Evaluating Management Accounting Role and Integration in Business

VerifiedAdded on 2024/06/05

|20

|4634

|233

Report

AI Summary

This report provides a comprehensive analysis of management accounting, examining its role in cost control, organizational planning, and inventory management. It discusses various management accounting systems like cost accounting, inventory management, job-costing, and price optimization. The report further explores how management accounting integrates within an organization, focusing on both financial and non-financial aspects, such as employee efficiency and cost management. It highlights the benefits of management accounting functions, including planning, forecasting, organizing, coordination, and cost control. Additionally, the report includes a financial statement analysis of two competitor organizations, Tate & Lyle and Kerry Group Plc, using key performance indicators and financial ratios over three years. Finally, it compares and contrasts three planning tools used in management accounting, evaluating their effectiveness with supporting evidence. Desklib offers students access to similar solved assignments and resources.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of contents

Introduction................................................................................................................................3

Task 1.........................................................................................................................................4

1. An explanation of the role of management accounting and management accounting

systems.......................................................................................................................................4

2. Explanation of how management accounting is integrated within an organisation...............5

3. The benefits of the function to the organisation.....................................................................6

Task 2.........................................................................................................................................8

A. Select two competitor organisations. Find the last three years of the organisations’

financial statements and analyse them with key performance indicators and appropriate

financial ratios............................................................................................................................8

B. Absorption costing and Marginal costing............................................................................11

(i) Absorption Costing..............................................................................................................12

(ii) Marginal Costing................................................................................................................13

Task 3.......................................................................................................................................14

Compare and contrast three planning tools used in management accounting, indicating how

effective you judge each to be and why. Your judgements should be supported by evidence 14

Conclusion................................................................................................................................17

Reference list............................................................................................................................18

2 | P a g e

Introduction................................................................................................................................3

Task 1.........................................................................................................................................4

1. An explanation of the role of management accounting and management accounting

systems.......................................................................................................................................4

2. Explanation of how management accounting is integrated within an organisation...............5

3. The benefits of the function to the organisation.....................................................................6

Task 2.........................................................................................................................................8

A. Select two competitor organisations. Find the last three years of the organisations’

financial statements and analyse them with key performance indicators and appropriate

financial ratios............................................................................................................................8

B. Absorption costing and Marginal costing............................................................................11

(i) Absorption Costing..............................................................................................................12

(ii) Marginal Costing................................................................................................................13

Task 3.......................................................................................................................................14

Compare and contrast three planning tools used in management accounting, indicating how

effective you judge each to be and why. Your judgements should be supported by evidence 14

Conclusion................................................................................................................................17

Reference list............................................................................................................................18

2 | P a g e

Introduction

The term “management accounting” indicates a particular system that takes care of not only

the financial activities, but the non-financial activities also. Management accounting is

considered to be one of the biggest organizational systems that influence growth of the

business (Ahmad, 2017). Here, in this study, the effectiveness of management accounting

will be analyzed in organizational context. At the same time, the study will also evaluate the

use of different systems under the management accounting like, cost accounting system and

inventory management system. Moreover, different planning tools under the management

accounting system will also be evaluated.

3 | P a g e

The term “management accounting” indicates a particular system that takes care of not only

the financial activities, but the non-financial activities also. Management accounting is

considered to be one of the biggest organizational systems that influence growth of the

business (Ahmad, 2017). Here, in this study, the effectiveness of management accounting

will be analyzed in organizational context. At the same time, the study will also evaluate the

use of different systems under the management accounting like, cost accounting system and

inventory management system. Moreover, different planning tools under the management

accounting system will also be evaluated.

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

1. An explanation of the role of management accounting and management accounting

systems

If management accounting in the organizational context is analyzed, the following key roles

will be identified:

Management accounting is a major player in the cost controlling system of the

business. Providing different cost accounting methods, management accounting helps

the organization controlling its cost to a standard level. There are several cost

accounting systems can be identified under management accounting like, marginal

costing system, absorption costing system and job-costing system (Ismail et al.,

2018).

The role of management accounting is also very significant in development of

organizational plans. As the system has enough access to different organizational

activities, it is able to understand the overall situation of the business (Ax and Greve,

2017). Due to this, under the management accounting system, developing the business

strategies or plans becomes easier.

Management accounting also plays vital role in inventory management. Under this

system, managers get access to different techniques of inventory management. Using

those techniques, managers can easily control the flow of inventory in the business,

which is essential for maintaining standard level of sales (Booth, 2018).

There are several systems under the management accounting and these systems are discussed

below:

Cost accounting system – It has been stated above that controlling the cost level of the

business is one of the major roles that management accounting plays in the business. Cost

accounting system helps management accounting in this context (Lanen, 2016). Analyzing

each business related cost, this system of management accounting helps in making const

controlling decisions and strategies.

Inventory management system – This is another vital management accounting system. The

primary aim of inventory management system is to help the organization maintaining

4 | P a g e

1. An explanation of the role of management accounting and management accounting

systems

If management accounting in the organizational context is analyzed, the following key roles

will be identified:

Management accounting is a major player in the cost controlling system of the

business. Providing different cost accounting methods, management accounting helps

the organization controlling its cost to a standard level. There are several cost

accounting systems can be identified under management accounting like, marginal

costing system, absorption costing system and job-costing system (Ismail et al.,

2018).

