Management Accounting System and Financial Problem Analysis for KEF

VerifiedAdded on 2021/02/20

|15

|4317

|96

Report

AI Summary

This report provides a detailed analysis of management accounting systems and their application within KEF. It begins by defining management accounting and exploring various systems like inventory, job costing, cost accounting, and price optimization. The report then presents different management accounting reporting methods, including budget reports, job reports, and inventory reports. It evaluates the benefits and drawbacks of each system, followed by a critical assessment of integrating these systems into organizational processes. Task 2 focuses on calculations using absorption and marginal costing techniques. Task 3 analyzes planning tools for budgetary control, including their advantages, disadvantages, and applications in budget preparation and forecasting. Finally, the report examines how KEF adapts management accounting to address financial problems, demonstrating how these systems contribute to sustainable growth and evaluating the planning tools used in this process.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Explaining the meaning of management accounting system and its essential requirement...3

Different methods of management accounting reporting.......................................................4

Evaluating the benefits of the management accounting systems and its application in the

organisation............................................................................................................................5

Critical evaluation of integration management accounting system and reporting in

organizational processes.........................................................................................................6

TASK 2............................................................................................................................................6

Calculations as per absorption and marginal costing techniques...........................................6

TASK 3............................................................................................................................................9

Presenting the advantages and disadvantages of the different types of planing tools in

budgetary control....................................................................................................................9

Analysis of the use of different planning tools and their application in preparing and

forecasting of budgets...........................................................................................................10

TASK 4..........................................................................................................................................11

Comparison of how organisations are adapting the management accounting systems to

respond to financial problems by KEF.................................................................................11

Presenting an explanation that dealing with financial problem through management

accounting system leads KEF to sustainable growth...........................................................12

Evaluation of the planning tools to be used to respond to financial problem......................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Explaining the meaning of management accounting system and its essential requirement...3

Different methods of management accounting reporting.......................................................4

Evaluating the benefits of the management accounting systems and its application in the

organisation............................................................................................................................5

Critical evaluation of integration management accounting system and reporting in

organizational processes.........................................................................................................6

TASK 2............................................................................................................................................6

Calculations as per absorption and marginal costing techniques...........................................6

TASK 3............................................................................................................................................9

Presenting the advantages and disadvantages of the different types of planing tools in

budgetary control....................................................................................................................9

Analysis of the use of different planning tools and their application in preparing and

forecasting of budgets...........................................................................................................10

TASK 4..........................................................................................................................................11

Comparison of how organisations are adapting the management accounting systems to

respond to financial problems by KEF.................................................................................11

Presenting an explanation that dealing with financial problem through management

accounting system leads KEF to sustainable growth...........................................................12

Evaluation of the planning tools to be used to respond to financial problem......................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is an analytical tool that is used by the business organization as

an application of the knowledge and skill in the preparation of accounting information in a

specific manner to assist the management of the business in formulating policies and controlling

and panning the operations of the business. The scope of management accounting is vast and its

assist the business in the decision-making process through use of financial as well as statistical

information. In the present report the management of KEF is presented with the meanings and

use of the various types of management accounting system and their pros and cons. With this

management accounting reporting are also explained For the new product launched calculations

are presented on the basis of absorption and marginal costing techniques. KEF is presented with

application of planning tools to respond to the financial problems and can lead to substantial

development.

TASK 1

Explaining the meaning of management accounting system and its essential requirement.

Management accounting:

As per the definition given by the cost and management accountants of London,

management accounting means the application of the professional knowledge and skill for

preparation of the accounting information in such way which assist the business management in

taking business decision and make policies, plan and control the operations of the business. This

includes the concepts and the methods which are essential for effective planning for selecting the

best alternative business action and controlling through evaluating and interpreting the business

performance (What Is a Management Accounting System, 2019). The management accounting

system and reports are integral part of the management accounting and it looks in to the events

while happens in and around the organisation along with considering the requirements of the

business. The data are elevated and gives estimated figures over which decisions can be based.

