analysis will be the most suitable method as it used monthly

electricity bill amount in a specific year along with related number of equipment hours.

However, it will be an effective method that could be used so as to determine total cost.

9

Particulars Amount (£)

Highest cost 56000

Lowest cost 20000

Highest unit 6100

Lowest unit 2100

Variable cost per unit 9

Total fixed cost 1100 = 1100

Variable cost per unit = (Highest cost - lowest cost) / (Highest unit - lowest unit)

Total fixed cost = [{Highest cost – (Variable cost per unit * Highest unit)} = {Lowest cost -

(Variable cost per unit * Lowest unit}]

Highest production volume: 6100 @ cost worth £56000

Lowest production volume: 2100 @ cost worth £20000

Variable cost per unit: Divergence of highest and lowest cost

Divergence of highest and lowest production volume

= (£56000-£20000)

(6100-2100)

= £9 per unit

Fixed cost: = £56000 – (£9*6100 units)

= £1100

Limitation of High low method

The major limitation of High low method is that it only includes fixed and variable costs

however, semi-variable costs are not considered in calculation.

The results based on high low costing method are not fully accurate, in case there is a

scenario of unstable cost.

Suitability and Benefit of regression analysis

To calculate monthly fixed cost of electricity as well as to compute variable rate for each

equipment hour, regression analysis will be the most suitable method as it used monthly

electricity bill amount in a specific year along with related number of equipment hours.

However, it will be an effective method that could be used so as to determine total cost.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