The role of management accounting is also very significant in development of

organizational plans. As the system has enough access to different organizational

activities, it is able to understand the overall situation of the business (Ax and Greve,

2017). Due to this, under the management accounting system, developing the business

strategies or plans becomes easier.

Management accounting also plays vital role in inventory management. Under this

system, managers get access to different techniques of inventory management. Using

those techniques, managers can easily control the flow of inventory in the business,

which is essential for maintaining standard level of sales (Booth, 2018).

There are several systems under the management accounting and these systems are discussed

below:

Cost accounting system – It has been stated above that controlling the cost level of the

business is one of the major roles that management accounting plays in the business. Cost

accounting system helps management accounting in this context (Lanen, 2016). Analyzing

each business related cost, this system of management accounting helps in making const

controlling decisions and strategies.

Inventory management system – This is another vital management accounting system. The

primary aim of inventory management system is to help the organization maintaining

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

standard level of inventory and sales in every financial year. The inventory management

system is very important for maintaining standard liquidity level in the business (Ax and

Greve, 2017). The techniques that management accounting suggests for better inventory

management are – FIFO, AVCO and LIFO.

Job-costing system – If the organization is a large production or manufacturing company,

job-costing is the most useful system for the company. Job-costing helps the organization

dividing its production and operational activities into small parts, which are known as jobs

and then analyzing and controlling the same (Booth, 2018). It makes large business process

easier for the managers.

Price optimization system – A business can sell its products efficiently only if the price level

of the products and services is standard. Price optimization system is such a system that can

help the company in this context (Ismail et al., 2018). Under this system, determining the

right price level becomes easier because this system determines the price after analyzing

internal and external business scenario.

2. Explanation of how management accounting is integrated within an organisation

As stated above, management accounting plays a major role in the growth of a company. This

is clearly indicating is management accounting is largely associated with organizational

activities. However, in order to understand how management accounting is integrated within

an organization, it is important to critically analyze the management accounting system of an

organization.

Management accounting takes care of non-financial as well as financial activities of the

business. Efficiency level of the employees is one of the key non-financial aspects of the

business. Management accounting takes care of this particular aspect of the business. Under

the management accounting system, the managers need to prepare the performance appraisal

reports, in which the performance standards of the employees are mentioned. This report

indicates the performance gaps, considering which the managers can develop strategies for

improving the efficiency level of the employees.

On the other hand, if the financial aspects are considered like, cost of the business,

management accounting provides the techniques that can help the firm identifying the right

costing technique for the business. This on the other hand helps to control the cost level of the

5 | P a g e

system is very important for maintaining standard liquidity level in the business (Ax and

Greve, 2017). The techniques that management accounting suggests for better inventory

management are – FIFO, AVCO and LIFO.

Job-costing system – If the organization is a large production or manufacturing company,

job-costing is the most useful system for the company. Job-costing helps the organization

dividing its production and operational activities into small parts, which are known as jobs

and then analyzing and controlling the same (Booth, 2018). It makes large business process

easier for the managers.

Price optimization system – A business can sell its products efficiently only if the price level

of the products and services is standard. Price optimization system is such a system that can

help the company in this context (Ismail et al., 2018). Under this system, determining the

right price level becomes easier because this system determines the price after analyzing

internal and external business scenario.

2. Explanation of how management accounting is integrated within an organisation

As stated above, management accounting plays a major role in the growth of a company. This

is clearly indicating is management accounting is largely associated with organizational

activities. However, in order to understand how management accounting is integrated within

an organization, it is important to critically analyze the management accounting system of an

organization.

Management accounting takes care of non-financial as well as financial activities of the

business. Efficiency level of the employees is one of the key non-financial aspects of the

business. Management accounting takes care of this particular aspect of the business. Under

the management accounting system, the managers need to prepare the performance appraisal

reports, in which the performance standards of the employees are mentioned. This report

indicates the performance gaps, considering which the managers can develop strategies for

improving the efficiency level of the employees.

On the other hand, if the financial aspects are considered like, cost of the business,

management accounting provides the techniques that can help the firm identifying the right

costing technique for the business. This on the other hand helps to control the cost level of the

5 | P a g e

business more efficiently. Similarly, management accounting also provides different methods

for managing inventory level of the firm. The FIFO, LIFO and AVCO methods are under the

management accounting system and these techniques efficiently manage the inventory level

of the business.

It has been mentioned before that under the system of management accounting different

reports are required to be prepared. Each of these reports indicates different areas of business.

For example, sales report, production report, capital budgeting report and many others show

the performance standard of the business in different departments.

Therefore, from the overall discussion and evaluation, it must be stated that management

accounting is closely integrated with the organizational system of a firm.