The different types of management accounting systems are:

Inventory management systems:

The inventory management system can be defined as the system for managing the

current system. This system looks at maintaining the optimal level of inventory with the business

and evaluate the requirement of stocks for procurement of the required production of the units to

reach the optimal and budgeted level of sales. In manages an effective control over the inventory

Management accounting is an analytical tool that is used by the business organization as

an application of the knowledge and skill in the preparation of accounting information in a

specific manner to assist the management of the business in formulating policies and controlling

and panning the operations of the business. The scope of management accounting is vast and its

assist the business in the decision-making process through use of financial as well as statistical

information. In the present report the management of KEF is presented with the meanings and

use of the various types of management accounting system and their pros and cons. With this

management accounting reporting are also explained For the new product launched calculations

are presented on the basis of absorption and marginal costing techniques. KEF is presented with

application of planning tools to respond to the financial problems and can lead to substantial

development.

TASK 1

Explaining the meaning of management accounting system and its essential requirement.

Management accounting:

As per the definition given by the cost and management accountants of London,

management accounting means the application of the professional knowledge and skill for

preparation of the accounting information in such way which assist the business management in

taking business decision and make policies, plan and control the operations of the business. This

includes the concepts and the methods which are essential for effective planning for selecting the

best alternative business action and controlling through evaluating and interpreting the business

performance (What Is a Management Accounting System, 2019). The management accounting

system and reports are integral part of the management accounting and it looks in to the events

while happens in and around the organisation along with considering the requirements of the

business. The data are elevated and gives estimated figures over which decisions can be based.

The different types of management accounting systems are:

Inventory management systems:

The inventory management system can be defined as the system for managing the

current system. This system looks at maintaining the optimal level of inventory with the business

and evaluate the requirement of stocks for procurement of the required production of the units to

reach the optimal and budgeted level of sales. In manages an effective control over the inventory

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

flow of KEF in for reduction in the total cost of inventory of the business (Kaplan and Atkinson,

2017). With the effective and efficient inventory management system KEF minimizes its

investment in the inventory and ensures higher profitability as this system assist the management

in keeping the optimal level of stock within the business.

Job costing systems:

The job costing system under management accounting refers to the recording of the cost

that is involved in the production of the good and commodities of the business. With the use of

this system cost and expenses incurred on each job ad activity is determined and a track of each

cost for particular job is kept. This is done to identifying the actual cost incurred on each activity

involved in production of the products of organization KEF. This system provides accurate

information which gives correct estimation of the cost incurred by the company for each of the

job and activity.

Cost accounting system:

The cost accounting system is that system under management accounting that allocate

the resources and cost to each of the activity within an organisation. KEF uses this framework to

estimate the cost of their goods and products for profitability analysis, valuation of the inventory

and controlling the cost. With determination of the cost of each of the commodity manufactured

by KEF, it can determine the sales price after adding the profit margin, the funds and quotative

required to produce a batch or each unit of product.

Price optimization systems:

The price optimization system under management accounting can be referred as that

system under which is used by KEF to set the price of the product which are affordable to the

consumers (Maas, chaltegger and Crutzen, 2016). This system assist the management of KEF in

creation of sales model and cost model which assist in determining the demand of the product.

This aid In evaluating the expenses incurred and sales target which are required to meet the profit

margin of the business.

Different methods of management accounting reporting

Budget reports:

The budget report is the basic report which is prepared for overall business of KEF. This

assist managers and owners of the business in understanding the cost and expenses which is

distributed throughout the organisation to each of the activity of the business. The identification

2017). With the effective and efficient inventory management system KEF minimizes its

investment in the inventory and ensures higher profitability as this system assist the management

in keeping the optimal level of stock within the business.

Job costing systems:

The job costing system under management accounting refers to the recording of the cost

that is involved in the production of the good and commodities of the business. With the use of

this system cost and expenses incurred on each job ad activity is determined and a track of each

cost for particular job is kept. This is done to identifying the actual cost incurred on each activity

involved in production of the products of organization KEF. This system provides accurate

information which gives correct estimation of the cost incurred by the company for each of the

job and activity.