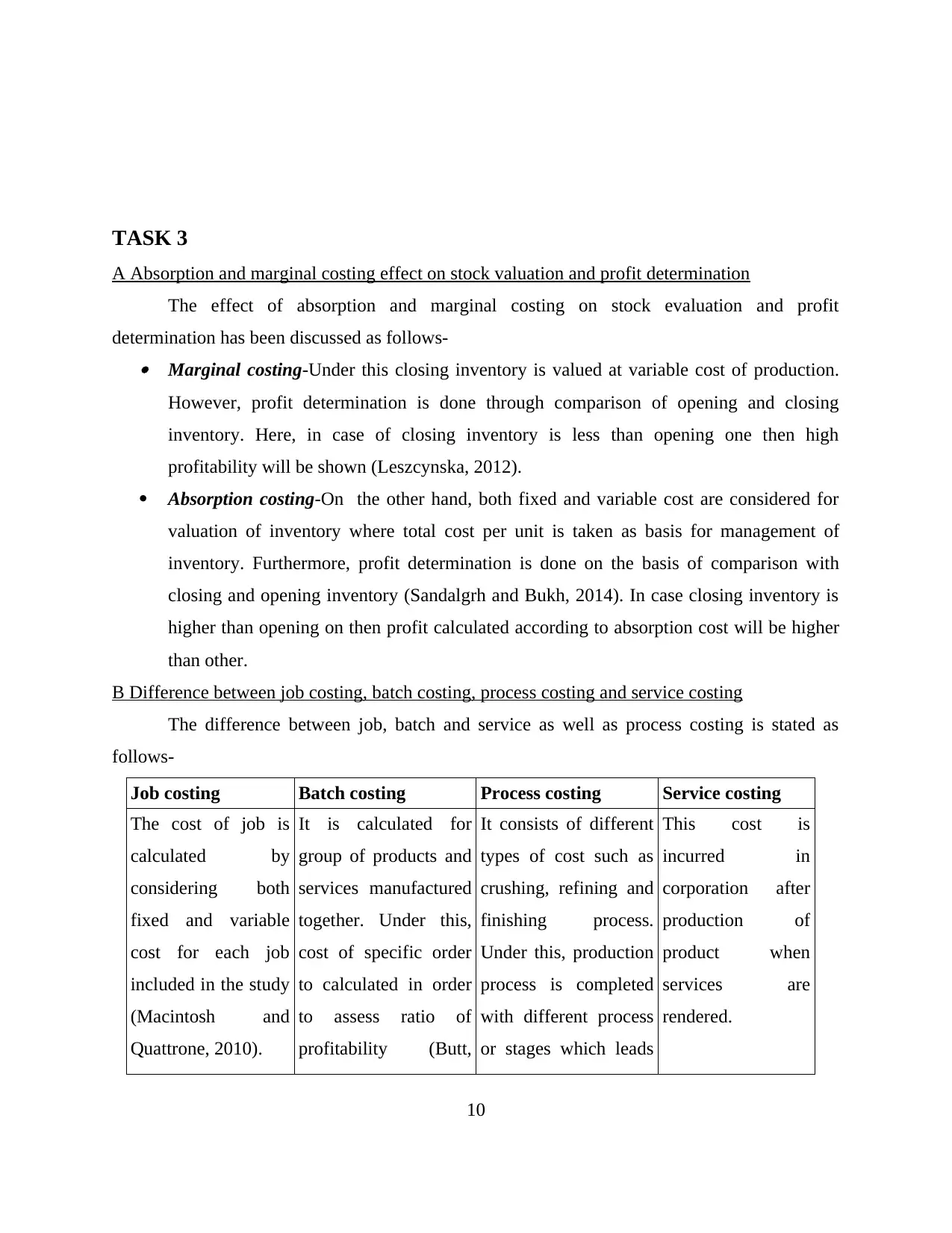

TASK 3

A Absorption and marginal costing effect on stock valuation and profit determination

The effect of absorption and marginal costing on stock evaluation and profit

determination has been discussed as follows- Marginal costing-Under this closing inventory is valued at variable cost of production.

However, profit determination is done through comparison of opening and closing

inventory. Here, in case of closing inventory is less than opening one then high

profitability will be shown (Leszcynska, 2012).

Absorption costing-On the other hand, both fixed and variable cost are considered for

valuation of inventory where total cost per unit is taken as basis for management of

inventory. Furthermore, profit determination is done on the basis of comparison with

closing and opening inventory (Sandalgrh and Bukh, 2014). In case closing inventory is

higher than opening on then profit calculated according to absorption cost will be higher

than other.

B Difference between job costing, batch costing, process costing and service costing

The difference between job, batch and service as well as process costing is stated as

follows-

Job costing Batch costing Process costing Service costing

The cost of job is

calculated by

considering both

fixed and variable

cost for each job

included in the study

(Macintosh and

Quattrone, 2010).

It is calculated for

group of products and

services manufactured

together. Under this,

cost of specific order

to calculated in order

to assess ratio of

profitability (Butt,

It consists of different

types of cost such as

crushing, refining and

finishing process.

Under this, production

process is completed

with different process

or stages which leads

This cost is

incurred in

corporation after

production of

product when

services are

rendered.

10

A Absorption and marginal costing effect on stock valuation and profit determination

The effect of absorption and marginal costing on stock evaluation and profit

determination has been discussed as follows- Marginal costing-Under this closing inventory is valued at variable cost of production.

However, profit determination is done through comparison of opening and closing

inventory. Here, in case of closing inventory is less than opening one then high

profitability will be shown (Leszcynska, 2012).

Absorption costing-On the other hand, both fixed and variable cost are considered for

valuation of inventory where total cost per unit is taken as basis for management of

inventory. Furthermore, profit determination is done on the basis of comparison with

closing and opening inventory (Sandalgrh and Bukh, 2014). In case closing inventory is

higher than opening on then profit calculated according to absorption cost will be higher

than other.

B Difference between job costing, batch costing, process costing and service costing

The difference between job, batch and service as well as process costing is stated as

follows-

Job costing Batch costing Process costing Service costing

The cost of job is

calculated by

considering both

fixed and variable

cost for each job

included in the study

(Macintosh and

Quattrone, 2010).

It is calculated for

group of products and

services manufactured

together. Under this,

cost of specific order

to calculated in order

to assess ratio of

profitability (Butt,

It consists of different

types of cost such as

crushing, refining and

finishing process.

Under this, production

process is completed

with different process

or stages which leads

This cost is

incurred in

corporation after

production of

product when

services are

rendered.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2010). to support final

outcome.