3. The benefits of the function to the organisation

There are several benefits of using management accounting techniques or incorporating

management accounting system in the business. The benefits of the functions of management

accounting to the organization are stated below:

One of the key functions of management accounting is developing better plans for the

business. With the help of this particular management accounting function, the

managers in the firm become able to develop advanced strategies for the operations

because while developing plans management accounting encourages the managers for

analyzing the business situations critically, which makes the strategy development

process easier.

Forecasting is another key function that management accounting performs. With the

help of forecasting, the managers can arrange the required amount of resources for the

future days, so that the business does not face any trouble during the operations.

Organizing is also a function of management accounting. The primary benefit of

organizing is that it helps the managers operating business activities in a systematic

manner. In the other words, it can be stated that organizing the activities the business

process becomes easier to the managers.

Management accounting is helpful in co-ordinates the activities of different

organizational departments. Preparing different organizational reports, management

accounting creates strong communication among the departments. The main benefit o

6 | P a g e

for managing inventory level of the firm. The FIFO, LIFO and AVCO methods are under the

management accounting system and these techniques efficiently manage the inventory level

of the business.

It has been mentioned before that under the system of management accounting different

reports are required to be prepared. Each of these reports indicates different areas of business.

For example, sales report, production report, capital budgeting report and many others show

the performance standard of the business in different departments.

Therefore, from the overall discussion and evaluation, it must be stated that management

accounting is closely integrated with the organizational system of a firm.

3. The benefits of the function to the organisation

There are several benefits of using management accounting techniques or incorporating

management accounting system in the business. The benefits of the functions of management

accounting to the organization are stated below:

One of the key functions of management accounting is developing better plans for the

business. With the help of this particular management accounting function, the

managers in the firm become able to develop advanced strategies for the operations

because while developing plans management accounting encourages the managers for

analyzing the business situations critically, which makes the strategy development

process easier.

Forecasting is another key function that management accounting performs. With the

help of forecasting, the managers can arrange the required amount of resources for the

future days, so that the business does not face any trouble during the operations.

Organizing is also a function of management accounting. The primary benefit of

organizing is that it helps the managers operating business activities in a systematic

manner. In the other words, it can be stated that organizing the activities the business

process becomes easier to the managers.

Management accounting is helpful in co-ordinates the activities of different

organizational departments. Preparing different organizational reports, management

accounting creates strong communication among the departments. The main benefit o

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

better co-ordination is that the managers can easily make decisions regarding business

activities.

Cost controlling is another major function that management accounting does. The

benefit of cost controlling is that the firm gets the scope of enhancing profit or income

level of the business. This makes the financial health of the business stronger.

Management accounting protects the assets of a firm, which is important for

maintaining a strong financial position in the market.

Therefore, considering the above points, it can be stated that each function of management

accounting is important to the firm. The functions of management accounting make the

business process easier and help to create a strong position of the company in the market.

7 | P a g e

activities.

Cost controlling is another major function that management accounting does. The

benefit of cost controlling is that the firm gets the scope of enhancing profit or income

level of the business. This makes the financial health of the business stronger.

Management accounting protects the assets of a firm, which is important for

maintaining a strong financial position in the market.

Therefore, considering the above points, it can be stated that each function of management

accounting is important to the firm. The functions of management accounting make the

business process easier and help to create a strong position of the company in the market.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 2