Cost accounting system:

The cost accounting system is that system under management accounting that allocate

the resources and cost to each of the activity within an organisation. KEF uses this framework to

estimate the cost of their goods and products for profitability analysis, valuation of the inventory

and controlling the cost. With determination of the cost of each of the commodity manufactured

by KEF, it can determine the sales price after adding the profit margin, the funds and quotative

required to produce a batch or each unit of product.

Price optimization systems:

The price optimization system under management accounting can be referred as that

system under which is used by KEF to set the price of the product which are affordable to the

consumers (Maas, chaltegger and Crutzen, 2016). This system assist the management of KEF in

creation of sales model and cost model which assist in determining the demand of the product.

This aid In evaluating the expenses incurred and sales target which are required to meet the profit

margin of the business.

Different methods of management accounting reporting

Budget reports:

The budget report is the basic report which is prepared for overall business of KEF. This

assist managers and owners of the business in understanding the cost and expenses which is

distributed throughout the organisation to each of the activity of the business. The identification

of cost is in the context of each of the department and each job of KEF. The expenses of the

previous years are evaluated and then it makes the estimated budgets for the nest coming years.

Job reports:

The job costing report are preshared to identify the cost and expenses of each of he job

within KEF. This gives detailed view of the total cost incurred on a job and defines cost

bifurcation for each part of the job (Types of Managerial Accounting Reports, 2019). The reports

assist the management of KEF in evaluation of the profitability of each specific job and aid them

in optimizing the cost and expenses in the limit of resource allocated to that specific job.

Inventory and manufacturing report:

KEF manufactures products and it is engaged production activities primarily. This type

of business have a low endurance regarding any shift in the inventory as this can result in major

losses and fall back in the productions. For this the inventory and manufacturing reports are of

high value (Quattrone, 2016). This also assist in centralising the data related with inventory cost,

labour and other overhead which are incurred in the production process with presenting a raw

data for optimizing the cost.

Evaluating the benefits of the management accounting systems and its application in the

organisation

Inventory management systems:

The advantage of the inventory management system includes keeping a track on the

supplies and presenting the information to the management of KEF. This system aids the

company in controlling inventory holding cost as identifies actual requirement of raw material

in stock and the produce the goods as per demand which increase the profitably and efficiency in

production. The disadvantage associated with this system is that it is complex and to determine

the actual demand is very tough as its fluctuate rapidly. The process is time consuming and

required skilled person to prepare the system.

Job costing systems:

The job costing system's benefits includes ascertainment of the cost and expenses related

with each of the activity of the KEF. This assist the business in determination of each specific

cost required to conduct various activities of business. This assist management of KEF in

allocation of resources effectively. The drawback of this system is that there is no standard set to

previous years are evaluated and then it makes the estimated budgets for the nest coming years.

Job reports:

The job costing report are preshared to identify the cost and expenses of each of he job

within KEF. This gives detailed view of the total cost incurred on a job and defines cost

bifurcation for each part of the job (Types of Managerial Accounting Reports, 2019). The reports

assist the management of KEF in evaluation of the profitability of each specific job and aid them

in optimizing the cost and expenses in the limit of resource allocated to that specific job.

Inventory and manufacturing report:

KEF manufactures products and it is engaged production activities primarily. This type

of business have a low endurance regarding any shift in the inventory as this can result in major

losses and fall back in the productions. For this the inventory and manufacturing reports are of

high value (Quattrone, 2016). This also assist in centralising the data related with inventory cost,

labour and other overhead which are incurred in the production process with presenting a raw

data for optimizing the cost.

Evaluating the benefits of the management accounting systems and its application in the

organisation

Inventory management systems:

The advantage of the inventory management system includes keeping a track on the

supplies and presenting the information to the management of KEF. This system aids the

company in controlling inventory holding cost as identifies actual requirement of raw material

in stock and the produce the goods as per demand which increase the profitably and efficiency in

production. The disadvantage associated with this system is that it is complex and to determine

the actual demand is very tough as its fluctuate rapidly. The process is time consuming and

required skilled person to prepare the system.