C Preparing profit and loss statement for North and South area under absorption costing

North

Absorption costing Standard Super Delux Total

Sales 3680000 1920000 1680000 7280000

Less: costs of production

Purchase 2944000 1440000 1232000 5616000

Variable Transportation costs 92000 48000 42000 182000

Fixed costs of transportation 73600 38400 33600 145600

Total costs of production 3109600 1526400 1307600 5943600

Gross profit(Sales-cost of goods sold) 570400 393600 372400 1336400

Less: Other expenses

Variable packaging cost 80000 40000 20000 140000

Fixed packaging costs 160000 80000 40000 280000

Variable advertisement cost 92000 40000 28000

16000

Fixed advertisement cost 184000 80000 56000 320000

Total expense 516000 240000 144000 900000

Profit/Loss 54400 153600 228400 436400

South

Absorption costing Standard Super Delux Total

Sales 1200000 1920000 2400000 5520000

Less: Variable costs

Purchase 960000 1440000 1760000 4160000

Variable Transportation costs 30000 48000 60000 138000

Fixed costs of transportation 24000 38400 48000 110400

Total costs of production 1014000 1526400 1868000 4408400

Gross profit(Sales-cost of goods sold) 186000 393600 532000 4656800

Less: Other expenses

Variable packaging cost 12000 20000 16000 48000

Fixed packaging costs 24000 40000 32000 96000

Variable advertisement cost 30000 40000 40000 110000

Fixed advertisement cost 60000 80000 80000 220000

Total expenes 126000 180000 168000 474000

Profit/Loss 60000 213600 364000 637600

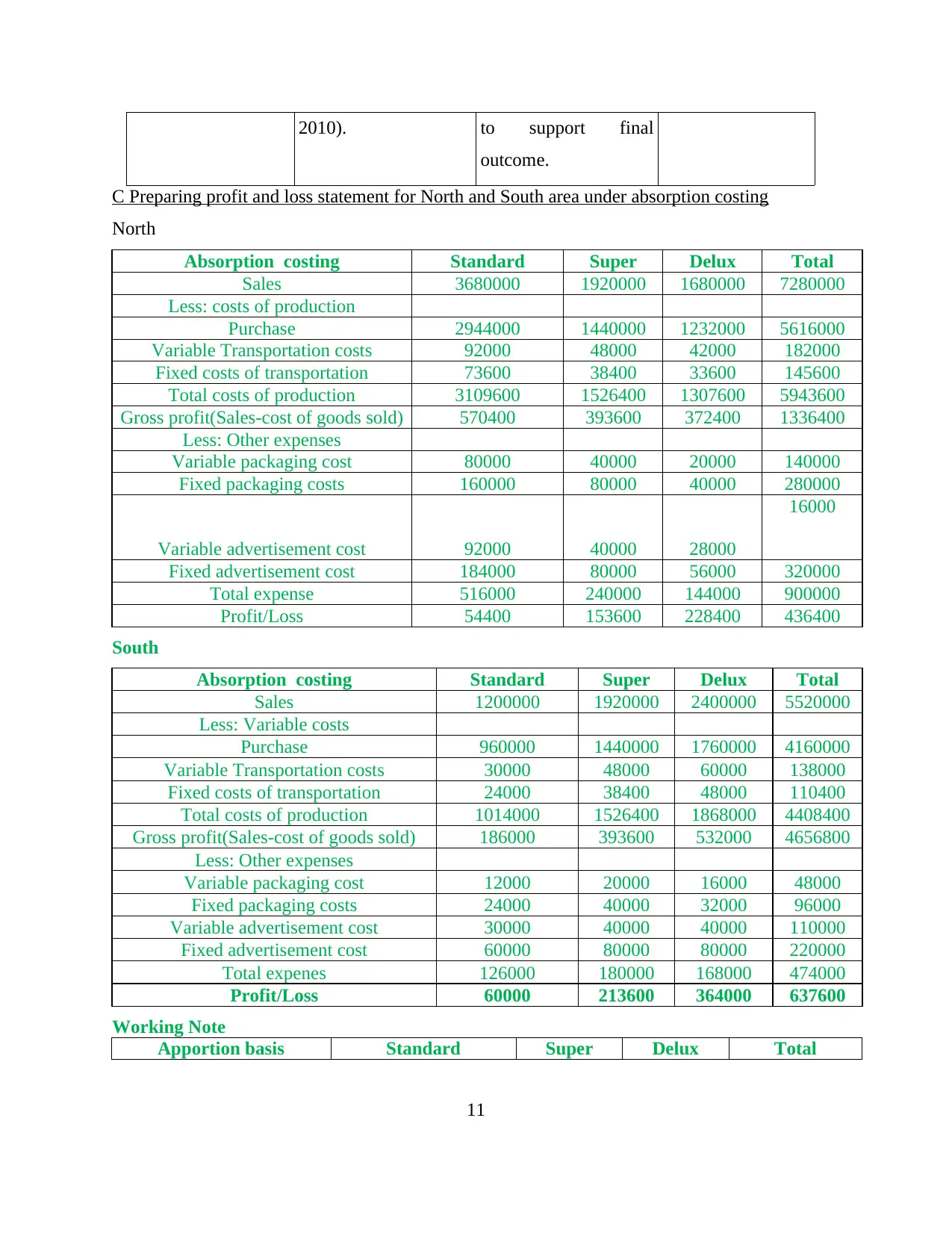

Working Note

Apportion basis Standard Super Delux Total

11

outcome.