A. Select two competitor organisations. Find the last three years of the organisations’

financial statements and analyse them with key performance indicators and

appropriate financial ratios

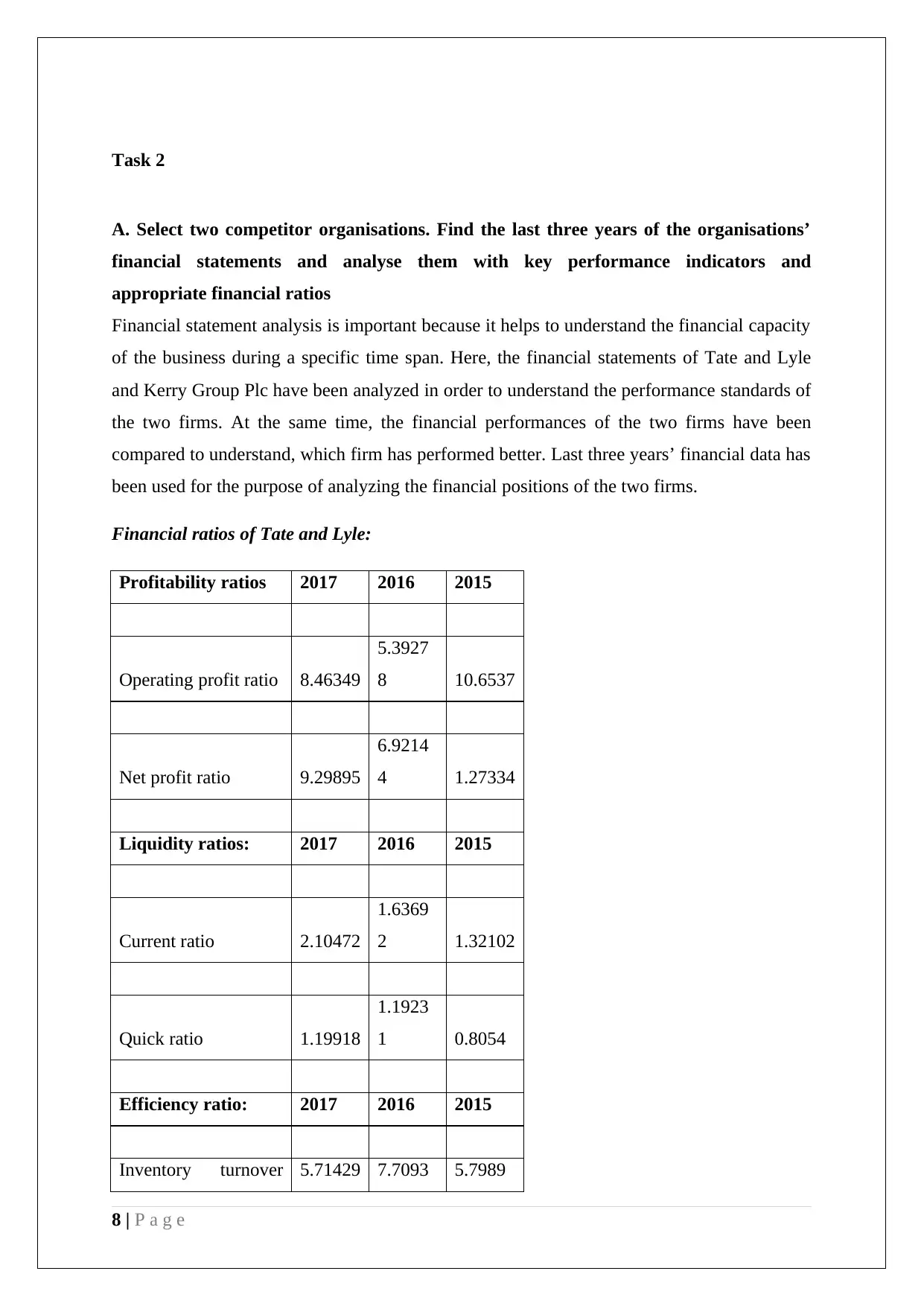

Financial statement analysis is important because it helps to understand the financial capacity

of the business during a specific time span. Here, the financial statements of Tate and Lyle

and Kerry Group Plc have been analyzed in order to understand the performance standards of

the two firms. At the same time, the financial performances of the two firms have been

compared to understand, which firm has performed better. Last three years’ financial data has

been used for the purpose of analyzing the financial positions of the two firms.

Financial ratios of Tate and Lyle:

Profitability ratios 2017 2016 2015

Operating profit ratio 8.46349

5.3927

8 10.6537

Net profit ratio 9.29895

6.9214

4 1.27334

Liquidity ratios: 2017 2016 2015

Current ratio 2.10472

1.6369

2 1.32102

Quick ratio 1.19918

1.1923

1 0.8054

Efficiency ratio: 2017 2016 2015

Inventory turnover 5.71429 7.7093 5.7989

8 | P a g e

A. Select two competitor organisations. Find the last three years of the organisations’

financial statements and analyse them with key performance indicators and

appropriate financial ratios

Financial statement analysis is important because it helps to understand the financial capacity

of the business during a specific time span. Here, the financial statements of Tate and Lyle

and Kerry Group Plc have been analyzed in order to understand the performance standards of

the two firms. At the same time, the financial performances of the two firms have been

compared to understand, which firm has performed better. Last three years’ financial data has

been used for the purpose of analyzing the financial positions of the two firms.

Financial ratios of Tate and Lyle:

Profitability ratios 2017 2016 2015

Operating profit ratio 8.46349

5.3927

8 10.6537

Net profit ratio 9.29895

6.9214

4 1.27334

Liquidity ratios: 2017 2016 2015

Current ratio 2.10472

1.6369

2 1.32102

Quick ratio 1.19918

1.1923

1 0.8054

Efficiency ratio: 2017 2016 2015

Inventory turnover 5.71429 7.7093 5.7989

8 | P a g e

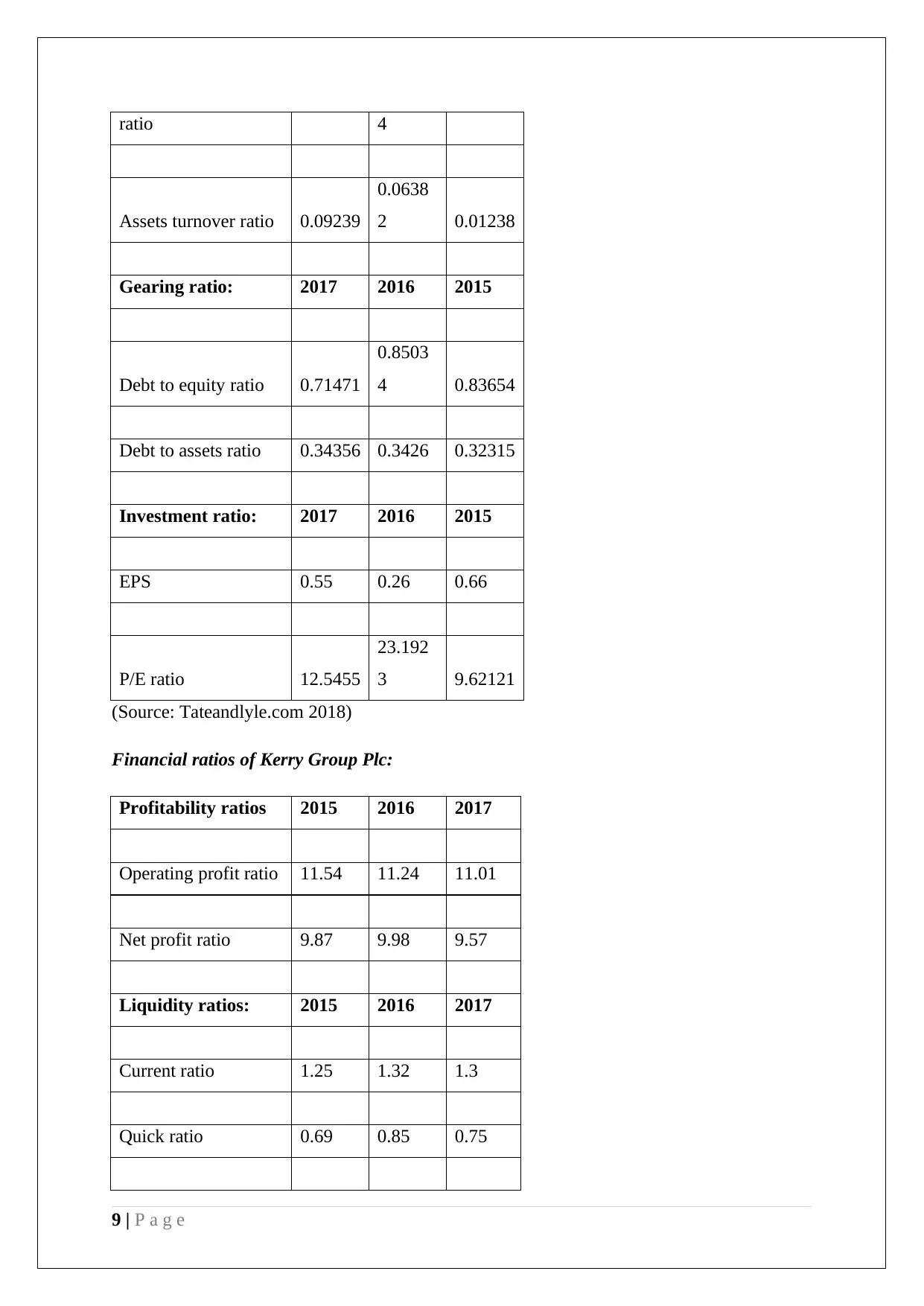

ratio 4

Assets turnover ratio 0.09239

0.0638

2 0.01238

Gearing ratio: 2017 2016 2015

Debt to equity ratio 0.71471

0.8503

4 0.83654

Debt to assets ratio 0.34356 0.3426 0.32315

Investment ratio: 2017 2016 2015

EPS 0.55 0.26 0.66

P/E ratio 12.5455

23.192

3 9.62121

(Source: Tateandlyle.com 2018)

Financial ratios of Kerry Group Plc:

Profitability ratios 2015 2016 2017

Operating profit ratio 11.54 11.24 11.01

Net profit ratio 9.87 9.98 9.57

Liquidity ratios: 2015 2016 2017

Current ratio 1.25 1.32 1.3

Quick ratio 0.69 0.85 0.75

9 | P a g e

Assets turnover ratio 0.09239

0.0638

2 0.01238

Gearing ratio: 2017 2016 2015

Debt to equity ratio 0.71471

0.8503

4 0.83654

Debt to assets ratio 0.34356 0.3426 0.32315

Investment ratio: 2017 2016 2015

EPS 0.55 0.26 0.66

P/E ratio 12.5455

23.192

3 9.62121

(Source: Tateandlyle.com 2018)

Financial ratios of Kerry Group Plc:

Profitability ratios 2015 2016 2017

Operating profit ratio 11.54 11.24 11.01

Net profit ratio 9.87 9.98 9.57

Liquidity ratios: 2015 2016 2017

Current ratio 1.25 1.32 1.3

Quick ratio 0.69 0.85 0.75

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Efficiency ratio: 2015 2016 2017

Inventory turnover

ratio 7.53 4.48 6.9

Assets turnover ratio 0.94 0.85 0.86

Gearing ratio: 2015 2016 2017

Debt to equity ratio 0.72 0.6 0.48

Debt to assets ratio 2.51 2.4 2.07

Investment ratio: 2015 2016 2017

EPS 2.99 3.03 3.34

P/E ratio

20.538

5 24.6535 20.003

(Source: Kerrygroup.com 2018)