Job costing systems:

The job costing system's benefits includes ascertainment of the cost and expenses related

with each of the activity of the KEF. This assist the business in determination of each specific

cost required to conduct various activities of business. This assist management of KEF in

allocation of resources effectively. The drawback of this system is that there is no standard set to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

determine the cost and expenses estimations. There is more clerical work involved in this system

and maintenance of detailed information is also required.

Cost accounting system:

The pros related with this system is that cost related with activity is easily identifiable

and this gives management of KEF an opportunity to conduct comparison of spending on each

activity and take cost controlling measures accordingly (Messner, 2016). This cons related with

this system are that this system is time consuming and to determine the cost of each activity is

quite lengthy. A wrong detection of the cost can lead to misallocation of the resources and can

hamper the performance efficiency.

Price optimization systems:

The advantages associated with this system is that it allows the KEF to set such prices

which are dearer to consumers and they can afford the same. This system efficiently reduces the

manual resource engagement for determining the selling price of the business products. This

cons related with this system is that it s hard to determine the level of price that is affordable to

the consumer as their taste and preference changes frequently.

Critical evaluation of integration management accounting system and reporting in organizational

processes

The management accounting system are related with presenting a coherent system for

managing the activities of the business of KEF. That provide the management with the data and

figures over cost, spendings, resources and their allocation to each of the activity of the business.

The management accounting reports are prepared by the KEF to determine performance of the

business and its related activities. The integration can be shown as on the basis of the

management accounting systems the reports are prepared and both of falls under the scope of the

management accounting. Moreover, management accounting is related with stating system to

conduct the operation of the business of KEF and the other is related with detecting and

evaluation of the performance and each setting the goals for each of the activity of the business.