C Preparing profit and loss statement for North and South area under absorption costing

North

Absorption costing Standard Super Delux Total

Sales 3680000 1920000 1680000 7280000

Less: costs of production

Purchase 2944000 1440000 1232000 5616000

Variable Transportation costs 92000 48000 42000 182000

Fixed costs of transportation 73600 38400 33600 145600

Total costs of production 3109600 1526400 1307600 5943600

Gross profit(Sales-cost of goods sold) 570400 393600 372400 1336400

Less: Other expenses

Variable packaging cost 80000 40000 20000 140000

Fixed packaging costs 160000 80000 40000 280000

Variable advertisement cost 92000 40000 28000

16000

Fixed advertisement cost 184000 80000 56000 320000

Total expense 516000 240000 144000 900000

Profit/Loss 54400 153600 228400 436400

South

Absorption costing Standard Super Delux Total

Sales 1200000 1920000 2400000 5520000

Less: Variable costs

Purchase 960000 1440000 1760000 4160000

Variable Transportation costs 30000 48000 60000 138000

Fixed costs of transportation 24000 38400 48000 110400

Total costs of production 1014000 1526400 1868000 4408400

Gross profit(Sales-cost of goods sold) 186000 393600 532000 4656800

Less: Other expenses

Variable packaging cost 12000 20000 16000 48000

Fixed packaging costs 24000 40000 32000 96000

Variable advertisement cost 30000 40000 40000 110000

Fixed advertisement cost 60000 80000 80000 220000

Total expenes 126000 180000 168000 474000

Profit/Loss 60000 213600 364000 637600

Working Note

Apportion basis Standard Super Delux Total

11

Number of orders 40000 20000 10000 70000

Number of orders 6000 10000 8000 24000

Total 94000

Variable packaging Standard Super Delux Total

North No. of orders 80000 40000 20000 140000

South No. of orders 12000 20000 16000 48000

Total 188000

Fixed Packaging Standard Super Delux Total

North no. of order 160000 80000 40000 280000

South no. of order 24000 40000 32000 96000

Total 376000

Advertisement Apportion basis Standard Super Delux Total

North Units sold 92000 40000 28000 160000

South Units sold 30000 40000 40000 110000

Total 270000

Variable

advertisement Standard Super Delux Total

North Units sold 92000 40000 28000 160000

South Units sold 30000 40000 40000 110000

Total 270000

Fixed advertisement Standard Super Delux Total

North Units sold 184000 80000 56000 320000

South Units sold 60000 80000 80000 220000

Total 540000

Fixed transportation Standard Super Delux Total

North Sales value 73600 38400 33600 145600

South Sales value 24000 38400 48000 110400

Total 256000

Variable

transportation Standard Super Delux Total

North Sales value 92000 48000 42000 182000

12

Number of orders 6000 10000 8000 24000

Total 94000

Variable packaging Standard Super Delux Total

North No. of orders 80000 40000 20000 140000

South No. of orders 12000 20000 16000 48000

Total 188000

Fixed Packaging Standard Super Delux Total

North no. of order 160000 80000 40000 280000

South no. of order 24000 40000 32000 96000

Total 376000

Advertisement Apportion basis Standard Super Delux Total

North Units sold 92000 40000 28000 160000

South Units sold 30000 40000 40000 110000

Total 270000

Variable

advertisement Standard Super Delux Total

North Units sold 92000 40000 28000 160000

South Units sold 30000 40000 40000 110000

Total 270000

Fixed advertisement Standard Super Delux Total

North Units sold 184000 80000 56000 320000

South Units sold 60000 80000 80000 220000

Total 540000

Fixed transportation Standard Super Delux Total

North Sales value 73600 38400 33600 145600

South Sales value 24000 38400 48000 110400

Total 256000

Variable

transportation Standard Super Delux Total

North Sales value 92000 48000 42000 182000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.