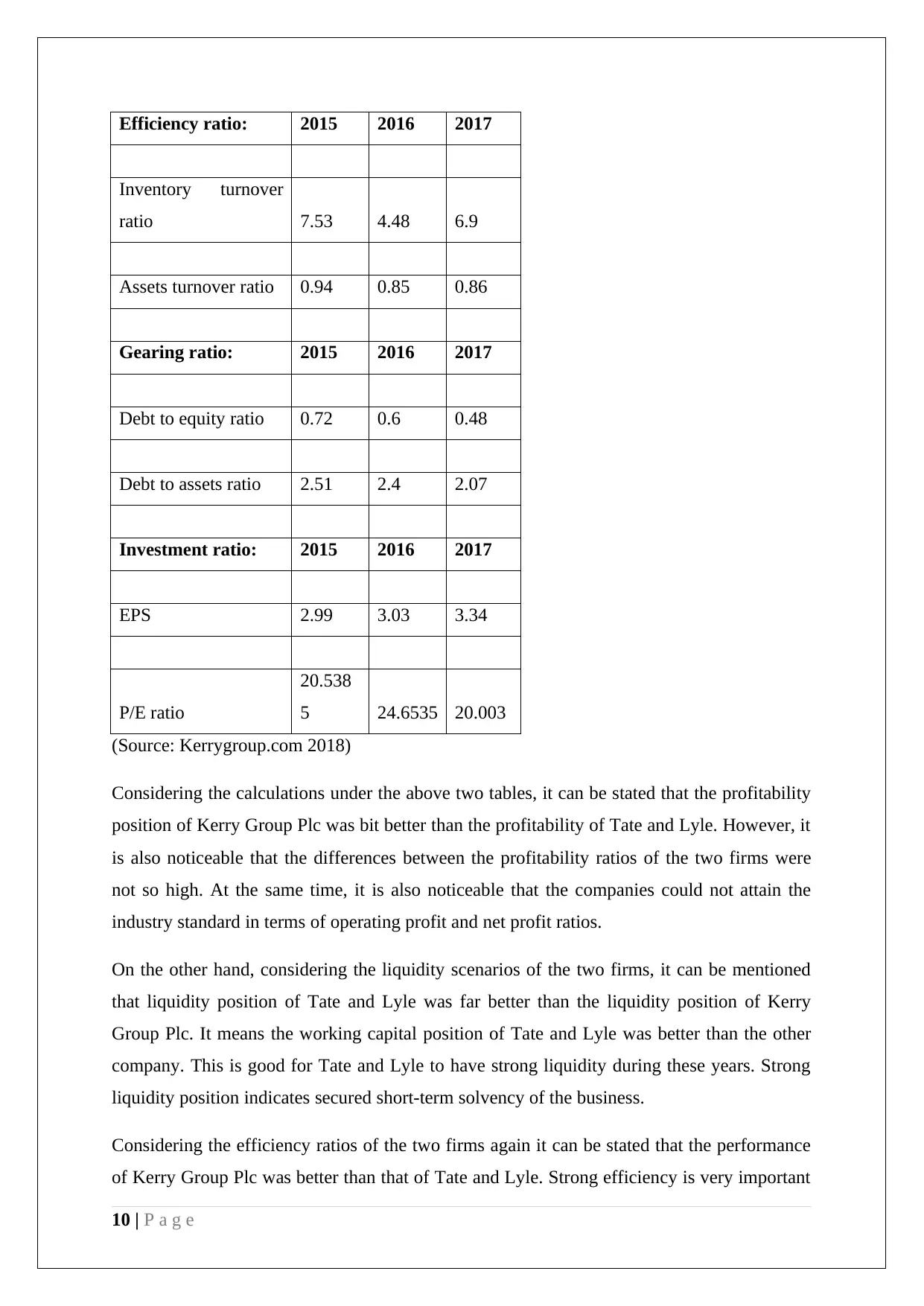

Considering the calculations under the above two tables, it can be stated that the profitability

position of Kerry Group Plc was bit better than the profitability of Tate and Lyle. However, it

is also noticeable that the differences between the profitability ratios of the two firms were

not so high. At the same time, it is also noticeable that the companies could not attain the

industry standard in terms of operating profit and net profit ratios.

On the other hand, considering the liquidity scenarios of the two firms, it can be mentioned

that liquidity position of Tate and Lyle was far better than the liquidity position of Kerry

Group Plc. It means the working capital position of Tate and Lyle was better than the other

company. This is good for Tate and Lyle to have strong liquidity during these years. Strong

liquidity position indicates secured short-term solvency of the business.

Considering the efficiency ratios of the two firms again it can be stated that the performance

of Kerry Group Plc was better than that of Tate and Lyle. Strong efficiency is very important

10 | P a g e

Inventory turnover

ratio 7.53 4.48 6.9

Assets turnover ratio 0.94 0.85 0.86

Gearing ratio: 2015 2016 2017

Debt to equity ratio 0.72 0.6 0.48

Debt to assets ratio 2.51 2.4 2.07

Investment ratio: 2015 2016 2017

EPS 2.99 3.03 3.34

P/E ratio

20.538

5 24.6535 20.003

(Source: Kerrygroup.com 2018)

Considering the calculations under the above two tables, it can be stated that the profitability

position of Kerry Group Plc was bit better than the profitability of Tate and Lyle. However, it

is also noticeable that the differences between the profitability ratios of the two firms were

not so high. At the same time, it is also noticeable that the companies could not attain the

industry standard in terms of operating profit and net profit ratios.