TASK 2

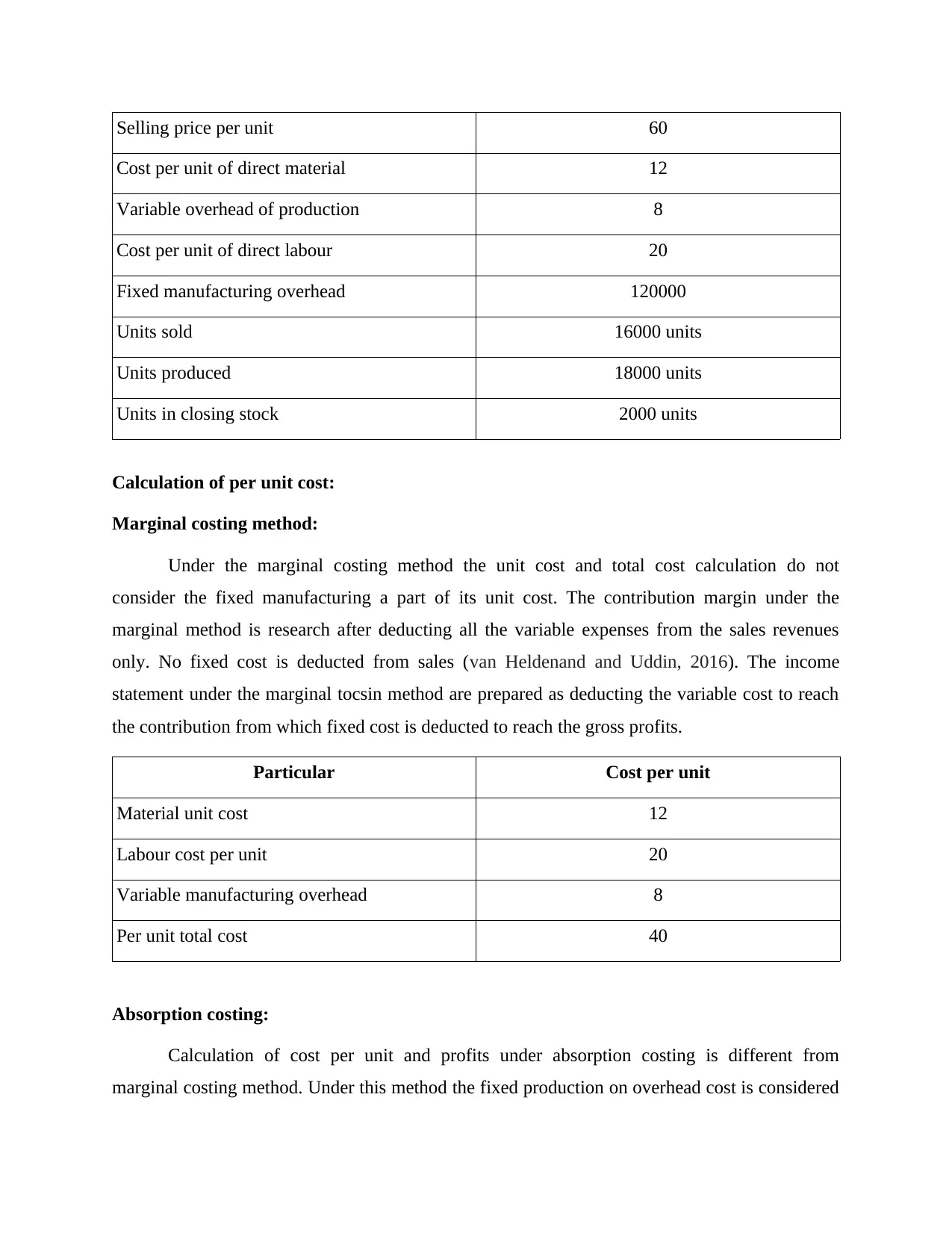

Calculations as per absorption and marginal costing techniques

Details given

Particular Amount in Pounds

and maintenance of detailed information is also required.

Cost accounting system:

The pros related with this system is that cost related with activity is easily identifiable

and this gives management of KEF an opportunity to conduct comparison of spending on each

activity and take cost controlling measures accordingly (Messner, 2016). This cons related with

this system are that this system is time consuming and to determine the cost of each activity is

quite lengthy. A wrong detection of the cost can lead to misallocation of the resources and can

hamper the performance efficiency.

Price optimization systems:

The advantages associated with this system is that it allows the KEF to set such prices

which are dearer to consumers and they can afford the same. This system efficiently reduces the

manual resource engagement for determining the selling price of the business products. This

cons related with this system is that it s hard to determine the level of price that is affordable to

the consumer as their taste and preference changes frequently.

Critical evaluation of integration management accounting system and reporting in organizational

processes

The management accounting system are related with presenting a coherent system for

managing the activities of the business of KEF. That provide the management with the data and

figures over cost, spendings, resources and their allocation to each of the activity of the business.

The management accounting reports are prepared by the KEF to determine performance of the

business and its related activities. The integration can be shown as on the basis of the

management accounting systems the reports are prepared and both of falls under the scope of the

management accounting. Moreover, management accounting is related with stating system to

conduct the operation of the business of KEF and the other is related with detecting and

evaluation of the performance and each setting the goals for each of the activity of the business.

TASK 2

Calculations as per absorption and marginal costing techniques

Details given

Particular Amount in Pounds

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Selling price per unit 60

Cost per unit of direct material 12

Variable overhead of production 8

Cost per unit of direct labour 20

Fixed manufacturing overhead 120000

Units sold 16000 units

Units produced 18000 units

Units in closing stock 2000 units

Calculation of per unit cost:

Marginal costing method:

Under the marginal costing method the unit cost and total cost calculation do not

consider the fixed manufacturing a part of its unit cost. The contribution margin under the

marginal method is research after deducting all the variable expenses from the sales revenues

only. No fixed cost is deducted from sales (van Heldenand and Uddin, 2016). The income

statement under the marginal tocsin method are prepared as deducting the variable cost to reach

the contribution from which fixed cost is deducted to reach the gross profits.

