Management Accounting for Cost Control at Lake Ltd. Analysis

VerifiedAdded on 2023/06/12

|18

|2151

|67

Report

AI Summary

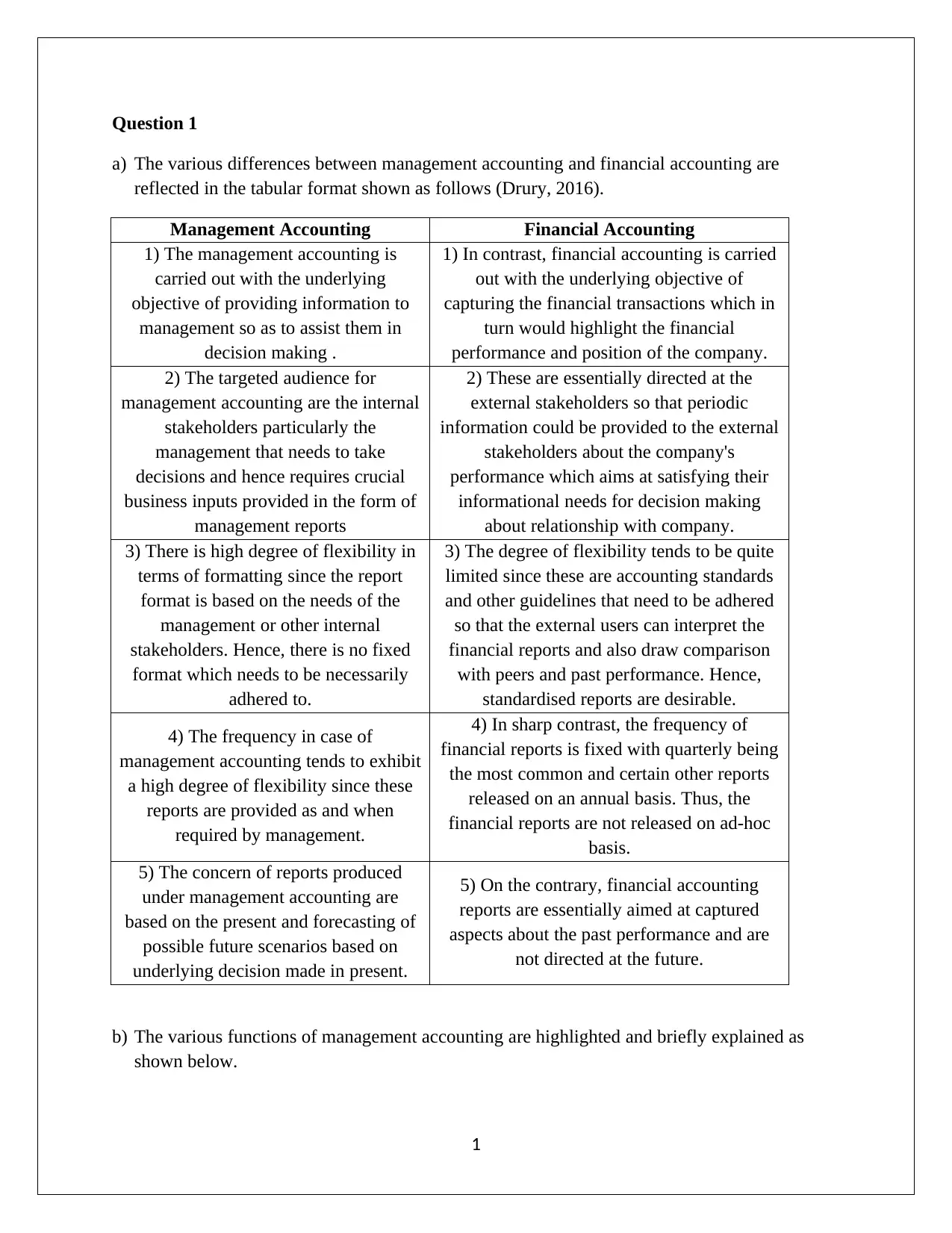

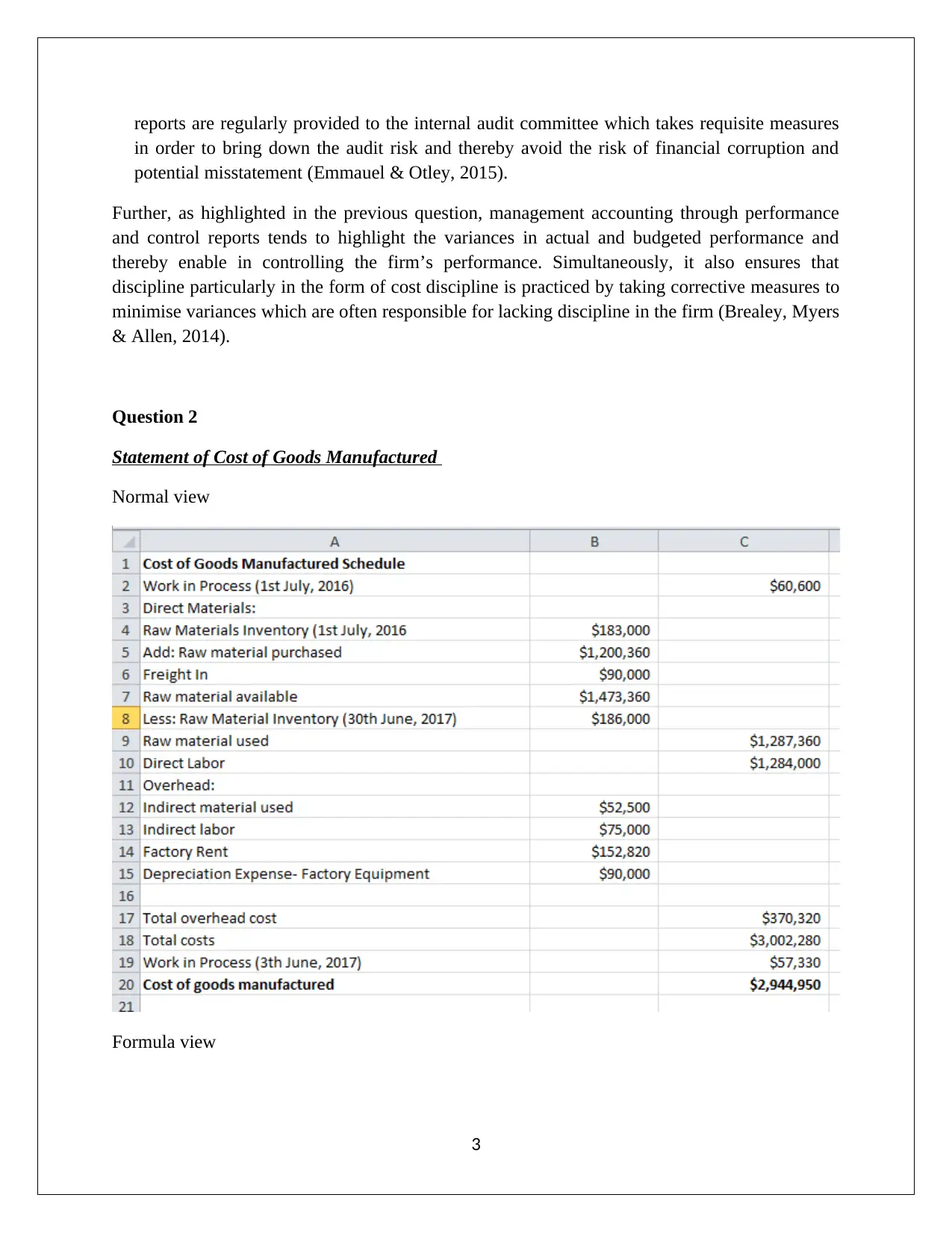