On the other hand, considering the liquidity scenarios of the two firms, it can be mentioned

that liquidity position of Tate and Lyle was far better than the liquidity position of Kerry

Group Plc. It means the working capital position of Tate and Lyle was better than the other

company. This is good for Tate and Lyle to have strong liquidity during these years. Strong

liquidity position indicates secured short-term solvency of the business.

Considering the efficiency ratios of the two firms again it can be stated that the performance

of Kerry Group Plc was better than that of Tate and Lyle. Strong efficiency is very important

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

utilizing the assets and other resources of the business effectively. However, in this context, it

must be stated that efficiency ratios of the two firms were not much high, which indicates that

improvements are required.

Considering the gearing ratios of the two businesses, it can be stated that both the companies

have used more debt capital than equity capital. However, the use of debt capital has

decreased in both the companies from 2015 to 2017. It means the financial risk associated

with capital structure has reduced during these years. However, if the concentration is made

on the debt to assets ratios, it can be identified that the Kerry Group Plc has used more debt

capital in its assets, which has increased the risk level of the assets.

If the investment ratios are considered, it will be noticed that Kerry Group Plc has performed

better than Tate and Lyle. Better investment ratios indicate that the company has satisfied its

stakeholders in a better way than Tate and Lyle. This is good for future growth of the

business. However, the investment ratios of Tate and Lyle were not so low.

Therefore, from the overall analysis, it can be stated that the performance of Kerry Group Plc

was better than the performance of Tate and Lyle. However, in order to understand the

performance standards of the two companies in a better way, it is important to analyze their

key performance indicators.

One of the major key performance indicators is the net profit of the business. Considering the

net profits of the two companies, it can be stated that the net profit of Tate and Lyle was

lower than its competitor Kerry Group Plc, which indicates that the performance of Kerry

Group Plc was better than that of Tate and Lyle. Another key performance indicator is the

cost of sales of the companies. In this context, it must be stated that the cost of sales of the

two companies was higher, which means the cost controlling systems of the companies must

be improved.

Therefore, from the overall discussion, it can be stated that the performance standards of both

the companies are needed to be improved as soon as possible. The managements in both the

companies need to take special care of the profitability positions of the businesses in the

coming financial years.

11 | P a g e

must be stated that efficiency ratios of the two firms were not much high, which indicates that

improvements are required.

Considering the gearing ratios of the two businesses, it can be stated that both the companies

have used more debt capital than equity capital. However, the use of debt capital has

decreased in both the companies from 2015 to 2017. It means the financial risk associated

with capital structure has reduced during these years. However, if the concentration is made

on the debt to assets ratios, it can be identified that the Kerry Group Plc has used more debt

capital in its assets, which has increased the risk level of the assets.

If the investment ratios are considered, it will be noticed that Kerry Group Plc has performed

better than Tate and Lyle. Better investment ratios indicate that the company has satisfied its

stakeholders in a better way than Tate and Lyle. This is good for future growth of the

business. However, the investment ratios of Tate and Lyle were not so low.

Therefore, from the overall analysis, it can be stated that the performance of Kerry Group Plc

was better than the performance of Tate and Lyle. However, in order to understand the

performance standards of the two companies in a better way, it is important to analyze their

key performance indicators.

One of the major key performance indicators is the net profit of the business. Considering the

net profits of the two companies, it can be stated that the net profit of Tate and Lyle was

lower than its competitor Kerry Group Plc, which indicates that the performance of Kerry

Group Plc was better than that of Tate and Lyle. Another key performance indicator is the

cost of sales of the companies. In this context, it must be stated that the cost of sales of the

two companies was higher, which means the cost controlling systems of the companies must

be improved.

Therefore, from the overall discussion, it can be stated that the performance standards of both

the companies are needed to be improved as soon as possible. The managements in both the

companies need to take special care of the profitability positions of the businesses in the

coming financial years.

11 | P a g e

B. Absorption costing and Marginal costing

Under the management accounting system, there are several costing techniques; however,

absorption costing and marginal costing are the two most popular costing techniques

available to the company. These two costing techniques and their uses are stated below:

Absorption costing – This is one of the traditional costing techniques under the system of

management accounting. In this technique, the management needs to identify the total costs

of by considering both fixed and variable costs (Fagundes et al., 2017).

Marginal costing – This is another costing technique, under which the total costs of the

company is calculated by considering only the variable costs of the business. This is also one

of the traditional costing techniques under management accounting (Arora and Soral, 2017).