Particular Cost per unit

Material unit cost 12

Labour cost per unit 20

Variable manufacturing overhead 8

Per unit total cost 40

Absorption costing:

Calculation of cost per unit and profits under absorption costing is different from

marginal costing method. Under this method the fixed production on overhead cost is considered

Cost per unit of direct material 12

Variable overhead of production 8

Cost per unit of direct labour 20

Fixed manufacturing overhead 120000

Units sold 16000 units

Units produced 18000 units

Units in closing stock 2000 units

Calculation of per unit cost:

Marginal costing method:

Under the marginal costing method the unit cost and total cost calculation do not

consider the fixed manufacturing a part of its unit cost. The contribution margin under the

marginal method is research after deducting all the variable expenses from the sales revenues

only. No fixed cost is deducted from sales (van Heldenand and Uddin, 2016). The income

statement under the marginal tocsin method are prepared as deducting the variable cost to reach

the contribution from which fixed cost is deducted to reach the gross profits.

Particular Cost per unit

Material unit cost 12

Labour cost per unit 20

Variable manufacturing overhead 8

Per unit total cost 40

Absorption costing:

Calculation of cost per unit and profits under absorption costing is different from

marginal costing method. Under this method the fixed production on overhead cost is considered

to be part of the unit cost. Under this method the fixed manufacturing overhead are considered as

pert of the production cost and are allocated to the unit cost of goods. The profits under this

methods are always high when the production is more than then the sales units. The calculation

of profits under income statement is done deducting value closing stock from sales revenue and

to reach gross profits and then deducting the total cost of manufacture including variable and

fixed cost to reach the net operating profits of the production of goods and commodities.

Particular Cost per unit

Material unit cost 12

Labour cost per unit 20

Variable manufacturing overhead 8

Fixed manufacturing overhead => (120000/18000) 6.67

Per unit total cost 40

Budgeted income statement under Marginal costing method:

Revenue from sales 16000*60 960000

Value of cl st 2000*40 80000

Total VC 40*16000 640000

Contribution margin 400000

Total fixed cost 120000 120000

G/p 280000

Budgeted income statement under absorption costing method:

Particular Working note Amount

Revenues from sales 16000*60 960000

Closing stock 2000*46.67 93340

G/P

Total cost of manufacturing 18000*46.67 840060

Net Op profit 213280

pert of the production cost and are allocated to the unit cost of goods. The profits under this

methods are always high when the production is more than then the sales units. The calculation

of profits under income statement is done deducting value closing stock from sales revenue and

to reach gross profits and then deducting the total cost of manufacture including variable and

fixed cost to reach the net operating profits of the production of goods and commodities.

Particular Cost per unit

Material unit cost 12

Labour cost per unit 20

Variable manufacturing overhead 8

Fixed manufacturing overhead => (120000/18000) 6.67

Per unit total cost 40

Budgeted income statement under Marginal costing method:

Revenue from sales 16000*60 960000

Value of cl st 2000*40 80000

Total VC 40*16000 640000

Contribution margin 400000

Total fixed cost 120000 120000

G/p 280000

Budgeted income statement under absorption costing method:

Particular Working note Amount

Revenues from sales 16000*60 960000

Closing stock 2000*46.67 93340

G/P

Total cost of manufacturing 18000*46.67 840060

Net Op profit 213280

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Actual income statement under Marginal costing method:

Particular Working note Amount

Revenues from sales 16000*60 960000

add: cl stk 2000*40 80000

less: V/C 40*16000 640000

Contribution margin 400000

Less: Total F/C 120000 120000

GP 280000

Actual income statement under absorption costing method

Particular Working note Amount

Revenues from sales 16000*60 960000

add: cl stk 3000*46.67 140010

G/P

less: cost of production 19000*46.67 886730

Net Op profit 213280

TASK 3

Budget preparation and its purpose:

The budgets are of various types and such as sales, operating, cash and others and each of

them is prepared by the organisation KEF with a view to determine the cost and spendings on

different activities of the business. This budget forecast the incomes and expenditure of the

business and by that the profitability of the business is evaluated. The main purpose of the

budget preparation is to present the estimated cost to the business where the activities to be

undertaken within allocated resources and funds.