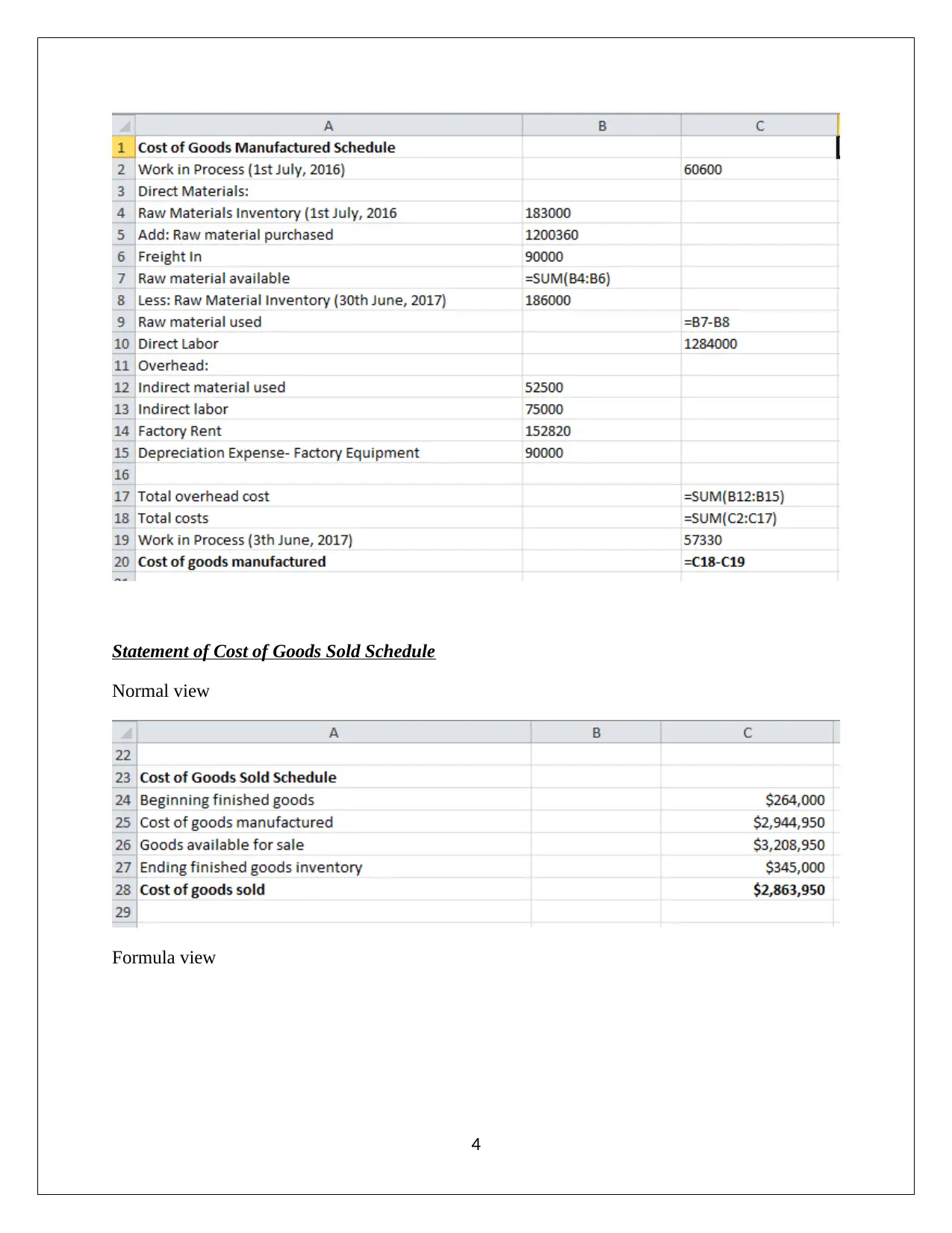

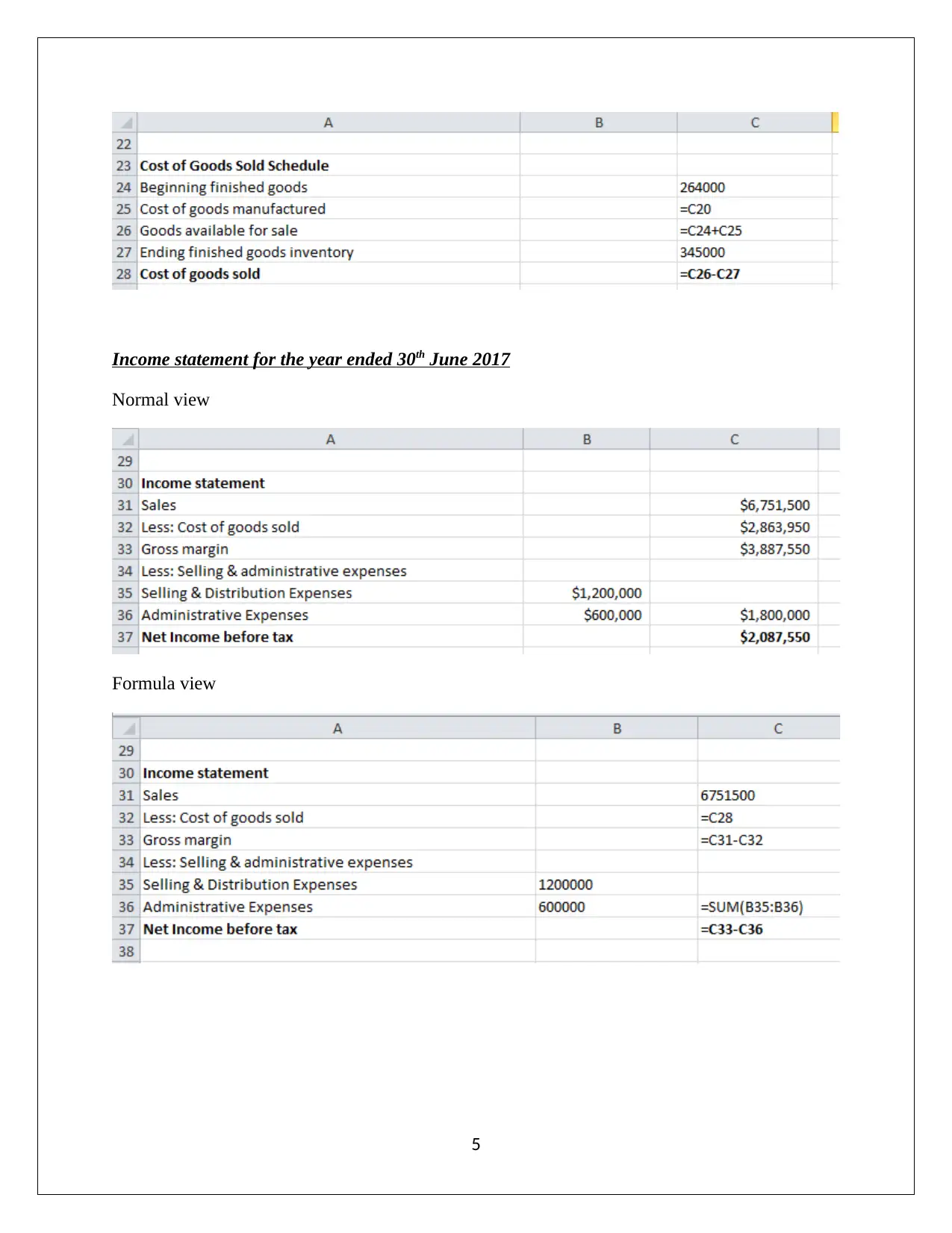

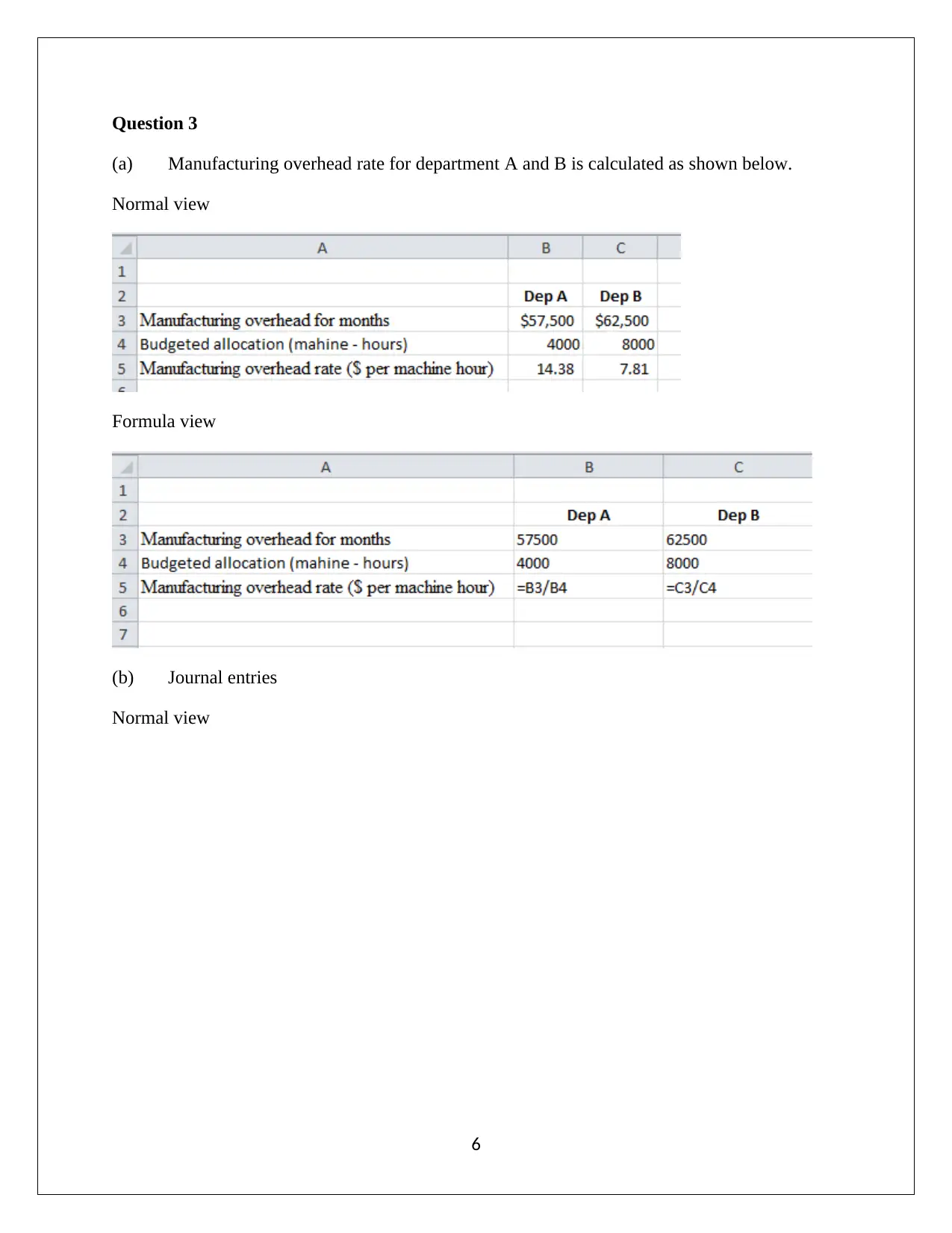

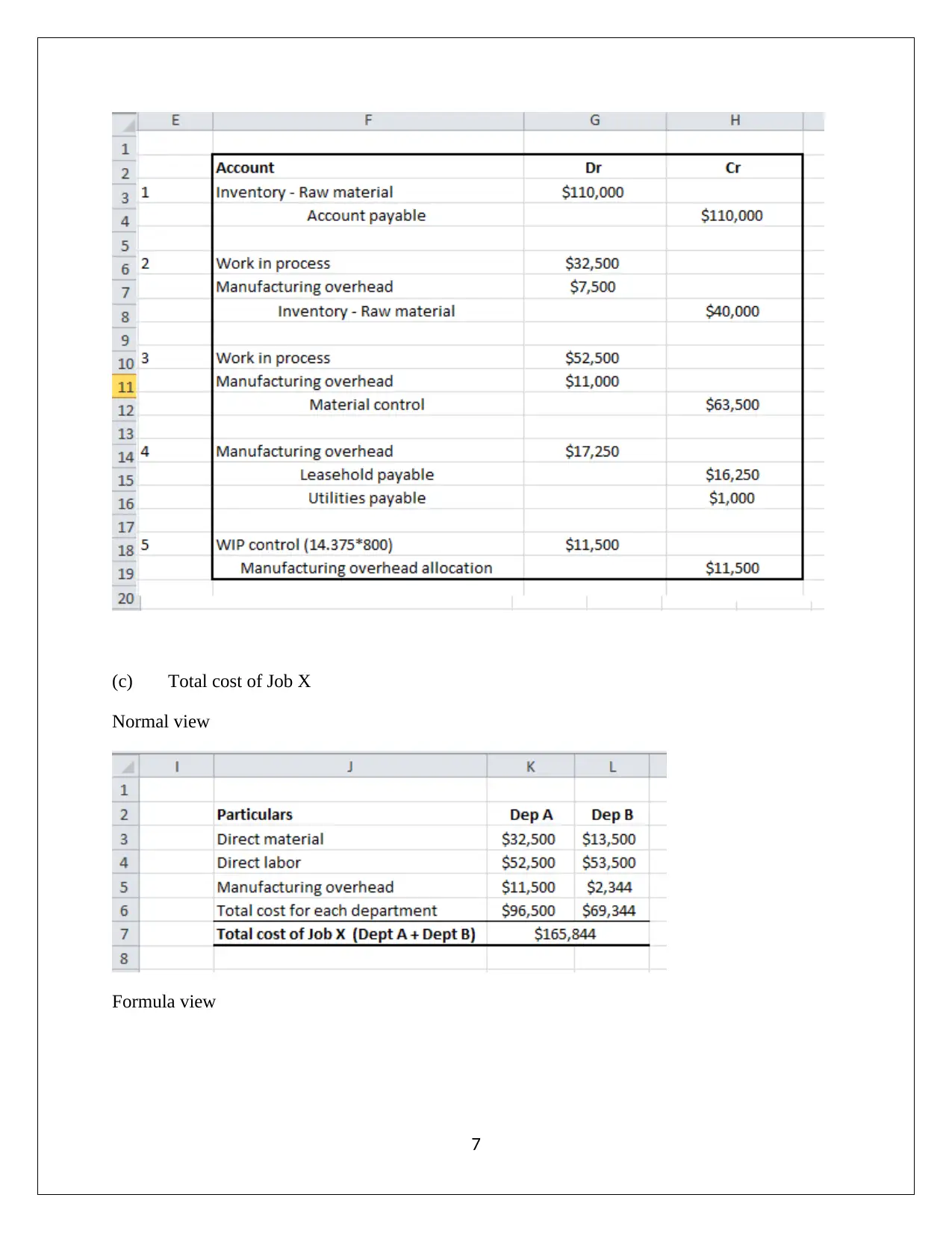

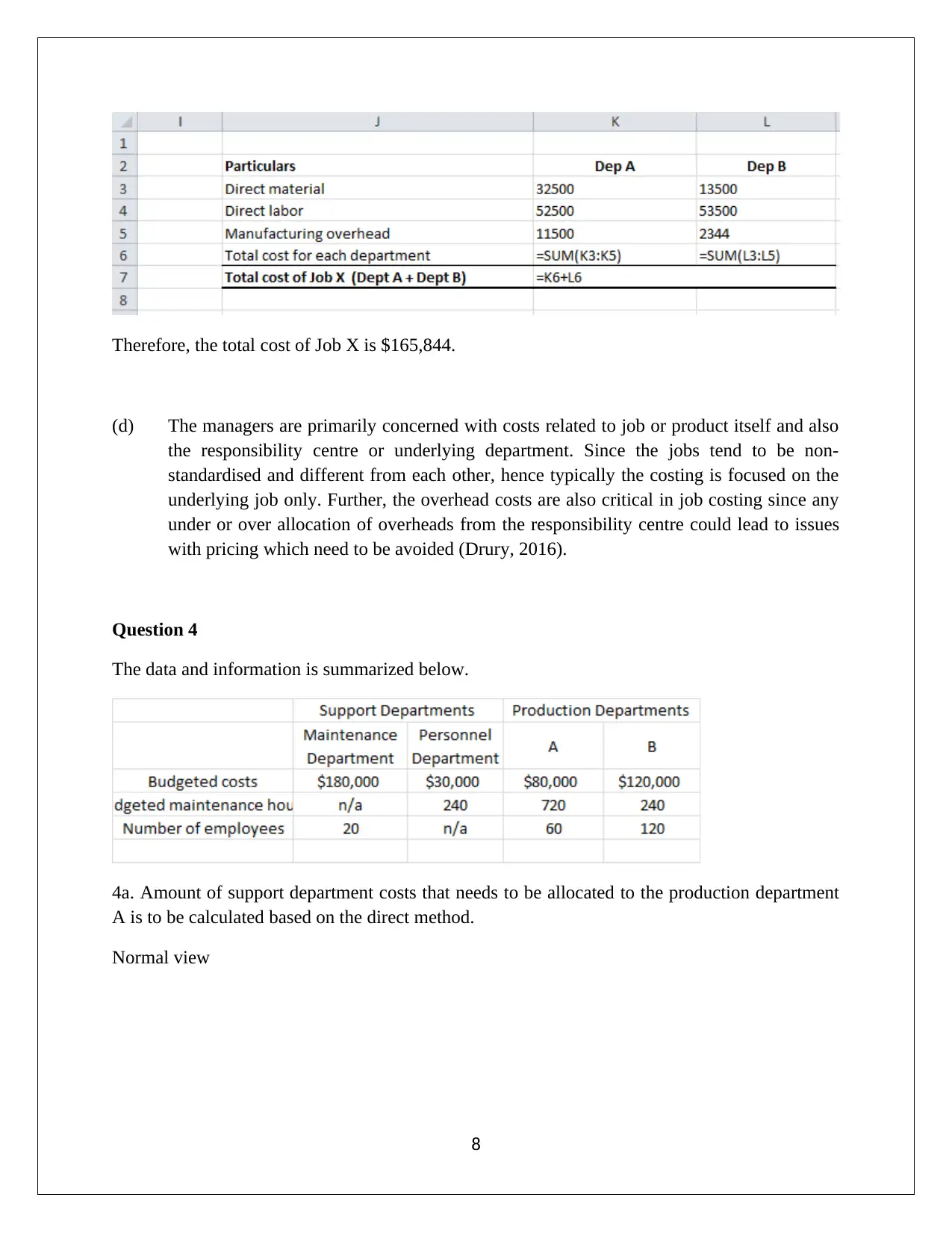