The application of these two costing techniques is shown below

In the given scenario, it can be identified that the company Areal Ltd. produces a product that

includes the following costs:

Direct materials - £200,000

Direct labour - £300,000

Fixed overheads - £300,000

Total production costs - £800,000

Sales in May - 100,000

Sales in June - 75,000

Sales per unit - £10

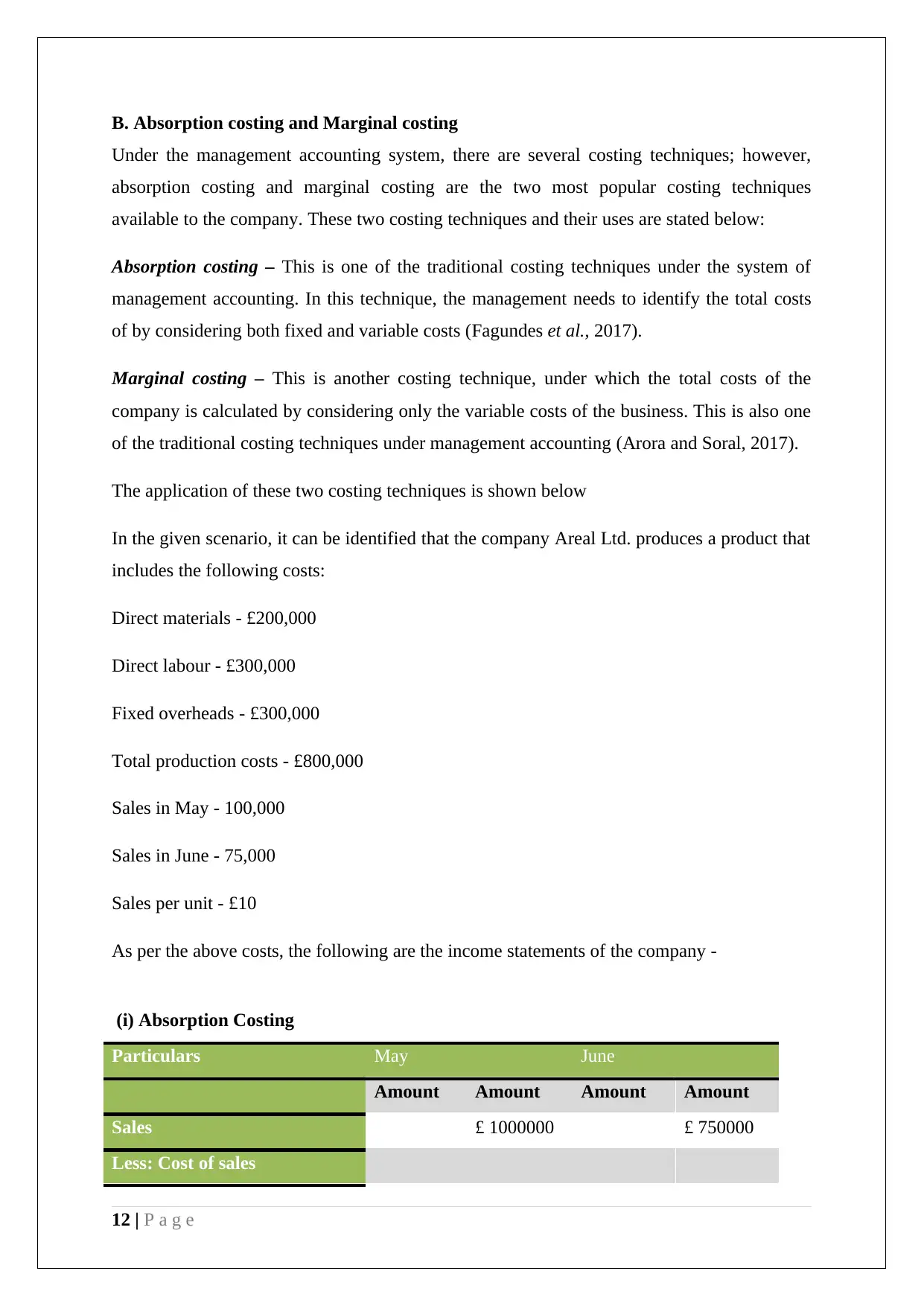

As per the above costs, the following are the income statements of the company -

(i) Absorption Costing

Particulars May June

Amount Amount Amount Amount

Sales £ 1000000 £ 750000

Less: Cost of sales

12 | P a g e

Under the management accounting system, there are several costing techniques; however,

absorption costing and marginal costing are the two most popular costing techniques

available to the company. These two costing techniques and their uses are stated below:

Absorption costing – This is one of the traditional costing techniques under the system of

management accounting. In this technique, the management needs to identify the total costs

of by considering both fixed and variable costs (Fagundes et al., 2017).

Marginal costing – This is another costing technique, under which the total costs of the

company is calculated by considering only the variable costs of the business. This is also one

of the traditional costing techniques under management accounting (Arora and Soral, 2017).

The application of these two costing techniques is shown below

In the given scenario, it can be identified that the company Areal Ltd. produces a product that

includes the following costs:

Direct materials - £200,000

Direct labour - £300,000

Fixed overheads - £300,000

Total production costs - £800,000

Sales in May - 100,000

Sales in June - 75,000

Sales per unit - £10

As per the above costs, the following are the income statements of the company -

(i) Absorption Costing

Particulars May June

Amount Amount Amount Amount

Sales £ 1000000 £ 750000

Less: Cost of sales

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.