Presenting the advantages and disadvantages of the different types of planing tools in budgetary

control

Zero based budget:

Particular Working note Amount

Revenues from sales 16000*60 960000

add: cl stk 2000*40 80000

less: V/C 40*16000 640000

Contribution margin 400000

Less: Total F/C 120000 120000

GP 280000

Actual income statement under absorption costing method

Particular Working note Amount

Revenues from sales 16000*60 960000

add: cl stk 3000*46.67 140010

G/P

less: cost of production 19000*46.67 886730

Net Op profit 213280

TASK 3

Budget preparation and its purpose:

The budgets are of various types and such as sales, operating, cash and others and each of

them is prepared by the organisation KEF with a view to determine the cost and spendings on

different activities of the business. This budget forecast the incomes and expenditure of the

business and by that the profitability of the business is evaluated. The main purpose of the

budget preparation is to present the estimated cost to the business where the activities to be

undertaken within allocated resources and funds.

Presenting the advantages and disadvantages of the different types of planing tools in budgetary

control

Zero based budget:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The benefits of preparation of this budget s that all the expenses are estimated freshly

with a zero base and all are justified as well. The KEF is ensured with this budget over spending

of each penny of the business (Malmi, 2016). The disadvantage of the business is that it take lot

of time to prepare the budget and it rewards short term thinking where the resources are shifted

to those area which give more profits.

Operating budget:

The pros of this budget is that KEF an keep a track of all the activities of the business.

This identifies the revenues earned and spending done by the business which let the business

know all actual profits earned and difference between income and expenditure. The cons of this

budget is that it is not flexible in nature and does not allow any changes in the estimated figures

during the year.

Cash budget:

Analysis of the use of different planning tools and their application in preparing and forecasting

of budgets

Zero based budget:

The Zero based budget is that budget which is prepared by the KEF from zero base for

each budgeting period which s generally a year. Under this budget reference from old budget is

taken ad all the expenses are estimated on fresh basis as per the prevailing conditions of business

operations such as production level, cost of raw material and others. The expenses estimated

under this budgets are required to be justifies as what are the basis for reaching the cost and

spendings for each of the activity of KEF.

Cash budget:

The cash budgets are the budget which is related with each expenditure of the business

exclusively. This budget defines cash spending that will be done by KEF in a budgeting periods

This budget take references form past budgets and prepare a new budget for each budgeting

period (Anessi-Pessina and et.al., 2016). The expenses and cost are estimated on the cash basis

that will incurred no each activity or production of the business. Preparation of cash budget is

beneficial for the company because it enables the organization in assessing the pattern of its cash

inflows and cash outflows. This aids the managers of KEF Ltd., in formulating more effective

with a zero base and all are justified as well. The KEF is ensured with this budget over spending

of each penny of the business (Malmi, 2016). The disadvantage of the business is that it take lot

of time to prepare the budget and it rewards short term thinking where the resources are shifted

to those area which give more profits.

Operating budget:

The pros of this budget is that KEF an keep a track of all the activities of the business.

This identifies the revenues earned and spending done by the business which let the business

know all actual profits earned and difference between income and expenditure. The cons of this

budget is that it is not flexible in nature and does not allow any changes in the estimated figures

during the year.

Cash budget:

Analysis of the use of different planning tools and their application in preparing and forecasting

of budgets

Zero based budget:

The Zero based budget is that budget which is prepared by the KEF from zero base for

each budgeting period which s generally a year. Under this budget reference from old budget is

taken ad all the expenses are estimated on fresh basis as per the prevailing conditions of business

operations such as production level, cost of raw material and others. The expenses estimated

under this budgets are required to be justifies as what are the basis for reaching the cost and

spendings for each of the activity of KEF.