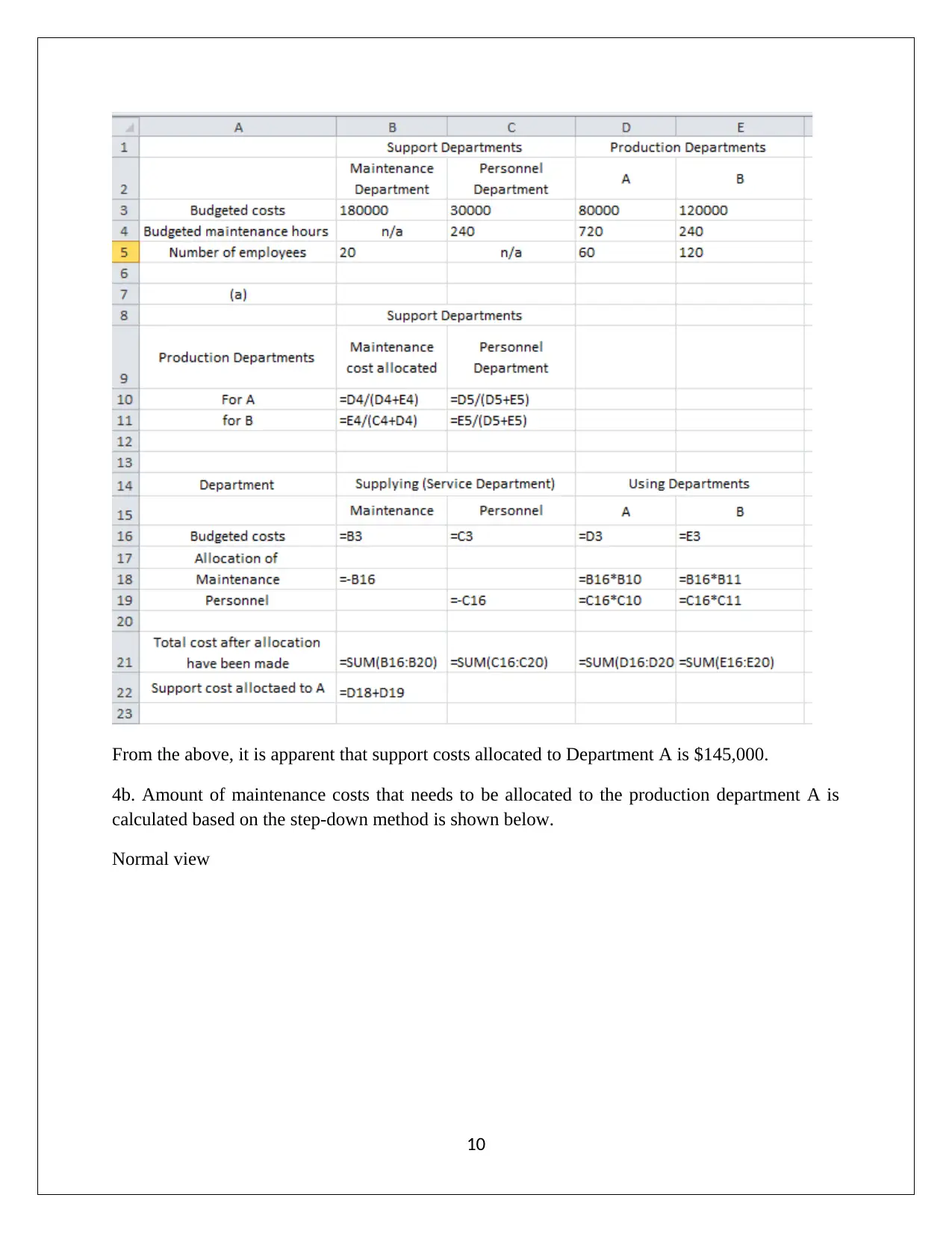

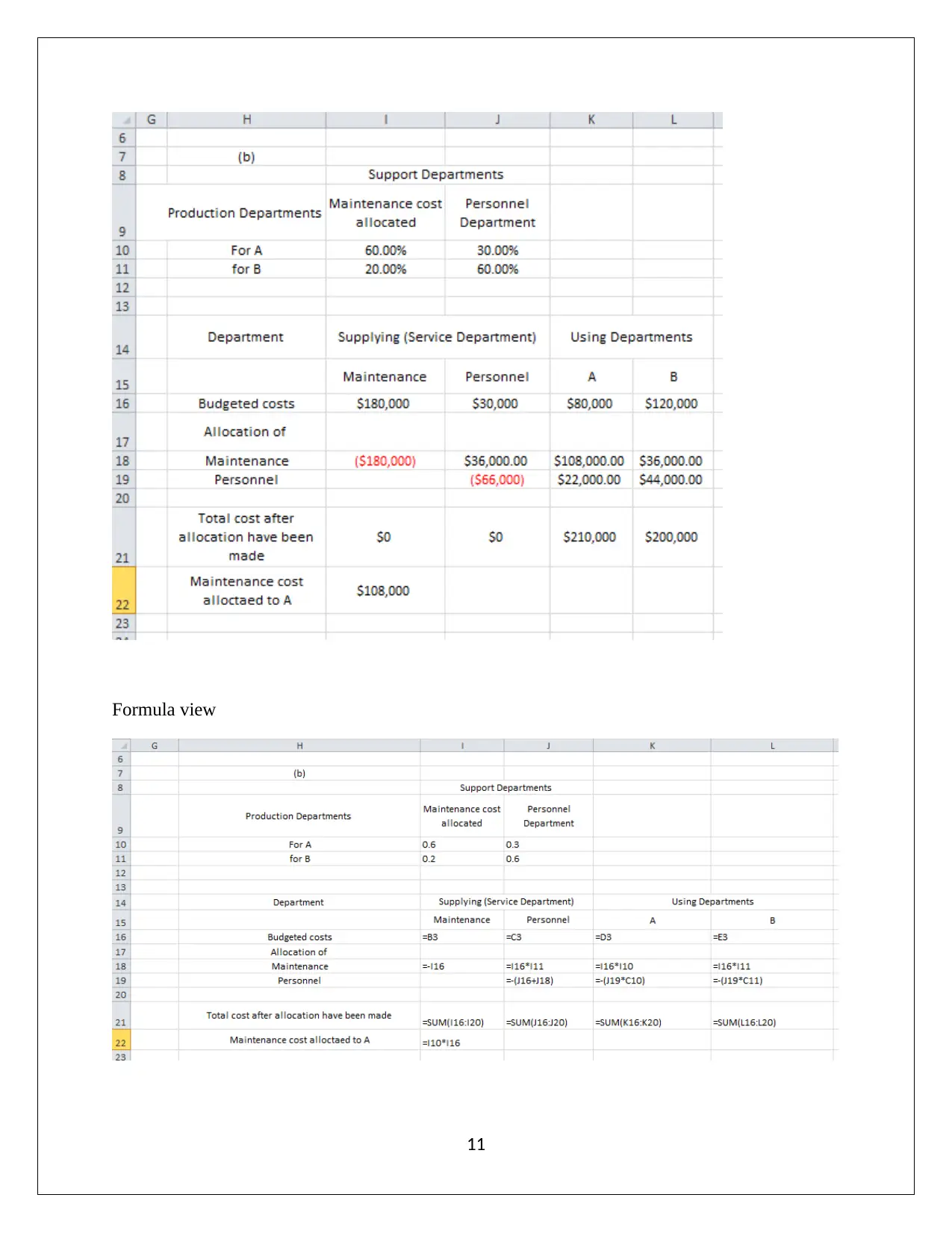

This report delves into the principles of management accounting, contrasting it with financial accounting and elucidating its core functions such as planning, organizing, controlling, and decision-making. It examines the relevance of concepts like panopticism in ensuring control and discipline within organizations. The report includes a detailed manufacturing statement, cost of goods sold schedule, and income statement for Lake Ltd., alongside calculations for manufacturing overhead rates and job costing. Furthermore, it analyzes overhead allocation methods, including direct, step-down, and reciprocal methods, to determine accurate departmental costs. The report also explores traditional costing systems versus activity-based costing (ABC), demonstrating how ABC provides a more accurate understanding of product profitability by assigning overhead costs based on activities. This comprehensive analysis provides insights into effective cost management and decision-making within a manufacturing context; this assignment is available for review and learning on Desklib, a platform providing study tools for students.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.