Cash budget:

The cash budgets are the budget which is related with each expenditure of the business

exclusively. This budget defines cash spending that will be done by KEF in a budgeting periods

This budget take references form past budgets and prepare a new budget for each budgeting

period (Anessi-Pessina and et.al., 2016). The expenses and cost are estimated on the cash basis

that will incurred no each activity or production of the business. Preparation of cash budget is

beneficial for the company because it enables the organization in assessing the pattern of its cash

inflows and cash outflows. This aids the managers of KEF Ltd., in formulating more effective

strategies for enhancing the cash inflows and keeping a check on the activities which are

consuming the financial resources and the benefits they are generating for the business entity.

Further, it helps the management of the bushiness enterprise in dealing with the financial

situations by making the realistic predictions and forecasting. Moreover, it facilitates the

company in its seasonal planning. Cash Budgets aids the managers in getting prepared for the

seasonal fluctuations in sales and expenses. For instance, this budget helps in setting aside a

particular amount of money for dealing with the seasonal peaks and recession. The drawback of

this budget is it requires trained professionals and experts which is a challenge for company to

find such personnel and retain. Further, it consumes too much of company resources in terms of

time and money.

Operating budge:

The operating budgets for KEF are prepared with a view to determine the projected

revenues and the expenses associated for the forthcoming period within the organization. It is

presented on the formate of income statement and the Management goes through the process of

compiling the budget before the start of each year. In this budget all the cost incurred within an

organisation are included such as variable, fixed, semi variable and operating cost.

TASK 4

Comparison of how organisations are adapting the management accounting systems to respond

to financial problems by KEF

The the management accounting system with KEF assist the management in decision

making process. The process of making decision includes the identification of choice presented

to the business under the system and selecting the appropriate one in accordance with the issues

and prevailing conditions as well. The process includes different stages and KEF make

thoughtful and deliberated decisions by organisation of the information and defining the

alternative solution to a give issue or task.

Issues/Problem Alternative 1 Alternative 2 Conclusion

There is decline in the

sales revenue of KEF

organisation and the

company is under a

The first solution is to

adopt the absorption

costing method

whether company can

Under the second

alternative of

marginal costing the

organization KEF is

This is suggested to

the KEF that the

decision of buying the

product is more

consuming the financial resources and the benefits they are generating for the business entity.

Further, it helps the management of the bushiness enterprise in dealing with the financial

situations by making the realistic predictions and forecasting. Moreover, it facilitates the

company in its seasonal planning. Cash Budgets aids the managers in getting prepared for the

seasonal fluctuations in sales and expenses. For instance, this budget helps in setting aside a

particular amount of money for dealing with the seasonal peaks and recession. The drawback of

this budget is it requires trained professionals and experts which is a challenge for company to

find such personnel and retain. Further, it consumes too much of company resources in terms of

time and money.

Operating budge:

The operating budgets for KEF are prepared with a view to determine the projected

revenues and the expenses associated for the forthcoming period within the organization. It is

presented on the formate of income statement and the Management goes through the process of

compiling the budget before the start of each year. In this budget all the cost incurred within an

organisation are included such as variable, fixed, semi variable and operating cost.

TASK 4

Comparison of how organisations are adapting the management accounting systems to respond

to financial problems by KEF

The the management accounting system with KEF assist the management in decision

making process. The process of making decision includes the identification of choice presented

to the business under the system and selecting the appropriate one in accordance with the issues

and prevailing conditions as well. The process includes different stages and KEF make

thoughtful and deliberated decisions by organisation of the information and defining the

alternative solution to a give issue or task.

Issues/Problem Alternative 1 Alternative 2 Conclusion

There is decline in the

sales revenue of KEF

organisation and the

company is under a

The first solution is to

adopt the absorption

costing method

whether company can

Under the second

alternative of

marginal costing the

organization KEF is

This is suggested to

the KEF that the

decision of buying the

product is more

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.